Embed Size (px)

Citation preview

COSTA RICACiti Transaction Services Latin America & Mexico

152COSTA RICA

COUNTRY OVERVIEW

BASIC DATACapital City:

Land Area:

Population:

Main Towns:

Climate:

Language:

Measures:

Currency:

Time:

Holidays:

San José

51,100 sq km; three major mountain ranges, central highland plateau andhighland valleys, with lowlands along Pacific and Atlantic coasts

4.4m

Main Towns: Population in ’000 (based on 2000 census) San José (capital) 310 Alajuela 233 Cartago 132 Puntarenas 106 Heredia 104 Limón 90Tropical in lowlands, warm temperate on highland plateau and valleys

Spanish

Metric system

1 colón (C) = 100 céntimos. Average exchange rates in 2011: C506:US$1; C704:€1

Six hours behind GMT

Agriculture Gloria AbrahamCulture Manuel ObregónEconomics & Insitutional Coordination Mayi AntillónEducation Leonardo Garnier RímoloEnvironment & Energy René CastroFinance Fernando HerreroForeign Relations Enrique CastilloForeign Trade Anabel GonzalezHealth Daisy CorralesHousing Irene CamposJustice Hernando FarísLabor & Social Security Sandra PiszkPlanning & Economic Policy Roberto Gallardo Núñez Presidency Carlos BenavidesPublic Security José María TijerinoPublic Works & Transport Francisco JiménezScience & Technology Eugenia Flores VindasTourism Allan Flores MoyaCentral Bank President Rodrigo Bolaños

Source: The Economist Intelligence Unit as of February 2012

Citi Transaction Services Latin America & Mexico

153COSTA RICA

B. POLITICAL STRUCTURE

Official Name Republic of Costa Rica

Form of State Presidential democracy with a Legislative Assembly

The Executive The president is head of state, elected for four years by universal adult suffrage; he or she appoints a cabinet, as well as the heads of public agencies and the Banco Central de Costa Rica (the Central Bank). Laura Chinchilla of the Partido Liberación Nacional (PLN) took office on May 8th 2010. Her team finishes in May 2014.

National Legislature Legislative Assembly, a 57-member single chamber directly elected for a four-year term by universal adult suffrage.

Legal System Supreme Court at the apex of a subordinate court system; magistrates are elected by the Legislative Assembly for an eight-year term.

Elections Laura Chinchilla of the Partido Liberación Nacional (PLN) was elected president for a four-year term in Febryary 2010. Her term began in May 2010. Last mayoral elections: December 2010. Next elections: February 2014 (presidential and Legislative Assembly), February 2016 (mayoral)

Main Political Organizations Government: Partido Liberación Nacional (PLN)Opposition: Partido Acción Ciudadana (PAC); Partido Movimiento Libertario (ML); Partido Unidad Social Cristiana (PUSC); Partido Unión para el Cambio (PUC); Bloque Patriótico Parlamentario (BP); Partido Auténtico Herediano (PAH); Partido Renovación Costarricense (PRC); Partido Unión Nacional (PUN); Partido Accessibilidad Sin Exclusión (PASE); Partido Frente Amplio (FA) President Laura Chinchilla First Vice-President Alfio Piva Mesén Second Vice-President Luis Liberman

COUNTRY OVERVIEW

154COSTA RICA

C. POLITICAL OUTLOOK 2012 – 2016

Costa Rica will remain one of the most politically stable countries in Latin America in 2012-16, helped by its long tradition of democracy (it has had a continuous democratic regime since 1949) and high levels of social stability. Nevertheless, the president, Laura Chinchilla, of the centrist Partido Liberación Nacional (PLN), will find it difficult to push through her political agenda owing to low levels of public approval, as well as an obstructionist legislature, which in 2011 formed an opposition bloc to counter the PLN’s majority. Broadly speaking, Ms Chinchilla will follow through on the liberalization efforts begun by the previous administration, the centerpiece of which has been the ratification of the Dominican Republic-Central America Free-Trade Agreement (DR-CAFTA) with the US in 2009, while maintaining strong social commitments and attempting to stem rising crime. Passage of a crucial tax reform is the main item currently on the agenda. This reform would help to bring down the country’s high fiscal deficit and provide resources for social and security spending in the longer term. Although the reform has been watered down from its original design, there is still controversy over certain key items such as the replacement of the current sales tax by a value-added tax (VAT), and the taxation on free-trade zones (FTZs). The Economist Intelligence Unit’s baseline scenario continues to assume that the plan will pass but now attaches a significant risk of it being shot down by the legislature or the courts. Even if the reform passes, its reduced effectiveness will require further piecemeal tax changes, as well as a commitment towards additional fiscal consolidation.

Despite its often-turbulent relationship with the opposition and the controversy over fiscal reform, the government is still capable of pushing through many of its policy proposals, particularly in areas where broad consensus exists. This will include raising security spending to combat crime, as well as measures to boost both public and private investment. Investment will be focused on modernizing infrastructure and allowing private participation in hitherto protected sectors, such as insurance, telecommunications and eventually, energy. Overall, the stability of political institutions will remain a fundamental asset in the forecast period, but growing political polarization and an adverse legislative environment will have a negative effect on governability over the remainder of Ms Chinchilla’s term. The rise in unemployment and poverty, despite a positive economic performance over the last year, will also step up pressure for a more socially-oriented agenda.

Costa Rica will continue to pursue trade policy initiatives and efforts to attract foreign investment in tourism, manufacturing, services and infrastructure. It will also seek to diversify its export markets, with a particular focus on Asia, where a number of free-trade agreements (FTAs) have been ratified (with China), have been signed (Singapore) or are being negotiated (South Korea). An FTA with Peru was also recently signed, and successful FTA negotiations were held with the EU in May 2010, with an agreement likely to come into force in 2012.

COUNTRY OVERVIEW

Citi Transaction Services Latin America & Mexico

155COSTA RICA

Relations with the US will remain strong, supported by DR-CAFTA and boosted by strong US investment in the high-tech sector. Costa Rica’s relations with its northern neighbor, Nicaragua, were severely strained by a recent territorial dispute but have since returned to normal. However, there will remain some lingering distrust with the Nicaraguan president, Daniel Ortega (recentlyreelected for a third term), who is seen as being the instigator of the conflict.

