Embed Size (px)

Citation preview

Annual Report 2012/13

Ceylon Investment PlC

Contents Corporate Information

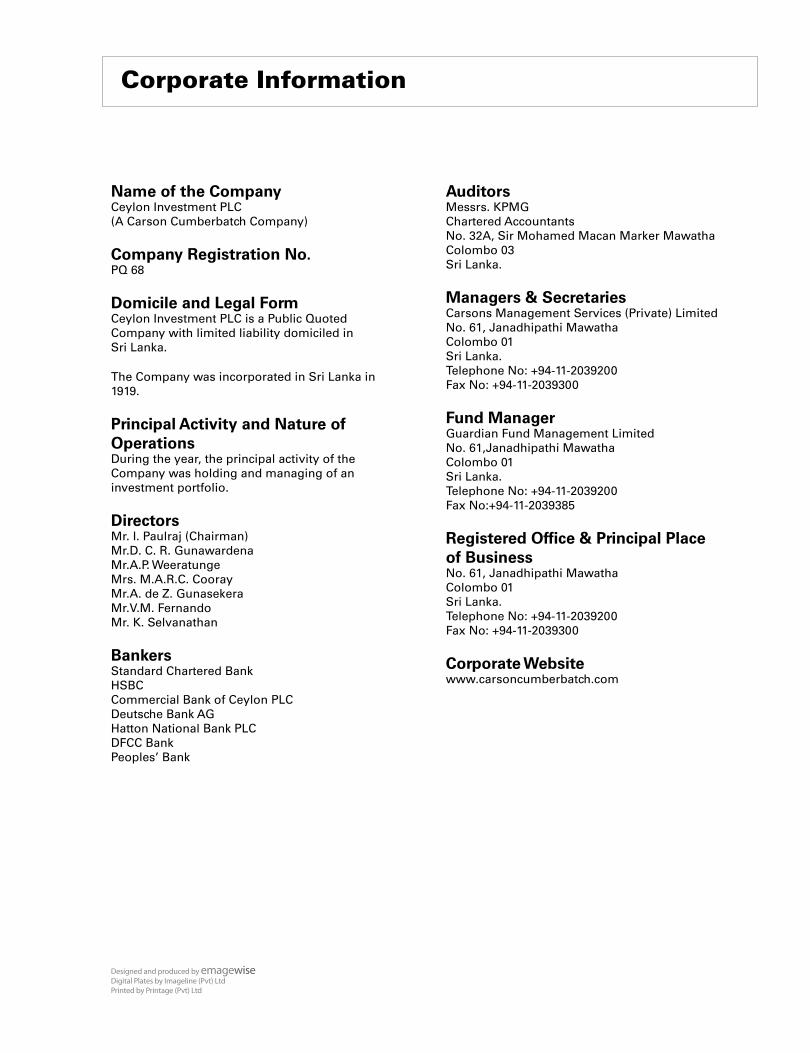

Name of the CompanyCeylon Investment PlC(A Carson Cumberbatch Company)

Company Registration No.PQ 68

Domicile and Legal Form Ceylon Investment PlC is a Public Quoted Company with limited liability domiciled in sri lanka.

the Company was incorporated in sri lanka in 1919.

Principal Activity and Nature of OperationsDuring the year, the principal activity of the Company was holding and managing of an investment portfolio.

Directorsmr. I. Paulraj (Chairman) mr.D. C. R. Gunawardenamr.A.P. Weeratungemrs. m.A.R.C. Cooray mr.A. de Z. Gunasekeramr.v.m. Fernando mr. K. selvanathan

Bankersstandard Chartered Bank HsBCCommercial Bank of Ceylon PlC Deutsche Bank AGHatton national Bank PlCDFCC Bank Peoples’ Bank

Auditors messrs. KPmG Chartered Accountantsno. 32A, sir mohamed macan marker mawatha Colombo 03sri lanka.

Managers & SecretariesCarsons management services (Private) limited no. 61, Janadhipathi mawathaColombo 01 sri lanka.telephone no: +94-11-2039200 Fax no: +94-11-2039300

Fund ManagerGuardian Fund management limited no. 61,Janadhipathi mawatha Colombo 01sri lanka.telephone no: +94-11-2039200Fax no:+94-11-2039385

Registered Office & Principal Place of Businessno. 61, Janadhipathi mawatha Colombo 01sri lanka.telephone no: +94-11-2039200 Fax no: +94-11-2039300

Corporate Websitewww.carsoncumberbatch.com

Designed and produced by emagewiseDigital Plates by Imageline (Pvt) Ltd Printed by Printage (Pvt) Ltd

