Embed Size (px)

Citation preview

Building effective board-management relationships

evidence and prescriptions from New Zealand

By Ljiljana Erakovic and Sanjay Goel

1

▼

he recent awareness of lack ofoversight in many boardrooms incorporate America has fuelled yetanother debate about the role and

efficacy of the board of directors as aninstitution in public corporations. This debateand, indeed, a variety of prescriptions offeredfrom a variety of perspectives have been incirculation for as long as boards have existed(Stiles and Taylor, 2001). The debate has notbeen limited to the American context alone. In

the UK, Sir Adrian Cadbury’s final report on“The Financial Aspects of CorporateGovernance” in 1998 was largely influential insetting in motion a chain of events thattransformed the composition and structure ofBritish boards.

The purpose of this paper is to explore thenature of the relationships between boards andmanagement in New Zealand. The paper is partof a larger study that considers corporate

T

▼

U N I V E R S I T Y O F A U C K L A N D Business Review

V o l u m e 6 N u m b e r 1 2 0 0 4

2

governance practice in two different types ofindustries: traditional and hi-tech. Here we presentour findings from companies that belong totraditional industries. We place particular emphasison the internal workings and dynamics of the boardsin these industries, thereby moving beyond thestructural debate about “who should be on theboard?” We believe this addresses the question of“how should boards govern the corporations?” bylooking directly at their functional contribution. Inaddition, this charges the board with the centralresponsibility of governing the corporation, andmanagers with managing it.

The major contribution of this paper is ininvestigating the board’s role as a resource via threekey governance processes. First, we investigate theboard’s level and sources of knowledge bases, andhow they are linked or deployed toward the roles aboard is supposed to play. Second, we investigatethe board’s involvement in the oversight andmonitoring of a company’s financial outcomes, itstop management and its strategic processes andoutcomes. Third, we investigate how the board’sreputation serves as a resource in and of itself tothe company, which may not require the board toplay any other functional role on behalf of thecompany. Drawing on the literature addressingboards of directors (e.g., Carter and Lorsch, 2004;Johnson, Daily and Ellstrand, 1996), we believe thatthese three processes characterise the dynamics ofboards. After describing our research method, wecontrast findings from three cases and developuseful prescriptions for governance of firms intraditional industries.

CHANGING WORLD OFCORPORATE GOVERNANCE

he emerging research on corporate governancehas extensively considered the changing role of

boards in modern corporations. Carter and Lorsch(2004), in their book Back To The Drawing Board,analysed a number of issues or paradoxes that boardsaround the world have to deal with and, accordingly,redesign themselves and their relationships withinand outside corporations. The major issues the

authors point to are the changing expectations thatmanagement, shareholders and other stakeholders(customers, employees and suppliers) have aboutdirectors’ knowledge, and contribution to andinvolvement in the company’s strategic affairs.

Other works have focused on the role of the boardalong more philosophical lines to trace the sources oftheir effectiveness or otherwise. For instance,Sundaramurthy and Lewis (2003) focus on theimportance of the dynamic balance between controland collaboration approaches in board-managementrelationships. According to the authors, a controlapproach protects a corporation from self-servingbehaviour and reduces goal conflict, whereas acollaborative approach encourages co-operationbetween board and management and fosters trust andgoal alignment. Acceptance, understanding andmanagement of control-collaboration tensionspromote learning and improve governance(Sundaramurthy and Lewis, 2003).

Goel and Erakovic (2003), however, highlight theseeming paradox in expecting boards to serve asmonitors and mentors of corporate managementsimultaneously when they require ratherincongruent skills. Similarly, Shen (2003) callsattention to the evolution of the CEO-boardrelationship. The dynamics of relationships betweenthe CEO and the board is one of the dimensions ofthe governance paradox mentioned above.Following the evolutionary perspective, Shen (2003)argues how the advisory role of a board has relativelyhigher significance in the early period of CEO tenurewhile the control-focused approach is moreemphasised in later CEO tenure. This approachdeals with the qualitative differences betweenmonitoring and mentoring by identifying specificepochs when each is needed, but does not provide aconceptual approach to combining them in a varietyof proportions.

Our research pursues a similar path of research,attempting to tackle a specific angle of the changingworld of corporate governance: relationshipsbetween boards and management in New Zealandcorporations.

T

A control approach protects a corporation from self-serving

behaviour and reduces goal conflict ... a collaborative approach

encourages co-operation and fosters trust and goal alignment

3

SETTING THE SCENE

ew Zealand’s model of corporate governancerelies on the Anglo-American system of

corporate governance where institutional investorsplay an important role. According to Farrar (2001),more than 50 per cent of all share capital in NewZealand is held by various institutions.

Recent international corporate failures,particularly in the US, have prompted reviews ofNew Zealand’s regulatory framework of corporategovernance. Regulatory authority has attempted tointroduce the changes that are applicable to the sizeand specific characteristics of the New Zealandeconomy. In addition, many companies have decidedto review their policies and introduce some newmeasures in their corporate governance practices.With this aim, the Institute of Directors in NewZealand has provided guidelines of best practice incorporate governance. This document, Code ofProper Practice for Directors, considers moral andethical responsibility of directors (the Institute,1999). The fundamental legal framework ofcorporate governance in New Zealand is regulatedby the Companies Act 1993.

The New Zealand outside-based regime ofcorporate governance perceives the role of directorsas monitoring, emphasising specific tasks inestablishing goals and performance policies,appointing the CEO, and protecting the company’sfinancial position (the Institute, 1999). In terms ofboard composition, New Zealand’s system prefers

boards dominated by non-executive or independentdirectors. The roles of board chairman and CEOare expected to be separated, and the chairmanshould be a non-executive director.

RESEARCH METHOD AND DESIGN

his paper is part of a larger research projectreviewing seven New Zealand companies from

different industries. Three cases are used here. Weselected cases from traditional industries so we canprovide transparent conclusions by eliminating hi-tech industry-specific external (and internal) factors.In addition, traditional-industry sectors still embracethe dominant economic activities in New Zealand.As a point of clarification, we define all resource-intensive (i.e., raw materials-processing industries),labour-intensive (e.g., textile industries) and scale-intensive industries (e.g., transportation, consumerelectronics) (OECD, 1996; as cited in Clarke andClegg, 1998) as traditional industries.