D. ECONOMIC PERFORMANCE

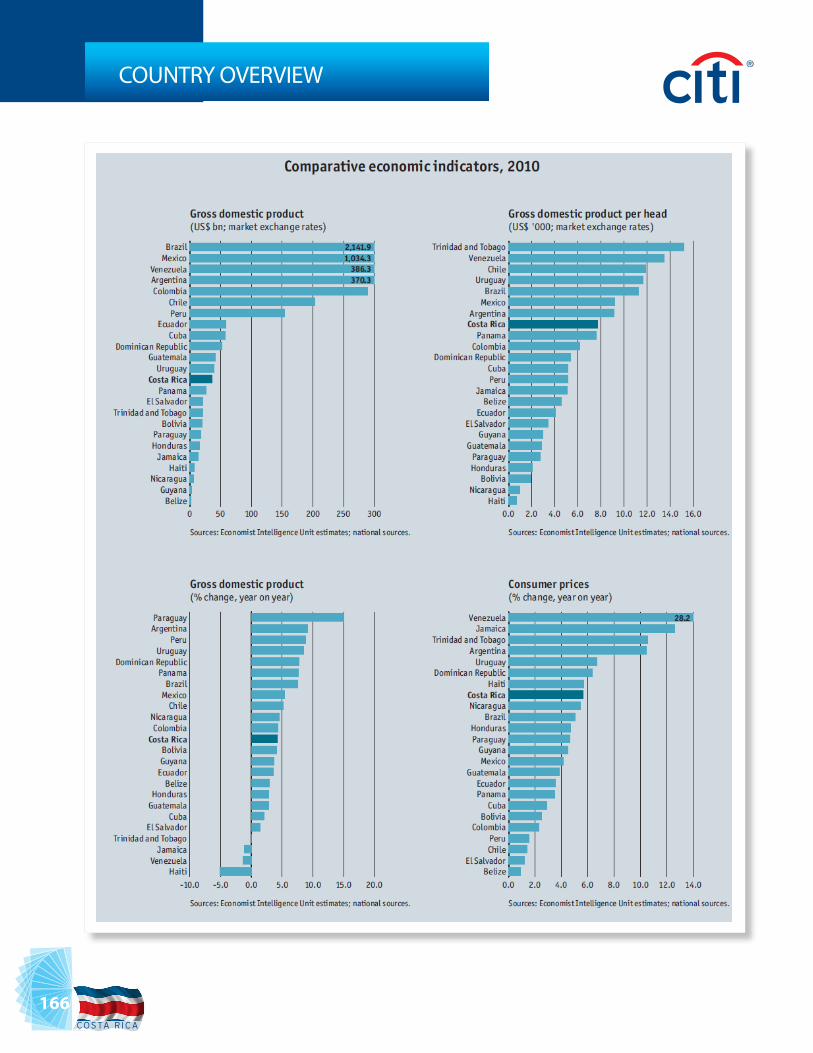

Third quarter GDP results showed that the Costa Rican economy grew at 4.9% year on year during July-September, the highest rate seen so far in 2011. In seasonally adjusted sequential terms, GDP grew by 1.2% compared with the second quarter, thereby maintaining the rhythm seen since January. With average growth of 3.6% in the first nine months, the economy is on course to expand by just over 4% for 2011 as a whole, slightly lower than 2010’s 4.2% expansion and well below the 6% average seen during the pre-crisis boom period of 2003-08. On the demand side, private consumption held up well, growing at 4.2% year on year in July-September, while budgetary constraints implemented to keep the deficit down led to a rise in government consumption of only 1.6%. Gross fixed capital formation expanded at a strong rate of 14.5%, while inventories contributed 1.2 percentage points to GDP growth. On the external side, net trade remained a negative contributor to GDP (1.6%), as exports increased by only 7%, compared with a 10.5% increase in imports.

On the demand side, growth was largely driven by services, which added nearly three-quarters of the year-on-year increase in GDP by factor cost (3% out of 4.7%). In year-on-year terms, the service sector as a whole expanded by 5.6% in the third quarter, led by transport and communications (7.7%) and financial services (5.3%), which compensated for a relatively weak showing for commercial activity, such as retail and wholesale (3.8%). Industry grew by 6% year on year, mostly driven by manufacturing, which at 7.7% had its strongest showing since the first quarter of 2010. Also on the positive side, construction contracted by only 0.1%, the lowest fall since the fourth quarter of 2008, making it likely that the sector’s three-year slump is at an end. Agriculture fared less well, contracting by 0.7%. Although final year figures will not be released until April, monthly economic activity as of November reached an accumulated 4% year on year, with a 6.1% rise in that month alone.

