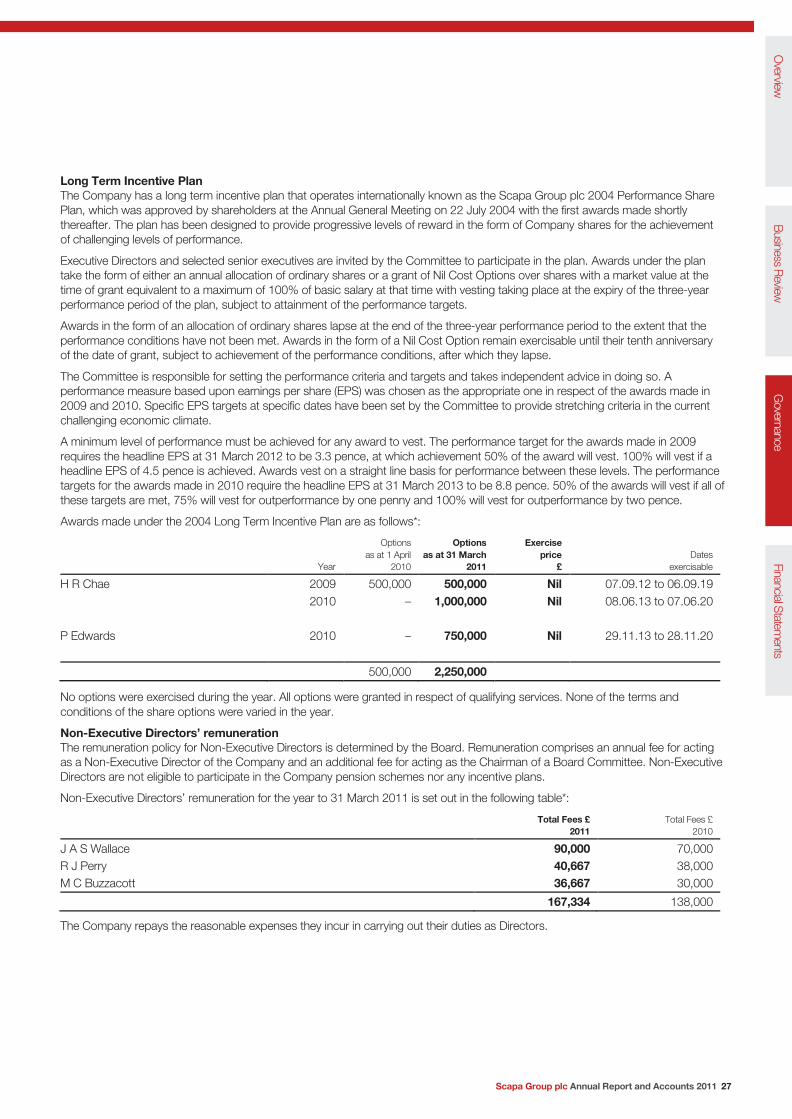

Embed Size (px)

Citation preview

Annual Report and Accounts 2011Annual Report and Accounts 2011

Building the foundation for sustainable and profitable growth

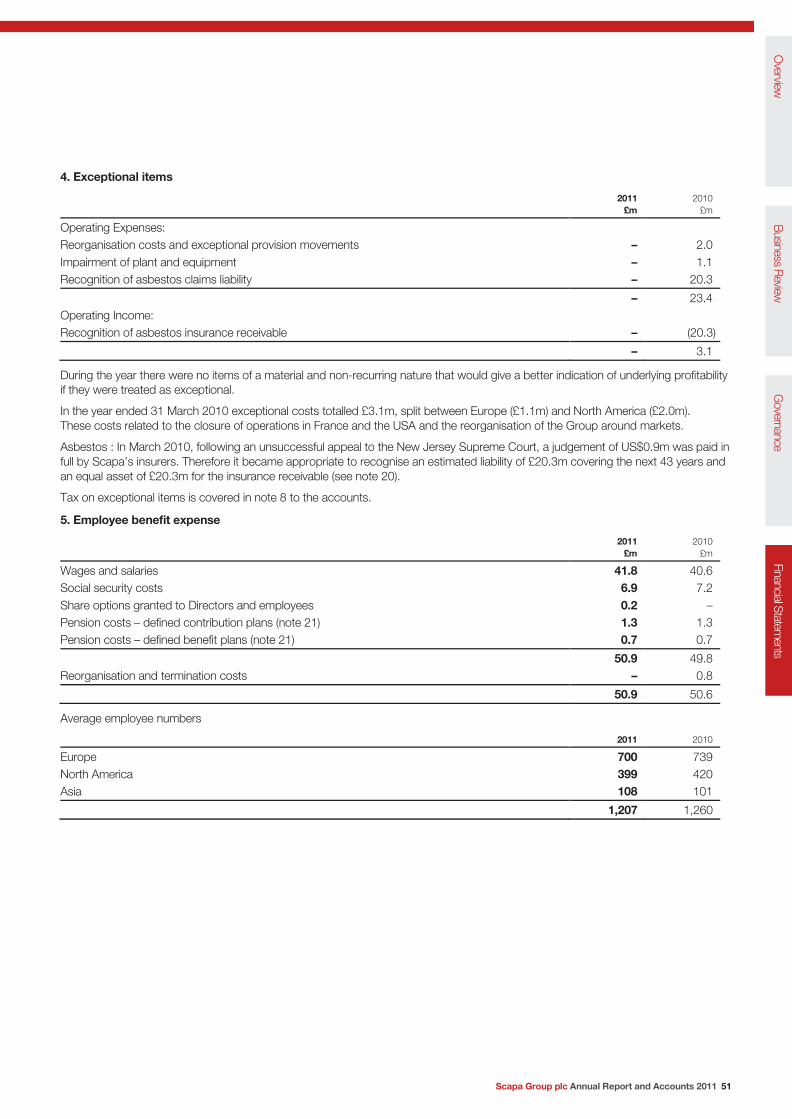

Scapa Group plc

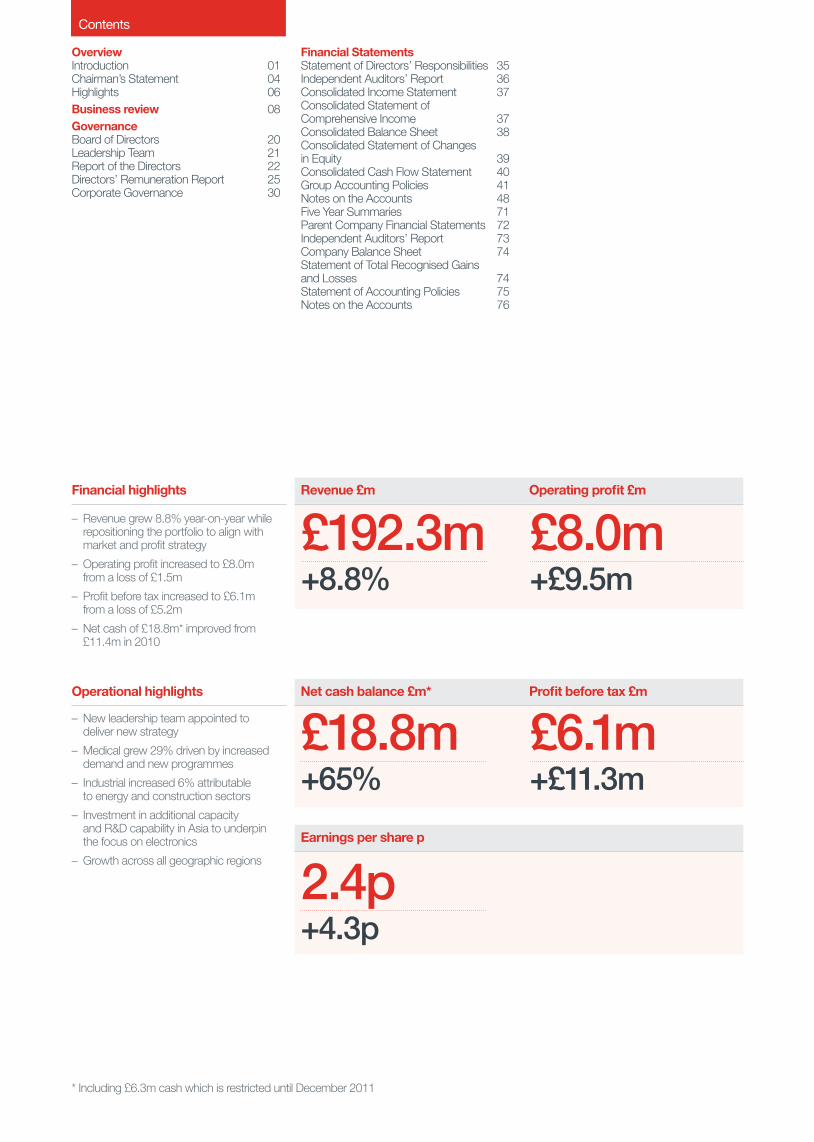

Contents

OverviewIntroduction 01Chairman’s Statement 04Highlights 06Business review 08Governance Board of Directors 20Leadership Team 21Report of the Directors 22Directors’ Remuneration Report 25Corporate Governance 30

Financial StatementsStatement of Directors’ Responsibilities 35Independent Auditors’ Report 36Consolidated Income Statement 37Consolidated Statement of Comprehensive Income 37Consolidated Balance Sheet 38Consolidated Statement of Changes in Equity 39 Consolidated Cash Flow Statement 40Group Accounting Policies 41Notes on the Accounts 48Five Year Summaries 71Parent Company Financial Statements 72Independent Auditors’ Report 73Company Balance Sheet 74Statement of Total Recognised Gains and Losses 74 Statement of Accounting Policies 75Notes on the Accounts 76

Revenue £m

Net cash balance £m*

Earnings per share p

Financial highlights Operating profit £m

Profit before tax £m

£192.3m+8.8%

£18.8m+65%

2.4p+4.3p

£8.0m+£9.5m

£6.1m+£11.3m

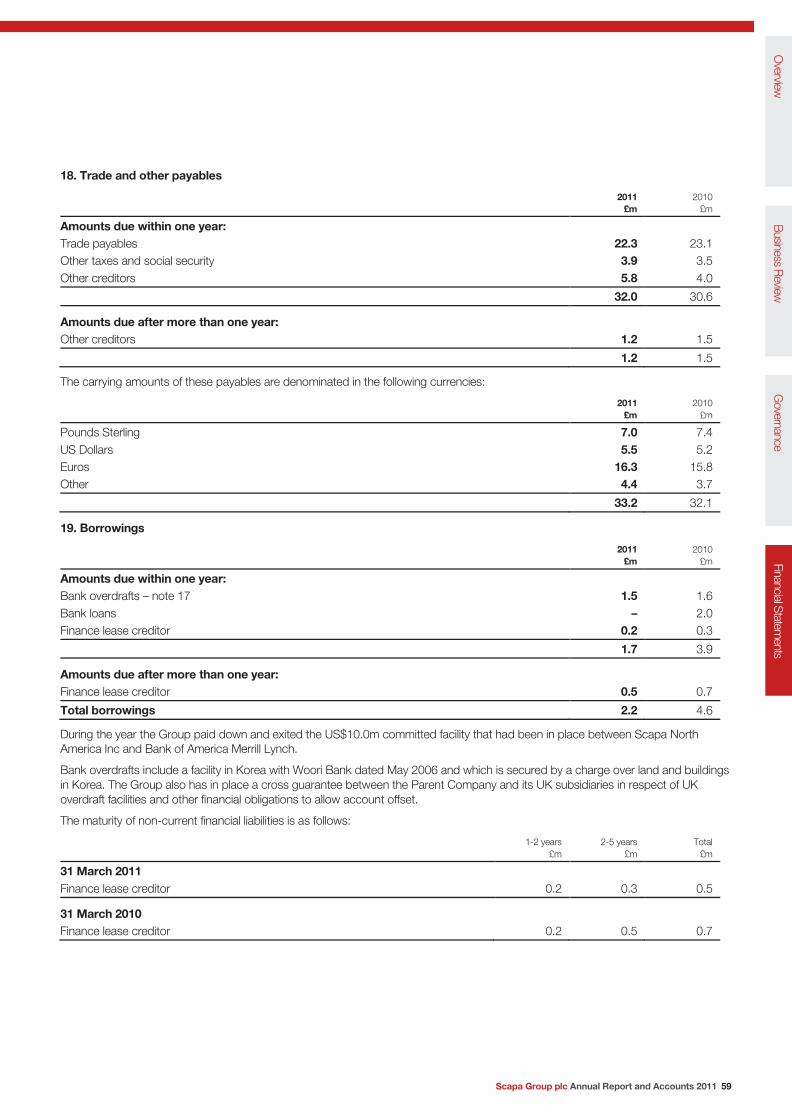

– Revenue grew 8.8% year-on-year while repositioning the portfolio to align with market and profit strategy

