Embed Size (px)

Citation preview

Central Clearing – Questions and Answers from the Buy-Side Perspective

April 15, 2010

2©2010 Sutherland Asbill & Brennan LLP

Agenda

Welcome and Opening RemarksRobin Powers, Sutherland

Dealers in the Clearing ProcessAlessandro Cocco, J.P. Morgan

Products and Operational ProcessCorry Bazley, ICE TrustMark Cox, CME Group

Energy/CFTC IssuesMichael Brooks, Sutherland

Legal and Credit IssuesWarren Davis, SutherlandPaul Turner, Sutherland

Q&A

3©2010 Sutherland Asbill & Brennan LLP

Welcome

Welcome

Overview of Current Environment

Introduction of SpeakersAlessandro Cocco, J.P. MorganCorry Bazley, ICE TrustMark Cox, CME GroupMichael Brooks, SutherlandWarren Davis, SutherlandPaul Turner, Sutherland

Dealers in the Clearing ProcessAlessandro CoccoManaging Director, Associate General Counsel

5©2010 Sutherland Asbill & Brennan LLP

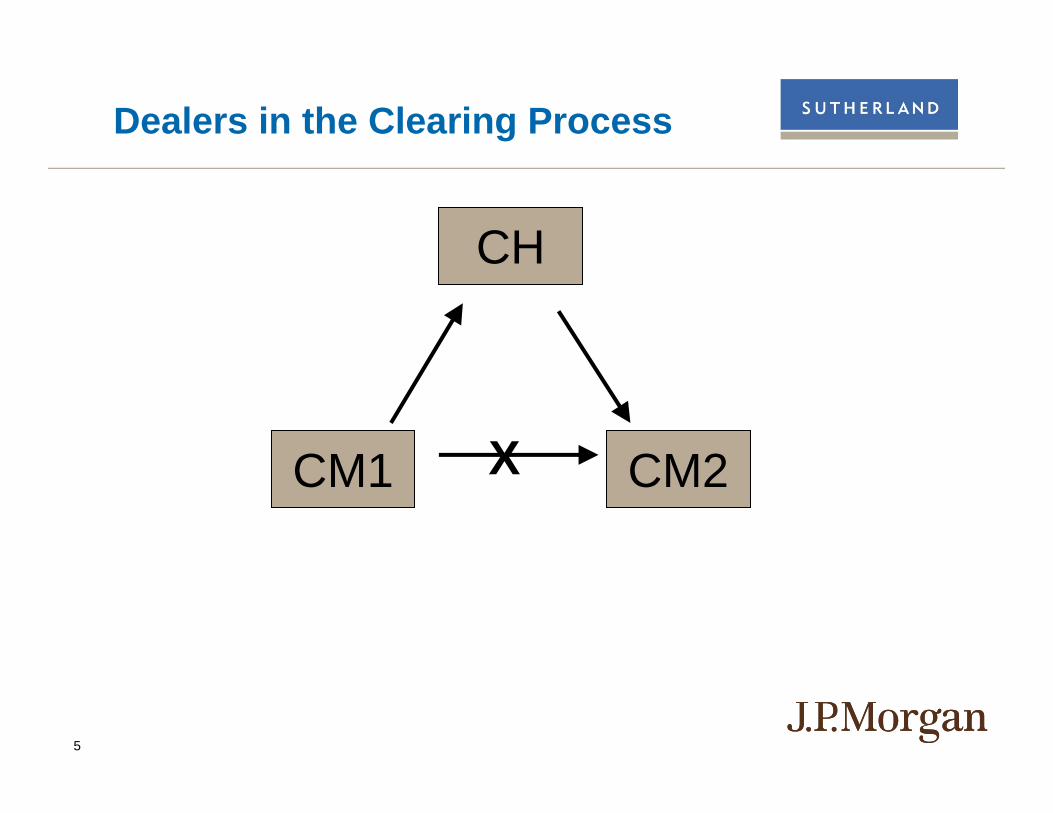

Dealers in the Clearing Process

XCM1 CM2

CH

6©2010 Sutherland Asbill & Brennan LLP

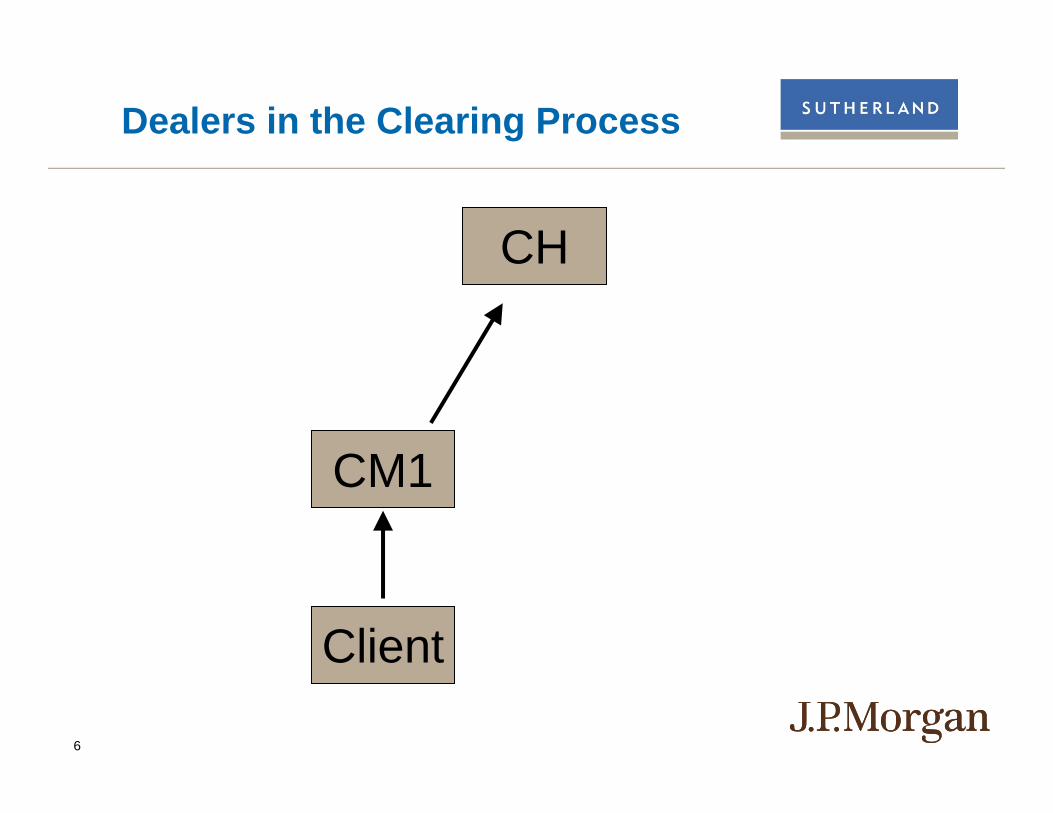

