Embed Size (px)

Citation preview

Combined Chapters

Aggregate Supply/Aggregate DemandFiscal

Classical/KeynesianMultiplier

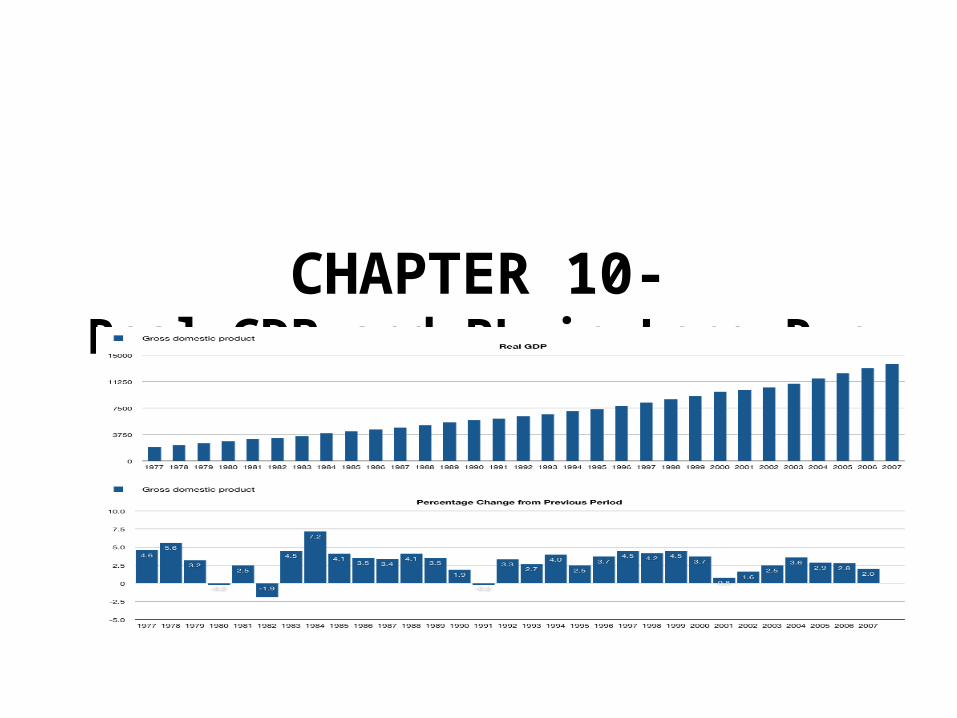

CHAPTER 10-Real GDP and PL in Long Run

GDP 2007 to 2010

OK… One more time…..

Component parts of GDP?C + I + G + (X-M) = GDP

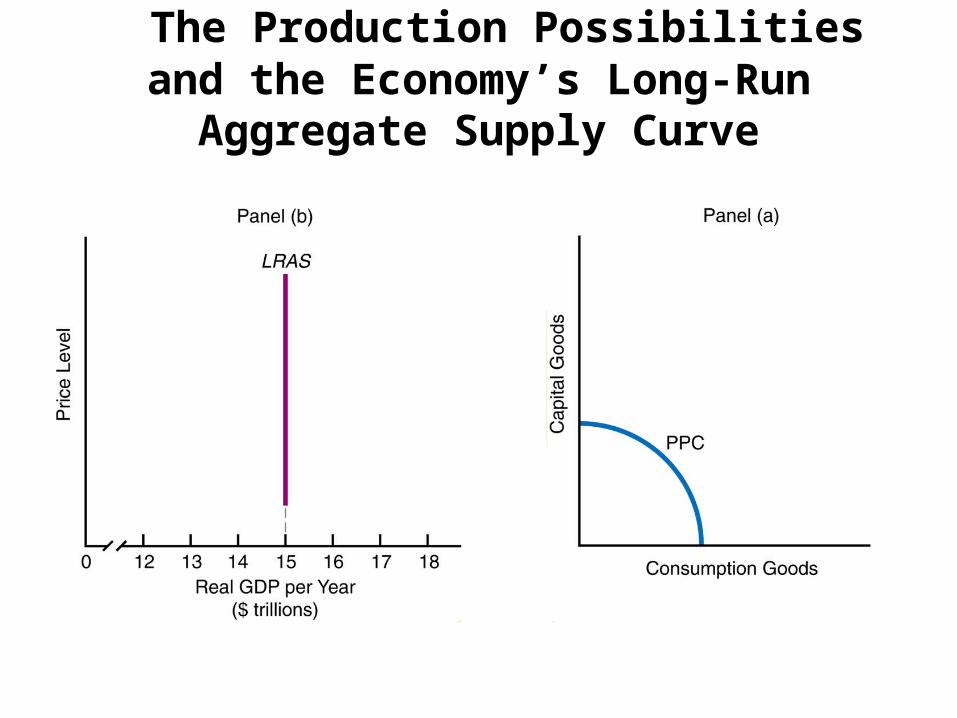

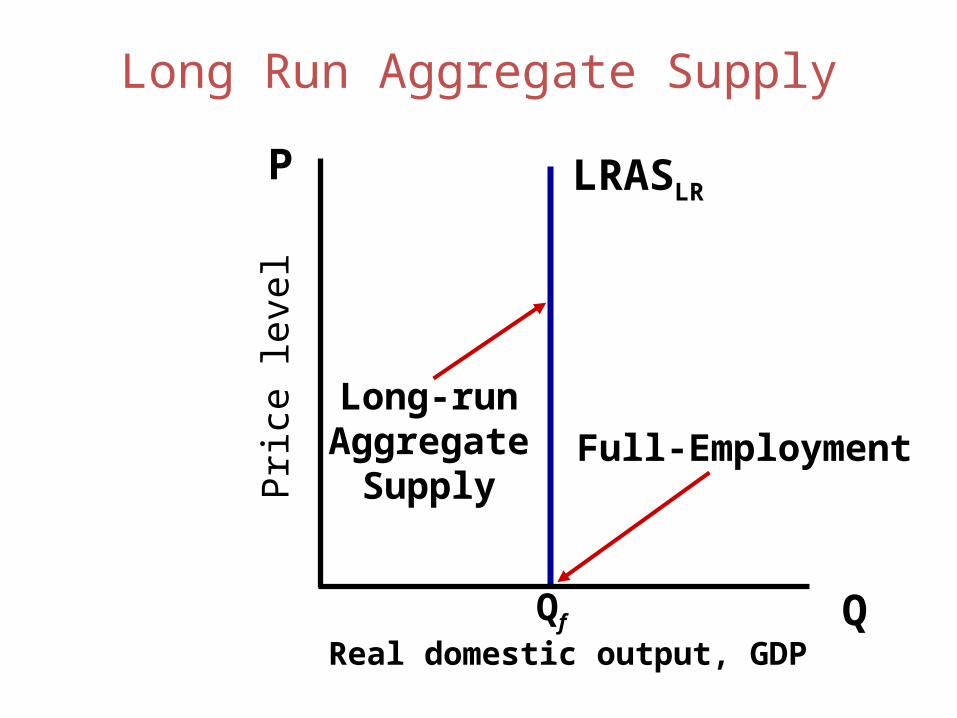

Long-Run Aggregate Supply Curve (LRAS)– A vertical line representing the real output of goods and services after

full adjustment has occurred

– It represents the real GDP of the economy under conditions of full employment; the economy is on its production possibilities curve