COUNTRY OVERVIEW

156COSTA RICA

COUNTRY OVERVIEW

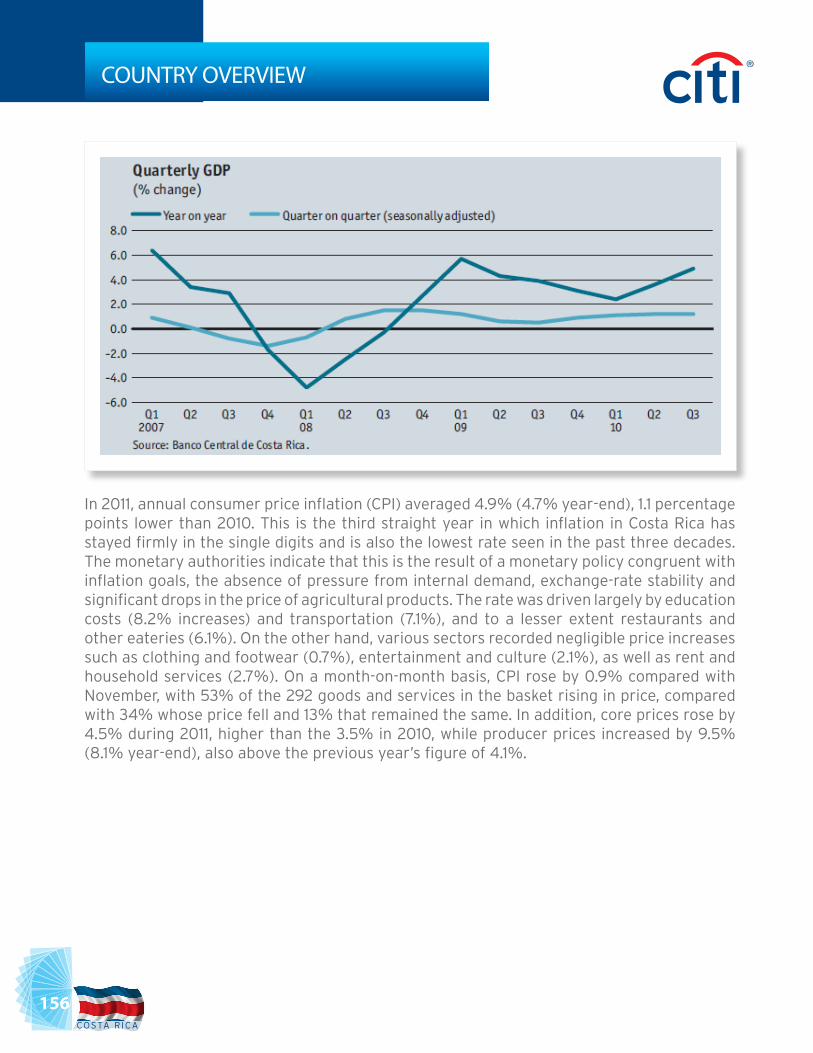

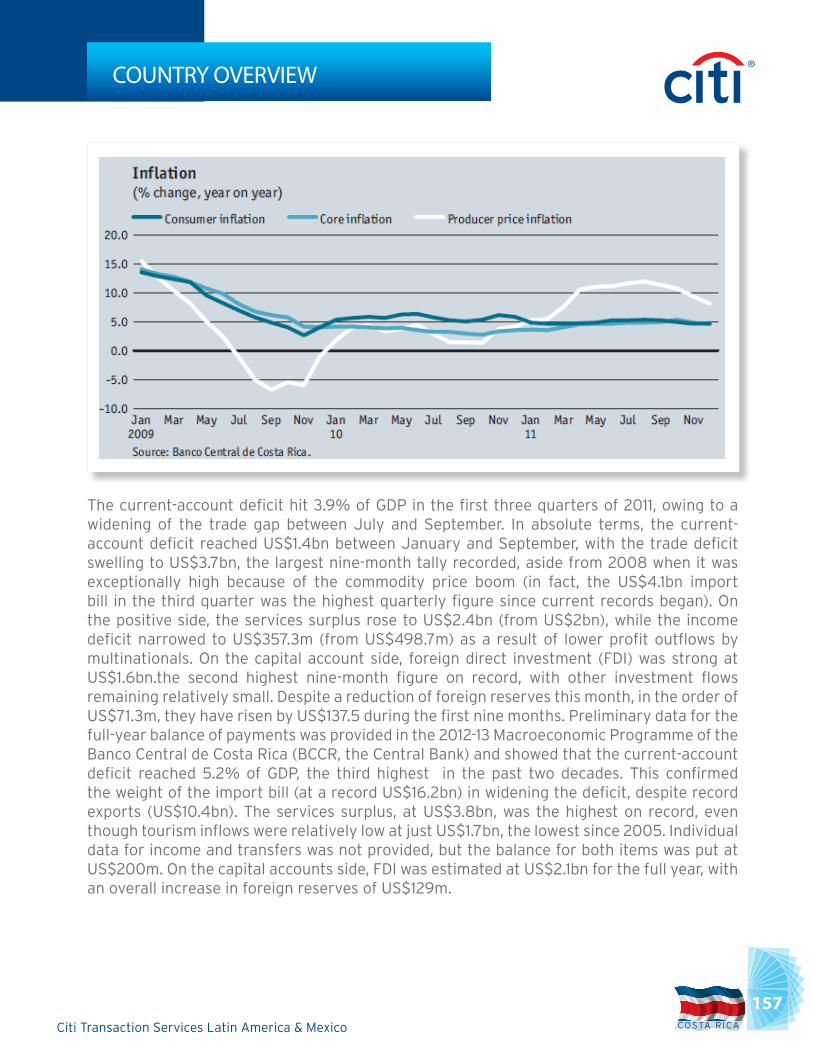

In 2011, annual consumer price inflation (CPI) averaged 4.9% (4.7% year-end), 1.1 percentage points lower than 2010. This is the third straight year in which inflation in Costa Rica has stayed firmly in the single digits and is also the lowest rate seen in the past three decades. The monetary authorities indicate that this is the result of a monetary policy congruent with inflation goals, the absence of pressure from internal demand, exchange-rate stability and significant drops in the price of agricultural products. The rate was driven largely by education costs (8.2% increases) and transportation (7.1%), and to a lesser extent restaurants and other eateries (6.1%). On the other hand, various sectors recorded negligible price increases such as clothing and footwear (0.7%), entertainment and culture (2.1%), as well as rent and household services (2.7%). On a month-on-month basis, CPI rose by 0.9% compared with November, with 53% of the 292 goods and services in the basket rising in price, compared with 34% whose price fell and 13% that remained the same. In addition, core prices rose by 4.5% during 2011, higher than the 3.5% in 2010, while producer prices increased by 9.5% (8.1% year-end), also above the previous year’s figure of 4.1%.

Citi Transaction Services Latin America & Mexico

157COSTA RICA

COUNTRY OVERVIEW

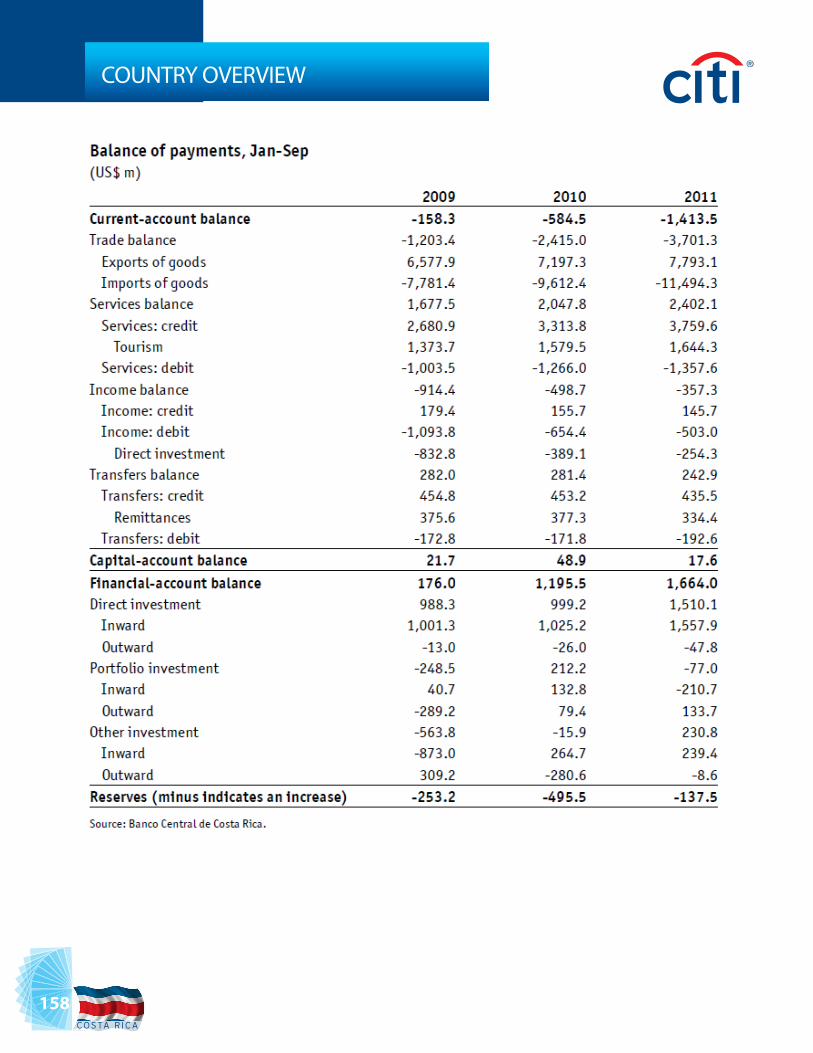

The current-account deficit hit 3.9% of GDP in the first three quarters of 2011, owing to a widening of the trade gap between July and September. In absolute terms, the current-account deficit reached US$1.4bn between January and September, with the trade deficit swelling to US$3.7bn, the largest nine-month tally recorded, aside from 2008 when it was exceptionally high because of the commodity price boom (in fact, the US$4.1bn import bill in the third quarter was the highest quarterly figure since current records began). On the positive side, the services surplus rose to US$2.4bn (from US$2bn), while the income deficit narrowed to US$357.3m (from US$498.7m) as a result of lower profit outflows by multinationals. On the capital account side, foreign direct investment (FDI) was strong at US$1.6bn.the second highest nine-month figure on record, with other investment flows remaining relatively small. Despite a reduction of foreign reserves this month, in the order of US$71.3m, they have risen by US$137.5 during the first nine months. Preliminary data for the full-year balance of payments was provided in the 2012-13 Macroeconomic Programme of the Banco Central de Costa Rica (BCCR, the Central Bank) and showed that the current-account deficit reached 5.2% of GDP, the third highest in the past two decades. This confirmed the weight of the import bill (at a record US$16.2bn) in widening the deficit, despite record exports (US$10.4bn). The services surplus, at US$3.8bn, was the highest on record, even though tourism inflows were relatively low at just US$1.7bn, the lowest since 2005. Individual data for income and transfers was not provided, but the balance for both items was put at US$200m. On the capital accounts side, FDI was estimated at US$2.1bn for the full year, with an overall increase in foreign reserves of US$129m.