The companies we present here belong to threedifferent industry sectors within the traditionalindustry framework. They have different ownershipstructures and are different in size and market inputand output orientations (Table 1). Our intent is tohighlight various governance issues in New Zealandcompanies. In selecting the companies for theresearch, therefore, we were looking more for adiverse rather than a representative sample. Wechose three archetypical companies with a widedifference in their context and ownership structure.

T

N

�

U N I V E R S I T Y O F A U C K L A N D Business Review

V o l u m e 6 N u m b e r 1 2 0 0 4

4

TABLE 1

Profile of companies represented in traditional industriesCase SOUTHERN STAR SAGITTARIUS ACRUX

Industry sector Building and Food manufacturer Transport infrastructureconstruction products

Established 1952 1979 1990

Revenue 2003 632,300 25,000 47,700(in NZ$ 000)

Staff 1100 120 73

Market orientation International Domestic (output) DomesticInternational (input)

Market status Major producer in Competitive MonopolyAustralasian region

Current ownership Publicly listed company Private company Mixed public/privatestructure

Number of directors 6 4 6

BOD composition 1 inside (CEO), 1 inside (CEO), All outside directors5 outside directors 3 outside directors

(all shareholders)*

* 60 per cent shareholding in Sagittarius lies with the board.

One is a publicly listed company with a more globalorientation; another company is a privately ownedcompany with a local orientation, and the thirdcompany is in a mixed ownership (local governmentand private) with a de facto monopoly position inthe local market. We used pseudonyms instead ofthe companies’ real names and labelled thecompanies Southern Star, Sagittarius and Acrux.

Since our research aims to explore specificorganisational relationships and eventually allowfor a conceptual elaboration of a large numberof often-conflicting individual, organisationaland contextual factors, we use a qualitativeapproach to our research question. Currentmanagement theories do not provide a holisticview of the phenomenon as they each tacklespecific angles of the relationship, albeit in acontrolled large sample. On the other hand,research observing the nature of corporategovernance relations requires an in-depthunderstanding of the social , managerial ,economic and cultural aspects of the process.Hence, a grounded-theory approach is taken asthe most appropriate methodology in studyingthese unexplored organisational interactions.Incorporating multiple cases, this study employedcomparative analyses across cases to identifymajor patterns.

Data was collected through interviews,questionnaires and secondary sources. Data fromsecondary sources (i.e., annual reports,organisational documents and companies’ websites)offered general information about the company andits task environment. The major source ofinformation was semi-structured interviews withmembers of the board and the top executive team.

In total, we conducted 14 interviews in threecompanies. Table 2 provides more details about thekey respondents.

THREE PATTERNS OFCORPORATE GOVERNANCE

ur data provided in-depth insights intorelationships between the board of directors

and management teams, and pointed out theimportant issues in their interactions. The dataalso indicated different patterns of corporategovernance in different organisations. The patternswere linked with three sets of governance processesor characteristics.

Board knowledge and knowledgeacquisition processes

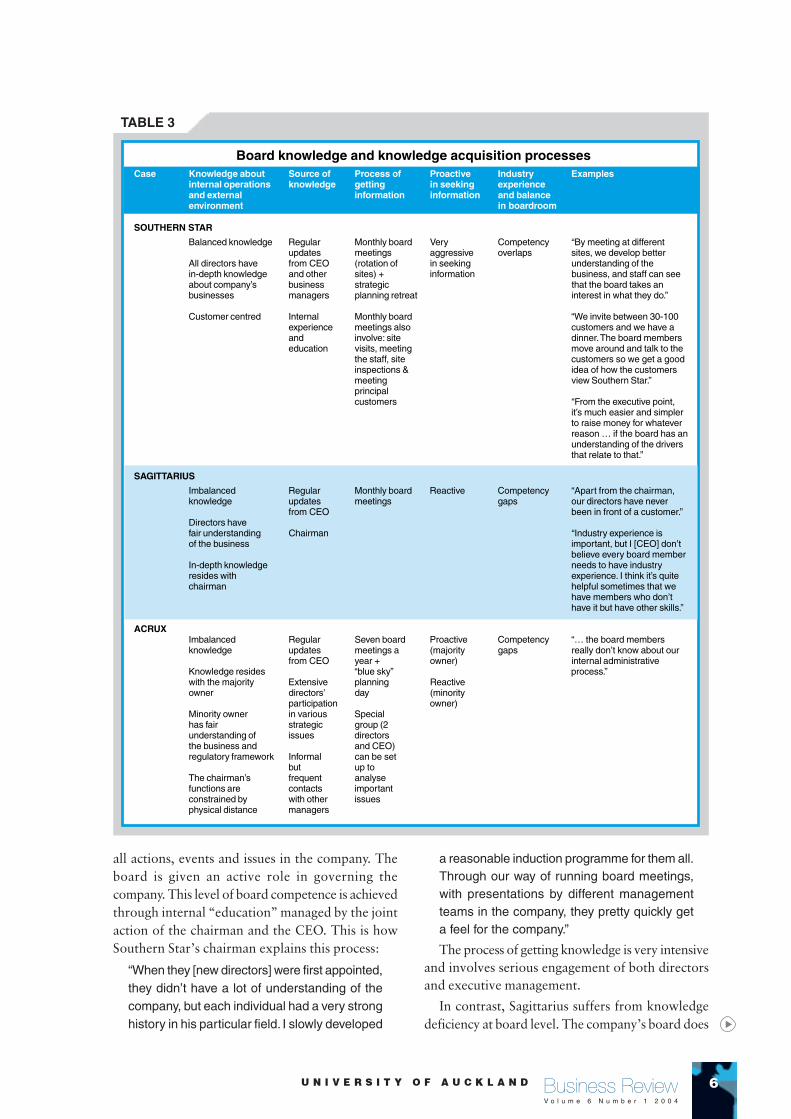

The first set of processes examined the directors’knowledge of the company’s business operations.We asked directors and executive managers abouttheir directors’ knowledge of internal operations andexternal environment, about their willingness toabsorb presented information and seek moreinformation about the company, and about theimportance of industry experience for the board’sfunctioning. Table 3 shows how companies differon four major concepts of board knowledge.

