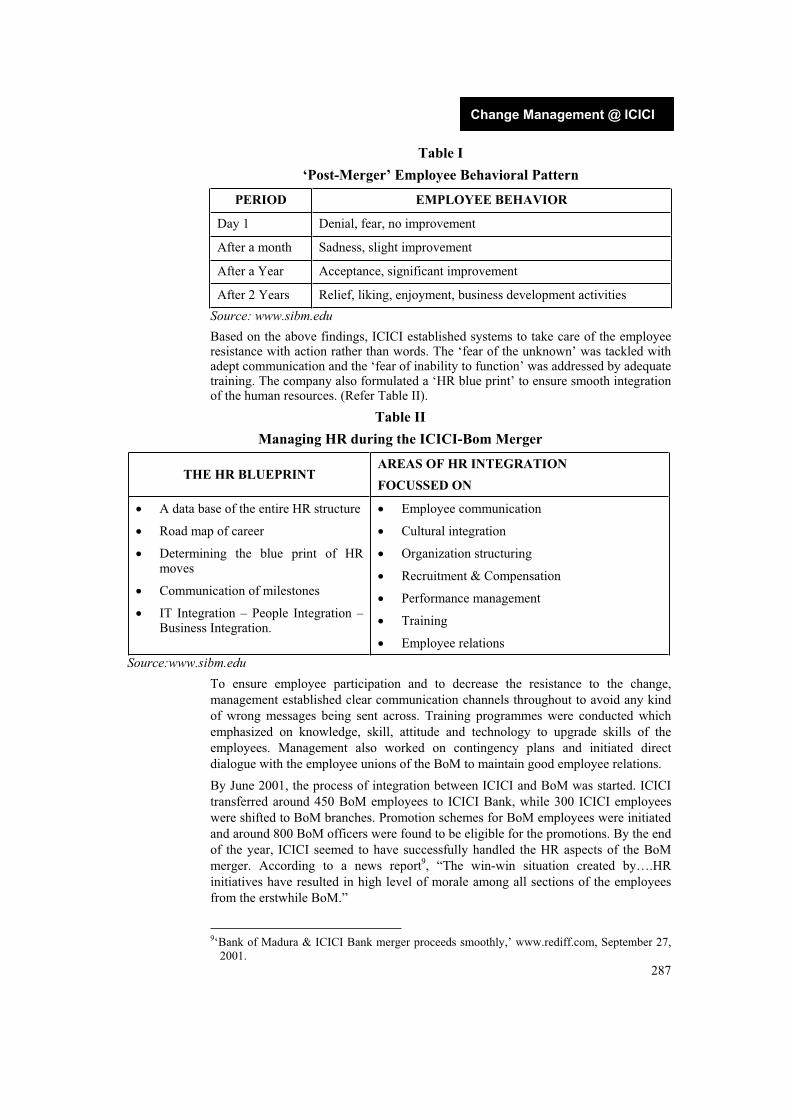

Embed Size (px)

Citation preview

Learning with Cases

INTRODUCTION

The case study method of teaching used in management education is quite different

from most of the methods of teaching used at the school and undergraduate course

levels. Unlike traditional lecture-based teaching where student participation in the

classroom is minimal, the case method is an active learning method, which requires

participation and involvement from the student in the classroom. For students who

have been exposed only to the traditional teaching methods, this calls for a major

change in their approach to learning.

This introduction is intended to provide students with some basic information about

the case method, and guidelines about what they must do to gain the maximum benefit

from the method. We begin by taking a brief look at what case studies are, and how

they are used in the classroom. Then we discuss what the student needs to do to

prepare for a class, and what she can expect during the case discussion. We also

explain how student performance is evaluated in a case study based course. Finally,

we describe the benefits a student of management can expect to gain through the use

of the case method.

WHAT IS A CASE STUDY?

There is no universally accepted definition for a case study, and the case method

means different things to different people. Consequently, all case studies are not

structured similarly, and variations abound in terms of style, structure and approach.

Case material ranges from small caselets (a few paragraphs to one-two pages) to short

cases (four to six pages) and from 10 to 18 page case studies to the longer versions (25

pages and above).

A case is usually a “description of an actual situation, commonly involving a decision,

a challenge, an opportunity, a problem or an issue faced by a person or persons in an

organization.”1 In learning with case studies, the student must deal with the situation

described in the case, in the role of the manager or decision maker facing the situation.

An important point to be emphasized here is that a case is not a problem. A problem

usually has a unique, correct solution. On the other hand, a decision-maker faced with

the situation described in a case can choose between several alternative courses of

action, and each of these alternatives may plausibly be supported by logical argument.

To put it simply, there is no unique, correct answer in the case study method.

The case study method usually involves three stages: individual preparation, small

group discussion, and large group or class discussion. While both the instructor and

the student start with the same information, their roles are clearly different in each of

these stages, as shown in Table 1.

1 Michiel R. Leeenders, Louise A. Mauffette-Launders and James Erskine, Writing Cases,(Ivey Publishing, 4th edition) 3.

l

2

Learning with Cases

Table 1

Teacher and Student Roles in a Regular Case Class

When Teacher Student or Participant

Assigns case and often readings Receives case and assignment

Prepares for class Prepares individually

BeforeClass

May consult colleagues Discusses case in small group

Deals with readings Raises questions regarding readings During Class

Leads case discussion Participates in discussion

Evaluates and records student participation

Compares personal analysis with colleagues’ analysis.

AfterClass

Evaluates materials and updates teaching note

Reviews class discussion for major concepts learned.

Source: Michiel R. Leeenders, Louise A. Mauffette-Launders and James Erskine,

Writing Cases, (Ivey Publishing 4th edition) 3.

CASE STUDIES IN THE CLASSROOM

Case studies are usually discussed in class, in a large group. However, sometimes,

instructors may require individuals or groups of students to provide a written analysis

of a case study, or make an oral presentation on the case study in the classroom.

Preparing for a Case Discussion

Unlike lecture-based teaching, the case method requires intensive preparation by the

students, before each class. If a case has been assigned for discussion in the class, the

student must prepare carefully and thoroughly for the case discussion.

The first step in this preparation is to read the case thoroughly. To grasp the situation

described in a case study, the student will need to read it several times. The first

reading of the case can be a light one, to get a broad idea of the story. The subsequent

readings must be more focused, to help the student become familiar with the facts of

the case, and the issues that are important in the situation being described in the case –

the who, what, where, why and how of the case.

However, familiarity with the facts described in the case is not enough. The student

must also acquire a thorough understanding of the case situation, through a detailed

analysis of the case. During the case analysis process, she must to attempt to identify

the main protagonists in the case study (organizations, groups, or individuals

described in the case) and their relationships.

The student must also keep in mind that different kinds of information are presented

in the case study2. There are facts, which are verifiable from several sources. There

are inferences, which represent an individual’s judgment in a given situation. There is

speculation, which is information which cannot be verified. There are also

assumptions, which cannot be verified, and are generated during case analysis or

discussion. Clearly, all these different types of information are not equally valuable

2 Michael A. Hitt, R. Duane Ireland and Robert E. Hoskisson, Strategic Management

(Thomson Southwestern, 6th Edition) Civ

3

Learning with Cases

for managerial decision-making. Usually, the greater your reliance on facts (rather

than speculation or assumptions), the better the logic and persuasiveness of your

arguments and the quality of your decisions.

Broadly speaking, the different stages in the case analysis process could be as

follows3:

1. Gaining familiarity with the case situation (critical case facts, persons, activities,

contexts)

2. Recognizing the symptoms (what are the things that are not as expected, or as

they should be?)

3. Identifying goals/objectives

4. Conducting the analysis

5. Making the diagnosis (identifying problems, i.e., discrepancies between goals and

performance, prioritizing problems etc.)

6. Preparing the action plan (identifying feasible action alternatives, selecting a

course of action, implementation planning, plan for monitoring implementation)

3 Adapted from: 1993, C. C. Lundberg and C. Enz, ‘A framework for student case preparation’, Case Research Journal, 13 (Summer):144/Michael A. Hitt, R. Duane Ireland and Robert E. Hoskisson, Strategic Management (Thomson Southwestern, 6th Edition) Ciii

Exhibit 1

Components of a Situation Analysis

1. Corporate level situation analysis

- Corporate mission and objectives

- Resources and competencies

- Environmental problems and opportunities

- Demographic

- Social-cultural

- Economic

- Technological

- Legal and regulatory

- Competition

- Portfolio analysis

2. Product level situation analysis

- Market analysis

- Describe the product-market structure

- Find out who buys

- Assess why buyers buy

- Determine how buyers make choices

- Determine bases for market segmentation

l

4

Learning with Cases

Source: Developed from Joseph Guiltinan and Gordon Paul, ‘Marketing

Management: Strategies and Programs’, Fourth Edition (New York: McGraw-Hill, 1990), Chapters 2-6/ Joseph Guiltinan and Gordon Paul, Cases in Marketing

Management (McGraw-Hill, International Edition 1992) 2.

