Embed Size (px)

Citation preview

Capital Structure Decisions

Business vs. financial risk

Capital structure theory

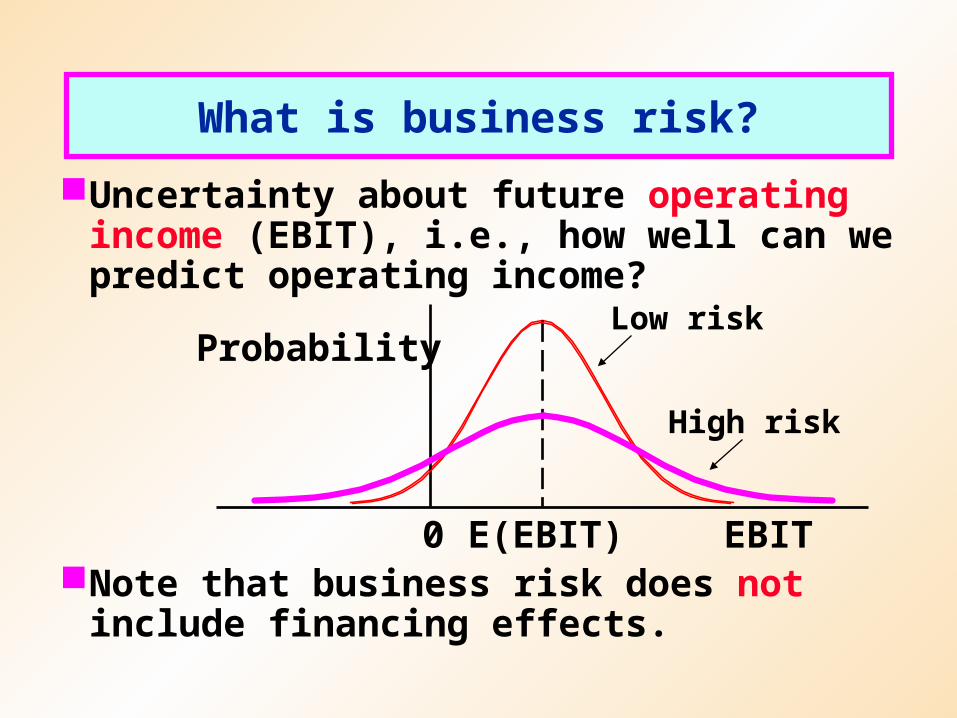

Uncertainty about future operating income (EBIT), i.e., how well can we predict operating income?

Note that business risk does not include financing effects.

What is business risk?

Probability

EBITE(EBIT)0

Low risk

High risk

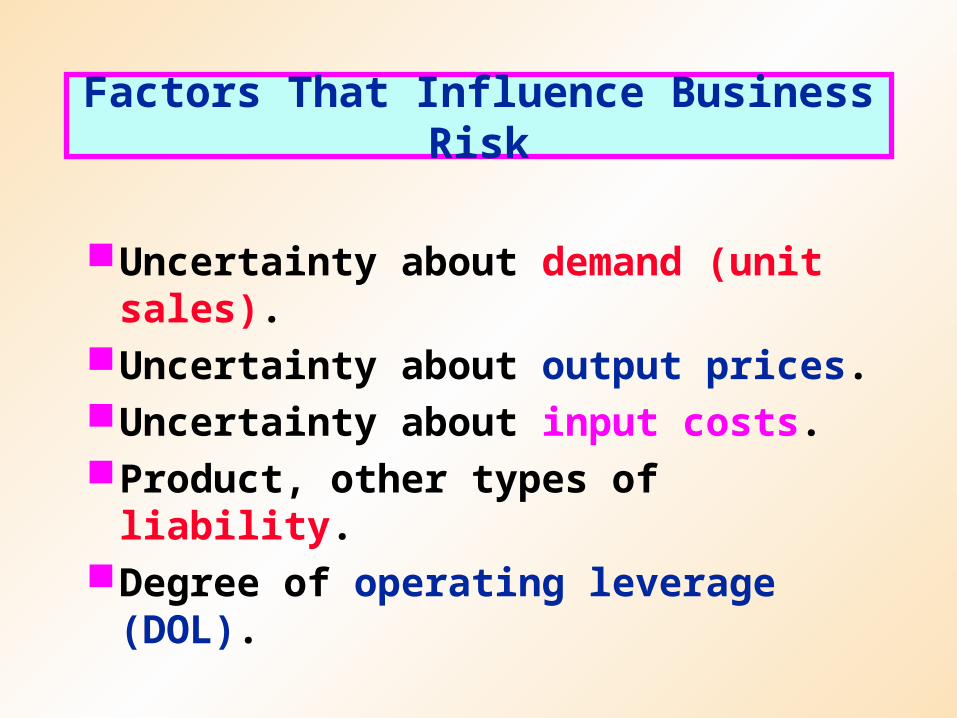

Factors That Influence Business Risk

Uncertainty about demand (unit sales).Uncertainty about output prices.Uncertainty about input costs.Product, other types of liability.Degree of operating leverage (DOL).