Dealers in the Clearing Process

CM1

CH

Client

7©2010 Sutherland Asbill & Brennan LLP

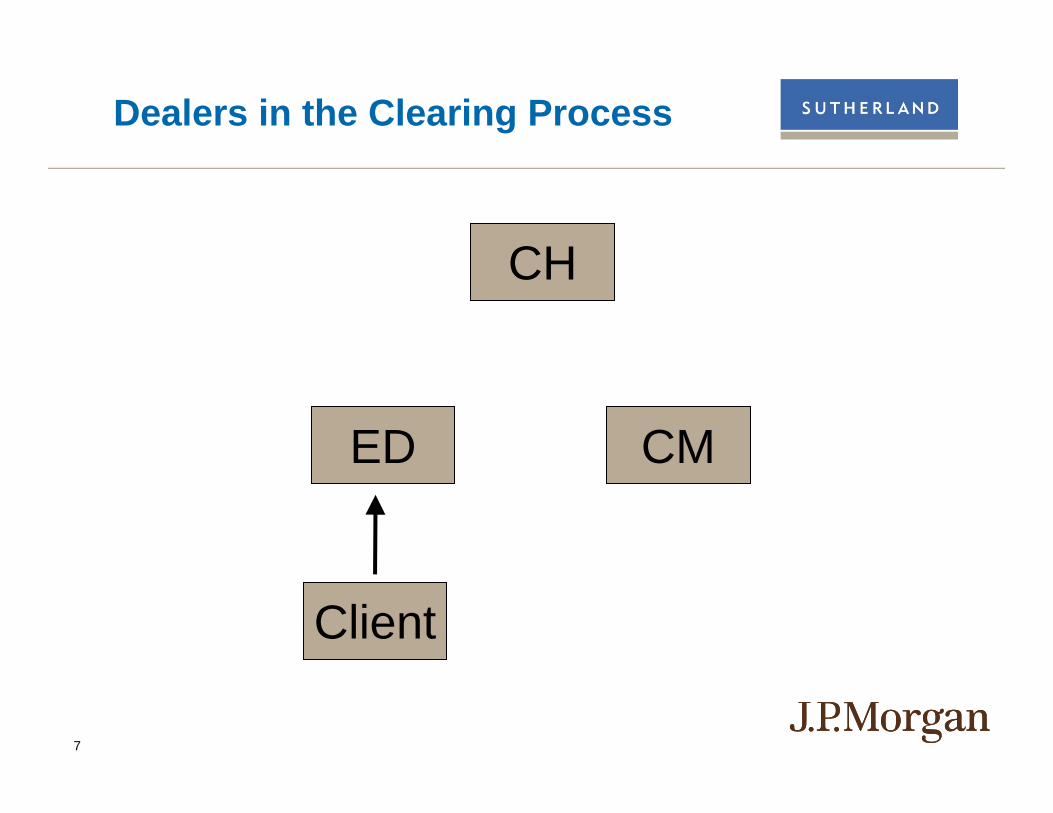

Dealers in the Clearing Process

Client

ED CM

CH

8©2010 Sutherland Asbill & Brennan LLP

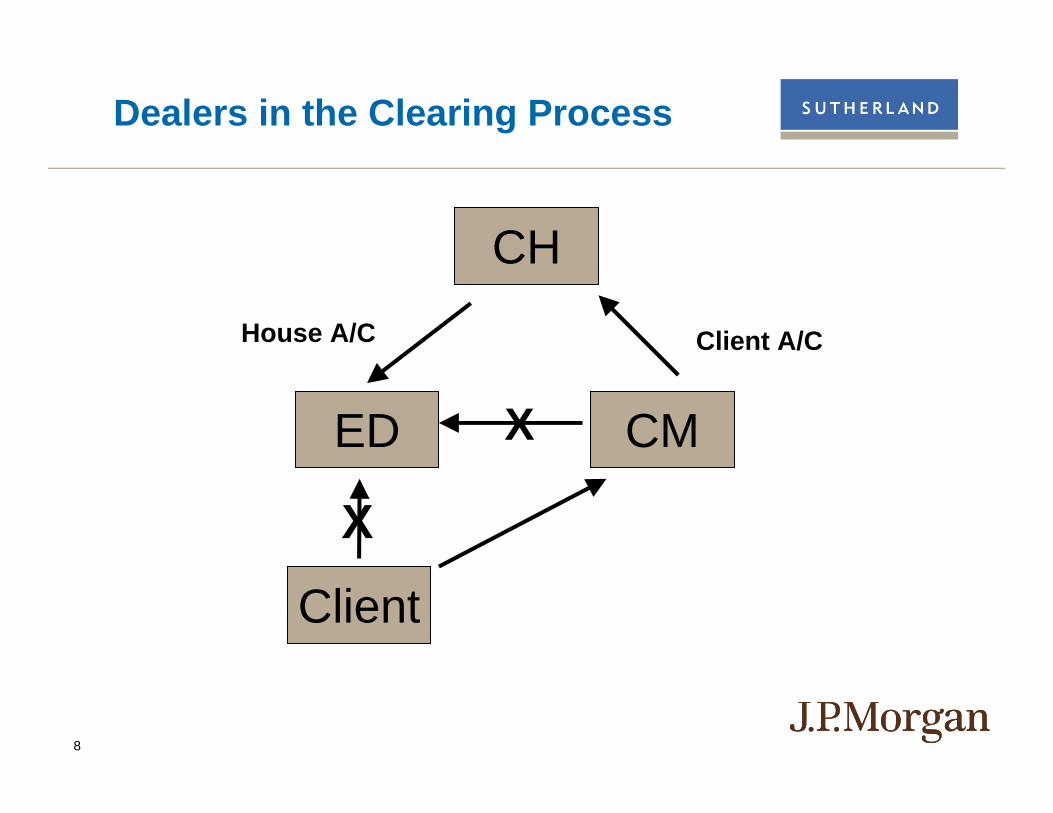

Dealers in the Clearing Process

Client

ED CM

CH

Client A/CHouse A/C

X

X

9©2010 Sutherland Asbill & Brennan LLP

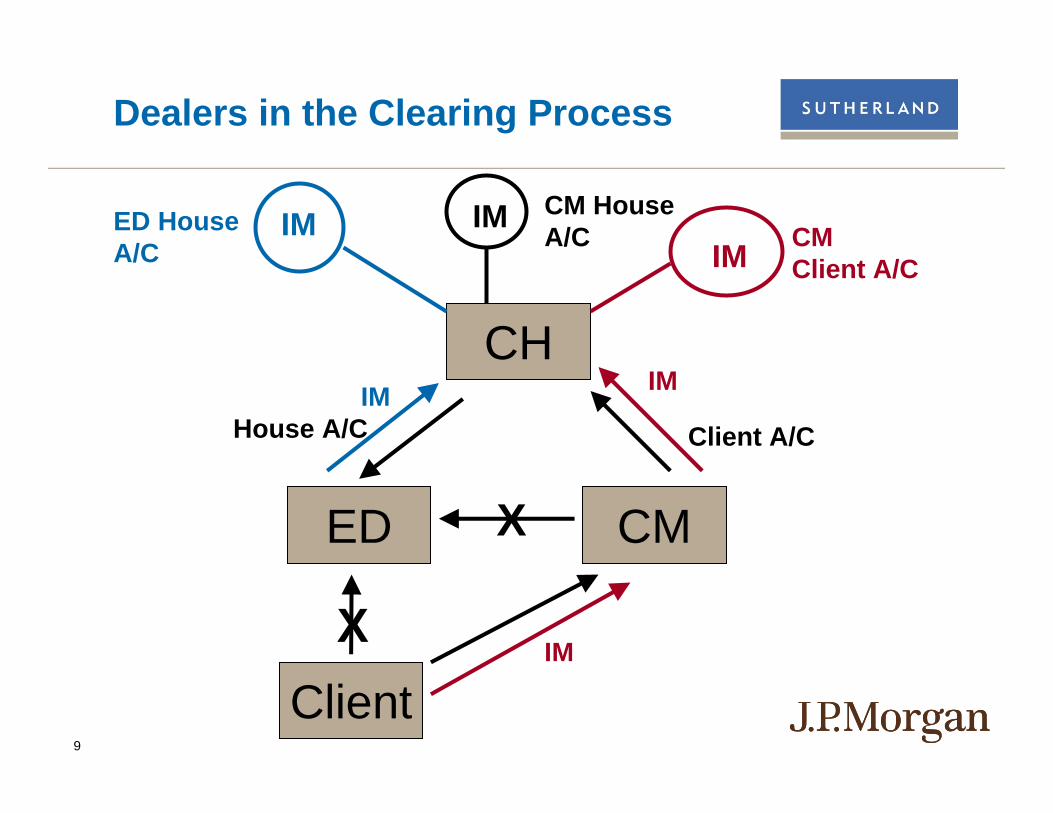

Dealers in the Clearing Process

Client

ED CM

CH

Client A/CHouse A/C

IM CM Client A/C

IM CM House A/CIMED House

A/C

IM

IM

IM

X

X

Products and Operational ProcessCorry BazleySenior Sales North America

Mark CoxDirector, CME Clearing Solutions

11©2010 Sutherland Asbill & Brennan LLP

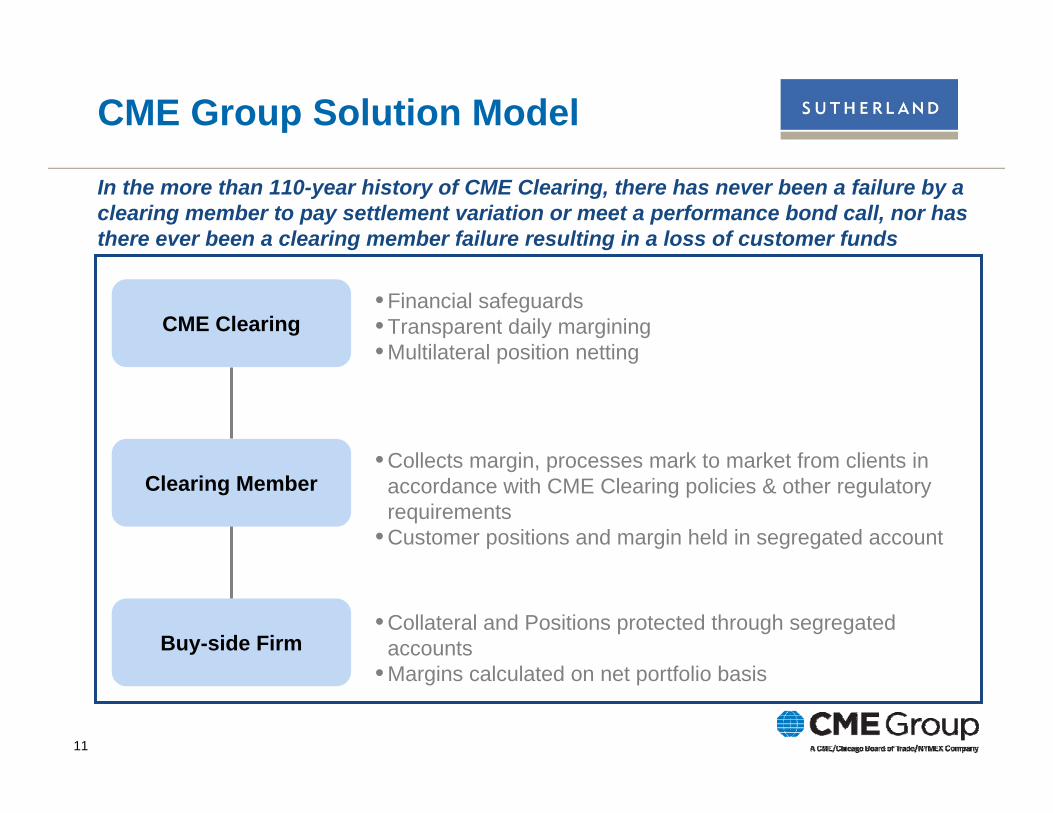

• Financial safeguards• Transparent daily margining• Multilateral position netting

• Collects margin, processes mark to market from clients in accordance with CME Clearing policies & other regulatory requirements

• Customer positions and margin held in segregated account

• Collateral and Positions protected through segregated accounts

• Margins calculated on net portfolio basis

CME Clearing

Clearing Member

Buy-side Firm

CME Group Solution Model

In the more than 110-year history of CME Clearing, there has never been a failure by a clearing member to pay settlement variation or meet a performance bond call, nor has there ever been a clearing member failure resulting in a loss of customer funds

12©2010 Sutherland Asbill & Brennan LLP

Total Guaranty Fund: ~$8B Total Collateral: >$100B

Temporary Liquidity Facility =

$600million

CME Capital Contribution =

Up to $100 million

Note: Financial Safeguards funding reported as of March 31, 2009

Total Financial Safeguards Package Overview

• CME Group’s Financial Safeguards Package is Being Extended to CDS, IRS and FX Products

• Designed to anticipate potential market exposures and ensure sufficient resources are available to cover future obligations

• Based on ability to cover at least the largest potential net debtor, accounting for collateral damage

