Embed Size (px)

Citation preview

8/14/2019 Capital Structure final updated file.pdf

http://slidepdf.com/reader/full/capital-structure-final-updated-filepdf 1/15

Application of Capital Structure Theory Presented by Modigliani & Miller

in the Real W orld: Comparison of Efficient & Inefficient Market.

ABSTRACT:

Financing through debt or equity remain a challenge for firms operat ing

in efficient and inefficient markets. Different theorist presented their opinions

and research to solve this dilemma. MM theory claims to sort this problem out

under certain assumptions. Literature presents support as well as crit icism of

the MM theory. To determine the financial health of proposed theory researcherwill conduct a series of empirical analyses in efficient (London Stock Exchange)

and inefficient (Karachi Stock Exchange). The data collected will be than

compared to Dubai Stock Exchange that holds all the three assumptions

suggested MM theory. This will involve qualita tive and quantitative research

techniques. The study is designed over a period of 3 years

.

Key Words: Trade-off theory, MM theory, financial leverage, Operational

leverage, efficient markets, inefficient markets, Capital Structure, Firm

characteristics.

8/14/2019 Capital Structure final updated file.pdf

http://slidepdf.com/reader/full/capital-structure-final-updated-filepdf 2/15

8/14/2019 Capital Structure final updated file.pdf

http://slidepdf.com/reader/full/capital-structure-final-updated-filepdf 3/15

risk plus financial risk (Janauri, 2005). The underlying study will consider

capital structure and its determinants with total leverage.

Neither equi ty nor debts are the best way of determining the capital st ructure of

a firm. This ironic statement twisted the minds of researchers and financials for

years and years. As Myers (1984 ) called it capital structure puzzle. Financing

businesses is a lways a difficult but inevitable task for corporations. Companies

financing decisions involve a wide range of policy issues (Abor, 2008) . A

number of internal and external factor determine the capital structure of

company (Ilyas, n.d.) . In this regard, different types of theories were presented

on different t imes. These theories are: static trade-off theory by Miller and

Modigliani (1958) , Pecking order theory by Donaldson’s (1961 ) and the markettiming theory (Spremann, Lang, Getzmann, 2010).

According to the propositions of the MM theory: the value of a firm is

independent from its corporate financing decisions under certain conditions. In

fact MM pointed out the direction that capital structure theories must take by

showing under what conditions capital structure is irrelevant (Harris and Raviv,

1991). Titman (2001) lists some fundamental conditions that make the MM

proposit ion hold:

1. No (distortionary) taxes,

2. No transaction costs,

3. No bankruptcy costs,

4. Perfect contracting assumptions, and

5. Complete and perfect market assumption.

Since the publication of MM’s irrelevance proposition, hundreds of articles on

the theory of capital structure have been carried out in order to find out under

what conditions capital structure does matter. In other words, i t is of great

8/14/2019 Capital Structure final updated file.pdf

http://slidepdf.com/reader/full/capital-structure-final-updated-filepdf 4/15

interest to investigate if capital structure choices become relevant once one or

more of the key conditions are relaxed.

Capital structure of firms differs from each other as they get affected by an

array of factors. Some firm have high leverages while other has low. They get

themselves financed through the issuance of common stock or preferred stock in

stock market or companies acquire long term debts through institutional

financing (Brigham, & Houston, 2010). According to Fama, (1970) the primary

role of capital market is allocation of ownership of economy’s capital stock. An

in-depth study of capital market points towards “efficient market hypothesis ”.

This hypothesis propose existence of three types of markets in economies that

are strong form market, semi strong form market and weak form market; firsttwo comes under the category of efficient market, while the last is referred as

inefficient market.

Turning back to the goal of this study, MM theory holds only in efficient market

while they do not work in inefficient market. This l i terary argument needs

empirical justification for the reason this study is being designed for a

comparison among Karachi stock exchange, London stock exchange and Dubai

stock exchange.

RESEARCH QUESTION:

What i s the application of Capital Structure Theory presented by M odigli ani and Mil ler in the

real world; a comparison of eff icient and in eff icient M arkets?