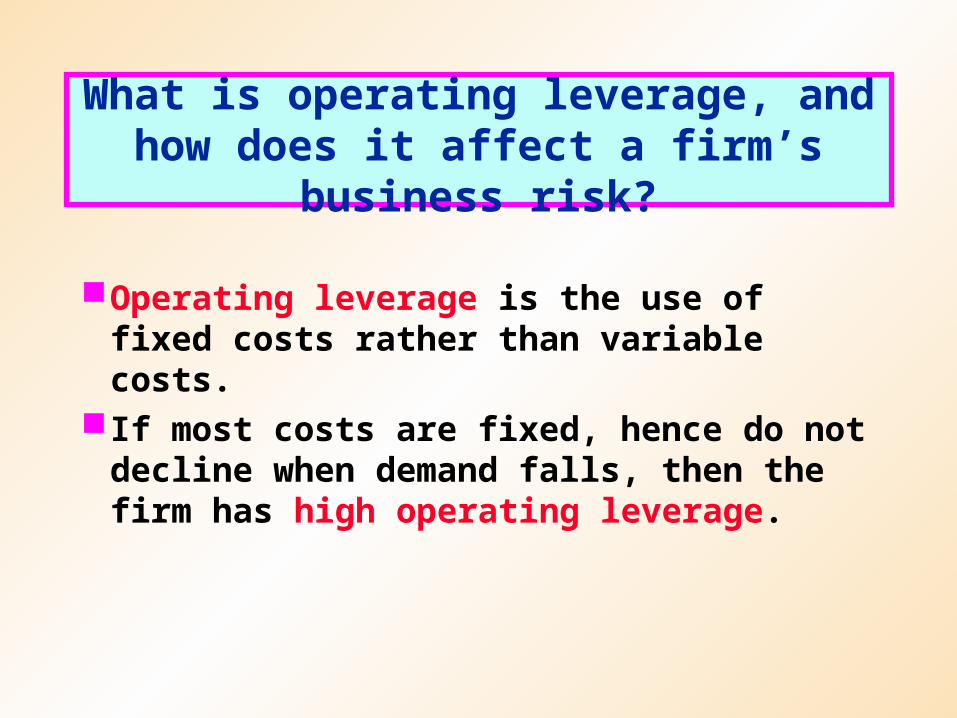

What is operating leverage, and how does it affect a firm’s business risk?

Operating leverage is the use of fixed costs rather than variable costs.

If most costs are fixed, hence do not decline when demand falls, then the firm has high operating leverage.

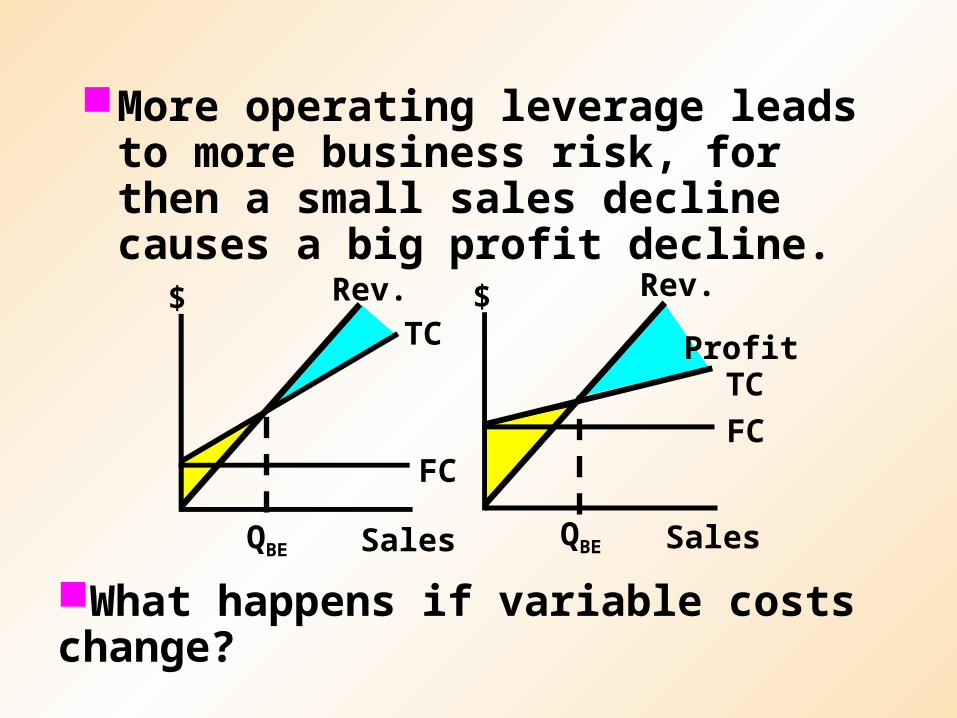

More operating leverage leads to more business risk, for then a small sales decline causes a big profit decline.