– Operating profit increased to £8.0m from a loss of £1.5m

– Profit before tax increased to £6.1m from a loss of £5.2m

– Net cash of £18.8m* improved from £11.4m in 2010

– New leadership team appointed to deliver new strategy

– Medical grew 29% driven by increased demand and new programmes

– Industrial increased 6% attributable to energy and construction sectors

– Investment in additional capacity and R&D capability in Asia to underpin the focus on electronics

– Growth across all geographic regions

Operational highlights

* Including £6.3m cash which is restricted until December 2011

Introduction

Who we are Scapa is a worldwide leading manufacturer of bonding solutions and adhesive components for applications in the medical, electronics, industrial and transportation markets.

What we do We help medical, industrial, electronics and transportation customers create better products by providing adhesive solutions and components. We design our offering around the requirements of global OEMs, distributors and consumers.

Our transition towards application-specific opportunities leveraging our global footprint and technologies is driving our portfolio towards value-added solutions from commodity products. Our aim is to accelerate the transition while continuing to deliver our financial expectations and value to shareholders.

Financial Statements

Governance

Business R

eviewO

verview

Scapa Group plc Annual Report and Accounts 2011 1

Introduction

IndustrialIndustrial is the largest segment of our business and represents a wide range of markets and applications. Reflecting the overall market, construction is the biggest portion of Industrial. We have a broad range of products that cover virtually every requirement needed in buildings. Our products are also used in many energy-related applications such as solar panels, oil and gas pipelines, and power and fibre cables. The increasing requirements for both traditional and alternative energy are driving the need and advancement of new bonding technology. The wide range

of applications for our products enables us to identify attractive emerging segments and position ourselves to benefit from increasing demand.

Scapa’s unrivalled product range and application knowledge, combined with our global footprint, ensure that customers in any market will consider us as their source for bonding materials and solutions. We sell our products through our own sales force as well as through our channel partners and distributors worldwide.

Scapa is a market leading developer and manufacturer of bonding materials and solutions. Our products are used extensively in a wide range of markets around the world. The applications range from plasters for minor cuts to optically clear adhesives in the latest smart phone. Our focus is to work with our customers to develop application-specific solutions for complex applications, which are continuously evolving.

More than tape

2 Scapa Group plc Annual Report and Accounts 2011

TransportationThe use of electronic components for the safety and comfort of passengers in cars, airplanes and trains is increasing. To help these electronic components communicate with each other, Scapa provides bonding solutions to wire harness manufacturers, meeting the highest OEM specifications, as well as logistic and support requirements of this industry, leveraging Scapa’s global footprint.

Global production platforms need global supply. With Scapa’s global manufacturing footprint we offer supply and local support to transportation customers. Function integration and focus on value-adding design systems help transportation customers to meet their customer and legislation demands.

ElectronicsThe requirements and needs of bonding solutions for the Electronics sector are increasingly demanding, driven by the innovation cycles of the market and global requirements of customers. As electronic products are becoming thinner and lighter, our products are replacing conventional fixings such as screws and connectors. Furthermore, our products are used as more than tape. We are working with our customers to incorporate other functionalities into

our products to address other needs such as heat dispersion and electro magnetic interference (EMI).

Scapa’s range of acrylic foam films and PU foam tapes ensures a lightweight and thin adhesive solution. Our range of thermal film pads, heat sinks and EMI tapes also incorporates functionality beyond tape.

MedicalIn receiving medical aids, whether it is a small plaster or life-saving surgery, the patient’s experience is initially defined by the sensation of the skin. As many medical applications and solutions are applied to the skin through adhesion, a bonding solution that is skin-friendly is a critical consideration in the medical products. We work with

global leaders in the medical industry to develop the next generation of skin-friendly products always with the patient’s comfort in mind.

Our products are used in a broad range of medical applications including medical devices, wound care and consumer products. The products include wound dressings, foams, films, drapes, ECG, pulse oximetry and MRI applications.

Financial Statements

Governance

Business R

eviewO

verview

Scapa Group plc Annual Report and Accounts 2011 3

Chairman’s Statement

James Wallace, Chairman

‘We are building the foundation for sustainable and profitable growth.’

4 Scapa Group plc Annual Report and Accounts 2011

In the fiscal year 2011, Scapa Group took significant steps towards sustainable and profitable growth, achieving results ahead of earlier expectations. Whilst we recognise that we are at the beginning of the journey, we are very pleased with our progress this year. We have reorganised the business around the four strategic markets of Medical, Industrial, Electronics and Transportation and strengthened the management team to deliver our expectations. We have focused our efforts on improving the quality of our business portfolio toward higher value, application-specific products rather than high volume commodities. We have improved our operational execution and efficiency to deliver and exceed our customers’ expectations. We have made investments, both in capital and people, to lay the foundations for our future and vision.

Financial highlightsRevenue increased 8.8% to £192.3m and operating profit significantly increased to £8.0m (2010: £1.5m loss) with no exceptional items charged during the year (2010: £3.1m). The operating margin improved progressively throughout the year.

The strong focus on working capital improved our net cash balance to £18.8m (2010: £11.4m) even after incurring a cash outflow of £6.1m relating to legacy issues.

No dividend is proposed for the year. The future recommendation of dividends will stay under review as the Group continues to make progress towards sustainable profitability and cash generation.

Business performanceMedical performance was strong, growing sales by 29%. The reorganisation around the market enabled us to properly allocate the resources and focus to maximise our position at our customers who are global leaders. Given our current market share at these customers and our long-standing relationships, we believe that our potential is significant.

Industrial grew 6% after concentrating on improved product mix. The focus on a higher quality portfolio resulted in a rationalisation of our product range and pricing strategy. As a consequence, we closed our Carlstadt facility in the USA and implemented a series of price adjustments to pass on the increases in input costs. The energy-related accounts, which we identified as strategic segments within Industrial, contributed to the increase in growth.

Electronics/Asia increased 3.2% as we re-profiled the portfolio from cash-consumptive trading business to locally manufactured products for the electronics market. During the year, we made significant investment to address the electronics market. We invested in new production capacity, opened a new R&D laboratory close to our strategic customers and built a team with significant experience in the sector. The focus this year has been to ensure that the investments are properly deployed and enable us to fully engage in this fast-growing and dynamic market.

Transportation grew 2.7% benefiting from improved second half performance. The recovery of the automotive industry during the year has continued into the current financial year.

Legacy issuesThe deficit on the Group defined benefit retirement plans now stands at £35.0m (2010: £38.6m), its lowest point in nine years. The Group deficit post tax is £25.6m (2010: £27.7m). The reduction in the deficit was the result of asset increases of £3.7m and a marginal increase in liabilities of £0.1m. The change in assumption in the UK to CPI from RPI to calculate deferred member pensions helped reduce the pension liabilities by around £3.2m.

We are now entering year two of our three-year contributions agreement with the UK pension trustees. During 2011/12 our UK and overseas contributions will be approximately £5.1m (2010: £4.4m) including £0.5m of PPF catch-up payments from

governance best practice. The exercise demonstrated that the current mix of talents and experience of the Board as a whole are appropriate to carry the Group into the next challenging phase of its development.

PeopleDuring the year we have assembled a team of experienced and capable executives to implement our strategy and the Board is confident that the new Leadership Team will deliver the short-term expectations as well as establish a platform of entrepreneurialism and accountability to drive sustainable and profitable growth. The quality of our people continues to be our core strength and I am delighted that we have further enhanced our capabilities in so many parts of the business and that cultural change is being embraced. On behalf of the Board, I would like to thank all our employees around the world for their commitment, hard work and continuing support over the last year.

OutlookOur focus for the coming year will continue to be profits and cash generation to further cement the foundation for the future. Much work will be done to generate greater return from our asset base through improved operational efficiencies and supply chain management. We will continue to prioritise profitable growth in strategic sectors over commodity volume business. We will also continue to invest in Medical and Electronics where we are confident of our strategy and competitive position. Within the Industrial market we are identifying and focusing on attractive segments with high potential that provide improved returns on our investment. The strategic management of our business portfolio will enable us to better respond to the many uncertainties in the current macro environment, particularly rising input costs.

As we build on the progress made last year, we are in a strong position to take advantage of market opportunities and we are confident that we will continue to improve and make further progress in the new financial year.

J A S Wallace Chairman

‘ Whilst we recognise that we are at the beginning of the journey, we are very pleased with our progress this year.’

2010/11 and £0.5m of performance-related top-ups, owing to the Group’s strong cash performance in this financial year. Going forward the Group is developing a road map to pursue all liability and administration cost-reduction initiatives that are in the interests of both pension scheme members and the Company.

During the previous financial year the Group undertook an actuarial and legal review of the outcome of all current and future potential asbestos-related claims against the Group. That review has been revalidated in respect of the current financial year. We remain confident that there will be no impact of these historic product liability claims on the Group’s profitability and there is adequate provision in the accounts for the continuing costs of defending against any claims.

BoardWe welcomed Paul Edwards as the new Finance Director during the year. Having been appointed since the last AGM, Paul will be proposed for election at the next AGM in July 2011. Richard Perry and Mike Buzzacott, the Non-Executive Directors who retire by rotation, will also be proposed for re-election at the AGM.

We believe that good governance adds value and reduces risk to the business and as such we continually develop and improve our governance structures. This year, as in previous years, the Board has carried out a rigorous exercise of self-assessment to ensure that its performance meets the needs of both the Company and corporate

Financial Statements

Governance

Business R

eviewO

verview

Scapa Group plc Annual Report and Accounts 2011 5

Highlights

Revenue by market

Medical £33.8m17.6%

Industrial £126.3m65.7%

Electronics £12.9m6.7%

Transportation £19.3m10%

Total £192.3m

IndustrialIndustrial represents a wide range of markets and applications, including construction, foam fabrication, military, printing & graphics and our energy markets of solar, cable and pipeline. Our range covers a larger portfolio of product types than virtually any other manufacturer in our markets.

Financial highlights 3-year trading historyMarkets

Revenue

£126.3m +6%% of Total Revenue

65%

TransportationTransportation is a world leader in the design and manufacture of speciality adhesive films and tapes for automotive production. We are engaged with the OEMs and their supply chain partners.

Revenue

£19.3m +2.7%% of Total Revenue

10%

‘Focused on attractive markets where we have a competitive position.’