It is evident that the balance of knowledge amongdirectors varies between the companies. Directors’knowledge in Southern Star is much more balancedthan in Sagittarius or Acrux. We found thatvariations rely on (1) source of knowledge; (2)process of getting knowledge; and (3) directors’active or inactive role in processing or seekinginformation.

Southern Star directors are knowledgeable about

TABLE 2

Distribution of primary respondents by caseCase (company) Total interviews BOD Key respondents Mgmt Key respondents

SOUTHERN STAR 6 3 Chairman + 2 directors 3 CEO, CFO, Gen. manager

SAGITTARIUS 4 2 Chairman + director 2 CEO, CFO

ACRUX 4 2 2 directors 2 CEO, CFO

O

Research observing the nature of corporate governance

relations requires an in-depth understanding of the social,

managerial, economic and cultural aspects of the process

5

TABLE 3

Board knowledge and knowledge acquisition processesCase Knowledge about Source of Process of Proactive Industry Examples

internal operations knowledge getting in seeking experienceand external information information and balanceenvironment in boardroom

SOUTHERN STAR

Balanced knowledge Regular Monthly board Very Competency “By meeting at differentupdates meetings aggressive overlaps sites, we develop better

All directors have from CEO (rotation of in seeking understanding of thein-depth knowledge and other sites) + information business, and staff can seeabout company’s business strategic that the board takes anbusinesses managers planning retreat interest in what they do.”

Customer centred Internal Monthly board “We invite between 30-100experience meetings also customers and we have aand involve: site dinner. The board memberseducation visits, meeting move around and talk to the

the staff, site customers so we get a goodinspections & idea of how the customersmeeting view Southern Star.”principalcustomers “From the executive point,

it’s much easier and simplerto raise money for whateverreason … if the board has anunderstanding of the driversthat relate to that.”

SAGITTARIUS

Imbalanced Regular Monthly board Reactive Competency “Apart from the chairman,knowledge updates meetings gaps our directors have never

from CEO been in front of a customer.”Directors havefair understanding Chairman “Industry experience isof the business important, but I [CEO] don’t

believe every board memberIn-depth knowledge needs to have industryresides with experience. I think it’s quitechairman helpful sometimes that we

have members who don’thave it but have other skills.”

ACRUXImbalanced Regular Seven board Proactive Competency “… the board membersknowledge updates meetings a (majority gaps really don’t know about our

from CEO year + owner) internal administrativeKnowledge resides “blue sky” process.”with the majority Extensive planning Reactiveowner directors’ day (minority

participation owner)Minority owner in various Specialhas fair strategic group (2understanding of issues directorsthe business and and CEO)regulatory framework Informal can be set

but up toThe chairman’s frequent analysefunctions are contacts importantconstrained by with other issuesphysical distance managers

all actions, events and issues in the company. Theboard is given an active role in governing thecompany. This level of board competence is achievedthrough internal “education” managed by the jointaction of the chairman and the CEO. This is howSouthern Star’s chairman explains this process:

“When they [new directors] were first appointed,they didn’t have a lot of understanding of thecompany, but each individual had a very stronghistory in his particular field. I slowly developed

a reasonable induction programme for them all.Through our way of running board meetings,with presentations by different managementteams in the company, they pretty quickly geta feel for the company.”

The process of getting knowledge is very intensiveand involves serious engagement of both directorsand executive management.

In contrast, Sagittarius suffers from knowledgedeficiency at board level. The company’s board does

�

U N I V E R S I T Y O F A U C K L A N D Business Review

V o l u m e 6 N u m b e r 1 2 0 0 4

6

not have an in-depth knowledge of the company’soperations. Knowledge resides with the chairmanwho has an intimate knowledge of, interest in, andpassion for the business. Two other outside directorson the board are more passive monitors of thecompany’s performance. The chairman of the boardrepresents a valuable source of information andknowledge for both the rest of the board andexecutive management. The chairman is activelyinvolved in the day-to-day management ofSagittarius. He communicates with the CEO on adaily basis, attends executive meetings regularly andis well informed about all external and internaldetails of the business. This situation creates twolevels of knowledge asymmetry in the company:(1) between the chairman and two outside directors;and (2) between the executive management andthe board.

In the case of Acrux, a specific imbalance ofknowledge exists among the directors of a boardsplit by ownership. The board consists ofrepresentatives (two-thirds) of the majority ownerand representatives (one-third) of the minorityowner. The first group has an in-depthunderstanding of the company’s goals. Therefore,their expertise and activities as directors are orientedtoward fulfilling the demands of the parentcompany. They play an active role in seekinginformation about the company’s operations andenvironmental trends from within the company (i.e.,executive management and lower-level managers)and very often from independent outsideinstitutions. Guided by the clear motive ofmaximising shareholder value, this group ofdirectors imposes certain pressures on themanagement team and challenges it on variousstrategic issues.

On the other hand, the directors of the minorityparty have a good understanding of the business,but are not as proactive as the first group. They actmore as observers, with the purpose of protectingthe interests of the wider community they represent.The chairman’s role additionally contributes to theexisting imbalance of knowledge between the two

groups. The chairman, who has extensiveknowledge of the industry, is only intermittentlyinvolved in the company’s business because he doesnot live in New Zealand and he is closely involvedwith the parent company’s overseas operations.Physical distance and functional dissociationconstrain his ability to share information withmanagement and other directors.

Whatever industry the companies operate in,their directors’ industry experience is perceived asan important condition of good corporategovernance. Industry experience of non-executivemembers of the board is emphasised as particularlyvaluable. Board members’ industry knowledgeenables directors to understand the ability ofmanagement and the company to influence strategicoutcomes. One of the Acrux directors specificallyemphasised the function of industry knowledge inevaluating management strategic options anddirecting the decision-making process. Accordingto his point of view:

“It is incredibly important to have somebodyelse [besides the CEO] with industry experience.You never even want to have a situation whereyou’ve got only one guy who can say, ‘I’m theexpert here’.”

