Embed Size (px)

Citation preview

COLLECTION AND BANKRUPTCY LAWS

December 3, 2010

Idaho Healthcare Financial Management Association

PRESENTED BY: MIKE CHAPMAN

Chapman Law Office, PLLC2100 Northwest Blvd, Suite 230

P.O. Box 1600Coeur d’Alene, ID 83816

• This information is not intended as legal advice and may not be used as legal advice. It should not be used to replace the advice of your own legal counsel.

TOPICS

• COLLECTION LAWSUITS

• BANKRUPTCY

COLLECTION LAWSUITS

• STATEMENTS AND ASSIGNMENTS– HIPAA

• STATUTE OF LIMITATIONS

• COMPLAINT/SERVICE

• DEBTOR’S RESPONSE

• GARNISHMENT/DEBTOR’S EXAMS

ITEMIZED STATEMENTS

• ITEMIZED STATEMENTS

– DATE(S) OF SERVICE & AMOUNT(S) OWED

– IF POSSIBLE, DEBTOR’S SIGNATURE ACCEPTING FINANCIAL RESPONSIBILITY.

ASSIGNMENTS

• AGREEMENT THAT TRANSFERS INTANGIBLES (I.E. ACCOUNT RECEIVABLES) TO ANOTHER PARTY FOR PURPOSES OF COLLECTION.

• LEGAL RIGHT TO COLLECT A DEBT.

• SUIT ON HOLD UNTIL RECEIVED FROM CLIENT

STATUTE OF LIMITATIONS

• MAXIMUM TIME LIMIT TO FILE A LAWSUIT

IDAHO-Oral Contract=4 Years

-Written Contract=5 Years

-Partial Payment Restarts the Statute

--Credit Reports- 7 years

COMPLAINT/SERVICE

• GENERALLY, MULTIPLE CREDITORS AND MULTIPLE ACCOUNTS

• FILED IN COUNTY WHERE DEBTOR RESIDES

• PERSONAL OR SUBSTITUTE SERVICE ON DEBTOR WITHIN SIX MONTHS

DEBTOR’S RESPONSE

• DO NOTHING/DEFAULT JUDGMENT

• CALL AND PIF OR ACCEPTABLE PAYMENT ARRANGEMENTS

• FILE ANSWER ADMITTING/DENYING CLAIMS—(INSURANCE/MEDICAID/ MEDICARE)

• BANKRUPTCY

JUDGMENT COLLECTIONS

* A JUDGMENT IS JUST A PIECE OF PAPER THAT SAYS YOU ARE ENTITLED TO MONEY FROM THE DEFENDANT.

* IN MOST CASES, THE DIFFICULT PART IS COLLECTING ON THE JUDGMENT BECAUSE PAYMENT IS NOT VOLUNTARY.

EXECUTIONS/ATTACHMENTS

* All personal property, real property and money is subject to execution/attachment unless exempt by law.

