Embed Size (px)

Citation preview

Building Bridges to Innovation

CONFIDENTIAL AND PROPRIETARY

Any use of this material without specific permission of McKinsey & Company

is strictly prohibited

Shanghai, November 13-14, 2018

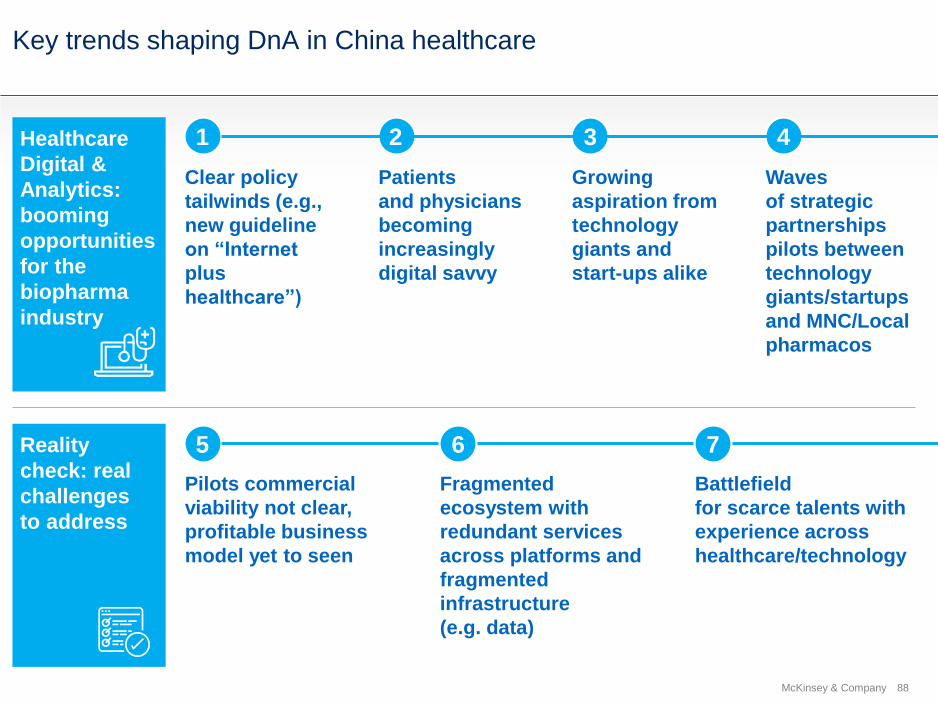

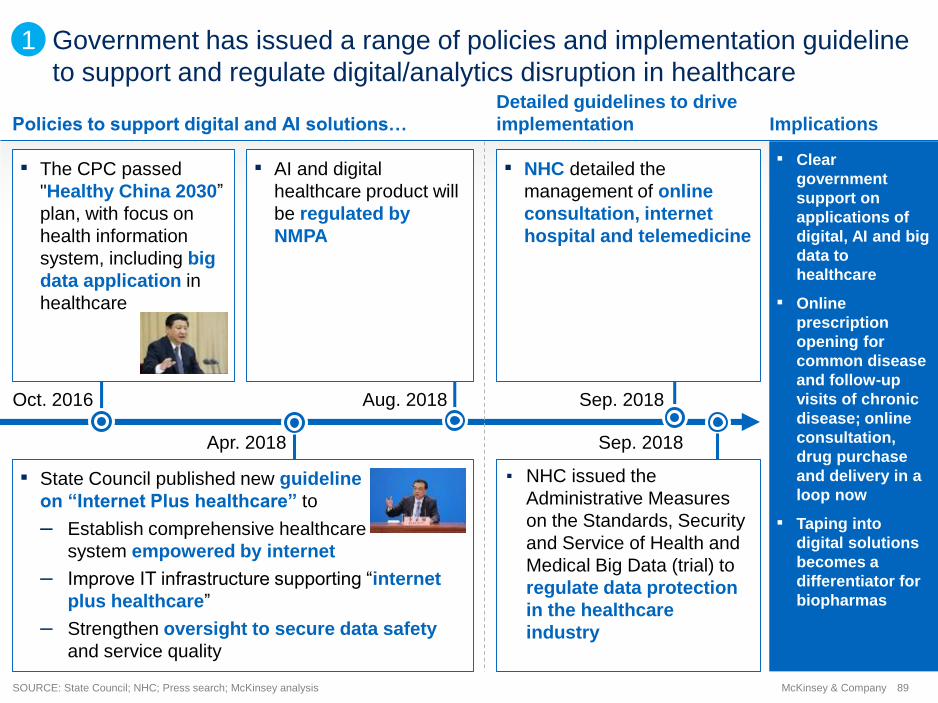

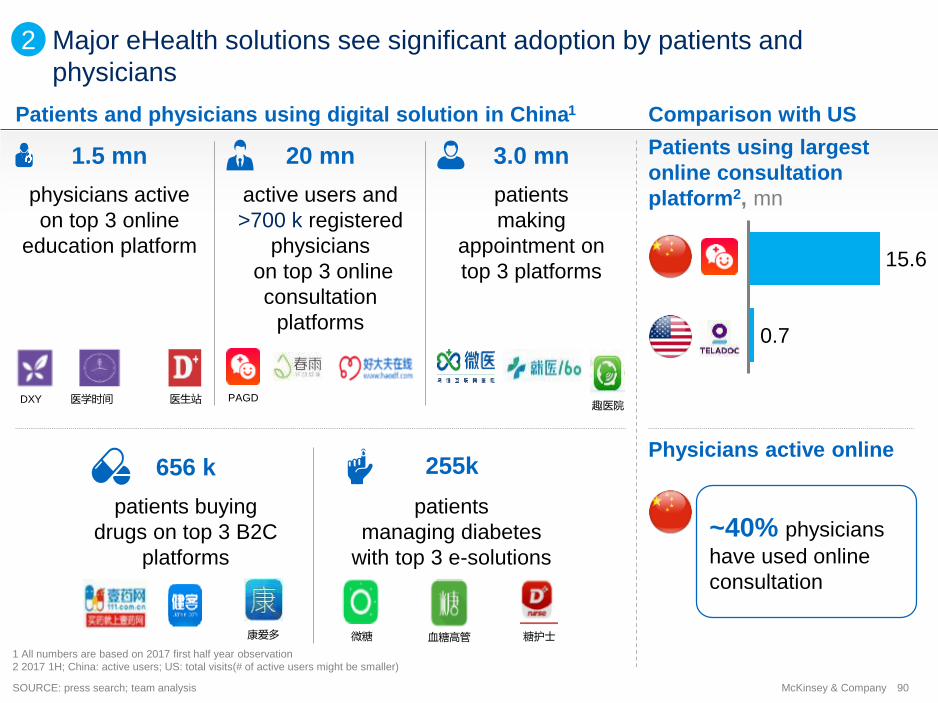

2McKinsey & Company

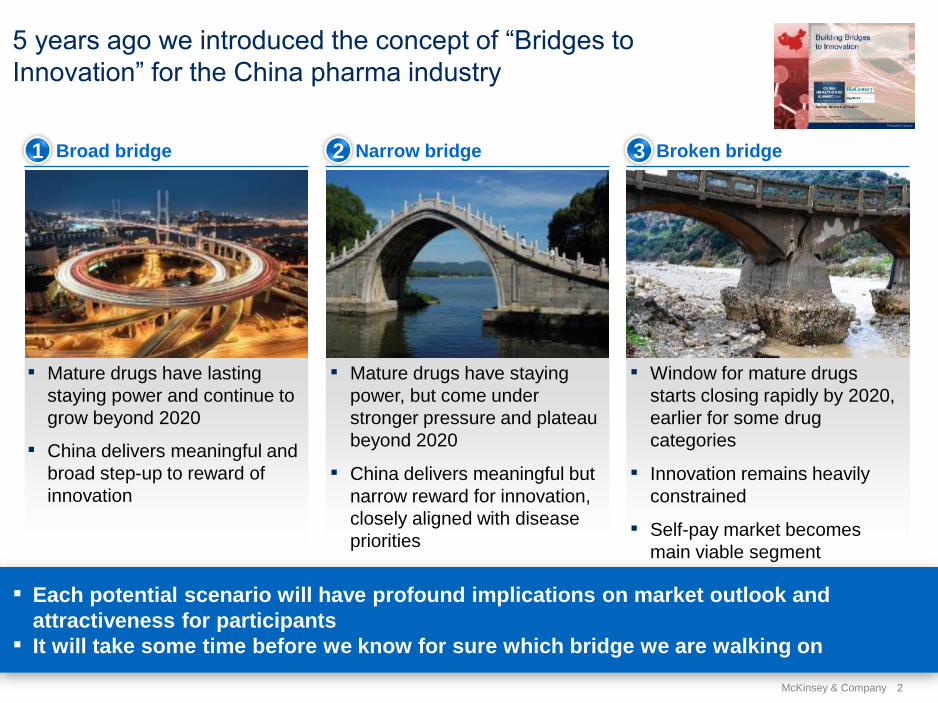

5 years ago we introduced the concept of “Bridges to

Innovation” for the China pharma industry

Broken bridgeNarrow bridgeBroad bridge1 2 3

▪ Mature drugs have lasting

staying power and continue to

grow beyond 2020

▪ China delivers meaningful and

broad step-up to reward of

innovation

▪ Mature drugs have staying

power, but come under

stronger pressure and plateau

beyond 2020

▪ China delivers meaningful but

narrow reward for innovation,

closely aligned with disease

priorities

▪ Window for mature drugs

starts closing rapidly by 2020,

earlier for some drug

categories

▪ Innovation remains heavily

constrained

▪ Self-pay market becomes

main viable segment

▪ Each potential scenario will have profound implications on market outlook and

attractiveness for participants

▪ It will take some time before we know for sure which bridge we are walking on

3McKinsey & Company

As of 2018, we are increasingly confident to say that we are progressing

on the ”narrow bridge”

Broken bridgeNarrow bridgeBroad bridge1 2 3

Uptake of innovation starting to

accelerate and showing signs of

pivot towards “broad bridge”

Mature products come under much

stronger pressure in the coming

few years - “reckoning time”?

4McKinsey & Company

4 key

questions to

explore …

Impact of Digital

and Analytics?

Momentum of the

innovation drive?

Speed of improvement

in market access?

Macro market

evolution? 01

02

03

04

5McKinsey & Company

4 key

questions to

explore …

Impact of Digital

and Analytics?

Momentum of the

innovation drive?

Speed of improvement

in market access?

Macro market

evolution? 01

02

03

04

6McKinsey & Company

2018 in the mirror

2018 in the mirror…and view from the top 01

View from the top: GMs outlook for the future

7McKinsey & Company

2018 in the mirror – another year of “China speed” development

NMPA reform stays the course…for now

Broadening of access accelerates

HKEX embraces Biotech

China innovation reaches global stage

Threat to mature brands reaches tipping point

Trade tensions begin…

War for talents at boiling point

China takes center stage for several large MNCs

21 3 4

5 6 7 8

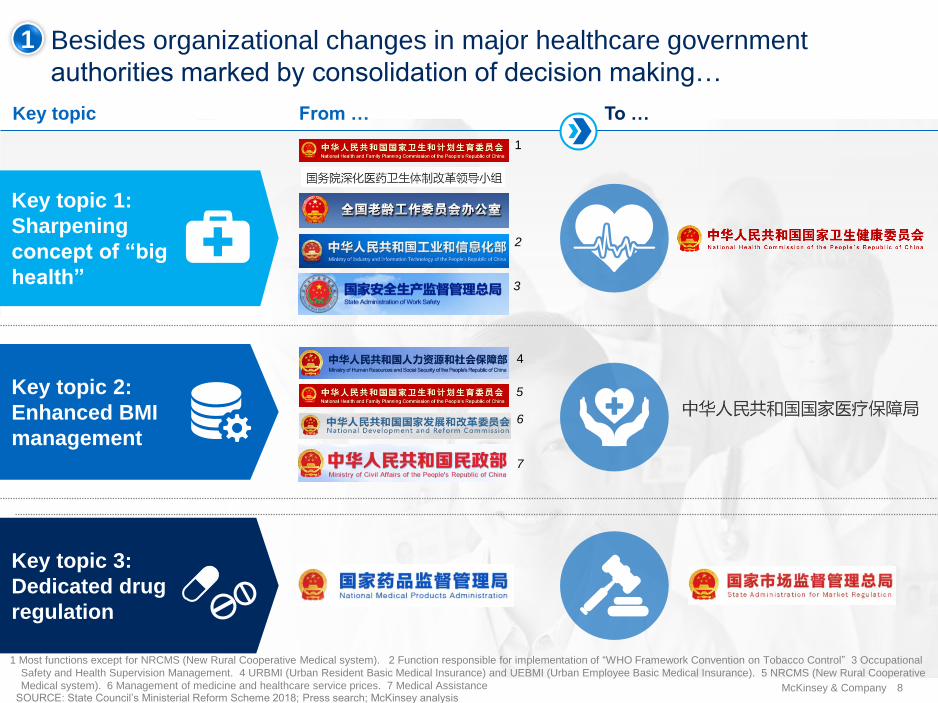

8McKinsey & CompanySOURCE: State Council’s Ministerial Reform Scheme 2018; Press search; McKinsey analysis

Key topic 3:

Dedicated drug

regulation

1

From … To …Key topic

Key topic 1:

Sharpening

concept of “big

health”

Key topic 2:

Enhanced BMI

management

Besides organizational changes in major healthcare government

authorities marked by consolidation of decision making…

1

2

3

4

5

6

1 Most functions except for NRCMS (New Rural Cooperative Medical system). 2 Function responsible for implementation of “WHO Framework Convention on Tobacco Control” 3 Occupational

Safety and Health Supervision Management. 4 URBMI (Urban Resident Basic Medical Insurance) and UEBMI (Urban Employee Basic Medical Insurance). 5 NRCMS (New Rural Cooperative

Medical system). 6 Management of medicine and healthcare service prices. 7 Medical Assistance

7

9McKinsey & Company

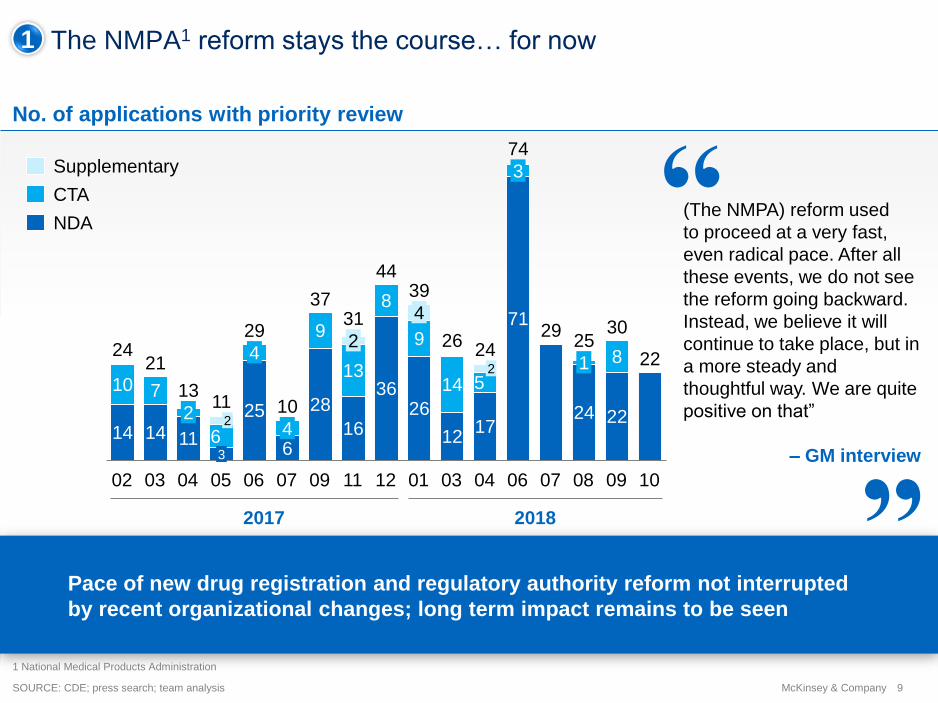

The NMPA1 reform stays the course… for now

14 14 11

25

6

28

16

3626

1217

7129

24 22

22

10 7

6

9

13

8

9

14 5

8

11

02

30

07

2424

03

74

04 05 06 01

4

1109 060412 03 07 08 09

3

10

29

21

37

1310

26

31

4439

25

4

2

1

2

4

3

2

2

No. of applications with priority review

2017 2018

1

Pace of new drug registration and regulatory authority reform not interrupted

by recent organizational changes; long term impact remains to be seen

(The NMPA) reform used

to proceed at a very fast,

even radical pace. After all

these events, we do not see

the reform going backward.

