Embed Size (px)

Citation preview

A WHITE PAPER PRODUCED BY FINEXTRA IN ASSOCIATION WITH VOLANTE TECHNOLOGIESOCTOBER 2018

CLEARING AND SETTLEMENT: THE NEW BATTLEGROUND FOR PAYMENTS INNOVATIONHow financial institutions can tackle complexity in an ever-evolving payments ecosystem

01 Introduction .......................................................... 3

02 New frontiers in payments initiation ........................ 4 03 Clearing and settlement complexity on the rise ......... 6

04 The question for banks ........................................... 7

05 Cross-border payments and SWIFT gpi… .................. 8

06 Distributed ledger technology: The banks hedge their bets… .................................10

07 Cryptocurrencies: Next generation innovation… .......13

08 ECB’s TIPS: Another alternative solution .................14

09 The US Context: domestic and cross-border ............16

10 Mastering complexity: Preparing for the diverse ecosystem… ........................................................18

11 About ..................................................................207 What should financial institutions be doing about blockchain right now? 25

| CLEARING AND SETTLEMENT: THE NEW

BATTLEGROUND FOR PAYMENTS INNOVATION

03

01INTRODUCTION

There is significant innovation and competition afoot in the world of payments initiation, driven by consumers and corporates on the demand side, and traditional banks, fintechs and challengers on the supply side.

This is mirrored by what can reasonably be called a revolution in the world of clearing and settlement. Real-time / instant payments, blockchain and distributed ledger, new solutions to the old problems of cross-border correspondent banking, and many other initiatives all have the potential to transform how payments are processed, cleared and settled.

Financial institutions therefore need to find ways to provide compelling business services based on new methods of payment initiation and novel customer experiences, while keeping pace with the multiplicity of back end clearing and settlement options – all while managing costs, staying ahead of compliance, and growing market share.

“ Banks also must accommodate competition and innovation in the clearing and settlement space, both domestic and cross-border. Here, too, change is coming thick and fast, with new entrants wading in and incumbents fighting back.”

| CLEARING AND SETTLEMENT: THE NEW

BATTLEGROUND FOR PAYMENTS INNOVATION

04

02NEW FRONTIERS IN PAYMENTS INITIATION

Competition – and innovation – in the payments initiation space are well-established trends. New regulations to encourage open banking, notably the revised European Payment Services Directive (PSD2), amendments to Japan’s Banking Act, and Australia’s Open Banking Review, as well as the US Federal Reserve’s recent focus on payments modernisation in the US, have an explicit goal of increasing innovation and competition in payments initiation. The fintech industry has also targeted much of its inventiveness at revolutionising how people – and increasingly businesses – make payments.

Innovations in the peer-to-peer payments arena, driven initially by new entrants, have forced incumbent providers to up their game, as we have seen with the launch of Zelle by a group of major US banks, in an attempt to offer a better alternative to fintech options such as Venmo or Square Cash. The rise of real-time, or instant, payments systems in many markets worldwide, supported by market infrastructures, can also be seen as a response by the financial industry to regulatory demand for, and fintech-driven, innovation in payments.

Underpinning all of this innovation has been the growing ubiquity of mobile payments, ever more widely adopted by a demanding, tech-savvy generation of consumers. And where consumer payments have led the way, corporate payments are following.

For financial institutions, though, keeping up with – and ahead of – how people and businesses make payments is only one part of the challenge. Banks also must accommodate competition and innovation in the clearing and settlement space, both domestic and cross-border. Here, too, change is coming thick and fast, with new entrants wading in and incumbents fighting back.

| CLEARING AND SETTLEMENT: THE NEW

BATTLEGROUND FOR PAYMENTS INNOVATION

05

It is tempting to examine drivers of innovation and disruption in clearing and settlement—the move to real-time, regulatory pressure, customer demand, new cross-border initiatives, open banking—in isolation. However, these trends are deeply interconnected. Like any other ecosystem, the payments ecosystem is best approached holistically. The Australian government, in its Open Banking foreword, said, “Open Banking should encourage competition. It should be done to increase competition for the banking products and services available to customers so that customers can make better choices.”

