Embed Size (px)

Citation preview

COLGATE PALMOLIVE INDIA LTD.

Disclaimer This Presentation and its related publication, release, webcast or communication (together the “Presentation”) is for general information purposes only. This Presentation does not solicit any action by Colgate-Palmolive (India) Limited (the “Company”) based on the material contained herein. Nothing in this Presentation is intended by the Company to be construed as legal, accounting, investment or tax saving advice. This Presentation includes statements that are, or may be deemed to be, “forward‐looking statements”(except for the historical information). These forward-looking statements appear in several places in the Presentation and are based on certain expectations, assumptions, anticipated developments and various other factors which are not limited to, risk and uncertainties regarding fluctuations in market share, earnings, market growth, intense competition and the pricing environment in the market, consumption level, ability to maintain and manage key business stakeholders and external factors having impact on the conduct of the business not limited to inflation, currency fluctuations, climatic changes, political and regulatory environment, Government policies and changes in international oil prices etc. The Company, therefore, in no way assures, represents, warrants, guaranty, undertake, express or imply, given that such statements, views, projections or forecasts are correct or that the objectives of the Company will be achieved as contained in the Presentation. The Company’s actual results of operations, financial condition, stability, liquidity, and the development of the industry / business sector in which the Company operates, may differ materially from those suggested by the forward‐looking statements contained in this Presentation. The Company may alter, amend, modify, revise or make necessary changes in any manner to any such forward looking statements contained herein including but not limited to oral forward looking statements as may be required from time to time on the basis of any subsequent developments, conditions, circumstances, information, events or otherwise.

The Company expressly disclaims and does not assume or undertake any obligation to update forward looking statements to reflect the events, developments or circumstances after the date of the Presentation. Neither the Company nor its affiliates or advisors or representatives nor any of its or their parent or subsidiary companies or undertakings or any such person's officers, directors or employees guarantees that such forward‐looking statements and its assumptions, including oral or implied, are error free, lacking omissions, fair, accurate and complete nor does either assume or accept any responsibility for such forward‐looking statements in future or the actual occurrence of such projections or forecast based on such forward-looking statements. This Presentation should not be in any manner whatsoever construed as an approval, acknowledgement, confirmation or acceptance by any statutory or regulatory authority in India including the stock exchanges in India. The material contained in this Presentation is subject to change without notice and past performance and historical trends or information is not indicative of future results. This Presentation is for information purposes only and does not constitute or should not be construed as an offer / invitation for sale or subscription of or solicitation for any securities of the Company. Investors are cautioned to exercise diligence before taking any investment decisions or otherwise and Company assumes no responsibility for any loss or damage suffered due to any decisions made on the basis of this Presentation.