Southern Star’s CEO shares the same perception:

“Industry experience ensures that themanagement are questioned about some of thethings that a non-industry professional wouldn’tknow to ask.”

In addition, intimate industry knowledgeincreases the overall value of the company asdirectors are able to provide easier access to thecustomer or supplier base at a board-to-board level.Industry knowledge, from this perspective, increasesthe credibility of directors versus managers.

Both directors and management believe industryknowledge is not the only condition of successfulfunctioning of the board. What most of them pointto is a good balance of expertise and skills in theboardroom, and respect for each other’s expertise.Directors with experience in other industries or withdifferent expertise provide challenges for the

Whatever industry the companies operate in, their

directors’ industry experience is perceived as an

important condition of good corporate governance

7

management and other directors. This is how thechairman of Southern Star comments on thecomposition of his board:

“I’ve chosen pretty strong people. I alwaysbelieve in managing as well as developing aboard with people who are going to challenge,not by intimidating you. I believe we have aboard of independent thinkers with differentdisciplines in their background and we havevery lively discussions. I’m sure by the time wefinish [the board meetings], we’ve sorted outmost of the issues.”

In all three companies, the chairmen haveintimate knowledge of their respective industries.Each has spent more than 30 years within the sameindustry and all were CEOs of large New Zealandor international companies. In two cases, Sagittariusand Acrux, an evident competency gap existsbetween the chairman and the rest of the board.The competency gap in Sagittarius is compensatedfor by a very close relationship between the

chairman and CEO, and the chairman’s mentoringrole in growing management and the wholecompany. In Acrux, however, the competency gapis deepened by the chairman’s physical isolationfrom the rest of the board and the CEO.

Board involvement

The second set of questions considered directors’involvement in strategy making and key businessissues. We asked directors and executive managersto explain the directors’ involvement in strategymaking, the way they work and their involvementin the company’s other business activities and withother managers. Table 4 shows how companiesdiffer on four major concepts of board involvement.

It is evident that the degree and balance ofinvolvement among directors varies between thecompanies. Directors’ involvement in Southern Staris much more intensive and balanced than inSagittarius or Acrux. We found that the variationsdepend on: (1) the roles the chairman and CEO

TABLE 4

Dimensions of board involvementDominanttopic atboardmeetings

Financialissues

Financialissues

Financialissues

Team work/group work

Collaborationwithout“group-think”

Synergy

Closerelationshipbetweenchairmanand CEO

“Group-think”behaviour

Closerelationshipbetweenchairmanand CEO

No teamwork

Coalition oftwo differentgroups

Lack of closerelationshipbetweenchairmanand CEO

Strategyprocess

Long-termstrategydevelopedand decidedby board

Business plandeveloped bymanagementand decidedby board

Chairman ishighly involved instrategy forming

Board reviewsstrategypresented to it

Board isinvolved instrategy-makingprocess in anearly phase(“blue skyplanning”) and infinal stage ofdecision making

Ownershipof finaldecision

Board ofdirectors

Chairman

Majorityownerdirectors

Case

SOUTHERNSTAR

SAGITTARIUS

ACRUX

Examples

“At times there is a very strongdifference in opinion, but werarely leave the board tablewithout having sorted thatdifference out.”

“I [CEO] do not think I’ve everchanged anything from when I’vepresented the strategies.”

“If the chairman says, ‘I agree’, itjust gets a tick in the box.”

“We’ve [majority owner directors]found it desirable to encouragecorrespondence outside of theboard forum. We don’t like havingjust the CEO as the conduitbetween the board andmanagement.”

“It would be rare that I [minorityowner director] would havecontact with management inbetween board meetings. I readmy board papers and turn up andproactively interact on the day.”

�

U N I V E R S I T Y O F A U C K L A N D Business Review

V o l u m e 6 N u m b e r 1 2 0 0 4

8

have in the company; (2) the directors’ perceptionsof their role in the company; and (3) the type of tiesthat link directors and managers.

In Southern Star, the CEO has initiated thedirectors’ involvement in strategy forming from theearly stages of the process. He believes that in thepast, the board was not sufficiently involved instrategy and that its input was not strong enough.He points out:

“It’s a very appropriate thing for a board to beinvolved in strategy. It must be involved in themaking and setting of the strategy.”

Southern Star’s board works as a team-orientedcoalition of individuals. This paradox is embeddedin the strong personalities of directors who arewilling to take their own perception on anyparticular subject on the one hand and who aretrying to reach consensus in their collective decisionson the other. As the CEO explains:

“There is no obvious leader, so there is notsomebody who is the loudest person talkingand everybody follows him. I think that isparticularly so because each one of themembers of the board represents a spoke inthe wheel in terms of the skill set andknowledge base and background.”

Thus, synergy and collaborative efforts existwithout “group-think”.

Such group dynamics are reinforced by the long-term social and business relationships directors andmanagers have developed over time. For example,the current chairman and CEO of Southern Starhave been working together for more than threedecades. They both, in different managementcapacities, have contributed to building theorganisation from a very small manufacturer to aleading company in the industry.

Directors’ involvement in Sagittarius’ businessstrategy is low. The logical consequence of theimbalance of knowledge among board members istheir imbalanced involvement in strategy and keybusiness issues. Sagittarius’ CEO explains thissituation this way:

“I don’t think our board contributes as much as

they could, as much as they should. Theirknowledge and their expertise, in what they doin their professional daily routines, are not fullyutilised in terms of what they could offer to ourbusiness. It is not voluntarily offered. It is morereactive than proactive.”

As a consequence, responsibility for thecompany’s governance is delegated to one person:the chairman. The relationships between thechairman and CEO are perceived as mentoring. Thechairman provides guidelines to the managementabout future directions and he also, together withthe CEO, maintains external relationships withcustomers, distributors and suppliers. The chairmanexplains his role:

“What I do as the chairman in [Sagittarius] isto add value, using my experience in theindustry, to grow and mentor and develop amanagement team.”