121.8

119.2

126.3

2008/09 2009/10 2010/11

£m

£m

£m

£m

£m

£m

17.6

18.8

19.3

2008/09 2009/10 2010/11

MedicalMedical is a fully integrated, worldwide supplier of customised medical adhesive solutions, component materials and converted products for the medical device, wound care, hospital, transdermal and consumer industries.

Revenue

£33.8m +29% % of Total Revenue

18% 25.1

26.2

33.8

2008/09 2009/10 2010/11

£m

£m

£m

ElectronicsElectronics has strong partnerships across the world with top tier electronics OEMs, including consumer electronics, telecommunications devices and equipment manufacturers. Our products are application-specific and incorporate functionalities beyond tape and bonding.

Revenue

£12.9m +3.2%% of Total Revenue

7%£m

£m

£m

£m

9.5

12.5

12.9

2008/09 2009/10 2010/11

6 Scapa Group plc Annual Report and Accounts 2011

North America – Revenue of £72.7m (2010: £63.1m) growth of 15.2% as we continue to expand our service offering to our customers

– Operating profit significantly increased to £5.3m (2010: £1.3m) improving operating margin to 7.5%

Financial highlights 3-year trading historyRegional highlights

Revenue

£72.7m +15.2%Operating profit

£5.3m +308%

Region locations

Europe North America

Asia

France Canada ChinaGermany USA Hong KongItaly KoreaSwitzerland IndiaUK Malaysia

Revenue by region

Europe £106.7m55.5%

North America

£72.7m37.8%

Asia £12.9m6.7%

Operating profit by region

Europe £3.3m

North America

£5.3m

Asia £0.4m

Global presence

Europe – Revenue of £106.7m (2010: £101.1m) growth of 5.5% following market restocking and improving macro

– Operating profit significantly increased to £3.3m (2010: £0.3m) as we have improved profits and margins through strong control of costs

– Improved operational performance through centralisation and closure of Barcelona warehouse

Revenue

£106.7m +5.5% Operating profit

£3.3m +1000% 100.2

101.1

106.7

2008/09 2009/10 2010/11

£m

£m

£m

64.3

63.1

72.7

2008/09 2009/10 2010/11

£m

£m

£m

£m

£m

£m

9.5

12.5

12.9

2008/09 2009/10 2010/11

Asia – Investing £1.2m in new line and research and development laboratory to effectively service demanding high growth Electronics industry

– Stepping away from low margin commodity products to more application-specific product portfolio

– Appointed a strong team to deliver the strategy

Revenue

£12.9m +3.2%Operating profit

£0.4m -43%

Financial Statements

Governance

Business R

eviewO

verview

Scapa Group plc Annual Report and Accounts 2011 7

Business Review

Heejae Chae, Group Chief Executive

‘In the past year we have deliveredagainst the core objectives.’

8 Scapa Group plc Annual Report and Accounts 2011

Our strategic objectivesOur strategy remains to align ourselves with the requirements of our global customers and focus on high growth and high margin markets.

The key markets are:

– Medical

– Industrial

– Electronics

– Transportation

We will continue to work closely with our global partners in our target markets to develop bonding materials and solutions. Our extensive technical knowledge and global footprint will enable us to increase our market share with existing customers, many of whom are market leaders.

In the past year we have delivered against the following core objectives:

– Focused on increasing cash through efficient utilisation of working capital

– Increasing margins through targeted price increases, operational efficiency and control of costs

– Significantly increased the strength and depth of the operational management team across the Group

These core objectives remain key to the success of Scapa. Cash generation and improved margins through the transition from manufacturing commodity-based products to developing and producing more application-specific tapes, films and foams will continue to be the focus of Scapa building a sustainable foundation from which we can grow further.

ResultsA summary of the financial results is set out in the table below:

2011 £m

2010 £m

Revenue 192.3 176.7

Operating profit/(loss) 8.0 (1.5)

Net finance costs (1.9) (3.7)

Profit/(loss) on ordinary activities before tax 6.1 (5.2)

Basic earnings/(loss) per share(p) 2.4 (1.9)

Revenue for the year was £192.3m (2010: £176.7m) generating operating profit of £8.0m (2010: £1.5m operating loss) with trading improving throughout the financial year. There was no material movement in revenue for the effects of exchange rates year-on-year.

The first half of the financial year accounted for 51% of revenue. Conversely the split for operating profit was 45% for the first half and 55% for the second half, reflecting the move away from low margin volume business to more application-specific higher margin product.

While the objective has been to concentrate on margins and cash generation, the Group has seen strong year-on-year growth in revenue across all markets, specifically Medical with growth of 29%. The exception is Asia where the strategy has been to delist commodity-based lower margin products while investing in research and development capability and a new production line to increase capacity and develop and drive the Electronics business forward in the coming years.

During the financial year the Group has seen cost pressures in most raw materials but has protected and built margins not only through the change in mix but also through the implementation of price increases across all product sectors and markets.

‘Our focus remains on further improving our margin and cash. We will continue to drive the business towards higher value-added products in growth markets and geographies.’

Scapa Group plc Annual Report and Accounts 2011 9

Overview

Business R

eviewG

overnanceFinancial Statem

ents

Market OverviewOur Global Medical Business Unit serves the Medical Device, Advanced Wound Care (AWC), Consumer, Ostomy and Transdermal markets. Throughout the year these markets continued to outperform underlying GDP. The AWC market continues to grow through aging populations, higher prevalence of obesity and diabetes and products which are used in the treatment of complex and hard to heal wounds, including chronic wounds such as diabetic wounds, pressure ulcers, trauma wounds and large burns. Pulse oximetry, diabetic blood glucose monitoring (BGM) and over-the-counter transdermal delivery segments of the medical device market continue to provide strong levels of growth.

Strategy Scapa Medical’s ‘Skin-Friendly Solutions’ strategy aligns the needs of the patient/clinician to Scapa’s core technology and service capabilities and the benefits of our silicon and polyurethane capabilities are validated by our strategic alliances with Dow Corning. With customer support we have upgraded our operational capability and our Medical team is now recognised as offering Turnkey/full service to our customers through integrated design, material, converting and packaging solutions.

PerformanceMedical continued to perform strongly in the second half of the year with full year revenue of £33.8m (2010: £26.2m), a growth of 29%. The continued momentum increased Medical’s percentage of total revenue to 17.6% (2010: 14.8%). The growth continues in both advanced wound care and devices and is primarily from existing accounts where we are focusing and further developing our relationships. In Europe we are continuing to engage with our customers and expand our coverage and services in wound care and silicon-based products. North America continues to perform well and in addition to maintaining strong relationships with our leading customers we continue to develop mid-tier accounts where we are seeing larger orders placed.

Meeting the growing needs of the medical sectorThe market for medical pressure sensitive products has been growing exponentially, driven by innovations in the expanding global medical market. Scapa’s solutions are used in markets such as advanced wound care, medical devices, drug delivery, consumer healthcare, ostomy and surgical. Every solution is developed with end user comfort in mind.

Scapa aims to be a development partner to our global customers, helping to pioneer solutions for the future medical environment.

OverviewMedical is a fully integrated, worldwide supplier of customised medical adhesive solutions, component materials and converted products for the medical device, wound care, hospital, transdermal and consumer industries.

Highlights– Growth from existing customers expanding

our market share– Focus on value-added solutions beyond coating – Recognised as Silver Level Supplier for Johnson

& Johnson Consumer Division– Signed joint development agreement with Dow

Corning on silicon-based adhesive solutions

Revenue

£33.8m +29%Medical

Business Review

10 Scapa Group plc Annual Report and Accounts 2011

Market OverviewThe Global Industrial Business Unit encompasses a variety of different markets including Printing & Graphics, Construction, and Industrial Assembly. The overall growth in the year was driven primarily through accessing these markets through our extensive distribution network as well as reaching market-focused Original Equipment Manufacturers (OEMs) with specialty products. The positive strength of the economy reinforced the strong position in the highlighted markets, driving further product demand. Specifically in the energy sector, the solar, pipeline and cable industries each performed well given the investment in infrastructure in all three of the market sectors.

Strategy The distribution network within the Global Industrial Business is a key focus. In Scapa Industrial we are actively expanding our existing product portfolio to meet a variety of different market needs served by our channel partners, further aiding them in their promotion of Scapa products in our primary market segments. Additionally, working in conjunction with OEMs, Scapa Industrial is actively leveraging our diverse manufacturing capabilities to develop an array of customer-specified product solutions.

PerformanceIndustrial remains the largest proportion of Group revenue with 65.7% (2010: 67.5%) of total sales. It services a wide number of diversified industries and sub-industries as traditional assembly methods and applications requirements are changing, increasing the use of tapes and bonding solutions. Revenue increased 6% to £126.3m (2010: £119.2m) with strong demand and performances from emerging technologies within the energy, cable and pipeline sectors.

Leverage the potential of the new energy sectorThe drive to develop sustainable, renewable energy sources has led to increased demand for specialised tapes. Within the photovoltaic industry, adhesive technology is seen as the cleanest, easiest and most flexible solution for most application processes. Scapa has developed highly specialised adhesive foams, tapes and films for various applications within this market which include junction box mounting, edge sealing and cell positioning tapes, as well as cable management and adhesives used for internal bonding or frame mounting.

Our close association with key market players and testing bodies informs us of the latest market trends and keeps us at the forefront of this ever-evolving market.

OverviewIndustrial represents a wide range of markets and applications, including construction, foam fabrication, military, printing & graphics and our energy markets of solar, cable and pipeline.

Our range covers a larger portfolio of product types than virtually any other manufacturer in our markets.

Highlights– Driven by strong performance in North America– Construction performed well, aided by general

economic recovery and restocking– Maximise our margin through better product

portfolio management which will lower our cost and simplify our operational complexity

– Focus on energy sector yielding dividend, particularly solar

Revenue

£126.3m +6%Industrial

Scapa Group plc Annual Report and Accounts 2011 11

Overview

Business R

eviewG

overnanceFinancial Statem

ents

Market OverviewConsumer electronics, IT & computing, network & telecommunications are all part of the large global electronics market. This market is a highly dynamic and fast-changing environment, where innovation is the basis of competition. With relentless consumer demand and material innovation, new products are continuously being introduced. Scapa has strong partnerships across the world with top tier electronics OEMs and component suppliers in the consumer electronics, telecommunications devices and equipment manufacturer industries.

StrategyScapa works closely with leading global partners in its target markets, developing specialised adhesive tape bonding solutions for OEMs, distributors and consumers. Scapa has a true global footprint, with production sites in Asia, Europe and North America. Our worldwide service and supply chain capabilities place us in an excellent position to partner with global customers.

With R&D focused on electronics applications and product development in adjacent locations to global Tier 1 OEMs, Scapa has significant ability to provide technical guidance to these OEMs on future applications, with timely technical and product support.

PerformanceYear-on-year growth in Electronics/Asia has been flat as we continue to pursue the strategy of stepping away from producing and selling low margin commodity industrial products in favour of application-specific solutions for the electronics industry. Revenue was £12.9m (2010: £12.5m) contributing 6.7% of the total sales (2010: 7.1%). This year we completed the investment of £1.2m in a new research and development facility as well as increased production capacity as we position ourselves for growth in a market which is dynamic and fast-changing, where innovation and customer service will enable us to develop sustainable margins and growth.

At the heart of today’s electronicsSales of ultra slim mobile devices such as smartphones and tablet computers are skyrocketing. Space-saving adhesive solutions allow the electronics manufacturers to stand out with modern sleek design. Scapa has developed a special product portfolio for the ultra slim world which includes foams, films and tapes for thermal management, EMI shielding and various bonding applications.

Our strong partnerships across the world with top tier electronics OEMs allow us to develop state of the art solutions to maximise their freedom of design.