Financial Results

Financial Strategy

Sales/ Volume

Margin

Non Variable

Overheads

Advertising

Operating Profit

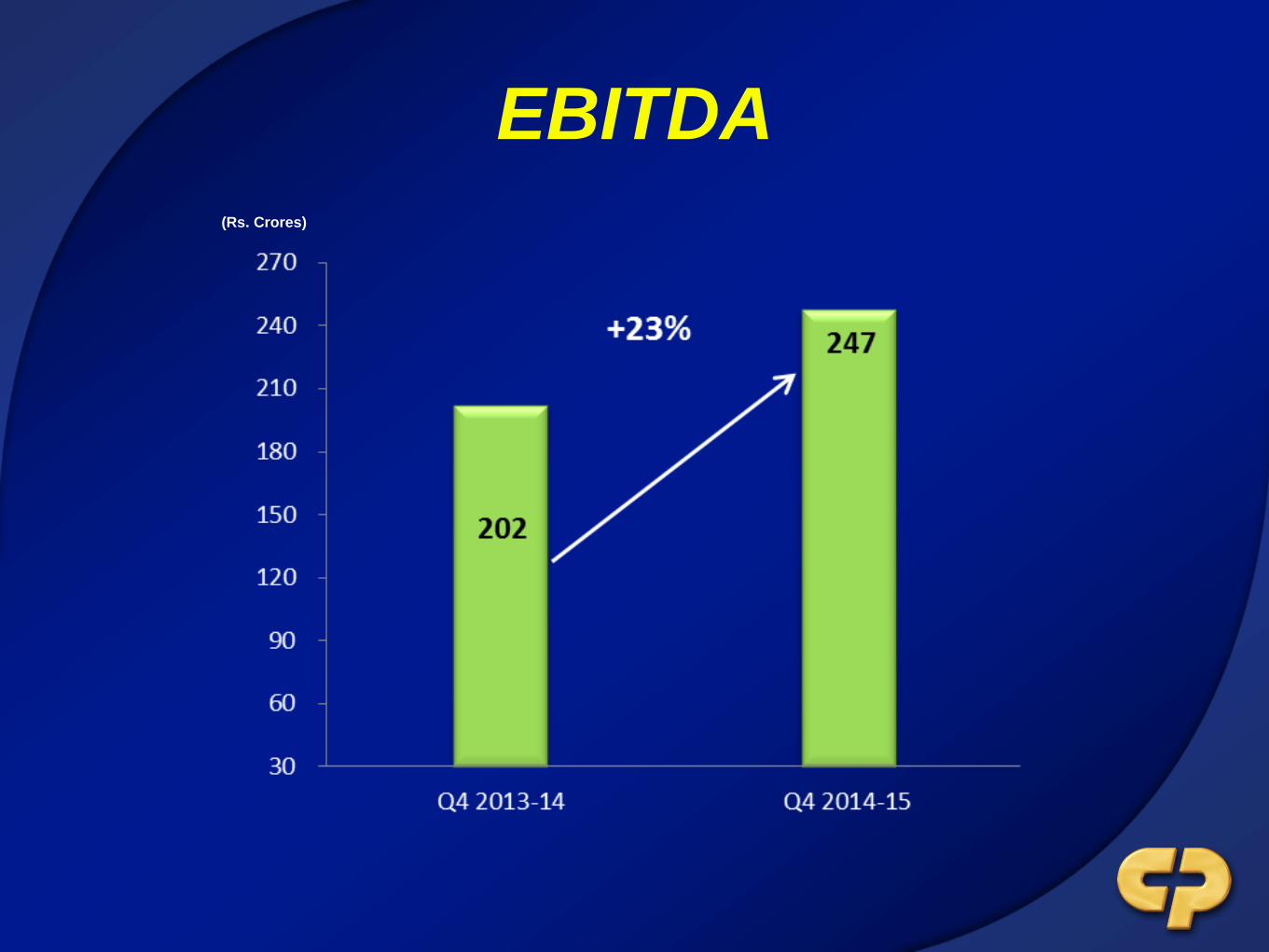