INNOVATION AND DISRUPTION IN CLEARING AND SETTLEMENT

Europe’s PSD2

Amendments to Japan’s Banking Act

Australia’s Open Banking Review Fast, digital services

The Clearing House’s RTP(Real Time Payments)

Australia’s New Payments Platform

India’s Immediate Payment Service

China’s IBPS (Internet Banking Payment System)

innovation and disruption in the payments initiationspace driven by regulation and consumer demand

Innovation anddisruption

“ RTP is designed to support not only the transfer of funds but also the ability to both request payments and provide critical information about a payment to efficiently deal with back office reconciliation issues.” – THE CLEARING HOUSE

“ To build the foundation for a full range of mobile based Banking services..” – NATIONAL PAYMENTS COUNCIL OF INDIA, OBJECTIVES OF INDIA IMMEDIATE PAYMENT SERVICE

| CLEARING AND SETTLEMENT: THE NEW

BATTLEGROUND FOR PAYMENTS INNOVATION

06

03CLEARING AND SETTLEMENT COMPLEXITY ON THE RISE

The backers of each initiative might believe theirs will become the global standard but, in all likelihood, more than one will prevail. And in this environment of rapid technological development, we will almost certainly see a further acceleration in innovation, with more new initiatives gaining ground, before any consolidation occurs.

Complexity in clearing and settlement is not a new phenomenon. But it is widely tipped to be a bigger trend in the coming years – with good reason, given the number of initiatives vying for attention. The list already includes SWIFT gpi, Ripple, MasterCard and distributed ledger-based solutions based on R3 Corda, Hyperledger, and Ethereum (to name just a few) and the European Central Bank’s Target Instant Payments Settlement (TIPS).

Layer these over domestic instant payment systems from national clearing houses, consider the variety of infrastructures and solutions in play across the globe, and think about innovations on the near horizon, such as central bank-backed cryptocurrencies. It’s clear that when it comes to payments clearing and settlement going forward, banks will be operating in a world of multiple options – including DLT-based infrastructures, ISO 20022-based standards, and proprietary data formats. PSD2 / Open Banking will also force innovations in bilateral / multilateral clearing and settlement requirements.

CLEARING AND SETTLEMENT INITIATIVES

DISTRIBUTED LEDGER TECHNOLOGYCLEARING AND SETTLEMENT INITIATIVES

R3 CordaHyperledger

Ethereum

TARGET INSTANT PAYMENTS SETTLEMENT

TIPSITS AIM IS TO ELIMINATE CREDIT RISK ACROSS A LARGE NUMBER OF PARTICIPANTS

LIVE NOVEMBER 2018

24/7/365

TIPS (Target Instant Payments Settlement- European Central Bank)Ripple

Mastercard

SWIFT gpi

| CLEARING AND SETTLEMENT: THE NEW

BATTLEGROUND FOR PAYMENTS INNOVATION

07

04THE QUESTION FOR BANKS

The question for banks will be how they can most efficiently and effectively operate in a world which requires them to connect to multiple clearing and settlement mechanisms while managing a plethora of new initiation channels and models. Where can they focus their limited innovation and R&D budgets?

While the initiation space is certainly strongly connected to something that banks care about deeply – the customer experience – the reality is that banks are increasingly losing control of the customer experience at the point of initiation. With PSD2 essentially allowing any third party to create their own initiation experiences, it is almost inevitable that banks will need to focus more on their ability to clear and settle rapidly and efficiently, across as many national boundaries as possible.

But this begs several questions. Will they have to participate in all the new solutions, or will they be able to restrict themselves to a few options? Will banks need to actively market different options directly to their clients, or will they be able to route payments in the background without user input? How much visibility will their customers seek over the options available to them – and how much accountability will the banks have when it comes to delivering least cost or fastest routing for payments (a comparable challenge is faced in the capital markets with the best execution obligations of MiFID II). How interoperable will the different options be, and what technology demands will connecting to them place on banks’ existing payments infrastructures?

In short, how can banks ensure that they, and their customers, avoid being swamped by diversity, and instead benefit from innovation and competition in payments clearing and settlement – mastering the complexity, and reaping gains in terms of efficiency, effectiveness, reach and cost?