158COSTA RICA

COUNTRY OVERVIEW

Citi Transaction Services Latin America & Mexico

159COSTA RICA

COUNTRY OVERVIEW

E. ECONOMIC FORECAST

Economic Growth

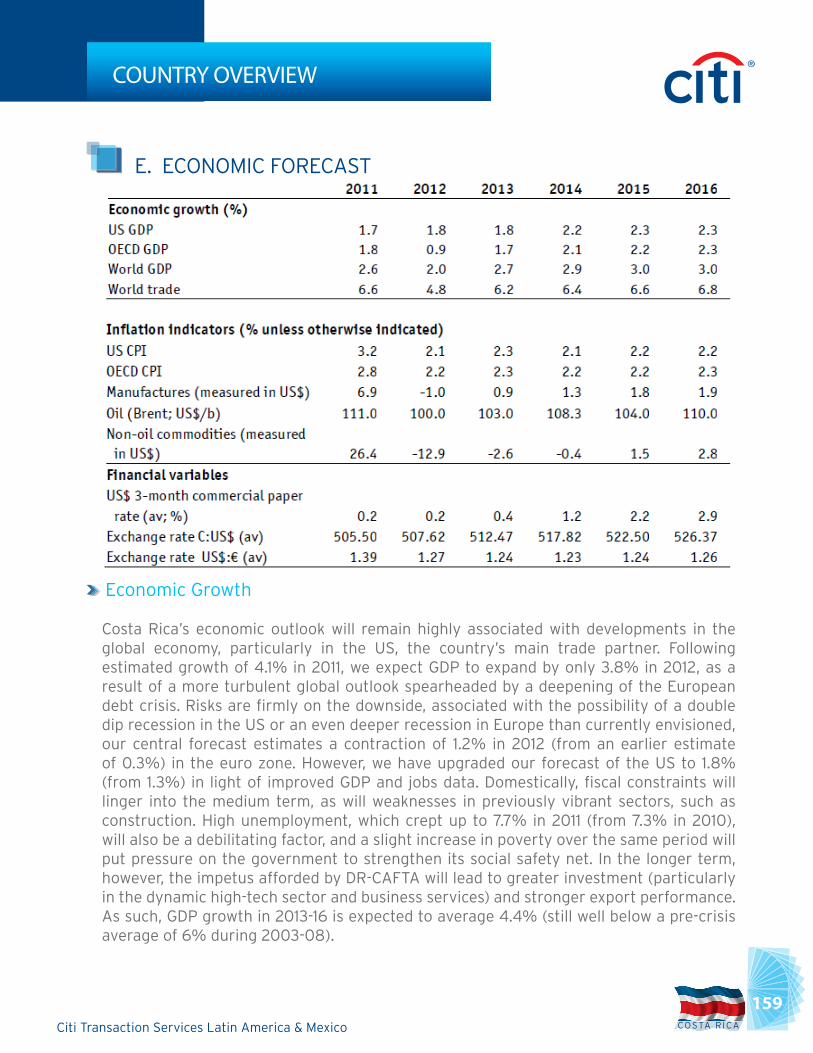

Costa Rica’s economic outlook will remain highly associated with developments in the global economy, particularly in the US, the country’s main trade partner. Following estimated growth of 4.1% in 2011, we expect GDP to expand by only 3.8% in 2012, as a result of a more turbulent global outlook spearheaded by a deepening of the European debt crisis. Risks are firmly on the downside, associated with the possibility of a double dip recession in the US or an even deeper recession in Europe than currently envisioned, our central forecast estimates a contraction of 1.2% in 2012 (from an earlier estimate of 0.3%) in the euro zone. However, we have upgraded our forecast of the US to 1.8% (from 1.3%) in light of improved GDP and jobs data. Domestically, fiscal constraints will linger into the medium term, as will weaknesses in previously vibrant sectors, such as construction. High unemployment, which crept up to 7.7% in 2011 (from 7.3% in 2010), will also be a debilitating factor, and a slight increase in poverty over the same period will put pressure on the government to strengthen its social safety net. In the longer term, however, the impetus afforded by DR-CAFTA will lead to greater investment (particularly in the dynamic high-tech sector and business services) and stronger export performance. As such, GDP growth in 2013-16 is expected to average 4.4% (still well below a pre-crisis average of 6% during 2003-08).

160COSTA RICA

COUNTRY OVERVIEW

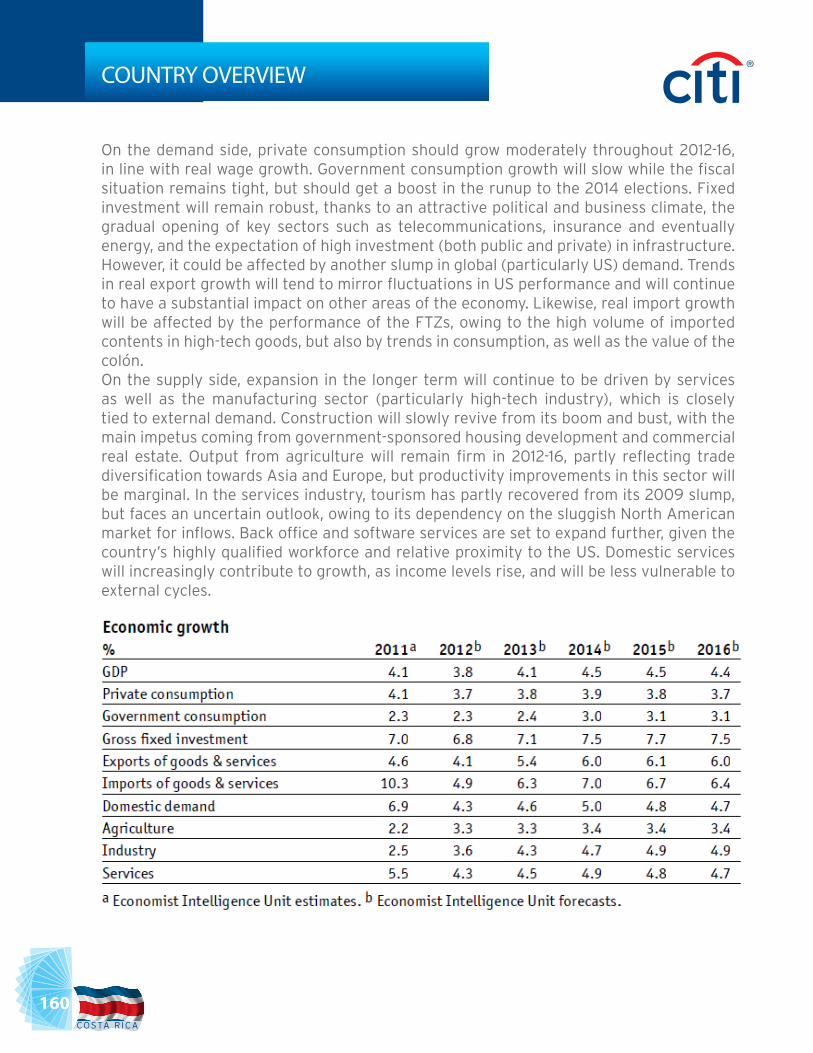

On the demand side, private consumption should grow moderately throughout 2012-16, in line with real wage growth. Government consumption growth will slow while the fiscal situation remains tight, but should get a boost in the runup to the 2014 elections. Fixed investment will remain robust, thanks to an attractive political and business climate, the gradual opening of key sectors such as telecommunications, insurance and eventually energy, and the expectation of high investment (both public and private) in infrastructure. However, it could be affected by another slump in global (particularly US) demand. Trends in real export growth will tend to mirror fluctuations in US performance and will continue to have a substantial impact on other areas of the economy. Likewise, real import growth will be affected by the performance of the FTZs, owing to the high volume of imported contents in high-tech goods, but also by trends in consumption, as well as the value of the colón.On the supply side, expansion in the longer term will continue to be driven by services as well as the manufacturing sector (particularly high-tech industry), which is closely tied to external demand. Construction will slowly revive from its boom and bust, with the main impetus coming from government-sponsored housing development and commercial real estate. Output from agriculture will remain firm in 2012-16, partly reflecting trade diversification towards Asia and Europe, but productivity improvements in this sector will be marginal. In the services industry, tourism has partly recovered from its 2009 slump, but faces an uncertain outlook, owing to its dependency on the sluggish North American market for inflows. Back office and software services are set to expand further, given the country’s highly qualified workforce and relative proximity to the US. Domestic services will increasingly contribute to growth, as income levels rise, and will be less vulnerable to external cycles.

Citi Transaction Services Latin America & Mexico

161COSTA RICA

COUNTRY OVERVIEW

Inflation

Average consumer price inflation (CPI) reached its lowest level on record in 2011, 4.9%.the third straight year of single-digit inflation and well within the BCCR’s target range of 4-6%. The BCCR has maintained this target range for 2012 and expectations should be anchored at around 5% over the medium term, as it moves towards a formal system of inflation targeting and a more flexible exchange- rate policy. There are risks to our baseline CPI forecasts, namely from the possibility of weather-related disruptions to agricultural supplies and from further bouts of volatility in global commodity prices (which contributed to double-digit inflation in 2008). Pressure from monetary aggregates is also unlikely as both broad money (M2) and private credit have been growing at less than one-half of their pre-crisis rates of 30-40%. At 4.5%, core inflation nearly matches the headline figure, confirming that domestic factors are the main source of inflationary pressure.

Exchange Rates

The BCCR is planning a gradual move from the current crawling band exchange-rate regime towards a managed float during 2012-13. During this period, the colón will be exposed to global market turbulence, as well as to changes in local demand for US dollars, in what is a highly dollarized economy. The colón has regained much of the ground lost during a global sell-off of emerging market currencies in August-September, and is now trading just above the band floor (set at C500:US$1). Nevertheless, pressure for further strengthening will be stymied by a generalised risk adversity owing to the ongoing euro zone crisis, which will put a premium on US dollar assets. This will also be complemented, to a lesser extent, by BCCR reserve purchases and a reserve requirement on foreign loans. We expect the colón to reach C510:US$1 by end-2012, after which a widening current-account deficit will push it to C528:US$1 at end-2016. Upside risks to the forecast can emerge from a worsening global economic outlook, which would result in a flight to safety into US dollars.