The rest of the board view their role primarily asauditors of past performance. Directors’ primaryfocus is on financial results rather than operationsor overall strategy. The board rarely tackles issuessuch as human-resource policies, research anddevelopment, or market expansion.

In the case of Acrux, the relationship betweenboard and management is dominated by directorswho represent the majority owner. They are veryactive in monitoring the management, settingorganisational performance levels and developingthe business. This group plays an intermediary rolebetween the Acrux management team and theinvestment company, a majority shareholder, whichputs constant pressure for high returns on itsinvestment. Minority owner-directors find itdifficult to influence company policy, as the twoparties have different expectations of the company.There is always a tension between the bottom-lineobjectives and as the minority-owner perceives aswider strategic objectives. Therefore, these twogroups of directors rarely work together. As theminority-shareholder director explains:

“The reality is that we cannot influence theoutcomes of Acrux with a minority share-

“It’s a very appropriate thing for a board to

be involved in strategy. It must be involved

in the making and setting of the strategy”

9

holding. We can influence them much easierfrom outside than from inside the camp.”

The chairman’s role and involvement ingovernance matters of Acrux, in practice, areconstrained by his physical isolation from thecompany. Both directors and management of Acruxpoint this out as a major problem of their company’sgovernance. Communications between the chairmanand CEO are irregular and usually performed byelectronic means. The CEO describes the situation:

“My chairman has a variety of demands uponhis time, he’s travelling the world a lot, and so90 per cent of our communication is just byemail wherever he may be. I see the guy onlyseven to nine times a year. So it’s not the idealrelationship. The ideal relationship of CEO tochairman is the fact that you can have a cup-of-coffee meeting every week and go throughissues for half an hour or so.”

This isolation makes the relationships betweenchairman and CEO more formal, emphasising theimportance of reporting and monitoring functions.The condition also forces the CEO to seek advicefrom other directors. That changes the boarddynamics.

In addition to the problems of two differentgroupings within the board and constrained contactsbetween the chairman and CEO, a third predicamentresides in relationships between directors andmanagement. The CEO and financial managermaintain formal interactions with the directors andact as a filter for all communications between thecompany and its board. Majority-owner directorsdisapprove of such a practice, believing that broaderinteractions with other executives would help thecompany and shareholders achieve their ultimateobjectives. One of the directors explains:

“If you were sitting on a board and you wereonly ever talking to the CEO, it would be pretty

frustrating stuff. I think it would be better forthe company if the management sat there. Idon’t know how open their internalmanagement system is, whether they have aMonday meeting where everyone sits around.They never told us. I think that if you have anopen forum, it’s good for everybody becausethen everyone gets a sense of which way thecompany is going and they get a sense ofwhere the board is coming from.”

Firm and board reputations

Finally, we examined directors’ and executivemanagers’ perspectives on the company’s and theboard’s reputations. We define reputation as positiveassociations that others make of a particularindividual or a formal group of individuals. Weconsider it important to analyse reputation in thecontext of this research as a company’s reputationcan reflect the quality of the relationship betweenboard and management, between management andthe firm’s business associates, as well as betweenthe board and other stakeholders. In addition, thedirectors’ good reputation is seen as an externalfactor that can attract desirable tangible andintangible assets, and as an internal factor that canincrease directors’ credibility within the companyand contribute to the development of more effectiverelationships between the board and management.

The set of questions on reputation focused onrelationships between the company and differentstakeholders, and on relationships between thecompany’s and the board’s reputation. We adopted aspecific approach, asking participants to give theirperceptions on stakeholders’ likely interpretation ofthe company’s reputation. We believe that directors’perceptions of the company’s reputation can influencethe intensity of their involvement with the company.On the other hand, executives’ perception of thecompany’s reputation can influence their expectations

“If you have an open forum, it’s good for everybody because

then everyone gets a sense of which way the company is

going and they get a sense of where the board is coming from”

�

U N I V E R S I T Y O F A U C K L A N D Business Review

V o l u m e 6 N u m b e r 1 2 0 0 4

10

toward directors’ input and behaviour. Table 5describes the specific concepts of the company’sreputation that emerged from the data.

Southern Star provides a good example of areputable company. Its directors and managementbelieve their company’s reputation depends on therelationships they have established with theirsuppliers and customers, in particular. They alsoemphasise the qualities of openness andtransparency as the key attributes of theirrelationships with various stakeholders. Both groupsstress two most important aspects of reputation: thecompany’s overall performance, and management’sintegrity and reputation. A director puts it this way:

“The most important factor is people, not money.Money is important, but people … I think it’s amuch bigger factor than people realise incorporate governance … it is the people.”

When the current owners acquired Sagittarius in1999, the company was in bad shape and had a badreputation. The board and new managementembarked on the difficult task of developing thebusiness and improving the company’s position. TheCEO explains the situation at that time:

TABLE 5

Firm and board reputationCase

SOUTHERNSTAR

SAGITTARIUS

ACRUX

Firm reputation

Reputation residesin stability

A true culture ofcustomer service

Integrity andreputation ofmanagement

Company’s overallperformance

Reputation intransition

Product brand

Reputation incollision

Shareholder value

Involvement withthe community

Major factors

� Steady returnson investment� Strongrelationshipswith customers� Partnershipswith suppliers� Respect fromcompetitors

� Financialperformance ofthe business� Marketposition

� Best possiblereturn oninvestment� Consultationswith community

Boardreputation

Collectivereputation

Individualreputation

Important toinvestors

Individualreputation(reputationof chairman)

Internalreputation

Important toinvestors

“Reputationof pushingboundaries”

Major factors

TransparencyHonestyLeadershipIntegrityStrong code ofethicsProfessionalismCommitment

OpennessFairnessConsistencyTrust

IndividualexpertiseHigh publicprofileCommunitylinks

Examples

“We’ve always had a verygood reputation with theinvestors in that we areopen. We tend to alwaysdeliver on ourcommitments andpromises and generallyhave a very strongsupport from theindustry”

“[The company’sreputation] I [CEO] thinkis seen more as how amanagement hasperformed, rather thanhow the board hasgoverned.”