Financial Highlights 1

Chairman’s statement 2

managers’ Review 4

Risk management 14

Annual Report of the Board of Directors on the

Affairs of the Company 19

Profiles of the Directors 26

management team Profile 28

Audit Committee Report 29

Financial Information 31

Independent Auditors’ Report 32

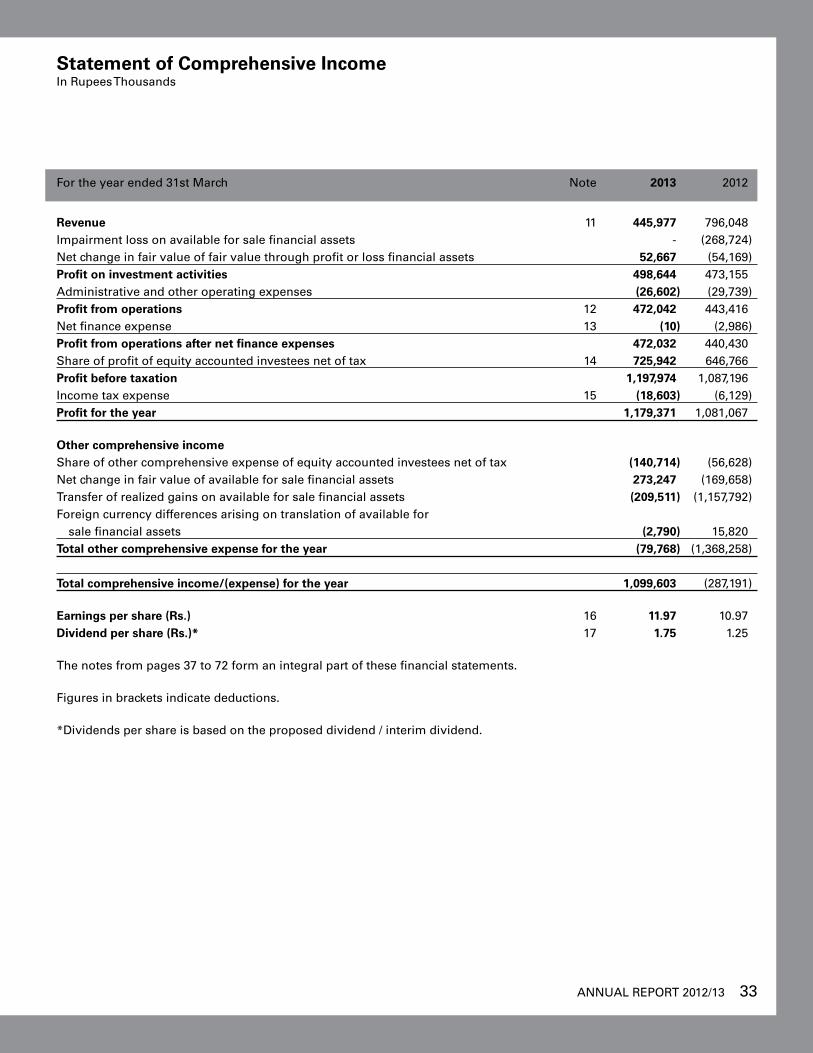

statement of Comprehensive Income 33

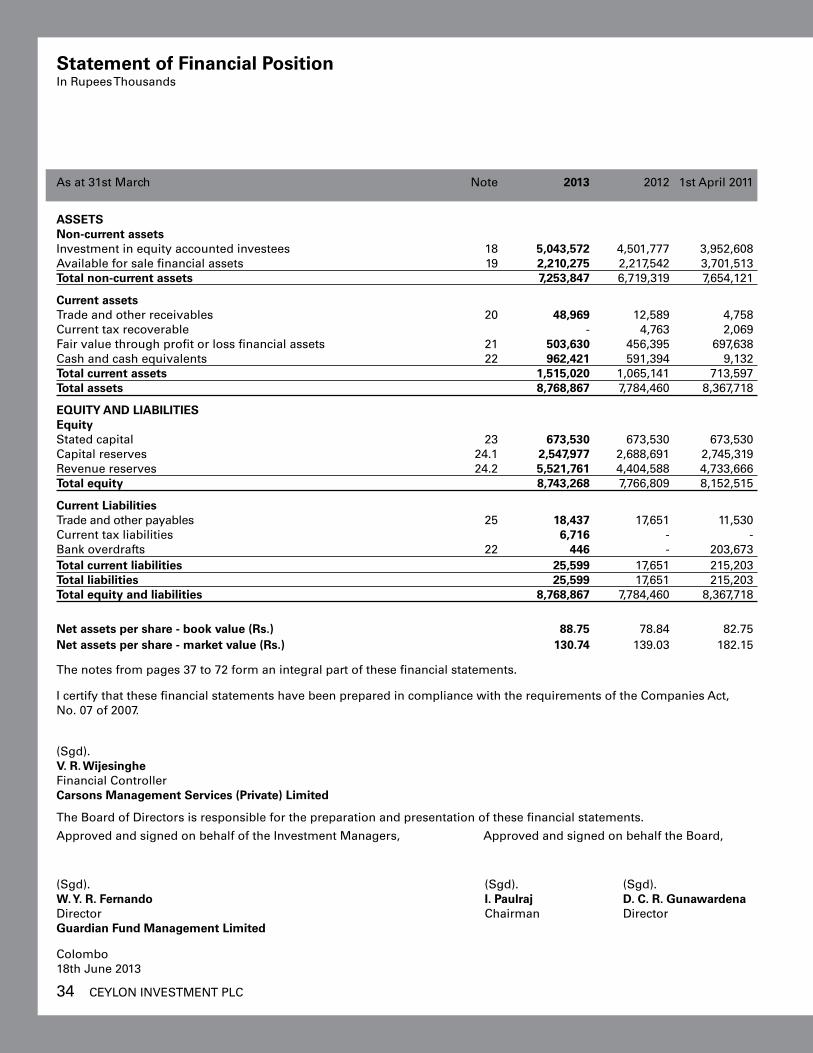

statement of Financial Position 34

statement of Changes in equity 35

Cash Flow statement 36

notes to the Financial statements 37

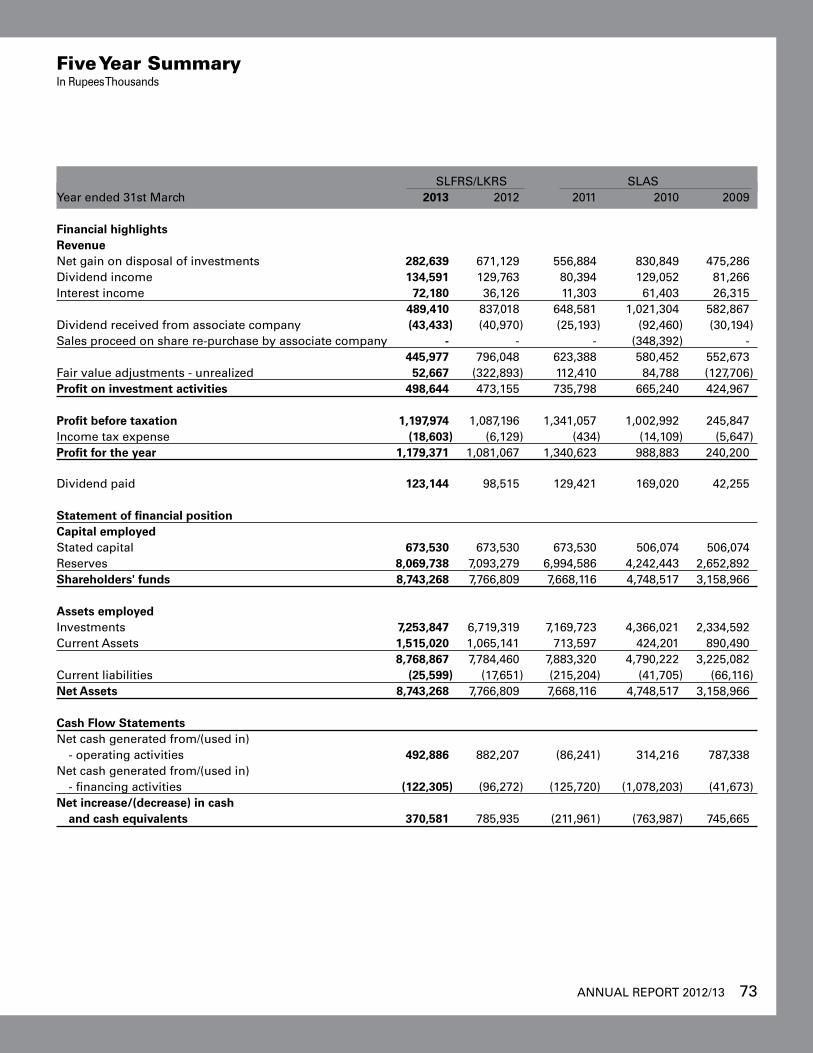

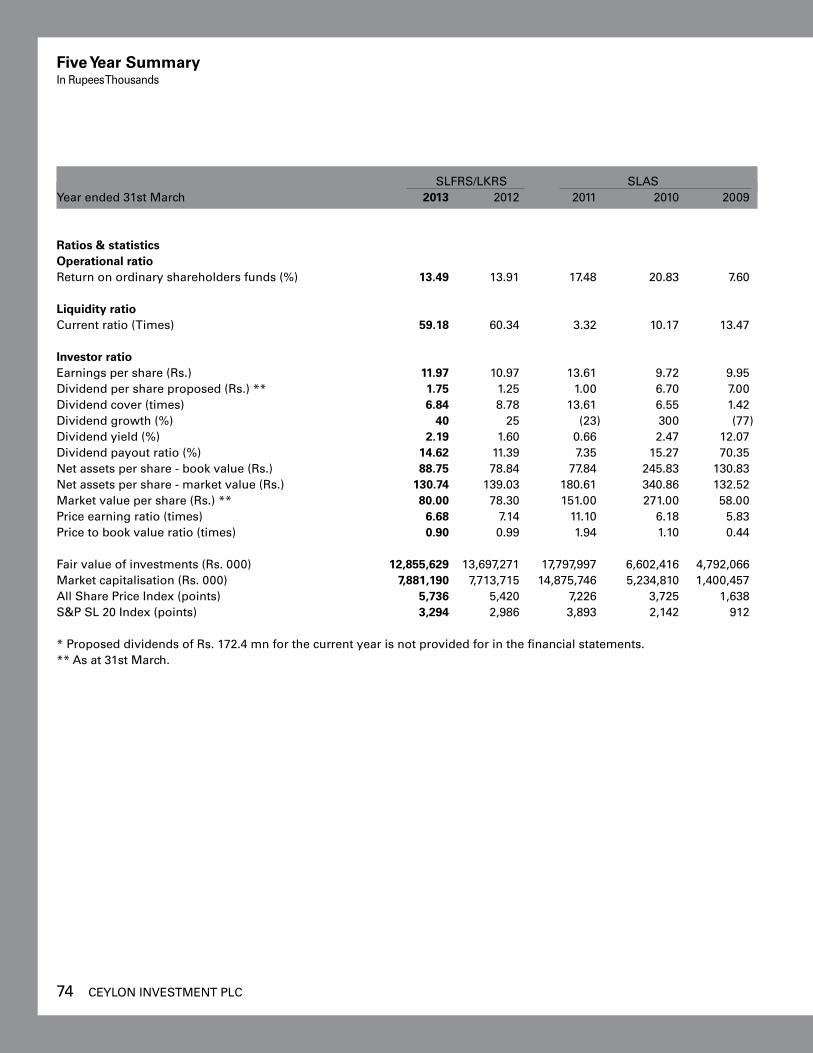

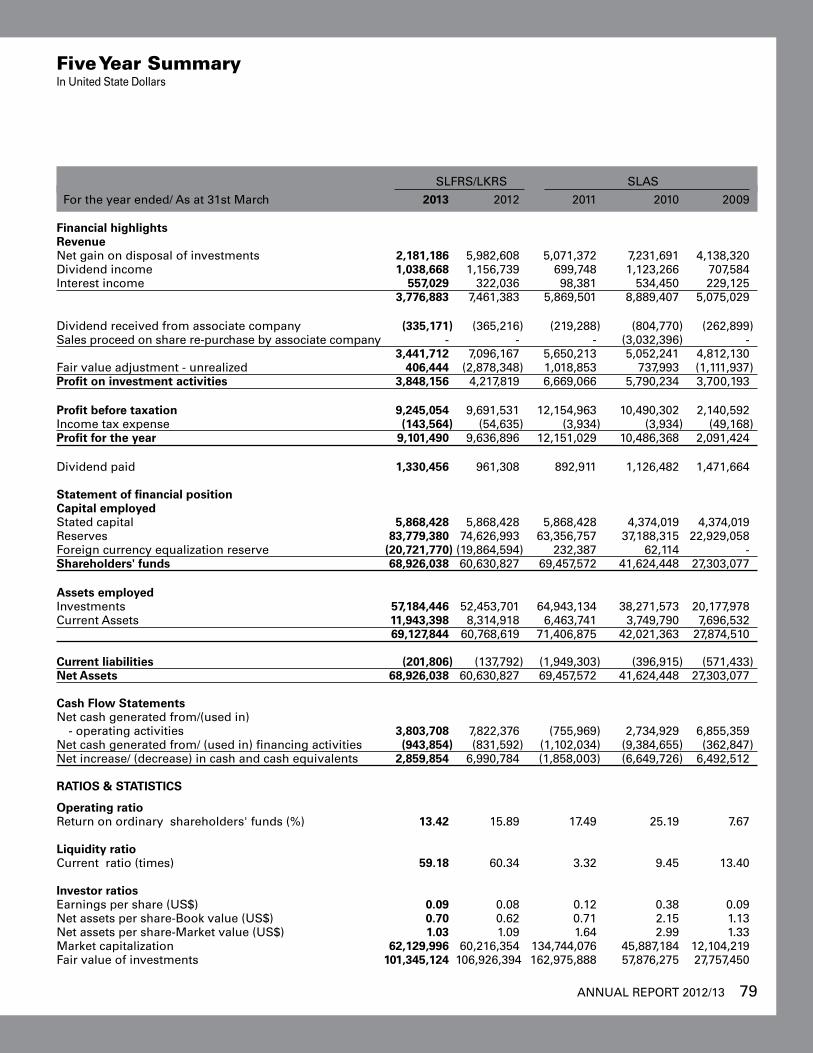

Five year summary 73

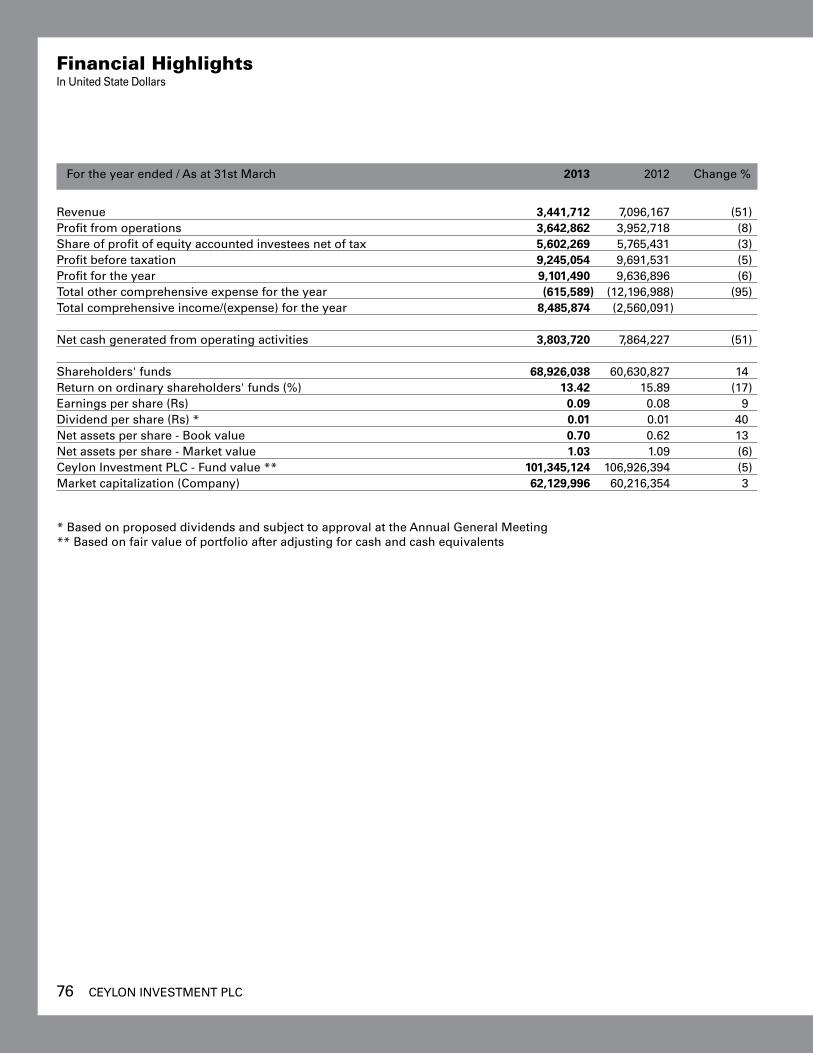

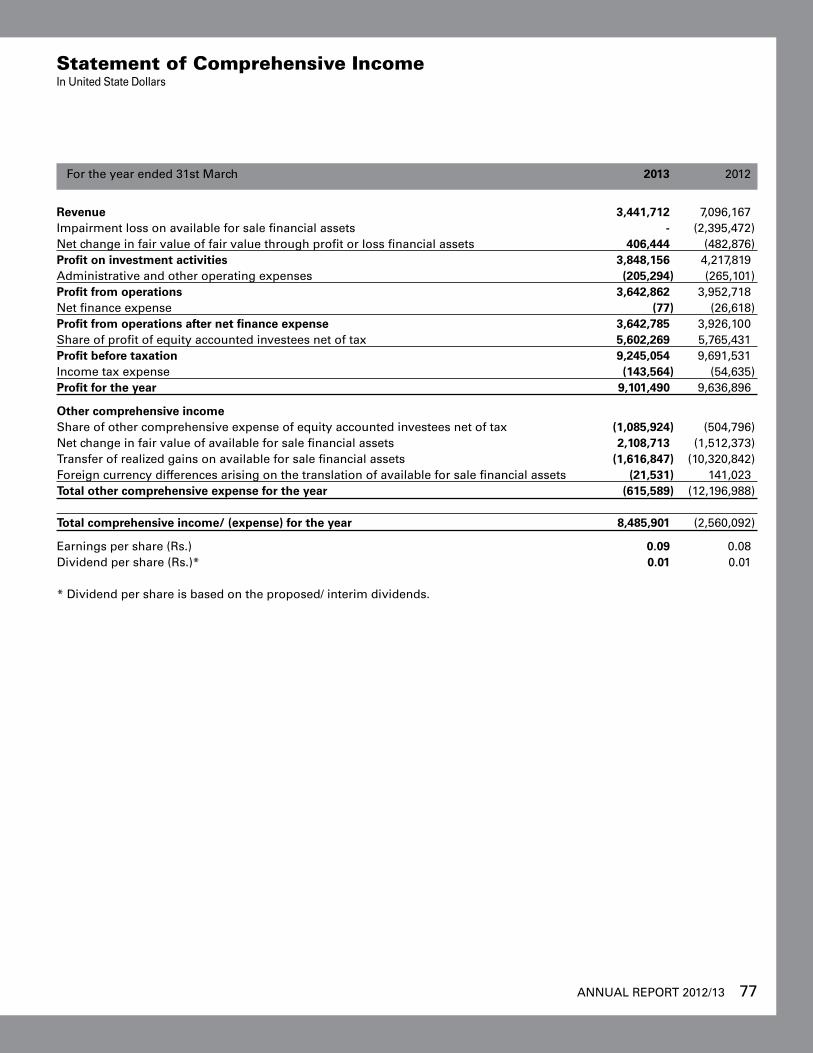

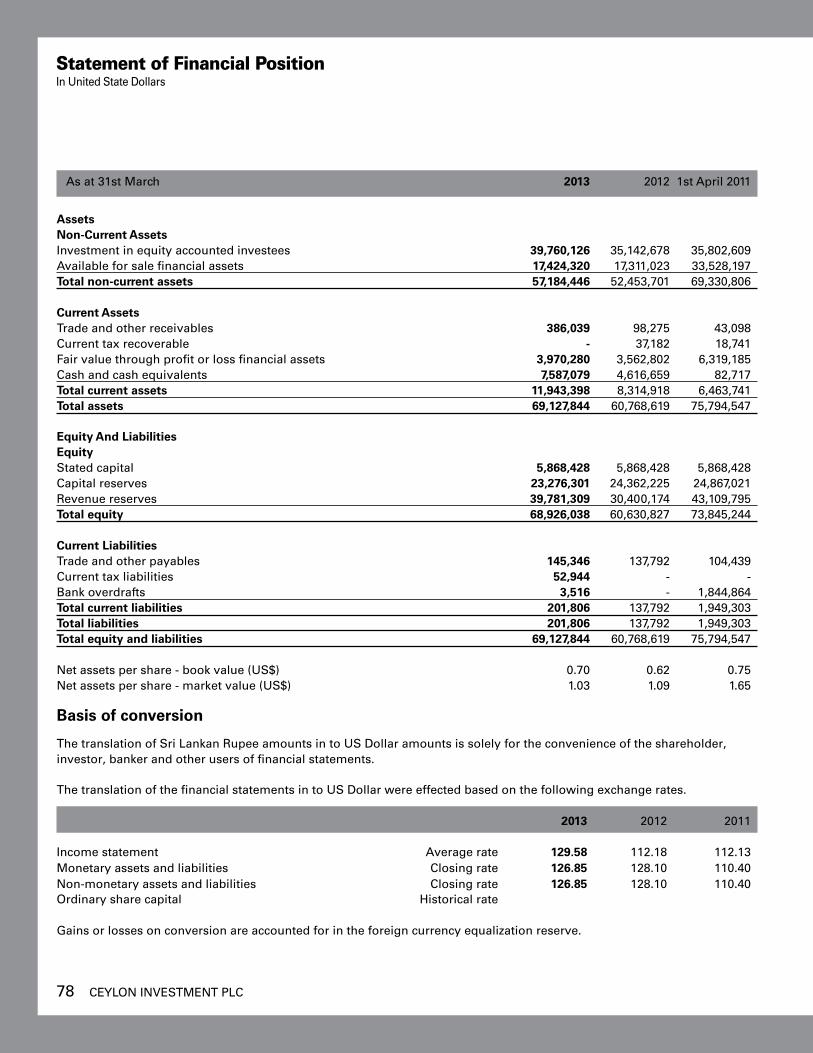

Us$ Financials 75

Information to shareholders and Investors 80

notice of meeting 82

Form of Proxy 83

ANNUAL REPORT 2012/13 1

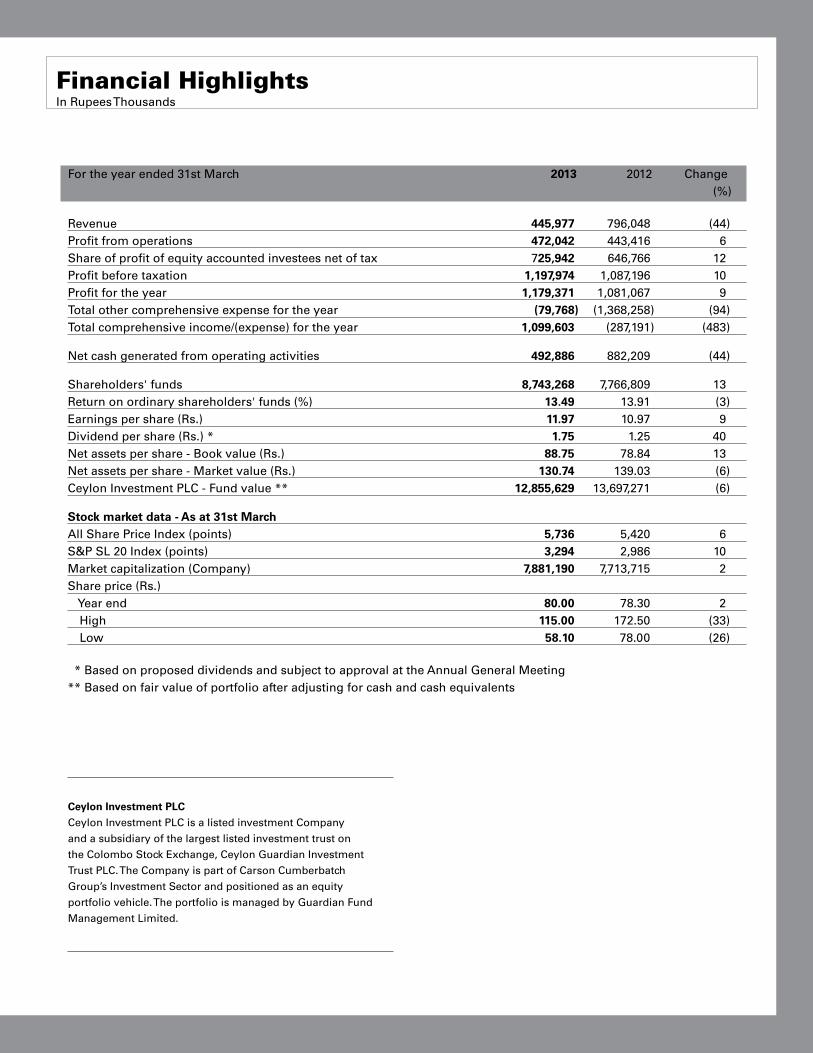

Financial HighlightsIn Rupees Thousands

For the year ended 31st March 2013 2012 Change (%)