8/14/2019 Capital Structure final updated file.pdf

http://slidepdf.com/reader/full/capital-structure-final-updated-filepdf 5/15

AIMS AND OBJECTIVES:

To study the capital structure differences in efficient and in efficient market

To study the implementation of MM theory in efficient and inefficient market

To compare the effects of MM theory in different economies (taxable and taxfree)

To study the asymmetric information effect on capital structure

To challenge the assumption taken by MM theory

To suggest improvements in financing theories

To add value to existing financial knowledge

SIGNIFICANCE OF THE STUDY:

The study will be significant for both academicians and practit ioners.

Academic Significance:

The study will be significant for academicians in the following ways:

1. Revisit of theory will test the propositions of MM theory which will provide the

academicians with the opportunity to make comparisons between efficient and inefficient

markets of different countries around the world.

2. It will help the academicians in identifying the gap in literature which exists in MM

theory in form of no differentiation between financing the business through debt or

equity.

3.

It will establish the comparability between different economies of the world i.e.

developed and developing. Developing economies like Pakistan are bound with taxes and

having different arrangements of capital structure as compare to the capital structure

arrangements of the developed countries.

8/14/2019 Capital Structure final updated file.pdf

http://slidepdf.com/reader/full/capital-structure-final-updated-filepdf 6/15

Practit ioner Significance:

Revisit of theory of finance will be significant for the practit ioners in the

following ways:

1. It will help the practit ioners in determining the extent of leverage.

2. It will be helpful in evaluating the optimal capital structure for the

smooth running of business.

3. It will help in determining the proportion of debt and equity in the capital

structure of the business.

4. It will help in determining the tradeoff between benefits and costs of

having debts for a business.

5. It will be useful for practit ioners as i t will find out that efficient and

inefficient markets should not be evaluated on the same propositions for

debt and equity presented in MM theory.

6. It will help the practit ioners in deciding the best determinants for the

capital structure.

8/14/2019 Capital Structure final updated file.pdf

http://slidepdf.com/reader/full/capital-structure-final-updated-filepdf 7/15

Section I has covered the introduction of the study its aims, objectives and

significance.

Section II will cover the Literature Review surrounding the MM theory.

Section III will cover the Research Methodology, data collection methods

and its paradigm.

Section IV will briefly report the time line of the thesis.

8/14/2019 Capital Structure final updated file.pdf

http://slidepdf.com/reader/full/capital-structure-final-updated-filepdf 8/15

Section II:

LITERATURE REVIEW:

In the recent years the concept of optimal capital structure was based on

asymmetric information (Abor 2008; Myer and Mujalif 1984). This means

firms prefer to finance internally if the cost of debt along with risk is high in

the market (Abor, 2008). This concept was replaced by theory presented by

Modigliani and Miller that provides an opportunity to debt financing as it

provides tax cover shield. As tax is not implementable on debts hold by

corporate, so share holders get high returns. But this income on dividing among

shareholders as profit becomes taxable.

Modigliani and Miller (1958) claim that under perfect capital market

conditions, a firm’s value depends on its operating profitabili ty rather than its

capital structure. In 1963, Modigliani and Miller (1963) fix the previous paper;

argue that, when there are corporate taxes then interest payments are tax

deductible, 100% debt financing is optimal. This means that the firm’s value

increases as debts increases.

The theory of optimal capital structure Modigliani and Miller value

invariance proposition I states that under certain conditions, the value of the

firm is independent of i ts capital structure (Firer, Ross, Westerfield and Jordan,

2008).One of these conditions is absence of tax. However, in the real world

taxes do exist and specifically interest payments on debt are tax deductible. The

value of firm will increase as the debt/equity ratio increases. Another way of

stating M&M proposition I, with taxes is that the value of levered firm is equal

to the value of firm with no debt plus the present value of the interest tax

shield. The interest tax shield is the benefit that results from the benefit that

results from the fact that profits are only taxed after tax payments have been

deducted. The tax benefits of the debt give a clear reason for the firms to

borrow rather than issue the equity ( Opler et al. , 1997).