“I [director] suspect that[some business partners]would probably notregard us as terribly nicepeople.”

11

“Our company carries a bit of baggage fromthe previous owner. When I started, we had avery average sales team and the reason forthat was it wasn’t a business that would attractgood people because of the inconsistency andthe reputation it had.”

The board and management believe the companyhas significantly improved in the meantime and thatmost stakeholders perceive Sagittarius as a moreprofessional and reputable business. Similar toSouthern Star, its directors see multiple linksbetween the company’s reputation, its overallbusiness performance, and management. Boardreputation, which is more important to investorsthan other stakeholders, is linked to the individualreputations of directors, the chairman in particular.One director put a specific emphasis on buildingthe “internal” reputation of the board, or trustbetween the management and the board. In a stageof transition, the board should be leading thecompany, but at the same time it should not bedealing outside its expected boundaries.

The directors and management of Acrux perceivetheir company’s reputation in different lights. For

the majority-owner directors, reputation isdependent on the financial outcomes. Therefore,the shareholder value is the major factor by whichthe company’s and the board’s reputation isestimated. One of the directors explains:

“There’s a bunch of rules [in the relationshipswith other stakeholders] here and we’re goingto play the game as hard as we can within therules. It’s not a case of that’s what we might beable to do, or could do … it’s that’s what weshould do because we’re managing the asseton behalf of our shareholders and ourshareholders deserve the best possible returnwe can get out of it.”

This attitude, which arises from the company’smonopolistic position, enables it to exercise variouspower games that produce conflicting situationswith other stakeholders. As a consequence, thestakeholders might perceive the company’sreputation in a less positive light.

As Acrux operates in the transport infrastructuresector, both groups of directors emphasise theimportance of the company’s reputation in thecommunity. They both perceive the company as “afairly good corporate citizen”, highlighting theirregular consultations with the community regardingvarious business developments and the companyinvestments in several community projects.

DISCUSSION

hese three cases illustrate three different patternsof relationships between the board and the

management team.

The pattern of relationships in Southern Starreflects collaboration between directors andmanagers. The board and the executive managementare functioning as a team, as a cohesive group. Everyissue is well studied and discussed, and conflict isacceptable behaviour. There are no dominant

players at board meetings and the board takes aninteractive approach in strategy making (Oliver,2000) working closely with management in variousstages of the strategy process. But the final decisionresides with the board. The board has developedstrong links with all stakeholders, customers inparticular, and the company’s reputation isembedded in these intensive external relationshipsand internal development of trust and consistencyat management and board levels. This is themonitoring perspective of the corporate governance,where clear boundaries exist between the board’sand management’s responsibilities. But teamwork,collaboration of multiple stakeholders, and path-dependent development of the company make thismonitoring a more sophisticated and multifacetedapproach that is far from a classical monitoring,controlling and measuring performance perspective.

Several contextual factors support this patternof corporate governance. First, the companyoperates in a mature and capital-intensive industry.It has a major position in the market and isfinancially successful. Second, historically thecompany has undergone stable development andgrowth without any transformational changes. It hasgrown mostly internally by developing relatedbusinesses. Southern Star has made recent largeacquisitions within the same industry. Third, overallstaff turnover is very low and, in terms ofmanagement development, Southern Star pursuesa tradition of internal promotion. Among seniormanagement, the CEO and a general manager ofthe largest division have been with the companyfor more than 30 years.

Sagittarius is a company in transition and itspattern of corporate governance reflects theintensive involvement of the chairman in strategicprocesses and even various management issues. Thechairman is the most knowledgeable person on the

T

�

U N I V E R S I T Y O F A U C K L A N D Business Review

V o l u m e 6 N u m b e r 1 2 0 0 4

12

Collaboration of multiple stakeholders makes the monitoring perspective

a more sophisticated and multifaceted approach that is far from

classical monitoring, controlling and measuring performance perspective

board and pursues a proactive approach (Oliver,2000) in strategy and business development. Theother board members, on the other hand, considertheir function in a traditional manner, ratifyingmanagement plans and acting as auditors of pastperformance. Their involvement is rather reactivethan active. The relationship between Sagittarius’chairman and management team can be describedas mentoring. The chairman has a role of coach,guiding management through the company’stransformation. The company has been undergoingchange, trying to rebuild its external reputation, withthe business community in particular, and its internalreputation, by building the confidence of the boardin its management. Respect and trust between boardand management are grounded in the chairman’sexpertise. This pattern of corporate governance issupported by specific contextual factors. First, theownership structure of the company suggests sucha type of governance relationship. The company isa private company and the directors own a majorityof equity. Among them, the chairman is the largestshareholder. Second, the chairman’s high reputationin the industry and business community haspredetermined his roles with management and therest of the board. The other board members expectthe chairman to be highly involved with thecompany and the management appreciate the valuehe adds to their efforts. Third, transitional changesrequire the board to provide more direction andguidelines and to perform like top-level strategists.

Acrux is a company whose pattern of corporategovernance reflects the conflicting interests of itstwo different shareholders. Majority-ownerdirectors play a dominant role in various governingissues. They pursue a clear goal of increasing theshareholding value for their investor. Minority-owner representatives, on the other hand, are moreconcerned with the wider stakeholders’ needs, butdo not have enough formal power to realise theirobjectives in full. Majority-owner directors followa proactive approach (Oliver, 2000) in strategydevelopment trying to be involved in all externaland internal processes. They constantly challengethe management by pushing the boundaries of the

company’s expected performance. At the same time,they maintain superficial, but respectfulrelationships with the minority owner, knowing thatthis party might harm their interests throughinformal (political) means outside the company.Although, on the surface, this corporate governancetriangle seems to function satisfactorily, underneathare some substantive and unresolved issues. First,there is a lack of open communication andconstructive discussion between the directors andexecutive management. Second, there is anasymmetry of information and knowledge betweenthe two groups of directors. Third, due to thephysical isolation of the chairman, there is a lack ofleadership and real collaboration in the boardroom.