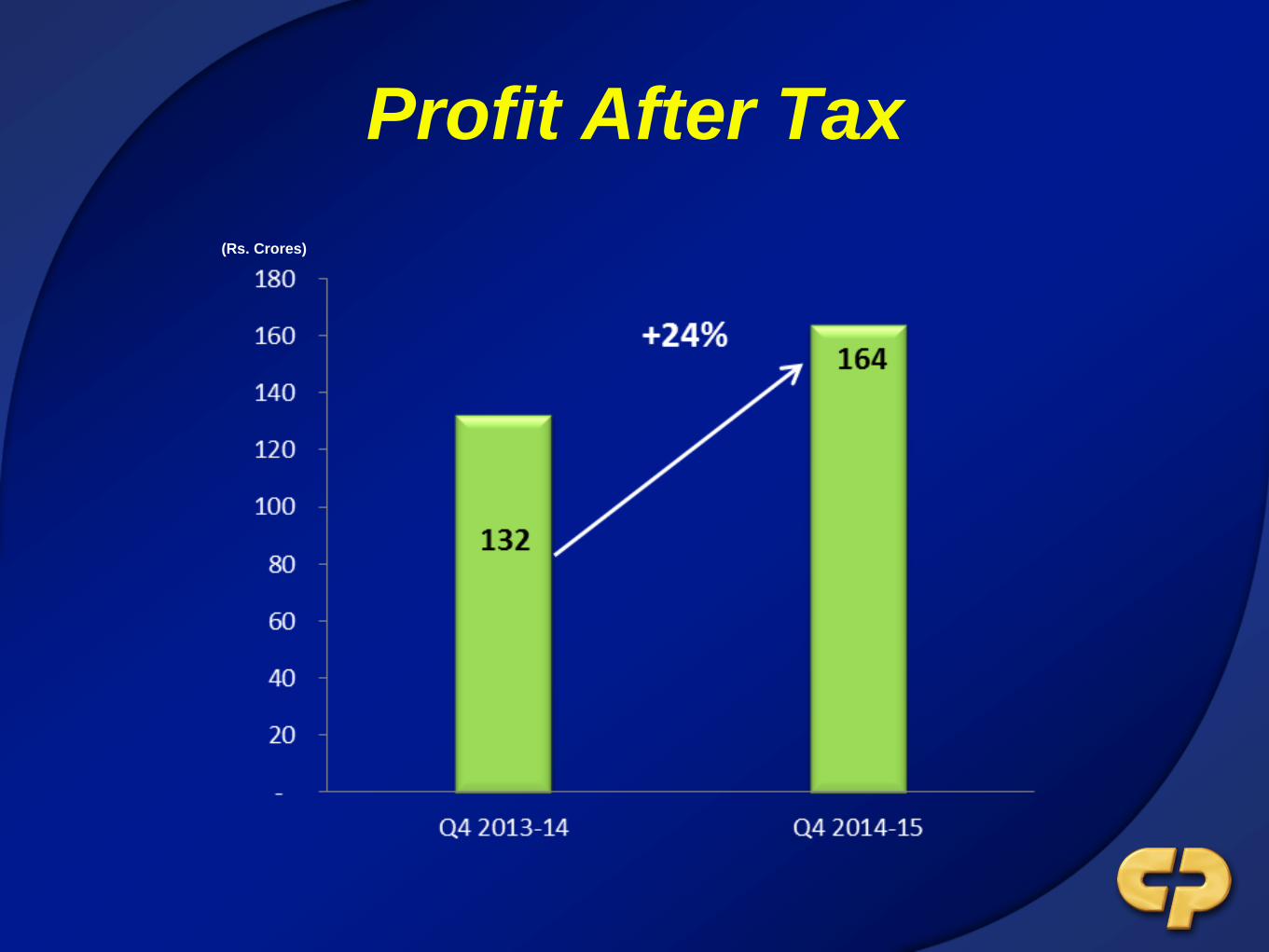

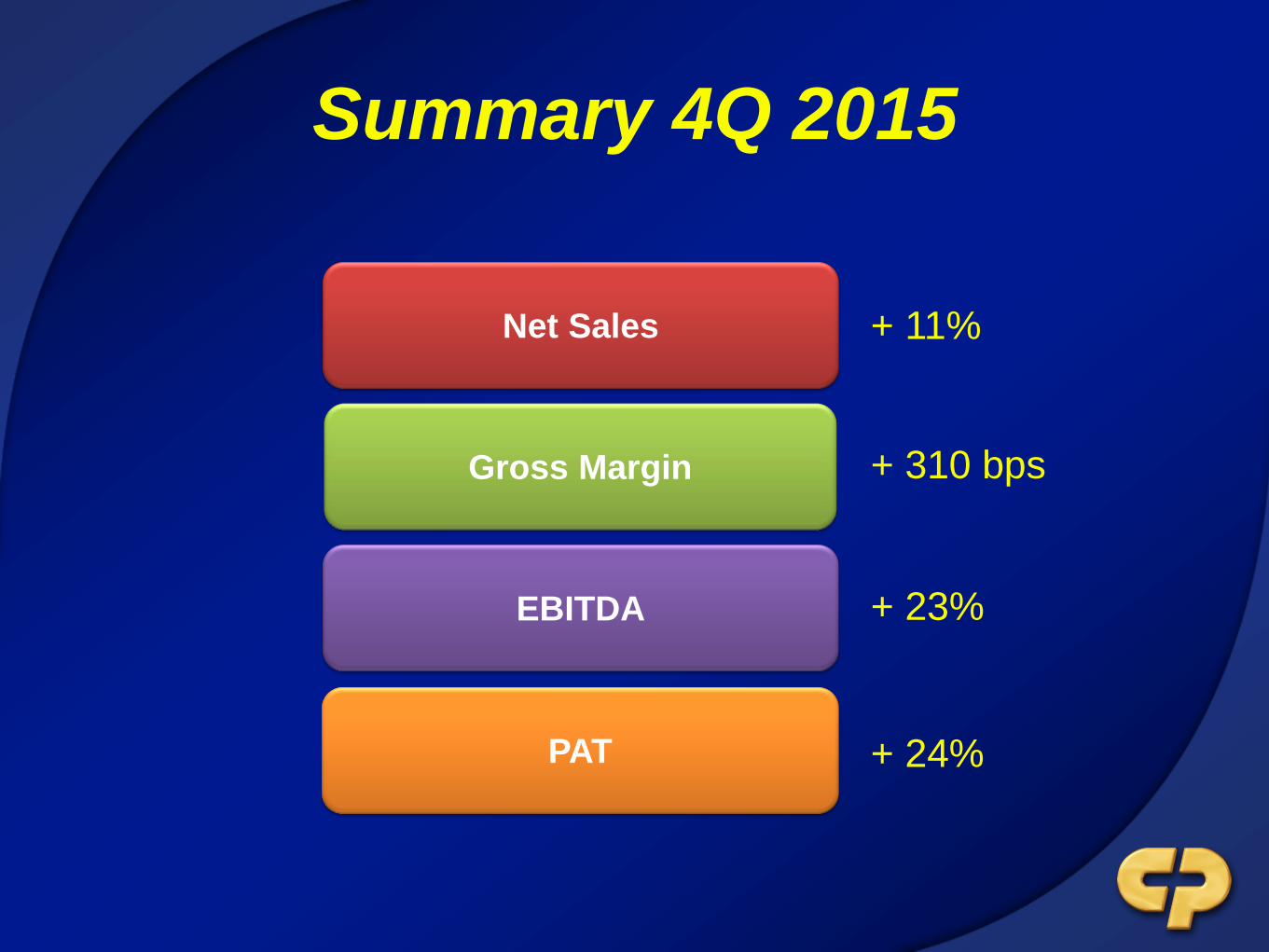

4Q 2015

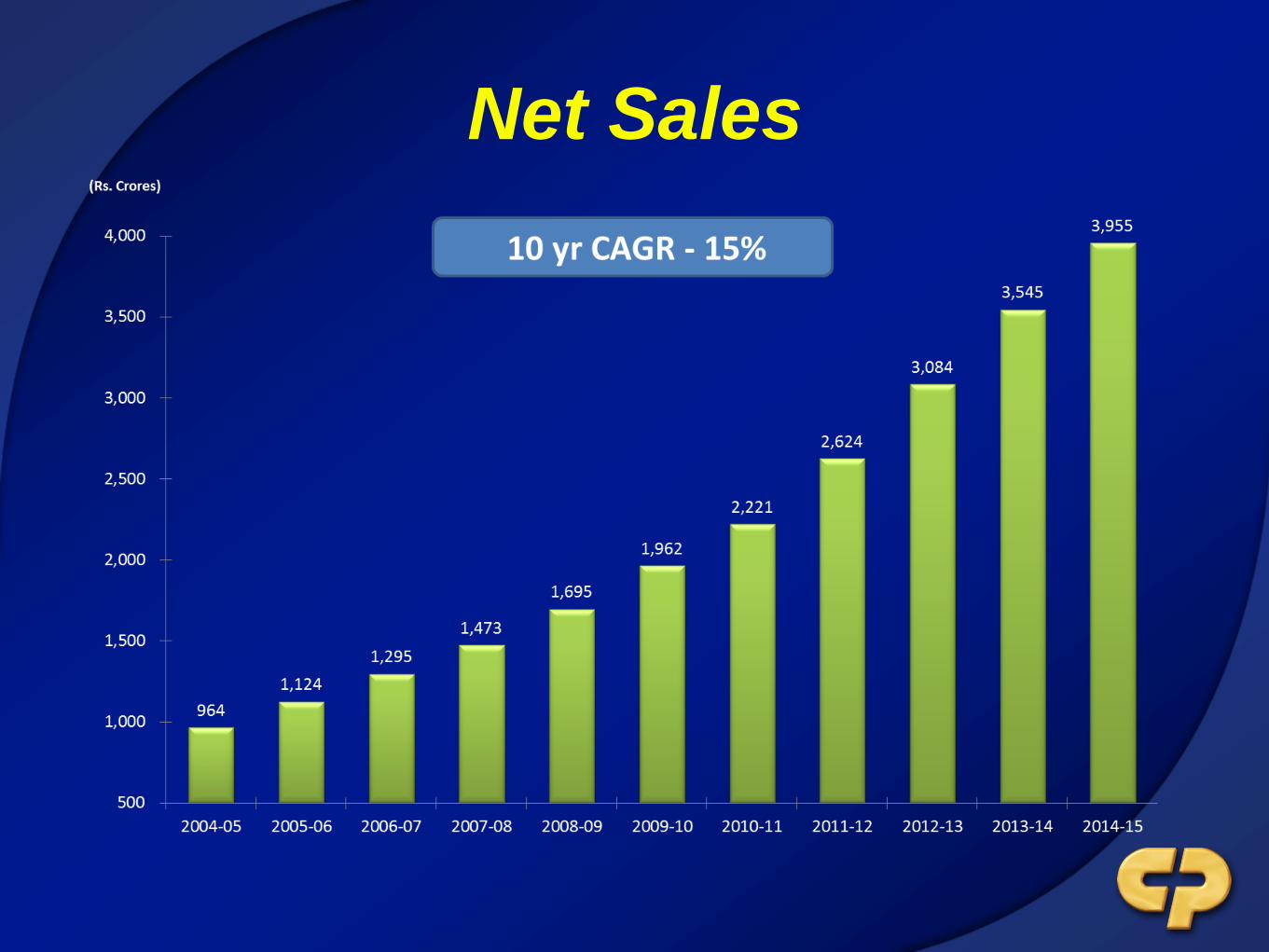