The components of a situation analysis for a typical marketing case are given

in Exhibit 1. This consists of situation analyses at the corporate and product

levels and a summary of the results of the analysis. Cases in other functional

areas such as strategy can also be analyzed using similar frameworks. As

mentioned earlier, the situation analysis should be followed by problem

diagnosis and action plan recommendations. While preparing for the case discussion, the student can also make notes with respect

to the key aspects of the situation and the case analysis. These could include points

such as the following:

Which company (or companies) is being talked about? Which industry is referred

to?

What are the products/services mentioned?

How/Why did the company land in problems (or became successful)?

What decision issues/problems/challenges are the decision makers in the case

faced with?

- Identify potential target markets

- Competitive analysis

- Identify direct competitors

- Assess likelihood of new competitors

- Determine stage in product life cycle

- Assess pioneer advantages

- Assess intensity of competition

- Determine the competitors’ advantages and disadvantages

- Market measurement

- Estimate market potential

- Determine relative potential of each geographic area

- Track industry sales trends

- Assess company or brand trends in sales and market share

- Make forecasts

- Profitability and productivity analysis

- Determine the cost structure

- Identify cost-volume-profit relationships

- Perform break-even and target profit analysis

- Make projections of sales or market share impact of marketing

expenditures

3. Summary - Assess performance (identification of symptoms)

- Define problems and opportunities

5

Learning with Cases

Case Discussions in the Classroom

A classroom case discussion is usually guided by the instructor. Students are expected

to participate in the discussion and present their views. In some cases, the instructor

may adopt a particular view, and challenge the students to respond. During the

discussion, while a student presents his point of view, others may question or

challenge him. Case instructors usually encourage innovative ways of looking at and

analyzing problems, and arriving at possible alternatives.

The interaction among students, and between the students and the instructor, must

take place in a constructive and positive manner. Such interactions help to improve

the analytical, communication, and interpersonal skills of the students.

Students must be careful that the contributions they make to the discussion are

relevant, and based on a sound analysis of the information presented in the case.

Students can also refer to the notes they have prepared during the course of their

preparation for the case discussion.

The instructor may ask questions to the class at random about the case study itself or

about the views put forward by an individual student. If a student has some new

insights about the issues at hand, she is usually encouraged to share them with the

class.

Students must respond when the instructor asks some pertinent questions. The

importance of preparing beforehand cannot be emphasized enough – a student will be

able to participate meaningfully in the case discussion only if he is knowledgeable

about the facts of the case, and has done a systematic case analysis. A case discussion

may end with the instructor (or a student) summarizing the key learning points (or

‘takeaways’) of the session.

Student performance in case discussions is usually evaluated, and is a significant

factor in assessing overall performance in the course. The extent of participation is

never the sole criterion in the evaluation – the quality of the participation is an equally

(or more) important criterion.

Working in a Group

If a group of students is asked to analyze a case, they must ensure that they meet to

discuss and analyze the case, by getting together for a group meeting at a suitable time

and location. Before the meeting, all the team members must read the case and come

with their own set of remarks/observations.

The group must ensure that all the group members contribute to the preparation and

discussion. It is important that the group is able to work as a cohesive team –

problems between team members are likely to have an adverse impact on the group’s

overall performance.

PREPARING A WRITTEN CASE ANALYSIS

Quite often, a written analysis of the case may be a part of the internal evaluation

process. When a written analysis of a case is required, the student must ensure that the

analysis is properly structured.

An instructor may provide specific guidelines about how the analysis is to be

structured. However, when submitting an analysis, the student must ensure that it is

neat and free from any factual, language and grammar errors. In fact, this is a

requirement for any report that a student may submit – not just a case analysis.

l

6

Learning with Cases

MAKING A CASE PRESENTATION

The instructor may ask a group of students to present their analysis and

recommendations to the class. Alternatively, an individual student can also be asked

to make a presentation.

The key to a good presentation is good preparation. If the case has been studied and

analyzed thoroughly, the content of the presentation should present no problems.

However, a presentation is more than the content. Some of points that need to be kept

in mind when making a case presentation are:

As far as possible, divide the content uniformly so that each team member gets an

opportunity to speak.

Use visual aids such as OHP slides, Power Point presentations,

advertisement/press clippings etc., as much as possible.

Be brief and to-the-point. Stick to the time limits set by the instructor.

Be well prepared.

EVALUATING STUDENT PERFORMANCE

The evaluation of a student’s performance in a case-driven course can be based on

some or all of the following factors:

Written case analyses (logical flow and structuring of the content, language and

presentation, quality of analysis and recommendations, etc.).

Case presentations (communication skills, logical flow and structuring of the

content, quality of analysis and recommendations, etc.).

Participation in classroom case discussions (quality and extent of participation).

Case writing assignments or similar projects.

Case-based examinations.

BENEFITS FROM THE CASE METHOD

The case benefit has several advantages over traditional teaching methods. The skills

that students develop by being exposed to this method are listed in Exhibit 2. The

consequences to the student from involvement in the method are listed in Exhibit 3.

Some of the advantages of using case studies are given below:

Cases allow students to learn by doing. They allow students to step into the shoes

of decision-makers in real organizations, and deal with the issues managers face,

with no risk to themselves or the organization involved.

Cases improve the students ability to ask the right questions, in a given problem

situation. Their ability to identify and understand the underlying problems rather

than the symptoms of the problems is also enhanced.

Case studies expose students to a wide range of industries, organizations,

functions and responsibility levels. This provides students the flexibility and

confidence to deal with a variety of tasks and responsibilities in their careers. It

also helps students to make more informed decisions about their career choices.

7

Learning with Cases

Source: Michiel R. Leeenders, Louise A. Mauffette-Launders and James Erskine, Writng Cases (Ivey Publishing, 4th edition) 7.

Source: 1993, C. C. Lundberg and C. Enz, ‘A framework for student case

preparation’, Case Research Journal, 13 (Summer) 134/ Michael A. Hitt, R. Duane

Ireland and Robert E. Hoskisson, Strategic Management (Thomson Southwestern, 6th

Edition) Cii.

Cases studies strengthen the student’s grasp of management theory, by providing real-life examples of the underlying theoretical concepts. By providing rich, interesting information about real business situations, they breathe life into conceptual discussions.

Exhibit 2

Inventory of Skills Developed by the Case Method

1. Qualitative and quantitative analytical skills, including problem identification

skills, data handling skills and critical thinking skills.

2. Decision making skills, including generating different alternatives, selecting

decision criteria, evaluating alternatives, choosing the best one, and

formulating congruent action and implementation plans.

3. Application skills, using various tools, techniques and theories.

4. Oral communication skills, including speaking, listening and debating skills.

5. Time management skills, dealing with individual preparation, small group

discussion and class discussion.

6. Interpersonal or social skills, dealing with peers, solving conflicts and

practicing the art of compromise, in small or large groups.

7. Creative skills, looking for and finding solutions geared to the unique

circumstances of each case.

8. Written communications skills, involving regular and effective note-taking,

case reports and case exams.

Exhibit 3

Consequences of Student Involvement with the Case Method

1. Case analysis requires students to practice important managerial skills-

diagnosis, making decisions, observing, listening, and persuading – while

preparing for a case discussion.

2. Cases require students to relate analysis and action, to develop realistic and

concrete actions despite the complexity and partial knowledge characterizing

the situation being studied.

3. Students must confront the intractability of reality-complete with absence of

needed information, an imbalance between needs and available resources,

and conflicts among competing objectives.

4. Students develop a general managerial point of view – where responsibility is

sensitive to action in a diverse environmental context.

l

8

Learning with Cases

Cases provide students with an exposure to the actual working of business and other organizations in the real world.

Case studies reflect the reality of managerial decision-making in the real world, in that students must make decisions based on insufficient information. Cases reflect the ambiguity and complexity that accompany most management issues.

When working on a case study in a group, students must also be able to understand and deal with the different viewpoints and perspectives of the other members in their team. This serves to improve their communication and interpersonal skills.

Case studies provide an integrated view of management. Managerial decision-making involves integration of theories and concepts learnt in different functional areas such as marketing and finance. The case method exposes students to this reality of management.

Lessons in Customer Service from Wal-Mart

“We are agents for our customers. We want to sell them what they want to buy, and

the name of the game is who can most efficiently deliver that merchandise from raw materials to the customer.” 1

- David Glass, former President, CEO and CFO, Wal-Mart.