The Production Possibilities and the Economy’s Long-Run Aggregate Supply Curve

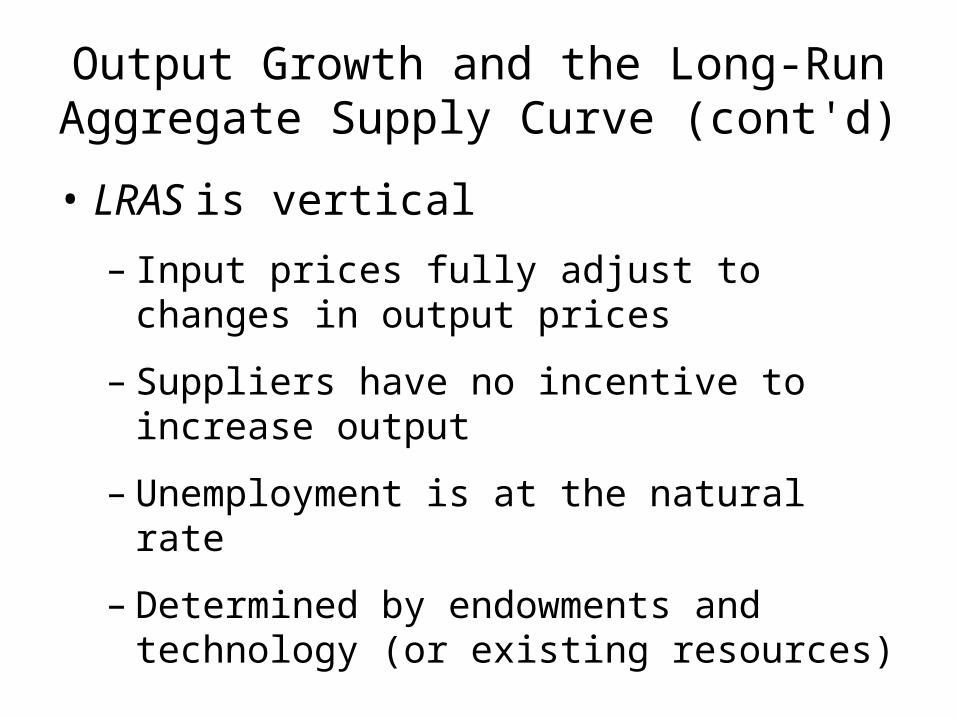

Output Growth and the Long-Run Aggregate Supply Curve (cont'd)

• LRAS is vertical

– Input prices fully adjust to changes in output prices

– Suppliers have no incentive to increase output

– Unemployment is at the natural rate

– Determined by endowments and technology (or existing resources)

Output Growth and the Long-Run Aggregate Supply Curve (cont'd)

• Growth is shown by outward shifts of either the production possibilities curve or the LRAS curve caused by

– Growth of population and the labor-force participation rate

– Capital accumulation

– Improvements in technology

Think: Why does AD slope downward?

Real domestic output, GDP

AD

Price

level

Vertical axis representsPrice level for ALL final goodsAnd services

The aggregate price levelIs measured by either GDPDeflator or CPI

The horizontal axis representsthe real quantity of all G&Spurchased as measured by thelevel of REAL GDP

Figure 10-4 The Aggregate Demand Curve

As the price level rises, real GDP declines

ASSUMPTION for Aggregate demand IS: If Price level is decreasing, so are incomes.

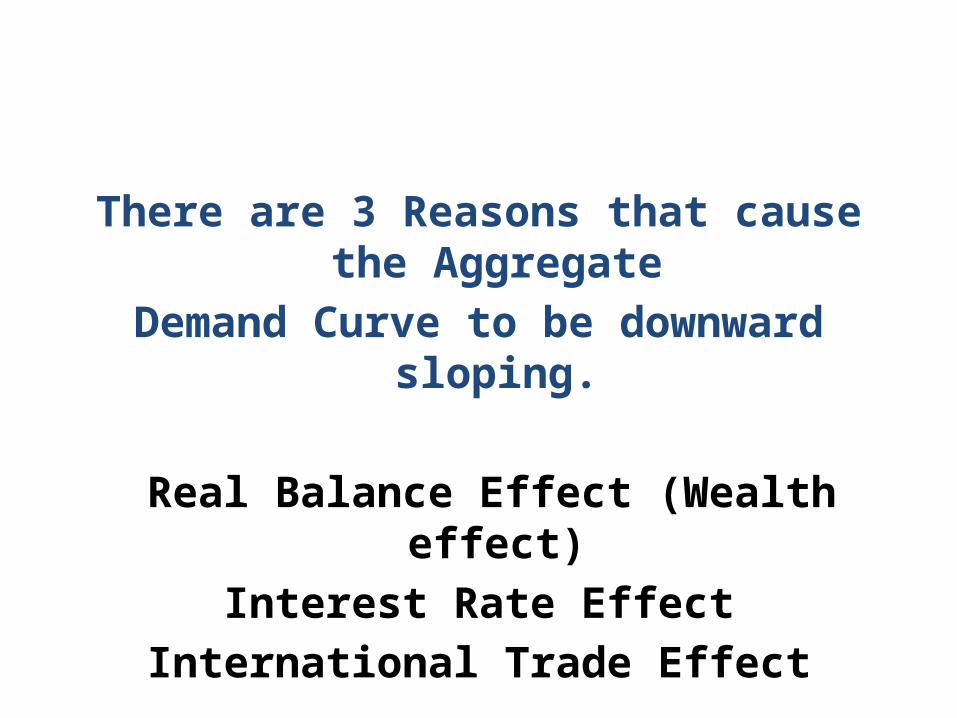

There are 3 Reasons that cause the Aggregate

Demand Curve to be downward sloping.

Real Balance Effect (Wealth effect)Interest Rate Effect

International Trade Effect

Real Balance Effect

Price level falls- causes purchasing power to rise… translates into more money to spend or monetary wealth improves.

1) Real Balance Effect (or wealth effect) – Higher price level means less consumption spending.

Real Balance Effect

The change in the purchasing power of dollar-

Relates to assets that result from a change in the price level

Interest Rate Effect

Inverse relationship between price level and quantity demanded of GDP – because households and businesses adjust to interest rates for those interest-sensitive purchases.

Price level falls (bundle of goods costs less) rest of money into savings, more money available for borrowing interest rate down.

Think of money as stationary… demand drives up price of money.