8/14/2019 Capital Structure final updated file.pdf

http://slidepdf.com/reader/full/capital-structure-final-updated-filepdf 9/15

Along with high interests on debts here comes two primary issues, one is off

bankruptcy of a fi rm (Titman, 1984) and the other is of agency cost that arises

between mangers and shareholders of a fi rm on issuance of more and more

equity. Debt may be a good option for financing but i t put management under

stress as i t lowers the stock price (Il lyas, 2008). Damodran (2001) advised

firms to select their financing plan carefully. Otherwise they can get themselves

into the troubles.

According to the theory, the firm borrows up to the point where tax

benefit from extra rand of debt is exactly equal to the cost that comes from the

increased probability of the financial distress. The II proposition of the statictrade off theory by MM stated that when proposition I held the cost of equity as

a linear increasing function of debt/equity ratio. The proposition implied that

weighted average of these cost of capital to a firm would remain the same no

matter what combination of financing sources the firm actually chose (Miller,

1988).

Two categories of leverages are in strong connection with financial risks

and operational risks that cumulate as total risk. According to Titman and

Wessel (1988) there exist six ways to calculate financial and operational

leverage. This includes dividing long term, short term, and convertible debt by

market value and booked value turn by turn.

Capital structure is actually backed by certain factor these may vary from

firm to firm and economy to economy. Yet a consensus about certain factor exist

in li terature these factors are age of the firm, firm size, asset structure,

profitabil ity, fi rm growth, firm risk, taxation, managerial ownership, type of

business (Abor, 2008; Il lays, 2008; Song, 2005; Harris & Raviv, 1991;

Titman & Wessels 1988).

8/14/2019 Capital Structure final updated file.pdf

http://slidepdf.com/reader/full/capital-structure-final-updated-filepdf 10/15

This propels the discussion toward efficient market hypothesis; i t

describes “ stocks are always in equilibrium and it is impossible for an investor

to consistently beat the market (Brigham, & Houston, 2010). This had become

possible with easy availabi lity of information with the help of technology. Now

the question is about quality and quantity of information about a particular

market as i t determines the efficiency level of a particular stock market. First

come weak form that states all information contained in past price movements is

fully reflected in current market prices ( Fama, 1970) . Second is semi- strong

form market, here all publically available information is reflected in stock

prices (Brigham, & Houston, 2010) . Finally strong form market reflects all

pertinent information weather publically or privately available in stock prices

( i b i d . ).Here the reason for discussing these market types was related to the

intentions of investor to finance capital for a particular firm or not. As their

intention vary from company to company and industry to industry thus creating

vast difference in capital structure.

8/14/2019 Capital Structure final updated file.pdf

http://slidepdf.com/reader/full/capital-structure-final-updated-filepdf 11/15

Section III:

METHODOLOGY:

S cope of the Study

The major purpose of this study is to explore and examine the application ofMM theory in Karachi Stock Market (Inefficient Market) that will be then

compared to application of MM theory in London Stock market (Efficient

Market). For reliabili ty and validity another market fulfil l ing the assumption set

by MM theory will be introduced as Control group that will justify the results

drawn from the above stated two markets.

Research Methodology:

The preferred methodology for the study will be

“TRIANGULATION”. Triangulation is a powerful technique that facilitates validation of

data through cross verification from more than two sources. In particular, it refers to the

application and combination of several research methodologies in the study of the same

phenomenon .

It can be employed in both quantitative (validation) and qualitative (inquiry) studies.

It is a method-appropriate strategy of founding the credibility of qualitative analyses. It becomes an alternative to traditional criteria like reliability and validity.

It is the preferred line in the social sciences.

By combining multiple observers, theories, methods, and empirical materials, researchers can

hope to overcome the weakness or intrinsic biases and the problems that come from single

method, single-observer and single-theory studies.

8/14/2019 Capital Structure final updated file.pdf

http://slidepdf.com/reader/full/capital-structure-final-updated-filepdf 12/15

Data collection Methods:

Qualitative & Quantitative Techniques:

Various articles and books written by different scholars helped to gain more

information about Karachi, London, and Dubai stock markets and practical

application of MM theory its problems and potential solutions.