“The secret of successful retailing is to give your customers what they want. And

really, if you think about it from your point of view as a customer, you want

everything: a wide assortment of good quality merchandise; the lowest possible prices; guaranteed satisfaction with what you buy; friendly, knowledgeable service;

convenient hours; free parking; a pleasant shopping experience.”2

- Sam Walton, founder of Wal-Mart.

INTRODUCTION

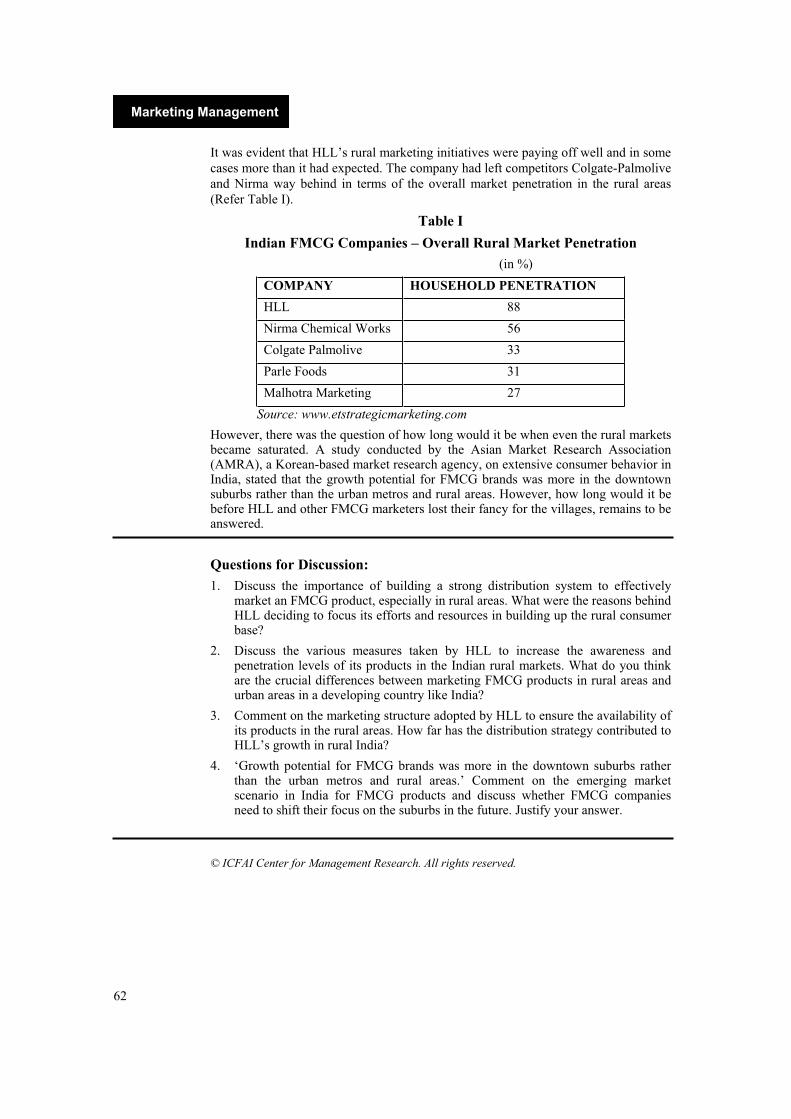

In March 2003, Fortune magazine ranked Wal-Mart as the world’s largest and America’s most admired company (Refer Exhibit I for awards and recognitions conferred on Wal-Mart). Fortune’s Managing Editor, Rik Kirkland, commented, “Eleven years after Sam Walton’s death, Wal-Mart, the company he founded, not only has grown tenfold to become the world’s biggest but also is now the world’s and America’s most admired. Best of all, Walton’s successors have achieved this unprecedented feat by preserving the unpretentious, relentlessly customer-focused culture.”3 In November 2002, Wal-Mart was ranked #1 by the customers in the 2002 department store customer satisfaction study, conducted by a leading consultancy firm, JD Power & Associates4 (Refer Exhibit II).

Since its inception, Sam Walton (Walton) had cultivated a customer-focused culture at Wal-Mart. In his autobiography “Sam Walton – Made in America: My Story,” Walton stated ten rules that he followed in managing his company (Refer Exhibit III). One of the rules said, “Exceed your customer’s expectations. If you do they’ll come back over and over. Give them what they want – and a little more. Let them know you appreciate them. Make good on all your mistakes, and don’t make excuses – apologize. Stand behind everything you do. ‘Satisfaction guaranteed’ will make all the difference.” The rule reflected Walton’s commitment to his customers.

Apart from being one of the core elements of its culture, Wal-Mart’s pursuit to

provide the best customer service had its effect on the pricing and purchasing policies

of the company. On the importance of providing customers value for their money,

Walton said, “We believe in the value of the dollar. We exist to provide value to our

customer, which means that in addition to quality and service, we have to save them

money. Every time Wal-Mart spends one dollar foolishly, it comes right of our

1 As quoted in the article, “In retailing, the rich are getting richer, and many of the poor will fall by the wayside”, by Sawaya, Z., in Forbes dated January 6, 1992.

2As quoted in the article, “Walmart.com, background information”, posted on www.walmart.com.

3 As quoted in the article, “The World's Most Admired Companies” by Paola Hjelt, Fortune,March 3, 2003.

4 Headquartered in California, JD Power and Associates is a global marketing information services firm that helps businesses and consumers make better decisions through credible and easily accessible customer-based information.

12

Marketing Management

customers’ pockets. Every time we save them a dollar, that puts us one more step

ahead of the competition – which is where we always plan to be.”5

Wal-Mart was one of the first few companies in the retailing industry to use IT to

offer value-added services to customers. Commenting on Wal-Mart’s venture into e-

business through the launch of its site, Wal-Mart spokeswoman, Melissa Brown, said,

“It is yet another way for us to take care of our customers.”6

WALTON – A CUSTOMER-FOCUSED LEADER

In July 1962, Walton – an economics graduate from the University of Missouri, established the first Wal-Mart Discount City in Rogers, a small town in the state of Arkansas, USA. He laid down three principles that later became an integral part of Wal-Mart’s culture. The principles were – respect for the individual, striving for excellence, and service to customers.

Wal-Mart’s employees, also known as associates, were given a place of importance in Walton’s scheme. Walton believed that if employees were respected and treated well, they would in turn treat the customers with respect, and satisfied customers would continue their relationship with Wal-Mart. Associates were encouraged to come up with innovative ideas to solve their day-to-day problems, set new performance goals, make their work enjoyable and strive for excellence. They conducted meetings, known as “grassroots”, where they discussed ways and means to improve their performance. Walton emphasized the importance of keeping overall operating expenses low, so that the benefits could be reaped by both the company, through enhanced profitability, and by the customers, through reduced prices.

Customers were the focus of all activities at Wal-Mart. To highlight the significance of customers, Walton had laid down rules for employees which read as follows:

Rule # 1: The customer is always right.

Rule # 2: If the customer happens to be wrong, refer to Rule # 1.

He used to say to his employees, “There is only one boss – the customer. And he can fire everybody in the company, from the chairman down, simply by spending his money elsewhere.”7

In his efforts to maximize customer satisfaction, Walton implemented several innovative practices in Wal-Mart. The employees were asked to display ‘aggressive hospitality,’ that is, the employees were encouraged to provide customer service which was beyond their expectations.

Such displays of aggressive hospitality enhanced Wal-Mart’s reputation as a customer-focused company. In one instance, Dremia Meier, an associate saved the life of a customer by conducting cardiopulmonary resuscitation (CPR).8 When she noticed that a customer in the parking lot had suffered a mild stroke, she immediately rushed to him and performed CPR, with the help of another associate, until the ambulance arrived. The customer’s life was saved and the manager of the Wal-Mart store later called on the customer at the hospital to enquire about his health.

5 As quoted in the book, “Sam Walton, Made in America: My Story”, by Sam Walton and John Huey, Page 13.

6 As quoted in the article, “A leader beyond bricks and mortar,” in Discount Store News, dated October 1999.

7 As quoted in the article “CRM's Not Just a Buzzword, It’s a Sound Business Principle,” by Aljosja Van Dorssen, Business Times, April 1, 2002.

8 CPR involves external cardiac massage and artificial respiration. This exercise attempts to restore circulation of the blood and prevents death/brain damage due to lack of oxygen in a person who has collapsed and has no pulse/stopped breathing.

13

Lessons in Customer Service from Wal-Mart

The customers were viewed and treated as guests at Wal-Mart. The company was known for its ‘greeters’ who greeted the customers with a warm welcome and a friendly smile, the moment they entered a store. They offered the customers shopping carts and conveyed them that Wal-Mart was glad to have them at the store. Regular customers at Wal-Mart were made to feel special by being addressed by name. Whenever Walton or any other noted dignitary visited a store, or on any occasion (like company meetings), the employees greeted them with the famous ‘Wal-Mart Cheer’ (Refer Exhibit IV), which ended by addressing the customer as “#1 at Wal-Mart.”