Instead, we believe it will

continue to take place, but in

a more steady and

thoughtful way. We are quite

positive on that”

– GM interview

SOURCE: CDE; press search; team analysis

1 National Medical Products Administration

Supplementary

CTA

NDA

10McKinsey & Company

Broadening of Access accelerates2

Improved accessibility since 2017 through…

▪ Cancer drugs exempted from

import taxes starting in May

▪ Premier Li’s visit to Roche

▪ Movie “Dying to Live” triggered

nationwide discussion on access

to innovative drugs

▪ Essential Drug List

updated in October,

expanding from 520 to

685 molecules; with

high priced & non-

NRDL listed drugs

included for the first

time

EDL update

Push from

central

government

▪ 128 western drugs were

added to the NRDL

through direct listing

▪ 36 of 44 drugs

participating in national

negotiation got listed on

NRDL

▪ 17 oncology drugs

further added to NRDL

through negotiation in

Q3 2018

National drug

negotiation

11McKinsey & Company

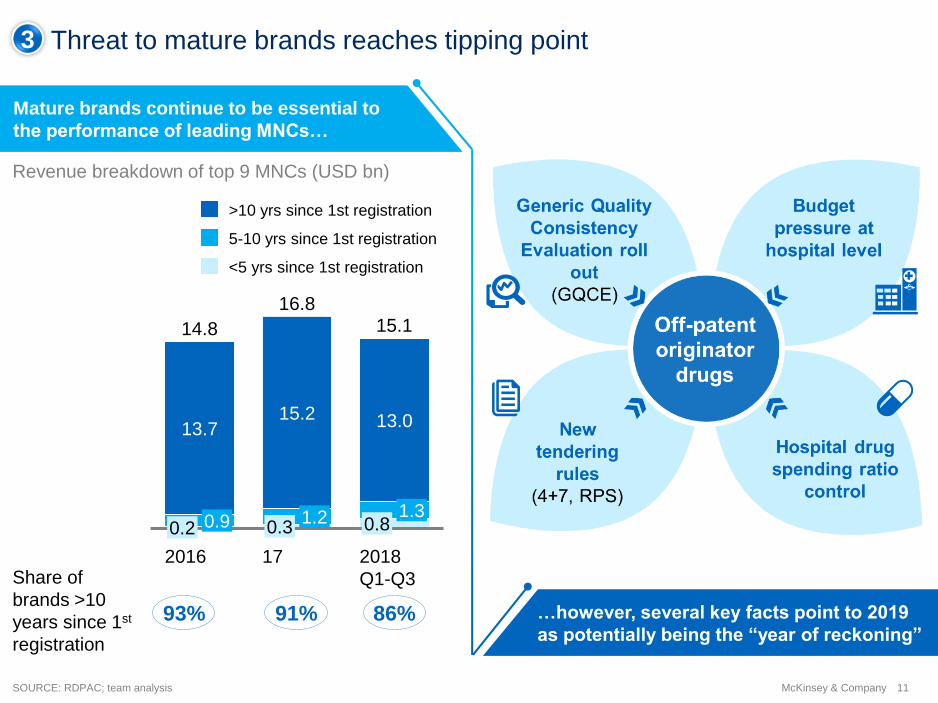

Threat to mature brands reaches tipping point3

Revenue breakdown of top 9 MNCs (USD bn)

SOURCE: RDPAC; team analysis

13.715.2 13.0

15.1

0.8

17

0.9

2016

0.21.2

0.31.3

2018

Q1-Q3

14.8

16.8

<5 yrs since 1st registration

>10 yrs since 1st registration

5-10 yrs since 1st registration

93% 91% 86%

Share of

brands >10

years since 1st

registration

…however, several key facts point to 2019

as potentially being the “year of reckoning”

Mature brands continue to be essential to

the performance of leading MNCs…

12McKinsey & Company

GQCE making strides in 2018, albeit with some challenges in

implementation roll-out

3

from leading local companies

>40 BE studies

Long way to go to complete “289 EDL”

by end of 2018

68 applications# of molecules out of the “289 EDL

products” under GQCE applications

18 approvals# of molecules out of the “289

EDL products” that passed GQCE

Local leaders emerging

~50 companiesconducting BE in selected molecules

(e.g., Amlodipine, Metformin)

Fierce competition for

selected molecules

SOURCE: GBI; press search; team analysis

AS OF OCT 31 2018

13McKinsey & Company

China takes center stage for several large MNCs

Leading MNCs restructure their organization with greater China centricity in mind

SOURCE: Annual reports; Press search, team analysis, expert interview

4

2019 – Building

‘China and

emerging market’

new BU

2017 – Promoted China

EVP, Leon Wang, to

oversee international

commercial business

from China

2017 – Relocated

Asia Development

Center from

Singapore to

Shanghai

2019 – Reorganizing into

three businesses with the

leadership team of

Established Medicines

business based in

China

2017 – Promoted

China GM XuDong

Yin to lead APMA

business

14McKinsey & Company

War for talents reaches boiling point – flow of key MNC talents towards

local biotechs under way

5

Min Liu

(Onc BU head)

Frank Jiang

(R&D head)

Kerry Blanchard

(R&D head)

William Liang

(Onc BU head)

Xiaobin Wu

(President)

Vivian Bian

(O&I BU head)

Zhi Hong

(SVP and head of

CoE for drug

discovery)

Joan Shen

(R&D head)

SOURCE: Annual reports; press search, team analysis

Transfer of talents from MNCs to Locals is also visible at mid level management, and will

particularly impact Development, Medical and Access functions

15McKinsey & Company

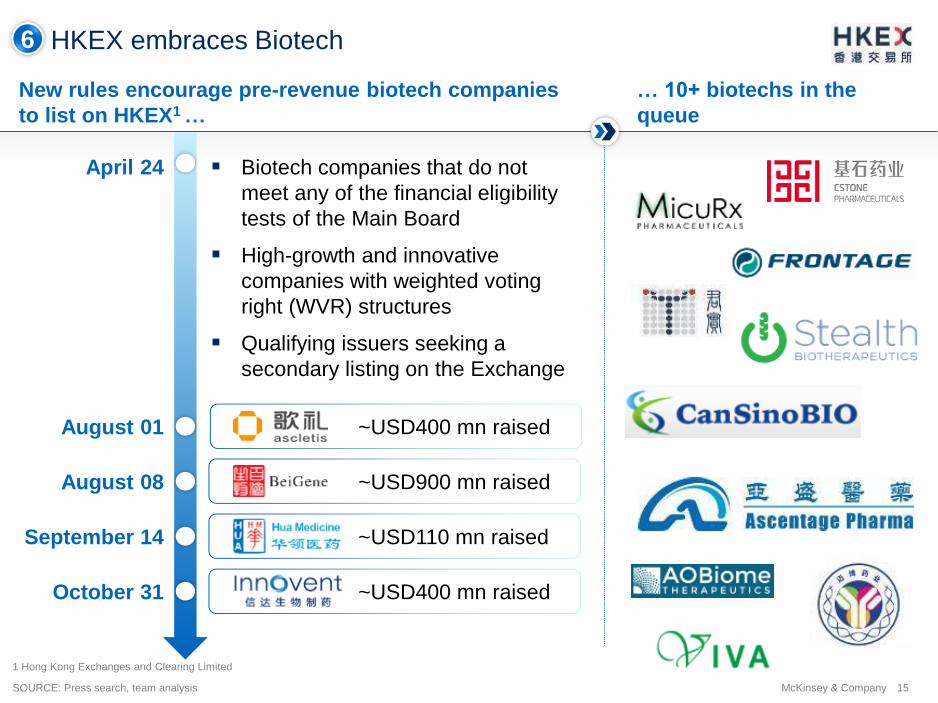

HKEX embraces Biotech

1 Hong Kong Exchanges and Clearing Limited

SOURCE: Press search, team analysis

New rules encourage pre-revenue biotech companies

to list on HKEX1 …

… 10+ biotechs in the

queue

April 24

August 01

~USD900 mn raised August 08

~USD110 mn raised September 14

6

▪ Biotech companies that do not

meet any of the financial eligibility

tests of the Main Board

▪ High-growth and innovative

companies with weighted voting

right (WVR) structures

▪ Qualifying issuers seeking a

secondary listing on the Exchange

October 31 ~USD400 mn raised

~USD400 mn raised

16McKinsey & Company

US-Sino trade tensions begin…

SOURCE: Ministry of Commerce of the People's Republic of China; office of United States Trade Representative; Press research

Ongoing US-Sino dispute involves more than USD200 billion worth of China and US

goods, which are subject to 5-25% additional tariff

V.S

US charge on China China charge on US

USD34 bn(25% tariff)

818 items incl.

medical products1

USD16 bn(25% tariff)

279 items

USD34 bn(25% tariff)

545 items

USD16 bn(25% tariff)

333 items

USD60 bn(5-10% tariff)

5,207 items

incl. medical

products

USD200 bn(from 10% to 25%

by the end of

2018)

Incl. illumination

products,

consumer goods

First

round

Second

round

Third

round

1 122 out of 1300 separate tariff lines involving biomedical products. 32 lines on medicinal chemicals, 38 on drugs or biological products, 52 on medical devices and related products

8

17McKinsey & Company

2018 in the mirror

2018 in the mirror…and view from the top 01

View from the top: GMs outlook for the future

18McKinsey & Company

We interviewed and surveyed GMs of most leading MNCs in China

Companies interviewed Structured GM survey

19McKinsey & Company

5 key predictions for the next 3 years

Digitalization has yet to

fundamentally transform

industry; however, digital

touch points become an

essential pillar for customer

engagement

Talent war for biopharma companies is underway with continuing expansion of China’s pharma market and boom of innovation ecosystem

Companies, especially

MNCs, march toward

innovative assets driven

portfolio; however, aggressive

reimbursement negotiation

may erode value of innovation1 Off patent originator

GQCE and

reimbursement reform

exert pricing pressure

on OPO1 products,

creating more funding for

innovation and overall

shifting China toward a

developed market profile

Importance of China

market likely to remain

steady, driven by

growing innovative

business but offset by

pressure on mature

products

01 02

03 04 05

20McKinsey & Company

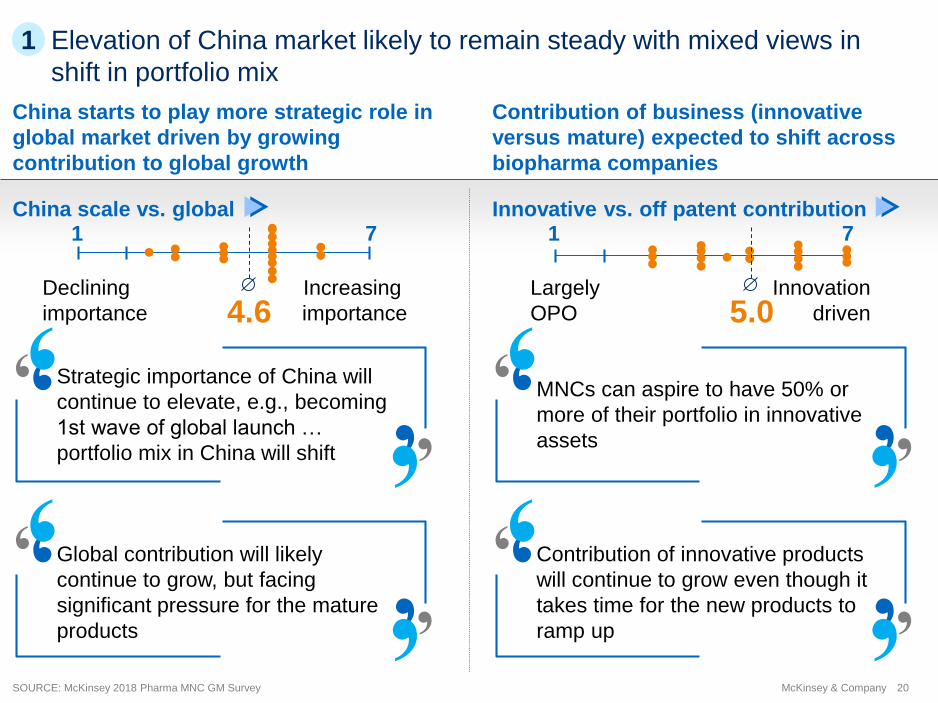

Elevation of China market likely to remain steady with mixed views in

shift in portfolio mix

Declining

importance

Increasing

importance

Largely

OPO

Innovation

driven

1

China starts to play more strategic role in

global market driven by growing

contribution to global growth

Contribution of business (innovative

versus mature) expected to shift across

biopharma companies

China scale vs. global Innovative vs. off patent contribution

Strategic importance of China will

continue to elevate, e.g., becoming

1st wave of global launch …

portfolio mix in China will shift

Global contribution will likely

continue to grow, but facing

significant pressure for the mature

products

MNCs can aspire to have 50% or

more of their portfolio in innovative

assets

Contribution of innovative products

will continue to grow even though it

takes time for the new products to

ramp up

1 7

4.6

1 7

5.0

SOURCE: McKinsey 2018 Pharma MNC GM Survey

21McKinsey & Company

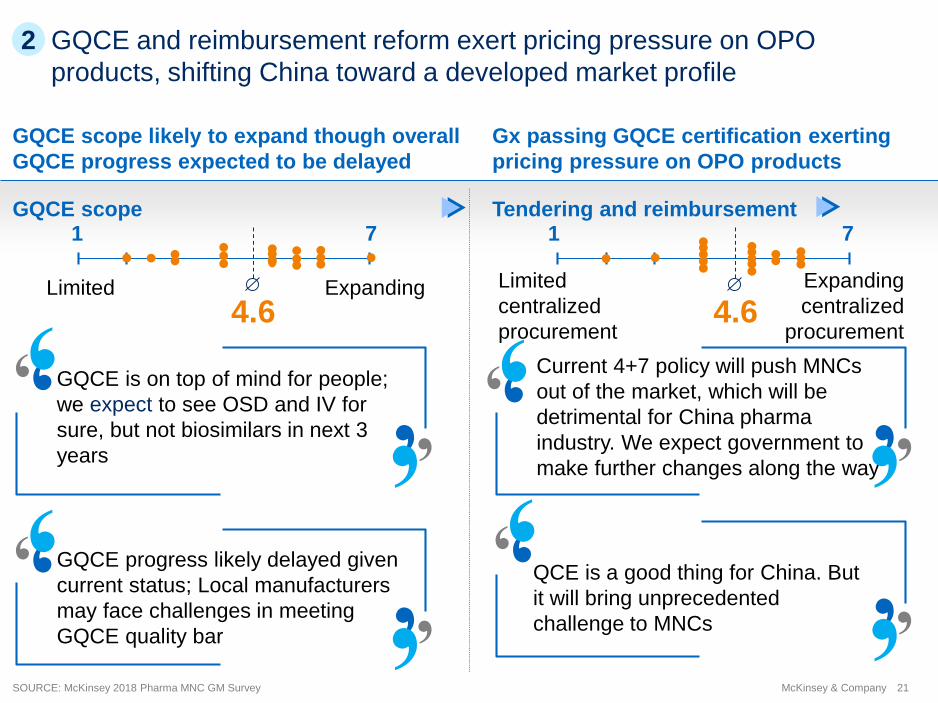

GQCE and reimbursement reform exert pricing pressure on OPO

products, shifting China toward a developed market profile

ExpandingLimited Expanding

centralized

procurement

Limited

centralized

procurement

2

GQCE scope likely to expand though overall

GQCE progress expected to be delayed

Gx passing GQCE certification exerting

pricing pressure on OPO products

GQCE scope Tendering and reimbursement

GQCE is on top of mind for people;