OverviewElectronics has strong partnerships across the world with top tier electronics OEMs, including consumer electronics, telecommunications devices and equipment manufacturers. Our products are application-specific and incorporate functionalities beyond tape and bonding.

Highlights– Invested in additional capacity and R&D Centre

in Korea to further enhance our production and product development capability

– Shifting to application-specific products manufactured locally which will slow the growth during the transition

– Developing solid product pipeline in display and smartphone applications

Revenue

£12.9m +3.2%Electronics

Business Review

12 Scapa Group plc Annual Report and Accounts 2011

Automotive technologyEvery year millions of vehicles are produced worldwide, with each new model requiring individual tape solutions. Scapa’s converting and die cutting capabilities offer customised solutions aimed at improving the manufacturing process whilst reducing waste material. Adhesive tapes offer many benefits during vehicle assembly, providing instant bonds that will maintain their strength throughout the vehicle’s lifetime.

Scapa’s aim is to develop adhesive solutions with transportation OEMs, utilising our converting capabilities and global footprint.

Market OverviewTransportation segments had to recover more than most industrial markets from the economic downturn of 2009. In 2010 segments grew again and, more significantly, established healthy platforms for 2011 and beyond. From aerospace and automotive to ship-building, the Scapa Transportation team delivers technical solutions for applications including electrical wire harness, noise and vibration, assembly and trim. Market product ranges utilise technically innovative materials and high performance adhesive systems to ensure full compliance to the stringent OEM specifications that drive this business and its key global customer requirements.

StrategyOur Global Transportation Business Unit continues to offer a wide range of solutions to meet the growing demands of the markets that it serves. We have established differential management of our OEM and Tier 1 customers in Europe, NA and Asia and co-ordination of customers globally where appropriate and beneficial. As a large percentage of our business is within the wire harness segment we have maintained a proactive approach to total product life cycle management, resulting in a change in the mix and profitability of our offering. We continue to leverage our global reach within the design systems segments with growth from our materials, coating and converted parts offerings.

PerformanceTransportation delivered revenue growth of 2.7% to £19.3m (2010: £18.8m) and remains 10% of the overall Group revenue. We continue to sell to OEMs and their supply chain partners and produce technically innovative products to satisfy the stringent specifications of a demanding market.

OverviewTransportation is a world leader in the design and manufacture of speciality adhesive films and tapes for automotive production. We are engaged with the OEMs and their supply chain partners.

Highlights– Demand has recovered throughout the year– Focus on margin and cost to serve– Expand beyond wire harness products– Increase market share from current global

customers

Revenue

£19.3m +2.7%Transportation

Scapa Group plc Annual Report and Accounts 2011 13

Overview

Business R

eviewG

overnanceFinancial Statem

ents

Business Review

EuropeThe trading performance in Europe improved with revenue growth to £106.7m compared to £101.1m in 2010, an increase of 5.5%. With only 10% of Group sales derived from the UK, the driver for growth was from the other main economies in Europe, specifically France and Germany as demand was driven by a mix of restocking and improving macro conditions in the Industrial and Transportation markets. Medical contributed strongly as we continue to improve and expand our relationships with our Medical customers in advanced wound care as they seek to improve their competitive position.

Operating profit was significantly ahead of the prior year at £3.3m (2010: £0.3m). As a consequence operating margins also improved to 3.1% (2010: 0.3%). In line with the rest of the business, Europe has incurred both energy-related and raw material cost pressure which was felt throughout the financial year particularly in rubber, cotton and specific resins. In the second half of the year we implemented a number of strategic price increases which contributed towards a much improved second half performance well ahead of the first, delivering £2.5m which was an operating margin of 4.6%, above the Group average of 4.2%.

The cost control initiatives and a plant closure have been completed and culminated in the closing of our warehouse in Barcelona. There has been a high level of attention to maintaining the benefits in the financial year and, coupled with improved efficiency and pricing, this has produced a solid improvement in the performance.

North AmericaRevenue in North America has increased year-on-year by 15.2% with strong performances across all segments. Medical contributed strongly with demand remaining steady throughout the year as we continue to win an increased market share from our current customers such as Johnson & Johnson and Covidien. Industrial also performed well with a strong contribution from emerging technologies and energy sectors. The growth is pleasing given the closure of our Carlstadt facility in New Jersey USA. Although loss-making in the prior financial year, the closure has removed capacity and impacted volume and therefore revenue in this financial year.

Operating profit for the region increased substantially to £5.3m (2010: £1.3m) accelerating margins to 7.3% for the year (2010: 2.1%).

‘Building a solid financialplatform for growth.’

Europe revenue £m

North America revenue £m

Asia revenue £m

£106.7m+5.5%

£72.7m+15.2%

£12.9m+3.2%

100.2

101.1

106.7

2008/09 2009/10 2010/11

£m

£m

£m

64.3

63.1

72.7

2008/09 2009/10 2010/11

£m

£m

£m

£m

£m

£m

9.5

12.5

12.9

2008/09 2009/10 2010/11

14 Scapa Group plc Annual Report and Accounts 2011

‘Strong growth driven by key markets where we have a competitive advantage.’

AsiaThis year has seen a change in strategy in our Asian operations. We are moving away from commodity low margin products and concentrating on more engineered application-specific technologies. To support this strategy in the year we completed the investment of £1.2m in a new production line and state of the art research and development facility in Anyang, South Korea, which is within a twenty mile radius of our strategic customers Samsung and LG. This ensures we can provide the close customer support and product development in line with the lifecycle of the development of our customers’ products.

As a consequence the second half of the year saw a revenue reduction of £0.9m on the first half which led to a modest increase in the level of turnover to £12.9m in 2011 compared to £12.5m in 2010.

This year has seen the Group invest in the Asia cost base to both improve our research and development capability and sales capacity throughout the region to help drive future growth in the Electronics market. As a result the operating profit was £0.4m compared to £0.7m in 2010, reducing the margin to 3.1% (2010: 5.6%).

CorporateHead office costs increased by £0.3m to £1.0m (2010: £0.7m) due to recruitment of a number of newly created senior positions within the Head Office. While cost control and value for money are fundamental building blocks in the Group’s make up, we are investing in the cost base to ensure the future development of the Group is supported and controlled. The introduction of a Group HR Director and global HR function alongside the investment in a Group business development team are two examples.

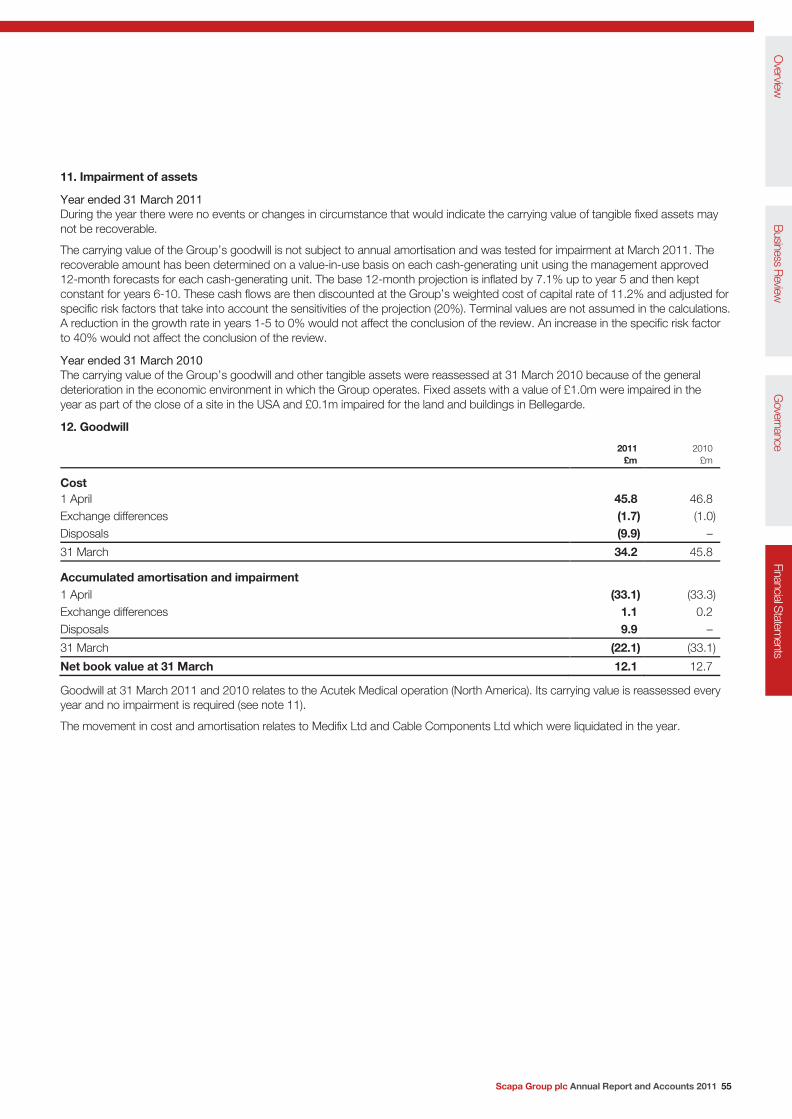

Exceptional itemsThere are no exceptional items (2010: £3.1m charge).

Finance costsNet finance costs decreased by £1.8m due to a decrease in the pension financing charge of £1.7m. The IAS 19 finance charge fell due to the increase in asset values in the previous year and reduction in the interest discount rate to 5.6% compared to 5.7% at March 2010. Although cash levels improved during the year, low interest rates have restricted returns.

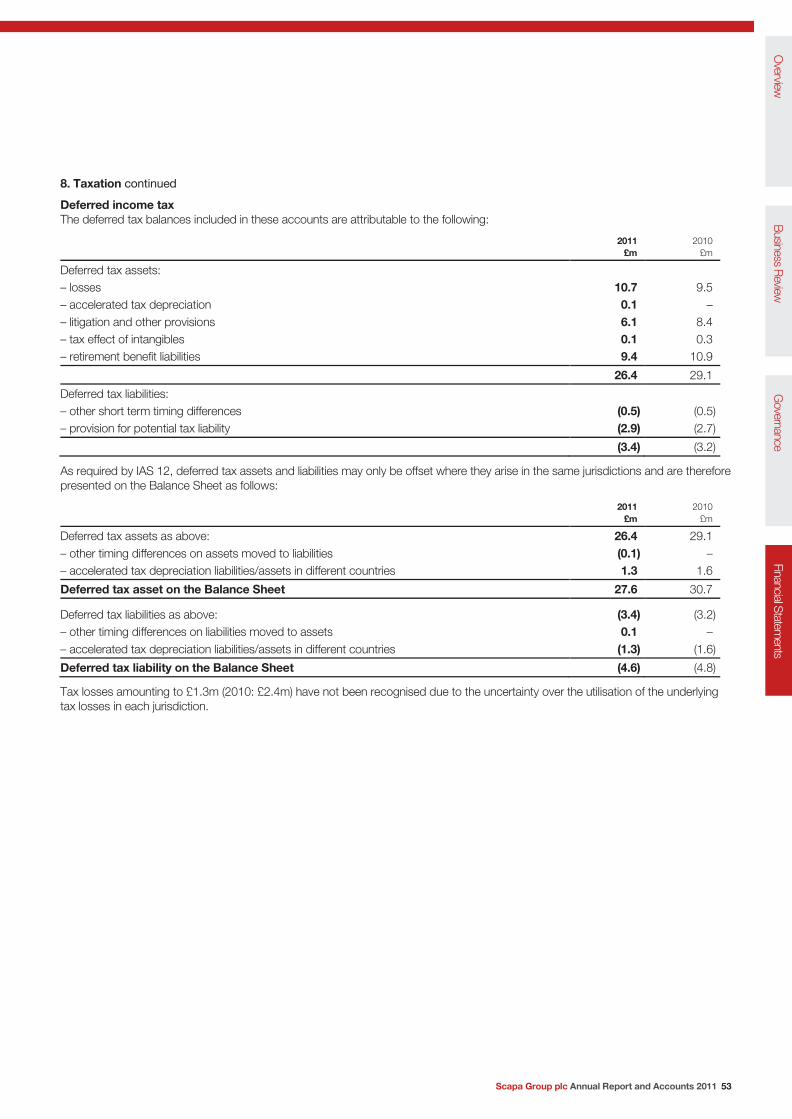

TaxationThe Group tax charge of £2.6m (2010: £2.4m credit) includes £2.1m charge (2010: £1.4m credit) on operating activities and £0.5m charge owing to a change in the UK tax rate (2010: £Nil).