• Wide variety of accepted security deposit collateral, including:– Cash (USD) – US Treasuries – CME-approved money market mutual

funds

Benefits of CME Group’s Cleared OTC Solution

13©2010 Sutherland Asbill & Brennan LLP

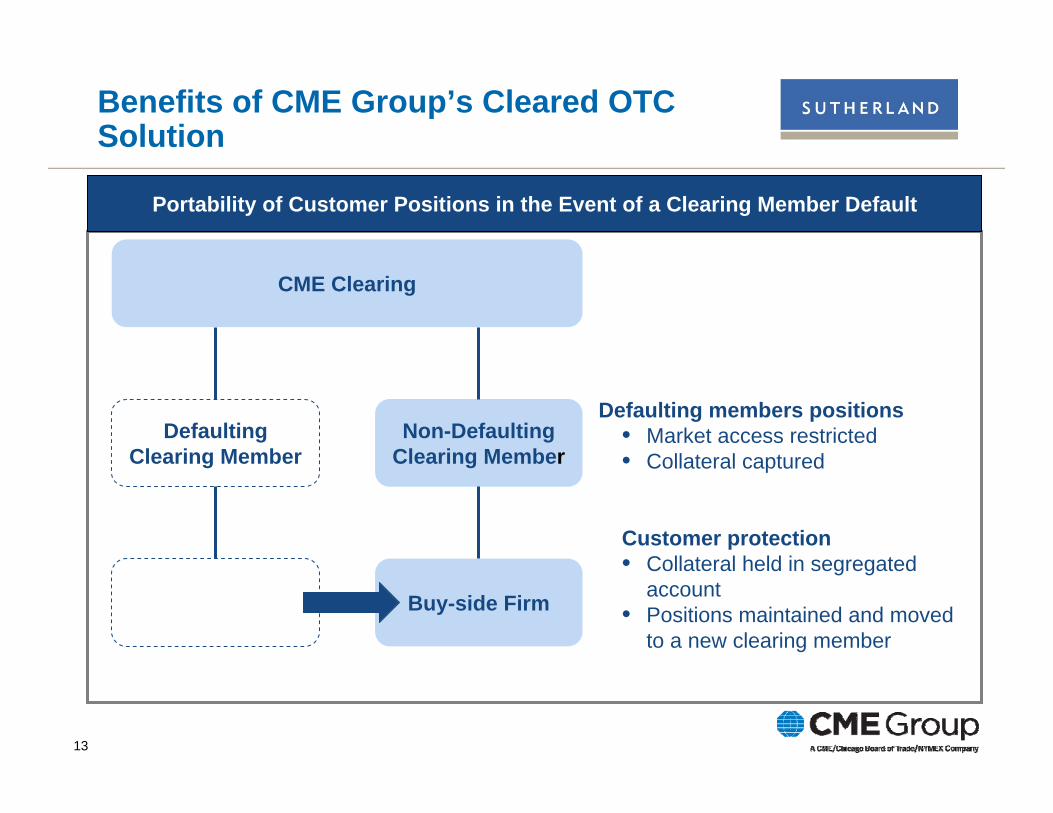

Portability of Customer Positions in the Event of a Clearing Member Default

Defaulting members positions• Market access restricted• Collateral captured

Customer protection• Collateral held in segregated

account • Positions maintained and moved

to a new clearing member

Benefits of CME Group’s Cleared OTC Solution

CME Clearing

Defaulting Clearing Member

Non-Defaulting Clearing Member

Buy-side Firm

14©2010 Sutherland Asbill & Brennan LLP

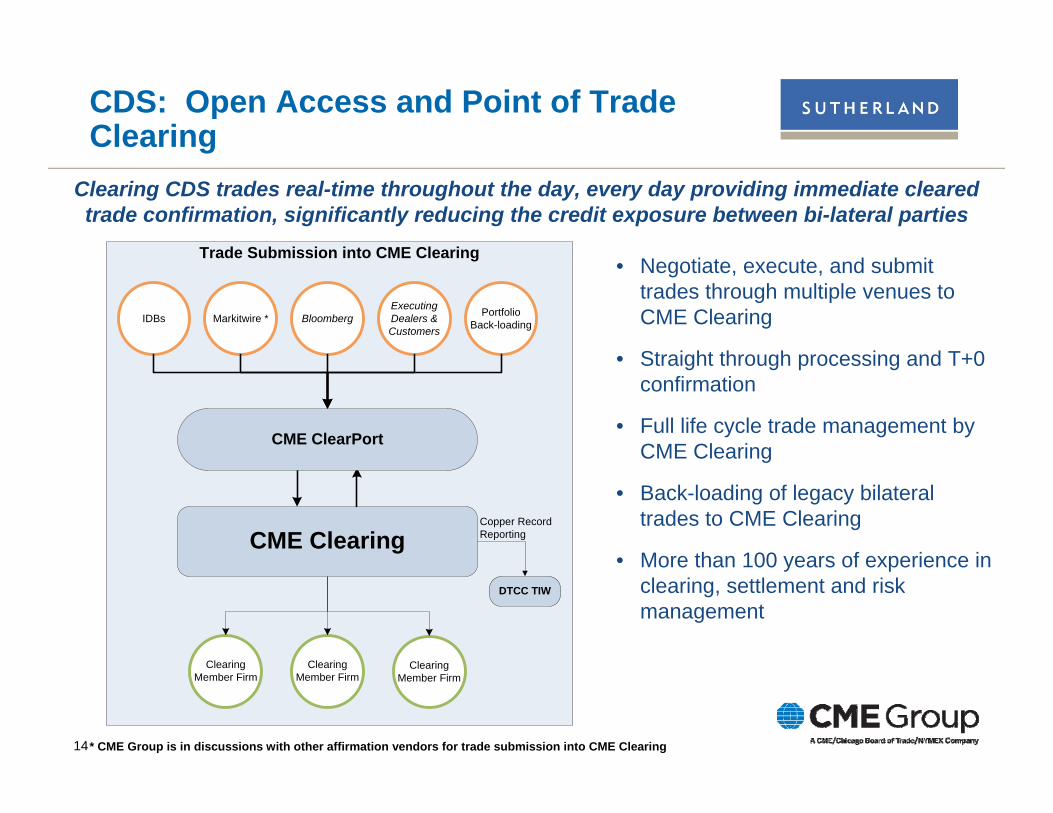

CDS: Open Access and Point of Trade Clearing

• Negotiate, execute, and submit trades through multiple venues to CME Clearing

• Straight through processing and T+0 confirmation

• Full life cycle trade management by CME Clearing

• Back-loading of legacy bilateral trades to CME Clearing

• More than 100 years of experience in clearing, settlement and risk management

Clearing CDS trades real-time throughout the day, every day providing immediate cleared trade confirmation, significantly reducing the credit exposure between bi-lateral parties

* CME Group is in discussions with other affirmation vendors for trade submission into CME Clearing

Trade Submission into CME Clearing

Markitwire *

Clearing Member Firm

Clearing Member Firm

Clearing Member Firm

IDBs

CME Clearing

CME ClearPort

Portfolio Back-loadingBloomberg

Executing Dealers & Customers

DTCC TIW

Copper Record Reporting

15©2010 Sutherland Asbill & Brennan LLP

ICE: Diverse Global Derivatives Markets

Global derivatives markets across energy, agriculture, equity indexes, FX and credit

Integrated execution and clearing: 3 futures exchanges, 2 OTC markets and 5 clearing houses

Market participants in more than 55 countries

Industry-leading innovation in products and technology

CDS infrastructure that fully encompasses trade execution, processing and clearing

ICE Integrated Marketplace

IntercontinentalExchange (ICE) is the leading operator of integrated futures and over-the-counter (OTC) markets, clearing, processing and data services for global derivatives markets.