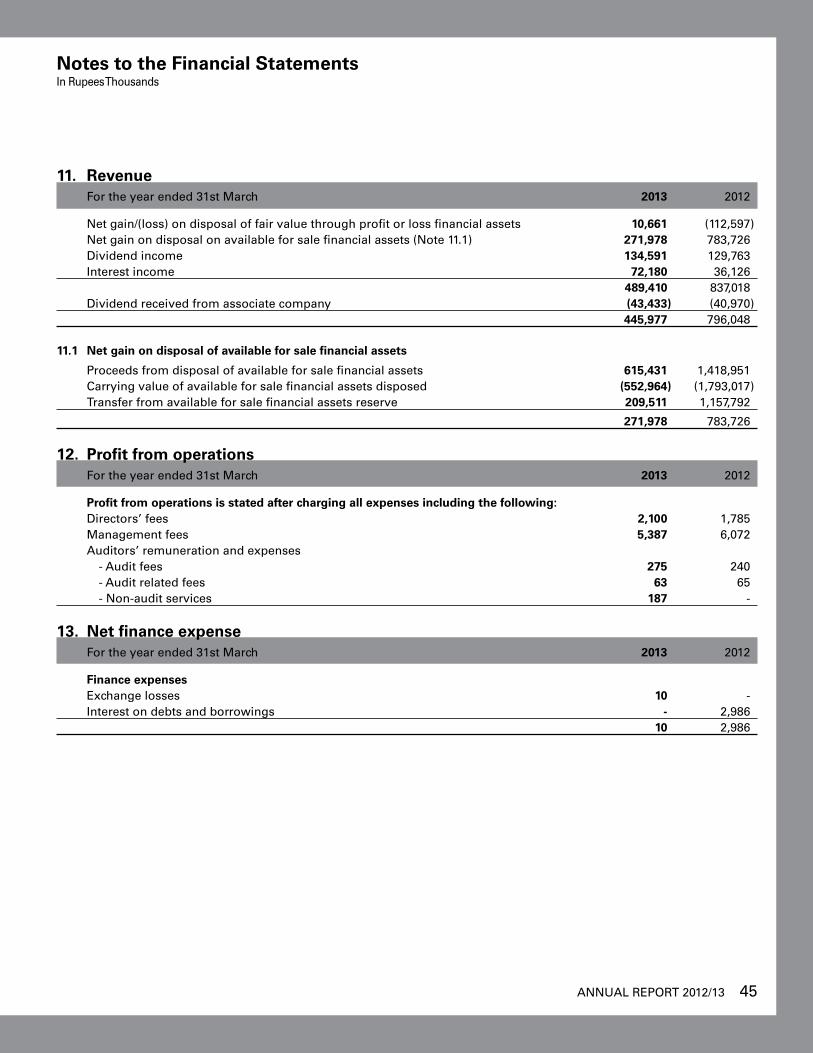

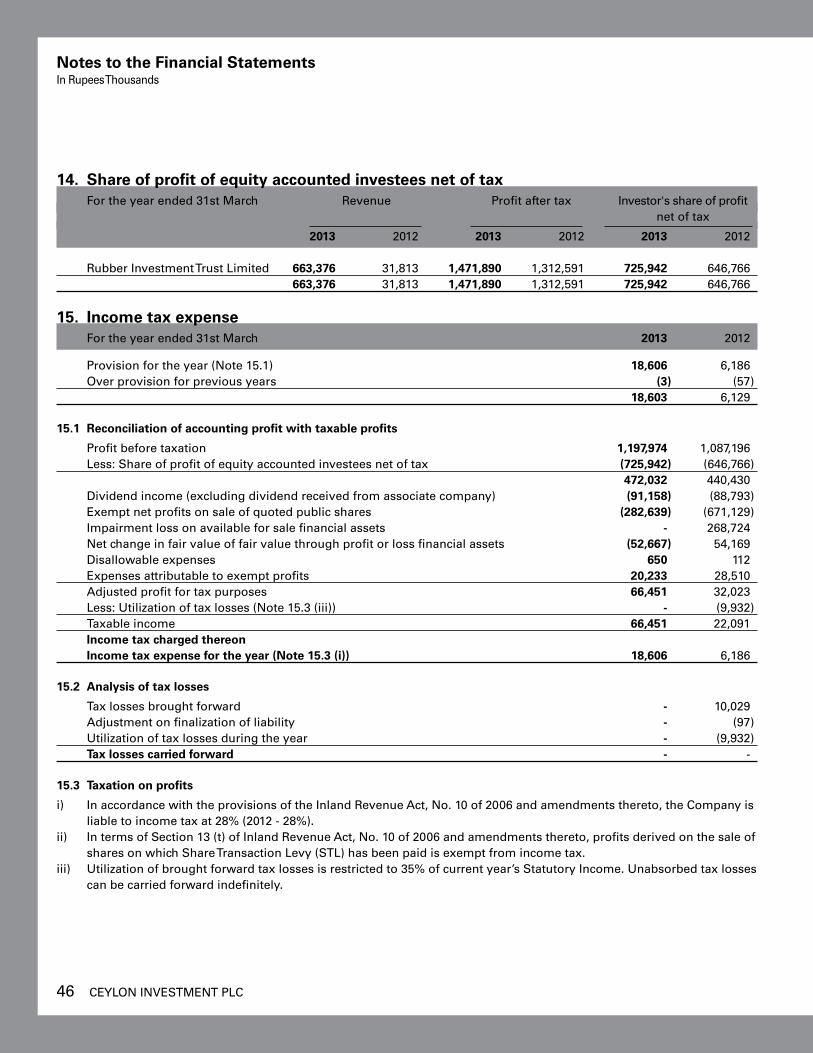

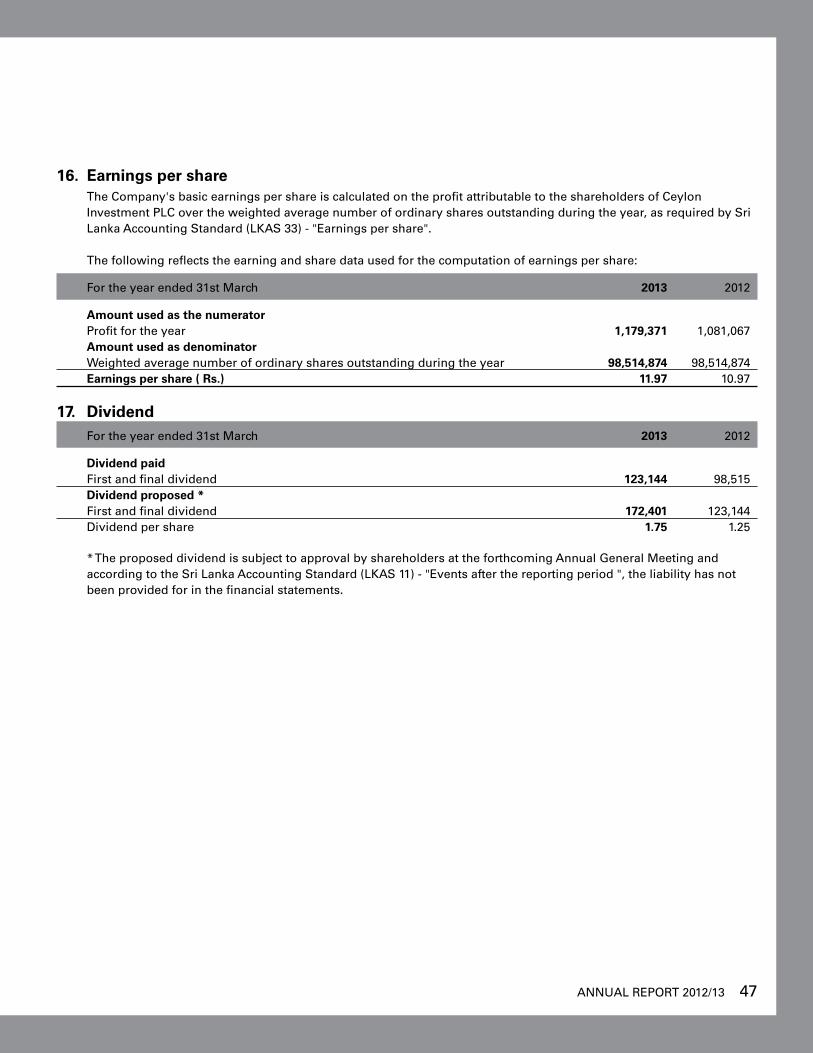

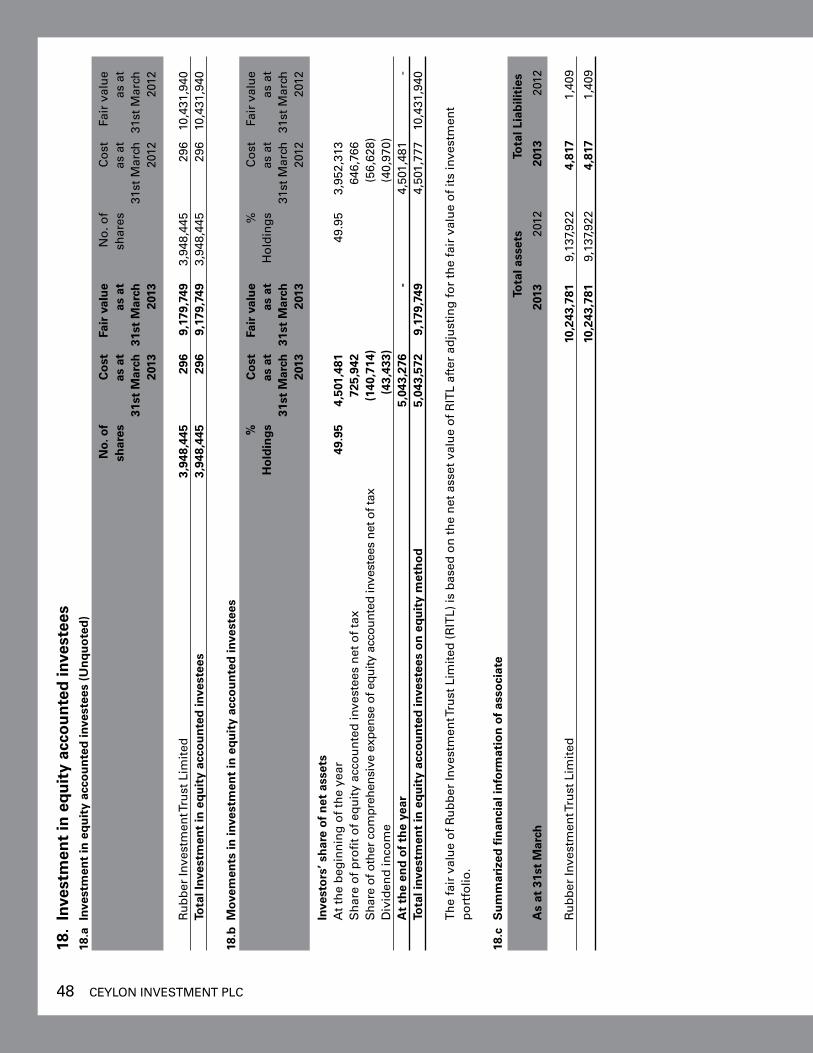

Revenue 445,977 796,048 (44)Profit from operations 472,042 443,416 6Share of profit of equity accounted investees net of tax 725,942 646,766 12Profit before taxation 1,197,974 1,087,196 10Profit for the year 1,179,371 1,081,067 9Total other comprehensive expense for the year (79,768) (1,368,258) (94)Total comprehensive income/(expense) for the year 1,099,603 (287,191) (483)

Net cash generated from operating activities 492,886 882,209 (44)

Shareholders' funds 8,743,268 7,766,809 13Return on ordinary shareholders' funds (%) 13.49 13.91 (3)Earnings per share (Rs.) 11.97 10.97 9Dividend per share (Rs.) * 1.75 1.25 40Net assets per share - Book value (Rs.) 88.75 78.84 13Net assets per share - Market value (Rs.) 130.74 139.03 (6)Ceylon Investment PLC - Fund value ** 12,855,629 13,697,271 (6)

Stock market data - As at 31st MarchAll Share Price Index (points) 5,736 5,420 6S&P SL 20 Index (points) 3,294 2,986 10Market capitalization (Company) 7,881,190 7,713,715 2Share price (Rs.) Year end 80.00 78.30 2 High 115.00 172.50 (33) Low 58.10 78.00 (26)

* Based on proposed dividends and subject to approval at the Annual General Meeting** Based on fair value of portfolio after adjusting for cash and cash equivalents

Ceylon Investment PLC

Ceylon Investment PLC is a listed investment Company

and a subsidiary of the largest listed investment trust on

the Colombo Stock Exchange, Ceylon Guardian Investment

Trust PLC. The Company is part of Carson Cumberbatch

Group’s Investment Sector and positioned as an equity

portfolio vehicle. The portfolio is managed by Guardian Fund

Management Limited.

2 CEYLON INvESTMENT PLC

Dear shareholder,I welcome you to the 67th Annual General Meeting of the Company on behalf of the Board of Directors, and take pleasure in presenting the Annual Report and Audited Accounts of the Company for the year ended 31st March 2013.

The year under review has been a challenging one with the Colombo stock market experiencing much volatility and recording marginal positive growth during the period under review. Domestic and global issues have clouded the sentiment of the Colombo Bourse and transactions have been subdued. Economic concerns added to the prevailing sentiment, driving investors to fixed income products in the backdrop of a rising interest rate scenario. However, on the international front, markets have been buoyant despite challenging economic problems; namely the debt crisis of the European Union and financial cliff overhang of the US and decline in GDP momentum of China. Despite this, foreign markets have been on positive ground, going against the economic fundamentals faced by these developed economies. Recent indications of a strengthening of the US economy, coupled with a signal that fiscal stimulus packages would slowdown, has led to an outflow of capital from emerging markets back to the US.

Confident of Future Growth ProspectsDespite the clouding effect of both local and overseas macro factors, at Ceylon Investment, we still remain confident of the long term potential of Sri Lankan equities and the sustainability of the economic development plans set in place after an end to a 30 year civil war in 2009. We believe that the long term development potential of Sri Lanka will flow through to its equity markets and ratios such as market capitalisation to GDP (currently 29%) will improve in the near

Chairman’s Statement

future to more mature markets levels. Short term blips however are likely to bring uncertainty to equity investors, but we remain confident that in the long haul, the vagaries of the market will be ironed out. Hence, Ceylon Investment being a long term investor remains buoyant and would look to exploit weaknesses in equity markets to our advantage.

Strong PerformanceThe Company recorded a profit after tax of Rs. 1.18 bn despite volatile market conditions, whereby the market ended on a positive note for the financial year 2012/13. Our above average performance was attributed to booking of profits on selected overvalued stocks, capturing market anomalies and booking substantial capital gains despite volatile market conditions. Our portfolio value decreased to Rs. 12.86 bn, from Rs. 13.69 bn a year earlier; recording a depreciation of 6.1% vis-à-vis a 5.8% increase in the benchmark All Share Index and 10.32% appreciation in the newly constructed Standard & Poor's Sri Lanka 20 Index.

On evaluating the medium term performance, five year compounded annual portfolio growth rate was 21.67% on market value basis and 33.1% on market capitalization, vis-à-vis an All Share Index growth of 17.6%. The long term track record of Ceylon Investment is thus highlighted, on reading market conditions effectively enabling shifting of funds between asset classes contributing to portfolio performance. We have not been weary of holding high cash positions and waiting out of equities, being patient during times of market uncertainty.

Guardian Fund ManagementThe initiative of managing and growing assets under management (AUM) has been entrusted to Guardian Fund Management Limited the asset management company, of the Guardian Group. It provides a variety of diverse services, namely, customized portfolios for institutional clients and country and mutual fund management. Our initiative to model group company assets in terms of risk appetite into listed and private equity has been done via the three listed investment companies of the Ceylon Guardian Group. Based on the above, the investment companies have been sub grouped to best represent these multiple asset classes. Ceylon Guardian Investment Trust PLC functions as the main holding entity with diverse interests while Ceylon Investment PLC concentrates on listed equity investing, both having a mix of trading and long term portfolios to add different flavors based on investment horizon and strategy. The focus on unlisted private equity comes via Guardian Capital Partners a riskier but lucrative asset class. Thus, our corporate structure has been formulated to suit different investor groups and asset classes. Hence, we remain confident that our model would enable us to attract strategic global partners who would want to be part of the country’s capital markets.

Guardian Fund Management Limited (GFM) is registered with the Securities and Exchange Commission of Sri Lanka. GFM over the years has built an experienced team whereby competencies in all aspects of

ANNUAL REPORT 2012/13 3

fund management have been addressed. Our model puts emphasis on fundamental style investing, driven by research. All company portfolios are currently managed by GFM and competencies have been expanded by way of growth in AUM internally and externally by pitching for new client portfolios. In managing external client and mutual funds, GFM leverages the expertise it has built on managing its own proprietary funds, a unique advantage it has, as opposed to fund managers who only manage outsourced portfolios.

Future OutlookTaking a long term view of the development of capital markets in Sri Lanka, our strategy has extended our services to manage retail funds via our joint venture with Acuity Partners (Private) Limited (the investment banking arm of the HNB and DFCC Bank). We believe that in the long term this segment will grow, given the progression of the economy in the island and increase in national savings rate. Also our international fund “The Sri Lanka Fund” which caters to institutional investors, funds of fund investors and Sri Lankan diasporas has been slow to raise funds due to global challenges. However we believe that this space would attract investments in the future with credibility of its long track record and accreditation as a restricted investment scheme in Singapore. Currently GFM has built competencies in managing the fixed income asset class and believes that in the future it would become a core segment given build-up of cash generated through sales proceeds of the company.

Public and private partnership in developing Sri Lanka has been skewed towards more public sector participation in development programs, playing the role of infrastructure developer. However, the government has shown its long term commitment in attracting foreign direct investments by offering many concessions to attract investors and engaging the private sector in the development of Sri Lanka. Thus, we should see entrepreneurial capital flowing into the growth of the stock market. Also, as the country progresses, state-owned enterprises which account for significant economic activity are likely to get listed and thus support the depth of the capital markets in the country. We believe that bold steps such as this are required to make a significant change in the economic progress of the country. The Company is encouraged by the tax concessions granted for listed debt and other steps to widen the debt markets and the results have been immediately forthcoming with an array of debt issues coming into the market shortly afterwards.

Hence, we are not discouraged by the present volatile sentiment at the Colombo Bourse, nor are we overconfident of future expectations on the equity front. We remain practical and our investments would be guided on pure fundamentals. We believe many areas need to be addressed to bring confidence and economic progress to the country. Clear government policy is needed to take the country to the next level of sustained growth. The current challenges faced by Sri Lanka on its international standing will have to be managed to attract direct investments and build the platform for economic prosperity.

AcknowledgementsIn conclusion, I would like to thank the shareholders for the confidence placed in the management over the years and to the regulators for supporting our businesses. I would also like to thank the members of our staff for their untiring contribution; the Audit Committee, the Remuneration Committee and the Nomination Committee for their guidance; and lastly, my colleagues on the Board for their input. We believe that all our stakeholders would benefit and be part of the identified growth trajectory of the company.