As soon as customers entered the store, the store associates looked after them completely. If customers asked where a product could be found, they were not merely shown the way, but were actually accompanied to the correct location. Even customers making low-value transactions were treated with the same respect and courtesy. All customers were allowed to exchange products or seek refunds for products if they wished.

Other practices at Wal-Mart for the benefit of customers were the “Sundown rule” and the “10-foot attitude rule.” According to the Sundown rule, associates had to resolve all service-related requests made by customers before the sun set. The rule aimed to induce a sense of urgency in meeting customer service requests. The quick response to customer calls demonstrated Wal-Mart’s dedication to better customer service. In most cases, the customers’ problems were dealt with immediately. In case they were not put right the same day, the associates kept the customers informed about the action being taken.

Employees followed the Sundown rule with complete dedication as could be seen on several occasions. In one particular instance, Jeff, a pharmacist at one of the Wal-Mart stores got a late night call from one of his customers, who was a diabetic patient. The customer said that she had mistakenly dropped her insulin in her garbage disposal bin. Conscious that it would be risky for a diabetic to be without insulin, Jeff immediately rushed to the store and saw to it that the insulin was delivered to the customer.

Employees also followed the ‘ten-foot attitude’ rule which stated that whenever an employee was within a distance of 10 feet from a customer, he had to look into the customer’s eyes, greet him/her, and ask if he could be of any help. The employees practiced this rule without slacking. To encourage employees to provide the best customer service, Walton would say, “Let’s be the most friendly – offer a smile of welcome and assistance to all who do us a favor by entering our stores. Give better service – over and beyond what our customers expect. Why not? You wonderful, caring associates can do it, and do it better than any other retailing company in the world . . . exceed your customers’ expectations. If you do, they’ll come back over and over again.”9

WAL- MART’S CUSTOMER- CENTRIC POLICIES

Since the very beginning, Wal-Mart’s pricing policies were based on the recognition that consumers always wanted the best bargain on the products purchased by them without compromising on the quality. Walton had used the captions –“We Sell for Less” and “Satisfaction Guaranteed” on the very first Wal-Mart signboard.

Wal-Mart followed what it called the Every Day Low Price (EDLP) policy. The policy was that Wal-Mart would always provide a wide variety of high quality, branded and unbranded products at the lowest possible price, offering better value for the customer’s money. A Wal-Mart advertisement explained: “Because you work hard for every dollar, you deserve the lowest price we can offer every time you make a

9 As quoted in the article, “Exceeding customer expectations,” posted on www.walmart.com.

14

Marketing Management

purchase. You deserve our Every Day Low Price. It’s not a sale; it’s a great price you can count on every day to make your dollar go further at Wal-Mart.”10

EDLP was extremely attractive to customers and emerged as the key contributor to Wal-Mart’s success over the years. Several initiatives the company took were based on the EDLP policy. For instance, Wal-Mart made heavy investments in technology to improve efficiency in distribution. Tim Crane, regional buyer for Wal-Mart said, “I’m proud to say EDLP has always been the philosophy of Wal-Mart. We offer value every day. Customers don’t have to wait for sales. We distribute 13 circulars a year, two during the Christmas period, one a month otherwise, and it is a rare day that we do any off-price advertising. We are not interested in co-op monies, exchanging terms, guaranteed sales, or any other deals which we feel add to the cost of the merchandise. We simply want the lowest net cost – we call that net down pricing. For EDLP to be successful, you must drive all the unnecessary costs out of the equation. When vendors work with the appropriate Wal-Mart buyers, they will, I assure you, work to achieve that.”11

Wal-Mart also introduced ideas like “rollback” of prices and “special buys” to

enhance customer satisfaction. Under the “rollback” program, Wal-Mart made a

commitment to its customers to reduce prices, whenever and wherever it could, and

pass on the maximum savings to them. Whenever the company was able to reduce the

procurement costs of products due to greater efficiency in its operations and supply

chain management practices, it cut prices, passing on the benefits to customers. When

prices were rolled back, a yellow “rollback smiley” logo appeared on the products in

the store racks. Under the “special buy” pricing program, products marked with the

‘special buy’ logo, had extra quantity of the same product or a new product, offered

for a limited period.

Offering the best price to its customers formed the basis for Wal-Mart’s purchasing

policies. Wal-Mart sourced merchandise directly from manufacturers. By eliminating

the middlemen, Wal-Mart was able to sell to customers at lower prices, and in turn

benefited from the large volumes of business generated. When Wal-Mart emerged as

the leading company in the retailing industry, manufacturers actually competed with

each other to offer Wal-Mart the best prices. Wal-Mart’s relationship with

manufacturers later evolved from a normal transaction-oriented relationship to a more

comprehensive vendor-retailer relationship, in which they became partners in their

drive to serve the customer in the best possible manner.

At the store level, customer service was a highly focused activity. Each Wal-Mart

store was required to cover the customers in the surrounding area. The store managers

were regularly updated on which products were moving and which were not. Based on

this information and an assessment of the tastes and preference of the consumers in

the vicinity of the store, Wal-Mart’s employees decided which goods to stock and

how to arrange them inside the store. Commenting on the importance of customer

service at Wal-Mart, Tom Coughlin, President and Chief Executive Officer, Wal-Mart

Stores division, said, “Wal-Mart's culture has always stressed the importance of

customer service. Our associate base across the country is as diverse as the

communities in which we have Wal-Mart stores. This allows us to provide the

customer service expected from each individual customer that walks into our stores.”12

The customer friendly policies of Wal-Mart, coupled with its major expansion drive

enabled the company to register significant growth rates during the 1970-2000 period.

10 As quoted in the article, “Pricing Philosophy,” posted on www.walmart.com. 11 As quoted in the article, “Wal-Mart’s top ten” by Loretta Roach, in Discount Merchandiser,

dated August 1993. 12 As quoted in the heading titled, “Three Basic Beliefs,” posted on www.walmart.com.

15

Lessons in Customer Service from Wal-Mart

During the 1970s, Wal-Mart’s sales increased from $31 million to $1.2 billion, a

significant growth rate of 287%. In the same period, the number of Wal-Mart stores

increased from 32 to 276. The growth continued in the 1980s with Wal-Mart’s sales

increasing at a compounded annual rate of over 36%. Wal-Mart’s growth in the 1980s

was fuelled by the introduction of the Sam’s Wholesale Clubs13 in 1983, and the

Hypermart (which was later known as Super Center14) in 1987.

In Wal-Mart’s annual report (1986-87), Walton again stressed on providing the best customer service in order to maintain its past successes. He said, “The key to success must be that we will all truly embrace the philosophy that our sole reason for being is to serve, even spoil those wonderful customers. To keep this focus on customer service despite our continuous change is just as critical today as it was in those dine stores thirty years ago.”

USING IT FOR CUSTOMER DELIGHT

Wal-Mart made heavy investments in IT in the 1980s. In the early 1980s, the

company began to use Electronic Data Interchange (EDI) systems. EDI linked the

computers at the stores and the distribution centers. It helped the company track the

movement of goods in real-time and quickly replenish the stock at the stores. EDI

helped in minimizing the incidences of stock-outs and enabled better inventory

management. The system eliminated the inconvenience to customers due to the non-

availability of products.

In 1987, Wal-Mart installed a satellite communication system, costing an estimated

$700 million. The system connected the stores, distribution centers and the suppliers’

systems and automated the entire distribution process of the company. The system

also connected all the stores of the company with the General Office with 2-way voice

and data communication, and one-way video communication.

Although logistical systems were installed earlier, it was only in the late 1980s that

Wal-Mart started thinking seriously of using IT to get more customer-related

information. Wal-Mart’s management realized that the rapid rate, at which the

company was expanding, was making it increasingly difficult to cater effectively to

the diverse needs of millions of consumers. Consumers’ buying habits, needs and

preferences differed from one area to another. Goods that were popular in one store

were not as popular in others. Wal-Mart therefore began investing in data

warehousing systems.

In 1989, Wal-Mart started building a huge database of customer information in its

data warehouse systems located at its headquarters at Bentonville, Arkansas. The

company collected sales and customer related information for each store and fed that

information into the warehouse systems. The data warehouse served as a storehouse of

data, but a proper analysis of the data was required to gain insights into consumers’

needs and preferences and their buying patterns. For this purpose, the company used

13 Sam’s Club was a club chain with a large store in warehouse-type buildings targeted at small business owners and bulk merchandise buyers. At low prices and with an annual membership fee, customers could make huge savings on the merchandise at Sam’s Clubs. The club provided branded merchandise and around 4,000 items like tires, cameras, batteries, watches, office supplies, cocktail sausages, soft drinks, clothing, home furnishings, auto supplies, etc.