16©2010 Sutherland Asbill & Brennan LLP

Global Leader in CDS Clearing

Liquidity13 dealers together with leading hedge funds and asset managers actively clearing today61 index contracts and 151 single names across US & Europe

Risk ManagementWorld class risk management specifically designed for CDS$3 billion guaranty fund -- completely separate from all other products Guaranty fund sized to cover losses from simultaneous default of 2 largest clearing members

CDS and Clearing ExpertiseManaged numerous Credit Events since launching CDS clearingLeading market connectivity processing thousands of CDS trades a dayCo-administrators of ISDA Cash settlement auctions

Ease of Doing BusinessNo changes to existing OTC trade execution requiredSimple legal framework leveraging existing ISDA documentationOpen access provided through support of multiple affirmation platforms

17©2010 Sutherland Asbill & Brennan LLP

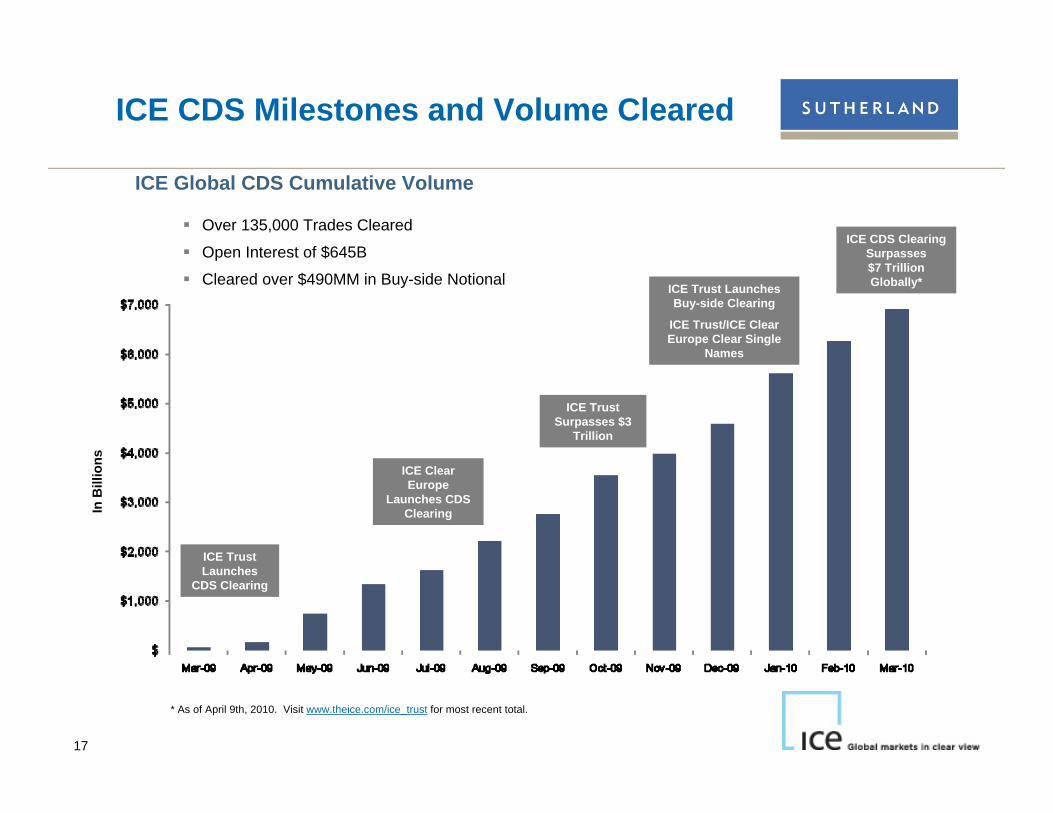

* As of April 9th, 2010. Visit www.theice.com/ice_trust for most recent total.

ICE CDS Milestones and Volume ClearedIn

Bill

ions

ICE Global CDS Cumulative Volume

ICE Trust Launches

CDS Clearing

ICE Clear Europe

Launches CDS Clearing

ICE Trust Surpasses $3

Trillion

ICE Trust Launches Buy-side Clearing

ICE Trust/ICE Clear Europe Clear Single

Names

ICE CDS Clearing Surpasses $7 Trillion Globally*

Over 135,000 Trades Cleared

Open Interest of $645B

Cleared over $490MM in Buy-side Notional

18©2010 Sutherland Asbill & Brennan LLP

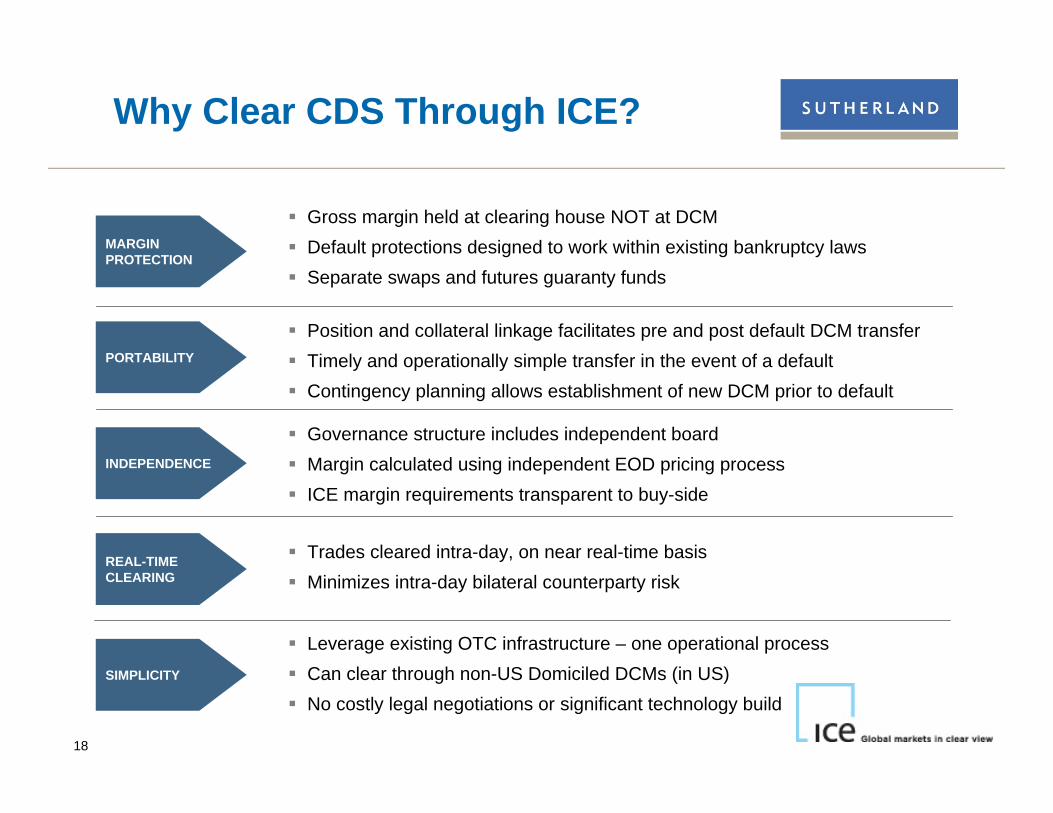

Why Clear CDS Through ICE?