(Sgd).Israel PaulrajChairman

Colombo18th June 2013

4 CEYLON INvESTMENT PLC

Managers’ Review

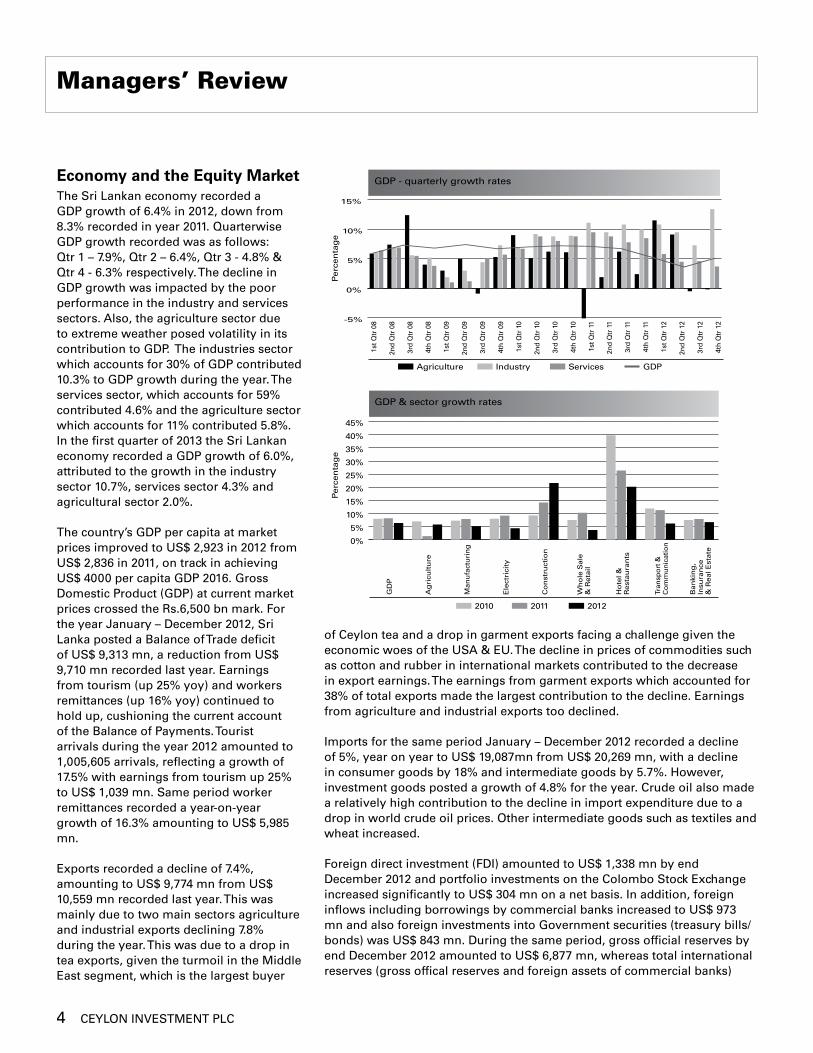

Economy and the Equity MarketThe Sri Lankan economy recorded a GDP growth of 6.4% in 2012, down from 8.3% recorded in year 2011. Quarterwise GDP growth recorded was as follows: Qtr 1 – 7.9%, Qtr 2 – 6.4%, Qtr 3 - 4.8% & Qtr 4 - 6.3% respectively. The decline in GDP growth was impacted by the poor performance in the industry and services sectors. Also, the agriculture sector due to extreme weather posed volatility in its contribution to GDP. The industries sector which accounts for 30% of GDP contributed 10.3% to GDP growth during the year. The services sector, which accounts for 59% contributed 4.6% and the agriculture sector which accounts for 11% contributed 5.8%. In the first quarter of 2013 the Sri Lankan economy recorded a GDP growth of 6.0%, attributed to the growth in the industry sector 10.7%, services sector 4.3% and agricultural sector 2.0%.

The country’s GDP per capita at market prices improved to US$ 2,923 in 2012 from US$ 2,836 in 2011, on track in achieving US$ 4000 per capita GDP 2016. Gross Domestic Product (GDP) at current market prices crossed the Rs.6,500 bn mark. For the year January – December 2012, Sri Lanka posted a Balance of Trade deficit of US$ 9,313 mn, a reduction from US$ 9,710 mn recorded last year. Earnings from tourism (up 25% yoy) and workers remittances (up 16% yoy) continued to hold up, cushioning the current account of the Balance of Payments. Tourist arrivals during the year 2012 amounted to 1,005,605 arrivals, reflecting a growth of 17.5% with earnings from tourism up 25% to US$ 1,039 mn. Same period worker remittances recorded a year-on-year growth of 16.3% amounting to US$ 5,985 mn.

Exports recorded a decline of 7.4%, amounting to US$ 9,774 mn from US$ 10,559 mn recorded last year. This was mainly due to two main sectors agriculture and industrial exports declining 7.8% during the year. This was due to a drop in tea exports, given the turmoil in the Middle East segment, which is the largest buyer

of Ceylon tea and a drop in garment exports facing a challenge given the economic woes of the USA & EU. The decline in prices of commodities such as cotton and rubber in international markets contributed to the decrease in export earnings. The earnings from garment exports which accounted for 38% of total exports made the largest contribution to the decline. Earnings from agriculture and industrial exports too declined.

Imports for the same period January – December 2012 recorded a decline of 5%, year on year to US$ 19,087mn from US$ 20,269 mn, with a decline in consumer goods by 18% and intermediate goods by 5.7%. However, investment goods posted a growth of 4.8% for the year. Crude oil also made a relatively high contribution to the decline in import expenditure due to a drop in world crude oil prices. Other intermediate goods such as textiles and wheat increased.

Foreign direct investment (FDI) amounted to US$ 1,338 mn by end December 2012 and portfolio investments on the Colombo Stock Exchange increased significantly to US$ 304 mn on a net basis. In addition, foreign inflows including borrowings by commercial banks increased to US$ 973 mn and also foreign investments into Government securities (treasury bills/bonds) was US$ 843 mn. During the same period, gross official reserves by end December 2012 amounted to US$ 6,877 mn, whereas total international reserves (gross offical reserves and foreign assets of commercial banks)

GDP - quarterly growth rates

-5%

0%

5%

10%

15%

Agriculture Industry Services GDP1s

t Qtr

08

2nd

Qtr

08

3rd

Qtr

08

4th

Qtr

08

1st Q

tr 0

9

2nd

Qtr

09

3rd

Qtr

09

4th

Qtr

09

1st Q

tr 1

0

2nd

Qtr

10

3rd

Qtr

10

4th

Qtr

10

1st Q

tr 1

1

2nd

Qtr

11

3rd

Qtr

11

4th

Qtr

11

1st Q

tr 1

2

2nd

Qtr

12

3rd

Qtr

12

4th

Qtr

12

Perc

en

tag

e

GDP & sector growth rates

2010 2011 2012

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

GD

P

Ag

ricu

ltu

re

Man

ufa

ctu

rin

g

Ele

ctri

city

Co

nst

ruct

ion

Wh

ole

Sale

&

Reta

il

Ho

tel &

Rest

au

ran

ts

Tran

spo

rt &

C

om

mu

nic

atio

n

Ban

kin

g,

Insu

ran

ce

& R

eal E

state

Perc

en

tag

e

ANNUAL REPORT 2012/13 5

amounted to US$ 8,357 mn equivalent to 5.2 months and 4.3 months of imports respectively.

Broad money (M2) recorded a yoy growth of 18.3% for the year 2012 in comparison to a year ago of 21.5%. This was due to restrictions imposed on credit to private sector. However, credit obtained by the public sector continued its momentum and caused broad money (M2b) to expand 17.5% during 2012. Average monthly credit expansion is about Rs. 25 bn down from the highs of Rs. 52 bn recorded in the peak of March 2012, where M2 growth was 35%. In the New Year, M2b expanded by 18.3% and M2 growth expanded by 15.5%.

The main policy interest rates of the Central Bank represented by the repurchase rate and the reverse repurchase rate remained the same at 7.50% and 9.50% respectively. Also, the statutory reserve ratio remained at 8.0%. However, it is a concern that even after relaxing monetary policy, interest rates on both deposit and lending rates still remain high.

Inflation measured by the yoy change in the Colombo Consumers Price Index (CCPI) decreased to 7.5% end March from a high of 9.8% in February 2013, up from 5.9% at end March 2012. Inflation on an annual average basis increased to 8.8% in March from 5.9% in March 2012. The annual average change continued to be maintained at single digit levels despite the drought experienced in the country. Meanwhile, core inflation increased to 6.4% on an annual average basis and 6.8% year on year basis. The contribution to monthly increase in the index came mainly from price increases in the food category. Within the non-food category, prices increased for water, electricity, furnishing & household while sub categories of transport, communication & education remained flat.

Dec 11 Mar 12 Jun 12 Sep 12 Dec 12 Mar 13

Treasury Bill 3M(%) 8.68 11.00 11.12 11.30 10.00 9.26

12M (%) 9.31 11.32 12.88 13.02 11.69 11.35

Call Money (%) 8.98 9.22 10.44 10.57 9.85 9.49

Prime Lending (%) 10.77 12.80 13.39 14.15 14.40 13.77

Market interest rates increased in 2012 as a result of tight monetary conditions. In the 3rd Qtr of 2012, call money rates increased to double digit levels of 10.57% but tapered off by end of the year. Also, on the Government

Securities front - the 3 month T-Bill rate closed the year at 10.0% (reaching a high of 11.44% in mid September), resulting in an increase of 132 basis points for the year and the 12 month T-Bill rate (peaked at 13.36% in mid September) closed the year at 11.69%, up 238 basis points for the year. Consequently, interest rates eased off in the New Year with T-Bill rates dropping to 9.10% (3 months) & 11.10% (12 months). However, the trend reversed in the month of March where interest rates were seen picking up. The government 2-5 year bonds are currently trading around 11.05% - 11.20% and 6 months to 1 year FD rates are in the region of 14%-14.25% (gross rate).

SLRs.Per unit as at 31/12/11

SLRs.Per unit as at 31/12/12

SLRs.Per unit as at 31/03/13

App./(Dep) for calendar Yr 2012

US $ 113.95 127.05 126.89 -11.50%

STG 175.59 204.59 192.07 -16.52%

Euro 147.48 168.13 162.13 -14.00%

Yen 1.47 1.47 1.35 0.00%

After the aggressive currency depreciation we saw at the beginning of the year in 2012, the dollar maintained and closed the year at Rs.127.05 (Dec 11 –SLRs.113.95) amounting to a depreciation of 11.50% for the calendar year 2012. The Rupee also depreciated against other major currencies such as the Sterling Pound (16.52%), Euro (14.00%) & Yen (0.00%).

We believe that low interest rates are imperative for positive capital market performance. Hence, for interest rates to remain low, inflationary pressures must ease which is unlikely given the recent hike in electricity tariffs. It poses a challenge to hold interest rates taking into account its cascading impact through the economy. Also, there is evidence of moral suasion to bring down interest rates with state banks reducing interest rates and persuading commercial banks to follow suit. Also, Government Securities rates coming down at the auctions is a way of representing the same. The current excess liquidity

Equity vs Fixed Income

0%2%4%6%8%

10%12%14%16%18%20%22%

010020030040050060070080090010001100

T.Bill - 3 months T.Bill - 12 months ASI Comp

Mar

-04

Sep

-04

Mar

-05

Sep

-05

Mar

-06

Sep

-06

Mar

-07

Sep

-07

Mar

-08

Sep

-08

Mar

-09

Sep

-09

Mar

-10

Sep

-10

Mar

-11

Sep

-11

Mar

-12

Sep

-12

Mar

-13

AS

I Co

mp

osi

te

Perc

en

tag

e

6 CEYLON INvESTMENT PLC

in the system is helping to momentarily bring down rates. However, to make an impact in the medium to long term, fiscal targets must be met. To achieve forecast GDP growth targets, momentum in the economy must be maintained and thus it’s vital to have low interest rates for credit growth. Weaker exchange rates too pose a challenge and growth in forex earnings is vital to strengthen the balance of payments.

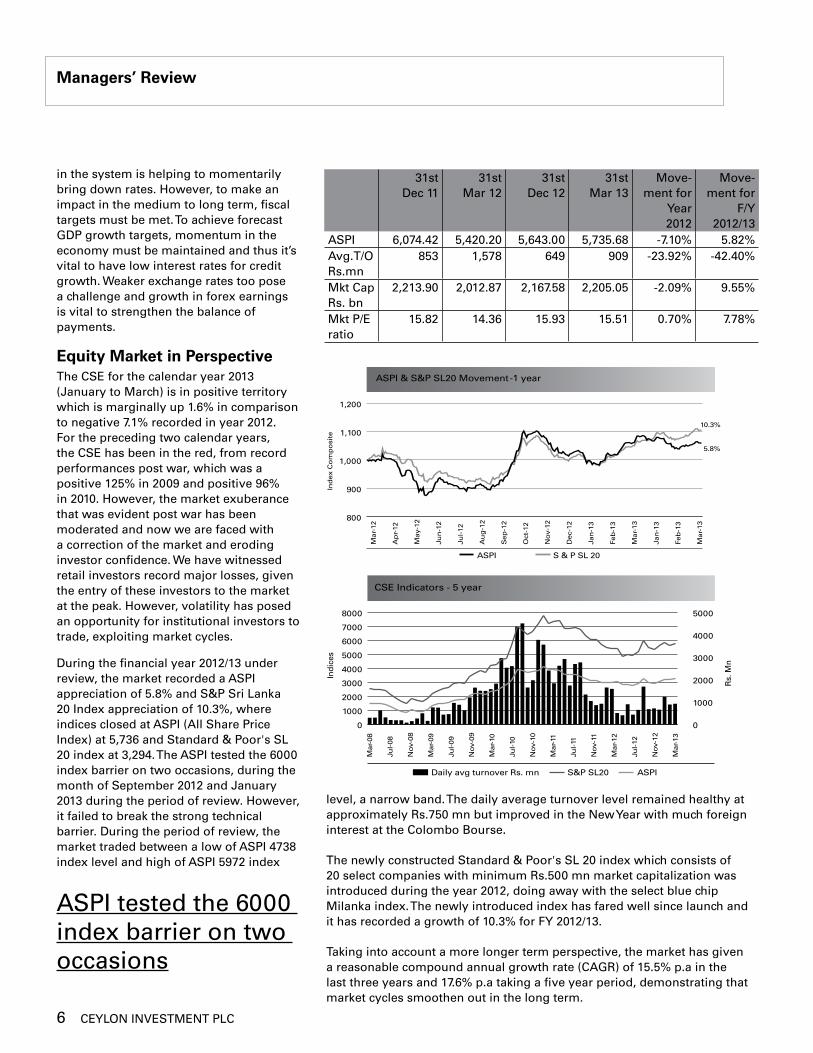

Equity Market in PerspectiveThe CSE for the calendar year 2013 (January to March) is in positive territory which is marginally up 1.6% in comparison to negative 7.1% recorded in year 2012. For the preceding two calendar years, the CSE has been in the red, from record performances post war, which was a positive 125% in 2009 and positive 96% in 2010. However, the market exuberance that was evident post war has been moderated and now we are faced with a correction of the market and eroding investor confidence. We have witnessed retail investors record major losses, given the entry of these investors to the market at the peak. However, volatility has posed an opportunity for institutional investors to trade, exploiting market cycles.

During the financial year 2012/13 under review, the market recorded a ASPI appreciation of 5.8% and S&P Sri Lanka 20 Index appreciation of 10.3%, where indices closed at ASPI (All Share Price Index) at 5,736 and Standard & Poor's SL 20 index at 3,294. The ASPI tested the 6000 index barrier on two occasions, during the month of September 2012 and January 2013 during the period of review. However, it failed to break the strong technical barrier. During the period of review, the market traded between a low of ASPI 4738 index level and high of ASPI 5972 index

Managers’ Review

CSE Indicators - 5 year

Daily avg turnover Rs. mn S&P SL20 ASPI

Mar

-09

No

v-08

Jul-

08

Mar

-08

Jul-

09

No

v-09

Mar

-10

Jul-

10

No

v-10

Mar

-11

Jul-

11

No

v-11

Mar

-12

Jul-

12

No

v-12

Mar

-13

Rs.

Mn

Ind

ices

0

1000

2000

3000

4000

5000

0

1000

2000

3000

4000

5000

6000

7000

8000

ASPI & S&P SL20 Movement -1 year

ASPI S & P SL 20

Mar-

12

Ind

ex C

om

po

site

Ap

r-12

May-

12

Jun

-12

Jul-

12

Au

g-1

2

Sep

-12

Oct

-12

No

v-12

Dec-

12

Jan

-13

Feb

-13

Mar-

13

800

900

1,000

1,100

1,200

5.8%

10.3%

Jan

-13

Feb

-13

Mar-

13

level, a narrow band. The daily average turnover level remained healthy at approximately Rs.750 mn but improved in the New Year with much foreign interest at the Colombo Bourse.