Net Sales

(Rs. Crores)

Gross Margin

EBITDA

(Rs. Crores)

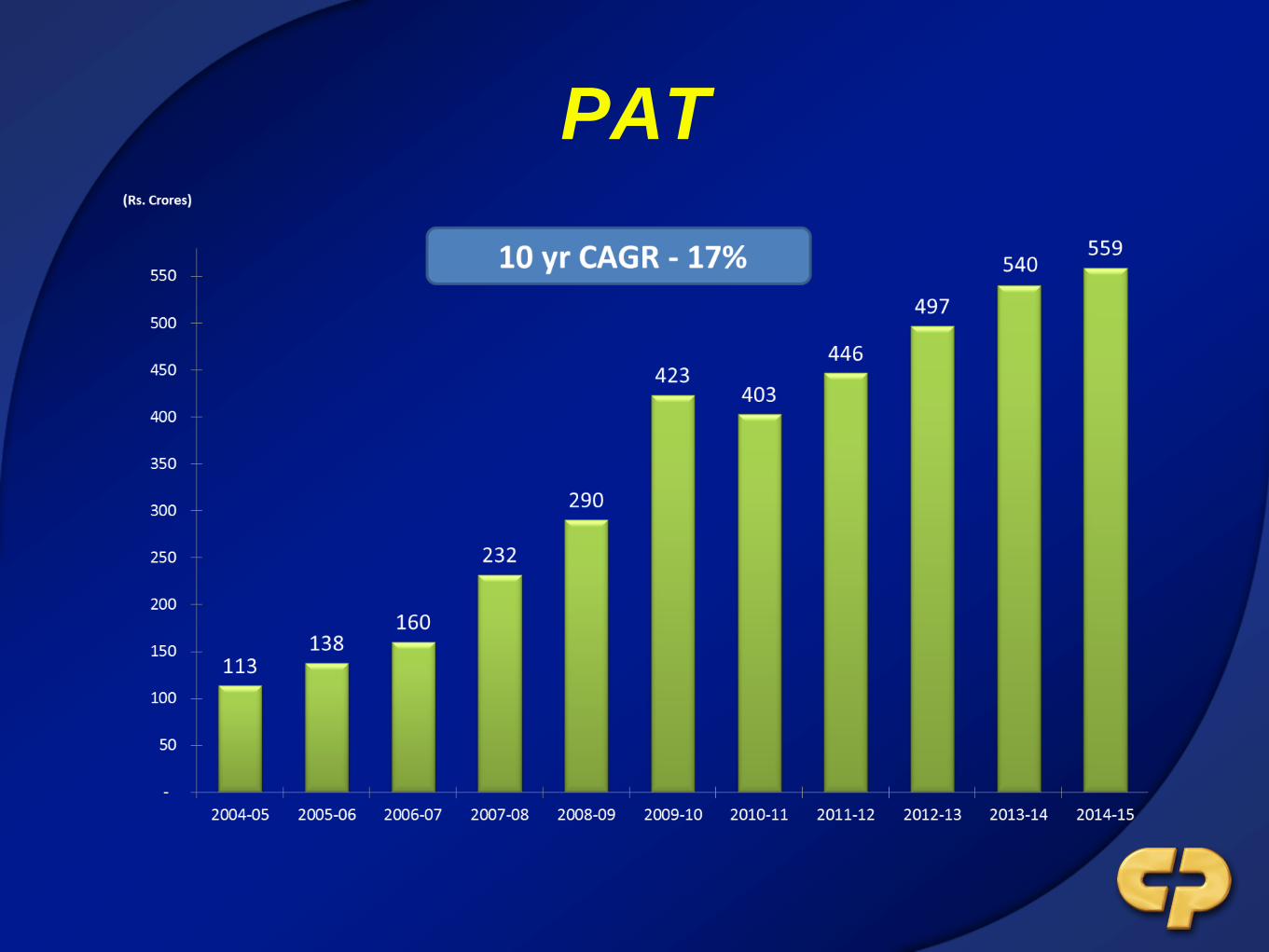

Profit After Tax

(Rs. Crores)