Following qualitative techniques and tools will be used:

Use of secondary data

Informal interviews

Focus group discussion

The major focus while collecting data from these resources will be about the

potential appl ication of MM theory in real world. Beside the above mentioned

sources, Social Science research Network website, Modigliani and Miller article

will help in the study.

Secondary data option is used to carry out the analysis and recommendationabout the application of MM theory in Karachi and London Stock Exchange.

The quantitative method provides a broad understanding of the concerns and

potential recommendations and conclusions using various scholarly works on t he

subject being investigated. The advantages of quantitative research compared to

qualitative research are given below:

It is an easy way to investigate breadth specific issues, in contrast to

qualitative method.

It is easy to collect quantitative data for inefficient markets rather

qualitative data.

The study move according to time series, while comforting researcher due

to planned occurring.

8/14/2019 Capital Structure final updated file.pdf

http://slidepdf.com/reader/full/capital-structure-final-updated-filepdf 13/15

Detailed relevant information can be obtained and participants feel no hesitation

in their findings. However the existence of relationships and exact numbers to

describe the issues is the strength of quantitative research method. Moreover it

is easy to analyse vast amounts of information to produce results especially in

time bounded environment.

The quantitative technique employed in the study will be STRUCTURED

QUESTIONNAIRE.

Research Paradigm:

“ Regardless of which paradigm you are employing, it is important that you payattention to all features and ensure that there are no contradictions and

deficiencies in your methodology ” (Collis and Hussey, 2003, p-55).

As the study employed both quantitative and qualitative methods. So, the

research paradigms for the study will be both positivism and Interpretivism.

Positivism – associated with quantitative research. Involves hypothesis testing

to obtain “objective” truth. Also used to predict what may happen at a future

date. Critical realism is a subtype of positivism that incorporates some value

assumptions on the part of the researcher. It involves looking at power in

society. Researchers primarily rely on quantitative data to do this.

Interpretivism – associated with qualitative research. Used to obtain an

understanding of the word from an individual perspective. Critical Humanism is

a subtype of the interpretive paradigm. The critical humanism approach is one inwhich the researcher involves people studied in the research process. Data is

used for social change.