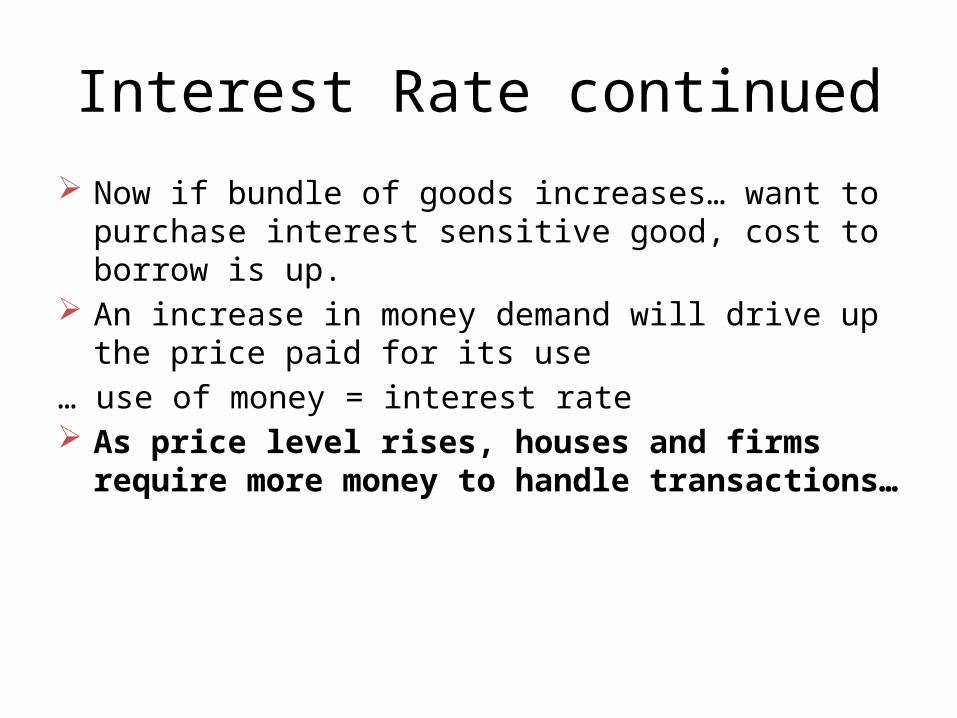

Interest Rate continued Now if bundle of goods increases… want to purchase interest

sensitive good, cost to borrow is up. An increase in money demand will drive up the price paid for

its use … use of money = interest rate As price level rises, houses and firms require more money to

handle transactions…

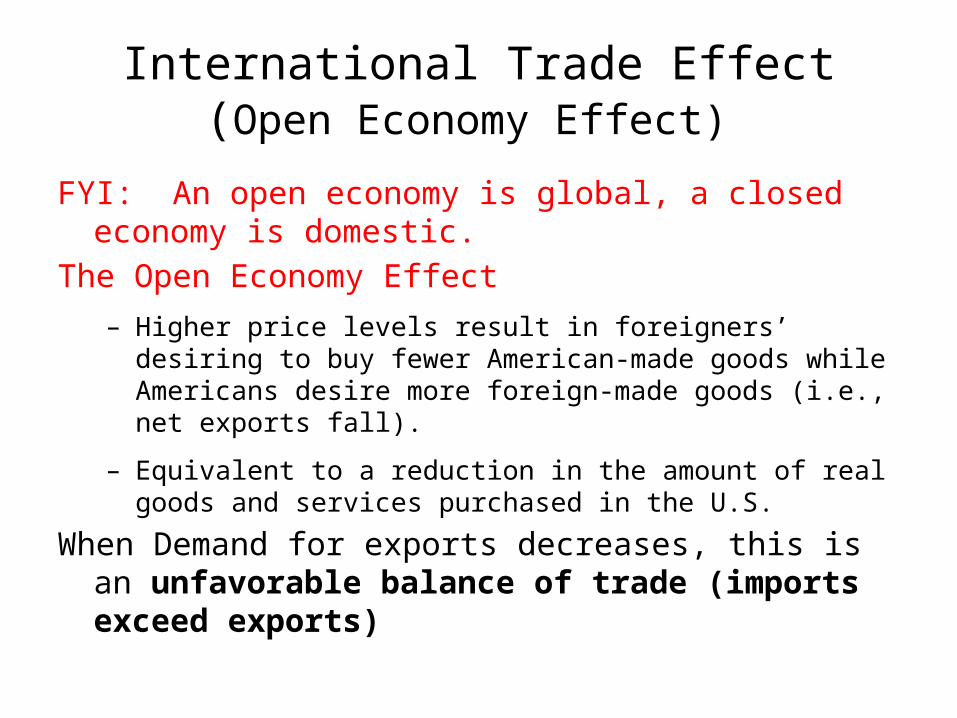

International Trade Effect (Open Economy Effect)

FYI: An open economy is global, a closed economy is domestic.The Open Economy Effect

– Higher price levels result in foreigners’ desiring to buy fewer American-made goods while Americans desire more foreign-made goods (i.e., net exports fall).

– Equivalent to a reduction in the amount of real goods and services purchased in the U.S.

When Demand for exports decreases, this is an unfavorable balance of trade (imports exceed exports)

Macro AD vs Micro D

Aggregate Demand versus Demand for a Single Good

When the aggregate demand curve is derived, we are looking at the entire circular flow of income and product.

When a market demand curve is derived, we are looking at a single product in one market only.

Change in QAD and Change in AD

What is the difference?

PL

GDP

A

B

PL

GDP

AD1AD 2

DETERMINANTS OF AGGREGATE DEMAND

Change in Consumer SpendingConsumption

•Consumer Wealth•Consumer Expectations (expect higher prices)• Interest rate (interest sensitive durables)

• Taxes

Changes in Investment Spending

• Real Interest Rates (rates high- not much I taking place)

• Expected Future Sales (health of economy- confidence is big)

• Business Taxes (higher taxes less profit)

Government Spending

This will be discussed further, but anytime government spends, it has an affect on GDP.Infrastructure – Health CareSupplies for militaryEducationEtc.

Net Export Spending

National Income Abroad-(when foreign nations do well, their incomes are higher- can buy more U.S. goods and services. – U.S. exports rise)

Exchange Rates- Price of one nation’s currency in terms of another. Dollar vs EuroOur currency appreciates if it takes more foreign $ to buy it.. (depreciates if it takes more of ours to buy theirs.) $1.00 to $1.25 Euro.Depreciation of nation’s currency makes foreign goods more expensive (but attracts foreigners to buy our goods.) Our exports rise. *this is why the Fed has not worried about our low dollar valuation.

Long-Run Equilibrium and the Price Level

For the economy as a whole, long-run equilibrium occurs at the price level where the aggregate demand curve (AD) crosses the long-run aggregate supply curve (LRAS).

Figure 10-5 Long-Run Economywide Equilibrium

SRAS

Period where adjustment occurs.