Examining some of the trends in clearing and settlement in a little more detail helps in the attempt to address these questions.

| CLEARING AND SETTLEMENT: THE NEW

BATTLEGROUND FOR PAYMENTS INNOVATION

08

05CROSS-BORDER PAYMENTS AND SWIFT GPI

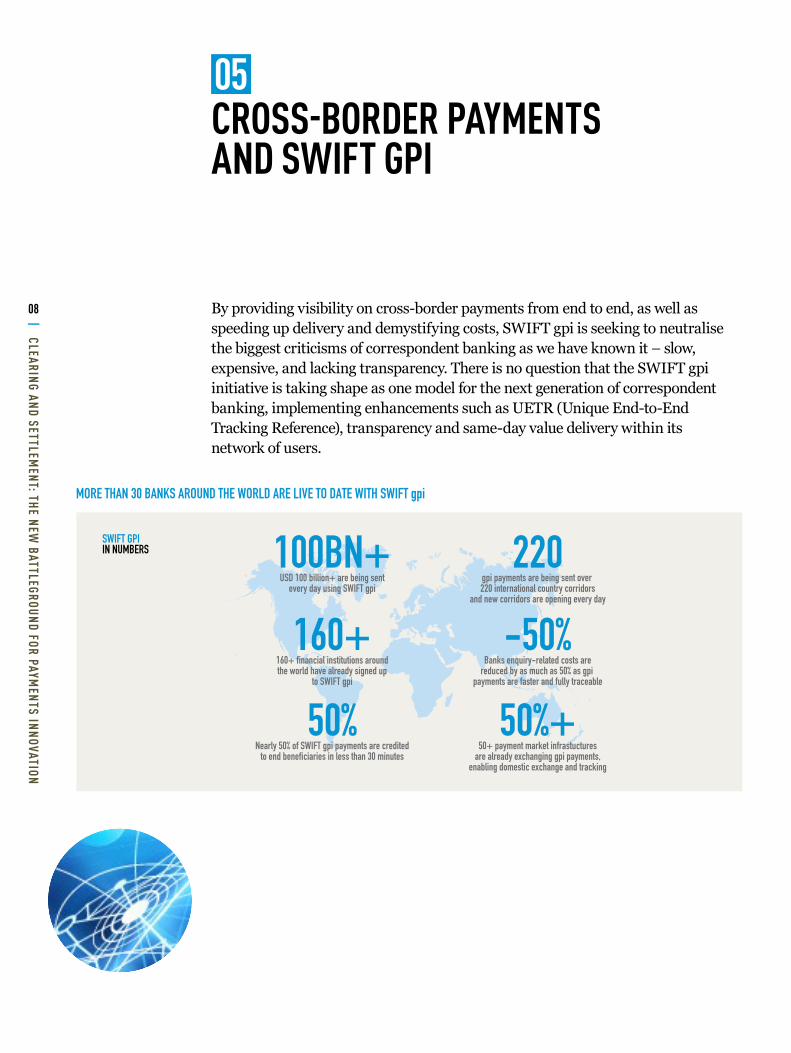

By providing visibility on cross-border payments from end to end, as well as speeding up delivery and demystifying costs, SWIFT gpi is seeking to neutralise the biggest criticisms of correspondent banking as we have known it – slow, expensive, and lacking transparency. There is no question that the SWIFT gpi initiative is taking shape as one model for the next generation of correspondent banking, implementing enhancements such as UETR (Unique End-to-End Tracking Reference), transparency and same-day value delivery within its network of users.

MORE THAN 30 BANKS AROUND THE WORLD ARE LIVE TO DATE WITH SWIFT gpi

100BN+USD 100 billion+ are being sent

every day using SWIFT gpi

SWIFT GPIIN NUMBERS 220

gpi payments are being sent over 220 international country corridors

and new corridors are opening every day

160+160+ financial institutions aroundthe world have already signed up

to SWIFT gpi

-50%Banks enquiry-related costs are

reduced by as much as 50% as gpi payments are faster and fully traceable

50%Nearly 50% of SWIFT gpi payments are credited

to end beneficiaries in less than 30 minutes

50%+50+ payment market infrastuctures

are already exchanging gpi payments,enabling domestic exchange and tracking

| CLEARING AND SETTLEMENT: THE NEW

BATTLEGROUND FOR PAYMENTS INNOVATION

09

All that said, SWIFT gpi is an evolution, rather than a revolution. A number of commentators have observed that a more radical solution will be required to enable more competition and to secure the incumbent role of banks in the future of cross-border payments.

Some have suggested that a hybrid model comprising SWIFT gpi alongside more disruptive technology-based solutions – using distributed ledger (or blockchain as it is also known) – could be the answer. SWIFT has setup a sandbox to explore DLT, and although their initial pilot has gone well there are no next concrete steps at this time.

It is clear, therefore, that while it is making an important and much valued contribution to improving the efficiency and effectiveness off cross-border payments clearing and settlement, SWIFT gpi will not be the only game in town – for example China and Russia are already exploring alternative cross-border payments options.