we expect to see OSD and IV for

sure, but not biosimilars in next 3

years

Current 4+7 policy will push MNCs

out of the market, which will be

detrimental for China pharma

industry. We expect government to

make further changes along the way

QCE is a good thing for China. But

it will bring unprecedented

challenge to MNCs

GQCE progress likely delayed given

current status; Local manufacturers

may face challenges in meeting

GQCE quality bar

1 7

4.6

1 7

4.6

SOURCE: McKinsey 2018 Pharma MNC GM Survey

22McKinsey & Company

Companies marching toward innovative assets focused portfolio but

value of innovation may diminish with aggressive reimbursement

negotiation

BroadeningNarrowing DynamicInfrequent

3

Speed of innovation continues to

increases due to sustained NMPA reform

Access will continue to improve, though

shadowed by increasing price pressure

It’s the right time for innovative drugs

to enter China with improvement and

globalization of registration process

and patent protection

Access will improve, especially for

innovative drugs, but price pressure will

also increase with reimbursement

negotiation. Given China’s scale in the

global market, China prices will also

have global implications

Innovation could be commoditized due

to reimbursement price cut. Price cut

does not have a good basis now, but

we have Taiwan, Korea as reference

countries. In a few years, China will be

wave 1 launch country without

reference price

Innovation will remain as the priority

for NMPA reform, and we expect

broadening of reform area to further

support innovation

Areas of focus for future NMPA reform NRDL update 1 7

4.9

1 7

5.0

SOURCE: McKinsey 2018 Pharma MNC GM Survey

23McKinsey & Company

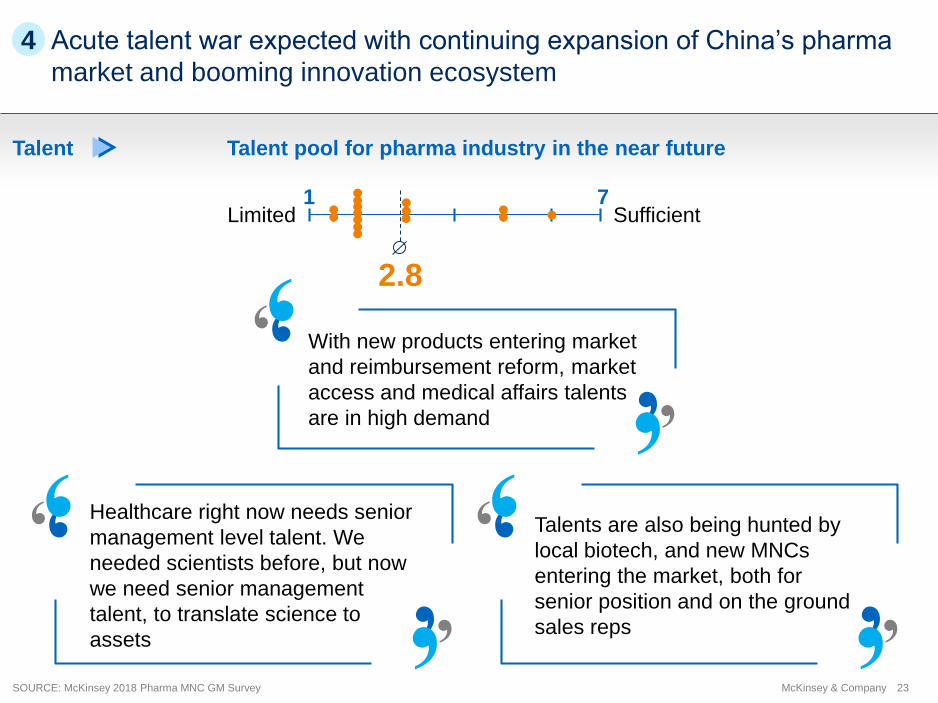

Acute talent war expected with continuing expansion of China’s pharma

market and booming innovation ecosystem

Limited Sufficient

4

Talent

Healthcare right now needs senior

management level talent. We

needed scientists before, but now

we need senior management

talent, to translate science to

assets

Talents are also being hunted by

local biotech, and new MNCs

entering the market, both for

senior position and on the ground

sales reps

With new products entering market

and reimbursement reform, market

access and medical affairs talents

are in high demand

Talent pool for pharma industry in the near future

1 7

2.8

SOURCE: McKinsey 2018 Pharma MNC GM Survey

24McKinsey & Company

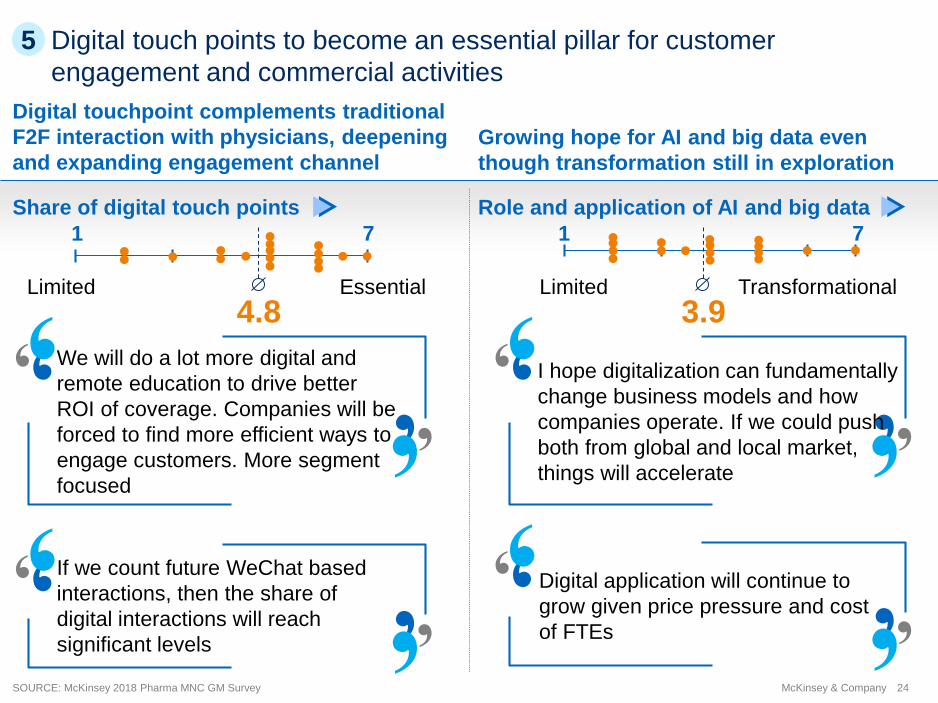

Digital touch points to become an essential pillar for customer

engagement and commercial activities

Limited Essential Limited Transformational

5

Digital touchpoint complements traditional

F2F interaction with physicians, deepening

and expanding engagement channel

Growing hope for AI and big data even

though transformation still in exploration

Share of digital touch points Role and application of AI and big data

We will do a lot more digital and

remote education to drive better

ROI of coverage. Companies will be

forced to find more efficient ways to

engage customers. More segment

focused

I hope digitalization can fundamentally

change business models and how

companies operate. If we could push

both from global and local market,

things will accelerate

Digital application will continue to

grow given price pressure and cost

of FTEs

If we count future WeChat based

interactions, then the share of

digital interactions will reach

significant levels

1 7 1 7

3.94.8

SOURCE: McKinsey 2018 Pharma MNC GM Survey

25McKinsey & Company

4 key

questions to

explore …

Impact of Digital

and Analytics?

Momentum of the

innovation drive?

Speed of improvement

in market access?

Macro market

evolution? 01

02

03

04

26McKinsey & Company

Momentum of China biopharma innovation – two topics

Momentum of

China biotech

Fresh view of China

biopharma innovation

ecosystem

27McKinsey & Company

Assess China innovation ecosystem along 5 dimensions

▪ Policy environment, Funding, Capability/infrastructure, Local

innovation output, Integration into global

▪ Calibrated against current U.S. levels (US = 8 out of 10

points)

Survey of 109 industry experts:

▪ 73% are CEOs/senior executives

▪ 63% with 15+ years of industry experiences

Approach: CDII survey in collaboration with

To gauge progress of China biopharma innovation ecosystem, we have

updated our China Drug Innovation Index (CDII)

▪ CDII was first initiated in 2015, followed by a second

edition in 2016

▪ 2018 is the 3rd edition, providing the latest view on China

biopharma innovation progressFresh and

holistic

assessment of

China

innovation

ecosystem

with

comparison to

2015 results

We also appreciate generous support from several industry

groups including SABPA, DIA, etc.

28McKinsey & Company

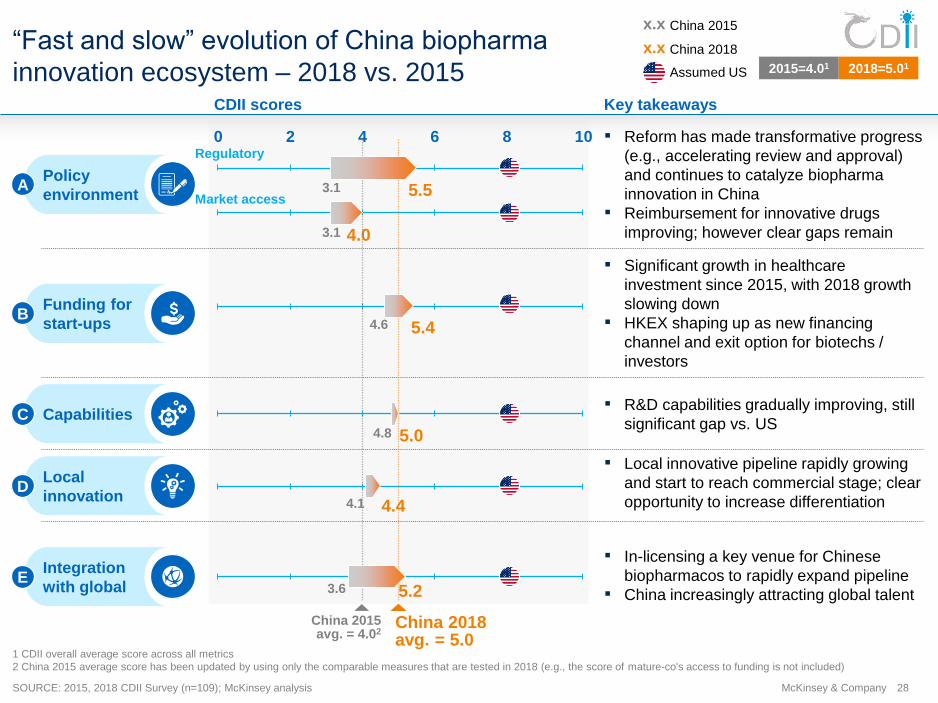

“Fast and slow” evolution of China biopharma

innovation ecosystem – 2018 vs. 2015

1 CDII overall average score across all metrics

2 China 2015 average score has been updated by using only the comparable measures that are tested in 2018 (e.g., the score of mature-co's access to funding is not included)

SOURCE: 2015, 2018 CDII Survey (n=109); McKinsey analysis

CDII scores

China 2018 avg. = 5.0

China 2015 avg. = 4.02

BFunding for

start-ups

EIntegration

with global

APolicy

environment

4.03.1

5.53.1

5.4

5.04.8

4.44.1

5.23.6

Market access

Regulatory

2015=4.01 2018=5.01

China 2015

China 2018

Assumed US

x.x

x.x

Key takeaways

▪ Significant growth in healthcare

investment since 2015, with 2018 growth

slowing down

▪ HKEX shaping up as new financing

channel and exit option for biotechs /

investors

C Capabilities ▪ R&D capabilities gradually improving, still

significant gap vs. US

DLocal

innovation

▪ Local innovative pipeline rapidly growing

and start to reach commercial stage; clear

opportunity to increase differentiation

▪ In-licensing a key venue for Chinese

biopharmacos to rapidly expand pipeline

▪ China increasingly attracting global talent

▪ Reform has made transformative progress

(e.g., accelerating review and approval)

and continues to catalyze biopharma

innovation in China

▪ Reimbursement for innovative drugs

improving; however clear gaps remain

0 102 4 6 8

4.6

29McKinsey & Company

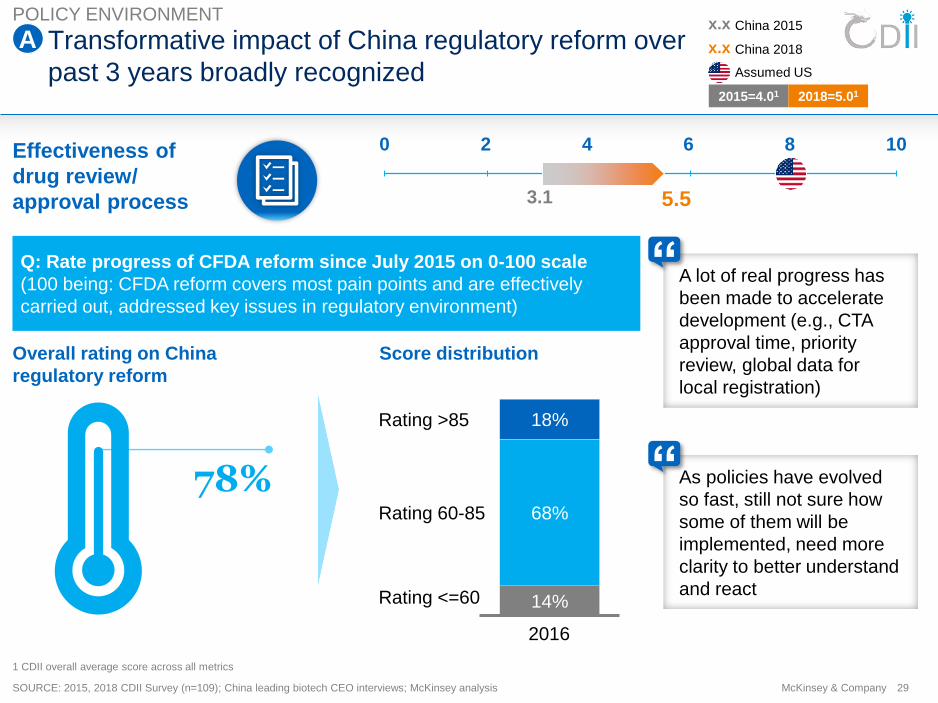

Transformative impact of China regulatory reform over

past 3 years broadly recognized

A

SOURCE: 2015, 2018 CDII Survey (n=109); China leading biotech CEO interviews; McKinsey analysis

Effectiveness of

drug review/

approval process

Overall rating on China

regulatory reform

Score distribution

14%

68%

18%

Rating 60-85

2016

Rating >85

Rating <=60

Q: Rate progress of CFDA reform since July 2015 on 0-100 scale

(100 being: CFDA reform covers most pain points and are effectively

carried out, addressed key issues in regulatory environment)

A lot of real progress has

been made to accelerate

development (e.g., CTA

approval time, priority

review, global data for

local registration)

As policies have evolved

so fast, still not sure how

some of them will be

implemented, need more

clarity to better understand

and react

“

3.1

0 102 4 6 8

5.5

China 2015

China 2018

Assumed US

x.x

x.x

“

78%

2015=4.01 2018=5.01

1 CDII overall average score across all metrics

POLICY ENVIRONMENT

30McKinsey & Company

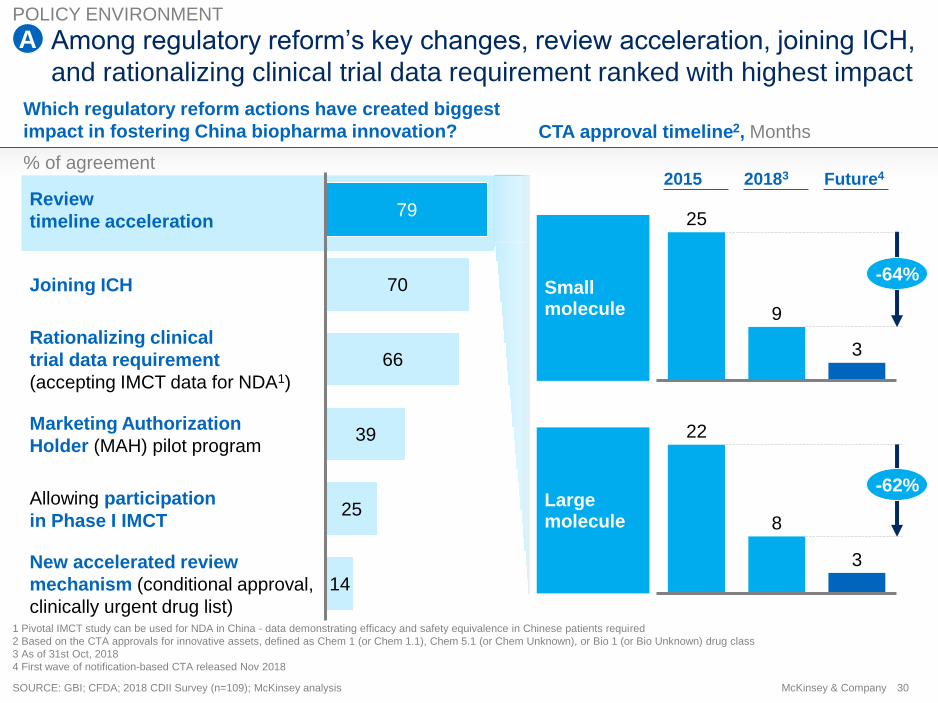

Among regulatory reform’s key changes, review acceleration, joining ICH,

and rationalizing clinical trial data requirement ranked with highest impact

79

70

66

39

25

14

Rationalizing clinical

trial data requirement

(accepting IMCT data for NDA1)

Review

timeline acceleration

Joining ICH

Allowing participation

in Phase I IMCT

Marketing Authorization

Holder (MAH) pilot program

New accelerated review

mechanism (conditional approval,

clinically urgent drug list)

Which regulatory reform actions have created biggest

impact in fostering China biopharma innovation?