14 A Supercenter was smaller than the hypermart and was an extension of the discount store. It was a combination of discount and grocery stores under one roof. It stocked food products and other necessities in a single retail outlet as a one-stop shopping facility. Each Supercenter was between 97,000 to 211,000 square feet and employed 200 to 550 associates.

16

Marketing Management

data mining15 tools that could be used to analyze information relating to the products

being sold upto the store level, and to determine the demographic and ethnic profile of

customers within the vicinity of a store, how frequently each product had to be

replenished and so on.

In the early 1990s, Wal-Mart continued to employ new technologies to facilitate better analysis of customer data as they became available. Wal-Mart’s IT experts used 3-D visualization tools to make accurate estimates of products most likely to be bought by customers on the basis of parameters such as ethnicity, geographic location, weather patterns, local sports affiliations, and around 10,000 other varied parameters. Wal-Mart made around 90% of its stock replenishments every month, based on the analysis of customer data generated through the data warehouse.

To make shopping at Wal-Mart a pleasant experience, Wal-Mart installed customer information kiosks16 in its stores in 1996. The kiosks helped customers find out the price of any product and get a brief description of it. Each Wal-Mart store had between two and five kiosks. To help customers locate a product which was out of stock in a particular store, Wal-Mart introduced an innovative hand-held product-locating devise called 960. If a customer found that a particular item was not available at a store, the store associate would enter the item number in the 960. The 960 would then indicate the nearest Wal-Mart store (within a 30-40 mile radius) that had the item, the location of the store, its telephone number and the quantity of the items left at the store. This helped customers find out where the item was available. The store associate also arranged for the product to be brought to the store, if needed urgently. The 960 device got a very positive response from customers.

In 1996, Wal-Mart launched its website – www.walmart.com – to provide information to its customers on all the products it stocked and to enable online sales. The online sales site had plenty of user-friendly features. For prompt delivery of the goods ordered online, Wal-Mart tied up with Fingerhut, a US-based direct marketing company. The customers who registered themselves at the site could access the features on the site directly. The site contained a store map. On entering their local zip code, the customers were linked to a Wal-Mart store in their area. They could make an online enquiry regarding the availability of a particular product in that store and order it.

The site also had advance features to ensure the security of online credit card transactions. It was also connected to a call centre, through which the customers could place their enquiries and grievances. The customers registered on the site were kept informed about in-store events such as sales promotions, price rollbacks, or ‘special buys’ in the Wal-Mart store in their area.

The website also had some customer service tools, such as Netflix, which enabled customers to report a package lost in the mail. The customer had to click on the relevant icon on the screen, and Wal-Mart would send the required product to the customer.

IT played an important role in improving the efficiency of operations at Wal-Mart. The benefits which accrued were passed on to customers, as per Wal-Mart’s policy. Wal-Mart’s Annual Report 1999 said, “The first and the most important thing about Wal-Mart’s information systems is precisely that the customer’s needs come first. By using technology to reduce inventory, expenses and shrinkage, we can create lower prices for our customers and better returns for our shareholders.”

15 Data mining means the extraction and analysis of data from a data warehouse. It has applications in many areas of business. Buyers can use it to keep store shelves adequatelystocked, marketers can use it in store design and advertising, and business analysts can use it for stock projections.

16 Computer terminals installed at several locations in the stores.

17

Lessons in Customer Service from Wal-Mart

RECENT CUSTOMER SERVICE INITIATIVES

At the dawn of the new millennium, Wal-Mart was one of the world’s largest companies, with revenues of $165 billion in fiscal 2000. Banking on its past success, Wal-Mart renewed its emphasis on customers and launched new initiatives to serve its customers better. One such initiative was the ‘store of the community’ program, launched in 2001. Under the program, Wal-Mart began remodeling its discount stores and super centers in the US to fulfill the needs of customers they served, in line with what the customers wanted. Explaining the program, Tom Coughlin, President and CEO of Wal-Mart Stores Division, said, “The one-size-fits-all concept simply doesn’t work anymore in the retail industry. Customers tell us what they want and it is our responsibility to meet those needs. Our store associates live and work in each store’s community and interact with over 100 million customers each week. If we utilize information from all available resources including customers, associates and suppliers, our store will reflect the interests of its community. We will sell merchandise the customers want to buy, not merchandise we want to sell. By accomplishing this goal, we create happy, satisfied customers because they can now complete all of their shopping in one location - our store.”17

Wal-Mart’s ‘store of the community’ program made effective use of bar code technology18 and advanced data mining techniques. The bar-code on each product sold in Wal-Mart’s stores was scanned at the time of billing. This enabled Wal-Mart to capture sales and customer details such as the product being purchased, its price, when it was purchased and by whom, and the other products in a customer’s shopping cart. This information was taken together with the demographics of the communities in the vicinity of the store, consumer feedback on various products, and the suggestions on various products made by the store associates.

A direct consequence of the ‘store of the community’ program was that the merchandize mix of a Wal-Mart store in one region differed substantially from that of another. For instance, a Wal-Mart store in a middle-income area in Decatur, Georgia, east of Atlanta, with a majority black population stocked African-American angels and ethnic Santas, as part of its Christmas decoration display. The music department in the store had more albums of black pop stars. In contrast, another Wal-Mart store, located in the high-income suburbs of Northern Atlanta, an area with a majority of white population, stocked pop-albums of popular country stars, and its music section had costlier items.

Similarly, the manner in which the products were displayed differed from one store to another. For instance, a Wal-Mart store located in Mountain View, California, which served the predominantly young and adventurous Silicon Valley population, had attractive displays of mountain bikes and had health supplements on offer. In contrast, a Wal-Mart store in Union city, California, surrounded by blue-collar employees stocked more of electronic items like home theater systems.

The program benefited Wal-Mart by increasing its sales to existing customers significantly and also attracting new customers. By stocking all the products likely to be purchased by customers at one time and one place, Wal-Mart also reaped the benefits of cross selling. For example, a store at Glen Ellyn, a suburb to the west of Chicago sold toys, batteries, stationary products, snacks and popular children VCDs for its kid customers.

17 As quoted in the article, “This store is your store,” in Wal-Mart Annual Report 2001. 18 Invented by Joseph Woodland and Bernard Silver in 1949, barcode technology was first used

commercially in 1974. The technology is used to identify the product and its price (among other details). A scanner transmits the information to a cash register or computer for action (such as printing out a receipt).

18

Marketing Management

The ‘store of the community’ program was a very successful initiative by Wal-Mart, which contributed to increased customer loyalty. By 2003, Wal-Mart was the world’s largest company, with revenues in fiscal 2002 amounting to $244.5 billion (Refer Exhibit V).

However, despite its widespread recognition and success owing to its customer-centric culture, Wal-Mart was criticized by a few of its customers, particularly for its overcrowded stores. Analysts felt that its continued focus on policies like EDLP might harness its growth prospects in the future. Expressing her dissatisfaction with Wal-Mart, a customer said, “The kind of crowd that Wal-Mart brings in can be a little scary. If I had a choice, I’d go somewhere else.”19

Questions for Discussion

1. Walton encouraged his employees by saying, “Give better service – over and beyond what our customers expect. Why not? You wonderful, caring associates can do it, and do it better than any other retailing company in the world.” Explain the role of Walton’s leadership in developing a customer-centric culture at Wal-Mart? Do you think that in order to provide the best customer-service, organizations must always follow a top-down approach? Discuss.

2. Wal-Mart’s focus on customers led to the development of several customer-centric policies. Explain how these policies benefited both the customers and the company. Do you think that providing the best customer-service is always a win-win proposition? Discuss.

3. Wal-Mart was one of the first few retailing companies to use IT in its operations as early as the 1980s. Explain how Wal-Mart used IT for the benefit of its customers.

© ICFAI Center for Management Research. All rights reserved.

19 As quoted in the article, “Meet Your Neighborhood Grocer,” by Brian O’Keefe, in Fortune, dated May 13, 2002.

19

Lessons in Customer Service from Wal-Mart

Exhibit I

Walmart’s Awards and Recognitions

Year Awards & Recognition Awarder

17th most respected company in the world and #1 most respected retailer in North America

Financial Times and PriceWaterhouse Coopers

1999

Retailer of the Century Discount Store News and Mass Market Retailers

5th most admired company in America Fortune2000

Ranked No. 5* on Fortune’s Global Most Admired Companies list – up from No. 7 in 1999

Fortune

3rd most admired company in America Fortune2001

Ranked as 8th most admired company in the world

Financial Times and Price/Waterhouse

Awarded the ‘Ron Brown’ Award for Corporate Leadership’

President of US 2002

Named #1 on the Fortune 500 list of world’s largest companies (2001)

Fortune

2003 Named the most admired company in America

Named #1 in the Fortune 500 list of world’s largest companies(2002)

Fortune

Source: www.walmartstores.com

NB:*Ranking was based on parameters like leadership selection, people-centric values and teamwork.