Gross margin held at clearing house NOT at DCMDefault protections designed to work within existing bankruptcy lawsSeparate swaps and futures guaranty funds

Position and collateral linkage facilitates pre and post default DCM transferTimely and operationally simple transfer in the event of a defaultContingency planning allows establishment of new DCM prior to default

Trades cleared intra-day, on near real-time basisMinimizes intra-day bilateral counterparty risk

Leverage existing OTC infrastructure – one operational processCan clear through non-US Domiciled DCMs (in US)No costly legal negotiations or significant technology build

MARGINPROTECTION

PORTABILITY

INDEPENDENCE

REAL-TIME CLEARING

SIMPLICITY

Governance structure includes independent boardMargin calculated using independent EOD pricing processICE margin requirements transparent to buy-side

19©2010 Sutherland Asbill & Brennan LLP

DTCC

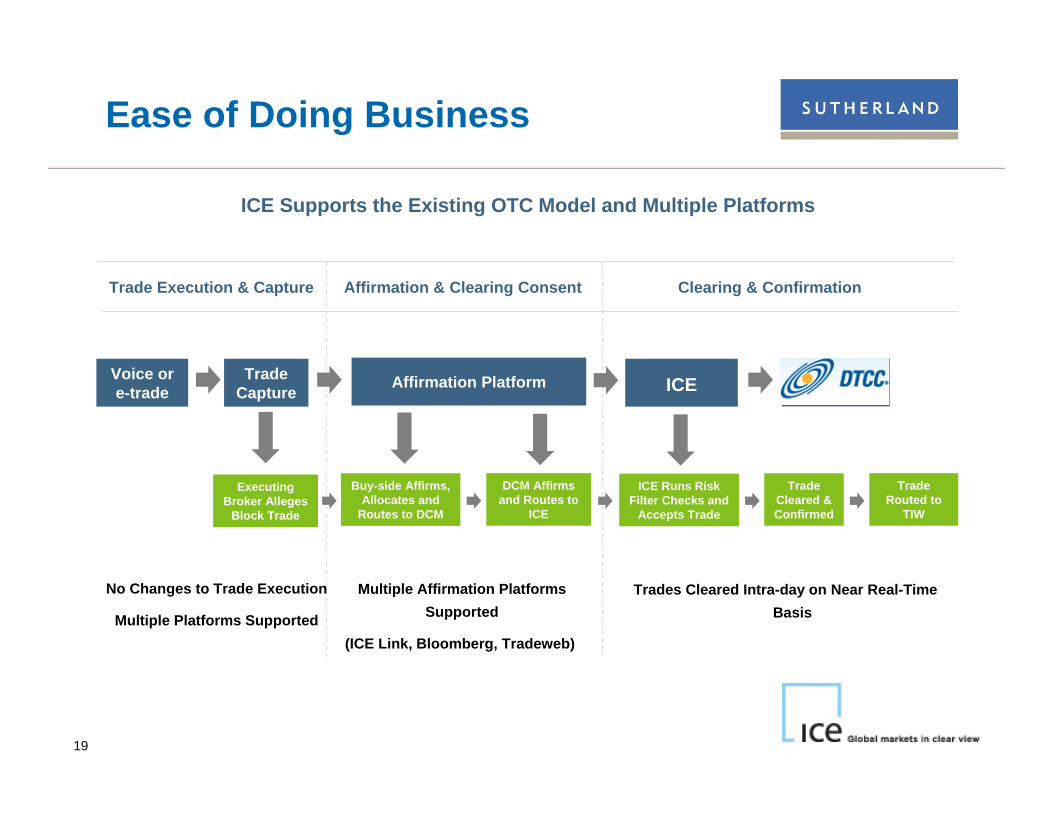

Ease of Doing Business

ICE Supports the Existing OTC Model and Multiple Platforms

Trade Execution & Capture Affirmation & Clearing Consent Clearing & Confirmation

Voice or e-trade

Trade Capture ICE

Executing Broker Alleges

Block Trade

Buy-side Affirms, Allocates and

Routes to DCM

DCM Affirms and Routes to

ICE

ICE Runs Risk Filter Checks and

Accepts Trade

Trade Cleared & Confirmed

Trade Routed to

TIW

No Changes to Trade Execution

Multiple Platforms Supported

Affirmation Platform

Multiple Affirmation PlatformsSupported

(ICE Link, Bloomberg, Tradeweb)

Trades Cleared Intra-day on Near Real-Time Basis

20©2010 Sutherland Asbill & Brennan LLP

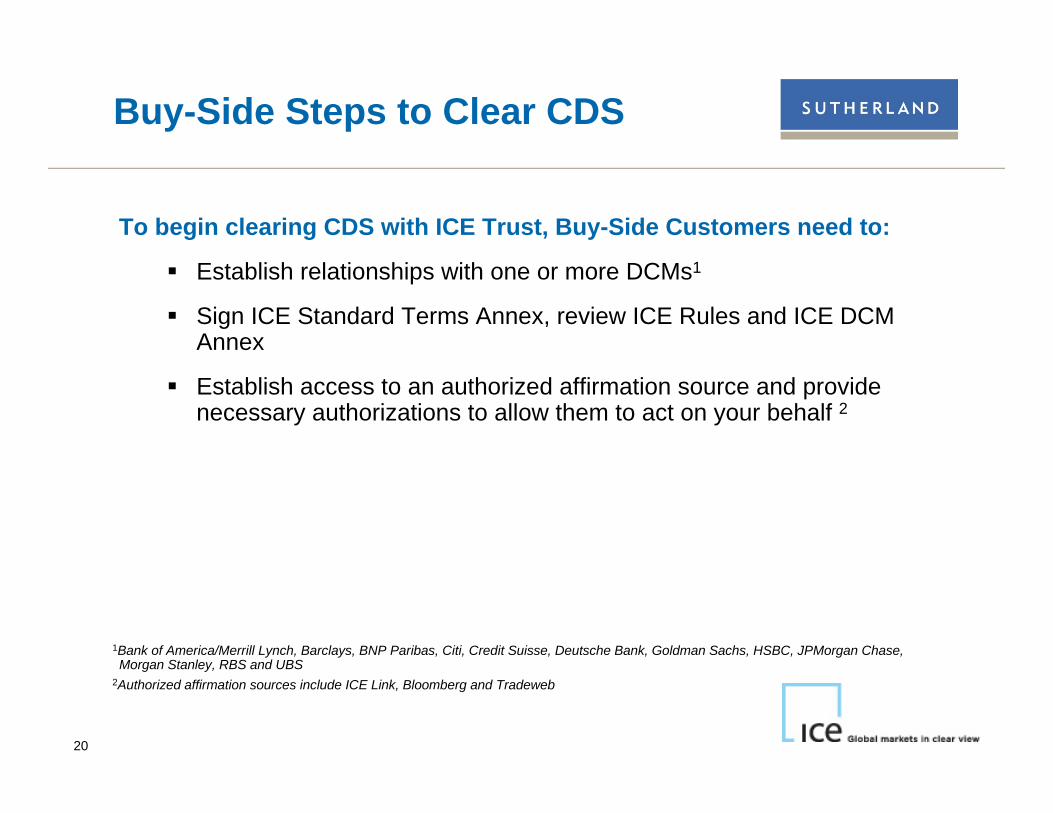

Buy-Side Steps to Clear CDS

To begin clearing CDS with ICE Trust, Buy-Side Customers need to:

Establish relationships with one or more DCMs1

Sign ICE Standard Terms Annex, review ICE Rules and ICE DCM Annex

Establish access to an authorized affirmation source and providenecessary authorizations to allow them to act on your behalf 2

1Bank of America/Merrill Lynch, Barclays, BNP Paribas, Citi, Credit Suisse, Deutsche Bank, Goldman Sachs, HSBC, JPMorgan Chase, Morgan Stanley, RBS and UBS

2Authorized affirmation sources include ICE Link, Bloomberg and Tradeweb

21©2010 Sutherland Asbill & Brennan LLP

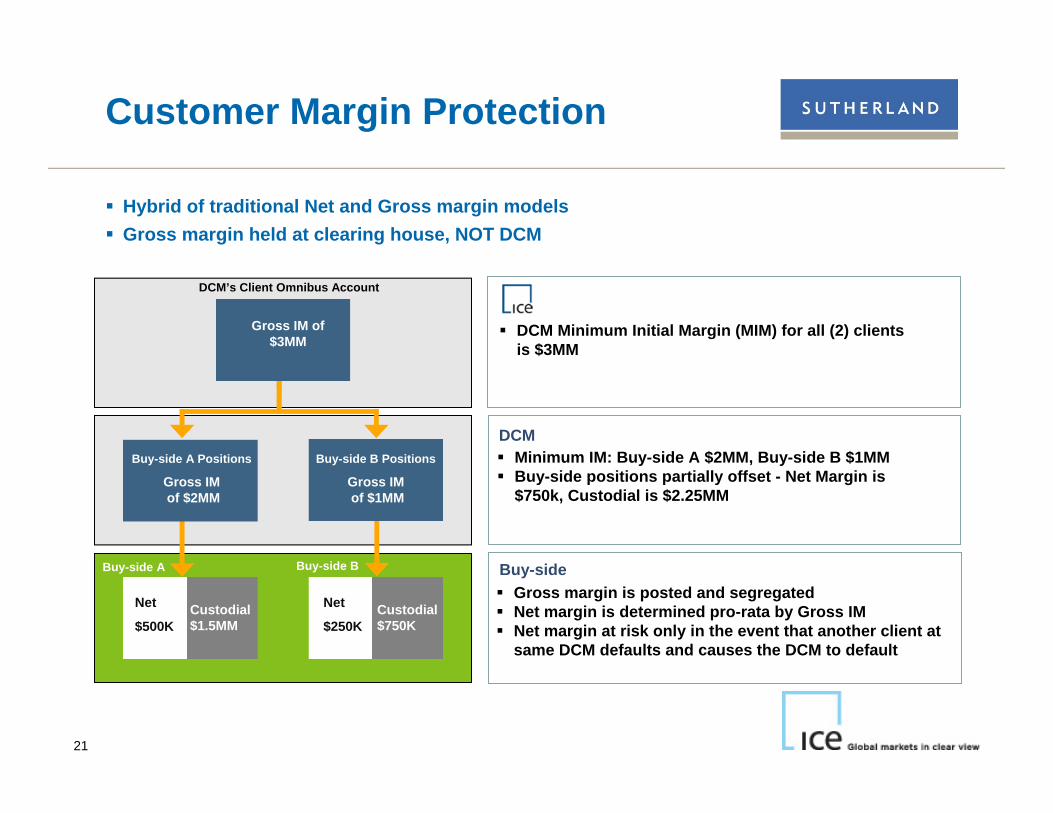

Customer Margin Protection

DCM 2

DCM Minimum Initial Margin (MIM) for all (2) clients is $3MM

Minimum IM: Buy-side A $2MM, Buy-side B $1MMBuy-side positions partially offset - Net Margin is $750k, Custodial is $2.25MM

Gross margin is posted and segregatedNet margin is determined pro-rata by Gross IMNet margin at risk only in the event that another client at same DCM defaults and causes the DCM to default

DCM

Buy-side

Hybrid of traditional Net and Gross margin modelsGross margin held at clearing house, NOT DCM

DCM’s Client Omnibus Account

Gross IM of $3MM

Buy-side A Positions

Gross IMof $2MM

Buy-side B Positions

Gross IMof $1MM

Buy-side A Buy-side B

Net

$500K

Net

$250KCustodial $1.5MM

Custodial $750K

22©2010 Sutherland Asbill & Brennan LLP

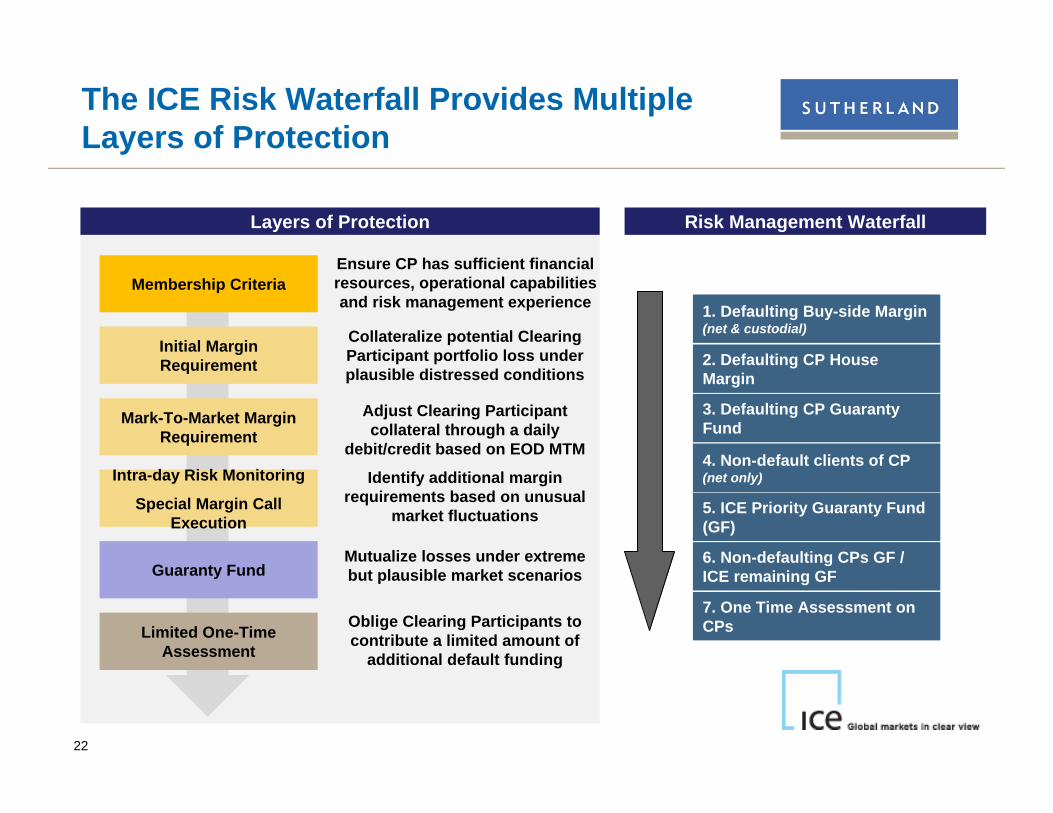

The ICE Risk Waterfall Provides Multiple Layers of Protection

Membership Criteria

Initial Margin Requirement

Mark-To-Market Margin Requirement

Guaranty Fund

Intra-day Risk Monitoring

Special Margin Call Execution

Limited One-Time Assessment

Ensure CP has sufficient financial resources, operational capabilities and risk management experience