The operating activities charge is made up of £1.1m of deferred tax and £1.0m of current tax.

The announcement during the year of the future UK corporation tax rate reduction from 28% to 26% had a deferred tax impact of £1.2m (2010: £Nil), of which £0.5m has been charged through the profit and loss account with the residue following the pensions movement through reserves.

The effective rate of tax for the Group, excluding the impact of the future rate change in the UK, is 34.4%. This is higher than the UK standard rate of 28% owing mainly to the Group operating in territories which have a higher statutory tax rate than the UK. Despite the high effective rate, the Group’s net cash tax payment in the year was minimal, due to the utilisation of tax losses and a tax repayment in the year of £0.3m.

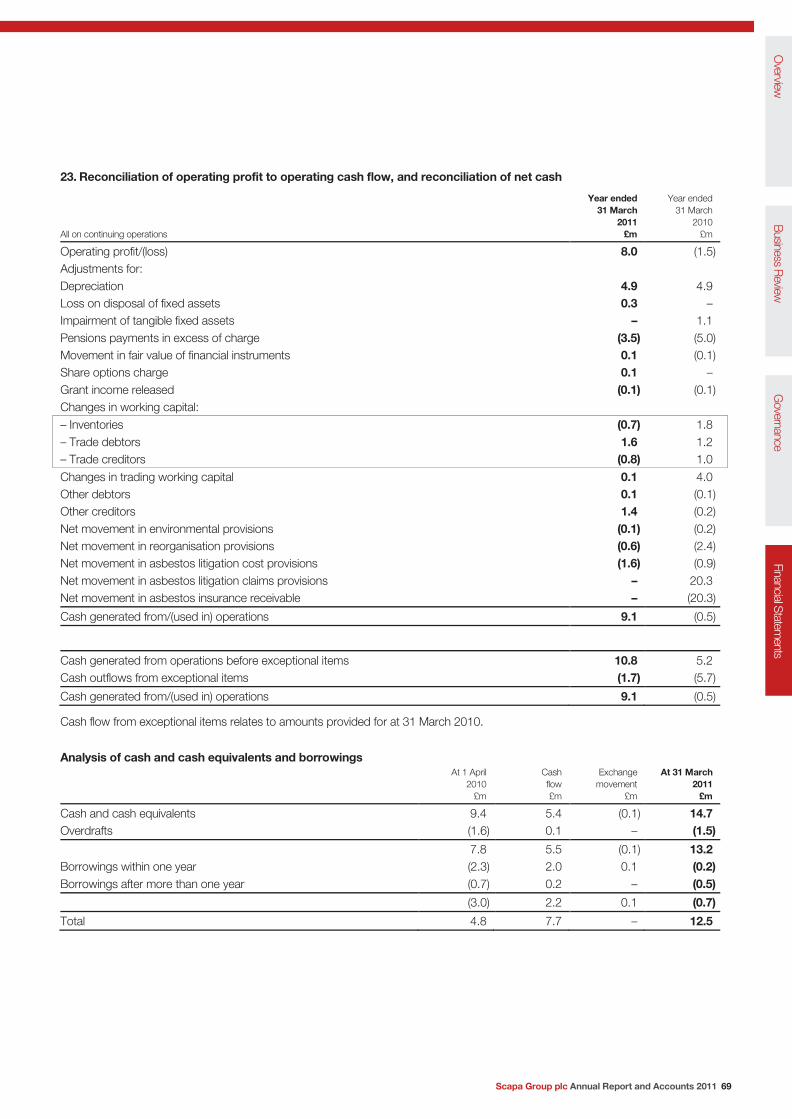

Cash flowThe Group ended the year with net cash of £18.8m (2010: £11.4m), an increase of £7.4m. This includes £6.3m (2010: £6.6m) of restricted cash; the restriction ends December 2011.

This is a creditable result given that it is after £4.4m (2010: £5.8m) of defined benefit pension payments, exeptional cash flows of £1.7m (2010: £5.7m) and £2.2m repayment of debt (2010: £0.2m). Effective management of working capital led to no outflow on cash despite the strong growth in sales (2010: £4.0m inflow), supported by a reduced capital expenditure programme of £1.6m (2010: £2.2m).

Scapa Group plc Annual Report and Accounts 2011 15

Overview

Business R

eviewG

overnanceFinancial Statem

ents

Business Review

‘Continued focus on margin improvementand a strong balance sheet.’

PensionsThe IAS 19 pension deficit has decreased by £3.6m to £35.0m (2010: £38.6m). The three UK defined benefit schemes, which are closed to new members and to future accrual, represent the largest portion of the deficit and that balance now stands at £28.8m (2010: £32.9m). The net movement in the UK deficits was the result of increases in asset values of £3.0m and a reduction in total liabilities of £1.1m, the latter being mainly the impact of the change in assumption from RPI to CPI.

Last year the Company concluded the negotiations with the Trustees of all three UK defined benefit pension schemes with respect to contributions for three years of which two years remain. Affordability and a strong sponsoring employer were the key shared objectives and as a result annual recurring contributions for the three years from 1 April 2010 were reduced by £0.5m per annum. During the three-year period this annual shortfall can be made good if cash flow targets are outperformed with any benefit being shared between the Company (67%) and the pension funds (33%), with the funds’ share limited to the cumulative shortfall. At the end of the three-year period contributions revert to their original level and any remaining cumulative deferred contributions are made good.

The net impact of the agreement has resulted in future UK cash pension costs of up to £3.5m per annum for the next two years. Total pension costs including UK and overseas schemes, plus PPF levy and administration expenses, will be £5.1m for 2011/12.

As noted above, the Group continues to recognise the deferred tax asset of £9.4m in respect of future pension deficit reduction payments which gain tax relief at the time of payment (as opposed to accrual). The pension deficit, net of deferred tax, is therefore £25.6m which includes a provision for future administration and PPF levy costs of around £6.5m.

Asbestos litigationDuring the previous financial year the Group undertook an actuarial and legal review of the outcome of all current and future potential claims against Scapa. That review has been revalidated in respect of the current financial year. In parallel, a similar review of the Group’s product liability insurance has been carried out.

As a result, the Group last year recognised a liability and an equal and opposite insurance asset of £20.3m. The position has been revalidated as referred to above, the only movements being foreign exchange and the unwind of the discount, giving a closing balance of £19.9m. In addition, provisions of £5.7m (2010: £7.5m) remain to pay the Group’s share of any future litigation costs.

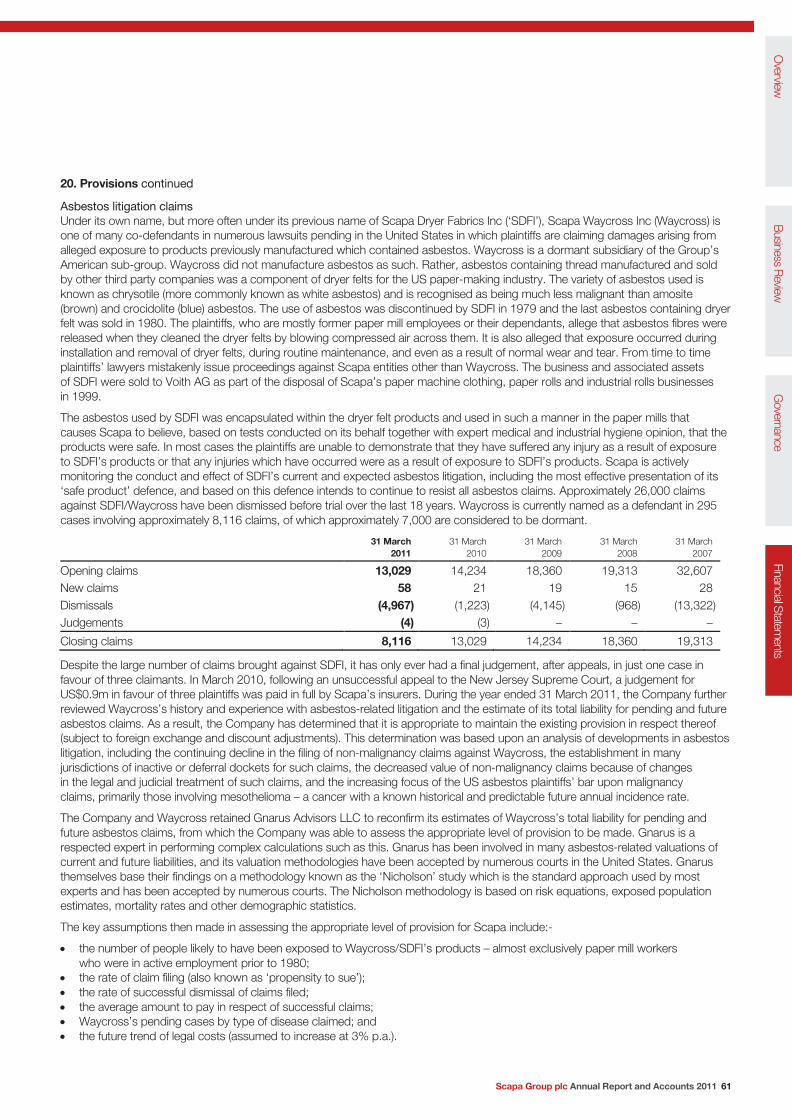

We continue to hold the view that Scapa’s products have not been the cause of any alleged personal injury and we therefore continue to adopt the same robust stance with respect to all of the remaining personal injury claims in the USA arising from businesses sold in 1999. During the year 4,967 more plaintiff claims were dismissed and the total now stands at 8,116, a reduction of almost 26,000 since the peak of around 34,000 in 2004.

Shareholder fundsShareholder funds have increased £3.3m to £68.6m (2010: £65.3m). Contribution from income was £2.9m (2010: £3.0m), being profit after tax of £3.5m with net pension gains of £0.9m (2010: £6.1m), offset by unfavourable currency impact on overseas asset values of £0.8m (2010: £0.3m) and tax charges of £0.7m (2010: £Nil). In addition, movements in equity relating to share issues and share options have added £0.4m.

Performance summaryThe Group’s performance this financial year is pleasing with growth across all business units and in all regions. Group profits have significantly improved on the prior year and the Balance Sheet continues to strengthen. Strong operational and financial management continues to improve working capital which has contributed to the balance of £18.8m cash on the Balance Sheet. All legacy issues are well understood and controlled and the Group is on a sound footing for sustainable performance.