The newly constructed Standard & Poor's SL 20 index which consists of 20 select companies with minimum Rs.500 mn market capitalization was introduced during the year 2012, doing away with the select blue chip Milanka index. The newly introduced index has fared well since launch and it has recorded a growth of 10.3% for FY 2012/13.

Taking into account a more longer term perspective, the market has given a reasonable compound annual growth rate (CAGR) of 15.5% p.a in the last three years and 17.6% p.a taking a five year period, demonstrating that market cycles smoothen out in the long term.

ASPI tested the 6000 index barrier on two occasions

31st Dec 11

31st Mar 12

31st Dec 12

31st Mar 13

Move- ment for

Year2012

Move-ment for

F/Y 2012/13

ASPI 6,074.42 5,420.20 5,643.00 5,735.68 -7.10% 5.82%Avg.T/O Rs.mn

853 1,578 649 909 -23.92% -42.40%

Mkt Cap Rs. bn

2,213.90 2,012.87 2,167.58 2,205.05 -2.09% 9.55%

Mkt P/E ratio

15.82 14.36 15.93 15.51 0.70% 7.78%

ANNUAL REPORT 2012/13 7

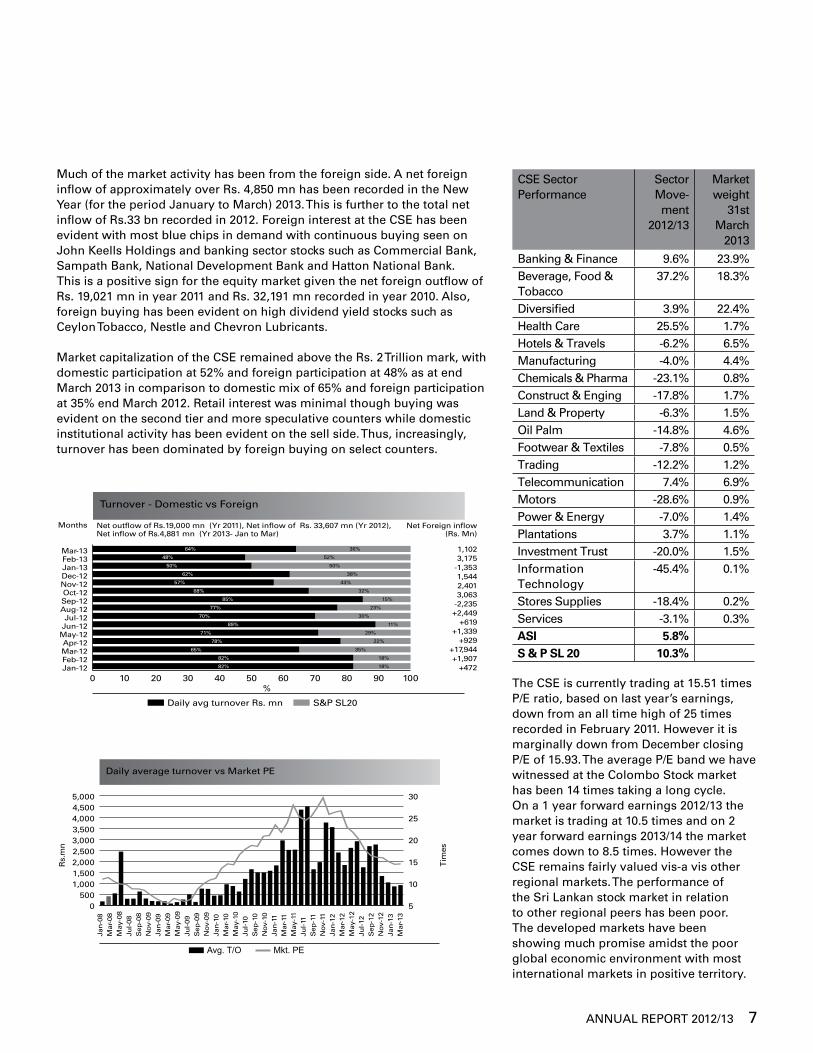

Much of the market activity has been from the foreign side. A net foreign inflow of approximately over Rs. 4,850 mn has been recorded in the New Year (for the period January to March) 2013. This is further to the total net inflow of Rs.33 bn recorded in 2012. Foreign interest at the CSE has been evident with most blue chips in demand with continuous buying seen on John Keells Holdings and banking sector stocks such as Commercial Bank, Sampath Bank, National Development Bank and Hatton National Bank. This is a positive sign for the equity market given the net foreign outflow of Rs. 19,021 mn in year 2011 and Rs. 32,191 mn recorded in year 2010. Also, foreign buying has been evident on high dividend yield stocks such as Ceylon Tobacco, Nestle and Chevron Lubricants.

Market capitalization of the CSE remained above the Rs. 2 Trillion mark, with domestic participation at 52% and foreign participation at 48% as at end March 2013 in comparison to domestic mix of 65% and foreign participation at 35% end March 2012. Retail interest was minimal though buying was evident on the second tier and more speculative counters while domestic institutional activity has been evident on the sell side. Thus, increasingly, turnover has been dominated by foreign buying on select counters.

CSE Sector Performance

Sector Move-ment

2012/13

Market weight

31st March

2013

Banking & Finance 9.6% 23.9%Beverage, Food & Tobacco

37.2% 18.3%

Diversified 3.9% 22.4%Health Care 25.5% 1.7%Hotels & Travels -6.2% 6.5%Manufacturing -4.0% 4.4%Chemicals & Pharma -23.1% 0.8%Construct & Enging -17.8% 1.7%Land & Property -6.3% 1.5%Oil Palm -14.8% 4.6%Footwear & Textiles -7.8% 0.5%Trading -12.2% 1.2%Telecommunication 7.4% 6.9%Motors -28.6% 0.9%Power & Energy -7.0% 1.4%Plantations 3.7% 1.1%Investment Trust -20.0% 1.5%Information Technology

-45.4% 0.1%

Stores Supplies -18.4% 0.2%Services -3.1% 0.3%ASI 5.8%S & P SL 20 10.3%

The CSE is currently trading at 15.51 times P/E ratio, based on last year’s earnings, down from an all time high of 25 times recorded in February 2011. However it is marginally down from December closing P/E of 15.93. The average P/E band we have witnessed at the Colombo Stock market has been 14 times taking a long cycle. On a 1 year forward earnings 2012/13 the market is trading at 10.5 times and on 2 year forward earnings 2013/14 the market comes down to 8.5 times. However the CSE remains fairly valued vis-a vis other regional markets. The performance of the Sri Lankan stock market in relation to other regional peers has been poor. The developed markets have been showing much promise amidst the poor global economic environment with most international markets in positive territory.

Turnover - Domestic vs Foreign

Daily avg turnover Rs. mn S&P SL20

0 10 20 30 40 50 60 70 80 90 100Jan-12Feb-12Mar-12Apr-12

May-12Jun-12Jul-12

Aug-12Sep-12Oct-12

Nov-12Dec-12Jan-13Feb-13Mar-13

Net out�ow of Rs.19,000 mn (Yr 2011), Net in�ow of Rs. 33,607 mn (Yr 2012), Net in�ow of Rs.4,881 mn (Yr 2013- Jan to Mar)

1,102

-1,3533,175

1,5442,4013,063

-2,235+2,449

+619+1,339

+929+17,944+1,907

+472

Net Foreign in�ow(Rs. Mn)

Months

%

18%82%

64%

48%

50%

62%

57%

68%

85%

77%

70%

89%

71%

78%

65%

82%

36%

52%

50%

38%

43%

32%

15%

23%

30%

11%

29%

22%

35%

18%

0500

1,0001,5002,0002,5003,0003,5004,0004,5005,000

Daily average turnover vs Market PE

Avg. T/O

Jan

-08

Mar

-08

May

-08

Jul-

08S

ep-0

8N

ov-

09Ja

n-0

9 M

ar-0

9M

ay-0

9Ju

l-09

Sep

-09

No

v-09

Jan

-10

Mar

-10

May

-10

Jul-

10S

ep-1

0N

ov-

10Ja

n-1

1 M

ar-1

1M

ay-1

1Ju

l-11

Sep

-11

No

v-11

Jan

-12

Mar

-12

May

-12

Jul-

12S

ep-1

2N

ov-

12Ja

n-1

3 M

ar-1

3

Tim

es

Rs.

mn

5

10

15

20

25

30

Mkt. PE

8 CEYLON INvESTMENT PLC

Managers’ Review

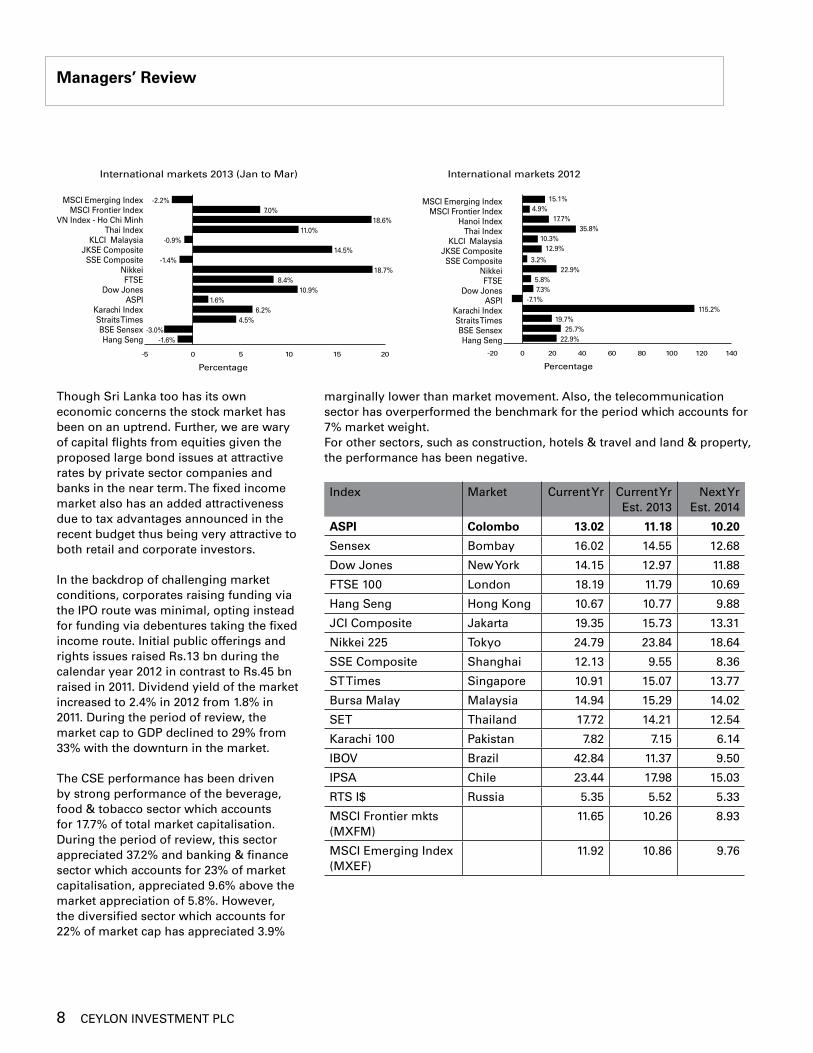

Though Sri Lanka too has its own economic concerns the stock market has been on an uptrend. Further, we are wary of capital flights from equities given the proposed large bond issues at attractive rates by private sector companies and banks in the near term. The fixed income market also has an added attractiveness due to tax advantages announced in the recent budget thus being very attractive to both retail and corporate investors.

In the backdrop of challenging market conditions, corporates raising funding via the IPO route was minimal, opting instead for funding via debentures taking the fixed income route. Initial public offerings and rights issues raised Rs.13 bn during the calendar year 2012 in contrast to Rs.45 bn raised in 2011. Dividend yield of the market increased to 2.4% in 2012 from 1.8% in 2011. During the period of review, the market cap to GDP declined to 29% from 33% with the downturn in the market.

The CSE performance has been driven by strong performance of the beverage, food & tobacco sector which accounts for 17.7% of total market capitalisation. During the period of review, this sector appreciated 37.2% and banking & finance sector which accounts for 23% of market capitalisation, appreciated 9.6% above the market appreciation of 5.8%. However, the diversified sector which accounts for 22% of market cap has appreciated 3.9%

marginally lower than market movement. Also, the telecommunication sector has overperformed the benchmark for the period which accounts for 7% market weight. For other sectors, such as construction, hotels & travel and land & property, the performance has been negative.

Index Market Current Yr Current Yr Est. 2013

Next Yr Est. 2014

ASPI Colombo 13.02 11.18 10.20

Sensex Bombay 16.02 14.55 12.68

Dow Jones New York 14.15 12.97 11.88

FTSE 100 London 18.19 11.79 10.69

Hang Seng Hong Kong 10.67 10.77 9.88

JCI Composite Jakarta 19.35 15.73 13.31

Nikkei 225 Tokyo 24.79 23.84 18.64

SSE Composite Shanghai 12.13 9.55 8.36

ST Times Singapore 10.91 15.07 13.77

Bursa Malay Malaysia 14.94 15.29 14.02

SET Thailand 17.72 14.21 12.54

Karachi 100 Pakistan 7.82 7.15 6.14

IBOv Brazil 42.84 11.37 9.50

IPSA Chile 23.44 17.98 15.03

RTS I$ Russia 5.35 5.52 5.33

MSCI Frontier mkts (MXFM)

11.65 10.26 8.93

MSCI Emerging Index (MXEF)

11.92 10.86 9.76

International markets 2013 (Jan to Mar)

-5 0 5 10 15 20

Hang SengBSE Sensex

Straits TimesKarachi Index

ASPIDow Jones

FTSENikkei

SSE CompositeJKSE Composite

KLCI MalaysiaThai Index

VN Index - Ho Chi MinhMSCI Frontier Index

MSCI Emerging Index

-1.6%-3.0%

4.5%6.2%

1.6%10.9%

8.4%18.7%

-1.4%14.5%

-0.9%11.0%

18.6%7.0%

-2.2%

Percentage

International markets 2012

-20 0 20 40 60 80 100 120 140

Hang SengBSE Sensex

Straits TimesKarachi Index

ASPIDow Jones

FTSENikkei

SSE CompositeJKSE Composite

KLCI MalaysiaThai Index

Hanoi IndexMSCI Frontier Index

MSCI Emerging Index

22.9%25.7%

19.7%115.2%

-7.1%7.3%5.8%

22.9%3.2%

12.9%10.3%

35.8%17.7%

4.9%15.1%

Percentage

ANNUAL REPORT 2012/13 9

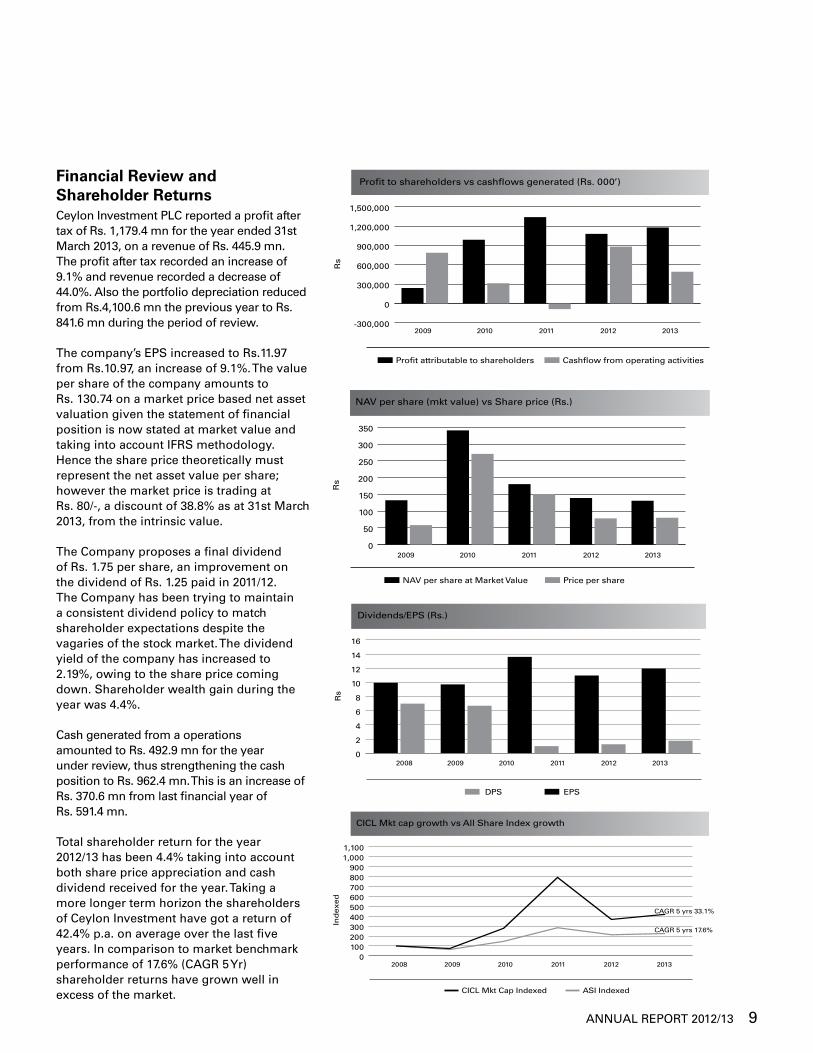

Financial Review and Shareholder ReturnsCeylon Investment PLC reported a profit after tax of Rs. 1,179.4 mn for the year ended 31st March 2013, on a revenue of Rs. 445.9 mn. The profit after tax recorded an increase of 9.1% and revenue recorded a decrease of 44.0%. Also the portfolio depreciation reduced from Rs.4,100.6 mn the previous year to Rs. 841.6 mn during the period of review.