1. Continuing Writ of Garnishment-Wages

2. Writ of Attachment-Bank Account

3. Judgment Lien on Real Property

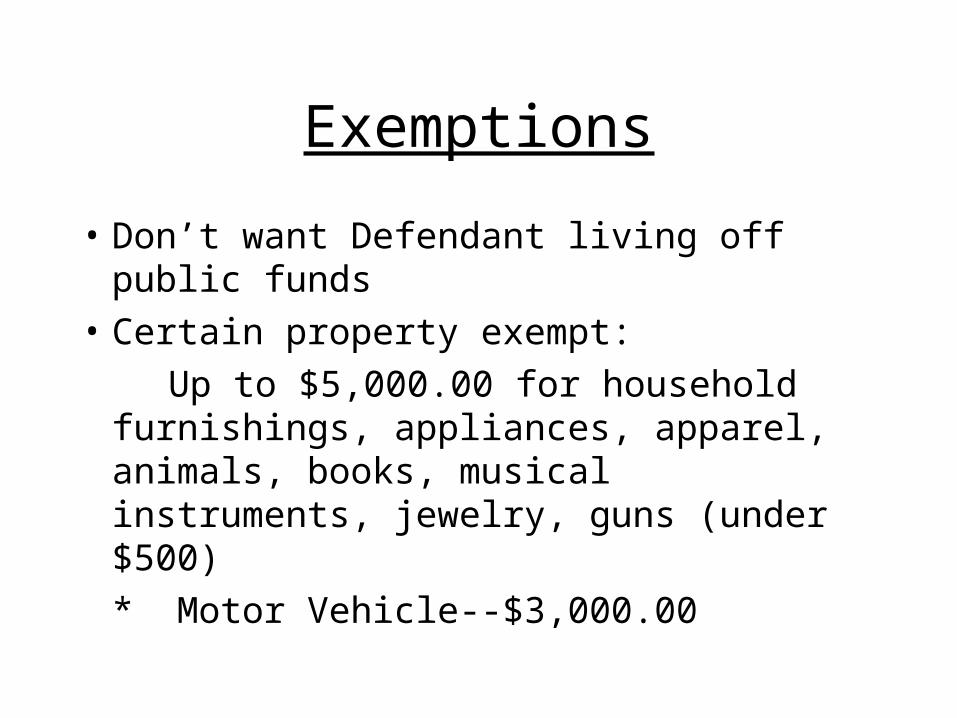

Exemptions

• Don’t want Defendant living off public funds

• Certain property exempt:

Up to $5,000.00 for household furnishings, appliances, apparel, animals, books, musical instruments, jewelry, guns (under $500)

* Motor Vehicle--$3,000.00

WAGES

• Continuing Garnishment until Paid in Full• Idaho provides that a Judgment Creditor can

garnish either a) 25% of net income or b) any amount over 30 times the federal minimum wage, whichever is greater.

DEBTOR EXAMS

• ADDRESS• PHONE NUMBER• MARITAL STATUS• CHILDREN• CHILD SUPPORT• EMPLOYMENT

• INCOME• MONTHLY

EXPENSES• BANK ACCOUNTS• TAX RETURNS• STUDENT LOANS• RENT/CAR

PAYMENTS

COMMON SCENARIOS

• Divorce– Community Property– Necessaries for Kids– Divorce Decree

Deceased Debtors

Minors- Power to disaffirm contracts, however can’t disaffirm contracts for necessaries if not living at home.

COMMON SCENARIOS

• Tribal Court

• Checks Marked Paid In Full

• Accepting Regular Small Payments

BANKRUPTCY

• FEDERAL STATUTES THAT RELEASE OR “DISCHARGE”A PERSON OR BUSINESS FROM ALL OR MOST OF THEIR DEBTS.

PURPOSE

• GIVE THE DEBTORS A FRESH START.

• EQUAL TREATMENT OF LIKE-SITUATED CREDITORS.

TYPES OF BANKRUPTCY

1)CHAPTER 7-LIQUIDATION• The debtor turns over all assets owned at the time of

bankruptcy to a trustee for liquidation. However, the debtor is entitled to retain certain exempt assets.

TYPES OF BANKRUPTCY

2) CHAPTER 11-REORGANIZATION• Most often used by corporations & partnerships.

3) CHAPTER 12-REORGANIZATION

Agricultural businesses.

TYPES OF BANKRUPTCY

4) CHAPTER 13-REORGANIZATION• Debtor is permitted to reorganize their personal

finances by paying accumulated debt out of their current income over a 3-5 year period.