“ Diversity means potential complexity, and this complexity must be managed by financial institutions in their payments processing strategies and infrastructures.”

| CLEARING AND SETTLEMENT: THE NEW

BATTLEGROUND FOR PAYMENTS INNOVATION

10

06DISTRIBUTED LEDGER TECHNOLOGY: THE BANKS HEDGE THEIR BETS

Distributed ledger-based solutions for payments are likely to feature strongly in the future. Indeed, in its ‘Top Trends in Payments 2018’ report, Capgemini’s sixth predicted trend is that banks and fintechs will “explore distributed ledger technology to transform cross-border payments”. This seems a safe bet for the coming years considering the wealth of activity that has already taken place in this area.

Many banks and regional associations are creating and exploring digital currencies and solutions based on R3’s Corda platform and DLT. Of particular interest on the central bank front is the Monetary Authority of Singapore’s Project Ubin, which is actively exploring the possibility of transacting Singapore Dollar (SGD) as a digital currency on a blockchain.

CROSS-BORDER PAYMENTS PLATFORM

UTILITY SETTLEMENT COIN PROJECT

R3 AND 22 MEMBER BANKS COLLABORATED ON A CROSS-BORDER PAYMENTS PLATFORM BUILT ON CORDA, TO ENABLE FIAT AND DIGITAL CURRENCIES TO BE TRANSACTED ON BLOCKCHAIN TECHNOLOGY,

ELIMINATING DELAYS AND COSTS OF CURRENT CROSS-BORDER PAYMENTS INFRASTRUCTURES,

AIM IS TO PROVIDEA REGULATED DIGITAL CASH

WITH THE BENEFITS OFCRYPTOCURRENCIES.

UBS GROUP INITIATIVETO CREATE A DIGITAL SYSTEM

TO SETTLE FINANCIAL TRANSACTIONSOVER BLOCKCHAIN,

R3MEMBER BANKS22MEMBER BANKS

MAJOR GLOBALBANKS

17

| CLEARING AND SETTLEMENT: THE NEW

BATTLEGROUND FOR PAYMENTS INNOVATION

11

In October 2017, blockchain consortium R3 and 22 of its member banks announced they had collaborated on the development of a cross-border payments platform built using R3’s Corda distributed ledger technology. The platform will enable both existing central bank currencies and any digital currencies developed in the future to be transacted via the blockchain, said R3. Backed by banks including Barclays, BBVA, CIBC, Commerzbank, DNB, HSBC, Intesa, KBC, KB Kookmin Bank, KEB Hana Bank, Natixis, Shinhan Bank, TD Bank, U.S. Bank and Woori Bank, the R3 solution has been positioned as a direct alternative to current cross-border payments infrastructures – promising to facilitate instant international payments, and to eliminate the delays and costs characterising existing mechanisms. Two months earlier, in August 2017, Credit Suisse Group and Barclays announced they were joining a UBS Group’s initiative to create a new type of digital money to settle financial transactions over blockchain. Banco Santander, Bank of New York Mellon, Canadian Imperial Bank of Commerce, Deutsche Bank, HSBC, Mitsubishi UFJ Financial Group, NEX Group and State Street Corp are also taking part in the Utility Settlement Coin project. The project aims to provide a regulated and near-term digital cash that provides the digital benefits of cryptocurrencies.

It is therefore clear how momentum is building around the development of DLT-based solutions; digitisation is pervasive in financial services and there is no sign of it slowing down, be it in the form of currency exchange, information exchange or clearing and settlement mechanisms. Major global players are either collaborating to explore DLT or going solo – add to this the gravitas that central banks and institutions bring to the narrative and it is obvious that DLT plays a large part in digital transformation. The nascence of this technology, however, makes it ever-more pressing for banks to accommodate the disintermediation in payments initiation, because it will increase before it narrows.

| CLEARING AND SETTLEMENT: THE NEW

BATTLEGROUND FOR PAYMENTS INNOVATION

12

Most prominent of all is Ripple. While Ripple’s cryptocurrency XRP displayed similar volatility to that of bitcoin during the early weeks of 2018, its distributed ledger network for the exchange of cross-border payments continues to go from strength to strength. In May 2018, Ripple announced successful results from a liquidity management pilot testing payments from the US to Mexico. Its network of banks using its cross-border payments solution now totals 75 banks. In April, it announced having signed ten more banks to RippleNet, its protocol for fast settlement of international payments. Ripple Labs has signed more than 100 banks to date.