8/14/2019 Capital Structure final updated file.pdf

http://slidepdf.com/reader/full/capital-structure-final-updated-filepdf 14/15

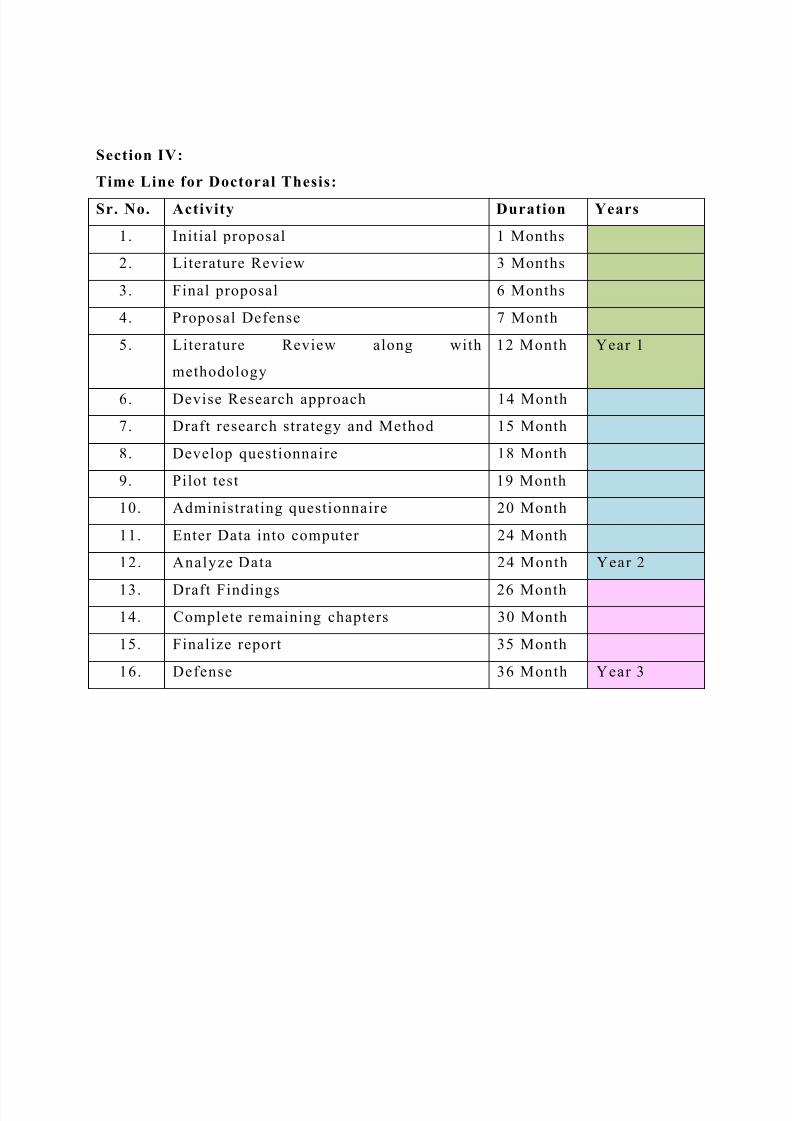

Section IV:

Time Line for Doctoral Thesis:

Sr. No. Activity Duration Years

1. Initial proposal 1 Months

2. Literature Review 3 Months

3. Final proposal 6 Months

4. Proposal Defense 7 Month

5. Literature Review along with

methodology

12 Month Year 1

6. Devise Research approach 14 Month

7. Draft research strategy and Method 15 Month

8. Develop questionnaire 18 Month

9. Pilot test 19 Month

10. Administrating questionnaire 20 Month

11. Enter Data into computer 24 Month

12. Analyze Data 24 Month Year 2

13. Draft Findings 26 Month14. Complete remaining chapters 30 Month

15. Finalize report 35 Month

16. Defense 36 Month Year 3

8/14/2019 Capital Structure final updated file.pdf

http://slidepdf.com/reader/full/capital-structure-final-updated-filepdf 15/15

References:

Illyas, J. (2008). The determinants of capital structure: Analysis of non

financial firms listed in Karachi stock exchange in Pakistan. Journal of

managerial sciences. Vol . 2(2) . Pp. 279-307. Damadoran, (2001) Corporate Finance, Theory and Practice . Wiley,

International Edition

Titman, Sheridan, and Robert Wessels, 1988, The determinants of capital

structure choice, Journal of Finance 43, 1-19.

Myers, S., and N. Majluf. (1984). “Corporate Financing and Investment

Decisions when Firms have Information that Investors do not

have.” Journal of Financial Economics 13, 187-221. Song, H-S. (2005).Capital Structure Determinants: An empirical study of

Swedish companies. Royal Institute of Technology, Center of Excellence

for studies in innovation and science, Department of Infrastructure.

Sweden

Abor, J. (2008). Determinants of the capital structure of Ghanaian firms.

African Economic Research Consortium. Research paper No. 176. Pp. 1-

29.

Modigliani, F., and M. Miller (1958). “The Cost of Capital, Corporation

Finance and the Theory of Investment.” American Economic Review 48,

261-297. 31

Titman, S. 1984. “The effect of capital structure on a firm’s liquidation

decisions”. Journal of Financial Economics , 13: 137 – 51.

Getzmann, A., Lang, Sebastian, & Spremann, K (2010). Determinents of

the target capital structure and adjustment speed evidence from Asian

capital markets. JEL-classification. pp. 1-30. Fama, E, F. (2005). Efficient capital markets II. The Journal of Finance.

Vol. 50(5). 1576-1609.

Saunders, M., Lewis, P., & Thornhill , A. (2006). Research methods for

business students. (3 r d ed.). India: Pearson Education.

![Relazione metodologica [file.pdf]](https://img.dokumen.tips/doc/110x75/586bef301a28ab6b518c0a10/relazione-metodologica-filepdf.jpg)