RECOMMENDATIONS

he practical insights arising from this studyspan a variety of core areas and emerge from

examining the differences between the casespresented here and correlating these with otherpublished studies (e.g., Carter and Lorsch, 2004;Lorsch and MacIver, 1989; Conger, Lawler andFinegold, 2001; Westphal, 1999). We divide theminto process issues (what the board could dointernally to become more competent as a board)and content issues (what the board could do in itsinteraction with management and its representationof various stakeholders).

Process issues

The major aspect to improving governance istesting and building trust at various levels – primarilytrust in management and in each other, but alsoencompassing trust in commitment to the company,trust in competency to advise, trust in caring aboutthe welfare of the company, as well as management.While these aspects may seem obvious, many boardsare ineffective because of a lack of trust of variouskinds. Some board members do not trust the topmanagement and some managers may not trust thatthe board has the best interests of the managers, andthe company, at heart. Boards that are better atmonitoring also seem to have a trust-basedrelationship with managers. As a result, the formerare more comfortable providing honest feedback, and

T

Some board members do not trust the top management and

some managers may not trust that the board has the best

interests of the managers, and the company, at heart

13

the latter are less defensive about any negativefeedback and do not impute any ulterior motive. Inour study, it was clear that Southern Star had thistrust-based relationship, which had a beneficial effecton governance, whereas Acrux did not have thisrelationship, which in turn inhibited governance.

We intentionally emphasise the importance of thewhole management team being considered in thedevelopment of trusting and open relationships ingovernance practice of modern corporations. Theboard should be able to communicate with all top-level managers, not only the CEO. Acrux providesa good example of lack of communication (andtrust) between executive management and the board.The role of CEO is ultimately important in enablingand nurturing these communications. Managers’presence at board meetings and their involvementin reporting and discussing various issues with boardmembers encourage trust development and increasethe credibility of the directors. The board shouldperiodically revisit this issue internally and with eachboard member, and identify impediments todeveloping trust. This may also help in identifyinginactive board members, who may be free-ridingon the contributions of other members.

The two aspects that help in trust developmentare board involvement and board knowledge.Boards need to ensure the involvement of all boardmembers internally. This is critical to build acollaborative team rather than pockets ofindividuals. Involvement could be both in andoutside the boardroom, as in meeting key customers.Without it, boards are likely to become fragmentedand unproductive. A very important part of thisinvolvement is the visibility of the board to variousstakeholders, including employee groups, in avariety of formal and informal settings. At SouthernStar, for example, all directors recognise the valueof their visibility to various stakeholders and invest

significant effort in responding to the company’sexpectations. On the other hand, inactivity in theboardroom or unbalanced involvement is clearlyexemplified in the case of Sagittarius, where thechairman is the only board member actively involvedin the company’s affairs.

In addition, board members must beknowledgeable about their corporation and itscontext. The board needs to develop a conceptualunderstanding of core competencies of thecorporation (including its core technologies) andcomprehend how these competencies translate intocorporate strategies, as well as how strategies deliverfinancial outcomes. In other words, the board’sknowledge must have as much of a conceptual basisas an operational one. Thus, at the process level,boards must focus on knowledge diffusion,assimilation and reproduction systems. Governinga corporation is an essentially cerebral activity andthese knowledge systems should be used to developa common understanding of the value-adding engineof the corporation. This would lead to an engagedand collaborative board and a better basis formonitoring in the board. Of course, boards musthave multiple knowledge bases, incorporating bothinternal and external alternate sources ofinformation. But our point is that a commitment todeveloping involvement and knowledge systemswould spur sustainable long-term initiatives at theboard level, suited to their specific context.

Finally, to close the loop on the governanceprocess, an annual or bi-annual performanceappraisal of board members – a peer and externalreview – is critical. It needs to be pointed outthat only one firm in our sample (Southern Star)has a formal performance appraisal of its boardmembers. We believe a formal performanceappraisal sensitises the need for accountabilityof individual board members.

Governing a corporation is an essentially cerebral activity and these

knowledge systems should be used to develop a common

understanding of the value-adding engine of the corporation

�

U N I V E R S I T Y O F A U C K L A N D Business Review

V o l u m e 6 N u m b e r 1 2 0 0 4

14

Content issues

It is vital that the board must develop anoverarching goal for governance. This goal mustoutline the approach the board will adopt towardthe corporation as an entity, its assets, as well as itstop managers. This goal must be developed by theboard on its own, without involvement of the topmanagement – although once developed, the goal maybe shared with top management. The goal needs tocover at least four key areas: (1) the boundariesbetween governance, board responsibility andmanagement representation of the company tostakeholders; (2) a stance toward monitoring topmanagement, including succession plans; (3)education about the corporation’s mission, vision,values and competencies; and (4) delivery of theboard’s unique resources and competencies to thecorporation.

The process of developing an overarching goalserves to bring the board together, as well asfamiliarising board members with each other’s skills.Differences among board members (especially whenthey belong to different owner or stakeholder groups)could be ironed out in the process. Ultimately, boardsmust serve the corporation for which they areconstituted, rather than represent the individualconstituencies that members represent. In our study,Acrux provides an example of a split board, wheretwo groups of directors guard interests of theirrespective shareholders, very often undermining theinterests of the company.

Boards play a critical role when they take ultimateresponsibility in developing the “big picture”. Thisis the natural outcome of the knowledgemanagement process outlined earlier. Boards shoulddevelop alternative visions for the future and thecorporation’s role/place in each of those scenarios.None of the three companies from our sampleexemplifies a full and critical commitment of boardmembers in designing the company’s future.Although all three boards have strategic annualretreats where directors and executive managementdiscuss various strategic issues, their respective CEOsdo not believe their boards are sufficiently involvedin developing and establishing the big picture.