Capgemini agrees with SWIFT that before the industry experiences widespread adoption of distributed leger technology, challenges related to scalability and lack of standardisation must be addressed. However, Capgemini also predicts a role for distributed ledger in remittances, cross-border B2B payments and cross-border interbank settlements. Given the amount of energy, time and resource being put by global banks into multiple distributed ledger experiments and solutions in the payments space, this conclusion seems inescapable.

But there won’t be one single blockchain solution for payments, and neither, it seems, will many banks back only one blockchain horse. Note the repeated bank names associated with the distributed ledger initiatives outlined above. This means that while it will deliver value, blockchain will also contribute to the increasing diversity and multiplicity of options within the cross-border payment clearing and settlement landscape.

Diversity means potential complexity, and this complexity must be managed by financial institutions in their payments processing strategies and infrastructures.

CROSS-BORDER PAYMENTS PLATFORM

UTILITY SETTLEMENT COIN PROJECT

R3 AND 22 MEMBER BANKS COLLABORATED ON A CROSS-BORDER PAYMENTS PLATFORM BUILT ON CORDA, TO ENABLE FIAT AND DIGITAL CURRENCIES TO BE TRANSACTED ON BLOCKCHAIN TECHNOLOGY,

ELIMINATING DELAYS AND COSTS OF CURRENT CROSS-BORDER PAYMENTS INFRASTRUCTURES,

AIM IS TO PROVIDEA REGULATED DIGITAL CASH

WITH THE BENEFITS OFCRYPTOCURRENCIES.

UBS GROUP INITIATIVETO CREATE A DIGITAL SYSTEM

TO SETTLE FINANCIAL TRANSACTIONSOVER BLOCKCHAIN,

R3MEMBER BANKS22MEMBER BANKS

MAJOR GLOBALBANKS

17

| CLEARING AND SETTLEMENT: THE NEW

BATTLEGROUND FOR PAYMENTS INNOVATION

13

07CRYPTOCURRENCIES: NEXT GENERATION INNOVATION

What will happen to the value of bitcoin is anyone’s guess, and whether, as some pundits have predicted, central banks will invest in a major way in existing cryptocurrencies also remains to be seen. But we do know that a number of governments – including those in the US, China, Japan, Canada, Russia, Estonia and Sweden among others – are either actively developing or thinking about developing some form of digital currency.

Few, if any, of these currencies, should they actually emerge, are likely to look much like bitcoin. In one key aspect in particular they will probably be crucially different: they will be centralised, rather than decentralised. Centralisation brings its own downsides of course but is clearly more consistent with a ‘central’ bank outlook.

The upsides of such digital currencies would include the potential for instant global electronic transactions, reduced counterfeiting and easier monitoring of transactions. Purists might say such currencies are by definition not cryptocurrencies: others would argue the mechanism is irrelevant, and the important attribute is digital money that is a liability with a central bank rather than a private bank, paving the way for a cheaper electronic payment system with fewer middlemen, and giving central banks more power to influence economic growth by working on the digital currency.

If, or perhaps more accurately when, some of these currencies start to become reality, one likely outcome is that they will add yet another dimension and possibly more complexity to the payments clearing and settlement landscape. Certainly, given the level of innovation and ingenuity being applied to payments as a result of rapid technological development, banks can expect no slowdown in the rate of change to the world of cross-border payments in which they must operate.