The company’s EPS increased to Rs.11.97 from Rs.10.97, an increase of 9.1%. The value per share of the company amounts to Rs. 130.74 on a market price based net asset valuation given the statement of financial position is now stated at market value and taking into account IFRS methodology. Hence the share price theoretically must represent the net asset value per share; however the market price is trading at Rs. 80/-, a discount of 38.8% as at 31st March 2013, from the intrinsic value.

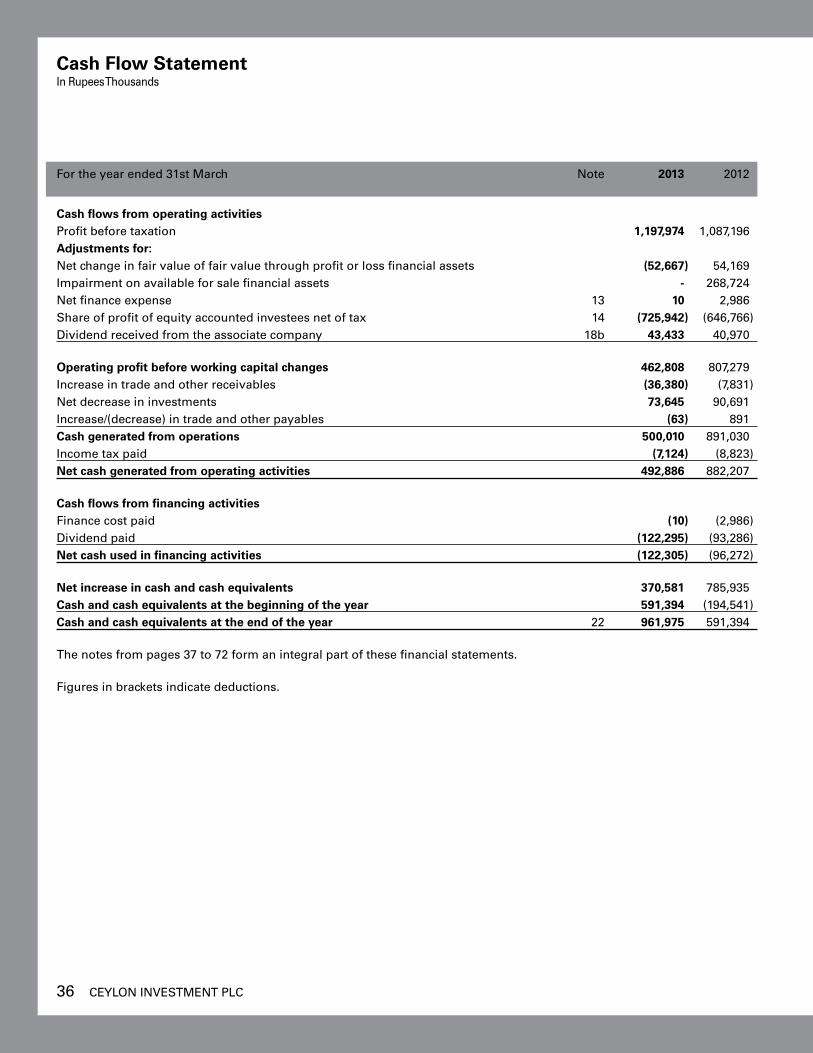

The Company proposes a final dividend of Rs. 1.75 per share, an improvement on the dividend of Rs. 1.25 paid in 2011/12. The Company has been trying to maintain a consistent dividend policy to match shareholder expectations despite the vagaries of the stock market. The dividend yield of the company has increased to 2.19%, owing to the share price coming down. Shareholder wealth gain during the year was 4.4%.

Cash generated from a operations amounted to Rs. 492.9 mn for the year under review, thus strengthening the cash position to Rs. 962.4 mn. This is an increase of Rs. 370.6 mn from last financial year of Rs. 591.4 mn.

Total shareholder return for the year 2012/13 has been 4.4% taking into account both share price appreciation and cash dividend received for the year. Taking a more longer term horizon the shareholders of Ceylon Investment have got a return of 42.4% p.a. on average over the last five years. In comparison to market benchmark performance of 17.6% (CAGR 5 Yr) shareholder returns have grown well in excess of the market.

Pro�t to shareholders vs cash�ows generated (Rs. 000’)

Pro�t attributable to shareholders Cash�ow from operating activities

2009 2010 2011 2012 2013R

s

-300,000

0

300,000

600,000

900,000

1,200,000

1,500,000

Dividends/EPS (Rs.)

DPS EPS

2008 2009 2010 2011 201320120

2

4

6

8

10

12

14

16

Rs

CICL Mkt cap growth vs All Share Index growth

CICL Mkt Cap Indexed ASI Indexed

2008 2009 2010 2011 2012 20130

100200300400500600700800900

1,0001,100

CAGR 5 yrs 33.1%

CAGR 5 yrs 17.6%

Ind

exed

NAV per share (mkt value) vs Share price (Rs.)

NAV per share at Market Value Price per share

2009 2010 2011 2012 2013

Rs

0

50

100

150

200

250

300

350

10 CEYLON INvESTMENT PLC

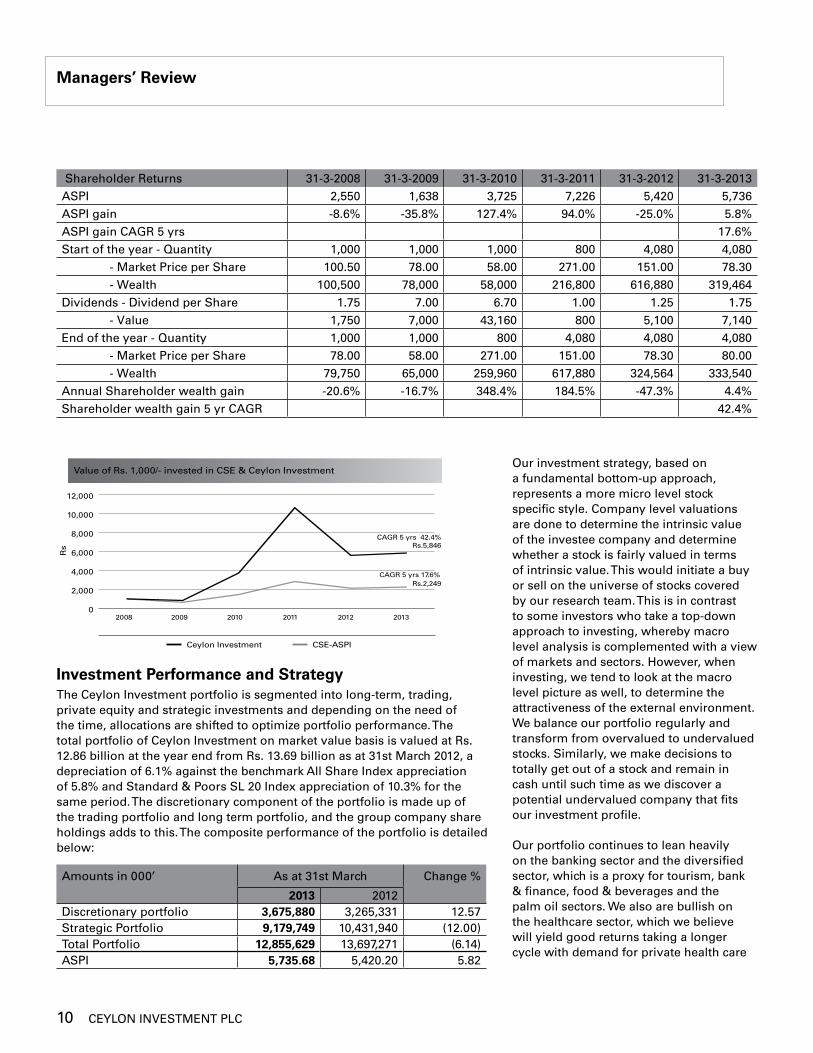

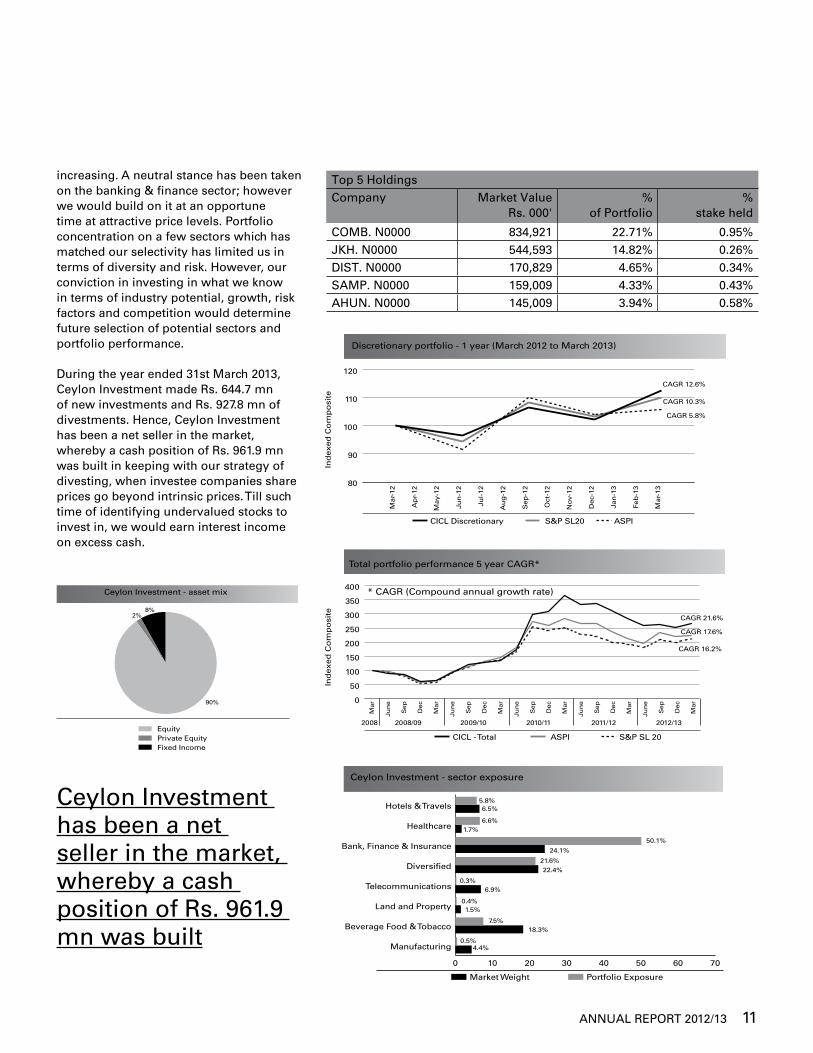

Investment Performance and StrategyThe Ceylon Investment portfolio is segmented into long-term, trading, private equity and strategic investments and depending on the need of the time, allocations are shifted to optimize portfolio performance. The total portfolio of Ceylon Investment on market value basis is valued at Rs. 12.86 billion at the year end from Rs. 13.69 billion as at 31st March 2012, a depreciation of 6.1% against the benchmark All Share Index appreciation of 5.8% and Standard & Poors SL 20 Index appreciation of 10.3% for the same period. The discretionary component of the portfolio is made up of the trading portfolio and long term portfolio, and the group company share holdings adds to this. The composite performance of the portfolio is detailed below:

Amounts in 000’ As at 31st March Change %

2013 2012Discretionary portfolio 3,675,880 3,265,331 12.57 Strategic Portfolio 9,179,749 10,431,940 (12.00)Total Portfolio 12,855,629 13,697,271 (6.14)ASPI 5,735.68 5,420.20 5.82

Our investment strategy, based on a fundamental bottom-up approach, represents a more micro level stock specific style. Company level valuations are done to determine the intrinsic value of the investee company and determine whether a stock is fairly valued in terms of intrinsic value. This would initiate a buy or sell on the universe of stocks covered by our research team. This is in contrast to some investors who take a top-down approach to investing, whereby macro level analysis is complemented with a view of markets and sectors. However, when investing, we tend to look at the macro level picture as well, to determine the attractiveness of the external environment. We balance our portfolio regularly and transform from overvalued to undervalued stocks. Similarly, we make decisions to totally get out of a stock and remain in cash until such time as we discover a potential undervalued company that fits our investment profile.

Our portfolio continues to lean heavily on the banking sector and the diversified sector, which is a proxy for tourism, bank & finance, food & beverages and the palm oil sectors. We also are bullish on the healthcare sector, which we believe will yield good returns taking a longer cycle with demand for private health care

Managers’ Review

Shareholder Returns 31-3-2008 31-3-2009 31-3-2010 31-3-2011 31-3-2012 31-3-2013 ASPI 2,550 1,638 3,725 7,226 5,420 5,736 ASPI gain -8.6% -35.8% 127.4% 94.0% -25.0% 5.8%ASPI gain CAGR 5 yrs 17.6%Start of the year - Quantity 1,000 1,000 1,000 800 4,080 4,080 - Market Price per Share 100.50 78.00 58.00 271.00 151.00 78.30 - Wealth 100,500 78,000 58,000 216,800 616,880 319,464Dividends - Dividend per Share 1.75 7.00 6.70 1.00 1.25 1.75 - value 1,750 7,000 43,160 800 5,100 7,140 End of the year - Quantity 1,000 1,000 800 4,080 4,080 4,080 - Market Price per Share 78.00 58.00 271.00 151.00 78.30 80.00 - Wealth 79,750 65,000 259,960 617,880 324,564 333,540 Annual Shareholder wealth gain -20.6% -16.7% 348.4% 184.5% -47.3% 4.4%Shareholder wealth gain 5 yr CAGR 42.4%

Value of Rs. 1,000/- invested in CSE & Ceylon Investment

Ceylon Investment CSE-ASPI

2008 2009 2010 2011 2012 20130

2,000

4,000

6,000

8,000

10,000

12,000

CAGR 5 yrs 42.4%

CAGR 5 yrs 17.6%

Rs Rs.5,846

Rs.2,249

ANNUAL REPORT 2012/13 11

increasing. A neutral stance has been taken on the banking & finance sector; however we would build on it at an opportune time at attractive price levels. Portfolio concentration on a few sectors which has matched our selectivity has limited us in terms of diversity and risk. However, our conviction in investing in what we know in terms of industry potential, growth, risk factors and competition would determine future selection of potential sectors and portfolio performance.

During the year ended 31st March 2013, Ceylon Investment made Rs. 644.7 mn of new investments and Rs. 927.8 mn of divestments. Hence, Ceylon Investment has been a net seller in the market, whereby a cash position of Rs. 961.9 mn was built in keeping with our strategy of divesting, when investee companies share prices go beyond intrinsic prices. Till such time of identifying undervalued stocks to invest in, we would earn interest income on excess cash.