SOURCE: GBI; CFDA; 2018 CDII Survey (n=109); McKinsey analysis

A

Small molecule

Large molecule

CTA approval timeline2, Months

2015 Future420183

22

8

3

-62%

25

9

3

-64%

1 Pivotal IMCT study can be used for NDA in China - data demonstrating efficacy and safety equivalence in Chinese patients required

2 Based on the CTA approvals for innovative assets, defined as Chem 1 (or Chem 1.1), Chem 5.1 (or Chem Unknown), or Bio 1 (or Bio Unknown) drug class

3 As of 31st Oct, 2018

4 First wave of notification-based CTA released Nov 2018

% of agreement

POLICY ENVIRONMENT

31McKinsey & Company

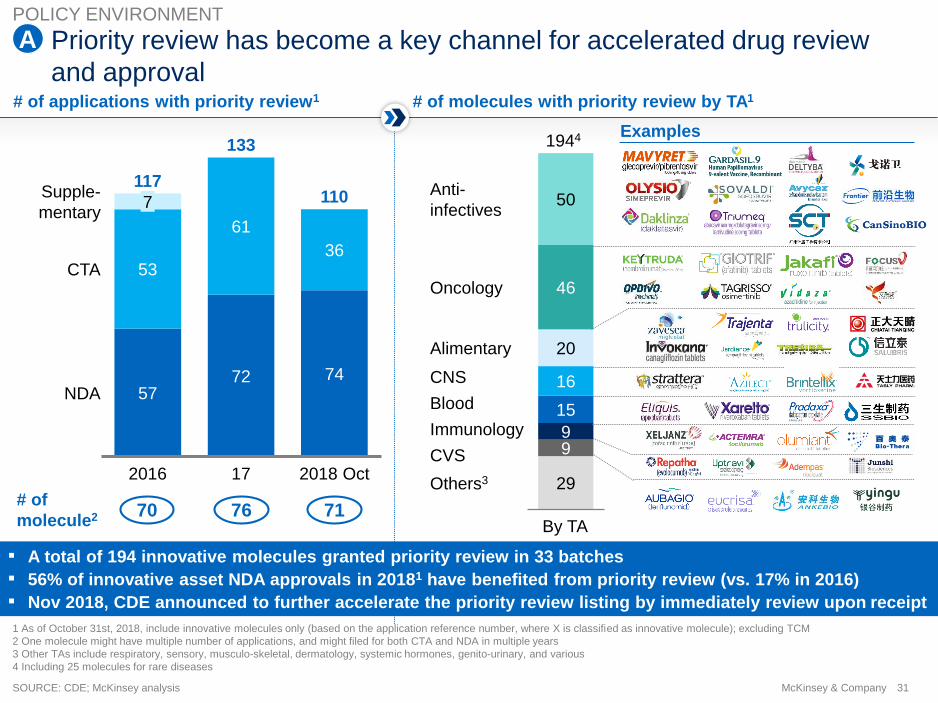

Priority review has become a key channel for accelerated drug review

and approval

1 As of October 31st, 2018, include innovative molecules only (based on the application reference number, where X is classified as innovative molecule); excluding TCM

2 One molecule might have multiple number of applications, and might filed for both CTA and NDA in multiple years

3 Other TAs include respiratory, sensory, musculo-skeletal, dermatology, systemic hormones, genito-urinary, and various

4 Including 25 molecules for rare diseases

SOURCE: CDE; McKinsey analysis

29

99

15

16

20

46

50

CVS

Immunology

Anti-

infectives

Alimentary

By TA

Oncology

CNS

Blood

Others3

1944

# of applications with priority review1 # of molecules with priority review by TA1

Examples

5772 74

53

61

36

7

2016

CTA

2018 Oct17

Supple-

mentary

117

NDA

133

110

▪ A total of 194 innovative molecules granted priority review in 33 batches

▪ 56% of innovative asset NDA approvals in 20181 have benefited from priority review (vs. 17% in 2016)

▪ Nov 2018, CDE announced to further accelerate the priority review listing by immediately review upon receipt

70 76 71# of

molecule2

APOLICY ENVIRONMENT

32McKinsey & Company

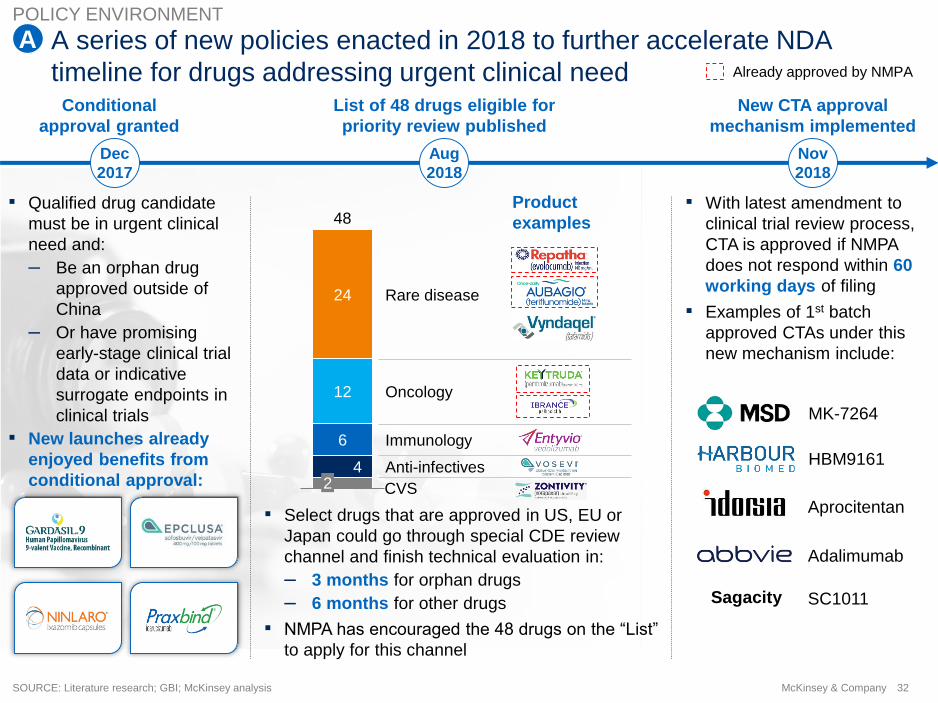

A series of new policies enacted in 2018 to further accelerate NDA

timeline for drugs addressing urgent clinical need

SOURCE: Literature research; GBI; McKinsey analysis

4

6

12

24 Rare disease

2Anti-infectives

Oncology

48

Immunology

Product

examples▪ Qualified drug candidate

must be in urgent clinical

need and:

– Be an orphan drug

approved outside of

China

– Or have promising

early-stage clinical trial

data or indicative

surrogate endpoints in

clinical trials

▪ New launches already

enjoyed benefits from

conditional approval:

▪ Select drugs that are approved in US, EU or

Japan could go through special CDE review

channel and finish technical evaluation in:

– 3 months for orphan drugs

– 6 months for other drugs

▪ NMPA has encouraged the 48 drugs on the “List”

to apply for this channel

List of 48 drugs eligible for

priority review published

Conditional

approval granted

New CTA approval

mechanism implemented

Already approved by NMPA

▪ With latest amendment to

clinical trial review process,

CTA is approved if NMPA

does not respond within 60

working days of filing

▪ Examples of 1st batch

approved CTAs under this

new mechanism include:

MK-7264

HBM9161

Aprocitentan

SC1011Sagacity

Adalimumab

Dec

2017

Nov

2018

Aug

2018

CVS

APOLICY ENVIRONMENT

33McKinsey & Company

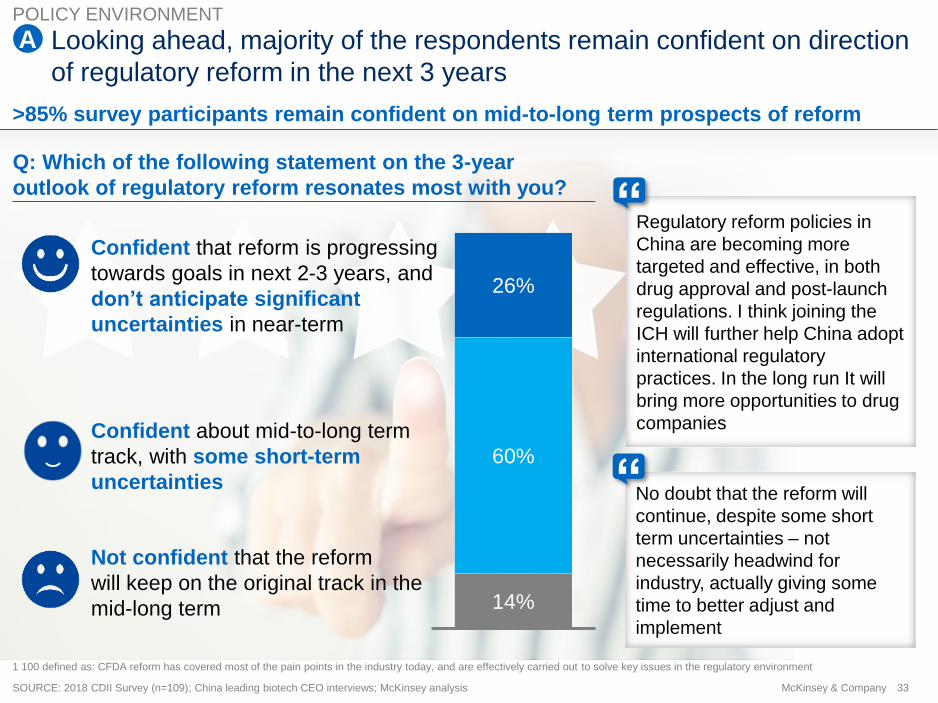

Looking ahead, majority of the respondents remain confident on direction

of regulatory reform in the next 3 years

14%

60%

26%

Not confident that the reform

will keep on the original track in the

mid-long term

Confident that reform is progressing

towards goals in next 2-3 years, and

don’t anticipate significant

uncertainties in near-term

Confident about mid-to-long term

track, with some short-term

uncertainties

1 100 defined as: CFDA reform has covered most of the pain points in the industry today, and are effectively carried out to solve key issues in the regulatory environment

>85% survey participants remain confident on mid-to-long term prospects of reform

SOURCE: 2018 CDII Survey (n=109); China leading biotech CEO interviews; McKinsey analysis

“Q: Which of the following statement on the 3-year

outlook of regulatory reform resonates most with you?

Regulatory reform policies in

China are becoming more

targeted and effective, in both

drug approval and post-launch

regulations. I think joining the

ICH will further help China adopt

international regulatory

practices. In the long run It will

bring more opportunities to drug

companies

“No doubt that the reform will

continue, despite some short

term uncertainties – not

necessarily headwind for

industry, actually giving some

time to better adjust and

implement

APOLICY ENVIRONMENT

34McKinsey & Company

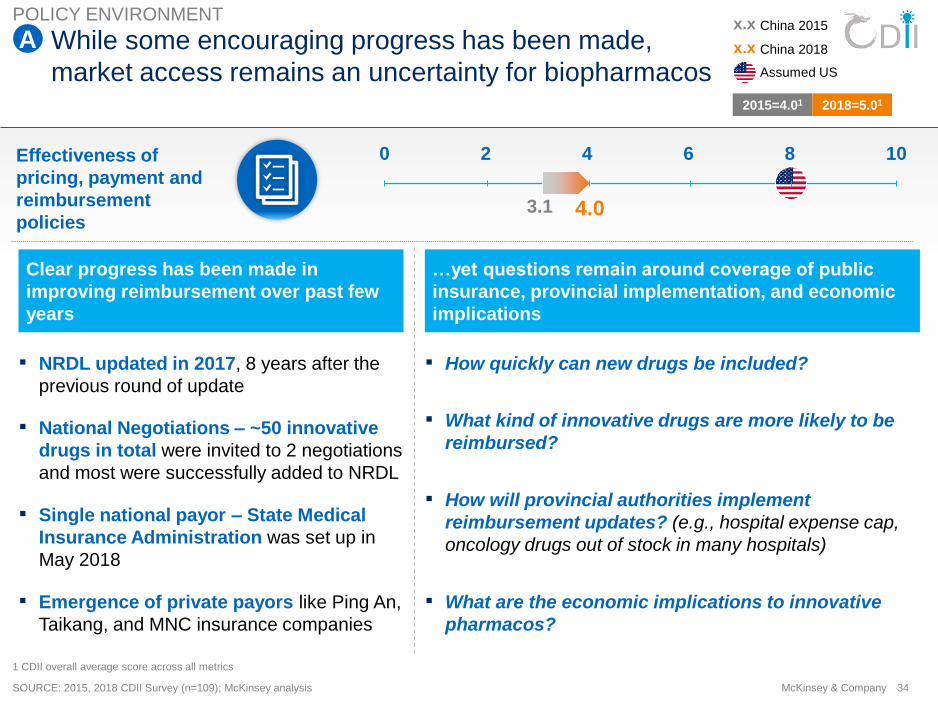

While some encouraging progress has been made,

market access remains an uncertainty for biopharmacos

Effectiveness of

pricing, payment and

reimbursement

policies

▪ National Negotiations – ~50 innovative

drugs in total were invited to 2 negotiations

and most were successfully added to NRDL

▪ NRDL updated in 2017, 8 years after the

previous round of update

1 CDII overall average score across all metrics

SOURCE: 2015, 2018 CDII Survey (n=109); McKinsey analysis

Clear progress has been made in

improving reimbursement over past few

years

…yet questions remain around coverage of public

insurance, provincial implementation, and economic

implications

▪ What kind of innovative drugs are more likely to be

reimbursed?

▪ How will provincial authorities implement

reimbursement updates? (e.g., hospital expense cap,

oncology drugs out of stock in many hospitals)

▪ Single national payor – State Medical

Insurance Administration was set up in

May 2018

▪ What are the economic implications to innovative

pharmacos?

▪ How quickly can new drugs be included?

▪ Emergence of private payors like Ping An,

Taikang, and MNC insurance companies

China 2015

China 2018

Assumed US

x.x

x.x

3.1

0 102 4 6 8

4.0

2015=4.01 2018=5.01

APOLICY ENVIRONMENT

35McKinsey & Company

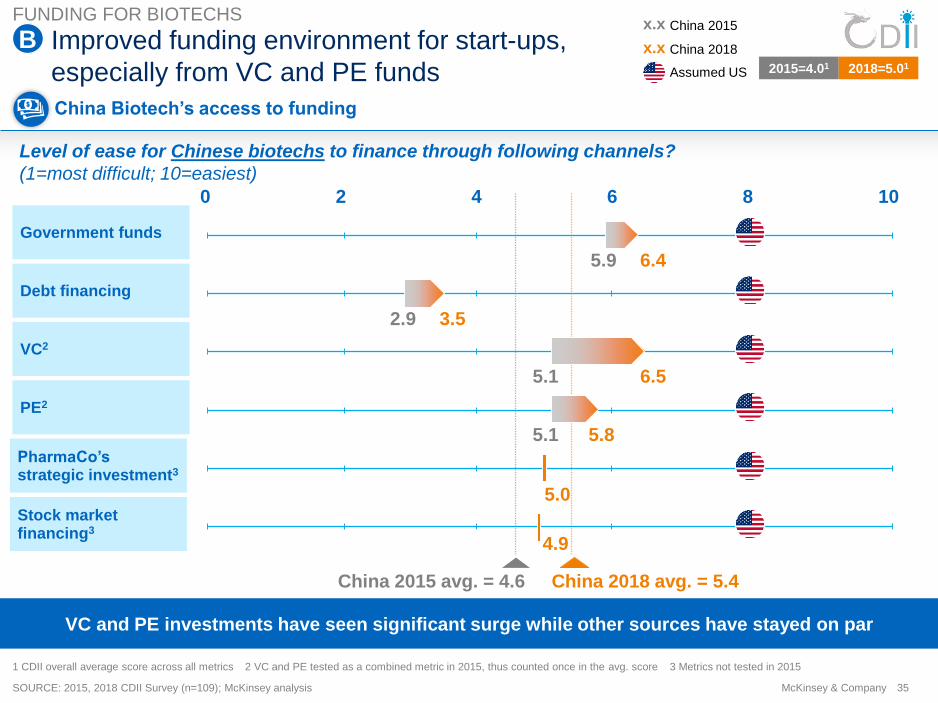

Improved funding environment for start-ups,

especially from VC and PE funds

China Biotech’s access to funding

VC2

Government funds

Debt financing

PE2

PharmaCo’s strategic investment3

Stock market financing3

1 CDII overall average score across all metrics 2 VC and PE tested as a combined metric in 2015, thus counted once in the avg. score 3 Metrics not tested in 2015

SOURCE: 2015, 2018 CDII Survey (n=109); McKinsey analysis

Level of ease for Chinese biotechs to finance through following channels?

(1=most difficult; 10=easiest)

China 2018 avg. = 5.4China 2015 avg. = 4.6

0 102 4 6 8

3.52.9

6.45.9

6.55.1

5.85.1

5.0

4.9

2015=4.01 2018=5.01

China 2015

China 2018

Assumed US

x.x

x.x

VC and PE investments have seen significant surge while other sources have stayed on par

BFUNDING FOR BIOTECHS

36McKinsey & CompanySOURCE: ChinaBio 2018 Report

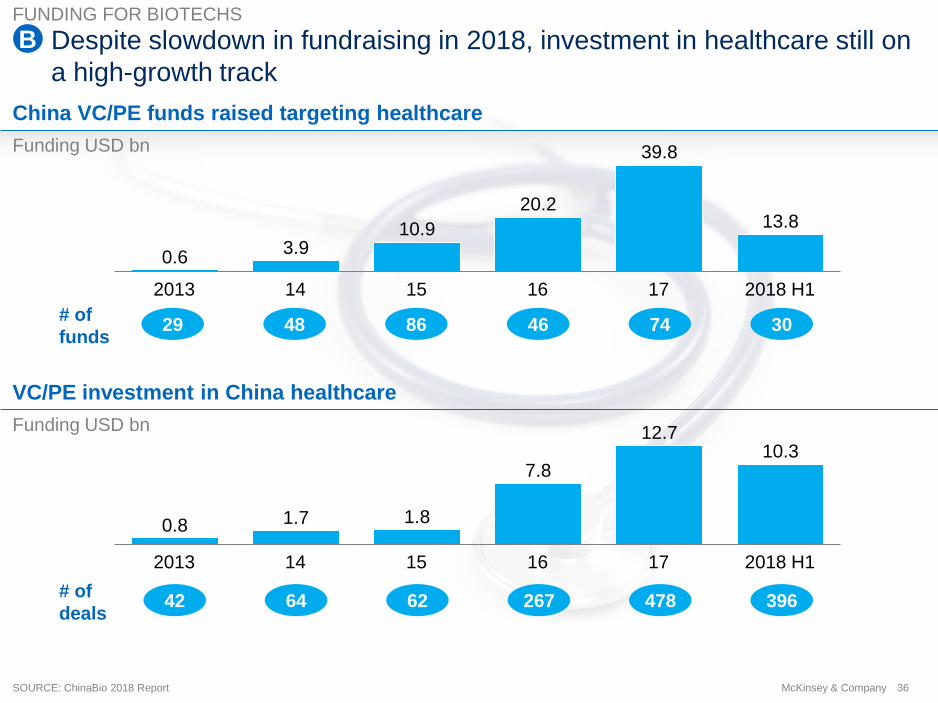

Despite slowdown in fundraising in 2018, investment in healthcare still on

a high-growth track

# of

deals6442 62 267

# of

funds4829 86 46 74

396

0.8 1.7 1.8

7.8

12.710.3

2018 H12013 14 15 16 17

0.63.9

10.9

20.2

39.8

13.8

2018 H12013 1714 15 16

Funding USD bn

VC/PE investment in China healthcare

Funding USD bn

China VC/PE funds raised targeting healthcare

30

478

BFUNDING FOR BIOTECHS

37McKinsey & Company

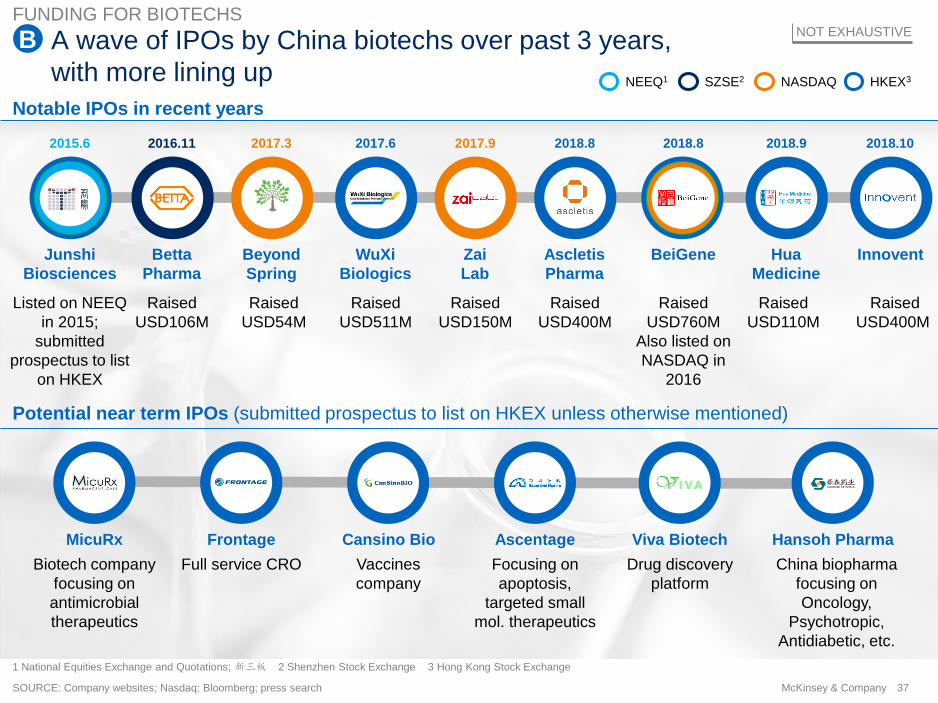

Notable IPOs in recent years

A wave of IPOs by China biotechs over past 3 years,

with more lining up

SOURCE: Company websites; Nasdaq; Bloomberg; press search

Potential near term IPOs (submitted prospectus to list on HKEX unless otherwise mentioned)