| CLEARING AND SETTLEMENT: THE NEW

BATTLEGROUND FOR PAYMENTS INNOVATION

14

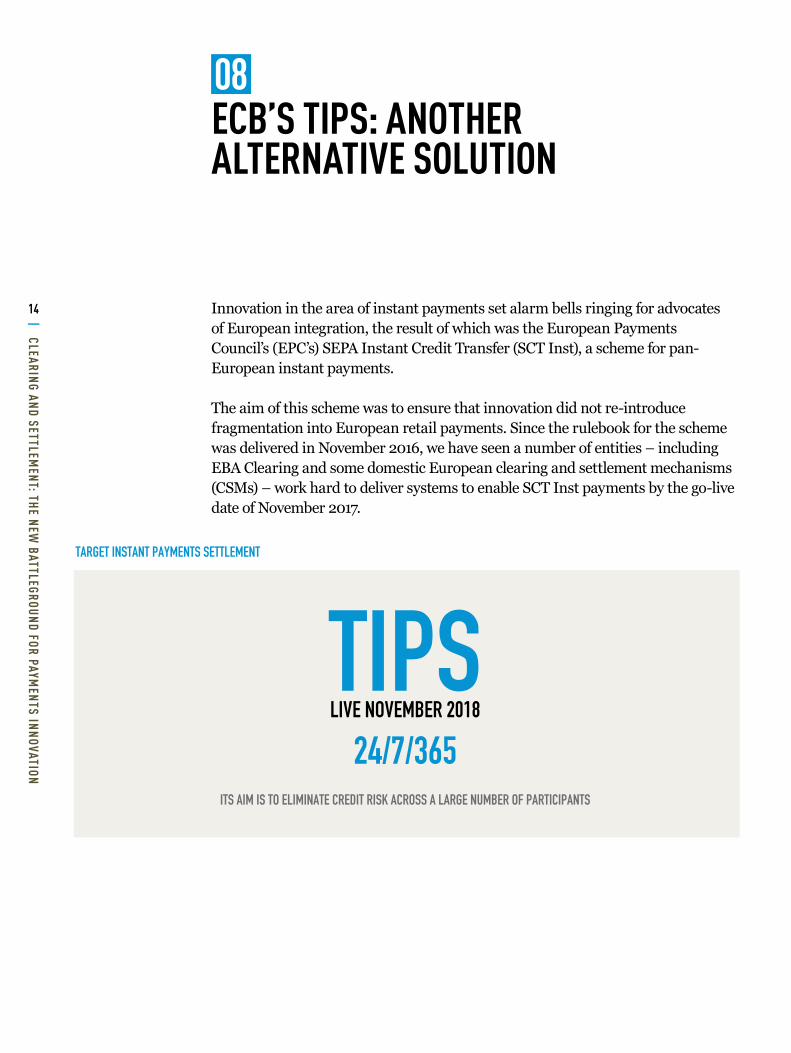

08ECB’S TIPS: ANOTHER ALTERNATIVE SOLUTION

Innovation in the area of instant payments set alarm bells ringing for advocates of European integration, the result of which was the European Payments Council’s (EPC’s) SEPA Instant Credit Transfer (SCT Inst), a scheme for pan-European instant payments.

The aim of this scheme was to ensure that innovation did not re-introduce fragmentation into European retail payments. Since the rulebook for the scheme was delivered in November 2016, we have seen a number of entities – including EBA Clearing and some domestic European clearing and settlement mechanisms (CSMs) – work hard to deliver systems to enable SCT Inst payments by the go-live date of November 2017.

CLEARING AND SETTLEMENT INITIATIVES

DISTRIBUTED LEDGER TECHNOLOGYCLEARING AND SETTLEMENT INITIATIVES

R3 CordaHyperledger

Ethereum

TARGET INSTANT PAYMENTS SETTLEMENT

TIPSITS AIM IS TO ELIMINATE CREDIT RISK ACROSS A LARGE NUMBER OF PARTICIPANTS

LIVE NOVEMBER 2018

24/7/365

TIPS (Target Instant Payments Settlement- European Central Bank)Ripple

Mastercard

SWIFT gpi

| CLEARING AND SETTLEMENT: THE NEW

BATTLEGROUND FOR PAYMENTS INNOVATION

15

Given the development of these systems, the advent of the Eurosystems’ Target Instant Payments Settlement (TIPS), set to go live in November 2018, came as quite a surprise to some. TIPS will offer final and irrevocable settlement for instant payments in central bank money on a 24/7/365 basis. It will allow participating banks to set aside part of their liquidity on a dedicated account opened with their central bank, from which instant payments could be settled around the clock.

According to the Eurosystem, instant settlement will eliminate credit risk for all involved participants and, it says, the broad participation criteria for TIPS will ensure a high level of reachability.

The European Central Bank has positioned TIPS as an essential element of the necessary “safe and efficient underlying market infrastructure that can process instant payments across Europe”. The system will, it says, ensure that demand for instant payments is met at a European level, and will further facilitate integration in the euro area.

Those infrastructures already building settlement mechanisms might well have argued that, contrary to the aim of driving competition and efficiency, TIPS could instead stifle competition by providing a cheap, de facto standard settlement service across the eurozone.

Obviously for banks – or countries – yet to make a decision on their instant payment strategies, TIPS could be a very convenient option. For others, it could be said to be introducing uncertainty by disrupting decisions made and strategies invested in. That notwithstanding, observers have agreed that TIPS will certainly boost reach and ubiquity for euro instant payments settlement.

What is sure is that TIPS will increase the diversity of instant payment settlement systems in Europe – adding a new option to those from EBA Clearing and CSMs such as STET, Equens Worldline and Nets – and mirroring in the retail payments space the growing range of options for processing commercial payments as distributed ledger alternatives to SWIFT gpi continue to emerge.