Sales

$ Rev.TC

FC

QBE Sales

$ Rev.

TC

FC

QBE

Profit

What happens if variable costs change?

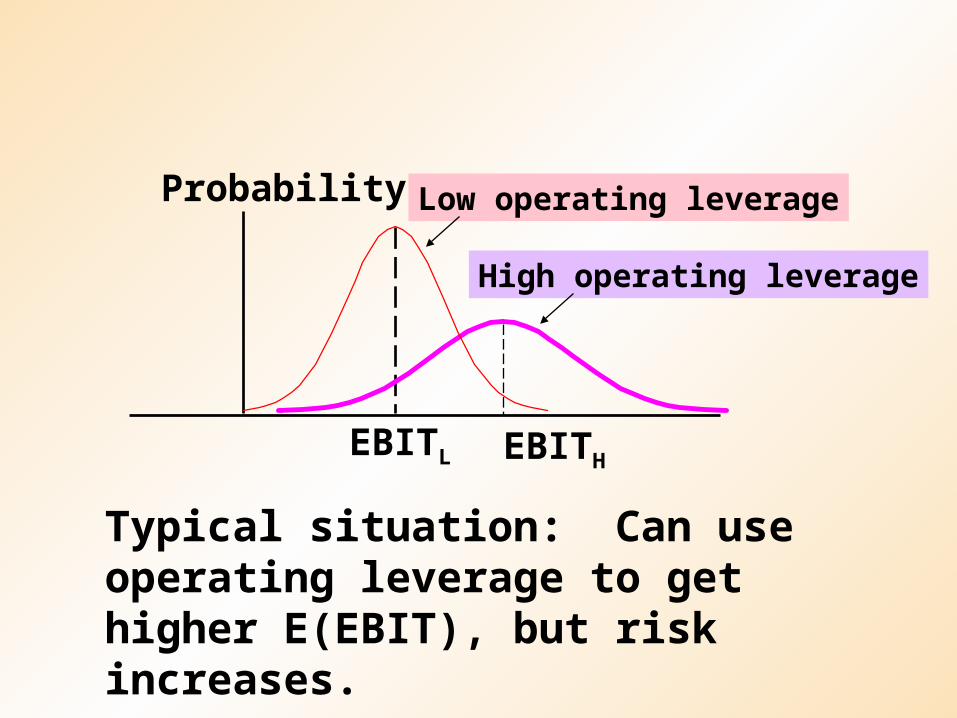

Probability

EBITL

Low operating leverage

High operating leverage

Typical situation: Can use operating leverage to get higher E(EBIT), but risk increases.

EBITH

What is financial leverage?Financial risk?

Financial leverage is the use of debt and preferred stock.

Financial risk is the additional risk concentrated on common stockholders as a result of financial leverage.

Business Risk vs. Financial Risk

Business risk depends on business factors such as competition, product liability, and operating leverage.

Financial risk depends only on the types of securities issued: More debt, more financial risk. Concentrates business risk on stockholders.

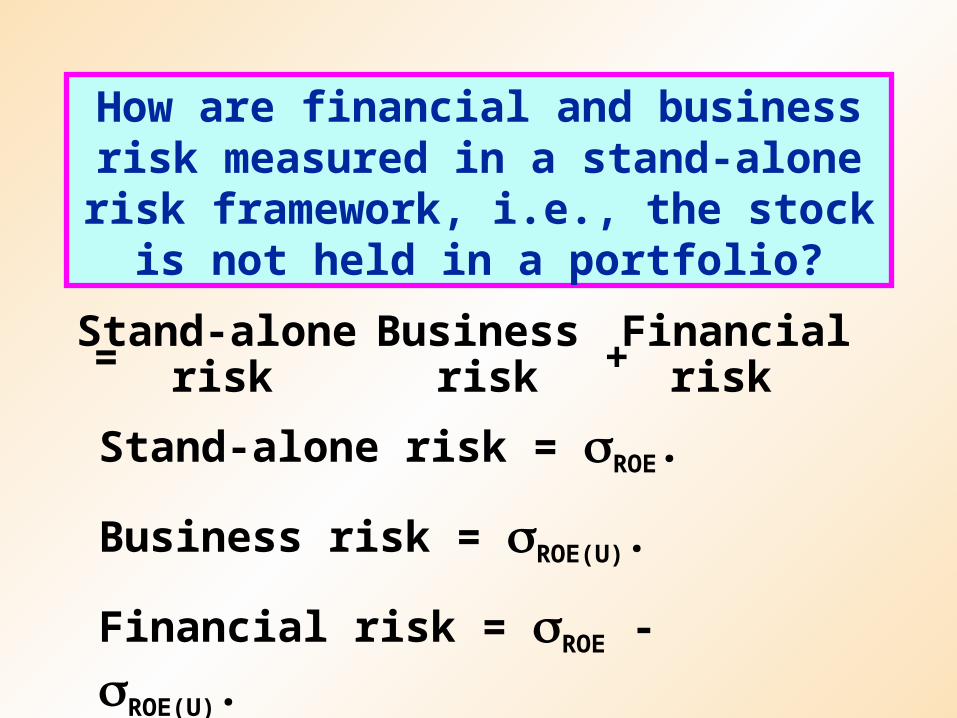

How are financial and business risk measured in a stand-alone risk framework,

i.e., the stock is not held in a portfolio?