16 Scapa Group plc Annual Report and Accounts 2011

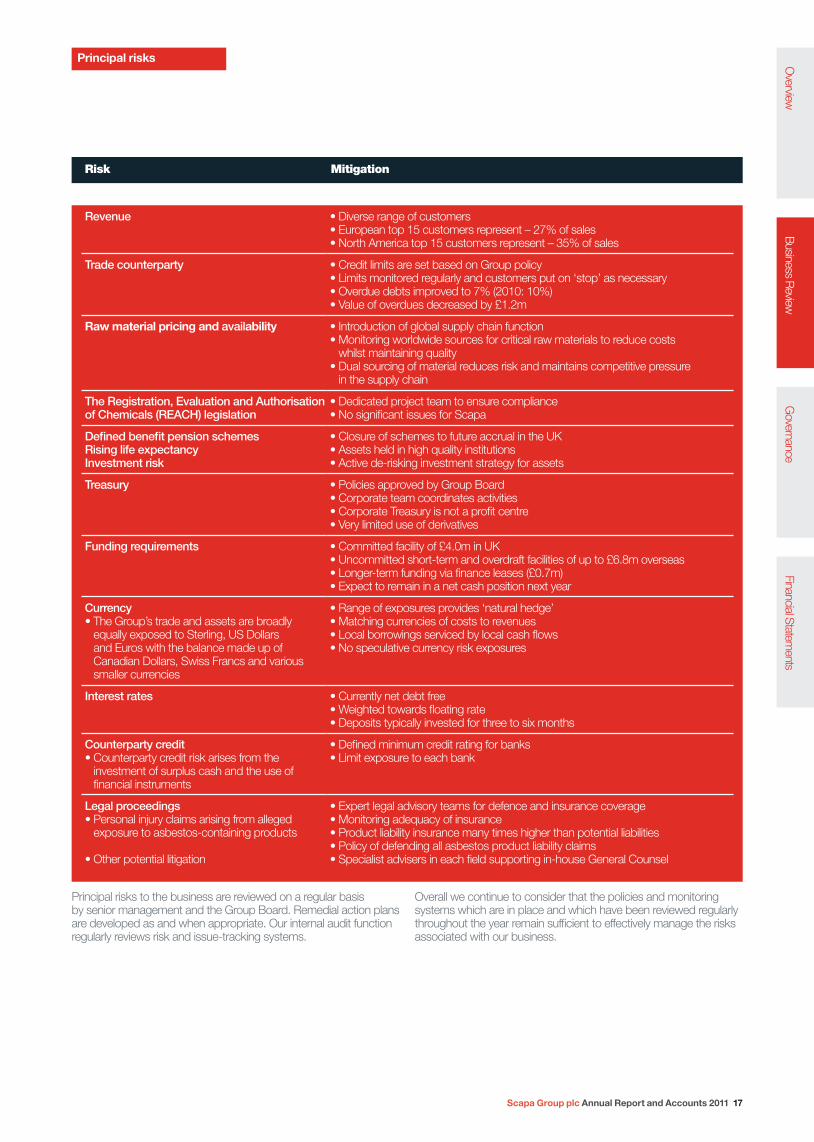

Principal risks

Risk Mitigation

Principal risks to the business are reviewed on a regular basis by senior management and the Group Board. Remedial action plans are developed as and when appropriate. Our internal audit function regularly reviews risk and issue-tracking systems.

Overall we continue to consider that the policies and monitoring systems which are in place and which have been reviewed regularly throughout the year remain sufficient to effectively manage the risks associated with our business.

Revenue • Diverse range of customers• European top 15 customers represent – 27% of sales• North America top 15 customers represent – 35% of sales

Trade counterparty • Credit limits are set based on Group policy• Limits monitored regularly and customers put on ‘stop’ as necessary • Overdue debts improved to 7% (2010: 10%)• Value of overdues decreased by £1.2m

Raw material pricing and availability • Introduction of global supply chain function• Monitoring worldwide sources for critical raw materials to reduce costs

whilst maintaining quality• Dual sourcing of material reduces risk and maintains competitive pressure

in the supply chain

The Registration, Evaluation and Authorisation of Chemicals (REACH) legislation

• Dedicated project team to ensure compliance• No significant issues for Scapa

Defined benefit pension schemes Rising life expectancyInvestment risk

• Closure of schemes to future accrual in the UK• Assets held in high quality institutions• Active de-risking investment strategy for assets

Treasury • Policies approved by Group Board• Corporate team coordinates activities• Corporate Treasury is not a profit centre• Very limited use of derivatives

Funding requirements • Committed facility of £4.0m in UK• Uncommitted short-term and overdraft facilities of up to £6.8m overseas• Longer-term funding via finance leases (£0.7m)• Expect to remain in a net cash position next year

Currency • The Group’s trade and assets are broadly

equally exposed to Sterling, US Dollars and Euros with the balance made up of Canadian Dollars, Swiss Francs and various smaller currencies

• Range of exposures provides ‘natural hedge’• Matching currencies of costs to revenues• Local borrowings serviced by local cash flows• No speculative currency risk exposures

Interest rates • Currently net debt free• Weighted towards floating rate• Deposits typically invested for three to six months

Counterparty credit• Counterparty credit risk arises from the

investment of surplus cash and the use of financial instruments

• Defined minimum credit rating for banks• Limit exposure to each bank

Legal proceedings • Personal injury claims arising from alleged

exposure to asbestos-containing products

• Other potential litigation

• Expert legal advisory teams for defence and insurance coverage• Monitoring adequacy of insurance• Product liability insurance many times higher than potential liabilities• Policy of defending all asbestos product liability claims• Specialist advisers in each field supporting in-house General Counsel

Overview

Business R

eviewG

overnanceFinancial Statem

ents

Scapa Group plc Annual Report and Accounts 2011 17

Business Review

‘We continue to implement Leanmanufacturing techniques.’

Protecting the environmentScapa Group plc continues to recognise the importance of managing the consumption of the world’s natural resources as well as providing a safe and healthy working environment for its employees, and also the neighbourhoods in which we operate. Clearly, however, the successful growth of our business will lead to the consumption of more resources, on an absolute basis. We therefore attempt to significantly reduce, or where possible eliminate, the amount of resource consumed for each unit of production. The Group routinely undertakes audits of our Environmental, Health and Safety programmes utilising both internal and external third parties where appropriate.

Air emissionsScapa actively seeks to minimise the discharge of VOCs, particulates and odour into the atmosphere. Solvent-based adhesive coating processes are used in many locations throughout Scapa. Evaporated solvents are captured and effectively destroyed using modern thermal oxidizers or condensed using solvent recovery systems. All sites using thermal oxidizers undergo strict third-party testing to ensure that all legislative requirements are met or exceeded.

Solvent consumptionWhilst Scapa utilises solvent-based adhesives in all regions, much work continues to be carried out to reduce the quantity of process solvent for environmental and cost reasons. Work continues by our Research and Development teams to develop adhesive solutions and processes to completely eliminate the use of solvents for specific applications. Within our Medical and Industrial businesses, we offer a wide range of solventless adhesive tape solutions and continue to investigate new and innovative adhesive solutions. We continue to identify opportunities where focused capital investment can help reduce solvent consumption.

Oil consumptionThere continues to be no significant direct use of oil within Scapa operations and where it is used it is predominantly for equipment lubrication. Lubrication oils are tested for maximum duration of use and disposed of through licensed disposal agents meeting all local and regional environmental standards.

Gas and electricity consumptionGas and electricity remain significant inputs to Scapa processes in all regions. Constant reduction of energy usage is a key component of the Scapa environmental programme. We continue to work to implement energy management systems at our various global sites to help reduce overall consumption.

Manufacturing wasteThe Group continues to drive its implementation of Lean manufacturing techniques across its sites. As this initiative extends and focuses upon the elimination of non-value-added activities, it will lead to reductions in manufacturing waste and our overall environmental footprint. Examples of improvement activities are:

– We continue to target the overall reduction in manufacturing waste sent to landfill at all sites

– In Valence (France) we have further optimised our coating and slitting processes to reduce ‘edge waste’ which we can then extend to other processes

– Across our North American sites the SAP System has been extended with real-time shop-floor data capture systems to provide timely data to drive significant reductions in waste

– In Windsor (USA) we have approved capital investment to upgrade the control systems on the adhesive coating lines

– For the twelfth consecutive year the Inglewood, CA site received a WRAP Award (Waste Reduction Awards Program) from the California Integrated Waste Management Board

18 Scapa Group plc Annual Report and Accounts 2011

REACHDuring 2010 a number of additional substances were added to the list of substances of very high concern (SVHCs) though none of these affect Scapa’s product portfolio. Some of the existing SVHCs are in Scapa’s product portfolio and two of these will be placed into annex XIV which means they will be banned from commercialisation unless authorisation is granted. In effect these two substances will be banned from 2015. Accordingly Scapa has notified existing customers regarding SVHCs and we have a programme of work to remove these materials from finished products which has already resulted in some reformulations. Accordingly we see no significant risk arising from current REACH legislation.

Improving safety cultureScapa considers its safety performance as a top priority. Our ultimate aim is, and must only be, to achieve a result where none of our employees comes to any harm whilst engaged in Scapa Group business. The Group realises that this is an extremely challenging goal that can only be achieved through constant vigilance and continuous improvement in the working environment and business processes, but above all through the attitude and behaviour of every single member of staff.

Scapa and its employees agree that the delivery of a safe working environment and safe systems of work is a shared responsibility. The Board believes that it is the ‘tone at the top’ that is a key driver of the Group’s safety culture. The Board is committed to reinforcing and improving health and safety activities within all sites to ensure the constant safety and wellbeing of our employees. Standards of performance are set and monitored by the Board and safety KPIs form a key part of the Group’s review process. The Leadership Team is responsible for providing guidance, focusing on best practices and overseeing auditing of our manufacturing sites and processes.

‘We continually strive to improvesafety across our processes.’

Health and Safety – Review of performanceThe Board safety targets for the year 2010/11 were increased to a minimum 20% annual improvement in all KPIs. This priority is strongly reinforced by the Board who remain directly involved in monitoring performance on a regular basis. Key focus areas include:

– Machine guarding

– Risk Assessment Review

– Material movement, handling and storage

– Proper and improved use of Personal Protective Equipment

– Employee training

– Auditing of Health and Safety policies and practices

In addition our key safety opportunities process identified more than 3,000 opportunities for potential improvement in our facilities during the year. All sites within the Group report Key Performance results monthly and are audited at least twice a year against a standard audit template to ensure a consistently high level of compliance and continuous improvement. Every serious incident or accident continues to be reviewed by the Group Operations Director, local site leadership teams and, in the most serious cases, the Board. During the year a new Group Health & Safety Leadership position was created to lead further improvements.

2011/12 Health and Safety goalsThe ultimate goal for all Scapa sites will always be zero accidents and zero lost days. Anything less would send the message that some level of injury is acceptable. We aim to make continued annual improvements to our performance and for the next financial year the Board has again targeted a 20% annual improvement in all safety KPIs. Constant vigilance and reinforcement of key messages is required from all our staff.

Underpinning this goal of improving the safety culture, bonus payments are made to Senior Managers and Directors which are, in part, dependent upon achievement of key health and safety goals.

Scapa Group plc Annual Report and Accounts 2011 19

Overview

Business R

eviewG

overnanceFinancial Statem

ents

Governance

R J PerryNon-Executive Director

Richard Perry was appointed to the Scapa Board in June 2005 and is Chairman of the Audit Committee. Richard is currently Group Finance Director of Fenner plc to which position he was appointed in 1994. He was formerly a senior audit partner with Price Waterhouse.

M C BuzzacottNon-Executive Director

Mike Buzzacott joined the Board in March 2008 and is currently Chairman of the Remuneration Committee. Mike has extensive experience of the global chemicals industry where he spent 14 years in operational roles in BP Chemicals, before retiring as Group Vice President Petrochemicals in 2004. Mike is currently Non-Executive Director at Genus PLC and Croda International Plc.