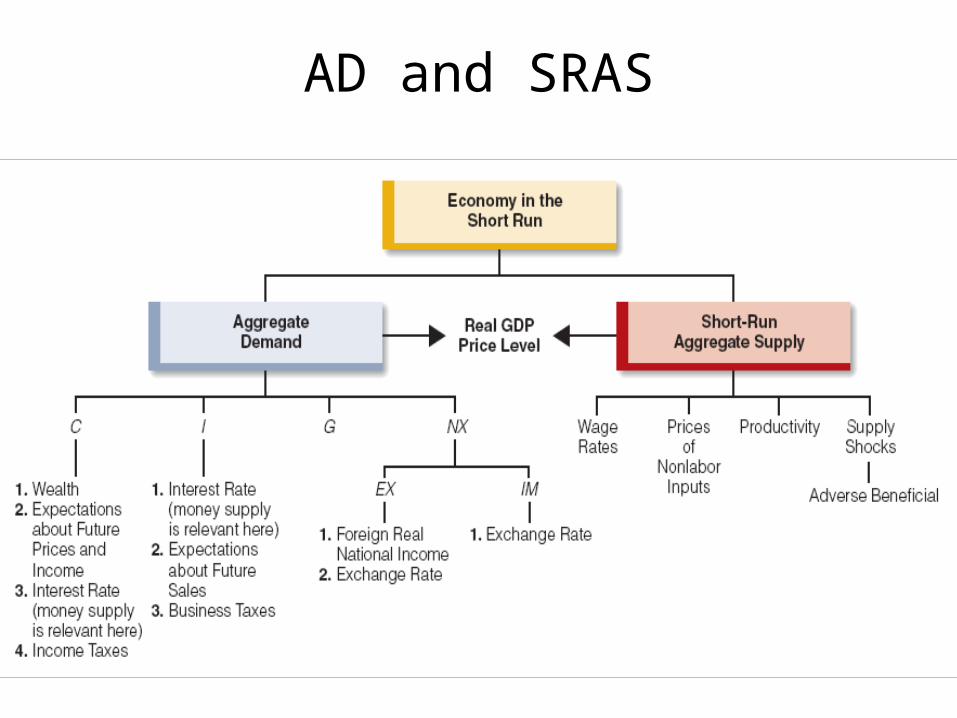

AD and SRAS

RealRateOfInterest

Money Supply

D1

D2

Can a Change in Money Supply Change AD?Probably… but it is a chain of events.MS changes, then Interest Rates, then chance in consumptionand investment. Then Change in AD

Long Run Aggregate Supply

Pric

e le

vel

Real domestic output, GDPQ

P LRASLR

Long-runAggregate

Supply

Qf

Full-Employment

LRAS

Goods & Services(real GDP)

Price level

P 100

YF

SRAS1

AD1

Unanticipated Increase in Aggregate Demand

In response to an unanticipated increase in AD for goods & services (shift from AD1 to AD2), prices will rise to P105 and output will temporarily exceed full-employment capacity (increases to Y2).

P 105

Y2

AD2

Short-run effects of an unanticipated increase in AD

LRAS1

Goods & Services(real GDP)

Price level

YF

AD

P 1

SRAS1

YF1

SRAS2

YF2

LRAS2

YF2 Here we illustrate the impact of economic growth due to capital formation or a

technological advancement, for example.

Both LRAS and SRAS increase (to LRAS2 and SRAS2); the full employment output of the economy expands from YF1 to YF2.

P 2

Growth in Aggregate Supply

A sustainable, higher level of real output and real income is the result. ***If the money supply is held constant, a new long-run equilibrium will emerge at a larger output rate (YF2) and lower price level (P2).

LRAS

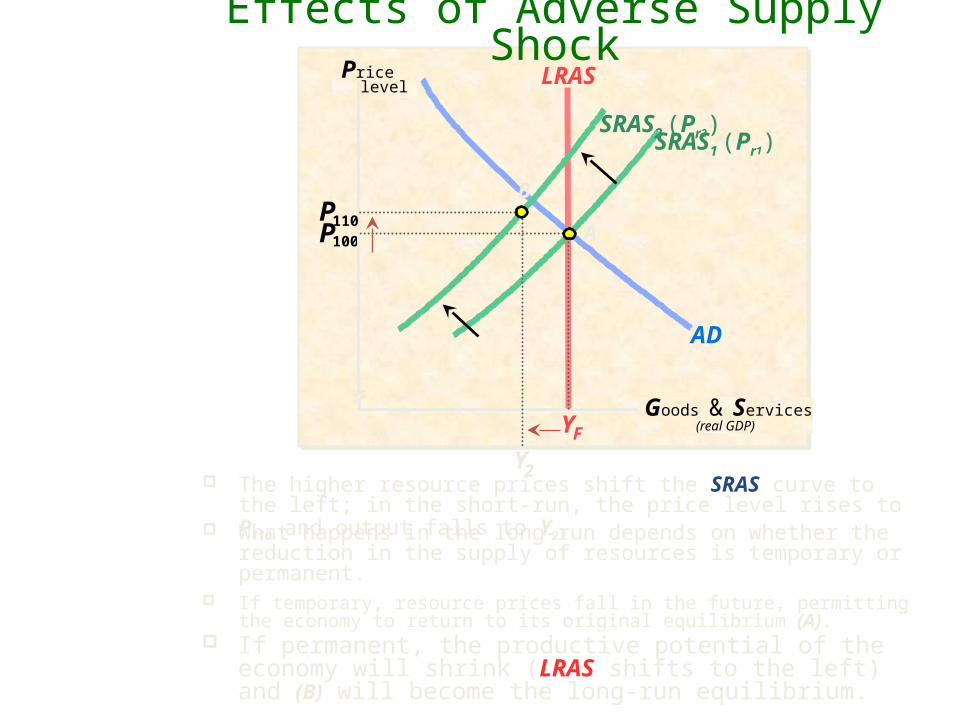

Goods & Services(real GDP)

Price level

AD

YF

P 100

SRAS1 (Pr1)

AP 110

Y2 The higher resource prices shift the SRAS curve to the left; in the short-run,

the price level rises to P110 and output falls to Y2. What happens in the long-run depends on whether the reduction in the

supply of resources is temporary or permanent.

Effects of Adverse Supply Shock

If temporary, resource prices fall in the future, permitting the economy to return to its original equilibrium (A).

If permanent, the productive potential of the economy will shrink (LRAS shifts to the left) and (B) will become the long-run equilibrium.

SRAS2 (Pr2)

B

Pric

e Le

vel

Real Domestic Output, GDP

Q

P ASAD1

INCREASES IN AD: DEMAND-PULL INFLATION

P2

P1

AD2

Qf Q1 Q2

Pric

e Le

vel

Real Domestic Output, GDP

Q

P AS1

AD1

DECREASES IN AS: COST-PUSH INFLATION

P2

QfQ1

a

b

AS2

P1

Long run growth

P

Y

xP1

Yf 1

AD1

Yf 2

LRAS1

AS1

AS2

AD2LRAS2

P2

Consumergoods

Capitalgoods

PPC shif ts out andLRAS shif ts right.