Exhibit II

Department Store Customer Satisfaction Study (2002)

In November 2002, J.D. Power and Associates, released the 2002 department store customer satisfaction study. The study attempted to measure the extent to which the largest moderate price and discount department stores in the US were satisfying the customers. The study was based on 2,100 telephone interviews from a representative sample of US households. Respondents include the adult in each household who most often shops in department stores and who had shopped the surveyed store in the past two months. The stores were ranked using a customer satisfaction index scale that ranged from 100 to 1,000. The parameters used to measure customer satisfaction, arranged in the order of their significance included:

Value

Sales and service associates

Services

Store environment

Merchandise

Reputation

Sales and promotion

Store location

20

Marketing Management

The top three companies in the discount department store category were:

COMPANY RANK NO.OF POINTS TOP RATINGS FROM THE CUSTOMERS FOR:

Wal-Mart 1 756 Value, Sales and service associates, Merchandise, and Sales and promotions

Target 2 744 Services, Store environment and Reputation.

Kmart 3 681 N.A

The top four companies in the moderate price category included:

COMPANY RANK NO.OF POINTS

Kohl’s 1 750

JC Penney 2 736

Mervyn’s 3 735

Sears 4 733

Adapted from the press release, “2002 Department Store Customer Satisfaction Study,” posted on www.jdpa.com, dated November 12, 2002.

Exhibit III

Walton's Rules for Building a Business

Rule 1

Commit to your business. Believe in it more than anybody else. I think I overcame

every single one of my personal shortcomings by the sheer passion I brought to my

work. I don't know if you're born with this kind of passion, or if you can learn it. But

I do know you need it. If you love your work, you'll be out there every day trying to

do it the best you possibly can, and pretty soon everybody around will catch the

passion from you - like a fever.

Rule 2

Share your profits with all your Associates, and treat them as partners. In turn,

they will treat you as a partner, and together you will all perform beyond your

wildest expectations. Remain a corporation and retain control if you like, but behave

as a servant leader20 in a partnership. Encourage your Associates to hold a stake in

the company. Offer discounted stock, and grant them stock for their retirement. It's

the single best thing we ever did.

Rule 3

Motivate your partners. Money and ownership alone aren't enough. Constantly,

day-by-day, think of new and more interesting ways to motivate and challenge your

partners. Set high goals, encourage competition, and then keep score. Make bets with

outrageous payoffs. If things get stale, cross-pollinate; have managers switch jobs

with one another to stay challenged. Keep everybody guessing as to what your next

trick is going to be. Don't become too predictable.

20 The term servant leader was used by Robert Greenleaf in his book Servant Leadership. According to Greenleaf, “The servant leader is servant first…… It begins with the natural feeling that one wants to serve, to serve first………”

21

Lessons in Customer Service from Wal-Mart

Rule 4

Communicate everything you possibly can to your partners. The more they know, the more they'll understand. The more they understand, the more they'll care. Once they care, there's no stopping them. If you don't trust your Associates to know what's going on, they'll know you don't really consider them partners. Information is power, and the gain you get from empowering your Associates more than offsets the risk of informing your competitors.

Rule 5

Appreciate everything your Associates do for the business. A paycheck and a stock option will buy one kind of loyalty. But all of us like to be told how much somebody appreciates what we do for them. We like to hear it often, and especially when we have done something we're really proud of. Nothing else can quite substitute for a few well-chosen, well-timed, sincere words of praise. They're absolutely free - and worth a fortune.

Rule 6

Celebrate your successes. Find some humor in your failures. Don't take yourself so seriously. Loosen up, and everybody around you will loosen up. Have fun. Show enthusiasm - always. When all else fails, put on a costume and sing a silly song. Then make everybody else sing with you. Don't do a hula on Wall Street. It's been done. Think up your own stunt. All of this is more important, and more fun, than you think, and it really fools the competition. "Why should we take those cornballs at Wal-Mart seriously?"

Rule 7

Listen to everyone in your company. And figure out ways to get them talking. The folks on the front lines - the ones who actually talk to the customer - are the only ones who really know what's going on out there. You'd better find out what they know. This really is what total quality is all about. To push responsibility down in your organization, and to force good ideas to bubble up within it, you must listen to what your Associates are trying to tell you.

Rule 8

Exceed your customers' expectations. If you do, they'll come back over and over. Give them what they want - and a little more. Let them know you appreciate them. Make good on all your mistakes, and don't make excuses - apologize. Stand behind everything you do. The two most important words I ever wrote were on that first Wal-Mart sign, "Satisfaction Guaranteed." They're still up there, and they have made all the difference.

Rule 9

Control your expenses better than your competition. This is where you can always find the competitive advantage. For 25 years running - long before Wal-Mart was known as the nation's largest retailer - we ranked No. 1 in our industry for the lowest ratio of expenses to sales. You can make a lot of different mistakes and still recover if you run an efficient operation. Or you can be brilliant and still go out of business if you're too inefficient.

Rule 10

Swim upstream. Go the other way. Ignore the conventional wisdom. If everybody else is doing it one way, there's a good chance you can find your niche by going in exactly the opposite direction. But be prepared for a lot of folks to wave you down and tell you you're headed the wrong way. I guess in all my years, what I heard more often than anything was: a town of less than 50,000 populations cannot support a discount store for very long.

Source: “Sam Walton, Made in America: My Story,” page nos 314-317.

22

Marketing Management

Exhibit IV

The Wal-Mart Cheer

Give me a W!

Give me an A!

Give me an L!

Give me a Squiggly!

Give me an M!

Give me an A!

Give me an R!

Give me a T!

What’s that spell?

Wal-Mart!

What’s that spell?

Wal-Mart!

Who’s number one?

THE CUSTOMER

Source: The book, “Sam Walton Made in America”, by Sam Walton and John Huey, Page 200.

Exhibit V

Wal-Mart’s Performance Milestones

YEAR SALES NET INCOME STORES

1970 31 mn 1.2 mn 32

1980 1.2 bn 41 mn 276

1990 26 bn 1 bn 1528

2000 165 bn 5 bn 2960

2003 244.5 bn 8 bn 3400

Source: Wal-Mart Annual Reports 1980, 1990, 2003.

23

Lessons in Customer Service from Wal-Mart

Additional Readings & References: 1. Weiner, S, Retailing, Forbes, January 8, 1990.

2. Edgerton, J, Netzer, B, The Biggest Blue Chips, Money, October 1990.

3. Sawaya, Z, In Retailing, The Rich are Getting Richer, and Many of the Poor Will Fall by the Wayside, Forbes, January 6, 1992.

4. Stalk Jr., G, Evans-Clark, P, Competing on Capabilities: The New Rules of Corporate Strategy, Harvard Business Review, March/April 1992.

5. Charan, Ram, Capabilities-Based Competition, Harvard Business Review, May/June 1992.

6. Life of a Salesman, Time, June 15, 1992.

7. Moore, James F, The Evolution of Wal-Mart: Savvy Expansion and Leadership,Harvard Business Review, May/June 1993.

8. Roach, Loretta, Wal-Mart's Top Ten, Discount Merchandiser, August 1993.

9. Scans Provide `Goods' For Data Warehouse, Automatic I.D. News, May 1996.

10. Schwartz, Ela, Helping Customers Help Themselves, Discount Merchandiser, January 1997.

11. Through the Eyes of a Customer, Discount Store News, March 3, 1997.

12. Harrison, Denise, Wal-Mart Taps NCR for Data Warehouse Expansion, ENT, March 19, 1997.

13. Verity, John W, Coaxing Meaning out of Raw Data, www.businessweek.com, February 3, 1997.

14. CIO Forum: Knowledge Payback, www.informationweek.com, September 14, 1998.

15. Wilcox, Joe, Torode, Christina, What CIO’s want, Computer Reseller News, September 28, 1998.

16. Holstein, William J, Sieder, Jill Jordan, Svetcov, Danielle, Data-crunching Santa, US.News & World Report, December 21, 1998.

17. Newsome, Dwight, What's the World's Largest Retailer's Customer Service Secret? Think Small. One Customer at a Time. One Associate at a Time. Business Perspectives, Summer 2000.