Full service CRO

Frontage Hansoh Pharma

Focusing on

apoptosis,

targeted small

mol. therapeutics

Ascentage

Biotech company

focusing on

antimicrobial

therapeutics

MicuRx

Vaccines

company

Cansino Bio

Drug discovery

platform

Viva Biotech

HKEX3SZSE2 NASDAQNEEQ1

NOT EXHAUSTIVE

1 National Equities Exchange and Quotations; 新三板 2 Shenzhen Stock Exchange 3 Hong Kong Stock Exchange

Beyond

Spring

Raised

USD54M

2017.3 2018.8

Ascletis

Pharma

Raised

USD400M

Listed on NEEQ

in 2015;

submitted

prospectus to list

on HKEX

2015.6

Junshi

Biosciences

2017.6

WuXi

Biologics

Raised

USD511M

BeiGene

Raised

USD760M

Also listed on

NASDAQ in

2016

2016.11

Betta

Pharma

Raised

USD106M

Raised

USD150M

2017.9

Zai

Lab

Raised

USD400M

Innovent

2018.9

Hua

Medicine

Raised

USD110M

2018.102018.8

China biopharma

focusing on

Oncology,

Psychotropic,

Antidiabetic, etc.

BFUNDING FOR BIOTECHS

38McKinsey & Company

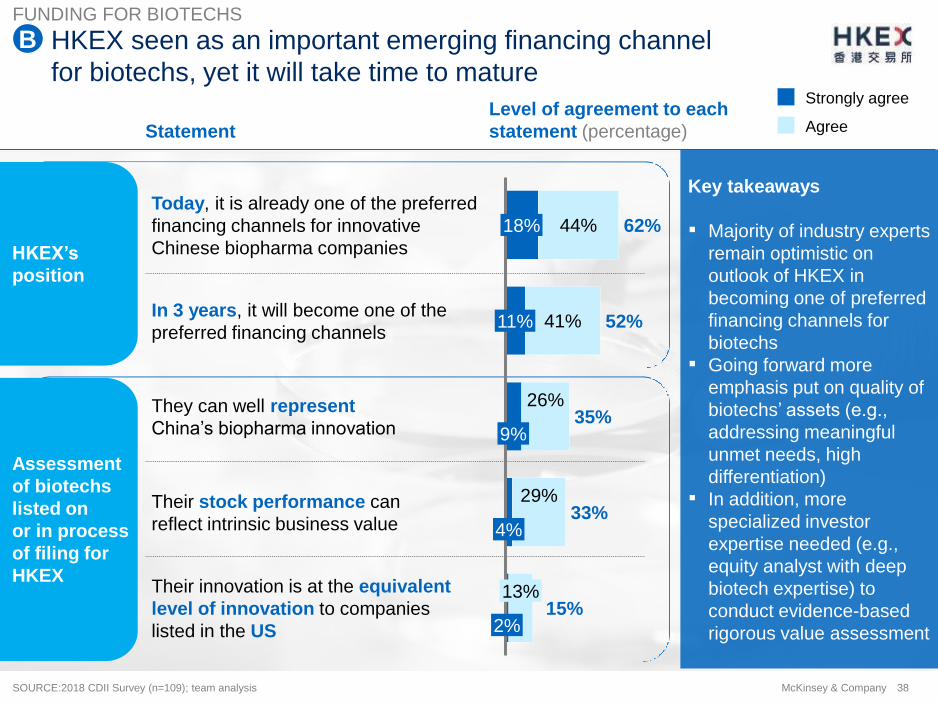

HKEX seen as an important emerging financing channel

for biotechs, yet it will take time to mature

44%

41%

26%

29%

62%18%

Today, it is already one of the preferred

financing channels for innovative

Chinese biopharma companies

11%

They can well represent

China’s biopharma innovation

In 3 years, it will become one of the

preferred financing channels

4%

9%

Their stock performance can

reflect intrinsic business value

13%

2%

Their innovation is at the equivalent

level of innovation to companies

listed in the US

52%

35%

33%

15%

Strongly agree

Agree

SOURCE:2018 CDII Survey (n=109); team analysis

Level of agreement to each

statement (percentage) Statement

Key takeaways

▪ Majority of industry experts

remain optimistic on

outlook of HKEX in

becoming one of preferred

financing channels for

biotechs

▪ Going forward more

emphasis put on quality of

biotechs’ assets (e.g.,

addressing meaningful

unmet needs, high

differentiation)

▪ In addition, more

specialized investor

expertise needed (e.g.,

equity analyst with deep

biotech expertise) to

conduct evidence-based

rigorous value assessment

Assessment

of biotechs

listed on

or in process

of filing for

HKEX

HKEX’s

position

BFUNDING FOR BIOTECHS

39McKinsey & Company

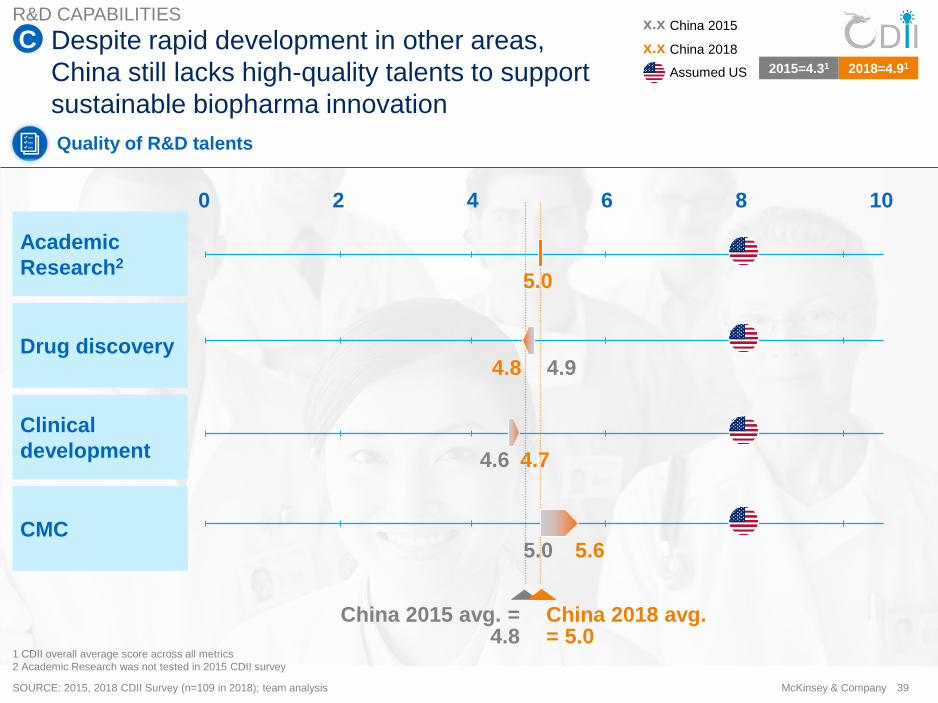

Despite rapid development in other areas,

China still lacks high-quality talents to support

sustainable biopharma innovation

1 CDII overall average score across all metrics

2 Academic Research was not tested in 2015 CDII survey

SOURCE: 2015, 2018 CDII Survey (n=109 in 2018); team analysis

Quality of R&D talents

2015=4.31 2018=4.91

China 2015

China 2018

Assumed US

x.x

x.xC

Clinical

development

Academic

Research2

Drug discovery

CMC

China 2018 avg. = 5.0

China 2015 avg. = 4.8

0 102 4 6 8

4.8 4.9

5.0

4.74.6

5.65.0

R&D CAPABILITIES

40McKinsey & Company

Novelty of innovative assets still lagging;

quality of R&Ds has clear room to grow

Quality of

R&D

Novelty of

Innovative pipeline

SOURCE: 2015, 2018 CDII Survey (n=109); China leading biotech CEO interviews; McKinsey analysis

China 2015 avg.3 = 4.1

China 2018 avg.3 = 4.4

PI2

CRO2

Sponsor2

Discovery

research

Clinical

development2

0 2 4 6 8 10

4.23.8

4.54.3

4.4

4.2

5.4

4.9

Clinical development capability

and capacity is a key pain point

for whole industry, especially for

early stage

“Still very few true innovation

in China. The only recent

example is the Ebola vaccine

“ Hard to catch up with the U.S. in

the next 5 years, as they have

invested much more into R&D

activities and have materially better

fundamental research capabilities

“

1 CDII overall average score across all metrics 2 Metrics not tested in 2015

3 Average of 'Novelty of innovative pipeline' and the average 'Quality of R&D' scores

2015=4.01 2018=5.01

China 2015

China 2018

Assumed US

x.x

x.xDLOCAL INNOVATION OUTPUT

41McKinsey & Company

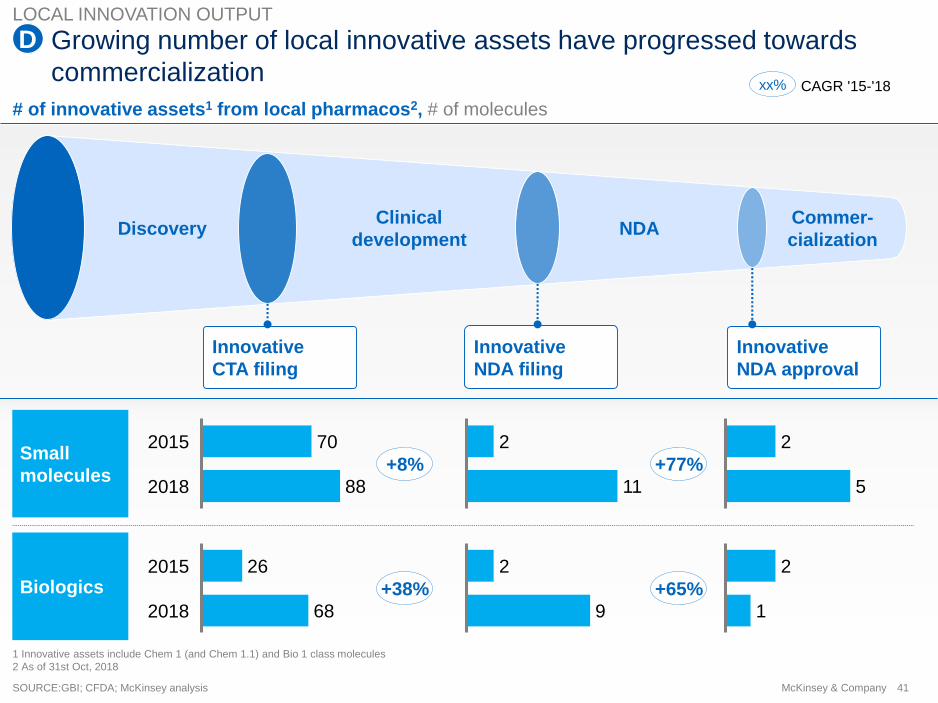

Growing number of local innovative assets have progressed towards

commercialization

Innovative

CTA filing

Innovative

NDA filing

Innovative

NDA approval

Small

molecules

Biologics

NDAClinical

development

Commer-

cializationDiscovery

70

882018

2015 2

11

2

5

26

68

2015

2018

2

9

2

1

SOURCE:GBI; CFDA; McKinsey analysis

# of innovative assets1 from local pharmacos2, # of molecules

1 Innovative assets include Chem 1 (and Chem 1.1) and Bio 1 class molecules

2 As of 31st Oct, 2018

+8%

+38%

+77%

+65%

CAGR '15-'18xx%

DLOCAL INNOVATION OUTPUT

42McKinsey & Company

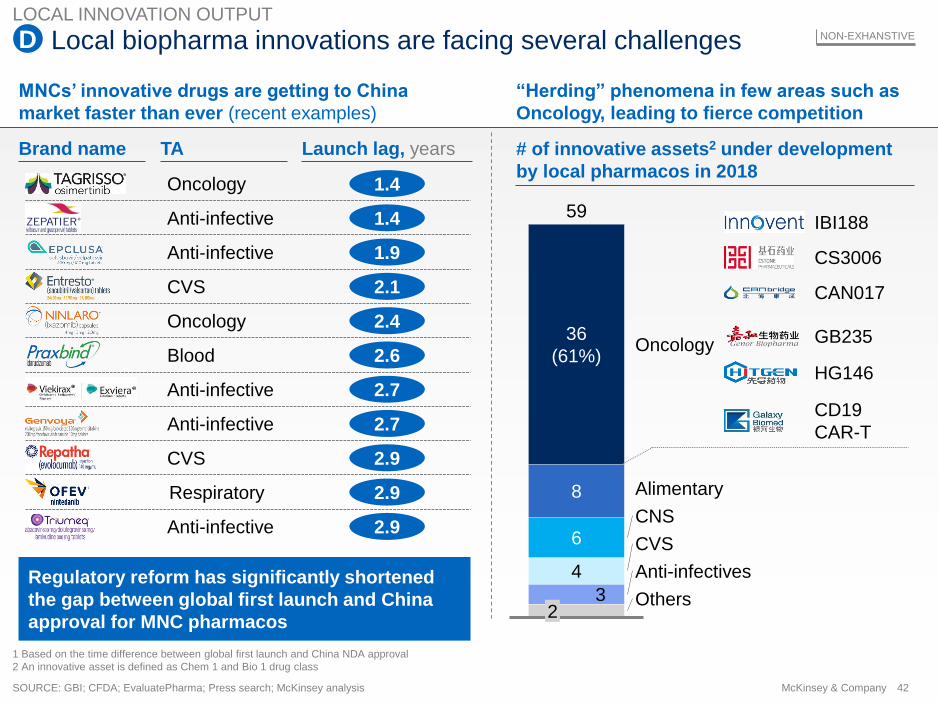

Local biopharma innovations are facing several challenges

MNCs’ innovative drugs are getting to China

market faster than ever (recent examples)

Regulatory reform has significantly shortened

the gap between global first launch and China

approval for MNC pharmacos

“Herding” phenomena in few areas such as

Oncology, leading to fierce competition

1 Based on the time difference between global first launch and China NDA approval

2 An innovative asset is defined as Chem 1 and Bio 1 drug class

# of innovative assets2 under development

by local pharmacos in 2018

3

4

6

8

36

(61%)

Anti-infectives

2

Oncology

CVS

Alimentary

CNS

Others

59IBI188

CS3006

CAN017

HG146

CD19

CAR-T

GB235

Brand name TA Launch lag, years

Oncology

Anti-infective

Anti-infective

1.4

1.4

2.1

2.4

CVS

Oncology

2.6Blood

2.7Anti-infective

Anti-infective

2.9CVS

Respiratory

Anti-infective 2.9

2.9

2.7

1.9

SOURCE: GBI; CFDA; EvaluatePharma; Press search; McKinsey analysis

NON-EXHANSTIVEDLOCAL INNOVATION OUTPUT

43McKinsey & Company

Recognizing intensifying competitions, industry experts anticipate clear

shift towards more differentiated innovations

15

45

20

20

100

Breakthrough (first in class)

Balanced mix of incremental

and breakthrough

“First to China” in areas with

significant unmet needs

Incremental (Me-too/me-better)

Which type of innovation should China

biopharmacos focus on …

% of agreement

China biopharma NMEs have skewed towards

me-too/me-better innovation to date

Looking ahead, industry experts expect clear

shift towards more innovative portfolio

First to China

Me-too/me-better

First in class global

Ad5-EBOV

(recombinant Ebola

virus vaccine)

GK1 (Dorzagliatin)

Examples of local biopharma innovations by MoA

Small molecule

Large molecule &

new modalities

IDH1 (Ivosidenib)