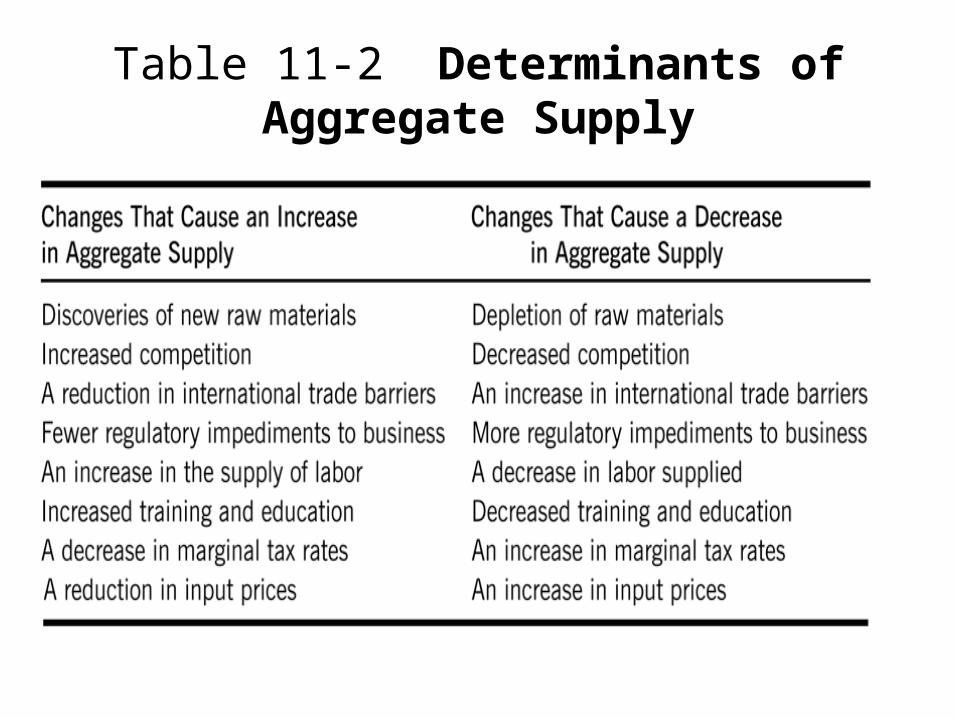

• Non-governmental actions that shift AS • Shift AS left:

– Raw materials cost rise– Wages rise faster than productivity– Worker productivity decreases– Obsolescence– Wars – Natural disasters

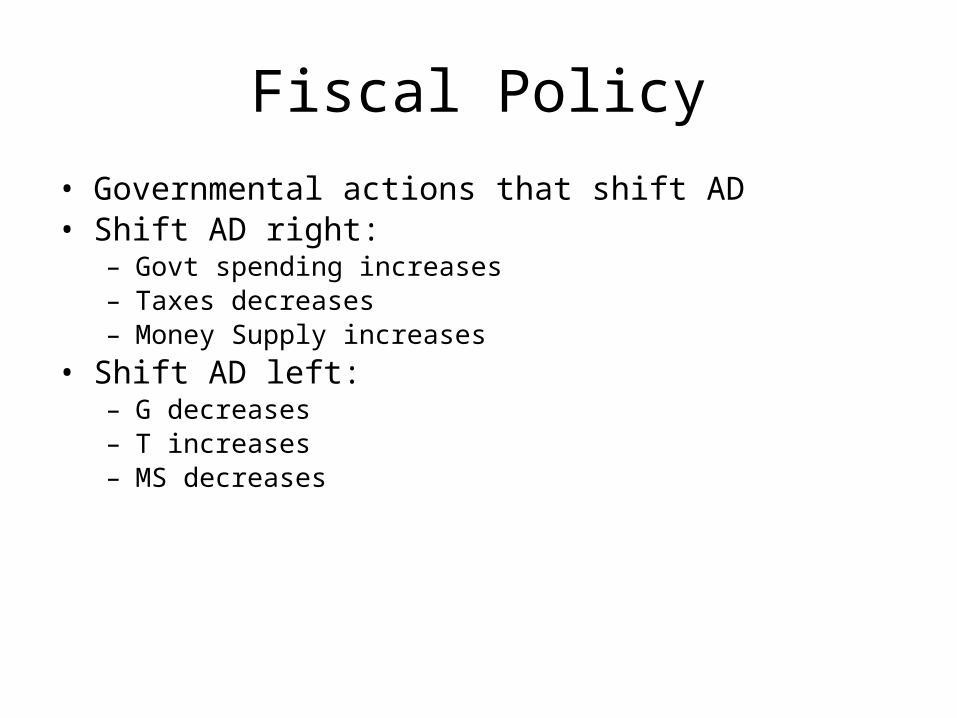

Fiscal Policy• Governmental actions that shift AD• Shift AD right:

– Govt spending increases– Taxes decreases– Money Supply increases

• Shift AD left:– G decreases– T increases– MS decreases

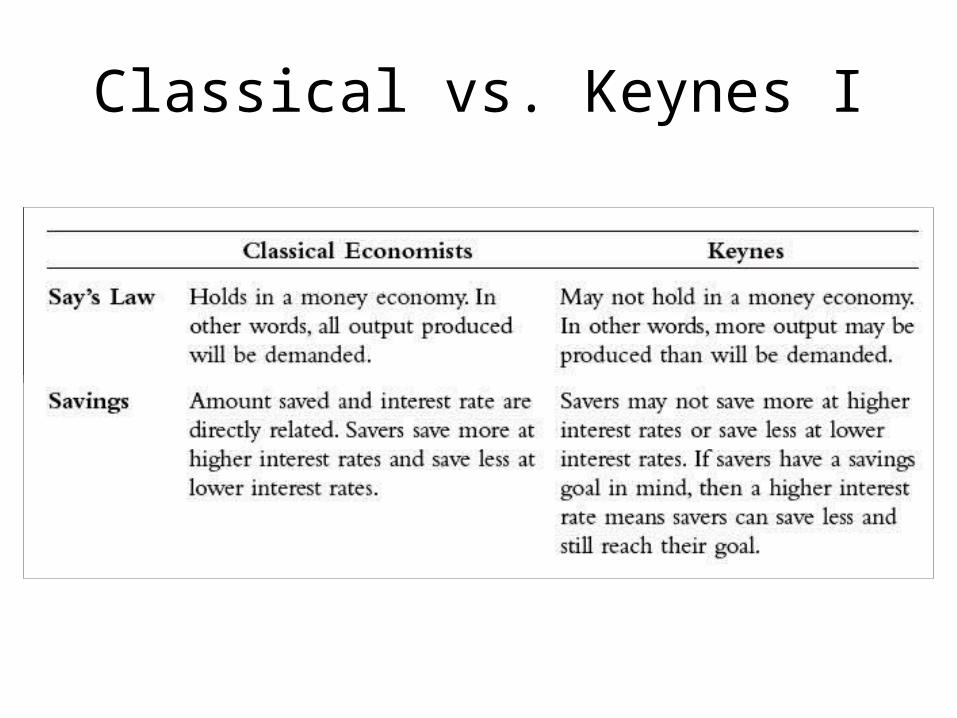

Chapter 11 Classical vs. Keynesian

CLASSICAL BELIEVES:Markets will behave according to S&D.