M R StirzakerCompany Secretary and General Counsel

Mark Stirzaker is a UK qualified solicitor and joined Scapa in January 2006 with responsibility for its company secretarial and legal affairs worldwide. He has extensive experience of commercial legal matters in the manufacturing industry, having previously been Head of Legal at British Vita PLC for over 20 years.

H R ChaeGroup Chief Executive

Heejae Chae joined the Board as Executive Director in September 2009 and subsequently became Group Chief Executive in November 2009. Prior to joining Scapa, Heejae was Group Chief Executive of Volex Group plc. He was previously the Group General Manager, Radio Frequency Worldwide, for Amphenol Corporation. He spent the early part of his career in finance at The Blackstone Group and Credit Suisse First Boston before moving into industry.

P EdwardsGroup Finance Director

Paul Edwards joined the Board in September 2010 as Group Finance Director. Prior to joining Scapa he was Group Finance Director of NCC Group plc. Paul is a Chartered Management Accountant and MBA and spent the earlier part of his career in manufacturing, logistics and services sectors.

J A S WallaceChairman

James Wallace joined the Board in August 2007 and became Chairman in October 2007. He is currently also Chairman of the Nominations Committee. An accountant by qualification, he spent the majority of his very successful executive career at Pifco Holdings PLC until 2001. James has held various Non-Executive Director positions and was Chairman of Bodycote plc from January 2002 until April 2008. Currently James is a Non-Executive Director of Manchester Airport Group plc and Cryptologic Ltd.

Board of Directors

20 Scapa Group plc Annual Report and Accounts 2011

G KimManaging Director – Asia

Gene Kim joined Scapa as Managing Director – Asia in February 2010. Prior to Scapa, Gene was Director of Strategic Projects at Cisco Systems. His prior experience also includes Samsung Electronics, Mercer Management Consulting and Arthur D Little.

T SheedyGroup HR Director

Tracy Sheedy joined Scapa in September 2010 as Group HR Director. Before joining the Company, Tracy was Head of Organisation and Capability Development with BAE Systems. Prior to this role Tracy held senior HR roles with ConvaTec, Georgia Pacific and Monsanto.

I R MarchantGroup Operations Director

Ian Marchant joined the Company in February 2010 as Group Operations Director. Prior to joining Scapa, Ian held a number of senior management positions with two international manufacturing businesses, Avon Rubber plc and General Electric Inc.

R SeufertGroup Commercial Director

Ralf Seufert joined Scapa as Group Commercial Director in October 2010. Before joining Scapa he was VP Sales & Marketing and member of the Board at Quadrant Plastic Composites AG in Switzerland. He has previously worked for GE Advanced Materials in senior management positions for global application development and sales.

Leadership Team

L-R: Gene Kim, Tracy Sheedy, Heejae Chae, Ian Marchant, Mark Stirzaker, Paul Edwards, Ralf Seufert

Scapa Group plc Annual Report and Accounts 2011 21

Overview

Business R

eviewG

overnanceFinancial Statem

ents

Report of the Directors

22 Scapa Group plc Annual Report and Accounts 2011

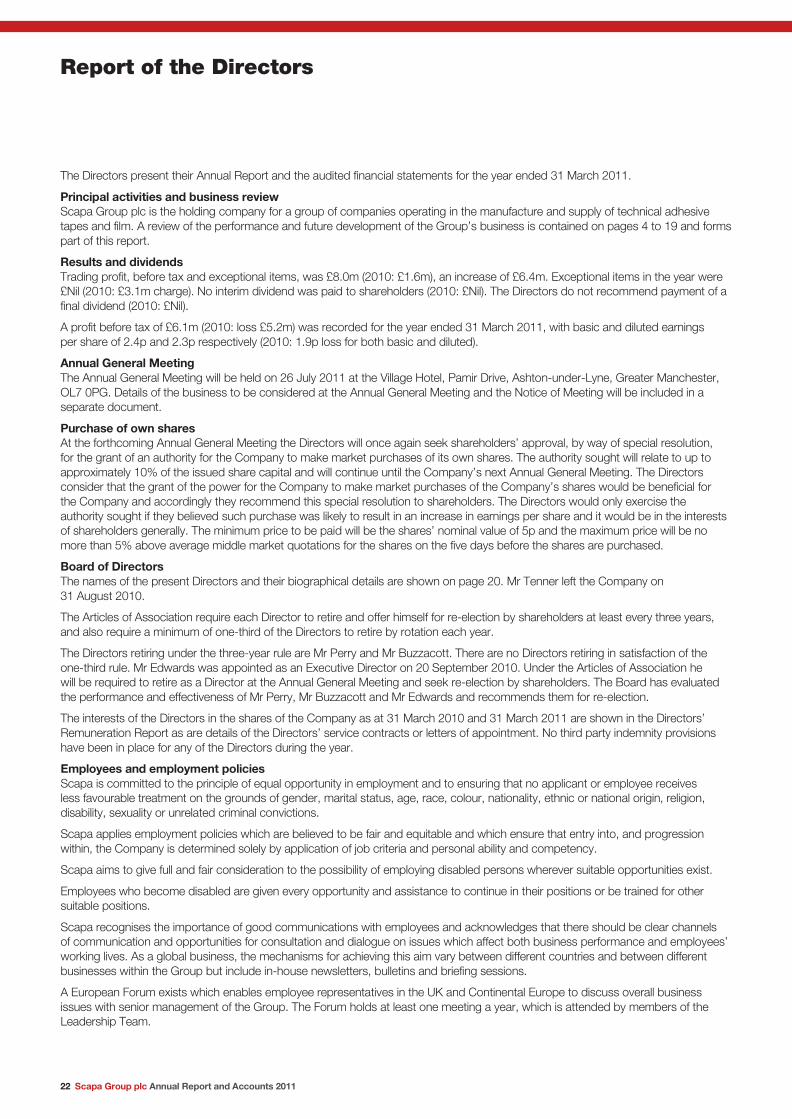

The Directors present their Annual Report and the audited financial statements for the year ended 31 March 2011.

Principal activities and business review Scapa Group plc is the holding company for a group of companies operating in the manufacture and supply of technical adhesive tapes and film. A review of the performance and future development of the Group’s business is contained on pages 4 to 19 and forms part of this report.

Results and dividends Trading profit, before tax and exceptional items, was £8.0m (2010: £1.6m), an increase of £6.4m. Exceptional items in the year were £Nil (2010: £3.1m charge). No interim dividend was paid to shareholders (2010: £Nil). The Directors do not recommend payment of a final dividend (2010: £Nil).

A profit before tax of £6.1m (2010: loss £5.2m) was recorded for the year ended 31 March 2011, with basic and diluted earnings per share of 2.4p and 2.3p respectively (2010: 1.9p loss for both basic and diluted).

Annual General Meeting The Annual General Meeting will be held on 26 July 2011 at the Village Hotel, Pamir Drive, Ashton-under-Lyne, Greater Manchester, OL7 0PG. Details of the business to be considered at the Annual General Meeting and the Notice of Meeting will be included in a separate document.

Purchase of own shares At the forthcoming Annual General Meeting the Directors will once again seek shareholders’ approval, by way of special resolution, for the grant of an authority for the Company to make market purchases of its own shares. The authority sought will relate to up to approximately 10% of the issued share capital and will continue until the Company’s next Annual General Meeting. The Directors consider that the grant of the power for the Company to make market purchases of the Company’s shares would be beneficial for the Company and accordingly they recommend this special resolution to shareholders. The Directors would only exercise the authority sought if they believed such purchase was likely to result in an increase in earnings per share and it would be in the interests of shareholders generally. The minimum price to be paid will be the shares’ nominal value of 5p and the maximum price will be no more than 5% above average middle market quotations for the shares on the five days before the shares are purchased.

Board of Directors The names of the present Directors and their biographical details are shown on page 20. Mr Tenner left the Company on 31 August 2010.

The Articles of Association require each Director to retire and offer himself for re-election by shareholders at least every three years, and also require a minimum of one-third of the Directors to retire by rotation each year.

The Directors retiring under the three-year rule are Mr Perry and Mr Buzzacott. There are no Directors retiring in satisfaction of the one-third rule. Mr Edwards was appointed as an Executive Director on 20 September 2010. Under the Articles of Association he will be required to retire as a Director at the Annual General Meeting and seek re-election by shareholders. The Board has evaluated the performance and effectiveness of Mr Perry, Mr Buzzacott and Mr Edwards and recommends them for re-election.

The interests of the Directors in the shares of the Company as at 31 March 2010 and 31 March 2011 are shown in the Directors’ Remuneration Report as are details of the Directors’ service contracts or letters of appointment. No third party indemnity provisions have been in place for any of the Directors during the year.

Employees and employment policies Scapa is committed to the principle of equal opportunity in employment and to ensuring that no applicant or employee receives less favourable treatment on the grounds of gender, marital status, age, race, colour, nationality, ethnic or national origin, religion, disability, sexuality or unrelated criminal convictions.

Scapa applies employment policies which are believed to be fair and equitable and which ensure that entry into, and progression within, the Company is determined solely by application of job criteria and personal ability and competency.

Scapa aims to give full and fair consideration to the possibility of employing disabled persons wherever suitable opportunities exist.

Employees who become disabled are given every opportunity and assistance to continue in their positions or be trained for other suitable positions.

Scapa recognises the importance of good communications with employees and acknowledges that there should be clear channels of communication and opportunities for consultation and dialogue on issues which affect both business performance and employees’ working lives. As a global business, the mechanisms for achieving this aim vary between different countries and between different businesses within the Group but include in-house newsletters, bulletins and briefing sessions.

A European Forum exists which enables employee representatives in the UK and Continental Europe to discuss overall business issues with senior management of the Group. The Forum holds at least one meeting a year, which is attended by members of the Leadership Team.

Scapa Group plc Annual Report and Accounts 2011 23

Scapa has a combination of unionised and non-unionised operations across the world and is committed to fostering positive employee relations at all of its locations. Training and links with the educational sector reinforce Scapa’s commitment to employee involvement and development.

The Sharesave share option plan gives the opportunity to all UK employees with qualifying service to participate in the equity of the Company. As at 31 March 2011, 61 employees were members of the scheme with 1,762,146 options over shares.

Supplier payment policy The Company’s policy, which is also applied by the Group, is to settle terms of payment with suppliers when agreeing the terms of each transaction, to ensure that suppliers are made aware of the terms of payment, and abide by the terms of payment.

Research and Development The Group’s spend on research and development is disclosed in note 3 and is focused on developing new derivative product applications for addressing and resolving customer and market requirements.

Health and Safety One of Scapa’s primary objectives is to achieve high standards of safety for its employees. Health and Safety is the first standing item on Group Board Meetings and Leadership Team Agendas. Appropriate senior executives, managers and supervisors have defined responsibilities for health and safety and are expected to ensure that the Company’s health and safety policy is adhered to. These responsibilities are reviewed regularly on a national and regional basis to ensure appropriate policy development.

Scapa continues to implement a programme of regular health and safety audits. These audits are undertaken across Scapa’s manufacturing sites. The purpose of the audit programme is to ensure compliance with health and safety legislation, best safety practices and to aim to secure the wellbeing of everyone affected by Scapa’s manufacturing operations.

Financial risk management The Group’s approach to managing financial risk is covered on page 46.

Business ethics The Company requires compliance by its companies and employees with the laws and standards of conduct of the countries in which it does business. This includes legislation implementing anti-corruption and competition law compliance. Employees are required to avoid conflicts of interest regarding Company business, to act lawfully and ethically, and to be responsible for communicating in good faith non-compliance issues of which they become aware.

During the year the Company adopted, and all senior employees formally subscribed to, a Code of Conduct to document and confirm such compliance.