18. Guglielmo, Connie, Attention Shoppers, Inter@ctive Week, June 28, 1999.

19. A Leader beyond Bricks and Mortar, Discount Store News, October 1999.

20. Online, Chain Store Age, October 1999.

21. Blankenhorn, Dana, Marketers Hone Targeting, Advertising Age, June 18, 2001.

22. Johnson, Bradford C, Retail: The Wal-Mart Effect, The McKinsey Quarterly, 2002 Number 1.

23. Schoenberger, Chana R, The Internet of Things, www.forbes.com, March 18, 2002.

24. Hospel, Holly, Down the Rabbit Hole, Chase down Meetings Data for Fun and Profit,www.gwsae.org, March 2001.

25. Blankenhorn, Dana, Marketers Hone Targeting, Advertising Age, June 18, 2001.

26. Foote, Paul Sheldon, Krishnamurthi, Malini, Forecasting Using Data Warehousing Model: Wal-Mart's Experience, Journal of Business Forecasting Methods & Systems,Fall 2001.

27. Smarter, Faster, More Profitable, www.intelligententerprise.com, October 4, 2001.

28. Stankevich, Debby Garbato, Sizing the Market, Retail Merchandiser, March 2002.

29. Evans, Bob, Business Technology: The Customer's Always Right, www.informationweek.com, April 22, 2002.

30. Newman, Christine, Growing Your Revenue and Profitability: It’s All about Your Data, www.teradatamagazine.com, Third Quarter 2002.

31. 2002 Department Store Customer Satisfaction Study, www.jdpa.com, November 12, 2002.

32. Tsao, Amy, Online Retailing Finds its Legs, BusinessWeek Online, December 20, 2002.

33. Hjelt, Paola, The World's Most Admired Companies, Fortune, March 3, 2003.

24

Marketing Management

34. Sarah Marcisz, New Self Check-Out Systems in at Marion. Wal-Mart Store Has Eight Do-It-Yourself Computer Lanes, www.chronicle-tribune.com, March 8, 2003.

35. Zellner, Wendy; Sager, Ira, Fewer Smiles in the Aisles, Business Week, April 28, 2003.

36. Walmart.com., PC Magazine, May 6, 2003.

37. Kalakota, Ravi, Robinson, Marcia, From e-Business to Services: Why and Why Now?, www.informit.com, August 15, 2003.

38. Port, Otis, Arndt, Michael, Carey, John, Smart Tools, Business Week, spring 2003.

39. Bianco, Anthony, Zellner, Wendy, Brady, Diane, France, Mike, Lowry, Tom, Byrnes, Nanette, Zegel, Susan, Arndt, Michael, Berner, Robert, Palmer, Ann Therese, Is Wal-Mart Too Powerful? Business Week, October 6, 2003.

40. Kesler, Kerry, Angels' save man's life at Asheboro Wal-Mart, www.courier-tribune.com.

41. Wal-Mart, www.walmart.com.

42. Showing the Value, www.wal-mart.com.

43. www.wal-martchina.com.

The Tasty Bite Story “Tasty Bite is a company that has virtually risen from the dead.”

- A & M, in October 2000.

THE TURNAROUND

In September 1998, stock market followers were surprised when the scrip of Tasty Bite Eatables Limited (TBEL), a small Ready-to-Serve (RTS)1 food company, reached Rs 36. This was a 930% increase over its 1996 price of Rs 3.50. What was even more surprising was the fact that till September 1998, TBEL was a Board for Industrial and Financial Reconstruction (BIFR)2 case.

Launched in the early 1990s, TBEL products were rejected by Indian consumers. Analysts said that the products had been launched ‘ahead of their time’ in the Indian markets. (TBEL products were made available in a pouch, which had to be boiled before serving.)3 Moreover, the fact that the products were priced very high added to their lackluster performance.

However, TBEL not only became the first Indian company to get itself de-registered from BIFR within a year, it also emerged as the largest brand in the US ethnic foods market. In 1999, the company posted its first ever profit of Rs 4.71 million. By the end of 2000, TBEL had become a $ 5 million brand in the US retail market and its products were available in 6,000 stores across the US.

THE BACKGROUND

TBEL was formed in 1986 by Ravi Ghai (Ghai) and Ravi Kiran Aggarwal. Ghai was

also the owner of the ice-cream brand Kwality, which was the market leader with a

market share of over 50%. TBEL set up a unit to process 10,000 tonnes per annum

(tpa) of frozen vegetables and 5000 tpa of RTS foods at Khutbao and Bhandgoan

villages of Maharashtra at a cost of Rs 55.5 million. In February 1987, TBEL brought

a public issue of Rs 7.5 million. The company commenced production in February

1989 and launched its first RTS products in 1990. Following a lukewarm response in

the Indian markets, in 1991, TBEL introduced its products in the Middle East, Russia,

and the US. The company did not fare well in these markets either. The lack of a

focussed marketing approach was considered to be the main reason for its failure.

In 1992, TBEL entered into a collaboration with the beverage company Pepsi. Pepsi was interested in collaborating with TBEL because government regulations required it to generate one dollar in export sales for every dollar it earned in India. Pepsi agreed to distribute TBEL’s RTS products abroad and help TBEL upgrade its facilities. In 1994, when the government abolished the export requirement norms for MNCs, Pepsi

1 The RTS food market can be categorized into ready-to-eat foods, mixes and powders, salted snacks and sweets.

2 The Board for Industrial and Financial Reconstruction (BIFR) is responsible for the revival of companies declared sick. A company is declared sick if it has incurred losses continuously for 3 years and its networth turns negative.

3 TBEL products were cooked and pasteurized in a multi-layer pouch, using high temperature and pressure for a short period of time. This technique, called Retort Pouch Packaging, protected the food from contamination and spoilage. As a result, there was no need to refrigerate the products.

26

Marketing Management - I

decided to walk out on TBEL, claiming that it would rather concentrate on its core business of soft drinks.

In 1995, ex-Pepsi executives Ashok Vasudevan (Vasudevan) and Kartik Kilachand

(Kilachand), who had been involved with TBEL earlier while they were in Pepsi,

decided to market TBEL’s products in the US. Their US based natural food marketing

and distribution company, Preferred Brands International (PBI), acquired the

exclusive marketing rights for TBEL’s products. In 1995, PBI launched five TBEL

products in Southern California, and later expanded the business to other parts of the

country also.

By the end of 1995, TBEL was in serious financial trouble due to excessive

borrowings. Poor response to its products and poor capacity utilization took a heavy

toll on the company’s financial health. In 1996, HLL acquired the Kwality ice-cream

brand and took over Grand Foods, the holding company of Kwality Frozen Foods.

Grand Foods happened to be the holding company of TBEL as well, so TBEL now

became an HLL company. However, TBEL continued to perform badly and by March

1997, the accumulated losses touched Rs 96 million. TBEL was declared a sick unit

and referred to BIFR.

Vasudevan, who had worked with HLL for about a decade before joining Pepsi,

convinced HLL’s management to get TBEL de-registered from BIFR by providing

financial assistance. While TBEL’s equity capital remained Rs 20 million, the HLL

group turned its Rs 120 million unsecured loans into preference capital at a premium

of Rs 19.50 per share. As a result, TBEL’s net worth turned positive and the company

was de-registered from BIFR. HLL began using TBEL’s idle capacity to process its

own products and also initiated efforts to make TBEL more market savvy to survive

in the competitive markets.

THE TURNAROUND STORY

In 1997, HLL decided against venturing into the frozen foods business. Consequently, it sold TBEL to PBI. PBI appointed Ravi Nigam (Nigam) of Britannia Industries as the President. The new management worked out a strategic initiative, which was named the ‘4C approach,’ for reviving the company and turning the business around (Refer Figure I).

The four Cs strategy divided the core business into areas that needed to be focused on: Concentration, Conversion, Collaboration and Cultivation. As part of “Concentration, TBEL decided to invest in intensive research for its RTS products. The company also planned to expand its business globally as well as in India. A decision to enhance the business through e-business was also taken. The second ‘C’ of the strategy - conversion - concerned entering into conversion contracts with the National Dairy Development Board (NDDB) and the Maharashtra Agricultural Development and Fertilizer Promotion Corporation (MAFCO) for utilizing TBEL’s individual quick freezing (IQF)4 facility at its plant.

The third ‘C’- collaboration – addressed the necessity of attaining optimum utilization of TBEL plant capacities through collaborations. TBEL’s 2,000-tonne cold storage facility for storing ice cream, pulp and vegetables was leased out to HLL and Tropicana (a juice brand from Pepsi). As a result of this, capacity utilization of the plant reached 90% in 1998-99. The fourth ‘C’ - cultivation – was reflected in the initiatives taken at Bhandgaon, Maharashtra, where the company’s 25-acre farm was situated. TBEL employed the local farmers and trained them in hi-tech methods of

4 A cold storage technology, freezes cooked or raw food products at certain temperatures for retaining the texture, nutrition and good taste.