In other words. S&D will respond accordingly to “Inflationary Gap, Recessionary Gap, and long run stability when all curves intersect.

Basic Macroeconomic Relationships

Say’s LawHow Classical Works (or not)Interest Rate and InvestmentIncome and Consumption (or

savings)Changes in spending and changes in

output

SAY’S LAWEconomists agree Says law works in Barter

economy and disagree about if it works in a money economy.

Supply creates its own demand… baker bakes enough bread to trade for what he wants.That works.

Classical economics believes it works in money economy and here is why.

The Classical Model (cont'd)

• Classical economists—Adam Smith, J.B. Say, David Ricardo, John Stuart Mill, Thomas Malthus, A.C. Pigou, and others—wrote from the 1770s to the 1930s.

• They assumed wages and prices were flexible, and that competitive markets existed throughout the economy.

The Classical Model (cont'd)

• Assumptions of the classical model

– Pure competition exists.

– Wages and prices are flexible.

– People are motivated by self-interest.

– People cannot be fooled by money illusion.

The Classical Model • Consequences of The Assumptions

– If the role of government in the economy is minimal,

– If pure competition prevails, and all prices and wages are flexible,

– If people are self-interested, and do not experience money illusion,

– Then problems in the macroeconomy will be temporary and the market will correct itself.

Classical TheoryClassical economists believed that prices, wages and

interest rates are flexible. Say’s law says when economy produces a certain level

of real GDP, it also generates the income needed to purchase that level of real GDP.) hence, always capable of achieving the natural level of GDP.

Fallacy here: no guarantee that the income received will be used to purchase g & s.----some will be saved.

But theory would be redeemed, if the savings goes into equal needed amounts of investment.

Classical belief on wages and pricesBelieved all markets competitive- (S&D * Key) –

adjust to surplus and shortage….

If oversupply of labor, wage rates drop and S&D of labor will be in sinc.

What holds for wages also applies to prices.

Prices adjust quickly to surplus or shortages

Equilibrium established again.

Three States of the Economy

1. Real GDP is less than Natural Real GDP (recessionary gap)

2. Real GDP is more than Natural Real GDP (inflationary gap)

3. Real GDP is equal to Natural Real GDP.What is Natural Real GDP? Real GDP that is produced at the natural unemployment

rate. (which we agree around 5%)

Key: Wage rates and prices will adjust quickly to surplus or shortage

1) In recession- unemployment rate higher than natural rate.

2) Surplus exists in labor market3) Drives down wage rate

++++++++++++++4) In inflationary gap, unemployment lower than natural

rate5) Shortage exists in labor market 6) Drives up the wage rate

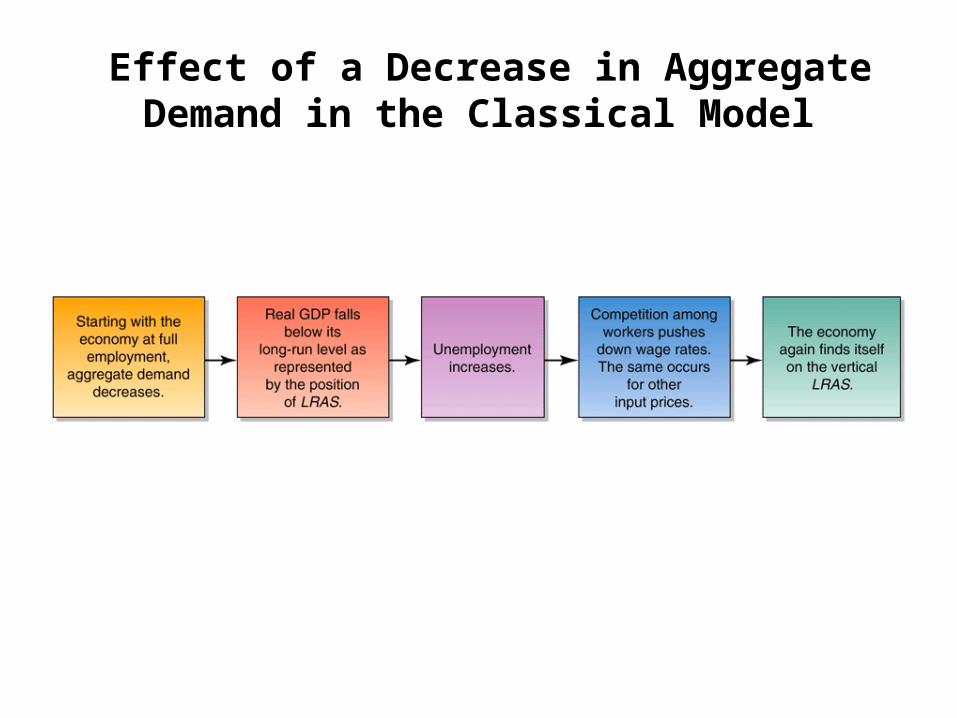

Effect of a Decrease in Aggregate Demand in the Classical Model

BOTH THEORIES CLASSICAL AND KEYNESIAN DO AGREE……

TWO THINGS WE CAN DO WITH DISPOSABLE INCOME-

SPEND OR SAVE!We all know that consumption is 2/3 (or more)