Stand-alone Business Financialrisk risk risk= + .

Stand-alone risk = ROE.

Business risk = ROE(U).

Financial risk = ROE - ROE(U).

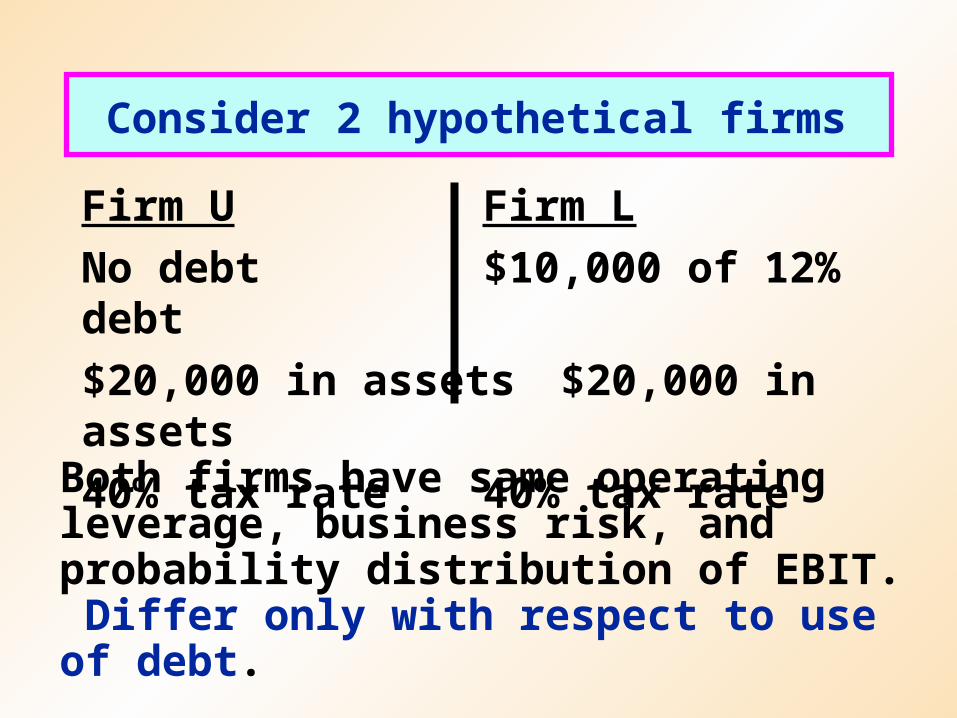

Firm U Firm L

No debt $10,000 of 12% debt

$20,000 in assets $20,000 in assets

40% tax rate 40% tax rate

Consider 2 hypothetical firms

Both firms have same operating leverage, business risk, and probability distribution of EBIT. Differ only with respect to use of debt.