Political and charitable donations It is not corporate policy to make any political donations and, accordingly, no political donations were made during this year. Charitable donations made during this year amounted to £12,159 (2010: £4,919). The majority of charitable donations made, on a discretionary basis, are to organisations based in the vicinity of Scapa sites, especially organisations which support health and educational causes.

Share options Details of the Company’s share capital and options over the Company’s shares under the Company’s employee share plans are given in note 22 of the accounts on page 68.

Major shareholders The Company has been notified that the following have an interest of 3% or more in the issued share capital of the Company, as at 26 May 2011:

%

Cazenove Capital Management 13.46 Rights & Issues Investment Trust 7.20 Schroders plc 6.60 Investec Asset Management 6.58 River & Mercantile Asset Management 6.23 UBS Global Asset Management 5.81 Cazenove UK Dynamic Absolute Return Fund 4.82 Royal Bank of Canada 4.54 Deutsche Bank AG 3.96 M&G Investment Management 3.57 Lowland Investment Company Plc 3.04

Overview

Business R

eviewG

overnanceFinancial Statem

ents

Report of the Directors continued

24 Scapa Group plc Annual Report and Accounts 2011

Takeover directive The Company has only one class of ordinary share and these shares have equal voting rights. The nature of individual Directors’ holdings is disclosed on page 28. There are no other significant holdings of any individual.

Auditors and disclosure of information to auditors So far as each Director is aware, there is no relevant audit information of which the Company’s auditors are unaware. Each Director has taken all the steps that he ought to have taken as a Director in order to make himself aware of any relevant audit information and to establish that the Company’s auditors are aware of that information.

The auditors, PricewaterhouseCoopers LLP, have indicated their willingness to continue in office and a resolution that they be re-appointed will be proposed at the Annual General Meeting.

Corporate governance The Company’s statement on Corporate Governance can be found in the Corporate Governance Report on pages 30 to 34 of these financial statements. The Corporate Governance Report forms part of this Directors’ Report and is incorporated into it by cross-reference.

By order of the Board Registered Office:

M R Stirzaker, BA, Solicitor Company Secretary 26 May 2011

Manchester Road Ashton-under-Lyne Greater Manchester OL7 0ED

Directors’ Remuneration Report

Scapa Group plc Annual Report and Accounts 2011 25

This report describes the role and composition of the Remuneration Committee (‘the Committee’), the Company’s remuneration policy and the arrangements currently applicable for the remuneration of Executive and Non-Executive Directors. The report has been prepared in accordance with the Directors’ Remuneration Report Regulations 2002, although the Regulations do not strictly apply to an AIM listed company. A resolution to approve the report will be proposed at the Annual General Meeting 2011.

The parts of the report which are subject to audit by PricewaterhouseCoopers LLP are indicated with an asterisk (*). All other parts of the Directors’ Remuneration Report are unaudited.

Remuneration Committee The Committee is comprised of the Non-Executive Directors of the Company, namely Mr Wallace, Mr Buzzacott (Chairman of the Committee) and Mr Perry. The members of the Committee have no personal financial interest in the Company other than as shareholders and the fees paid to them as Non-Executive Directors. The Company Secretary acts as secretary to the Committee.

The Chief Executive is not a member of the Committee but is invited to attend meetings if appropriate. The Committee liaises with the Chief Executive regarding proposals concerning the remuneration of the Group Finance Director and other specified senior executives. The Chief Executive is not present when the Committee considers issues relating to his remuneration.

The Committee determines, on behalf of the Board, the Company’s policy on the remuneration of the Executive Directors. The Committee determines the total remuneration packages for these individuals, including the recruitment terms, remuneration benefits, employment conditions, pension rights and any compensation payments on termination of office. The Committee also determines the remuneration framework for other specified senior executives. The Committee met four times in the year to 31 March 2011 and all members of the Committee attended each of the meetings.

Advisers The Committee takes professional advice from within and outside the Company when it feels it to be appropriate to do so.

Remuneration policy The Committee’s policy for the remuneration of Executive Directors aims to:

• pay basic salaries which equate with those paid by other comparator companies of similar market capitalisation and business sector;

• provide executives with opportunities to increase their remuneration by the attainment of key short-term and longer-term objectives;

• encourage the holding of shares in the Company (including the retention of shares acquired via company share-based plans); and • provide incentives which aim to align the interests of executives and shareholders and promote the creation of long-term value.

Components of remuneration The components of the remuneration packages for Executive Directors are as follows:

Basic salaries This is a fixed cash sum, payable monthly. Salaries are reviewed annually by the Committee in the light of individual performance and market comparisons for similar jobs. Factors considered for comparison purposes include company type and sector, measures of company size and degree of international scope. Changes to the Chief Executive’s salary are normally effective from 1 January, and any changes to the salaries of the other Executive Directors normally take effect from 1 April. The basic salaries of the Executive Directors for the year ending 31 March 2011 are set out in the table on page 26.

Annual bonus The Company operates a bonus scheme for the Executive Directors and senior executives based on a percentage of basic salary at the start of the financial year. Bonus payments are not pensionable. The basis of the Executive Directors’ bonus scheme and the targets to be attained are reviewed annually by the Committee.

For the year ended 31 March 2011 the Committee decided that the primary focus of the bonus scheme would be net cash flow, which the Committee felt to be important in maintaining the strength of the Company’s Balance Sheet during a continuing difficult economic climate, plus a challenging element in respect of operating profit performance (statutory profit adjusted for foreign exchange). Accordingly, 50% of the bonus related to cash flow performance and 50% to operating profit performance. 40% of the bonus was payable for achievement of the targets set out in the Group’s budget for the year, and the balance for significant outperformance in excess of the budget up to a maximum of 100% of basic salary.

In respect of 2011/12 the Committee has decided that cash flow and profit performance should remain the cornerstones of the bonus scheme but an element of personal performance would also be appropriate. Accordingly, 40% of the bonus will relate to cash flow performance, 40% to operating profit performance and 20% will relate to the achievement of pre-agreed personal objectives. Forty percent of the cash and profit elements will be payable for achievement of the targets set out in the Group’s budget for the year and the balance for significant outperformance in excess of the budget up to a potential maximum of 140% of basic salary in exceptional circumstances (inclusive of the personal performance element).

Overview

Business R

eviewG

overnanceFinancial Statem

ents

Directors’ Remuneration Report continued

26 Scapa Group plc Annual Report and Accounts 2011

Share price incentive bonus The Committee has decided to introduce a bonus scheme with the specific purpose of providing a meaningful incentive to key senior executives of the Company (including the Executive Directors) to achieve an outstanding, challenging and sustainable increase in value for the Company’s shareholders. If, in the four-year period commencing 1 July 2011, the mid-market price of the Company’s shares equals or exceeds £1.00, the scheme will reward the Executive Directors with a payment equal to 12 months’ basic salary. There will be no payment if the share price target is not maintained for a period of 30 consecutive days. If the mid-market price equals or exceeds £1.50 per share for 30 consecutive days within the four-year life of the scheme, the total payment will be equal to twice the basic salary of the relevant Executive Director.

Benefits in kind In addition to pension provisions, Executive Directors are also entitled to car allowances, private medical insurance, permanent health cover and life assurance.

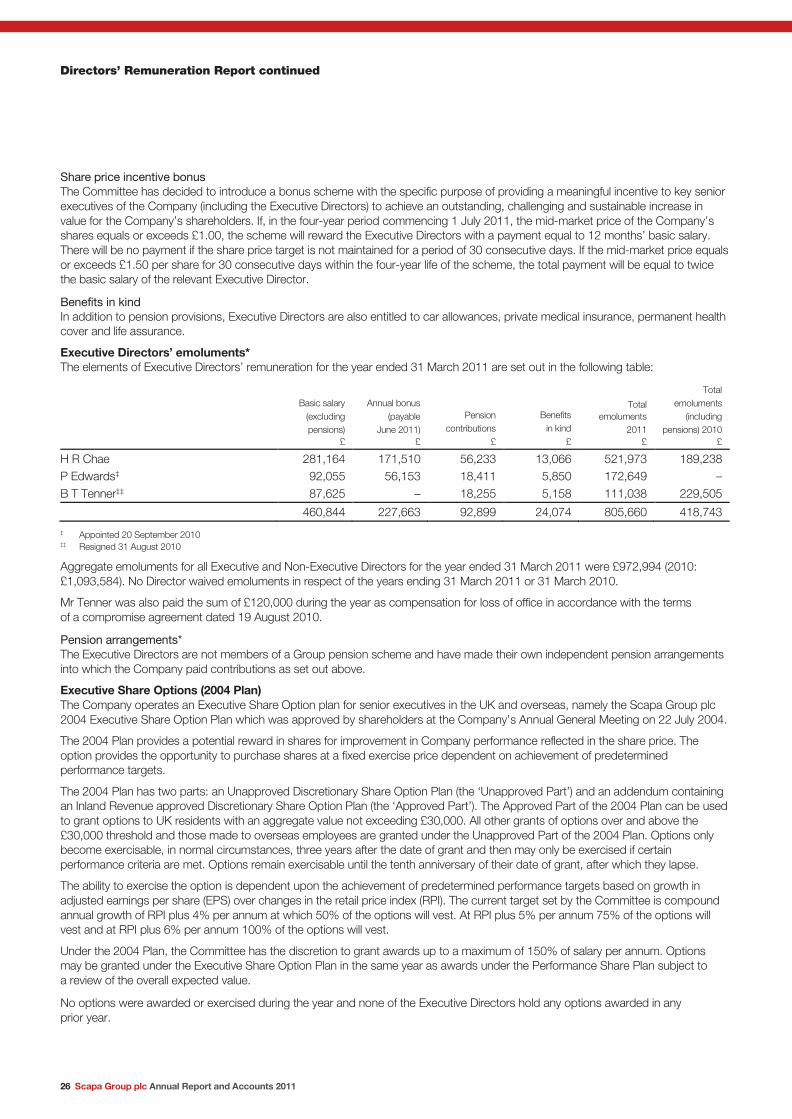

Executive Directors’ emoluments* The elements of Executive Directors’ remuneration for the year ended 31 March 2011 are set out in the following table:

Basic salary (excluding pensions)

£

Annual bonus (payable

June 2011) £

Pension contributions

£

Benefits in kind

£

Total emoluments

2011 £

Total emoluments

(including pensions) 2010

£

H R Chae 281,164 171,510 56,233 13,066 521,973 189,238 P Edwards‡ 92,055 56,153 18,411 5,850 172,649 – B T Tenner‡‡ 87,625 – 18,255 5,158 111,038 229,505

460,844 227,663 92,899 24,074 805,660 418,743

‡ Appointed 20 September 2010 ‡‡ Resigned 31 August 2010

Aggregate emoluments for all Executive and Non-Executive Directors for the year ended 31 March 2011 were £972,994 (2010: £1,093,584). No Director waived emoluments in respect of the years ending 31 March 2011 or 31 March 2010.

Mr Tenner was also paid the sum of £120,000 during the year as compensation for loss of office in accordance with the terms of a compromise agreement dated 19 August 2010.

Pension arrangements* The Executive Directors are not members of a Group pension scheme and have made their own independent pension arrangements into which the Company paid contributions as set out above.

Executive Share Options (2004 Plan) The Company operates an Executive Share Option plan for senior executives in the UK and overseas, namely the Scapa Group plc 2004 Executive Share Option Plan which was approved by shareholders at the Company’s Annual General Meeting on 22 July 2004.

The 2004 Plan provides a potential reward in shares for improvement in Company performance reflected in the share price. The option provides the opportunity to purchase shares at a fixed exercise price dependent on achievement of predetermined performance targets.