of GDP

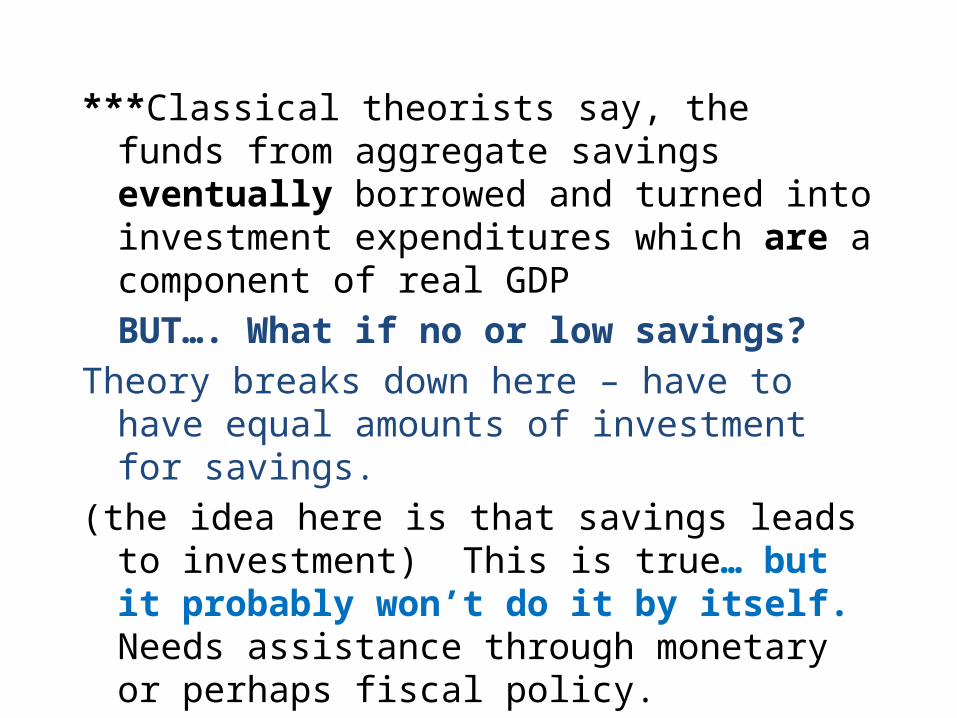

***Classical theorists say, the funds from aggregate savings eventually borrowed and turned into investment expenditures which are a component of real GDP BUT…. What if no or low savings?

Theory breaks down here – have to have equal amounts of investment for savings.

(the idea here is that savings leads to investment) This is true… but it probably won’t do it by itself. Needs assistance through monetary or perhaps fiscal policy.

The Classical View of the CreditMarket

In classical theory, the interest rate is flexible and adjusts so that saving equals investment.If saving increases and the saving curve shifts rightward the increase in saving eventually puts pressure on the interest rate and moves it downward. A new equilibrium is established where once again the amount households save equals the amount firms invest.

Long-run Equilibrium

The condition where the Real GDP the economy is producing is equal to the Natural Real GDP and the unemployment rate is equal to the natural unemployment rate.

Recessionary (Contractionary) Gap

The economy is currently in short-run equilibrium at a Real GDP level of Q1.

QN is Natural Real GDP or the potential output of the economy.

Notice that Q1< QN. When this condition (Q1< QN) exists, the economy is said to be in a recessionary gap.

Inflationary (Expansionary) Gap

The condition where the Real GDP the economy is producing is greater than the Natural Real GDP and the unemployment rate is less than the natural unemployment rate.

Policy Implication Laissez-faire

• Classical, new classical, and monetarist economists believe that the economy is self-regulating. For these economists, full employment is the norm: The economy always moves back to Natural Real GDP.

Laissez-faireA public policy of not interfering

with market activities in the economy.

Then what happened?

25% unemploymentBanks closedProduction ceasedDrought hitStocks worthlessNo money for purchasesNo jobsBleak!

ASADAD 1

AS 1

GDP

PRICE

LEVEL

Bottom Line

Classical viewpoint- not possible to overproduce goods because the

production of those goods would always generate a demand that was sufficient to purchase the goods.

(what would they say about the recent inventories of our auto industry?)

• Keynesian Ideas

The classical approach fell into disrepute during the economic decline of the 30’s. Real GDP fell by more than 30% 1930-33

In 1939- per capital income was still 10% less than in 1929.

*U.S. began to embrace John Maynard Keynes’s theory of stimulating the economy through aggregate demand (Lord Keynes) had studied classical economics and wrote his famous General Theory of Employment, Interest and Money. (which was a complete rebuttal of the classical theory)

Keynesian in a Nutshell

Keynes’s View of Say’s Lawin a Money Economy

According to Keynes, a decrease in consumption and subsequent increase in saving may not be matched by an equal increase in investment. Thus, a decrease in total expenditures may occur.

To learn more about John Maynard Keynes, click his photo above.

John Maynard Keynes and the Great Depression

• Classical Economics: In a recession,– Wages will fall (more will

be hired)– Prices will fall (more will

be bought)– The economy self-

regulates, and– Moves back to full-

employment GDP

• Keynes’ criticism: In a recession, – Wages would not fall.– Prices would not fall.– Self-regulation could not occur.– The economy could get “stuck” with high unemployment.

Keynes’ Prescription

• For an economy “stuck” at a high unemployment equilibrium,– Self-regulation was not working.– A “jumpstart” was needed:– An injection of new spending to get the economy

moving again.• The only spender who could do this was

Government.

Keynesian Economics

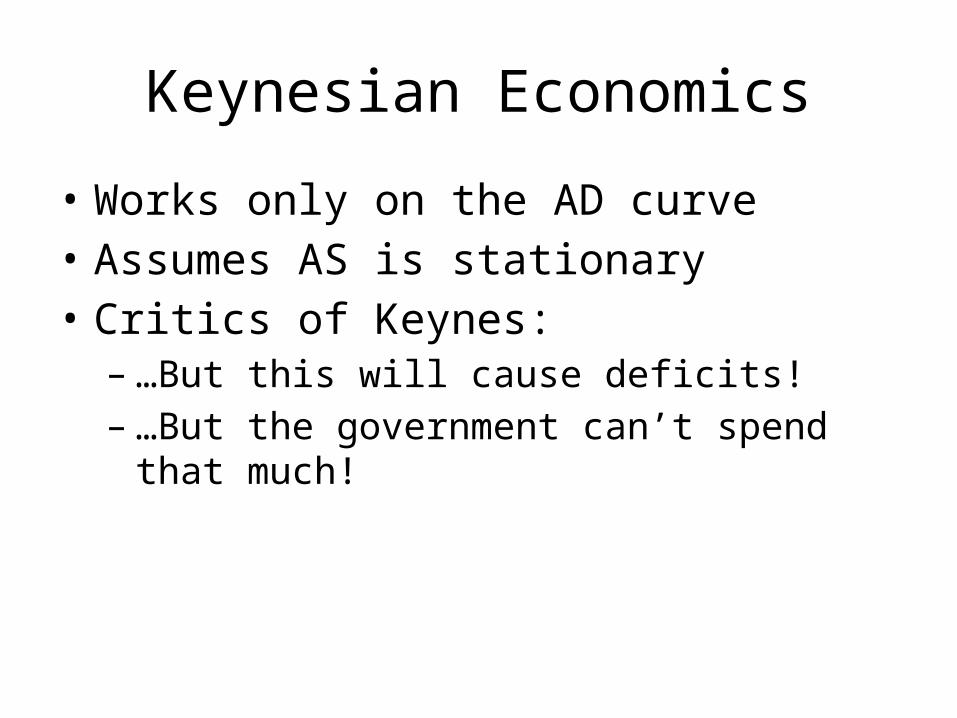

• Works only on the AD curve• Assumes AS is stationary• Critics of Keynes:

– …But this will cause deficits!– …But the government can’t spend that much!