Ceylon Investment - sector exposure

Market Weight Portfolio Exposure

0 10 20 30 40 50 60 70

Manufacturing

Beverage Food & Tobacco

Land and Property

Telecommunications

Diversi�ed

Bank, Finance & Insurance

Healthcare

Hotels & Travels

0%

5.8%6.5%

6.6%1.7%

50.1%

24.1%

21.6%22.4%

0.3%6.9%

0.4%1.5%

7.5%18.3%

0.5%4.4%

Top 5 HoldingsCompany Market value

Rs. 000' %

of Portfolio%

stake held

COMB. N0000 834,921 22.71% 0.95%JKH. N0000 544,593 14.82% 0.26%DIST. N0000 170,829 4.65% 0.34%SAMP. N0000 159,009 4.33% 0.43%AHUN. N0000 145,009 3.94% 0.58%

Total portfolio performance 5 year CAGR*

CICL - Total ASPI S&P SL 20

0

50

100

150

200

250

300

350

400

Mar

Jun

e

Sep

Dec

Mar

Jun

e

Sep

Dec

Mar

Jun

e

Sep

Dec

Mar

Jun

e

Sep

Dec

Mar

Jun

e

Sep

Dec

Mar

2008/09 2009/10 2010/11 2011/12 2012/13

CAGR 21.6%

CAGR 17.6%

CAGR 16.2%

2008

Ind

exed

Co

mp

osi

te

* CAGR (Compound annual growth rate)Ceylon Investment - asset mix

2%8%

90%

EquityPrivate EquityFixed Income

Ceylon Investment has been a net seller in the market, whereby a cash position of Rs. 961.9 mn was built

Discretionary portfolio - 1 year (March 2012 to March 2013)

CICL Discretionary S&P SL20 ASPI

Mar-

12

Ap

r-12

May-

12

Jun

-12

Jul-

12

Au

g-1

2

Sep

-12

Oct

-12

No

v-12

Dec-

12

Jan

-13

Feb

-13

Mar-

13

80

90

100

110

120

CAGR 12.6%

CAGR 10.3%

CAGR 5.8%

Ind

exed

Co

mp

osi

te

12 CEYLON INvESTMENT PLC

Managers’ Review

Profile of the Fund ManagersThe funds are managed by Guardian Fund Management Ltd (GFM), which is a fully owned subsidiary of the Guardian Group and is registered with the Securities and Exchange Commission of Sri Lanka. It manages the largest listed equity fund in Sri Lanka and has built up its competencies in the field of portfolio management, research and support services. GFM manages the Sri Lanka Fund which was formerly known as the Regent Sri Lanka Fund, established in 1993. However the fund was re-launched in August 2010 after the end to the 30 year civil war to exploit opportunities in raising foreign capital. The company has extended its business model to capture retail funds by managing unit trust funds via a joint venture partnership with Acuity Partners (Private) Limited. We recognize the growth potential of the mutual fund industry in Sri Lanka and yet feel its at an infancy stage, and therefore foresee increasing saving habits to drive investments amongst Sri Lankans. Our joint venture Guardian Acuity Asset Management will address those needs and structure investment schemes to meet varying demand.

The fund management company has a professional outfit set up with an effective compliance process, code of ethics & standards of professional conduct for employees. Hence, the structure has been set in place as a comprehensive fund management unit. Guardian Fund Management has expanded its operation by extending its fund management capabilities to companies outside the group and built a portfolio of external clients consisting of provident fund, pension funds, corporate clients and a country fund. To enable the management of external client funds, we have an independent compliance officer to monitor client interest and ensure that objectives are being met with the risk profile of the client. The AUM under this category has grown to a sizeable amount of Rs. 1.4 bn. The fund management company also built its capabilities in becoming a specialist in private equity, perfecting the style of evaluating, managing and structuring private equity deals. This is a long term business and very different to the investment expertise built in terms of listed investments.

In the year under review, GFM has expanded horizons in specializing in the fixed income asset class. As a result, research capabilities have been enhanced in detailing macro economic variables and forecasting, to support the fixed income side of business which is growing in AUM.

Our future viewInvestor sentiment at the Colombo bourse is likely to be mixed with strong interest from overseas and lukewarm interest on the domestic front. Aggressive foreign buying on heavyweight select counters has kept up a positive momentum. Retail interest is likely to come in when blue chip counters have rallied to second tier stocks and when interest rate momentum dries up.

We believe the catalyst to market performance would be the underlying corporate earnings of the companies. We remain skeptical about the ability of the companies to record above average growth due to low GDP growth targets and falling exports against the background of cautious investing by the private sector, amidst volatile interest and exchange rates. Furthermore, higher energy costs and rising wage bills will have a knock-on effect on investor confidence. Looking forward, we feel that the equity space might be crowded out with the pipeline of debentures in the market. Enticing investors to move funds to high yielding debentures given the perceived low risk return option, will prompt an asset class shift in 2013.

Despite uncertainties affecting the Colombo Bourse, we remain confident in the long term on the potential of equities. We at Ceylon Investment believe that equities offer above average returns in long cycles

Our portfolio continues to lean heavily on the banking sector and the diversified sector, which is a proxy for tourism, bank & finance, food & beverages and the palm oil sectors

ANNUAL REPORT 2012/13 13

The ASPI will test the 6000 technical barrier in the New Year, but for this to happen, the largest market cap stocks need to demonstrate performance. Also, the heavyweight banking sector needs to hold its ground. We do not foresee any major IPO's entering the market in the coming months. However, the alternate asset class of debt issuances is to be active, given the new tax incentives making it very attractive to investors.

Despite uncertainties clouding the Colombo Bourse, we remain confident in the long term on the potential of equities. We at Ceylon Investment believe that equities offer above average returns in long cycles and hence are not reluctant to commit long term capital in good companies at attractive price levels. At present, the CSE is trading at 15.5 times, relatively valued in comparison to other Asian markets and frontier markets. However, on a 1 year forward earnings, the market is at a P/E ratio of 10.5 times and 2 year forward earnings at a P/E of 9.0 times. Hence, we are of the view that the market offers value in the medium term.

Guardian Fund Management LimitedInvestment Managers

Colombo18 June 2013

14 CEYLON INvESTMENT PLC

Risk Management

Risk management is an integral part of our business, particularly since balancing risks against returns is a critical trade off decision we have to make everyday when it comes to making investment decisions. We recognise the importance of risk management and have built a comprehensive risk management process & structure that focuses on continuous identification and management of business risks. We have in place several measures to strengthen our risk management processes which are linked to our daily investment decisions. These include policies to mitigate business risks along with the upgrading of the support systems that enable easy monitoring and management of risks.

We believe that risk management is of paramount importance in safeguarding the interest of all stakeholders and have undertaken a comprehensive review to enhance the risk mitigating processes already set in place by Guardian Fund Management Limited, the investment managers of the Company.

We see risk management not as an effort to eliminate risk, but as managing risk given certain risk tolerance levels set by the company. Risks appropriate for a particular portfolio will be assessed against the risk preferences of the investor and overall portfolio strategy.

The risk management structure in placeGuardian Fund Management (GFM) has been set up as an independent fund management company and the management of the portfolios of the Ceylon Guardian Group has been delegated to this company. The Board of Directors has formulated and approved an investment framework and control limits for GFM’s fund management operation. GFM’s management team is responsible for the recommendation and execution of the investment decisions, during the course of which oversight and management of the business, financial and operational risks of the company come into play.

The Fund Manager (GFM) has been registered as an Investment Manager with the Securities and Exchange Commission of Sri Lanka since 2006 while Ceylon Guardian Investment Trust PLC and its subsidiary Ceylon Investment PLC have been registered as underwriters since 2009. GFM as well as the Company therefore, come under the purview of the capital market regulator and hence internal monitoring is done on a quarterly basis to ensure that the set regulations are adhered to. Audits by the Securities and Exchange Commission may also be carried out as required. Furthermore, as a listed company it

conforms to the listing rules and guidelines of the Colombo Stock Exchange.

The Board of Directors of the company have ultimate responsibility for risk management. Hence the Boards are supported by an organization structure that covers the entire risk management framework through an independent Compliance Officer who functions within GFM, as well as the internal audit function of the Carson Cumberbatch Group to which the Ceylon Guardian Group companies belong. The Audit Committee of the Company has oversight over the financial reporting function of the company, the system of internal controls; as well as the audit, compliance and risk management processes. Further, an Investment Committee drawn from across the Carsons Group directorate provide advice and insights to the fund management team to further sharpen and refine their decision making process. This organization structure determines the objectives and policies of our risk management framework and promotes a culture of risk awareness and balanced risk-taking within the company.

Risk categoriesCeylon Guardian has identified and categorized its risks into 4 categories, namely macro environmental risks, portfolio risks, regulatory risks and operational risks. Given below is its approach in managing these key risk areas.

Macro environmental risksCountry risksCountry risk is applicable if an investment is made in a security issued by an entity subject to foreign laws or if transactions are entered into in markets in other jurisdictions. The sums invested and profits or returns accruing maybe subject to exchange control regulations, currency fluctuations, transaction costs & taxes and other actions that may be imposed by the government or policy making bodies of the said countries.

This risk is not currently applicable to the Guardian Group as our exposure at present is only to Sri Lankan investments. Hence no risk mitigating systems are required to be in place. However, since the capital account has now been liberalised to the extent of permitting approved overseas investments upto a certain value by listed companies, this is a new risk that we would have to build into our framework into the future.

Currency riskWhere investments are denominated in currencies other than our primary reference currency which is the

ANNUAL REPORT 2012/13 15

Sri Lanka Rupee, and where the company is required to convert funds from one currency to another upon making investments, as well as in receiving the returns from those investments, the company is exposed to the risk of the foreign exchange parities moving against one’s investment.

This risk is not currently applicable to the Guardian Group as the current exposure to investments denominated in foreign currencies is nil. Hence no risk mitigating processes are required; but looking ahead we need to prepare for this due to the gradual exchange control de-regulation that is now taking place. A detailed investment policy would be developed in the year ahead in gaining exposure to new markets.

Market risk - domesticThe broad definition of market risk is exposure to adverse movements in the securities markets for both equity and fixed income investments, which can result in value loss as well as variations in the anticipated returns from those securities. All financial institutions face market risks, created by changes in the macro environment related to political factors, national security, economic management and globalization influences which have an impact on systematic risk factors such as interest rates, currency parity, inflation, and availability of credit. Therefore, understanding market risks requires considering multiple dimensions and complexity in the macro environment.

Market risks are inherent in every security and are thus collectively considered at the portfolio level to take into account the asset allocation decisions of the portfolio. Thus market risks affecting a particular class of security are mitigated by switching to asset classes that are assessed to be less risky in a particular scenario.

All market participants such as Ceylon Investment should ideally develop its business model taking into account exposure limits and parameters to sustain itself when faced with market risks that can affect portfolio values temporarily. The only mitigating process is to develop a sound research base to determine changing economic fundamentals of the country and determine the impact on equity vs fixed income investments and the prompt shifting of funds between asset classes. This is of vital importance in trading portfolio decisions where quick encashment of equities is carried out if macro indicators move adversely leading to a slow down in stock market activity.

The process of assessing market risks on investee companies also forms a vital part of our research process, where sensitivity of stock valuations to changes in economic indicators are monitored.

Market risk - international and externalThese risks cannot be diversified or mitigated by the company. We as investors in the equity market in Sri Lanka have to live with the risk of international happenings affecting our market. There is an indirect impact of risks of other markets to our domestic market as clearly seen in the past with the spiraling impacts of the global financial crisis spreading to other Western countries and impacting Asian countries and in turn Sri Lanka.

In the global world of cross border trade and cross border investment flows, the impact of changing economic indicators and policy will be high for the domestic economy, especially in a country such as ours which is import dependent for vital commodities.

Hence in determining fund strategy we monitor key economic indicators such as interest rates, exchange rates, inflation, budget deficits of key economic super powers, as well as global commodity prices since Sri Lanka is a net importer of essential commodities. This enables the fund team to get a feel of changing international market dynamics and in turn relate that to local developments. The entry and exit of foreign investor interest on the local market is also determined by the macro economic trends prevailing in foreign markets and relative valuations of our market vis-a-vis developed and other comparative Asian markets. Information to monitor and interpret global developments in capital markets is vital to assess and mitigate this risk.

We believe that building expertise in foreign markets is of paramount importance going forward with possible further liberalisation on the cards. In mitigating the risk we are looking to tie up or collaborate with foreign entities that have expertise in such markets at such times when we have the ability to invest overseas.

Portfolio RisksGeneral Securities riskAny trading in securities carries inherent investment risks associated with the entity issuing those securities. In particular the price or value of any security can and does fluctuate and may even become valueless, resulting in possible loss not only of returns and profits, but even also of all or part of the principal sums invested in the case of a fixed income instrument. These risks arise as a result of the overall risks faced by the issuing entity which affects its ability to provide a return to the investors holding the securities issued by it. Particularly in the case of equities, past performance of any investment is not necessarily indicative of future performance. At Guardian

16 CEYLON INvESTMENT PLC

Risk Management

our approach focuses on the fact that there is no substitute for fundamental security assessment. Our portfolio management and investment selection process is designed to maximize the risk/return tradeoff to our shareholders and we employ a bottom up investment selection process.

Our risk mitigating methodology is based on our internal research process that has added value over time to our choice of investments. Prospective investments are selected from fundamental analysis and contact with corporate management of the issuing company through company visits. Once an investment is made, a continuous process of monitoring the performance of that investment is adopted.

We manage the concentration risk arising from over exposure to one security by monitoring sector exposure and single company exposure as mitigation strategies. Loss limits are set to monitor stocks performing below their cost of acquisition to determine whether temporary capital erosion is a concern. This helps us mitigate the downside risk of any security in the portfolio.

Liquidity riskUnder certain market conditions, an investor may find it difficult or impossible to liquidate a position. This can occur when trading is suspended by the exchange on which a security is listed or when poor market sentiment dries up investor interest in an investment. In addition, there may not be a ready market for certain investments due to low levels of publicly traded quantities. Some investments will have to be held to maturity. Proper information for determining the value of certain investments may also not be available under such circumstances of low liquidity. However the strategy of holding big stakes might be a limiting factor when selling, if the stock is illiquid or in the case of a change in fundamentals.

We mitigate this risk by investing in companies with a reasonable free float and where securities are heavily traded. Also by limiting the portfolio’s buy list to highly traded blue chips, the risk of illiquidity can be mitigated. Good research will enable the fund team to identify changes in fundamentals and be proactive in investment decision making.

In instances where we are presented with a promising investment opportunity, being short of funds to pursue that opportunity is also an extension of liquidity risk. A shortage may arise due to the inability of disposing existing positions with inferior risk/return trade off or the need to commit more money than available on hand to fully exploit the opportunity. To guard against this risk, we have

arranged several overdraft facilities, which have not been utilized as yet. However close monitoring of interest rate movements and liquidation of positions to cover overdrafts after 3-6 months exposure would be the risk mitigation methods used to ensure low exposure to interest rate risks.

Performance volatility risks The composition of portfolio investments will determine the portfolio’s ability to out perform the market. If more volatile stocks that respond more than proportionately to market movements are selected, there is a likelihood that the portfolio will outperform the benchmark All Share Price Index in a growing market, while in a downturn it can under-perform the market. It is once again an attempt at balancing good performance with a certain risk tolerance in a volatile environment.

Measuring portfolio volatility through calculation of a portfolio beta is one method of keeping ourselves aware of the sensitivities of the portfolio. In the case of the long term portfolio, we would not attempt to handle market volatility by encashing stocks, but would rather attempt to hold into fundamentally strong stocks and ride out low performing cycles. For this, we ensure adequate cash generation by way of dividend and other income flows to keep our daily operations running smoothly while we ride out low market periods. On the other hand, in the case of the trading portfolio, it is necessary to keep an even closer tab on market volatility, since it needs to regularly encash its profitable positions to remain a high performing portfolio.

Investment performance riskThis is the risk that the portfolio will not meet the investment objectives by over-performing the benchmark indices. This can adversely affect the reputation of the company and have impact in the future in terms of proven track record and confidence when raising money on future capital calls.

We mitigate this risk by setting a process which seeks to meet investment targets within stated risk parameters. Portfolio performance, valuations and risks are monitored by fund managers and managed on a regular basis.

Regulatory Risks Legal compliance The legal support services to Guardian Fund Management comes through the management services company of the Carson Cumberbatch Group, which ensures that the Guardian Group complies with all legal and regulatory provisions applicable to it. The legal function proactively identifies and advices GFM to set up appropriate systems

ANNUAL REPORT 2012/13 17

and processes for legal and regulatory compliance in respect of all our investments and regulated activities. We also ensure legal and regulatory compliance in any foreign country that we operate in, and in such instances through legal counsel retained in those environments.

Proactive monitoring of compliance process is followed and we see that our investments are made and trades are executed in keeping to the Companies Act, SEC regulations, tax regulations, exchange control regulations and other applicable guidelines. The legal advisors of the Company also carry out periodic awareness programmes to educate all staff members.