FGF and VEG

(Brivanib)

FGFR2b

(Bemarituzumab)

PARP (Fluzoparib,

Mefuparib,

IMP4297)

VEGF (Conbercept,

Affecizx)

EGFR TKI (BPI-

7711, HS-10296,

Neptinib, ES-072)

PD-1/PD-L1 (SHR-

1210, CS1001,

GB226)

DPP-4 (Besigliptin,

Retagliptin, Imigliptin,

Ulogliptin )

PCSK9 (SHR-

1209, IBI306,

AK102)

SOURCE: GBI; Press search; McKinsey analysis

1 Glucokinase

DLOCAL INNOVATION OUTPUT

44McKinsey & Company

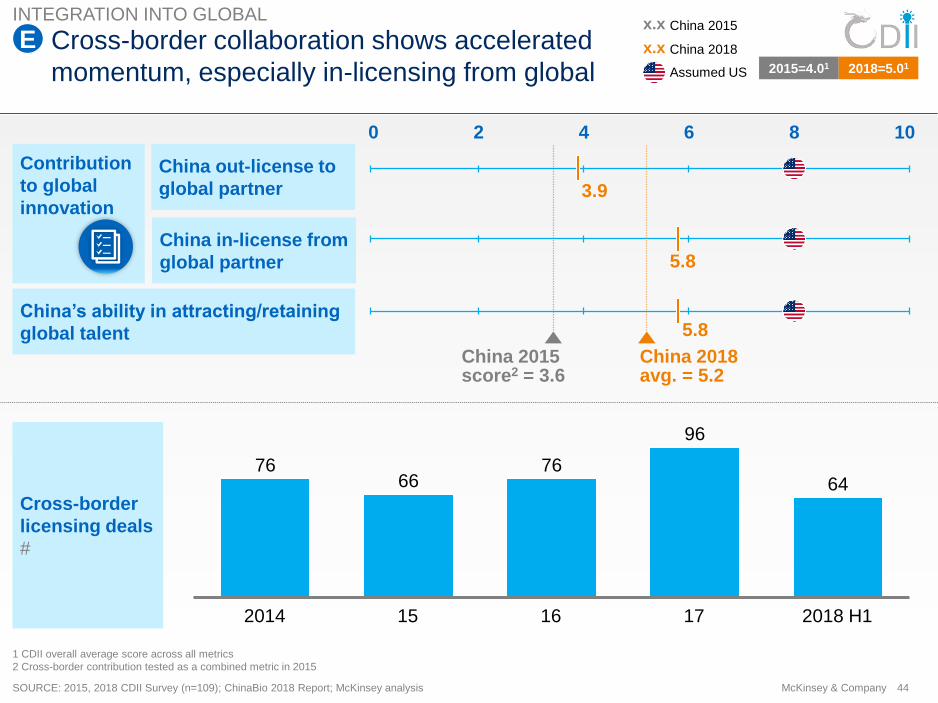

Cross-border collaboration shows accelerated

momentum, especially in-licensing from global

Cross-border

licensing deals

#

7666

76

96

64

2014 15 16 17 2018 H1

Contribution

to global

innovation

China out-license to

global partner

China in-license from

global partner

SOURCE: 2015, 2018 CDII Survey (n=109); ChinaBio 2018 Report; McKinsey analysis

1 CDII overall average score across all metrics

2 Cross-border contribution tested as a combined metric in 2015

China’s ability in attracting/retaining

global talent

China 2015 score2 = 3.6

China 2018 avg. = 5.2

0 2 4 6 8 10

3.9

5.8

5.8

2015=4.01 2018=5.01

China 2015

China 2018

Assumed US

x.x

x.xEINTEGRATION INTO GLOBAL

45McKinsey & Company

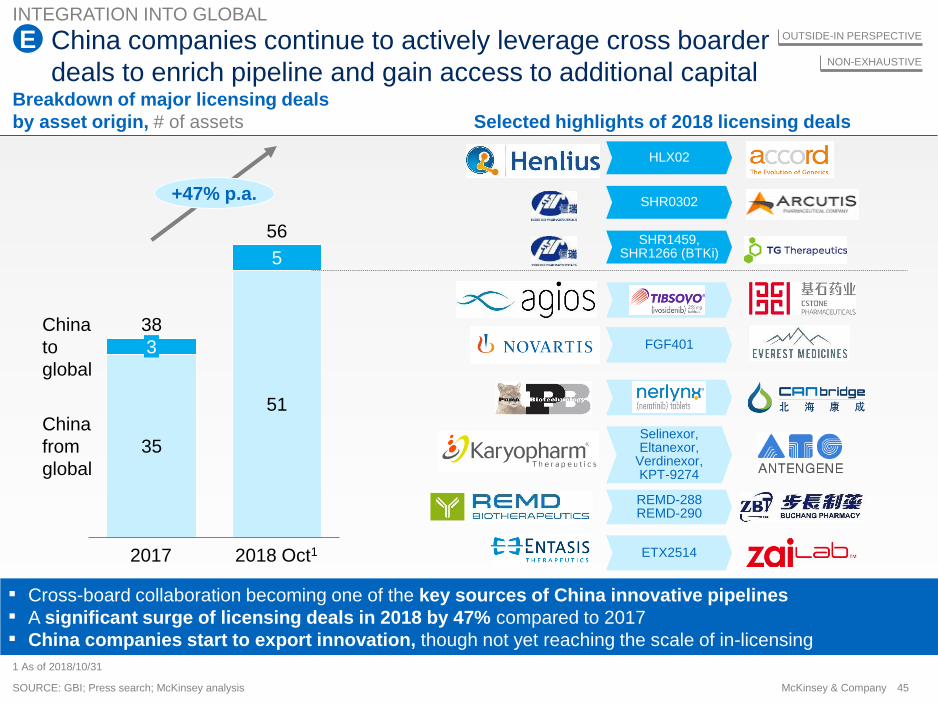

China companies continue to actively leverage cross boarder

deals to enrich pipeline and gain access to additional capital

35

51

5

3

2018 Oct12017

China

to

global

China

from

global

38

56

+47% p.a.

Breakdown of major licensing deals

by asset origin, # of assets

SOURCE: GBI; Press search; McKinsey analysis

OUTSIDE-IN PERSPECTIVE

Ivosidenib

Selinexor, Eltanexor,

Verdinexor, KPT-9274

FGF401

Neratinib

HLX02

NON-EXHAUSTIVE

SHR0302

SHR1459, SHR1266 (BTKi)

REMD-288REMD-290

▪ Cross-board collaboration becoming one of the key sources of China innovative pipelines

▪ A significant surge of licensing deals in 2018 by 47% compared to 2017

▪ China companies start to export innovation, though not yet reaching the scale of in-licensing

1 As of 2018/10/31

Selected highlights of 2018 licensing deals

ETX2514

EINTEGRATION INTO GLOBAL

46McKinsey & Company

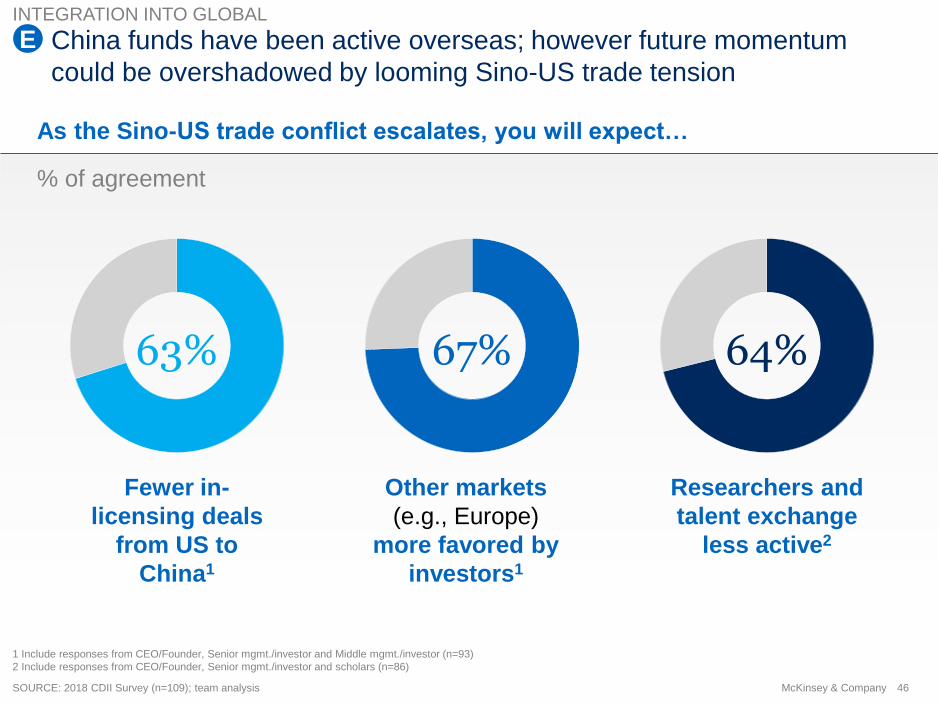

China funds have been active overseas; however future momentum

could be overshadowed by looming Sino-US trade tension

As the Sino-US trade conflict escalates, you will expect…

SOURCE: 2018 CDII Survey (n=109); team analysis

1 Include responses from CEO/Founder, Senior mgmt./investor and Middle mgmt./investor (n=93)

2 Include responses from CEO/Founder, Senior mgmt./investor and scholars (n=86)

Fewer in-

licensing deals

from US to

China1

Other markets

(e.g., Europe)

more favored by

investors1

Researchers and

talent exchange

less active2

63% 67% 64%

E

% of agreement

INTEGRATION INTO GLOBAL

47McKinsey & Company

In summary…

▪ Regulatory

environment

▪ Investment into

biotech

▪ Cross-boarder

licensing deals

▪ Shaping market access

policies to properly

reward innovation

▪ Continue to enhance R&D

capabilities and elevate

innovation, building on

promising momentum

47McKinsey & Company

Opportunities ahead

Rapid progress made in

“bright spots”

48McKinsey & Company

Momentum of China biopharma innovation – two topics

Fresh view of China

biopharma innovation

ecosystem

Momentum of

China biotech

49McKinsey & Company

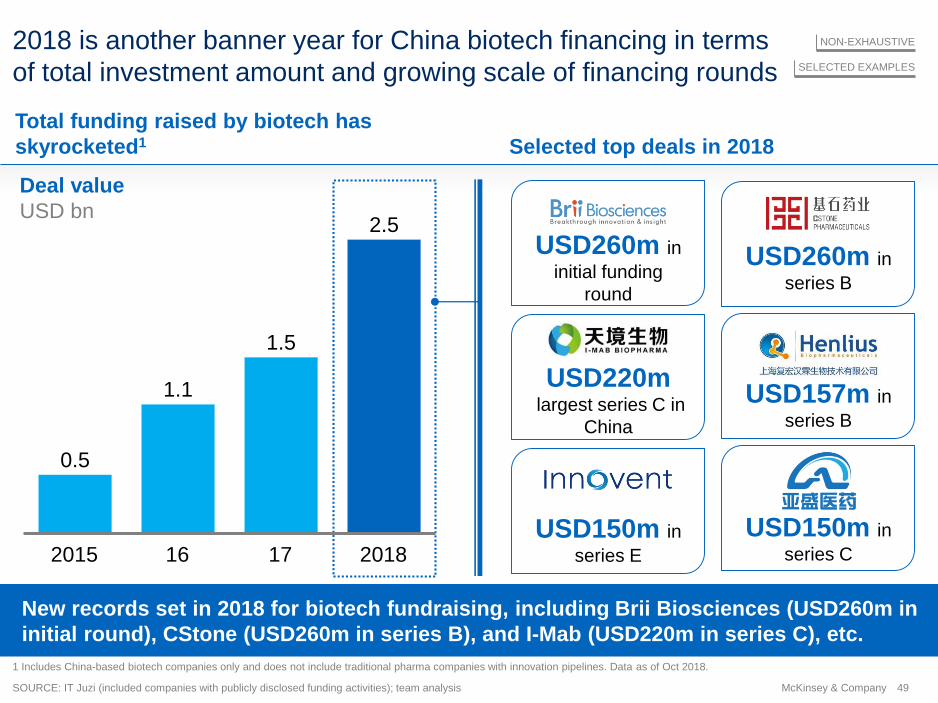

2018 is another banner year for China biotech financing in terms

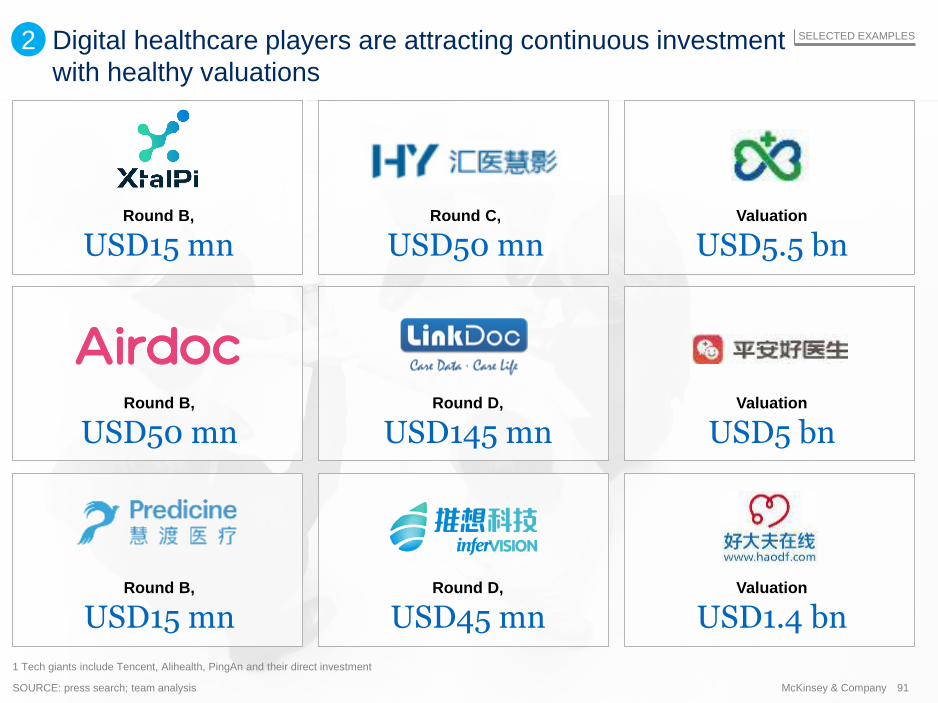

of total investment amount and growing scale of financing rounds SELECTED EXAMPLES

NON-EXHAUSTIVE

SOURCE: IT Juzi (included companies with publicly disclosed funding activities); team analysis

0.5

1.1

1.5

2.5

20182015 16 17

Deal value

USD bn

New records set in 2018 for biotech fundraising, including Brii Biosciences (USD260m in

initial round), CStone (USD260m in series B), and I-Mab (USD220m in series C), etc.

Total funding raised by biotech has

skyrocketed1

USD260m in

series B

USD157m in

series B

Selected top deals in 2018

USD150m in

series C

USD260m in

initial funding

round

USD220mlargest series C in

China

USD150m in

series E

1 Includes China-based biotech companies only and does not include traditional pharma companies with innovation pipelines. Data as of Oct 2018.