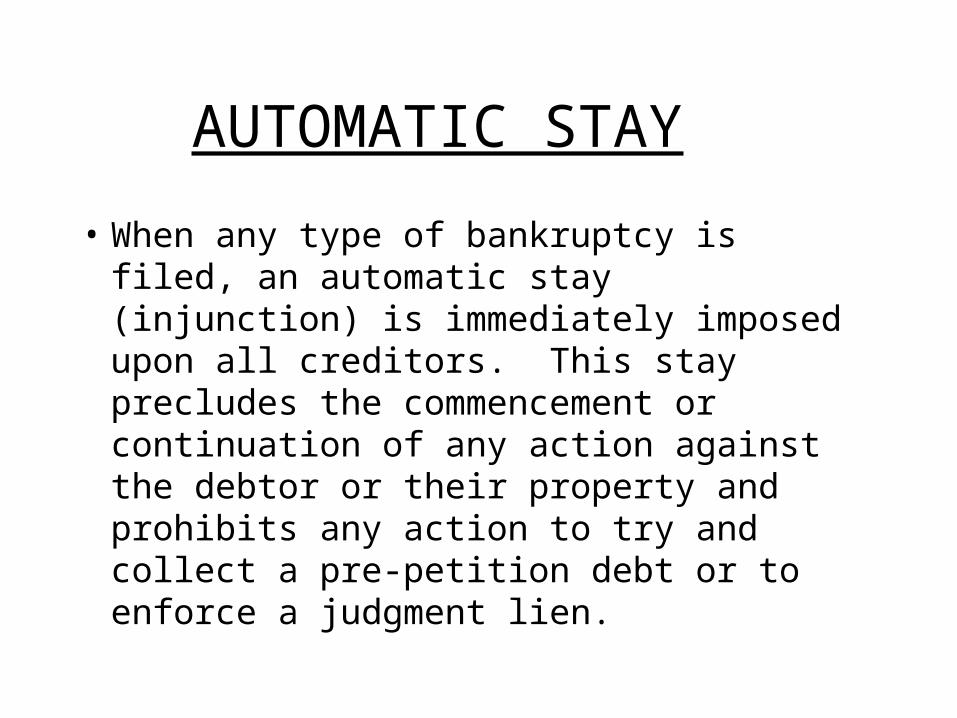

AUTOMATIC STAY

• When any type of bankruptcy is filed, an automatic stay (injunction) is immediately imposed upon all creditors. This stay precludes the commencement or continuation of any action against the debtor or their property and prohibits any action to try and collect a pre-petition debt or to enforce a judgment lien.

NOTICE OF AUTOMATIC STAY

• Any action taken without court approval after the bankruptcy is filed is a violation of the automatic stay, whether or not the creditor knew of the bankruptcy filing. Moreover, any action taken in violation of the stay is subject to contempt proceedings before the bankruptcy court and the imposition of fines, including attorney fees.

2005 BANKRUPTCY REFORM ACT

• Most substantial revision to the bankruptcy laws in almost 30 years.

• Effective date October 17, 2005

HIGHLIGHTS

• NONPROFIT CONSUMER CREDIT COUNSELING-MANDATORY

• MEANS TEST• CHANGES TO AUTOMATIC STAY

RULES• NOTICES REQUIRED TO BE GIVEN TO

CREDITORS• MORE DOCUMENTATION REQUIRED

HIGHLIGHTS

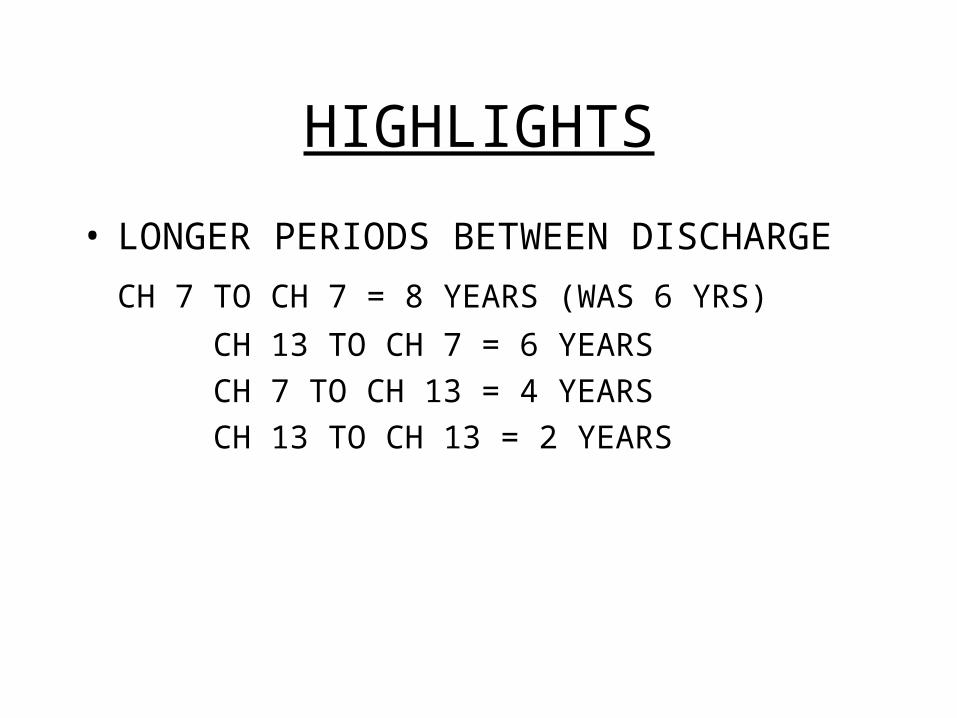

• LONGER PERIODS BETWEEN DISCHARGE

CH 7 TO CH 7 = 8 YEARS (WAS 6 YRS)

CH 13 TO CH 7 = 6 YEARS

CH 7 TO CH 13 = 4 YEARS

CH 13 TO CH 13 = 2 YEARS

COMMON SCENARIOS

• Preferences – Why is the Trustee asking me to give money back?

• Reaffirmation Agreements

• My Account Is Not Listed—Blanket Discharge

• Voluntary Payments—After Bankruptcy