-

7/27/2019 Capital Market Line and the Efficient Frontier

1/6

Capital market theory

ASSUMPTIONS OF CAPM MODEL

The CAP-model is a ceteris paribus model. It is only valid

within a special set

of assumptions. They are:

Investors are risk averse individuals who maximize the expected

utility of

their end of period wealth. Implication: The model is a one

period model.

Investors have homogenous expectations (beliefs) about asset

returns.

Implication: all investors perceive identical opportunity sets.

This is,

everyone have the same information at the same time. Asset

returns are distributed by the normal distribution.

There exists a risk free asset and investors may borrow or lend

unlimited

amounts of this asset at a constant rate: the risk free rate

(kf).

There is a definite number of assets and their quantities are

fixed within the

one period world.

All assets are perfectly divisible and priced in a perfectly

competitive

marked. Implication: e.g. human capital is non-existing (it is

not divisible

and it cant be owned as an asset).

Asset markets are frictionless and information is costless and

simultaneously

available to all investors. Implication: the borrowing rate

equals the lending

rate.

There are no market imperfections such as taxes, regulations, or

restrictions

on short selling.

Capital Market Line and the Efficient Frontierthe efficient

frontier is trying to do is determine the best possible combination

of assets in a

portfolio that maximises the expected level of returns for a

given level of risk (as defined by

volatility / standard deviation). In effect the efficient

frontier gives a very formal relationship

between risk and returns. Any portfolio that is below the

efficient frontier line is deemed to be sub-

optimal this is quite intuitive as any point below will offer

the same return for greater risk or

same risk and less return. This leads to 2 formal

definitions:

1) Maximise expected return for a given level of volatility

-

7/27/2019 Capital Market Line and the Efficient Frontier

2/6

2) Minimise volatility for a given level of returns

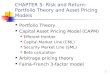

The set of optimal portfolios that we get from all the possible

combinations of portfolios in the risk-

return is known as the efficient frontier. You can see a very

clear illustration below where the

lighter pinkish area is the set of all possible portfolios and

the dark red line is the actual efficient

frontier.

Efficient Frontier

Investors can make a choice of how they allocate funds between

the risk free asset and the risky

portfolio. This can range from all assets in the risk free asset

to all (or more than all with leverage)

in the risky portfolio. When we plot this in a graphical fashion

we get a linear line with mean on

the Y axis and the volatility on the x axis. Note that the line

is linear as the risk free asset has no

volatility. The important point to take away here is that each

risky portfolio will have its own capital

allocation line. The capital allocation line that lies at a

tangent to the efficient frontier and is the

highest possible line is known as the Capital Market line

(because it is the market portfolio).

Given the mean-variance criterion all investors will hold their

portfolio in the same weights as the

market portfolio (and hence lie on the capital market line).

The CML is derived by drawing a tangent line from the intercept

point on the efficient

frontier to the point where the expected return equals the

risk-free rate of return.

The CML is considered to be superior to the efficient frontier

since it takes intoaccount the inclusion of a risk-free asset in

the portfolio. The capital asset pricing

model (CAPM) demonstrates that the market portfolio is

essentially the efficientfrontier. This is achieved visually

through the security market line (SML).

Limitations of Capital Asset Pricing Model in Capital

Markets

http://thinxlabs.com/tmain/wp-content/uploads/2012/06/Efrontier.png

-

7/27/2019 Capital Market Line and the Efficient Frontier

3/6

The Capital Asset Pricing Model (CAPM) states that it uses

various assumptions aboutmarkets and investment behavior to predict

the rate of return of an asset for a systematicrisk. However, there

are many flaws with the valuation model. Different investors

requiredifferent required rate of return,there are no transaction

costs or no taxes, holding periodvaries from one investor to

another and borrowing rate is not equal as lending rate andmany

others. CAPM fails to act as an efficient valuation model in

reality because the

model works on a generalized principle rather than breaking it

apart for different kind ofinvestments.

The beta coefficient used in CAPM is basically a variance of an

assets price to the

market. Investors usually use beta for stocks to generate the

required rate ofreturn.

The time value does matter when evaluating the required rate of

return. The

short-term and long-term rate would be affected so does the

borrowing andlending cost. CAPM should consider the short-term

rates as a risk-free ratesrather than using long-term rates because

the outlook for the country is negative

and perhaps they may get downgraded again. Capital Asset Pricing

Model- CAPM valuation model is not a suitable model to use in

stock exchange or for any other investments for many

reasons.

It is based on a number ofunrealistic assumptions.

It is difficult to test the validity.

Betas do not remain stable over time. (Beta is a measure of

a

securitys risk).

Implifications of cml for investors

. Capital asset pricing model (CAPM) based on a number of

assumptions.Given those assumptions, it provides a logical basis

for measuring risk andlinking risk and returnCapital asset pricing

model (CAPM) has the following implications,

Investors will always combine a risk free asset with a

marketportfolio of risky assets. They will invest in risky assets

in proportionto their market value.