Collateralize potential Clearing Participant portfolio loss under plausible distressed conditions

Adjust Clearing Participant collateral through a daily

debit/credit based on EOD MTM

Identify additional margin requirements based on unusual

market fluctuations

Mutualize losses under extreme but plausible market scenarios

Oblige Clearing Participants to contribute a limited amount of

additional default funding

Layers of Protection

1. Defaulting Buy-side Margin(net & custodial)

2. Defaulting CP House Margin

3. Defaulting CP Guaranty Fund

4. Non-default clients of CP(net only)

7. One Time Assessment on CPs

6. Non-defaulting CPs GF / ICE remaining GF

5. ICE Priority Guaranty Fund (GF)

Risk Management Waterfall

Energy and CFTC IssuesMichael Brooks, Sutherland

24©2010 Sutherland Asbill & Brennan LLP

Clearing OTC Energy Contracts

• Concerns about oil market volatility in 2007-08 have driven Congress and CFTC Chairman Gensler to press for greater transparency through mandated clearing and other means

• But there are real questions as to whether the system is brokenInstitutional “longs” largely have been operating in the regulated futures marketsIt is not at all clear that price spikes originate in the OTC markets, however much they may lack transparencyMany standardized OTC energy contracts already have migrated to the clearing houses

25©2010 Sutherland Asbill & Brennan LLP

Clearing OTC Energy Contracts

• There are real concerns that “forced” clearing of standardized agreements will undermine market efficiencies

End users continue to lobby for exemption from clearing and margin requirementsSome believe that important non-standardized OTC contracts will not survive the transition (e.g. basis swaps)

• Existing law gives the regulators substantial powers to supervise both the OTC and the forward energy markets

• There are hints that the final legislation will not be as aggressive as some on the Hill and at the Commission would wish

Legal and Credit IssuesWarren Davis, SutherlandPaul Turner, Sutherland

27©2010 Sutherland Asbill & Brennan LLP

Subchapter IV of Chapter 7

•Bankruptcy Code’s Subchapter IV of Chapter 7: Liquidation of Commodity Brokers

Facilitates transfer of customer accounts to different (solvent)commodity brokerIf customer accounts identifiable, then trustee must heed requests for return of customer property and/or transfer to new commodity brokerIf cannot be identified or cannot be transferred, then contract liquidatedIf customer owed money after transfer/liquidation/offset, customer receives ratable distribution (higher priority than non-customer claims)CFTC has right to appear and be heard on issuesChapter 5 provisions apply

28©2010 Sutherland Asbill & Brennan LLP

Bankruptcy Issues

Many concerns originate out of Lehman bankruptcyLBIE (UK entity) had customer accounts released by exchanges to LBIE’s administrators, leaving customers without adequate remedy

Customer protection requires segregation & portabilityFactors in segregation: security interest vs. transfer of title, clearinghouse collection of margin, type of margin held, location where margin is held, commingling, rehypothecationPortability relies highly on segregation; e.g., margin must be held away from commodity broker and must not be commingled

29©2010 Sutherland Asbill & Brennan LLP

CFTC Rule

•Final Ruling Effective May 6, 2010Amends existing regulations to create new “account class”

Significance of account classNew category applies only in cases of bankrupt commodity broker that is FCMApplies to cleared OTC derivatives and money, securities or other property securing them

Comments expressed concerns:Bankruptcy courts could decline to find cleared-only contracts as “commodity contracts”Rule did not address bankruptcy of clearing organization

30©2010 Sutherland Asbill & Brennan LLP

Predictions

Continued focus on bankruptcy issues for near- and intermediate- term, particularly if legislation passes requiring more derivatives to be clearedLegislative and regulatory response will leave some gapsAs economy improves, most could lose focus on key issuesProblems will not fully come to light until next major crisis

31©2010 Sutherland Asbill & Brennan LLP

Selective Non-Insolvency Buy-Side Legal Issues

• Status of Trade Before Accepted for Clearing

• Initial Margin Issues

• Porting Transactions

32©2010 Sutherland Asbill & Brennan LLP

Status of Trade Before Accepted for Clearing

• What happens if counterparty enters into a trade with the expectation that it will become a cleared trade and for whatever reason that does not happen?

• Possible Relevant Documentation:Clearing House Rules and ProceduresAgreement with clearing member/counterparty and/or executing broker (in case of “Give-Up Agreement”)Note: ISDA Nov. 2009 Recommended Common Principles for Relationship Between Customer and Executing Broker and Clearing Member

33©2010 Sutherland Asbill & Brennan LLP

Initial Margin Issues

Questions: 1. Will Initial Margin always be custodied at the Clearing House?2. Will Initial Margin required by the Clearing Member in excess of the

Clearing House’s requirement for Initial Margin be custodied at the Clearing House?

3. May a customer utilize securities to satisfy its Initial Margin requirements?

4. If yes, what kinds of securities will be eligible and will there be haircuts?

5. If a customer posts cash to satisfy initial margin, will he be entitled to receive interest on the cash?

6. If yes, will be rate be negotiated between the customer and the Clearing Member or between the Clearing Member and the Clearing House?

34©2010 Sutherland Asbill & Brennan LLP

Possible Relevant DocumentationClearing House Rules Agreement between Clearing House and Clearing MemberAgreement between Clearing Member and Customer

In case of ICE Trust Existing ISDA and CSA and “New”ISDA and for Cover Transactions.

Initial Margin Issues

35©2010 Sutherland Asbill & Brennan LLP

Porting Transactions (Before Clearing Member Insolvency)

Questions:1. When can transactions be moved?2. What is the procedures for moving transactions?

Possible Relevant Documentation:Clearing House Rules Agreement between Clearing House and Clearing MemberAgreement between Clearing Member and CustomerAgreement between Customer and New Clearing Member

36©2010 Sutherland Asbill & Brennan LLP

Questions?

Corry BazleySenior Sales North AmericaICE [email protected]

Alessandro CoccoManaging DirectorAssociate General CounselJ.P. [email protected]

Mark CoxDirector, CME Clearing SolutionsCME [email protected]

Michael BrooksSutherland Asbill & Brennan [email protected]

Warren DavisSutherland Asbill & Brennan [email protected]

Robin PowersSutherland Asbill & Brennan [email protected]

Paul TurnerSutherland Asbill & [email protected]