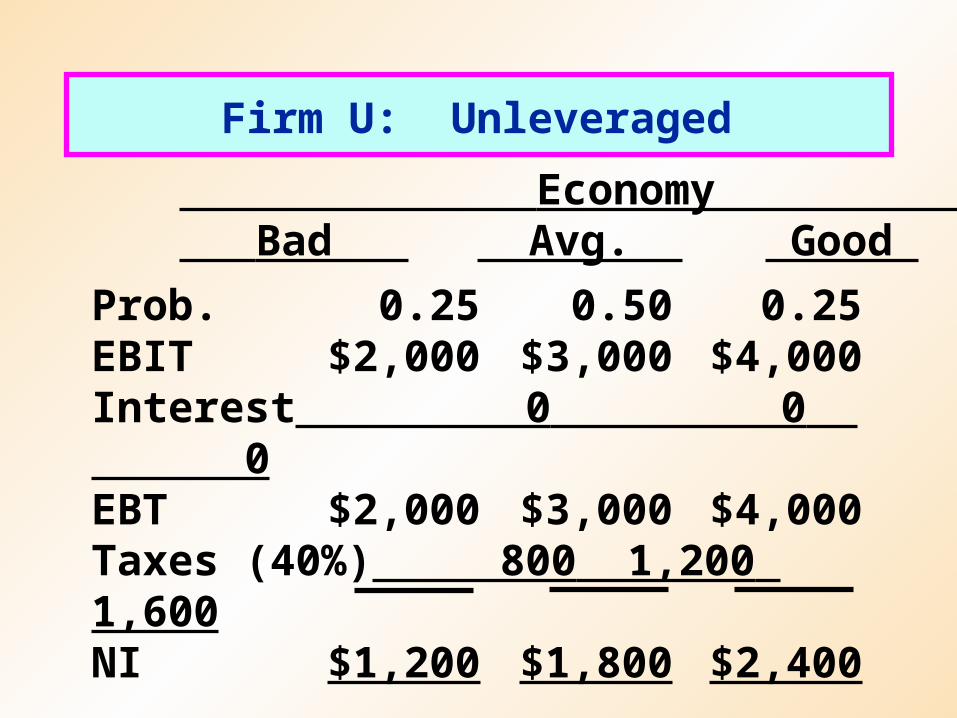

Firm U: Unleveraged

Prob. 0.25 0.50 0.25EBIT $2,000 $3,000 $4,000Interest 0 0 0EBT $2,000 $3,000 $4,000Taxes (40%) 800 1,200 1,600NI $1,200 $1,800 $2,400

Economy Bad Avg. Good

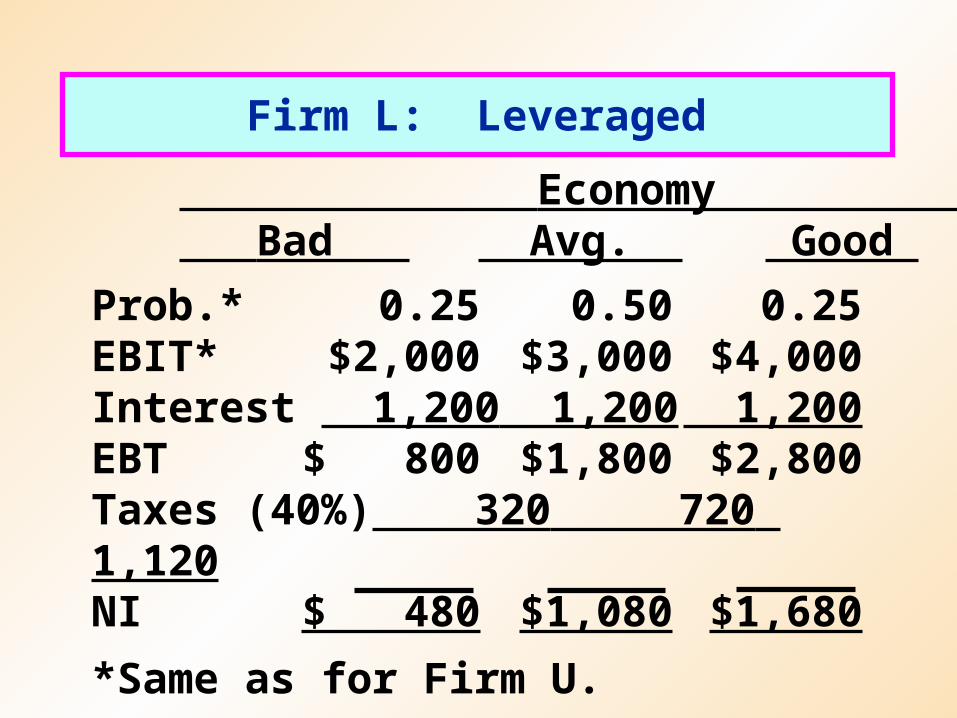

Firm L: Leveraged

Prob.* 0.25 0.50 0.25EBIT* $2,000 $3,000 $4,000Interest 1,200 1,200 1,200EBT $ 800 $1,800 $2,800Taxes (40%) 320 720 1,120NI $ 480 $1,080 $1,680

*Same as for Firm U.