50McKinsey & Company

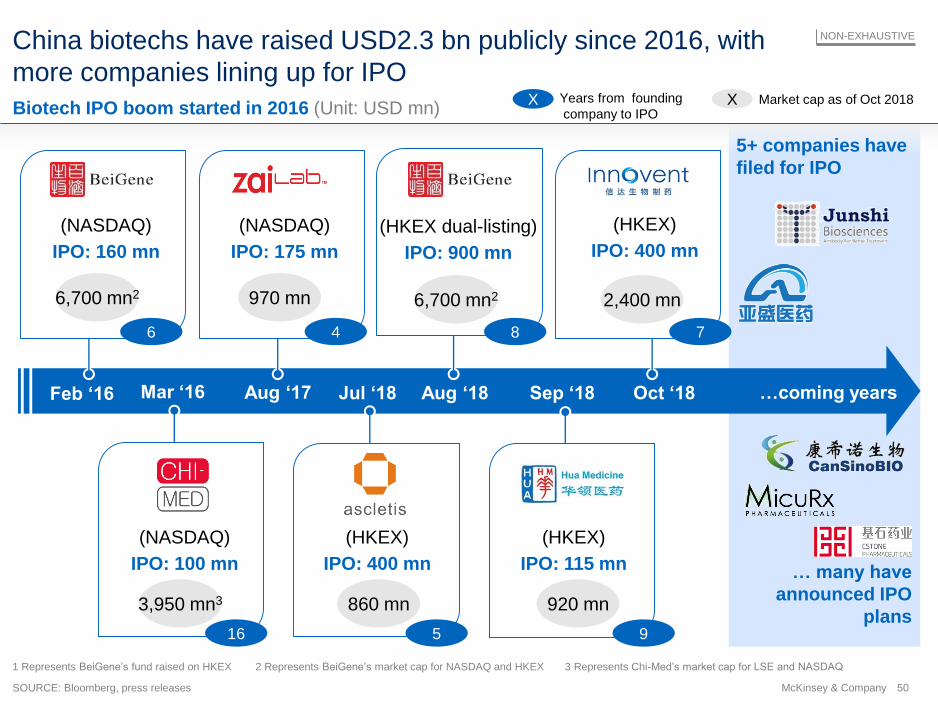

China biotechs have raised USD2.3 bn publicly since 2016, with

more companies lining up for IPO

Biotech IPO boom started in 2016 (Unit: USD mn)

5+ companies have

filed for IPO

Jul ‘18 Aug ‘18 Sep ‘18 Oct ‘18 …coming years

SOURCE: Bloomberg, press releases

… many have

announced IPO

plans

Aug ‘17Feb ‘16 Mar ‘16

(HKEX)

IPO: 400 mn

1 Represents BeiGene’s fund raised on HKEX 2 Represents BeiGene’s market cap for NASDAQ and HKEX 3 Represents Chi-Med’s market cap for LSE and NASDAQ

860 mn 920 mn3,950 mn3

2,400 mn

(NASDAQ)

IPO: 160 mn

(NASDAQ)

IPO: 175 mn

(NASDAQ)

IPO: 100 mn

(HKEX)

IPO: 400 mn

(HKEX)

IPO: 115 mn

(HKEX dual-listing)

IPO: 900 mn

6,700 mn2 6,700 mn2970 mn

Market cap as of Oct 2018XX Years from founding

company to IPO

6 4 8 7

16 5 9

NON-EXHAUSTIVE

51McKinsey & Company

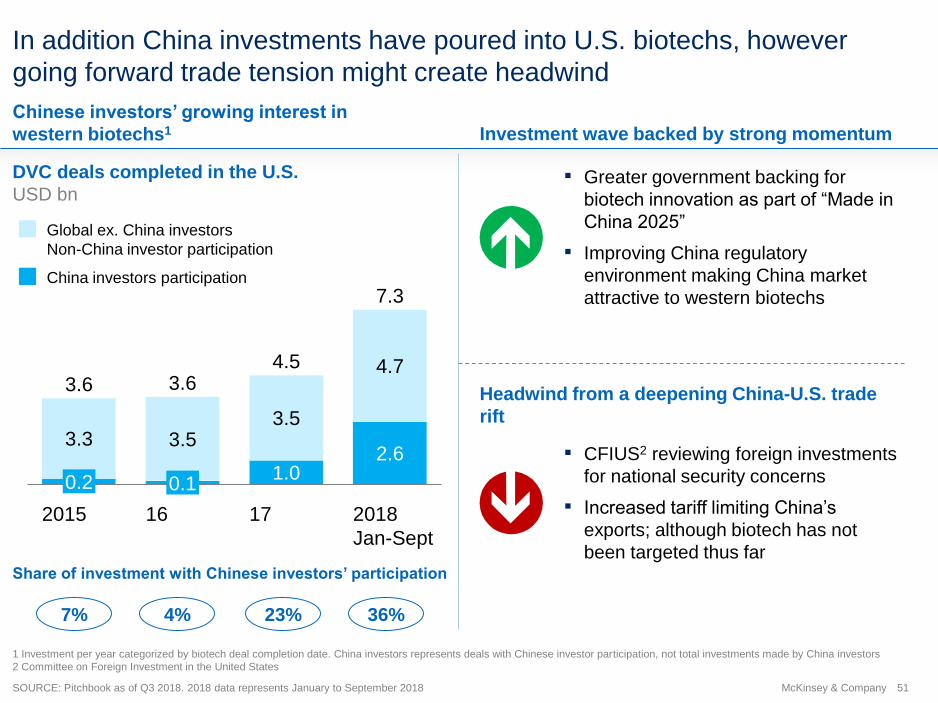

In addition China investments have poured into U.S. biotechs, however

going forward trade tension might create headwind

Headwind from a deepening China-U.S. trade

rift

1 Investment per year categorized by biotech deal completion date. China investors represents deals with Chinese investor participation, not total investments made by China investors

2 Committee on Foreign Investment in the United States

1.02.6

3.3 3.53.5

4.73.63.6

0.2

17162015

0.1

2018

Jan-Sept

4.5

7.3

SOURCE: Pitchbook as of Q3 2018. 2018 data represents January to September 2018

Global ex. China investors

Non-China investor participation

China investors participation

7% 4% 23% 36%

Share of investment with Chinese investors’ participation

Chinese investors’ growing interest in

western biotechs1 Investment wave backed by strong momentum

▪ Greater government backing for

biotech innovation as part of “Made in

China 2025”

▪ Improving China regulatory

environment making China market

attractive to western biotechs

▪ CFIUS2 reviewing foreign investments

for national security concerns

▪ Increased tariff limiting China’s

exports; although biotech has not

been targeted thus far

DVC deals completed in the U.S.

USD bn

52McKinsey & Company

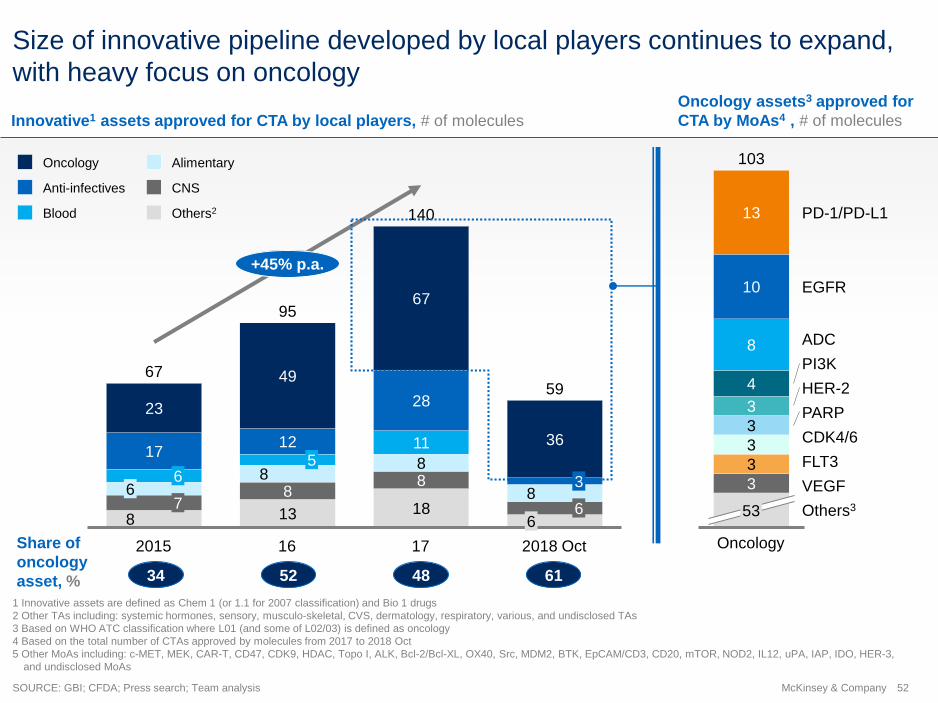

Size of innovative pipeline developed by local players continues to expand,

with heavy focus on oncology

SOURCE: GBI; CFDA; Press search; Team analysis

8 13 188

888

8

1117

12

28

36

23

49

6795

2015

66

7

5

3

16 17

140

66

2018 Oct

6759

+45% p.a.

3

3

3

3

3

4

8

10

13

Others3

PI3K

ADC

EGFR

53

PD-1/PD-L1

Oncology

CDK4/6

HER-2

PARP

FLT3

VEGF

103Oncology

Anti-infectives

Blood

CNS

Alimentary

Others2

Innovative1 assets approved for CTA by local players, # of molecules

1 Innovative assets are defined as Chem 1 (or 1.1 for 2007 classification) and Bio 1 drugs

2 Other TAs including: systemic hormones, sensory, musculo-skeletal, CVS, dermatology, respiratory, various, and undisclosed TAs

3 Based on WHO ATC classification where L01 (and some of L02/03) is defined as oncology

4 Based on the total number of CTAs approved by molecules from 2017 to 2018 Oct

5 Other MoAs including: c-MET, MEK, CAR-T, CD47, CDK9, HDAC, Topo I, ALK, Bcl-2/Bcl-XL, OX40, Src, MDM2, BTK, EpCAM/CD3, CD20, mTOR, NOD2, IL12, uPA, IAP, IDO, HER-3,

and undisclosed MoAs

Oncology assets3 approved for

CTA by MoAs4 , # of molecules

Share of

oncology

asset, % 34 52 48 61

53McKinsey & Company

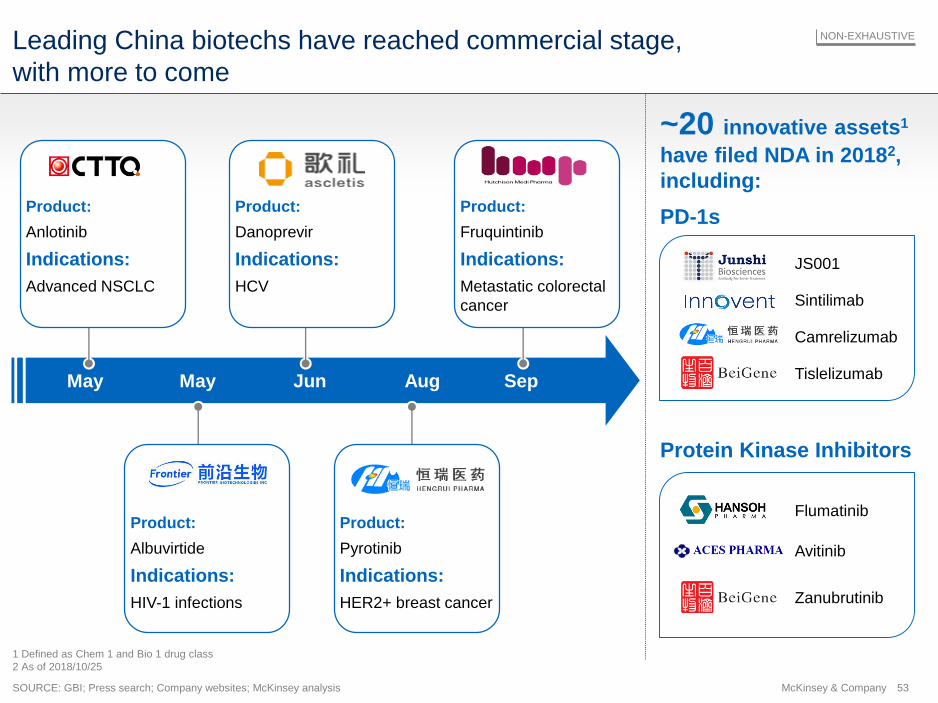

Leading China biotechs have reached commercial stage,

with more to come

PD-1s

Protein Kinase Inhibitors

NON-EXHAUSTIVE

~20 innovative assets1

have filed NDA in 20182,

including:

JS001

Sintilimab

Tislelizumab

Camrelizumab

Flumatinib

Avitinib

Zanubrutinib

May May Jun Aug Sep

HER2+ breast cancer

Pyrotinib

Product:

Indications:

HIV-1 infections

Albuvirtide

Product:

Indications:

Advanced NSCLC

Anlotinib

Product:

Indications:

HCV

Danoprevir

Product:

Indications:

Metastatic colorectal

cancer

Fruquintinib

Product:

Indications:

SOURCE: GBI; Press search; Company websites; McKinsey analysis

1 Defined as Chem 1 and Bio 1 drug class

2 As of 2018/10/25

54McKinsey & Company

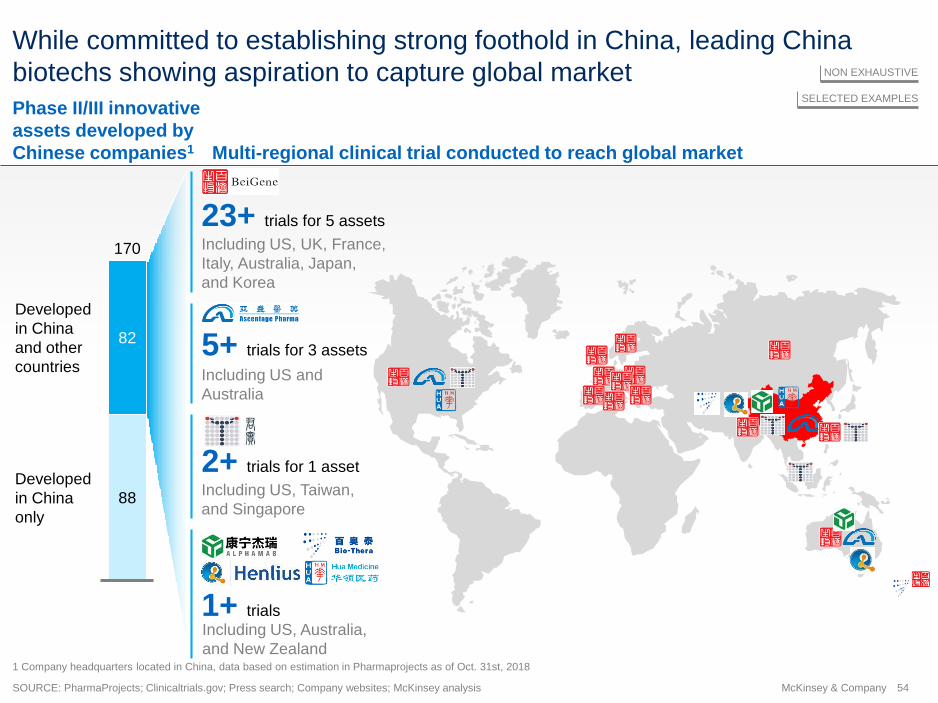

Multi-regional clinical trial conducted to reach global market

Phase II/III innovative

assets developed by

Chinese companies1

While committed to establishing strong foothold in China, leading China

biotechs showing aspiration to capture global market

SOURCE: PharmaProjects; Clinicaltrials.gov; Press search; Company websites; McKinsey analysis

NON EXHAUSTIVE

SELECTED EXAMPLES

88

82

170

Developed

in China

only

Developed

in China

and other

countries

1 Company headquarters located in China, data based on estimation in Pharmaprojects as of Oct. 31st, 2018

Including US, Australia,

and New Zealand

1+ trials

23+ trials for 5 assets

Including US, UK, France,

Italy, Australia, Japan,

and Korea

Including US and

Australia

5+ trials for 3 assets

Including US, Taiwan,

and Singapore

2+ trials for 1 asset

55McKinsey & Company

Significant unmet medical

needs in China and beyond China biotechs’ two innovation approaches

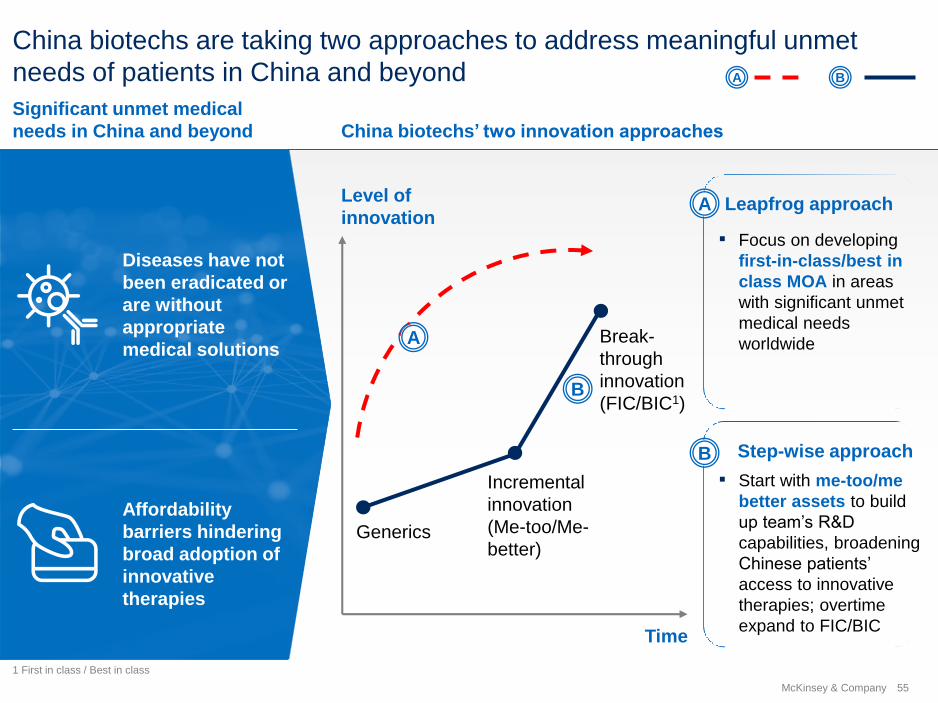

China biotechs are taking two approaches to address meaningful unmet

needs of patients in China and beyond

Leapfrog approach

▪ Focus on developing

first-in-class/best in

class MOA in areas

with significant unmet

medical needs

worldwide

Step-wise approach

▪ Start with me-too/me

better assets to build

up team’s R&D

capabilities, broadening

Chinese patients’

access to innovative

therapies; overtime

expand to FIC/BIC

A

B

Level of

innovation

Time

Generics

Incremental

innovation

(Me-too/Me-

better)

Break-

through

innovation

(FIC/BIC1)