Summary 4Q 2015

Net Sales

Gross Margin

PAT

EBITDA

+ 11%

+ 310 bps

+ 23%

+ 24%

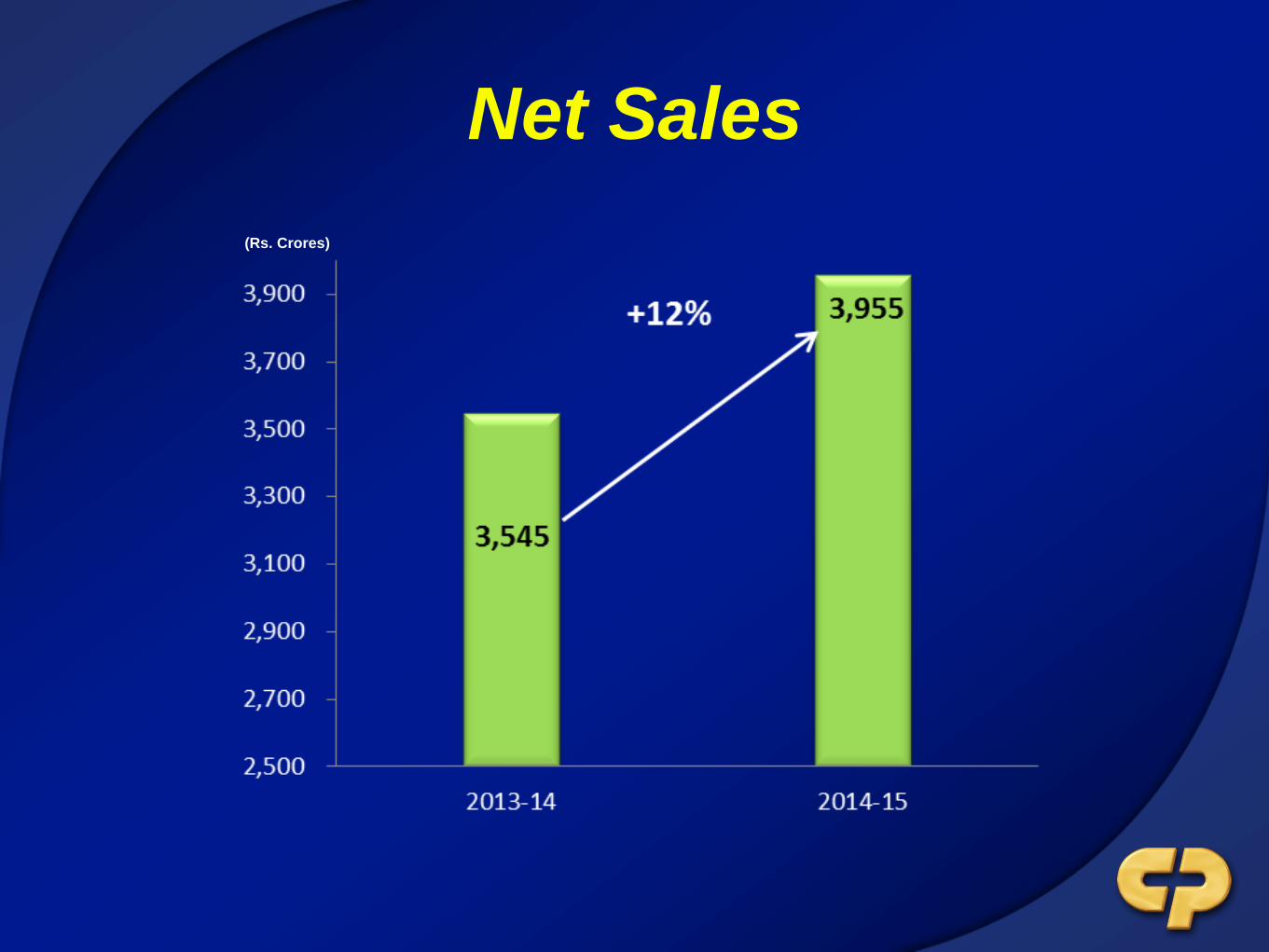

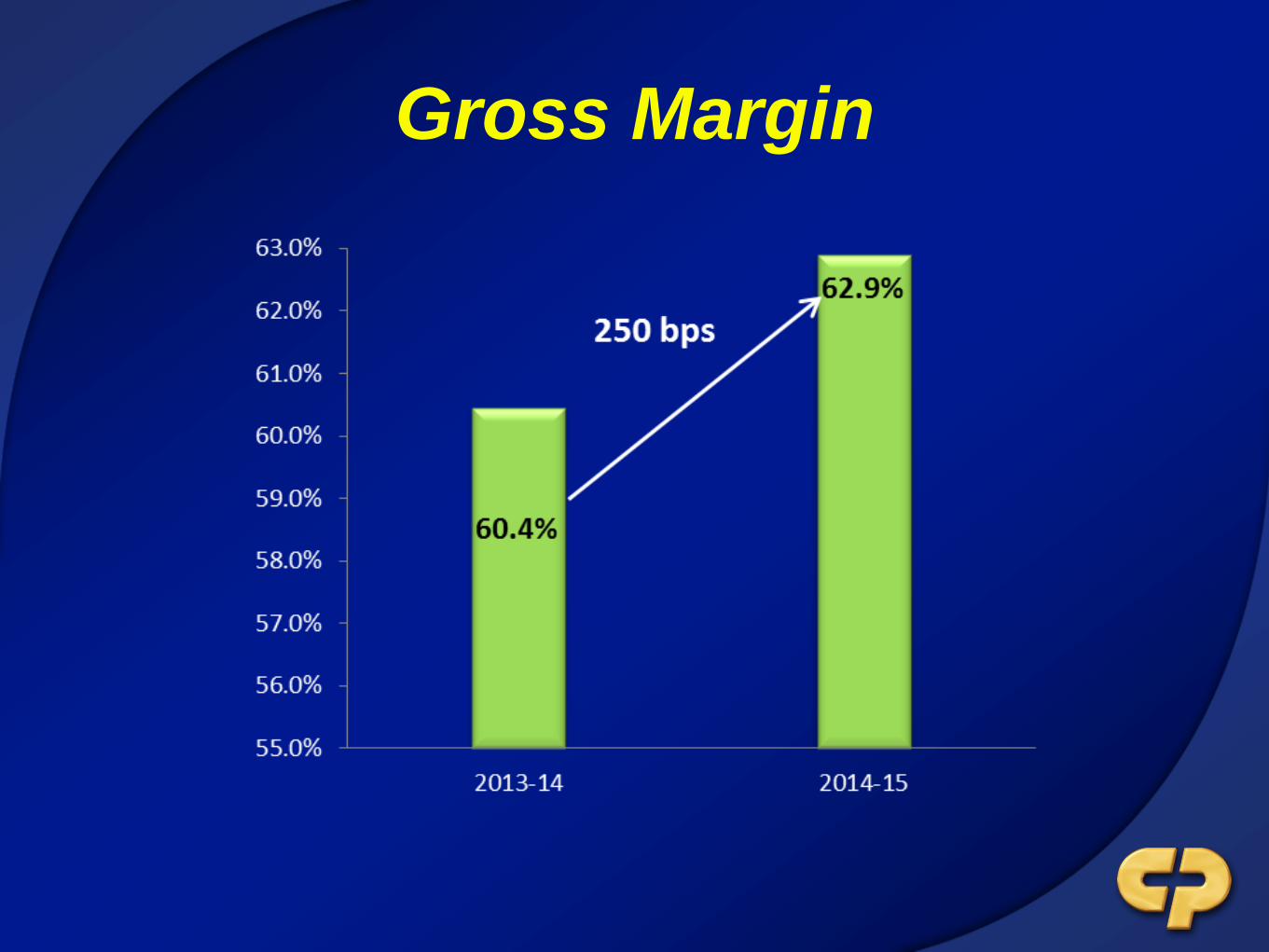

Full Year 2014-2015

Net Sales

(Rs. Crores)

Gross Margin

EBITDA

(Rs. Crores)

Profit After Tax

- 2013-14 PAT is excluding exceptional items due to GSSO slump sale

(Rs. Crores)

Summary 2014-2015

Net Sales

Gross Margin

PAT

EBITDA

+ 12%

+ 250 bps

+ 24%

+ 14%

It has been a challenging

environment

GDP Growth

9.5 9.6 9.3

6.7

8.6 8.9

6.7

4.7 5.0 5.6

FY0

6

FY0

7

FY0

8

FY0

9

FY1

0

FY1

1

FY1

2

FY1

3

FY1

4

FY1

5E

Source: Citibank Macro Flash reports (old series)

FMCG Growth

7.5%

4.8%

9.1% 8.5%

6.8%

5.4% 4.5% 4.4%

4.9% 5.0% 4.5% 4.6%

4.3%

2.3%

4.0%

4.2%

3.2% 5.8%

4.3%

1.0%

1.2%

2.9% 4.3%

5.7%

11.7%

7.1%

13.2% 12.6%

10.0%

11.2%

8.8%

5.4% 6.1%

8.0%

8.8%

10.3%

Price led growth Consumption growth Value growth

Source: Nielsen RMS All India (U+R)