External Sector

A large and growing structural deficit in goods trade will lead to a widening of the current-account deficit, from an estimated 5.2% of GDP in 2011 to 5.3% of GDP in 2016. This structural deficit is owing to the fact that a large proportion of Costa Rica’s manufactured exports are import-dependent and the country lacks a domestic consumer goods industry, relying on imports. The trade balance will also deteriorate in 2012-16, owing to worsening terms of trade, as a result of Costa Rica’s position as a net commodity importer and rising demand for imported consumer and intermediate goods. However, the services surplus will rise in the longer term, mostly owing to tourism, one of the major sources of foreign

162COSTA RICA

COUNTRY OVERVIEW

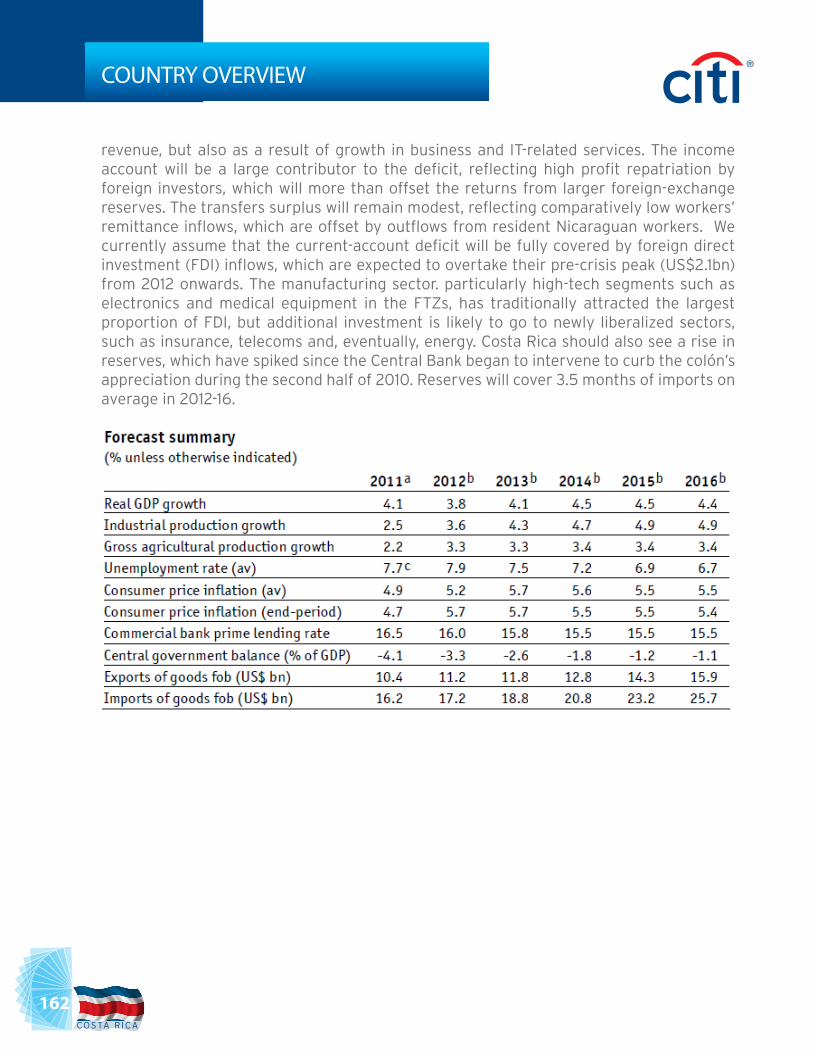

revenue, but also as a result of growth in business and IT-related services. The income account will be a large contributor to the deficit, reflecting high profit repatriation by foreign investors, which will more than offset the returns from larger foreign-exchange reserves. The transfers surplus will remain modest, reflecting comparatively low workers’ remittance inflows, which are offset by outflows from resident Nicaraguan workers. We currently assume that the current-account deficit will be fully covered by foreign direct investment (FDI) inflows, which are expected to overtake their pre-crisis peak (US$2.1bn) from 2012 onwards. The manufacturing sector. particularly high-tech segments such as electronics and medical equipment in the FTZs, has traditionally attracted the largest proportion of FDI, but additional investment is likely to go to newly liberalized sectors, such as insurance, telecoms and, eventually, energy. Costa Rica should also see a rise in reserves, which have spiked since the Central Bank began to intervene to curb the colón’s appreciation during the second half of 2010. Reserves will cover 3.5 months of imports on average in 2012-16.

Citi Transaction Services Latin America & Mexico

163COSTA RICA

COUNTRY OVERVIEW

164COSTA RICA

COUNTRY OVERVIEW

Citi Transaction Services Latin America & Mexico

165COSTA RICA

COUNTRY OVERVIEW

166COSTA RICA

COUNTRY OVERVIEW

Citi Transaction Services Latin America & Mexico

167COSTA RICA

BANKING SYSTEM

A. BANKS IN COSTA RICA

Costa Rica’s banking system continues to be dominated by the three state owned financial institutions that were nationalized in 1949, though they are slowly yielding a percentage of their market to the private sector banks. These three public-sector banks Banco Nacional de Costa Rica, Banco de Costa Rica and Banco Popular y de Desarrollo Comunal—controlled half of the financial system’s total assets and nearly 45% of the financial system’s loan portfolio in early 2009, according to the General Superintendency of Financial Entities (Superintendencia General de Entidades Financieras—SUGEF). Banco Nacional de Costa Rica is the biggest lender, with 26.0% of the financial system’s loan portfolio at 2011 year-end.

The SUGEF is in charge of supervising and regulating the financial sector, according to the Organic Law of the Costa Rican Central Bank (Law 7558, of 1995). In 1995 SUGEF was granted powers to supervise domestic and offshore banks that operate as part of Costa Rican financial holding groups. In September 2005, however, the attorney general ruled that SUGEF did not in fact have the authority to supervise offshore banks. SUGEF enforces the policy of the central bank (Banco Central de Costa Rica—BCCR) and monitors compliance with capital requirements, registration and operations. The Supervisory Council of the Financial System (Consejo Nacional de Supervisión del Sistema Financiero—Conassif) was created in 1997 to oversee the functions of SUGEF, the General Superintendency of Securities (Superintendencia General de Valores—SUGEVAL) and the General Superintendency of Pensions (Superintendencia General de Pensiones—SUPEN). In addition to providing direction for policies related to the financial sector, Conassif provides support and serves as a co-ordinating body for the three superintendencies.

Financial reforms in 1995 liberalised capital markets and guaranteed the free exchange of foreign currency. They also allowed all financial institutions subject to SUGEF supervision to be granted access to the BCCR’s discount window. Law 7558 increased the BCCR’s independence in administering monetary and credit policy. The BCCR is authorised to intervene in financial markets in emergency situations to alleviate economic imbalances or liquidity crises. In such cases it may establish surcharges on imports, limit credit growth, impose reserve requirements and establish the maximum rate of intermediation (the ratio of deposits to loans) for banks.

Citi’s presence in Costa Rica dates back more than 40 years to 1968, when it opened a representative office. In 1993, Citi underwent the transition from a non-banking financial institution into a private bank. In 2007, Citi Central America expanded its consumer operations in that region by acquiring Grupo Financiero Uno and Banco Cuscatlán. Two years later, it inaugurated its Citi Gold centers to support private banking clients and in 2010 Citi Costa Rica set up a franchise office to meet the needs of offshore private banking clients.

168COSTA RICA

B. CITIBANK IN COSTA RICA

Citibank has been established in Costa Rica since 1960. There are currently 16 branches around the country.

Location of Branches

• Alajuela• Curridabat• Escazú• Heredia• Liberia• Limón• Moravia• Multiplaza del Este• Multiplaza Escazú• Paseo de las Flores• Pérez Zeledón• Rohrmoser• San José • Santa Ana• Terramall• La Uruca

Services Offered to Citibank Clients

• Trade Services and Finance• Supply Chain Finance • Cash Management (Payment and Collection Services)• Agency and Trust Services• Treasury Services• FX Management• Credit Services - lending• Investment Banking Services• Buy/sell bonds, stocks, mutual funds• Consumer Banking

BANKING SYSTEM

Citi Transaction Services Latin America & Mexico

169COSTA RICA

CLEARING SYSTEM

The Clearing system in Costa Rica is a public service. The types of documents processed are local current account checks and coupon bonds of both the Banco Central de C.R. The Clearing system in C.R. takes place from Monday through Friday, and is centralized at the Banco Central de C.R through SINPE (Sistema Nacional de Pagos Electrónicos).