CONCLUSION

he dominant theme emerging from our studyof corporate governance in three companies in

traditional industries is the importance of a trust-based relationship between management and theboard, based on the board members’ knowledge ofthe firm and its context, and their involvement inthe process of governance. This relationship helpsthe board do a better job of monitoring topmanagement, protecting stakeholder interests and,where required, offer advice and other resources.This is evident from the contrast between the threecases presented here. Where both the CEO and thechairman expressed a high degree of satisfactionwith their relationship in terms of knowledge andinvolvement, the monitoring function was wellserved. Where this did not happen, the resultingmismatch and friction compromised the monitoringfunction. As shown, internal “education” ofdirectors, their commitment to learn and theirregular exposure to various stakeholders improvethe process of knowledge acquisition, lessen thecompetence gaps and promote trust buildingbetween directors and management.

The second major insight emerging from thecontrast between the cases presented is the need forthe board to work as a group. This need may seemobvious, but achieving it may require a lot of effort.Where only some members are knowledgeableabout the issues, their involvement and participationsuffer, compromising the monitoring function.Collaboration within the boardroom and thedevelopment of close working relationships betweenthe CEO and the chairman increase the board’seffectiveness and create synergy. The board shouldbe able to serve as a sounding board with bestsolutions emerging from active debate among allboard members. The active participation of only apart of the board may generate “group-think”behaviour. This creates a false impression ofinformed consensus, when it is actually a reflectionof passive agreement. This does not serve theinvestors and management well.

The third major insight refers to the increasingneed for a board’s greater involvement in long-term

T

15

Collaboration within the boardroom and the development of close

working relationships between the CEO and the chairman

increase the board’s effectiveness and create synergy

REFERENCES

Carter, C.B., & Lorsch, J.W. (2004). Back to the drawing board: Designingcorporate boards for a complex world. Boston: Harvard Business School Press.

Clarke, T., & Clegg, S. (1998). Changing paradigms: The transformation ofmanagement knowledge for the 21st century. London: Harper Collins Business.

Conger, J.A., Lawler, E.E., III, & Finegold, D.L. (2001). Corporate boards:Strategies for adding value at the top. San Francisco: Jossey-Bass.

Fama, E., & Jensen, M.C. (1983). Separation of ownership and control. Journalof Law and Economics, 26: 301-326.

Farrar, J.H. (2001). Corporate governance in Australia and New Zealand.Melbourne: Oxford University Press.

Jensen, M.C., & Meckling, W. (1976). Theory of the firm: Managerial behavior,agency costs and ownership structure. Journal of Financial Economics, 3: 305-360.

Johnson, J.L., Daily, C.M, & Ellstrand, A.E. (1996). Boards of Directors: A reviewand research agenda. Journal of Management, 22/3: 409-438.

Knepper, W.E., & Bailey, D.A. (1998). Liability of corporate officers and directors(6th ed.). Charlottesville, VA: Lexis Publishing.

Goel, S., & Erakovic, Lj. (2003). Monitoring versus mentoring: Role ambiguityand contextual tensions in the task of board of directors. Paper presented atCorporate Governance Workshop of European Academy of Managementmeeting, Milan.

Lorsch, J.W., & MacIver, E.A. (1989). Pawns or potentates: The reality ofAmerica’s corporate boards. Boston: Harvard Business School Press.

Oliver, R.W. (2000). The Board’s role: Driver’s seat or rubber stamp? The Journalof Business Strategy, 21: 7-9.

Shen, W. (2003). The dynamics of the CEO-Board relationship: An evolutionaryperspective. Academy of Management Review, 28/3: 466-476.

Stiles, P., & Taylor, B. (2001). Boards at work: How directors view their roles andresponsibilities. Oxford: Oxford University Press.

Sundaramurthy, C., & Lewis, M. (2003). Control and collaboration: Paradoxes ofgovernance. Academy of Management Review, 28/3: 397-415.

Institute of Directors in New Zealand (1999). Code of proper practice for directors.Retrieved March 10, 2003, from http://www.iod.org.nz/publications.html

Westphal, J.D. (1999). Collaboration in the boardroom: Behavioral andperformance consequences of CEO-Board social ties. Academy of ManagementJournal, 42: 7-25.

strategy making. Our research findings andrecommendations advocate a critical role for theboard in designing the company’s future. Bothshareholders and management expect the board tobe active in developing ideas, refining possiblesolutions, deciding the final strategy and reviewingthe process of strategy implementation. Finally, ourresearch shows that directors’ reputations can beconsidered as an additional factor in analysingcontemporary governance practice. Here theindividual directors’ reputations (embedded inpersonal integrity, leadership, commitment andindividual expertise) and the collective reputationof the company (built on strong financialperformance, market position and respectfulcustomer service) can contribute to the developmentof more effective relationships between the boardand management on the one hand, and the boardand the company’s investors on the other.

The findings reported here are part of a largerstudy on corporate governance in a wide variety ofindustries and ownership variations in New Zealand.Also, a large number of not-for-profit organisations(e.g., NGOs and trusts) implement a similar modelof governance as corporate entities in New Zealand.Our conclusion can also be applied for their boardsof directors. For the specific recommendations,however, further study needs to be done on theseorganisations’ specific contexts. While we are quiteoptimistic about the overall quality of governancein New Zealand in general, in this paper we proposesome steps to improve the boards as governancebodies, with the implicit co-operation ofmanagement. We make one overriding presumptionin this effort, however: that both boards and

Ljiljana ErakovicLECTURER

Department of Management and Employment Relations

The University of Auckland

Email: [email protected]

Sanjay GoelASSISTANT PROFESSOR

Department of Management Studies

Labovitz School of Business and Economics

University of Minnesota, Duluth

Email: [email protected]

ACKNOWLEDGEMENT

Sanjay Goel gratefully acknowledges the research assistance andhospitality provided by The University of Auckland Business Schoolin connection with the Corporate Governance Research Project.

managers are really interested in better governanceof the corporation. Because of their unique,relatively rarefied perch in the corporate hierarchy,no real change can occur if boards and managersdo not commit to a need for a change.

U N I V E R S I T Y O F A U C K L A N D Business Review

V o l u m e 6 N u m b e r 1 2 0 0 4

16