FMCG nos. does not include Soft Drinks/ Liquor/ Juices

We continue to focus on our

proven strategic initiatives

Key Strategic Initiatives

• Engage to build our brands

• Innovation for growth

• Effectiveness & Efficiency

• Leading to Win

Our consumer franchise &

equity continue to grow

Toothpaste shares

54.5 55.9 56.7 57.8

23.8 22.8 21.5 19.9

13.9 13.5 13.4 13.4

2012 2013 2014 YTD 2015

Competitor 1

Competitor 2

Source: AC Nielsen Retail Audit YTD April 2015; Volume Shares

Toothbrush shares

39.8 41.6 42.4 42.1

18.8 18.4 18.3 18.3

6.7 7.4 7.9 8.8

2012 2013 2014 YTD 2015

Source: AC Nielsen Retail Audit YTD April 2015; Volume Shares

Competitor 1

Competitor 2

India’s Most Trusted Brand

# 1 Brand across all sectors

4 Years in a row

Only brand in top 3 since the survey’s inception in 2000

Source: Economic Times Brand Equity Survey 2014

India’s Most Purchased Brand

Source: Kantar Worldpanel Report 2014

And we are

Investing to Grow

Key Growth Drivers

• Innovation

• Engaging with consumers to build

our brands

• Winning on the Ground

• Strong professional partnerships

Innovating to create new segments

Whitening

Whiter + Shinier Teeth in 1 week

Innovating to create new segments

Sensitivity

Repairs Enamel for Lasting Sensitivity Relief

Innovating to create new segments

Premium Anti-Cavity

Fights Sugar Acids, the #1 cause of Cavities

Innovating to create new segments

Deep & Gentle Cleaning, with

Charcoal Infused Bristles

A Nielsen Survey

Innovating to create new segments

Deep Cleaning Between Teeth

First mass ‘black’ toothbrush

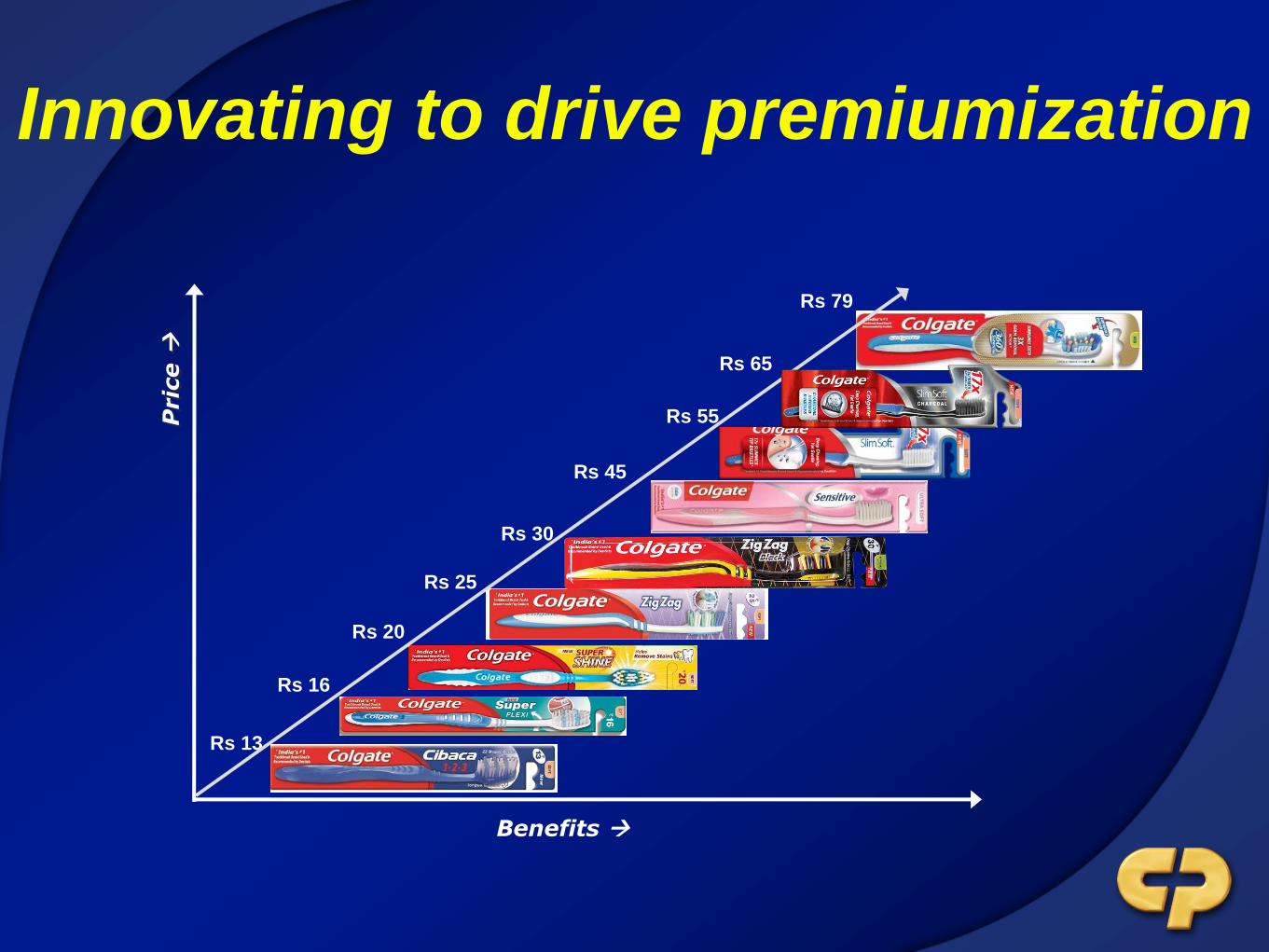

Innovating to drive premiumization P

ric

e

Rs.5

15g

Rs.10

35g

Rs.17

50g

Rs.20

50g

Rs.46

100g

Rs.60

70g

Rs.85

100g

Rs.95

70g

Benefits

Innovating to drive premiumization

Rs 13

Rs 16

Rs 20

Rs 25

Rs 30

Rs 45

Rs 65

Rs 79

Pric

e

Benefits

Rs 55

Key Growth Drivers

• Innovation

• Engaging with consumers to build

our brands

• Winning on the Ground

• Strong professional partnerships

Engaging with consumers on

digital

Over 3.1 MM fans on India Facebook pages

Engaging with consumers on

digital

Main page of leading portals turned black for the ‘first time ever’

Reached 23 million consumers

Product launch of SlimSoft Charcoal on digital platform

Engaging with consumers on

Mobile

Colgate Scholarship Offer

Over 1.5 Million call-ins

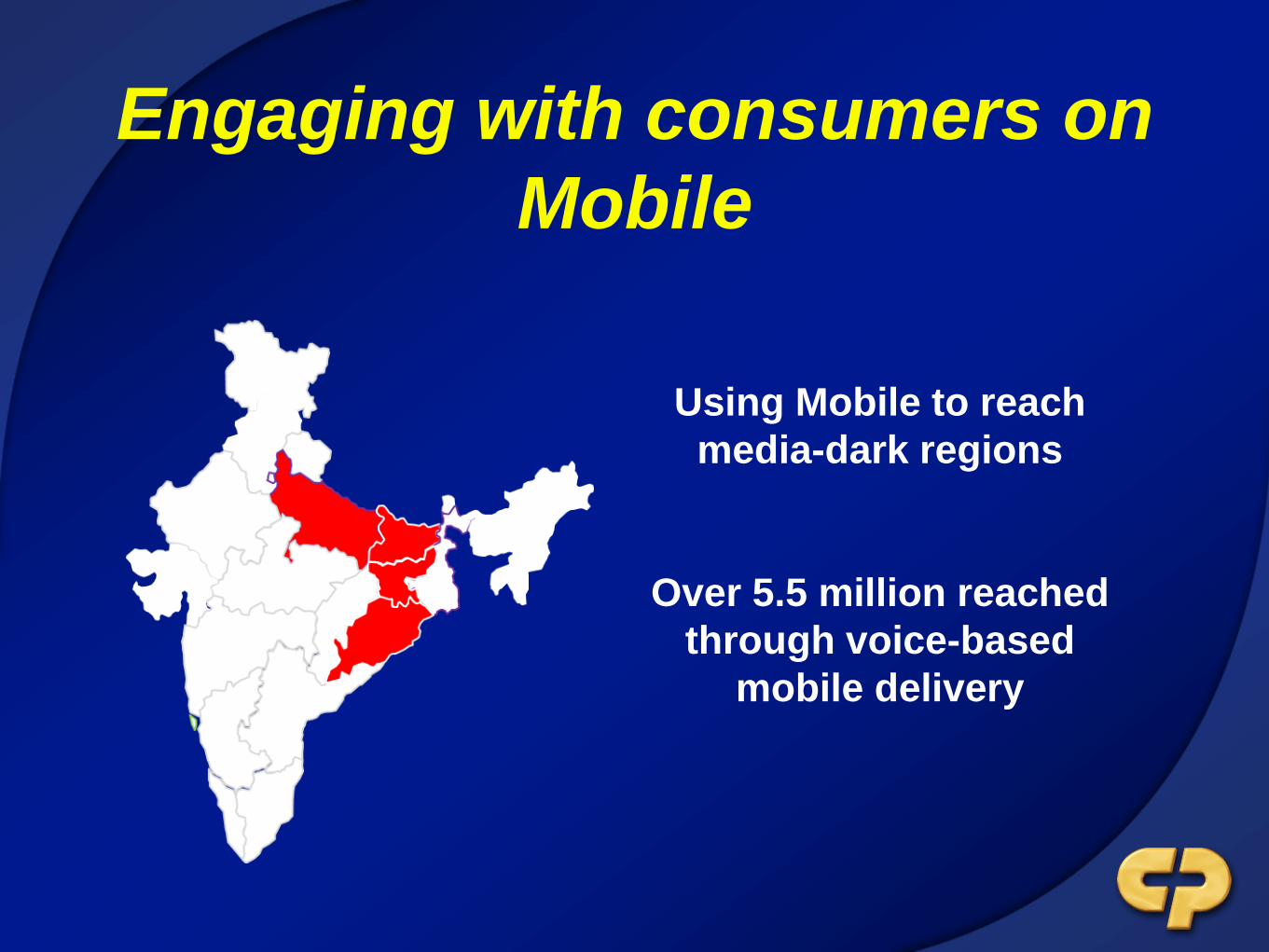

Engaging with consumers on

Mobile

Using Mobile to reach

media-dark regions

Over 5.5 million reached

through voice-based

mobile delivery

Key Growth Drivers

• Innovation

• Engaging with consumers to build

our brands

• Winning on the Ground

• Strong professional partnerships

Increasing distribution &

availability

Colgate available in 4.8MM outlets

Increasing distribution &

availability

Invested behind infrastructure

340

801 951

2012 2013 2014

No. of rural vans

Servicing the Growth

Toothpaste facility at Sanand, Gujarat.

Commissioned from March 2014

Servicing the Growth

Toothbrush facility at Sricity, Andhra Pradesh.