A. CLEARING SCHEDULE

Outgoing Funds Transfer

Cut-off Time: 1:00 pmFunding Date: Same dayClient Dr. /Cr. Date: Same dayClient Value Date: Same Day

Incoming Funds Transfer

Cut-off Time: 3:00 pmFunding Date: Same dayClient Dr. /Cr. Date: Same dayClient Value Date: Same Day

Book to Book

Cut-off Time: 6:00 pm (electronic), 1:00 pm (manual)Funding Date: Same dayClient Dr. /Cr. Date: Same dayClient Value Date: Same Day

FCY Payment

Cut-off Time: 3:00 pmFunding Date: Same dayClient Dr. /Cr. Date: Same dayClient Value Date: Day 2

Incoming Checks

Cut-off Time: 2:00 pmFunding Date: Next dayClient Dr. /Cr. Date: Same dayClient Value Date: 2nd day after deposit

170COSTA RICA

CLEARING SYSTEM

B. PROCESS DESCRIPTION

Day 1

The client deposits a local currency check in their account.

Day 2

Early in the morning, Citibank presents its checks for clearing at the SINPE. At the end of each session, if the balance is positive in favor of Citibank, then the Banco Central deposits the credit in Citibank’s account on the same day. Banks are allowed to return checks in case of insufficient funds, incorrect signature, etc.

C. FOREIGN CHECK CLEARING

US Dollar checks drawn against banks domiciled in the US are sent daily via courier to Citibank NY branch. The clearing takes approximately 2 to 3 banking days, however due to credit considerations; banks usually place a 15 day hold on availability of funds. Foreign currency checks are handled on a collection basis.

Citi Transaction Services Latin America & Mexico

171COSTA RICA

On October 17th 2006 Costa Rica abandoned its long-standing system of Costa Rican Central Bank (Banco Central de Costa Rica BCCR)-controlled, daily mini-devaluations to set the value of Costa Rica’s colón in favor of a managed float based on market conditions and exchange rate bands. The BCCR sets a minimum and maximum exchange rate, which debuted at C514.78:US$1 and C530.22:US$1, respectively, in 2006. Within this range, each bank can set its own exchange rates, and the BCCR publishes the banks. Rates on its website. The BBCR will intervene, buying or selling foreign exchange to keep the exchange rate within the band.

Local and foreign residents and companies may freely move capital across Costa Rican borders. The Financial Reform Law of 1995 guaranteed free exchange and remittance in foreign currency. Costa Ricans commonly maintain funds abroad for purchasing imports or to hedge against devaluation. All transactions are made at the prevailing exchange rate, and remittances of investment profits, dividends, interest and principal on private foreign debt, royalties, etc, usually take less than a week. Exports must be reported, but only for statistical-compilation and tax purposes. Paperwork has been centralised at the Ministry of Foreign Trade’s (Ministerio de Comercio Exterior) one-stop office. Although the central bank monitors capital inflows from exports, private banks are no longer required to sell any part otheir foreign currency.

A money-laundering law went into effect in 1999. Banks must inform the Financial Analysis Unit (Unidad de Analisis Financiero UAF), a unit of the Centre of Antinarcotics Joint Intelligence (Centro de Inteligencia Conjunto Antidrogas), of transactions of more than C500,000. They also are required to inform officials of accounts they deem suspicious. Offenders face jail terms of 5-15 years.

The Financial Action Task Force, an OECD-affiliated inter-governmental body that issues guidelines on money-laundering, continues to consider Costa Rica a co-operative jurisdiction. An important element in this positive designation was the Psychotropic Substances, Unauthorised Drugs and Related Activities Law, which became effective in January 2002. The law increased the range of punishable offences and now requires banks to freeze suspicious accounts.

A. EXPORTS

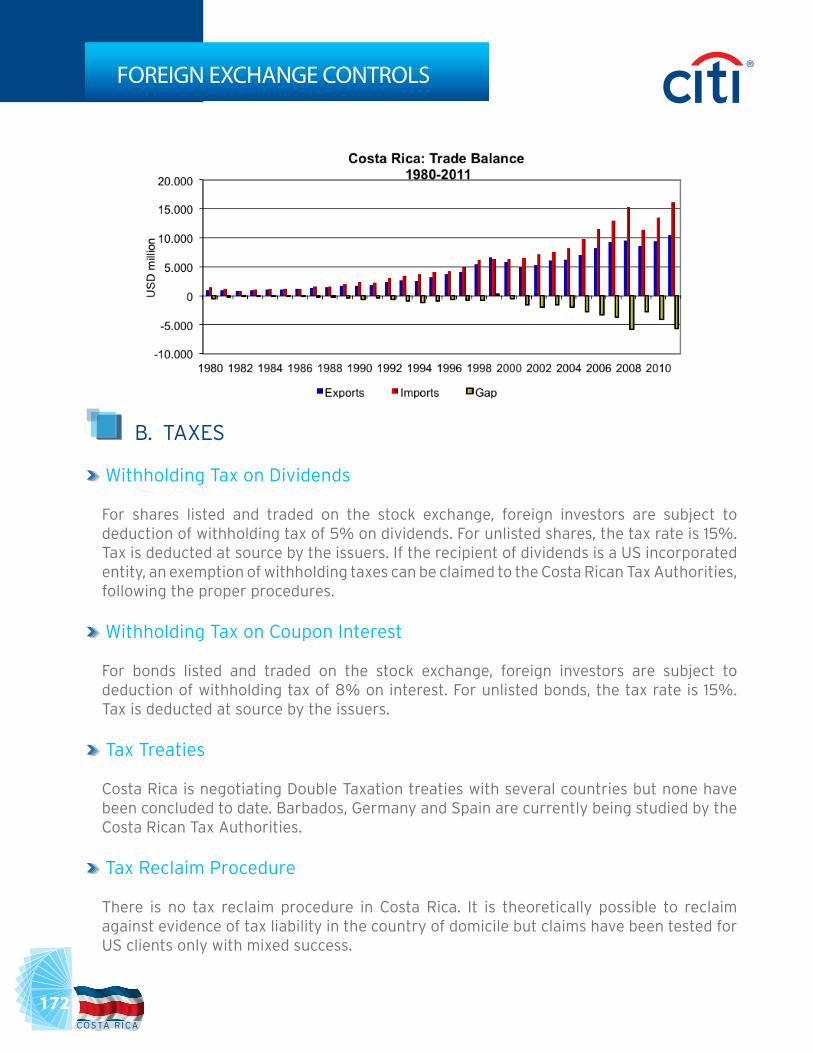

Exports have grown at an average annual rate of 7.1% since 2001. Costa Rica exports 4,255 different products to 148 destination countries. Exports of goods represent 26% of the total GDP. Costa Rica’s trade flows grew 35% in the last 5 years. The country’s trade balance behavior has been stable during the last 10 years, showing a very strong import tendency.

FOREIGN EXCHANGE CONTROLS

172COSTA RICA

B. TAXES

Withholding Tax on Dividends

For shares listed and traded on the stock exchange, foreign investors are subject to deduction of withholding tax of 5% on dividends. For unlisted shares, the tax rate is 15%. Tax is deducted at source by the issuers. If the recipient of dividends is a US incorporated entity, an exemption of withholding taxes can be claimed to the Costa Rican Tax Authorities, following the proper procedures.

Withholding Tax on Coupon Interest

For bonds listed and traded on the stock exchange, foreign investors are subject to deduction of withholding tax of 8% on interest. For unlisted bonds, the tax rate is 15%. Tax is deducted at source by the issuers.

Tax Treaties

Costa Rica is negotiating Double Taxation treaties with several countries but none have been concluded to date. Barbados, Germany and Spain are currently being studied by the Costa Rican Tax Authorities.

Tax Reclaim Procedure

There is no tax reclaim procedure in Costa Rica. It is theoretically possible to reclaim against evidence of tax liability in the country of domicile but claims have been tested for US clients only with mixed success.