Regulatory ComplianceThe operations of the Guardian Group come within the rules and regulations applicable to all market participants operating in the equity (listed and unlisted) and debt markets of Sri Lanka, as well as the regulatory provisions applicable to companies listed on the CSE and regulations applicable to securities trading set by the Securities and Exchange Commission of Sri Lanka.

Our systems and processes are structured to satisfy the criteria set by these regulations, and staff is constantly kept aware of the compliance needs imposed by these regulations. An independent compliance officer undertakes responsibility for maintaining a check on the overall compliance process and he is supported by the internal audit function of the Carsons Group. GFM, as an Investment Manager registered with the SEC, is also subject to further regulation by the capital markets regulator.

Operational RisksProfessionalism in operational dealingsGuardian Fund Management (GFM) emphasizes professionalism in the manner in which the staff interacts with clients as well as market intermediaries, since it is vital for maintaining the company’s standing within the investment community. GFM staff has signed a Code of Ethics at the time of recruitment by the company, which lays down professional standards of conduct and dealing that is expected of staff. Structures to avoid conflicts of interest and compromising of best practices are set up. Staff education covers these areas of practice, and annual declarations by the staff members on compliance in personal equity trading are mandatory.

Compliance with SEC trading rules on insider trading, front running, market manipulation etc are checked by comparing trading statistics between portfolios and

pre-approved personal transaction of employees, by the Compliance Officer.

Compliance with the Code of Ethics ensures that the conduct of fund managers and other staff do not violate the code of ethics to which employees are signatories. Some of the areas that have been highlighted include avoiding conflict of interest between portfolios through coordination of trades between portfolio managers within the company, as well as internal controls and audits to ensure monitoring & compliance. .

Systems and process risksWe manage operational risks by identifying areas of risk, formulating plans for their management, promoting best practices, implementing internal controls and systems, and monitoring compliance with these internal guidelines for managing operational risks. Operational risks mainly cover the areas of system failure, continuity of decision making, dealing with contingencies and ensuring efficiency in operations and correct application of recommended management practices. Operational risk is the risk of loss resulting from inadequate or failed internal processes, people and systems or from external events.

In order to deal with unexpected contingencies, we have developed and implemented a business continuity plan, which looks after aspects such as staff deployment and systems backup in case of an unexpected disruption to the business. This business continuity plan forms a part of the Carsons Group’s business continuity plan, which is regularly tested.

The internal audit function of the Carsons Group, ensures the safeguarding of company assets and recommends process improvements in areas where process control failures are noted. Compliance with the investment objectives of each portfolio involves checking whether fund managers have adhered to the investment guidelines for each portfolio operating within set limits & not falling to prohibited investments; as well as monitoring portfolio performance against the benchmarks set. Further compliance with the operating process manual involves checking the application of proper internal controls such as segregation of duties, authority limits, approvals and that cash management processes are in order.

Systems support for the portfolio management software is made available through an annual maintenance agreement with the software vendor which ensures on line support for

18 CEYLON INvESTMENT PLC

Risk Management

system issues and queries. At the same time the financial transaction processing and reporting system are based on an ERP system in use at Carsons Group level and as such back up support services for this system are available through the parent company’s management services company.

Staff risksA fund management operational unit requires qualified professionals with experience in the fund management industry. Knowledge of the operating mechanism of the market as well as its norms and ethics is of importance. We attempt to pass on this valuable local knowledge to our staff at all levels. Having diversity in the team, developing a strong second level, training and development opportunities, are standard practices of the industry, which we benchmark ourselves with. A performance related incentive scheme for the staff is in place and is being reviewed. The networking ability of key staff source deals is important in running a successful fund management operation by being shown both important buy side and sell side deals by brokers.

The staff of GFM are all professionally qualified with a track record of experience in the industry. A strong research team has been developed to complement the fund management operation and raise the standard of the investment decision making process.

Staff training and development is identified as an important areas of concern, while retention is managed through a comprehensive reward structure & incentive scheme, opportunities for career progression and a culture of being HR oriented. Collectively, these steps help us work towards having an effective succession plan in place.

Reputation riskAs a company which carries out a role of trust between itself and a client, it is vital to safeguard the good name and reputation of the business. Further, now being in the public domain through unit trusts, safeguarding reputation risk is of utmost importance.

Employees are communicated the right values from the inception both by formal communication and by example. Our screening process at interviews, attempts to select people of the right caliber, while training them for higher responsibility is ongoing. The extensive compliance process also ensures that the company does not take the risk of process failure that will lead to reputation risk. Maintaining good relationships with all industry and government stakeholders further helps manage any crisis situations that can damage reputation.

Guardian Fund Management LimitedInvestment Managers

Colombo18 June 2013

ANNUAL REPORT 2012/13 19

Annual Report of the Board of Directors on the Affairs of the Company

The details set out herein provide the pertinent information required by the Companies Act, No. 07 of 2007, Listing Rules of the Colombo Stock Exchange and recommended best accounting practices. The Annual Report was approved by the Board of Directors on 18th June 2013.

1. GENERAL The Directors have pleasure in presenting to the

shareholders their report together with the audited financial statements for the year ended 31st March 2013 of Ceylon Investment PLC (the “Company”), a public limited liability company incorporated in Sri Lanka in 1919.

2. THE PRINCIPAL ACTIVITIES OF THE COMPANY

The principal activities of the Company and its associate company are to act as specialised investment vehicles focusing on listed equity investments, in order to better manage the risk profile of the portfolio to one specialized asset class.

There were no significant changes in the nature of the principal activities of the Company during the financial year under review.

3. REVIEw OF OPERATIONS AND FUTURE DEVELOPMENTS

The Chairman’s Statement and Managers’ Review on pages 2 to 13 provide an overall assessment of the business performance of the Company and its future developments. These reports together with the audited financial statements reflect the state of affairs of the Company.

4. FINANCIAL STATEMENTS The financial statements which comprise the

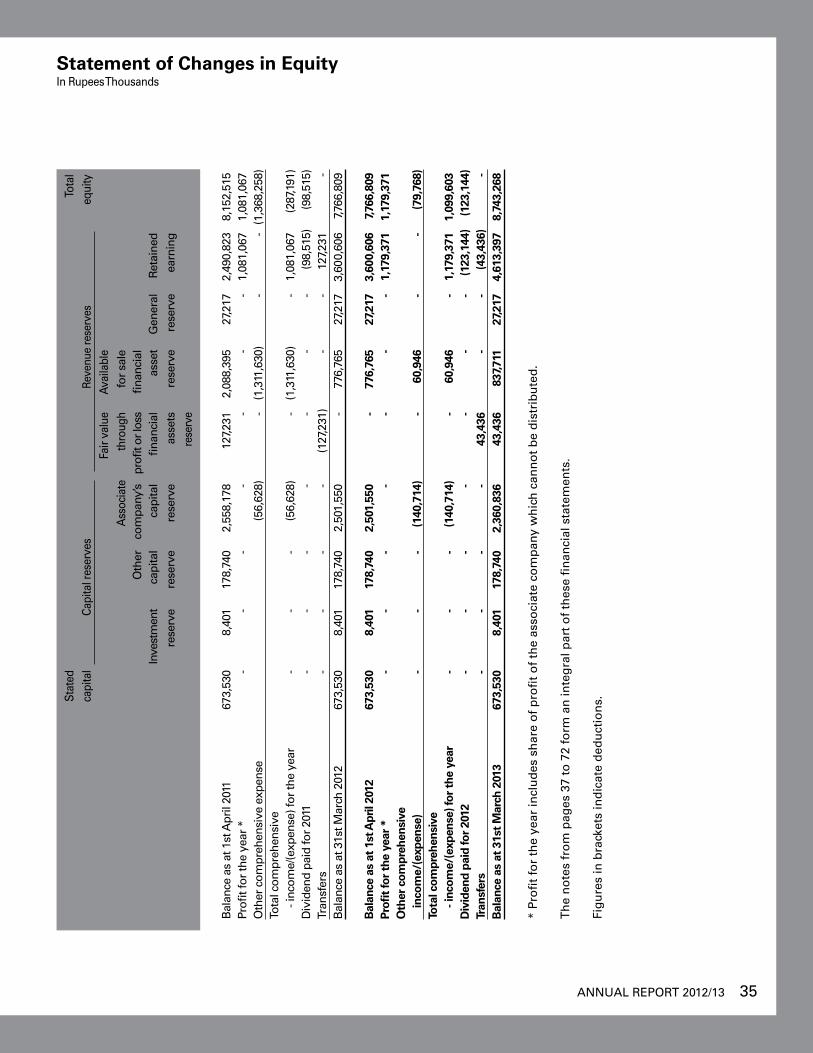

Statement of Comprehensive Income, Statement of Financial Position, Cash Flow Statement, Statement of Changes in Equity and notes to the financial statements of the Company for the year ended 31st March 2013 are set out on pages 33 to 72. These financial statements do comply with the requirements of the Companies Act, No. 7 of 2007.

4.1 Revenue The Company generated a revenue of Rs. 445.9 mn

(2012 – Rs.796.0 mn). A detailed analysis of the revenue for the period is given in note 11 to the financial statements.

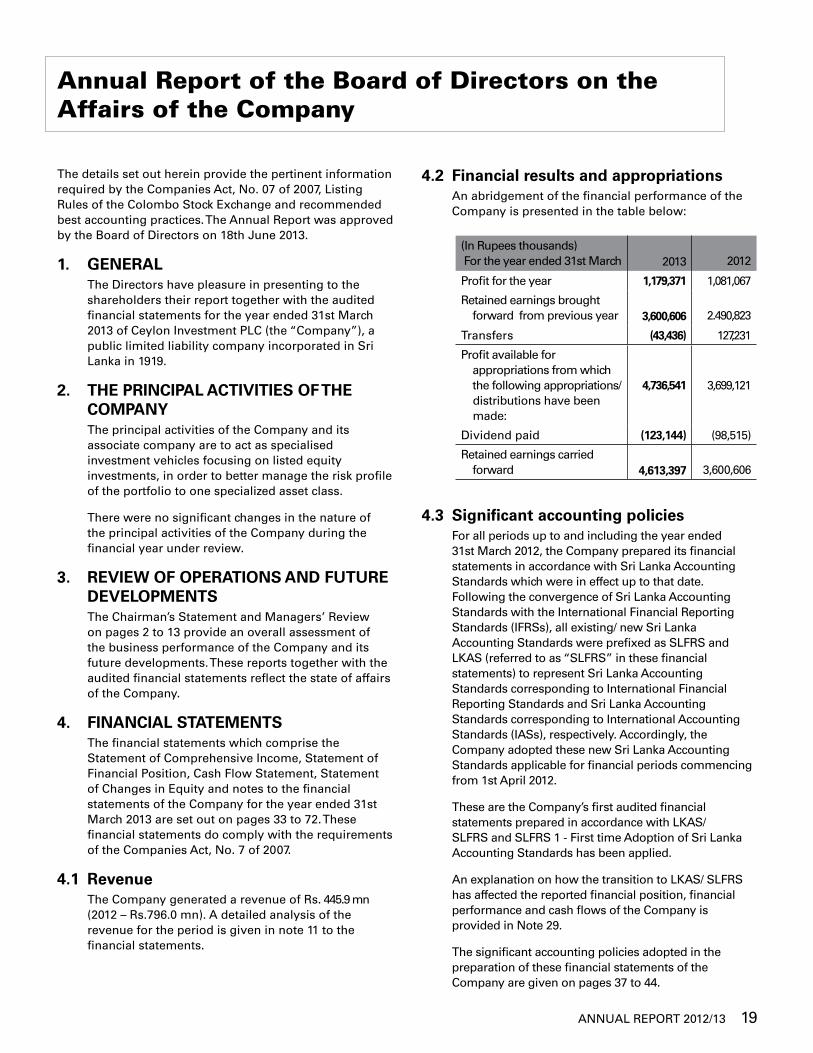

4.2 Financial results and appropriations An abridgement of the financial performance of the

Company is presented in the table below:

(In Rupees thousands) For the year ended 31st March

2013

2012

Profit for the year 1,179,371 1,081,067

Retained earnings brought forward from previous year

3,600,606

2.490,823

Transfers (43,436) 127,231

Profit available for appropriations from which the following appropriations/ distributions have been made:

4,736,541 3,699,121

Dividend paid (123,144) (98,515)

Retained earnings carried forward

4,613,397

3,600,606

4.3 Significant accounting policies For all periods up to and including the year ended

31st March 2012, the Company prepared its financial statements in accordance with Sri Lanka Accounting Standards which were in effect up to that date. Following the convergence of Sri Lanka Accounting Standards with the International Financial Reporting Standards (IFRSs), all existing/ new Sri Lanka Accounting Standards were prefixed as SLFRS and LKAS (referred to as “SLFRS” in these financial statements) to represent Sri Lanka Accounting Standards corresponding to International Financial Reporting Standards and Sri Lanka Accounting Standards corresponding to International Accounting Standards (IASs), respectively. Accordingly, the Company adopted these new Sri Lanka Accounting Standards applicable for financial periods commencing from 1st April 2012.

These are the Company’s first audited financial statements prepared in accordance with LKAS/ SLFRS and SLFRS 1 - First time Adoption of Sri Lanka Accounting Standards has been applied.

An explanation on how the transition to LKAS/ SLFRS has affected the reported financial position, financial performance and cash flows of the Company is provided in Note 29.

The significant accounting policies adopted in the preparation of these financial statements of the Company are given on pages 37 to 44.

20 CEYLON INvESTMENT PLC

4.4 Reserves As at 31st March 2013, the total reserves of the Company

stood at Rs. 8,069.7 mn (2012 - Rs. 7,093.3 mn).

The movements are set out in the Statement of Changes in Equity and note 24 to the financial statements.

4.5 Fair value through profit or loss financial assets reserve

Any gains arising from fair value adjustment will be transferred from retained earnings to “Fair value through profit or loss financial assets reserve” at reporting date and any realised losses arising will be transferred from “Fair value through profit or loss financial assets reserve” to retained earnings to the extent that loss does not exceed the balance held in the said reserve as at the date.

Accordingly, during the year an amount of Rs. 43.4 mn was transferred to (2012 - Rs.127.2 mn was transferred from) “Fair value through profit or loss financial assets reserve” resulting from the movements in fair value adjustment of Fair value through profit or loss financial asset as shown in the Statement of Changes in Equity.

4.6 Available for sales financial assets reserve

During the year, the net positive movement reflected in the ‘Available for sale financial asset reserve’ amounted to Rs. 60.9 mn (2012 - a net negative movement of Rs. 1.311.6 mn) arising out of realized gain and adjustment on fair valuation of investments in Available for sale financial assets.

5. STATEMENT OF DIRECTORS’ RESPONSIbILITIES

The responsibilities of the Directors, in relation to the financial statements are detailed in the following paragraphs, while the responsibilities of the Auditors are set out in the Independent Auditors’ Report.

According to the Companies Act, No. 7 of 2007 and Sri Lanka Accounting and Auditing Standards Act, No. 15 of 1995, Directors are required to prepare financial statements for each financial year, giving a true and fair view of the state of affairs of the Company as at the end of the financial year and of the performance for the said period.

The financial statements comprise of inter alia :

• aStatementoffinancialposition,whichpresentsa true and fair view of the state of affairs of the Company and its associate company as at the end of the financial year:

• aStatementofcomprehensiveincomeoftheCompany and its associate company, which presents a true and fair view of the profit and loss of the Company and its associate company for the financial year. In preparing these financial statements, the Directors are required to ensure that:

• appropriateaccountingpolicieshavebeenselected and applied consistently, while material departures, if any, have been disclosed and explained;

• allapplicableaccountingstandardshavebeencomplied with;

• reasonableandprudentjudgementsandestimates have been made; and

• providestheinformationrequiredbyandotherwise comply with the Colombo Stock Exchange.

The Directors are responsible for ensuring that the Company maintains sufficient accounting records to disclose with reasonable accuracy, the financial position of the Company, for ensuring that the financial statements have been prepared and presented in accordance with the Sri Lanka Accounting and Auditing Standards Act, No. 15 of 1995 and meet with the requirements of the Companies Act, No. 7 of 2007.

They are also responsible for taking reasonable measures to safeguard the assets of the Company and in this regard to give proper consideration to the establishment and effective operation of appropriate systems of internal control with a view to prevent, detect and rectify fraud and other irregularities.

These financial statements have been prepared on a going concern basis, since the Directors are of the view that the Company has adequate resources to continue in operation, for the foreseeable future from the date of signing these financial statements.

The Directors are also of the view that they have discharged their responsibilities as set out in this statement.