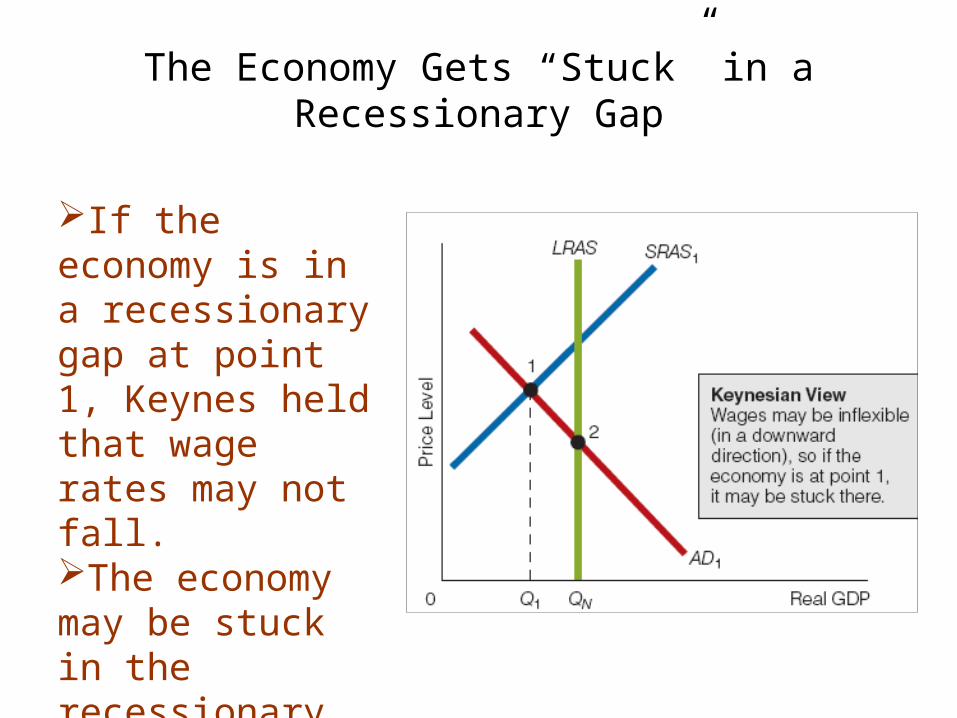

The Economy Gets “Stuck” in aRecessionary Gap

If the economy is in a recessionary gap at point 1, Keynes held that wage rates may not fall. The economy may be stuck in the recessionary gap.

Keynesian Economics and the Keynesian Short-Run Aggregate Supply Curve (cont'd)

• Real GDP and the price level, 1934–1940– Keynes argued that in a depressed economy, increased

aggregate spending can increase output without raising prices.

– Data showing the U.S. recovery from the Great Depression seem to bear this out.

– In such circumstances, real GDP is demand driven.

Keynesian Economics was the answer to Classical economic theories and the suggested way to “jump-start” the economy again… pull out of the depression.

Idea: Government enters the economy.Stimulates the economy through Aggregate Demand.Fiscal policy would move the production engine by

stimulating “spending.” increased employment, jobs would be filled,

production would begin people would purchase with money they earned from

jobs.

Classical vs. Keynes I

A Question of How Long It Takes forWage Rates and Prices to Fall

Suppose the economy is in a recessionary gap at point 1.

Wage rates are $10 per hour, and the price level is P1.

The issue may not be whether wage rates and the price level fall, but how long they take to reach long-run levels

• The speed at which wage rate falls is a keyTo whether Keynesian or Classical theory Is more valid. Answers never for sure.

Keynes rejected the classical notion of self-adjustment, (????) and he predicted things would get worse once a spending shortfall emerged.

Example:• Business expectations of future sales worsens.• Business investment is cut back.• Unsold capital goods begins to pile up (includes office equip.

machinery, airplanes, etc.)• *this is an “undesired” change…• Worsened sales expectations causes decline in investment

spending that shifts the AD curve to the left leading to pileups of unwanted inventory.

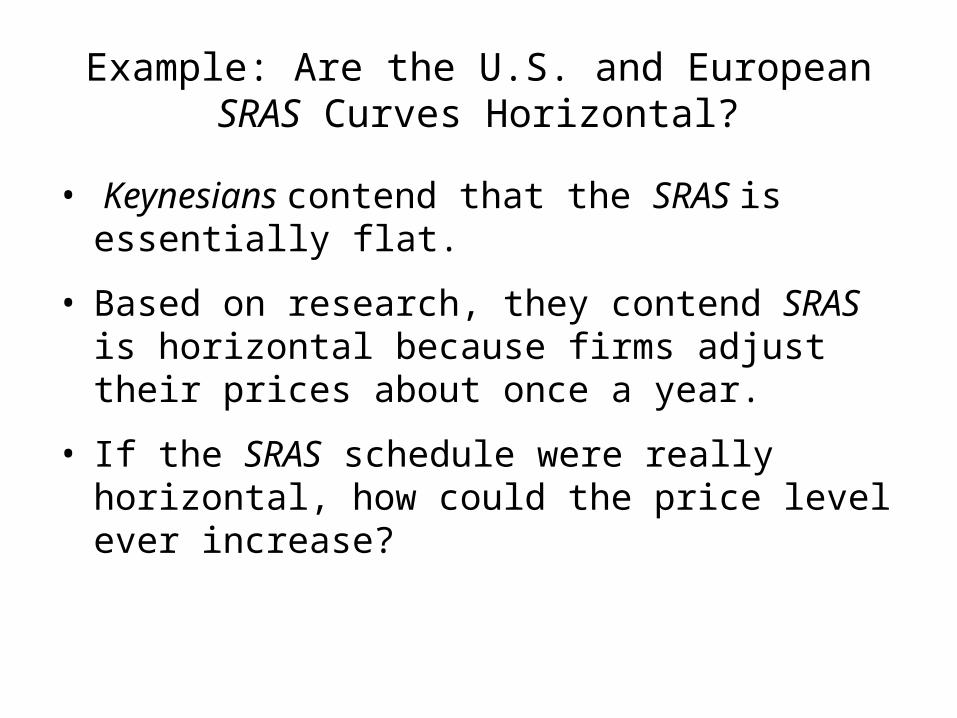

Example: Are the U.S. and European SRAS Curves Horizontal?

• Keynesians contend that the SRAS is essentially flat.

• Based on research, they contend SRAS is horizontal because firms adjust their prices about once a year.

• If the SRAS schedule were really horizontal, how could the price level ever increase?

Keynesian Theory

AS

LRAS

PRICE

LEVEL

Real GDP OutputKeynesian Theory

AD unstable, prices and wages are inflexible AD no effect on prices until LRAS

AD 1 AD 2 AD 3 *PriceGoes up

Figure 11-9 Real GDP Determination with Fixed versus Flexible Prices

Table 11-2 Determinants of Aggregate Supply

QUESTIONS?