27

The Tasty Bite Story

cultivation for producing high quality vegetables. This in-house sourcing of raw material enabled TBEL to maintain quality standards besides reducing its dependence on others.

The company’s expansion plans required a considerable amount of money. Payments

for placing a product in just one store of a chain in US ranged between $ 5000 and $

10,000. Even with a narrower base of natural food store chains, it was difficult for PBI

to pay $10,000 to each of the 200 stores it had shortlisted. To overcome this problem,

the company undertook a cluster analysis study5 in various US cities and generated a

demographic profile6 of the customers they needed to concentrate on. The company

found that its potential customer’s age group was between 25-54, with average

earnings of $ 75,000 a year. This helped the company narrow its focus and reduce its

list of stores from 200 to 80. This reduced the amount of payments to be made to

stores from $ 2 million to a more manageable $ 800,000. A smaller list of stores also

led to a more focussed distribution strategy.

Unlike other Indian food companies, PBI worked very hard to offer its customers products beyond pickles, spices and papads.7 The company thus decided to launch a wider range of products specifically targeted towards local US customers. After some

5 Cluster Analysis is an analytical statistical technique that arranges research data into mutually exclusive and collectively exhaustive groups (or clusters) where the contents of each cluster are similar to each other, but different to the other clusters in the analysis.

6 Demographic Profile is based on the age, gender, life-cycle stage and occupation of consumers.

7 An Indian side dish generally made of black gram flour.

TASTY BITE

Concentration Conversion Collaboration Cultivation

RTS New Products

US Expansion

New Global Markets

India

E business

Maximize Asset Utilization

Converting existing relation-ships into long-

term contracts.

Contract Farming

Global Demo Farm

Integrated

Grading Center

Partner with Key national and Global Players

Manufacturing

Figure I

Tasty Bite’s 4 ‘C’ Strategy

The 4 C Approach

Source: A&M, October 15, 2000.

28

Marketing Management - I

intensive research, it decided to launch the Tasty Bite range in the $5 billion natural food category8 through mainstream retail chains in the US.

PBI also began advertising through sweepstakes9 at the retail level and in-store

demonstrations, thus enhancing awareness and encouraging customers to experiment.

This also helped in lowering advertising costs significantly. The company also

focused on increasing the Americans’ understanding of Indian food. PBI realized that

the average American customer was not able to understand the products being offered

and their Hindi language names did not make sense to the customers. The company

thus decided to slash the product portfolio from 25 to 8 and retained only those

products that were familiar to the American consumer. Also, products were renamed

in English for instant identification and easy understanding. Thus, ‘Palak Paneer’

became ‘Kashmir Spinach,’ ‘Navratan Korma’ became ‘Jaipur Vegetables’ and ‘Alu

Chole’ became ‘Bombay Potatoes,’ and so on. The recipes were also modified to suit

the western palate. PBI also modified the packaging to suit customer requirements.

Earlier, products were sold in pack sizes that ranged from 200 gms to 1 Kg. This was

replaced with a standard size of 300 gms, as unlike mainstream food in the US, Indian

food was not consumed in large quantities. The smaller pack size motivated the

consumers to give the products a try. By August 2001, the pack size was changed to

285 gms (10 ounces) to bring it in line with American standards of measurement. This

also meant that a store shelf now accommodated nine packs as compared to the seven

earlier.

By 1998-99, TBEL began reaping the benefits of its turnaround efforts and recorded a

net profit of Rs 4.7 million. By the end of 2000, its products were available in 27 US

states through 33 leading natural food stores and mainstream supermarkets. By 2001,

TBEL’s profits increased nearly three fold to Rs 13.42 million (Refer Table I).

According to SPINS, an agency that tracked the market shares and consumer

preferences of natural food brands in the US, TBEL was the largest brand in the

category. Bombay Potatoes (Alu Chole) had become a common side dish for many

Americans. TBEL’s entry into Holland, Switzerland and UK was also showing

positive results

Table I

Growth of Revenues and Profits

YEAR REVENUES ( Rs Million)

PROFIT (LOSS) (Rs Million)

1996-97 23.6 (17)

1997-98 36.0 (2.6)

1998-99 54.7 4.7

1999-00 90.24 10.03

2000-01 131.07 13.42

Source: Business World, August 20, 2001.

8 The natural foods category consists of products that are minimally processed and are free from artificial ingredients, preservatives and other chemicals that do not occur naturally in food.

9 Sweepstakes includes any procedure in which a person is required to purchase something, pay something of value or make a donation as a condition of awarding a prize or receiving, using, competing for, or obtaining information about a prize.

29

The Tasty Bite Story

FUTURE PLANS

In September 2000, TBEL began working towards repeating its export market success in the domestic market. TBEL divided the Indian market into two broad segments: the domestic segment focusing on working women, and the institutional segment comprising fast food restaurants, hotel chains, airline flight kitchens and the Indian Army and Navy. Nigam said, “Although Tasty Bite is the No. 1 selling Indian food brand in the US, the task in India is daunting. The challenge, therefore, is to first establish the category and then associate it with the brand.”

TBEL was optimistic that its earlier dismal performance in the domestic market would not be repeated. A national study on the food and grocery sector GROFAST (Grocery and Food Advantage Study), conducted by KSA Technopak,10 showed that 73% of Indian consumers preferred to have traditional Indian meals in the RTS format rather than western food. This attitude was mainly attributed to the shift in the preferences of consumers and readiness of Indian consumers to experiment with food. A TBEL source remarked, “In India there is a paradigm shift among women. The Indian woman is no longer just a housewife, but is more the manager of the household. Also, the working woman is not guilty about eating outside food at home. Tasty Bite products, therefore, are designed to collaborate and not compete with the new Indian woman.” TBEL management felt that the Indian market had become mature enough to appreciate the convenience and value of RTS foods.

TBEL launched its products in Pune, Mumbai, Bangalore, Chennai and Hyderabad without much advertisement and promotion support. Encouraged by the good sales reports, TBEL decided to launch the products nationally by the end of 2001. The company also decided to spend 40% of its domestic revenues to launch a billion brand-building campaign during 2001-02. TBEL also started conducting research for launching RTS sweets and non-vegetarian food.

By 2001, HLL, Dabur Foods, MTR and Amul had also entered the Rs 10 billion Indian RTS food market. TBEL planned to increase its turnover to Rs 1 billion by 2003. The company seemed to be working hard to fulfil Kilachand’s vision of becoming ‘the most respected food company in India.’

Questions for Discussion:

1. Examine Pepsi’s and HLL’s involvement with TBEL. Do you think that their fleeting interest in TBEL was disadvantageous for the company? Give reasons to support your answer.

2. A renewed focus on customer service was one of the key components in TBEL’s turnaround. Prepare a detailed note outlining the major components of TBEL’s turnaround strategy and comment on their efficacy.

© ICFAI Center for Management Research. All rights reserved.

10 Kurt Salmon Associates (KSA Technopak) is a Management Consulting firm, offering integrated strategy, process and technology deployment solutions to the Retail, Fashion, Food & Grocery and Healthcare industries.

30

Marketing Management - I

Additional Readings and References: 1. Tasty Bite in Limelight, January 26, 1998, Business Standard.

2. Sule Surekha, Tasty Bite turns savory, January 30, 1998, Indian Express.

3. Gupta Shalini, Avoid the offer, September 21, 1998, Business Standard.

4. Fernando V S, Investors begin to taste the turnaround of Tasty Bite, October 2 1999, Express India.

5. Jordan Miriam, A Pune company turns hot favorite on dining tables in US, February 28, 2000, Financial Express.

6. Jordan Miriam, Tasty Bite Eatables spices up its marketing to serve top US ethnic brand, March 1, 2000, Expressindia.com

7. Joseph K Mini, Tasty Bite eyes Nasdaq listing via ADR float, June 28, 2000, Financial Express.

8. Pande Shamni, Retailing Mother’s Recipe, July 22, 2000, Business Today.

9. Tasty Bite targets Rs 100 crore turnover by 2003, September 1, 2000. Expressindia.com

10. Krishnan Aarti, Tasty Bite Eatables: Avoid/Hold fresh Exposures, December 31, 2000, Hindu Business Line

11. Kaul Pummy, Tasty Bite's sales, ad initiatives to go national, March 22, 2001, Financial Express.

12. Tasty Bite to sink teeth into regional specialties market, April 1, 2001, The Economic Times.

13. Tasty Bite tickles southern palate, July 4, 2001, Business Standard.

14. Kohli Vanita, A Taste of India, August 20, 2001, Business World.

15. www.aandm.com

16. www.dhan.com

17. www.indiainfoline.com

18. www.tastybite.com

Unilever in India: Building the Ice Cream Business