Economy Bad Avg. Good

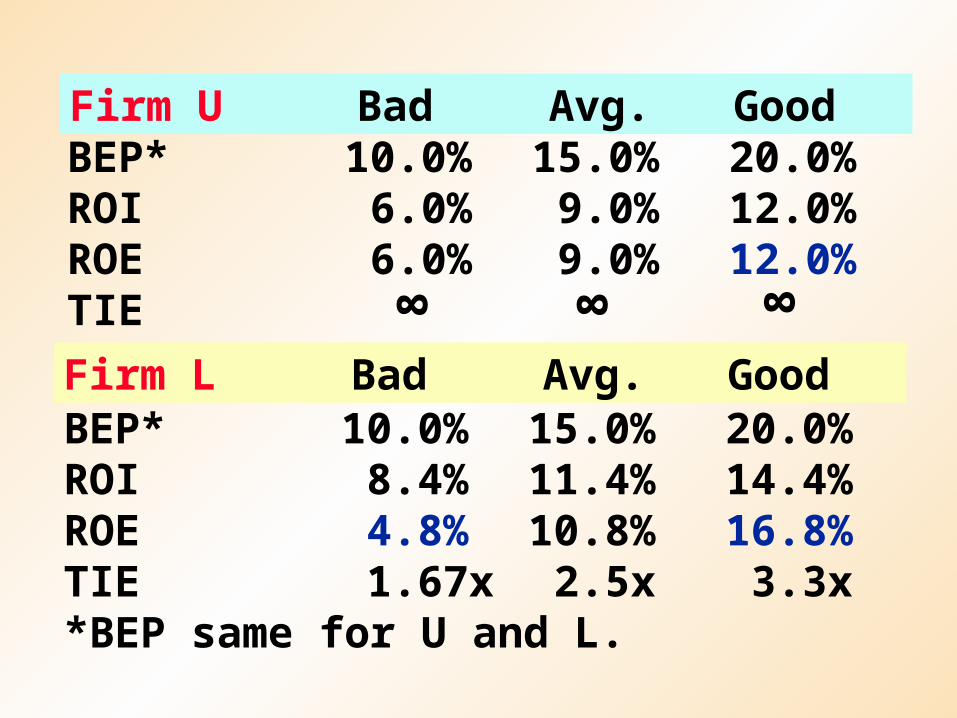

Firm U Bad Avg. GoodBEP* 10.0% 15.0% 20.0%ROI 6.0% 9.0% 12.0%ROE 6.0% 9.0% 12.0%TIE

Firm L Bad Avg. GoodBEP* 10.0% 15.0% 20.0%ROI 8.4% 11.4% 14.4%ROE 4.8% 10.8% 16.8%TIE 1.67x 2.5x 3.3x*BEP same for U and L.

8 8 8

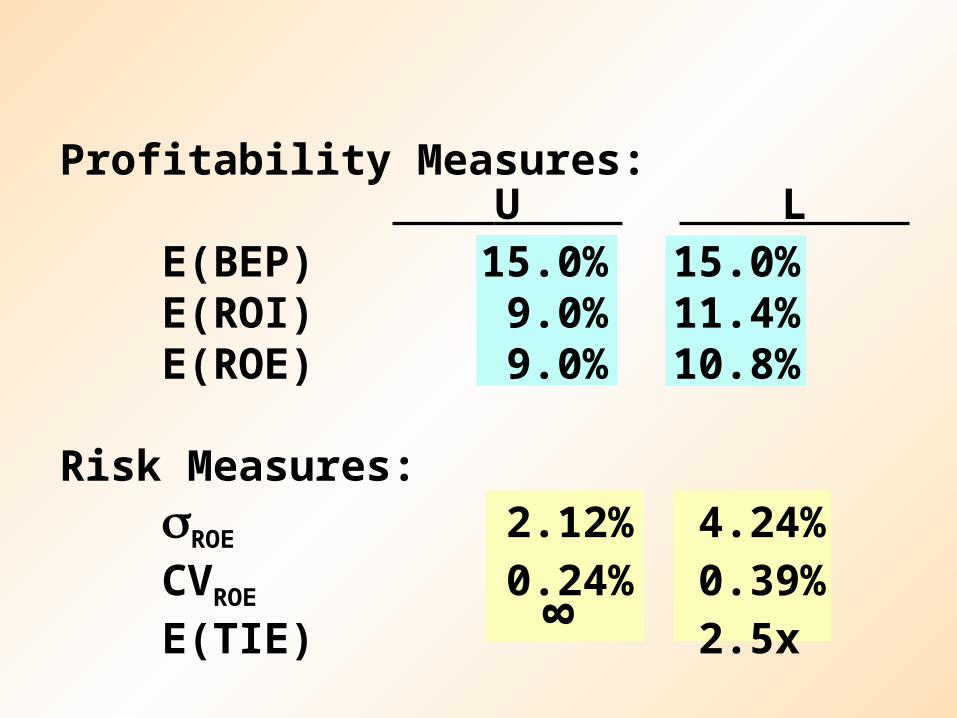

Profitability Measures:

E(BEP) 15.0% 15.0%E(ROI) 9.0% 11.4%E(ROE) 9.0% 10.8%

Risk Measures:ROE 2.12% 4.24%CVROE 0.24% 0.39%E(TIE) 2.5x

U L

8

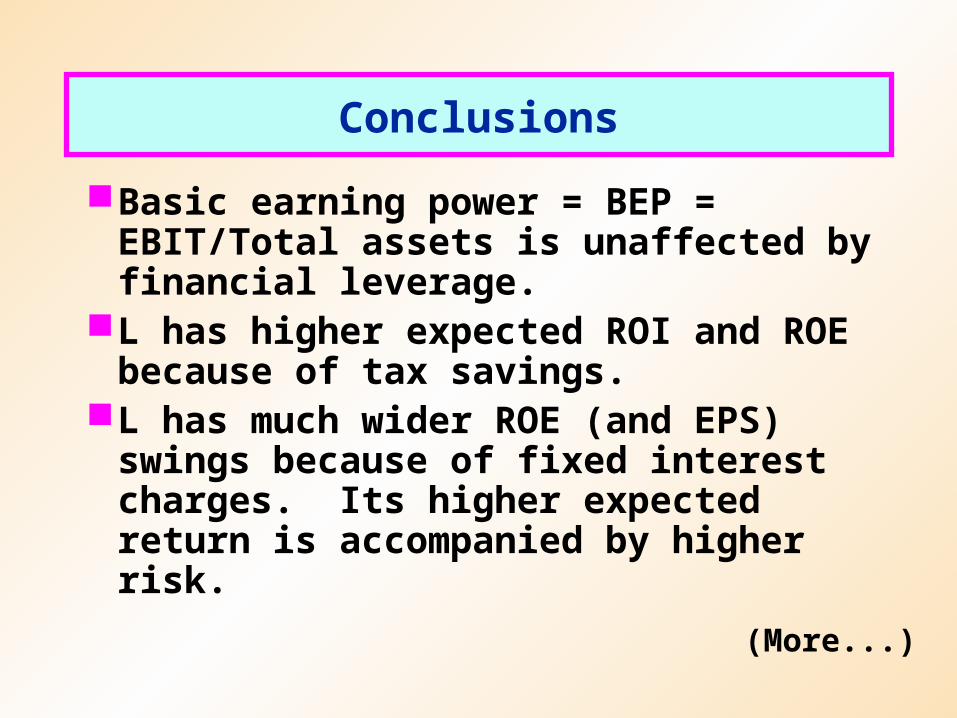

Conclusions

Basic earning power = BEP = EBIT/Total assets is unaffected by financial leverage.

L has higher expected ROI and ROE because of tax savings.

L has much wider ROE (and EPS) swings because of fixed interest charges. Its higher expected return is accompanied by higher risk.

(More...)

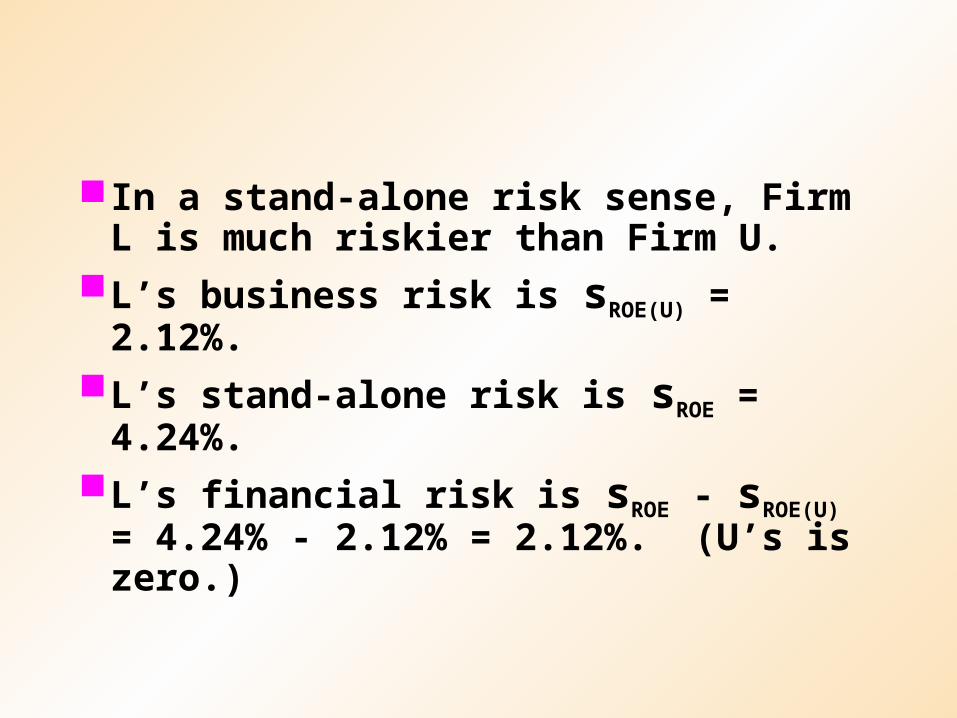

In a stand-alone risk sense, Firm L is much riskier than Firm U.

L’s business risk is sROE(U) = 2.12%.L’s stand-alone risk is sROE = 4.24%.L’s financial risk is sROE - sROE(U) = 4.24%

- 2.12% = 2.12%. (U’s is zero.)

For leverage to raise expected ROE, must have ROA > kd(1 - T). (ROA = ROEU = 9%.)

Why? If kd(1 - T) > ROA, then the interest expense will be higher than the operating income produced by debt-financed assets, so leverage will depress net income and ROE.

Capital Structure Theory

MM theoryTrade-off theorySignaling theoryDebt financing as a managerial

constraint

MM Theory

The effect of taxesThere is no tax on debt( bond).

The effect of bankruptcy costsThreat of bankruptcy from using

debt.

Trade-off between the use of debt (bond) and equity (preferred stock and common stock).