Investors will be compensated only for that risk which they

cannotdiversify. This is the market related systematic risk. Beta

which is a

ratio of the covariance between the asset returns and the

marketreturns divided by the market variance is the most

appropriatemeasure of an assets risk.

Investors can expect returns from their investment according to

therisk. This implies a liner relationship between the assets

expectedreturn and its beta.

http://sovereignfundinggroup.blogspot.com/http://stephenpiercescam.net/?page_id=168http://sovereignfundinggroup.blogspot.com/http://stephenpiercescam.net/?page_id=168

-

7/27/2019 Capital Market Line and the Efficient Frontier

4/6

The concepts of risk and return as developed under capital asset

pricingmodel (CAPM) have intuitive appeal and they are quite simple

tounderstand. Financial managers use these concepts in a number

offinancial decisions making such as valuation of securities, cost

of capitalmeasurement, investment risk analysis excreta. However in

spite of its

intuitive appeal and simplicity capital asset pricing model

(CAPM) suffersfrom a number of practical problems.

Assumptions of CAPM

There are many investors. They behave competitively (price

takers).

All investors are looking ahead over the same (one

period)planning horizon.

All investors have equal access to all securities.

No taxes. No commissions.

Each investor cares only about ErC and C.

All investors have the same beliefs about the

investmentopportunities: rf , Er1,. . .,Ern, all i, and all

correlations

(homogeneous beliefs) for the n risky assets.

Investors can borrow and lend at the one riskfree rate.

Investors can short any asset, and hold any fraction of an

asset

Aim to maximize economic utilities.

Are rational and risk-averse.

Are broadly diversified across a range of investments.

Trade without transaction or taxation costs.

Deal with securities that are all highly divisible into small

parcels.

Assume all information is available at the same time to all

investors.

-

7/27/2019 Capital Market Line and the Efficient Frontier

5/6

What is Portfolio Revision ?

The art of changing the mix of securities in a portfolio is

called as portfolio revision.

The process of addition of more assets in an existing portfolio

or changing the ratio of fuinvested is called as portfolio

revision.

The sale and purchase of assets in an existing portfolio over a

certain periodof time to maximize returns and minimize risk is

called as Portfolio revision.

Need for Portfolio Revision

An individual at certain point of time might feel the need

toinvest more. The need for portfolio revision arises when

anindividual has some additional money to invest.

Change in investment goal also gives rise to revision in

portfolio.Depending on the cash flow, an individual can modify his

financialgoal, eventually giving rise to changes in the portfolio

i.e. portfoliorevision.

Financial market is subject to risks and uncertainty. An

individualmight sell off some of his assets owing to fluctuations

in thefinancial market.

Portfolio Revision Strategies

There are two types of Portfolio Revision Strategies.

1. Active Revision Strategy

Active Revision Strategy involves frequent changes in an

existingportfolio over a certain period of time for maximum returns

andminimum risks.

Active Revision Strategy helps a portfolio manager to sell and

purchasesecurities on a regular basis for portfolio revision.

2. Passive Revision Strategy

Passive Revision Strategy involves rare changes in portfolio

only undercertain predetermined rules. These predefined rules are

known asformula plans.

According to passive revision strategy a portfolio manager can

bringchanges in the portfolio as per the formula plans only.

What are Formula Plans ?

Formula Plans are certain predefined rules and regulations

decidingwhen and how much assets an individual can purchase or sell

forportfolio revision. Securities can be purchased and sold only

when thereare changes or fluctuations in the financial market.

Why Formula Plans ?

Formula plans help an investor to make the best possible use

offluctuations in the financial market. One can purchase shares

whenthe prices are less and sell off when market prices are

higher.

-

7/27/2019 Capital Market Line and the Efficient Frontier

6/6

With the help of Formula plans an investor can divide his funds

intoaggressive and defensive portfolio and easily transfer funds

fromone portfolio to other.

Aggressive Portfolio

Aggressive Portfolio consists of funds that appreciate quickly

and guarantee

maximum returns to the investor.

Defensive Portfolio

Defensive portfolio consists of securities that do not fluctuate

much andremain constant over a period of time.

Formula plans facilitate an investor to transfer funds from

aggressive todefensive portfolio and vice a versa.

Assumptions of Markowitz Theory

The Modern Portfolio Theory of Markowitz is based on the

following assump-tions:1. Investors are rational and behave in a

manner as to

maximise their. utility with a given level of income

ormoney.

2. Investors have free access to fair and correct information

on

the returns and risk.3. The markets are efficient and absorb the

information quickly

and perfectly.

4. Investors are risk averse and try to minimise the risk

and

maximise return.5. Investors base decisions on expected returns

and variance or

standard deviation of these returns from the mean.6. Investors

prefer higher returns to lower returns for a givenlevel of

risk.

A portfolio of assets under