Elsewhere in the world, instant or real-time payments initiatives are flourishing. Examples include The Clearing House’s Real-Time Payments (RTP) in the US, live in November 2017 with BNY Mellon having initiated the first ever US RTP payment, Australia’s New Payments Platform, India’s Immediate Payment Service, China’s IBPS – the list is extensive. While different in their own way, nearly all are driven by competition authorities that see real-time payments schemes as a way of stimulating competition in the payments arena. Payment services providers increasingly view instant payments as a basis for launching new and innovative products through overlay services.

| CLEARING AND SETTLEMENT: THE NEW

BATTLEGROUND FOR PAYMENTS INNOVATION

16

09THE US CONTEXT: DOMESTIC AND CROSS-BORDER

The big story in US domestic payments over the past twelve months has been the launch and rollout of The Clearing House’s Real-Time Payments (RTP) network. RTP is a major milestone, the first truly new clearing and settlement mechanism in the US in nearly forty years. With 50% of all accounts projected to be RTP-ready by the end of 2018, RTP plans to deliver on the target set by the Federal Reserve’s Faster Payments Task Force, for making “receipt of faster payments available to every U.S. consumer and business by 2020”.

As was the case in Europe, however, and encouraged by the US’s market-based rather than regulation-driven payments ecosystem, RTP is not the only game in town. Consumers and small businesses seeking instant payment services already have a plethora of options in the form of Venmo, Square Cash, and most recently Zelle. PayPal introduced an instant account transfer capability based on debit card rails in June 2017, charging users $0.25 for the privilege, an early test case for market appetite to pay for instant transfer services.

Although strictly speaking TCH can inter-operate with any of the above channels – it could serve as an instant settlement vehicle for them, for example – US banks do need to think carefully about where to make their real-time payments infrastructure investments, based on the most attractive use cases for their customer base and growth plans. It is perfectly possible for a bank to participate in both Zelle and RTP, as long as the go-to-market strategy for each is clearly differentiated.

On the cross-border front, given that by definition such transactions involve at least one party in another country, it is not surprising that many of the innovations making an impact in other jurisdictions – SWIFT gpi, Ripple etc. – are doing so in the US as well. However, the distinctive features of the US market mean that the US will likely end up with a different distribution of winners and losers.

| CLEARING AND SETTLEMENT: THE NEW

BATTLEGROUND FOR PAYMENTS INNOVATION

17

Consider SWIFT – only about a quarter of US institutions are connected to SWIFT, the remainder using larger-bank partners to clear cross-border traffic. This could imply strong headwinds for gpi adoption in the US. Also, unlike their counterparts in Europe and Asia, cross-border payments are of concern to a much smaller percentage of US consumers and businesses. Those that do require high-capacity cross-border services that are primarily focused on the US’s largest trading partners, Canada and Mexico, for which mechanisms like the Federal Reserve’s FedGlobal ACH have been in operation for a while, seamlessly connected into corporate ACH processing workflows.

In sum, the US payments landscape is seeing a heady mix of innovation and competition in both domestic and cross-border payments, and in the whole payment value chain from initiation through to clearing and settlement. Given the US’s status as the world’s largest single national payments market, this represents both a significant business opportunity for challengers, as well as a major threat for established players.

“ If, or perhaps more accurately when, some of these digital currencies start to become reality, one likely outcome is that they will add yet another dimension and possibly more complexity to the payments clearing and settlement landscape.”

| CLEARING AND SETTLEMENT: THE NEW

BATTLEGROUND FOR PAYMENTS INNOVATION

18

10MASTERING COMPLEXITY: PREPARING FOR THE DIVERSE ECOSYSTEM

With customers’ options for payment initiation mushrooming on the one hand and banks’ options for routing, clearing and settling payments ballooning on the other, change really is the only constant for financial institutions’ payments processing infrastructures.

Back to the million-dollar question– How can banks manage this unprecedented level of flux?

While there is no single right or wrong answer (the right answer for one bank may be the wrong answer for another), it is clear that banks need to be prepared, now, for a sea change in the payments landscape. That preparation also needs to be based on a core premise: payments transformation is an imperative, to deliver the business agility and customer experience differentiation required to run a modern payments business.

Once committed to the payments transformation journey, banks then need to plot out the exact shape of the route and the territory it will traverse. While it is obvious that merely refreshing legacy silos does not constitute payments transformation, the often-recommended approach of combining silos into a single monolithic hub, which centralises risk as well as processing flows, has also frequently failed to deliver results. A new paradigm is needed.