Commissioned from March 2015

Superior In-Store Execution

Making our brands…

• Available

• Visible

• Irresistable

Superior In-Store Execution

Partnering modern retailer customers on

planogramming & shopability

Superior In-Store Execution

Impactful In-store visibility for new launches

Superior In-Store Execution

Impactful In-store visibility for new IMCs

Superior In-Store Execution

Customised hanger packs for traditional trade

Superior In-Store Execution

Customised solutions for traditional trade

Superior In-Store Execution

Key Growth Drivers

• Innovation

• Engaging with consumers to build

our brands

• Winning on the Ground

• Strong professional partnerships

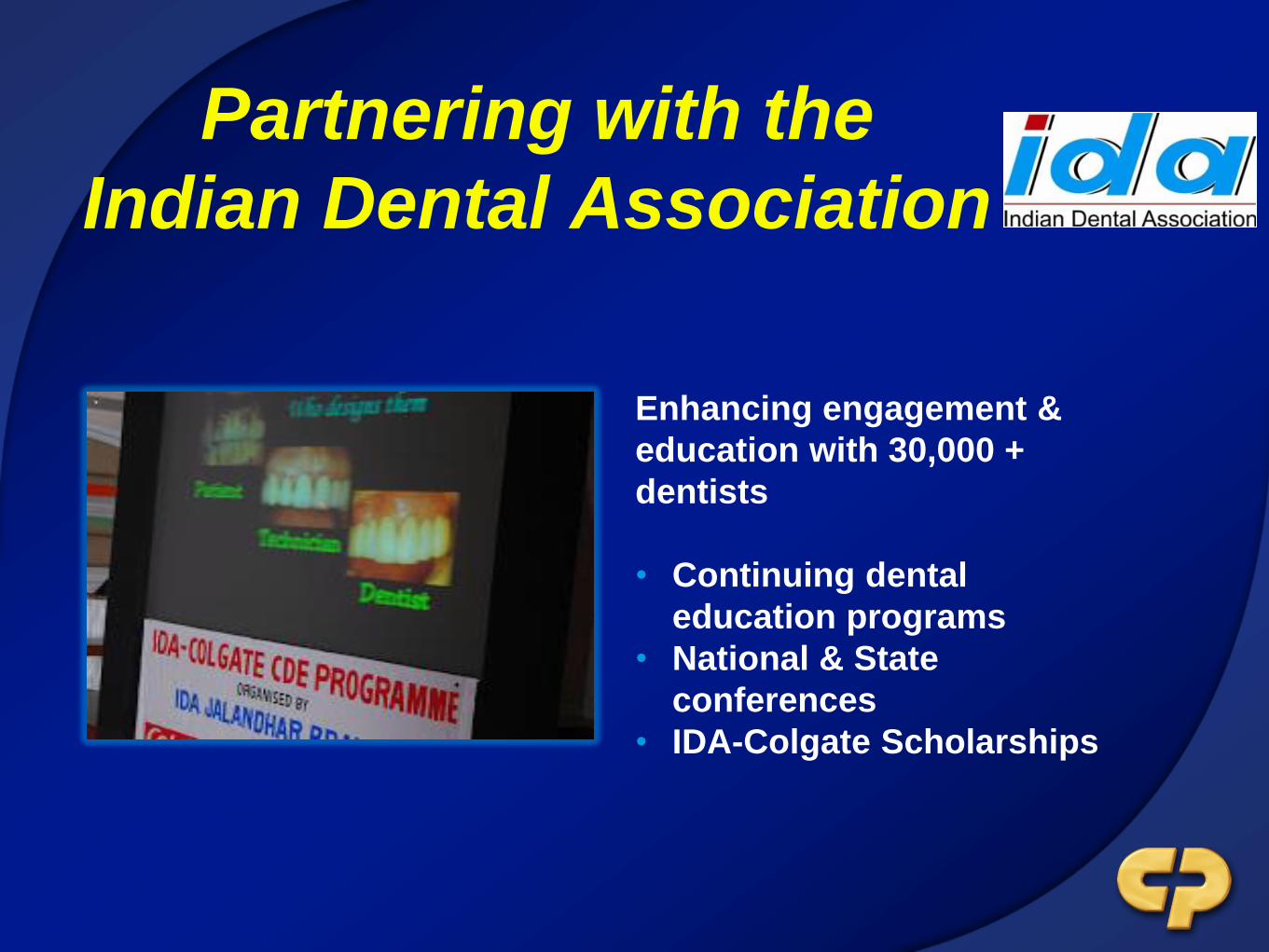

Partnering with the

Indian Dental Association

Enhancing engagement &

education with 30,000 +

dentists

• Continuing dental

education programs

• National & State

conferences

• IDA-Colgate Scholarships

Alliance for a Cavity-Free Future

Creating an external voice to raise awareness

on dental caries

Academicians + Dentists + Pediatrician + NGO Partners

Leading with the Profession on

recommendations & usage

CP Competitior 1 Competitior 2 Competitior 3

65

7 4 3

CP Competitior 1 Competitior 2 Competitior 3

74

3 6 4

Brand Recommended Most Often by Dentists

Brand Used Most Often by Dentists

Source: Ipsos Dentist Track Dec 2014

Key Growth Drivers

• Innovation

• Engaging with consumers to build

our brands

• Winning on the Ground

• Strong professional partnerships

Huge Headroom for Growth

Penetration

250MM

consumers do not

use Toothpaste 91.2 92.3

2013 2014

72.8 74.1

2013 2014

Urban

Source: Indian Readership Survey (HHs), IMRB**

Rural

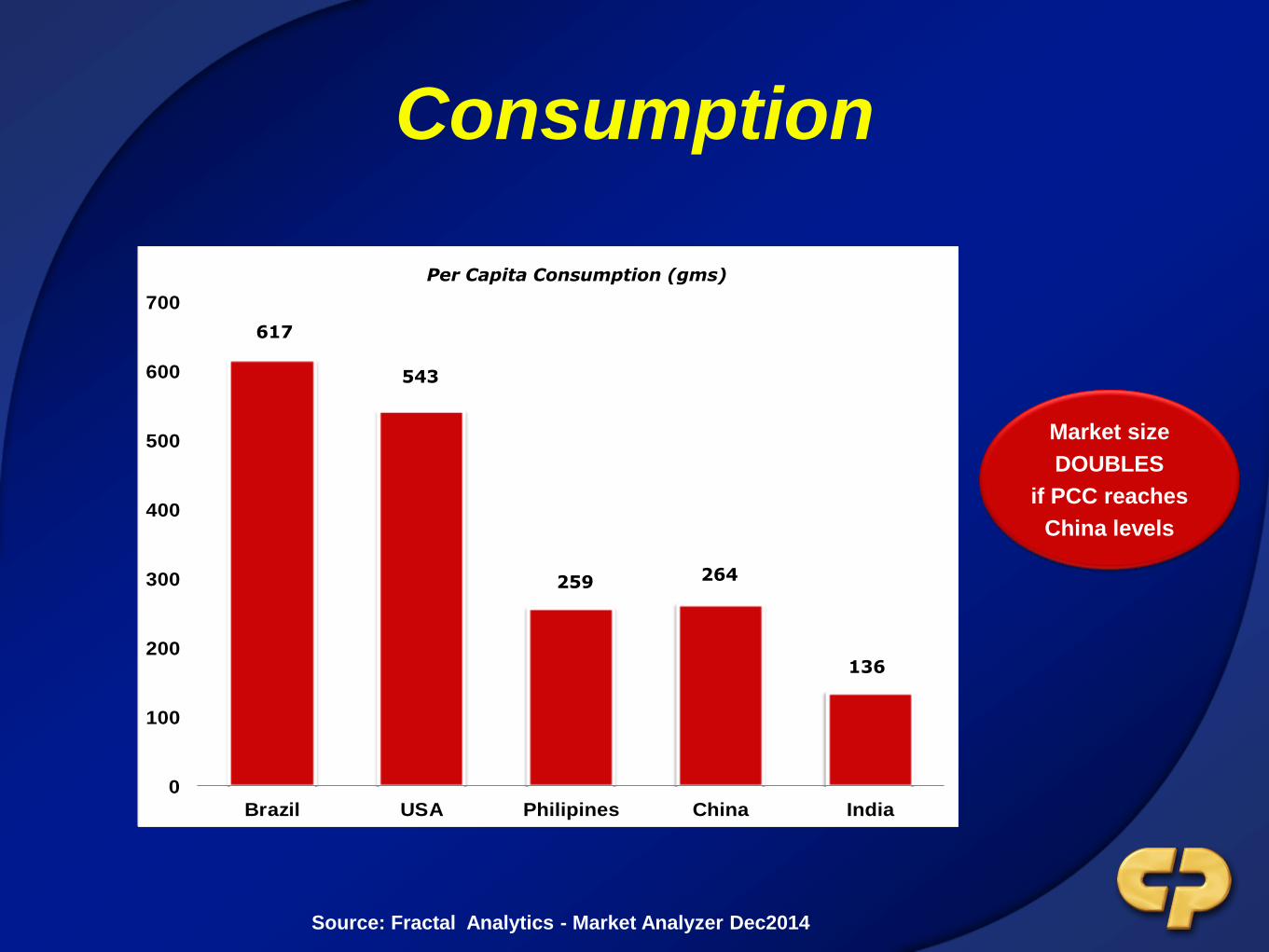

Consumption

0

100

200

300

400

500

600

700

Brazil USA Philipines China India