FOREIGN EXCHANGE CONTROLS

Citi Transaction Services Latin America & Mexico

173COSTA RICA

TRADE REGULATIONS

A. IMPORT AND EXPORT GOVERNMENT ENTITIES

Information regarding Costa Rica’s policies and regulations, and import/exports statistics can be obtained through the Ministerio de Comercio Exterior (COMEX): www.comex.go.cr

Promotora del Comercio Exterior de Costa Rica (PROCOMER) is another important source of information. PROCOMER promotes exports and foreign investments in Costa Rica, and supports the Ministerio de Comercio Exterior in certain key areas: www.procomer.com

A. FREE TRADE ZONES

Free Trade Zones are a widely developed option for companies looking to establish Shared Service Centers and hubs. They are restricted zones with no resident population, authorized to serve as such by the Government’s Executive Branch. These facilities are intended to accommodate operations engaging in input and raw material imports, manufacturing and assembly or marketing of export goods and provision of export-related services.

Ease of operation, tax incentives, first-rate communications, electric power, utilities, and highly-qualified labour are the elements underlying the development of free-zone companies. Further information as well as the Free Zone Regime Law can be obtained from PROCOMER.

B. REGIONAL TRADE ASSOCIATIONS

Costa Rica is located in the middle of American continent, with ports on both the Pacific and Atlantic oceans, making it an excellent option for establishing an operations base for world markets.

The country currently has several free trade agreements in place; both multilateral, such as the US-Central American-Dominican Republic Free Trade Agreement (CAFTA-DR) and the one with the Caribbean Community (CARICOM), and bilateral agreements, with Canada, Chile, Mexico, Dominican Republic, Panama and the recently approved agreement with China.

Other agreements are currently under negotiations with Perú, Singapur and Europe (Central America/EU).

174COSTA RICA

INVESTMENT OPPORTUNITIES

A. GOVERNMENT AND CENTRAL BANK BONDS

Government and central bank issue fixed income and zero coupon bonds between 1 year and 20 years for Local Currency and USD. There is a weekly auction and also bonds are traded in the secondary market. Yields are between 8,80% and 11,90% for Local Currency and between 2% and 6,38% for USD.

Tax ConsequencesInterest is subject to 8% withholding tax. However, all bonds are traded with net yields.

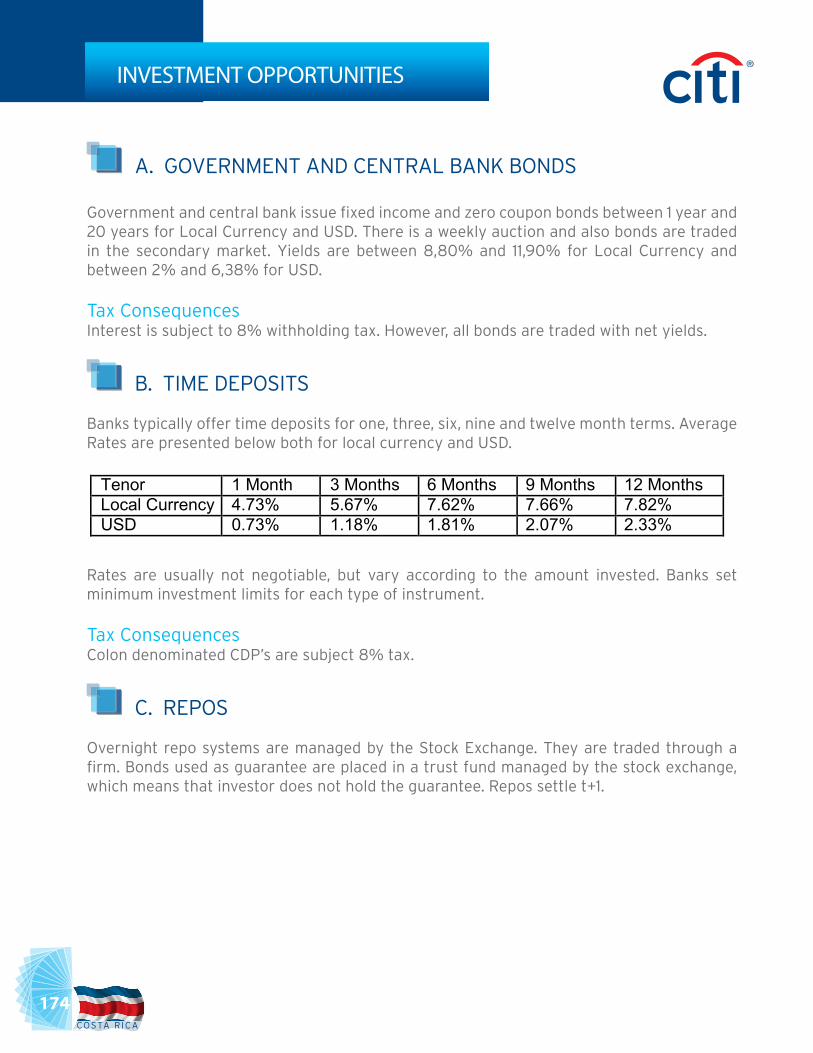

B. TIME DEPOSITS

Banks typically offer time deposits for one, three, six, nine and twelve month terms. Average Rates are presented below both for local currency and USD.

Tenor 1 Month 3 Months 6 Months 9 Months 12 Months Local Currency 4.73% 5.67% 7.62% 7.66% 7.82% USD 0.73% 1.18% 1.81% 2.07% 2.33%

Rates are usually not negotiable, but vary according to the amount invested. Banks set minimum investment limits for each type of instrument.

Tax ConsequencesColon denominated CDP’s are subject 8% tax.

C. REPOS

Overnight repo systems are managed by the Stock Exchange. They are traded through a firm. Bonds used as guarantee are placed in a trust fund managed by the stock exchange, which means that investor does not hold the guarantee. Repos settle t+1.

Citi Transaction Services Latin America & Mexico

175COSTA RICA

INVESTMENT OPPORTUNITIES

Tax ConsequencesTransactions on the overnight systems are subject to an 8% tax.

D. Commercial Paper

Local companies are frequent issuers of commercial paper (CP), which may be purchased through the stock market or directly from the issuing firm. No specialised firms exist for CP trading.

Tax ConsequencesWithholding tax of 8% applies to interest paid on bonds and CP bought through an authorized stock exchange and issued by a company registered with the General Superintendency of Securities (Superintendencia General de Valores).

176COSTA RICA

CITI SOLUTIONS AND SERVICES

CASH MANAGEMENT SERVICES

A. CITI’S ACCOUNT SERVICES SOLUTIONS IN COSTA RICA

Types of Deposit Demanding Accounts

Resident and Non Resident Smart Accounts * US Dollars• Interest Rate: Current accounts earn interests by amount• Minimum Average Balance Requirement: U.S. $12.5 Million (monthly)• Overdraft Facility: Is available but discouraged due to the lack of automated systems.

Documentation Requirements• Due Diligence form (CADD): Filled out with name, complete address, telephone number, type of business, references, and other information, all verified by bank officer.• Signature cards: Verified by bank officer. Copies of local identity cards (“cédulas de identidad”) or passports are also included.• General Resolution (personería juridical) Contains the corporations’ instructions regarding the handling of the account, specifies if single or joint signatures are required, • Global and Local Account Conditions• Deed of Incorporation: Copy of deed of incorporation of the company, duly registered.• Meeting of Board of Directors: Copy of the minutes of the meeting where the board of directors authorizes the opening of the account with Citibank, N.A.(optional).• Check Book: Signed checkbook request form. If a special checkbook is required, the company must send a sample and specifications.• Bank and Commercial References

B. CITI’S PAYMENT SOLUTIONS IN COSTA RICA

Cross-Border Payments

WorldLink and Citidirect

Local Payments

Citibank PayLink

C. CITI’S COLLECTIONS SOLUTIONS IN COSTA RICA

International Collections

Citi Transaction Services Latin America & Mexico

177COSTA RICA

• Incoming Funds Transfer – International transfers may be received in US Dollars and have a same day value date.

Domestic Collections

• Domestic fund transfers are made through an ACH (SINPE) or a manager’s check, which normally has a two days holding period. • SpeedCollect and Regional Collections are available.• Pick-up service also available for specific customers.

D. DELIVERY SYSTEMS AVAILABLE

Citidirect and Netbanking, our customer internet banking platform.