Trade-off between bankruptcy cost and the effect of tax

Trade-off theory

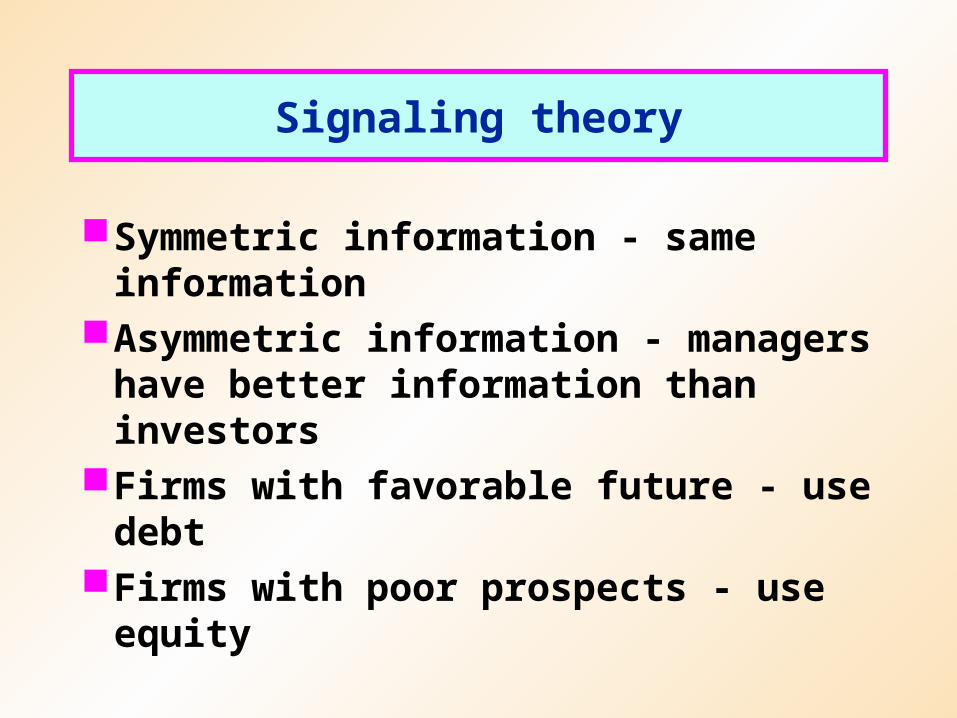

Symmetric information - same information

Asymmetric information - managers have better information than investors

Firms with favorable future - use debtFirms with poor prospects - use equity

Signaling theory

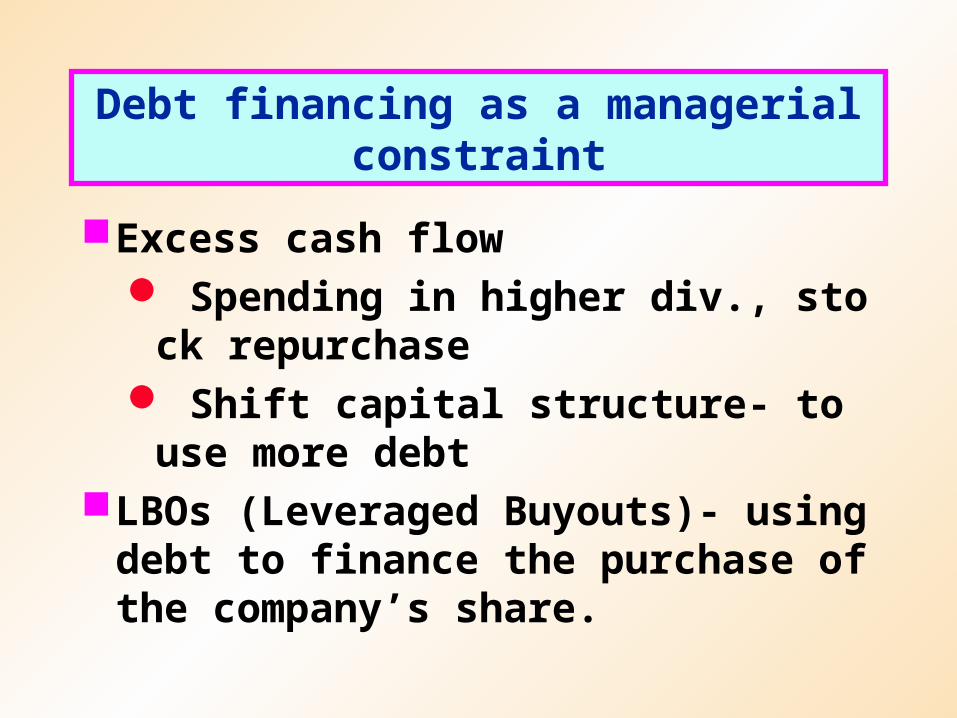

Excess cash flow Spending in higher div., stock repurch

ase Shift capital structure- to use more deb

tLBOs (Leveraged Buyouts)- using debt to

finance the purchase of the company’s share.

Debt financing as a managerial constraint