Chart Title

Market size

DOUBLES

if PCC reaches

China levels

Per Capita Consumption (gms)

617

543

259 264

136

Source: Fractal Analytics - Market Analyzer Dec2014

Premiumization

Average Selling

Price($) Per KG of

Toothpaste

18

13

11 6

3X 2.2X 1.8X X

Average Selling

Price($)

Per Toothbrush

2.7 1.7 0.6 0.2

13.5X 8.5X 3X X

Source: Fractal Analytics - Market Analyzer Dec2014

Market size

DOUBLES

if ASP reaches

China levels

Leading to Win Working with our Community

Bright Smiles, Bright Futures

Over 125 million school children

contacted in the program

Oral Health Month

In association with IDA, over 5.5 Million

free dental check-ups done in 2014

Working with NGO Partners

Conservation of Natural Resources,

Vocational training for self sustenance

of villagers, Girl child empowerment.

Addressing Inequalities- Payroll

giving program to sponsor

children affected and infected by

HIV.

Providing quality education to

underprivileged of children ;

Program ‘Read India’- improve basic

reading, writing and arithmetic skills

In closing,

a summary of our long term

performance

Net Sales

Gross Margin

PAT

EPS

DPS

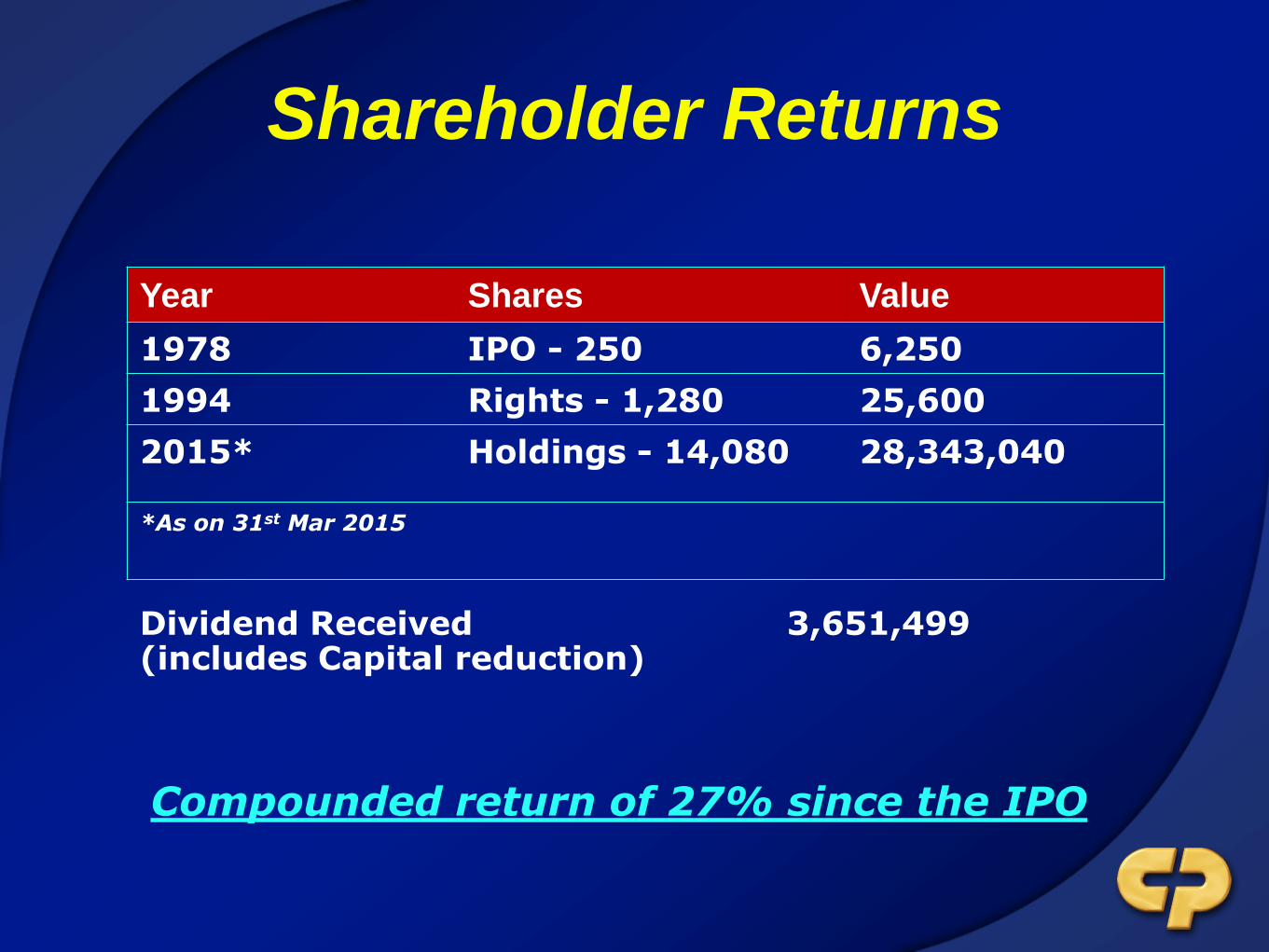

Shareholder Returns

Year Shares Value

1978 IPO - 250 6,250

1994 Rights - 1,280 25,600

2015* Holdings - 14,080 28,343,040

*As on 31st Mar 2015

Dividend Received 3,651,499 (includes Capital reduction)

Compounded return of 27% since the IPO

Well-poised to continue to grow

shareholder value

Lets Talk

![colgate palmolive (india) - WordPress.com · [COLGATE PALMOLIVE (INDIA)] Colgate is a large global dental hygiene brand. Colgate is an equally strong brand in India and enjoys almost](https://img.dokumen.tips/doc/110x75/5e1519190e008e148238feef/colgate-palmolive-india-colgate-palmolive-india-colgate-is-a-large-global.jpg)