“ The new paradigm must ensure that banks retain that flexibility and agility as regulations, formats, standards, APIs, business requirements and technologies continue to evolve over time. The diversity of options available will grow before it converges.”

| CLEARING AND SETTLEMENT: THE NEW

BATTLEGROUND FOR PAYMENTS INNOVATION

19

That new paradigm must look at the bank holistically, understanding that payments will originate from both bank-owned as well as third party API-driven channels, carry rich data payloads, require differentiated processing in the middle office, and then distribution to an increasingly diverse set of clearing and settlement mechanisms. It must ensure that transformation can be achieved in quick sprints, with well-defined business goals, rather than marathon projects based on technical objectives. It must simplify the process of onboarding customers on the front end and incorporating new clearing and settlement options on the back end, by reducing the heavy integration burden imposed by traditional payments renovation programmes.

Finally – and most importantly – it must ensure that banks retain that flexibility and agility as regulations, formats, standards, APIs, business requirements and technologies continue to evolve over time. The diversity of options available will grow before it converges. Banks that are able to address these concerns and get payment transformation right will be ideally positioned to weather the storm of change in both payment initiation and clearing and settlement, and position themselves as natural innovators against the competition.

CLEARING AND SETTLEMENT

BANK

Mobile

Corporate

Retail

Remittances

Partner Banks

Open Banking APIs

DLT / Blockchain Infrastructures

Clearings

SWIFT Network

Real-time Payments

Open Banking APIs

Partner BanksPre-processing Dist

ributi

on

Processing

| CLEARING AND SETTLEMENT: THE NEW

BATTLEGROUND FOR PAYMENTS INNOVATION

20

11ABOUT

Finextra This report is published by Finextra Research.

Finextra Research is the world’s leading specialist financial technology (fintech) news and information source. Finextra offers over 100,000 fintech news, features and TV content items to visitors to www.finextra.com.

Founded in 1999, Finextra Research covers all aspects of financial technology innovation and operation involving banks, institutions and vendor organisations within the wholesale and retail banking, payments and cards sectors worldwide.

Finextra’s unique global community consists of over 30,000 fintech professionals working inside banks and financial institutions, specialist fintech application and service providers, consulting organisations and mainstream technology providers. The Finextra community actively participate in posting their opinions and comments on the evolution of fintech. In addition, they contribute information and data to Finextra surveys and reports.

For more information:Visit www.finextra.com, follow @finextra, contact [email protected] or call +44 (0)20 3100 3670

Volante TechnologiesSince 2001, Volante has focused on addressing the challenges in the full payments lifecycle, including; capture, pre-processing, processing and clearing, as well as those in financial message and data integration. We serve over 85 financial institutions and corporate enterprises in more than 35 countries around the world by providing them with the business agility needed to be competitive and thrive in the new digital payments age. We enable our clients to quickly take advantage of new business opportunities as they arise. Volante supports its diverse client base from offices in Jersey City (HQ), London, Dubai, Mexico City, Bogotá, Chennai, Hyderabad and Pune. Volante’s diverse client base means that product evolution and development is driven very effectively through a best practice approach. Volante’s VolPay Suite of payments processing products and its time proven Volante Designer development platform, provide the speed and flexibility needed for project completion in months not years, or weeks not months for smaller projects. This dramatic acceleration is made possible through Volante products’ inherent high degrees of automation, configuration rather than coding, in-built desktop testing and access to a huge maintained and growing library of hundreds of out-of-the-box international and domestic standards plugins, transformations and processor modules. Volante’s VolPay Suite of payment products can be licensed and deployed on premise or on the cloud. Volante also offers the option of VolPay Suite payment processing applications on a subscription basis as ‘Payments as a Service’ on the cloud.

For more information visit: www.volantetech.com

ABOUT

| CLEARING AND SETTLEMENT: THE NEW

BATTLEGROUND FOR PAYMENTS INNOVATION

21

| CLEARING AND SETTLEMENT: THE NEW

BATTLEGROUND FOR PAYMENTS INNOVATION

22

NOTES

Finextra Research Ltd 1 Gresham StreetLondonEC2V 7BXUnited Kingdom

Telephone+44 (0)20 3100 3670

Webwww.finextra.com

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopy, recording or any information storage and retrieval system, without prior permission in writing from the publisher.

© Finextra Research Ltd 2018