TRADE SERVICES

A. PRODUCTS

Citi offers a wide variety of local and international trade solutions in Costa Rica:

Trade Finance• Import Financing• Pre & Post Export Financing

Trade Services• Letters of Credit*• Documentary Collections*

Supply Chain Finance• Discount of invoices and bills of exchange• Supplier financing*

B. DELIVERY SYSTEMS AVAILABLE

Electronic solutions for Trade Services and Supply Chain Finance products are available via our global platform: Citidirect.

CITI SOLUTIONS AND SERVICES

178COSTA RICA

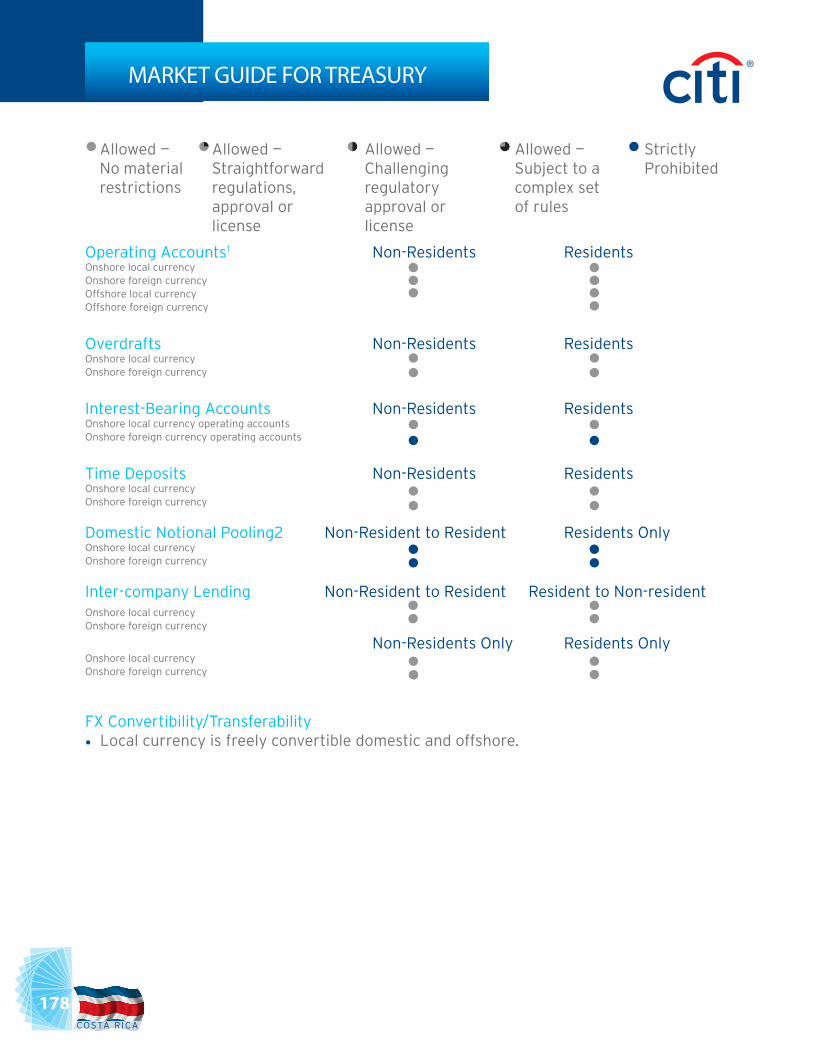

MARKET GUIDE FOR TREASURY

Allowed —No materialrestrictions

Operating Accounts1 Non-Residents ResidentsOnshore local currencyOnshore foreign currencyOffshore local currency Offshore foreign currency

Overdrafts Non-Residents ResidentsOnshore local currencyOnshore foreign currency

Interest-Bearing Accounts Non-Residents Residents Onshore local currency operating accountsOnshore foreign currency operating accounts

Time Deposits Non-Residents ResidentsOnshore local currencyOnshore foreign currency

Domestic Notional Pooling2 Non-Resident to Resident Residents OnlyOnshore local currencyOnshore foreign currency

Inter-company Lending Non-Resident to Resident Resident to Non-residentOnshore local currencyOnshore foreign currency

Non-Residents Only Residents OnlyOnshore local currencyOnshore foreign currency

FX Convertibility/Transferability• Local currency is freely convertible domestic and offshore.

Allowed —Straightforwardregulations,approval orlicense

Allowed —Challengingregulatoryapproval orlicense

Allowed —Subject to acomplex setof rules

StrictlyProhibited

Citi Transaction Services Latin America & Mexico

179COSTA RICA

MARKET GUIDE FOR TREASURY

Other Payment and Clearing Considerations for Treasury• No major restrictions on ACH.• No major restrictions on Non-Residents making payment on behalf of Residents.

For more information, please visit www.transactionservices.citi.com.

Notes:1 Offshore accounts are available only in USD.2 Notional pooling is not available at local market in CR.

180COSTA RICA

CONTACT INFORMATION

Sales Heads

Industry Sector Heads

Carolina JuanTreasury and Trade Solutions Client Sales ManagementLatin America & Mexico HeadCiti Transaction ServicesEmail: [email protected]: + 57 (316) 743 - 9347Of. Phone: +57 (1) 639 - 4026

Industrials SectorInes Vargas BarreraEmail: [email protected]: +52 (181) 8366 - 5190Of. Phone: +52 (81) 1226 - 8525

Branding, Consumer and Healthcare SectorOscar MazzaEmail: [email protected]: +1 (305) 588 - 9396Of. Phone: +1 (305) 347 - 1336

Technology, Media and Telecom SectorGabriel KirestianEmail: [email protected]: +54 (911) 3301 - 4826Of. Phone: +54 (11) 4329 - 1516

Energy, Power and Chemicals SectorPeter LangshawEmail: [email protected]: +55 (11) 6183 - 6958Of. Phone: +55 (11) 6183 - 6958

Public SectorJorg PaascheEmail: [email protected]: +52 (1) 55 5453 - 0103Of. Phone: +52 (55) 2226 - 6020Based: Mexico DF, Mexico

Non Bank FI Sector (NFBI)Ricardo DessyEmail: [email protected]: +54 (911) 6641 - 9752Of. Phone: +54 (11) 4329 - 1471Based: Buenos Aires, Argentina

BrazilAdoniro CestariEmail: [email protected]: +55 (11) 7130 - 9447Of. Phone: +55 (11) 4009 - 7838Based: Sao Paulo, Brazil

Central AmericaEvelin MadridEmail: [email protected]: + 506 8701 - 4529Of. Phone: +506 2588 - 7541Based: San Jose, Costa Rica

MexicoMiguel YtuarteEmail: [email protected]: +52 (1) 55 4088 - 2284Of. Phone: +5255 (1226) 8895Based: Mexico DF, Mexico

Andean RegionCarolina JuanEmail: [email protected]: + 57 (316) 743 - 9347Of. Phone: +57 (1) 639 - 4026Based: Bogota, Colombia

ArgentinaAdrian ScosceiraEmail: [email protected]: +54 (911) 5674 - 6966Of. Phone: +54 (11) 4329 - 1194Based: Buenos Aires, Argentina

Citi Transaction Serviceswww.transactionservices.citi.com

© 2012 Citibank, N.A. All rights reserved. Citi and Arc Design is a trademark and service mark of Citigroup Inc., used and registered throughout the world. All other trademarks are the property of their respective owners.

BrazilAdoniro CestariEmail: [email protected]: +55 (11) 7130 - 9447Of. Phone: +55 (11) 4009 - 7838Based: Sao Paulo, Brazil

Central AmericaEvelin MadridEmail: [email protected]: + 506 8701 - 4529Of. Phone: +506 2588 - 7541Based: San Jose, Costa Rica

MexicoMiguel YtuarteEmail: [email protected]: +52 (1) 55 4088 - 2284Of. Phone: +5255 (1226) 8895Based: Mexico DF, Mexico

Andean RegionCarolina JuanEmail: [email protected]: + 57 (316) 743 - 9347Of. Phone: +57 (1) 639 - 4026Based: Bogota, Colombia

ArgentinaAdrian ScosceiraEmail: [email protected]: +54 (911) 5674 - 6966Of. Phone: +54 (11) 4329 - 1194Based: Buenos Aires, Argentina