BA

Diseases have not

been eradicated or

are without

appropriate

medical solutions

Affordability

barriers hindering

broad adoption of

innovative

therapies

A

B

1 First in class / Best in class

56McKinsey & Company

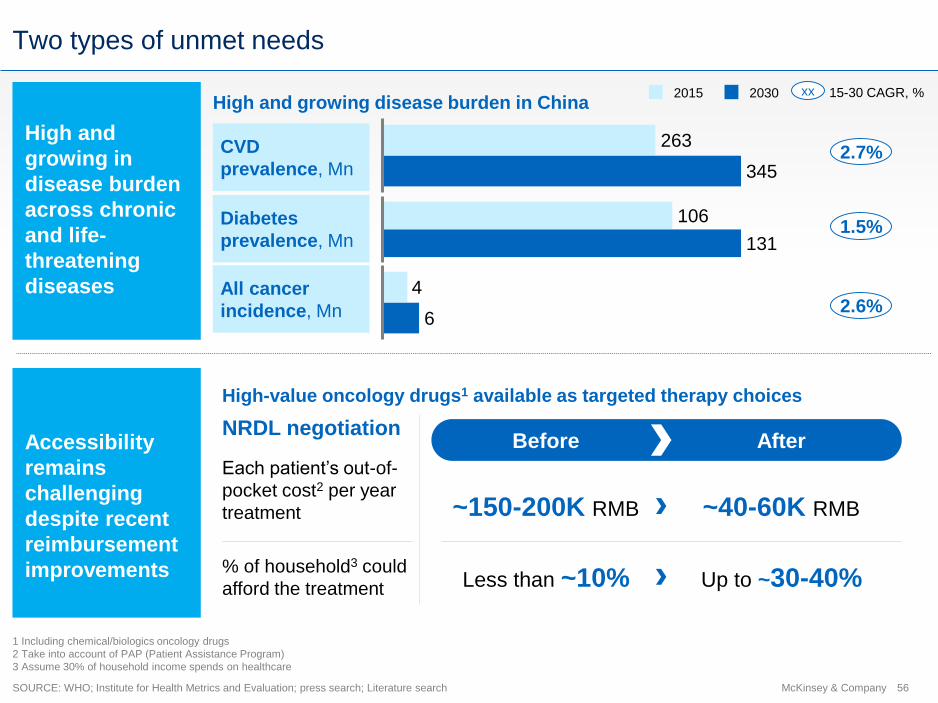

Two types of unmet needs

SOURCE: WHO; Institute for Health Metrics and Evaluation; press search; Literature search

1 Including chemical/biologics oncology drugs

2 Take into account of PAP (Patient Assistance Program)

3 Assume 30% of household income spends on healthcare

xx 15-30 CAGR, %

High-value oncology drugs1 available as targeted therapy choices

NRDL negotiationBefore After

Each patient’s out-of-

pocket cost2 per year

treatment ~150-200K RMB ~40-60K RMB

High and

growing in

disease burden

across chronic

and life-

threatening

diseases

Accessibility

remains

challenging

despite recent

reimbursement

improvements

Diabetes

prevalence, Mn

CVD

prevalence, Mn

All cancer

incidence, Mn

106

131

2015 2030

1.5%

263

345

High and growing disease burden in China

4

6

2.7%

2.6%

% of household3 could

afford the treatment Less than ~10% Up to ~30-40%

57McKinsey & Company

Many China biotechs share several characteristics

01 0302 ++

Scaled and

risk-balanced

portfolio

Unraveled

speed to

establish lead

Experimenting

with innovative

business

model

58McKinsey & Company

“

China biotechs have relative scaled portfolio compared to global peers 1

SOURCE: GBI database; press search; China leading Biotech CEO interviews; team analysis

8

6

9

3

2

9

8

3

8

7

3

2

3

1

1

Avg:10

1

1

17

15

13

11

4

8

7

5

3

4

3

3

6

2

3

3

4

2

1

1

1

1

1

1

Avg: 4

7

7

6

5

4

4

4

4

2

1

1 Assets at all stages and all kind of right (e.g., licensed-in assets with region right) listed in the IPO prospectus; number of combo therapies are not included

2 Based on IPOs in Nasdaq capital market and global market as of 2018/09/25, and biotech company classification based on Capital IQ classification

Pre-clinical

Clinical

NDA filed/launched

China biotech Global biotech

# of assets1 by companies when

filed IPO in HKEX in 2018

# of assets1 by companies when

IPOed in Nasdaq in 20182

We have a strategy to

license-in relative late stage

assets and develop early

stage assets in house to

ensure we build our pipeline

with scale and momentum

– CEO of leading China-

based biotechs

– CEO of leading China-

based biotechs

Our portfolio play is a way to

stand out in fierce

competition. If we follow the

traditional US biotech path,

we will not be able to

leapfrog

“

59McKinsey & Company

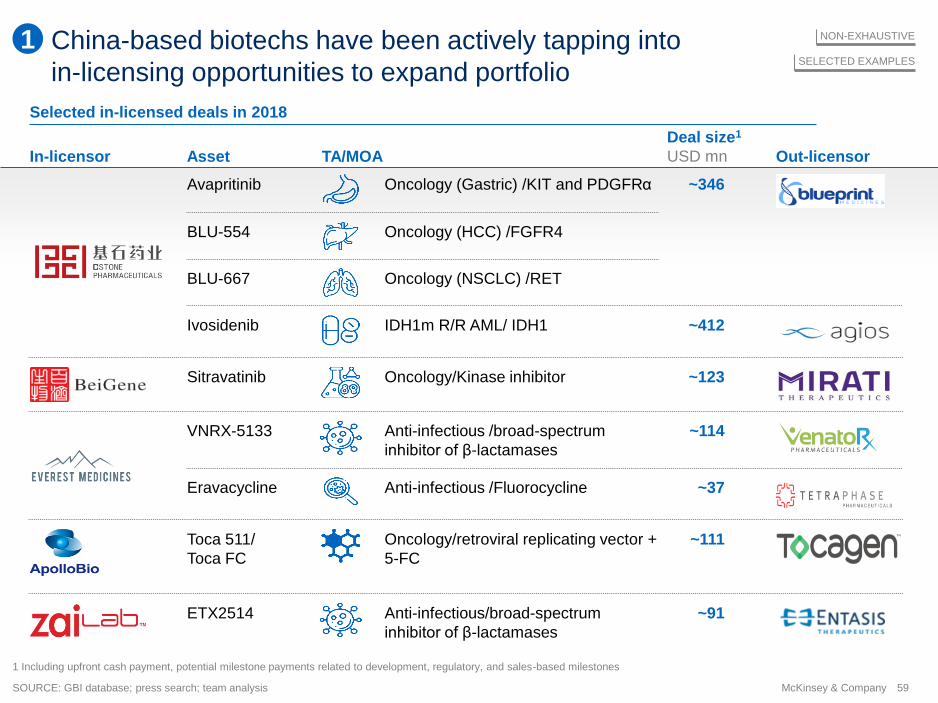

China-based biotechs have been actively tapping into

in-licensing opportunities to expand portfolio

SOURCE: GBI database; press search; team analysis

1 Including upfront cash payment, potential milestone payments related to development, regulatory, and sales-based milestones

NON-EXHAUSTIVE

SELECTED EXAMPLES

Selected in-licensed deals in 2018

In-licensor Out-licensorAsset TA/MOA

Avapritinib Oncology (Gastric) /KIT and PDGFRα

Deal size1

USD mn

~346

BLU-667 Oncology (NSCLC) /RET

BLU-554 Oncology (HCC) /FGFR4

Sitravatinib Oncology/Kinase inhibitor ~123

ETX2514 ~91Anti-infectious/broad-spectrum

inhibitor of β-lactamases

VNRX-5133 Anti-infectious /broad-spectrum

inhibitor of β-lactamases

~114

Eravacycline Anti-infectious /Fluorocycline ~37

Toca 511/

Toca FC

Oncology/retroviral replicating vector +

5-FC

~111

Ivosidenib IDH1m R/R AML/ IDH1 ~412

1

60McKinsey & Company

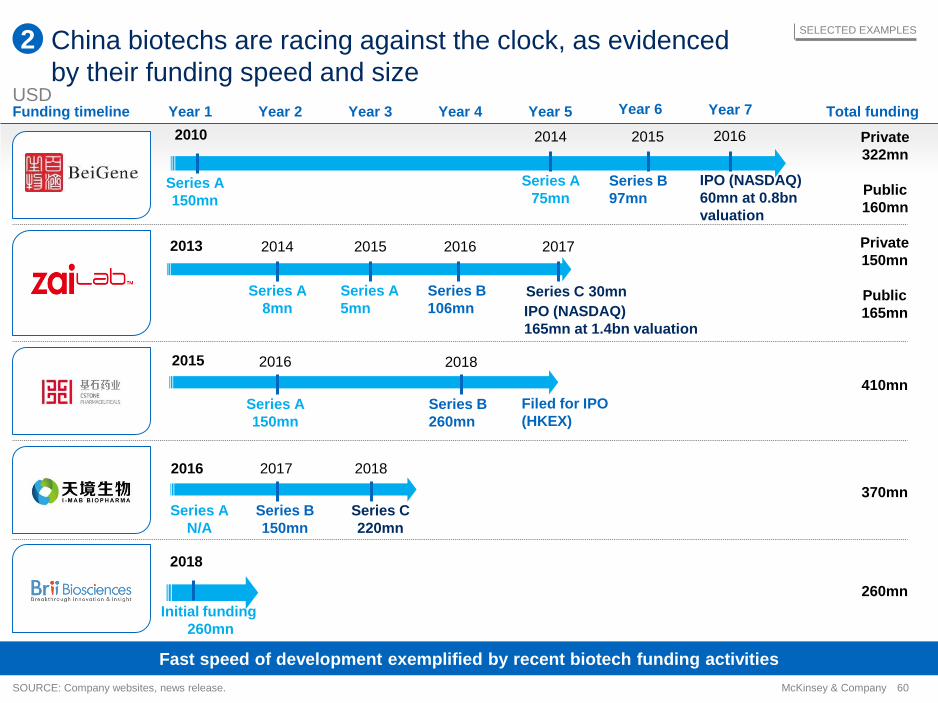

Fast speed of development exemplified by recent biotech funding activities

Total fundingFunding timeline

Private

150mn

Public

165mn

2013 2014

Series A

8mn IPO (NASDAQ)

165mn at 1.4bn valuation

2015

Series A

5mn

2016

Series B

106mn

2017

Series C 30mn

410mn

2015 2016 2018

Series A

150mn

Series B

260mn

260mn

2018

Initial funding

260mn

370mn

2016 2017

Series B

150mn

2018

Series C

220mn

Series A

N/A

SOURCE: Company websites, news release.

2010

Series A

150mn

Year 1 Year 2 Year 3 Year 4 Year 5

2014

Series A

75mn

2015

Series B

97mn

Year 6 Year 7

2016

IPO (NASDAQ)

60mn at 0.8bn

valuation

Private

322mn

Public

160mn

China biotechs are racing against the clock, as evidenced

by their funding speed and size

SELECTED EXAMPLES

2

USD

Filed for IPO

(HKEX)

61McKinsey & Company

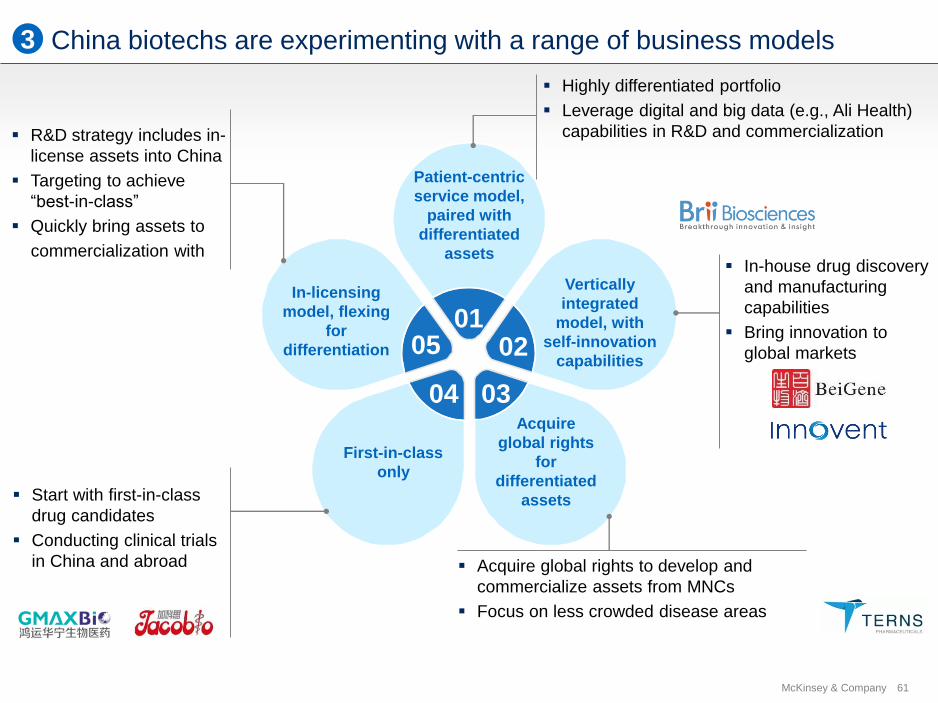

China biotechs are experimenting with a range of business models

Vertically

integrated

model, with

self-innovation

capabilities

▪ In-house drug discovery

and manufacturing

capabilities

▪ Bring innovation to

global markets

Patient-centric

service model,

paired with

differentiated

assets

▪ Highly differentiated portfolio

▪ Leverage digital and big data (e.g., Ali Health)

capabilities in R&D and commercialization

Acquire

global rights

for

differentiated

assets

▪ Acquire global rights to develop and

commercialize assets from MNCs

▪ Focus on less crowded disease areas

In-licensing

model, flexing

for

differentiation

▪ R&D strategy includes in-

license assets into China

▪ Targeting to achieve

“best-in-class”

▪ Quickly bring assets to

commercialization with

First-in-class

only

▪ Start with first-in-class

drug candidates

▪ Conducting clinical trials

in China and abroad

0201

0304

05

3

62McKinsey & Company

Top of mind questions for China biotech CEOs

▪ How to ensure high

quality in clinical

development while

progressing multiple trials

at rapid pace?

▪ How quickly will

reimbursement policies

evolve to properly reward

innovation? What types of

innovative therapies will

get reimbursed?

▪ What is the solution to

find quality talent to

sufficiently support

demand in clinical

development and

commercialization?

▪ How to create sustainable

differentiation? Will it

come from shift towards

FIC/BIC assets,

differentiated clinical

strategy or creative

commercial model?

Quality

Talents

Reimbursement

Competition

SOURCE: China leading biotech CEO interviews

63McKinsey & Company

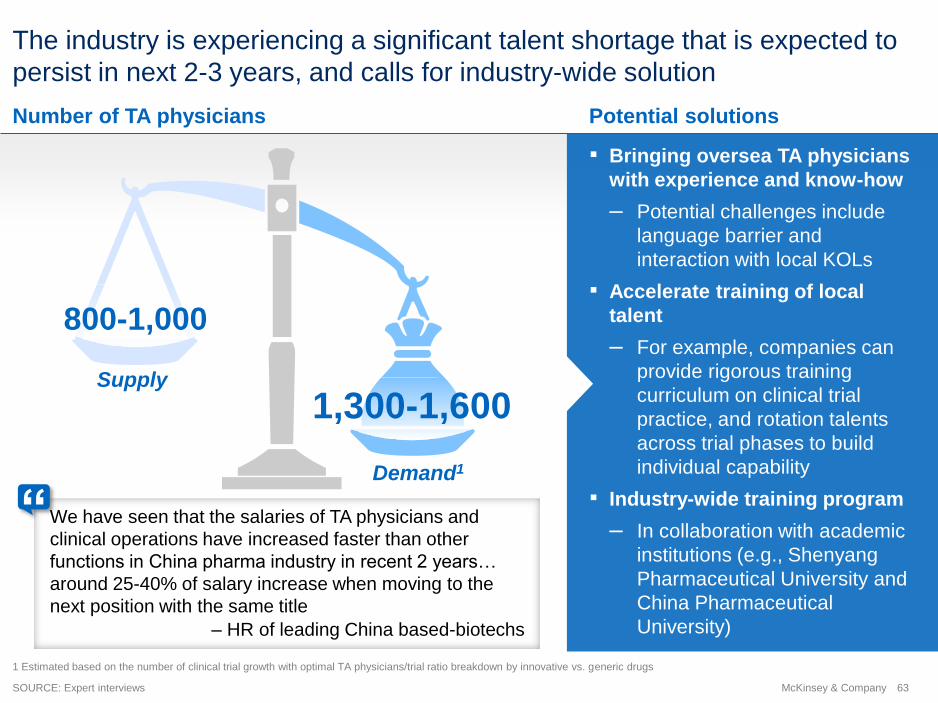

The industry is experiencing a significant talent shortage that is expected to

persist in next 2-3 years, and calls for industry-wide solution

Number of TA physicians

SOURCE: Expert interviews

We have seen that the salaries of TA physicians and

clinical operations have increased faster than other

functions in China pharma industry in recent 2 years…

around 25-40% of salary increase when moving to the

next position with the same title

– HR of leading China based-biotechs

Potential solutions

▪ Bringing oversea TA physicians

with experience and know-how

– Potential challenges include

language barrier and

interaction with local KOLs

▪ Accelerate training of local

talent

– For example, companies can

provide rigorous training

curriculum on clinical trial

practice, and rotation talents

across trial phases to build

individual capability

▪ Industry-wide training program

– In collaboration with academic

institutions (e.g., Shenyang

Pharmaceutical University and

China Pharmaceutical

University)

Supply

Demand1

800-1,000

1,300-1,600

1 Estimated based on the number of clinical trial growth with optimal TA physicians/trial ratio breakdown by innovative vs. generic drugs

“

64McKinsey & Company

Looking into the crystal ball – what is the 3-5 year future of China biotech

industry?

Positive momentum continues: Expect significant progress on the

overall innovation level, yet still with major gap compared to the US

Emerging global presence: A handful of companies and

assets will reach global stage

Market will tell: Market will be the gold standard for biotech pioneers and

the China innovation model (step wise approach, license in arbitrage,

etc.) as part of building a healthy industry

Funding cycle expected: Investment will likely be more

cautious before a bounce back as we witness the failures

and success of early pipelines

65McKinsey & Company

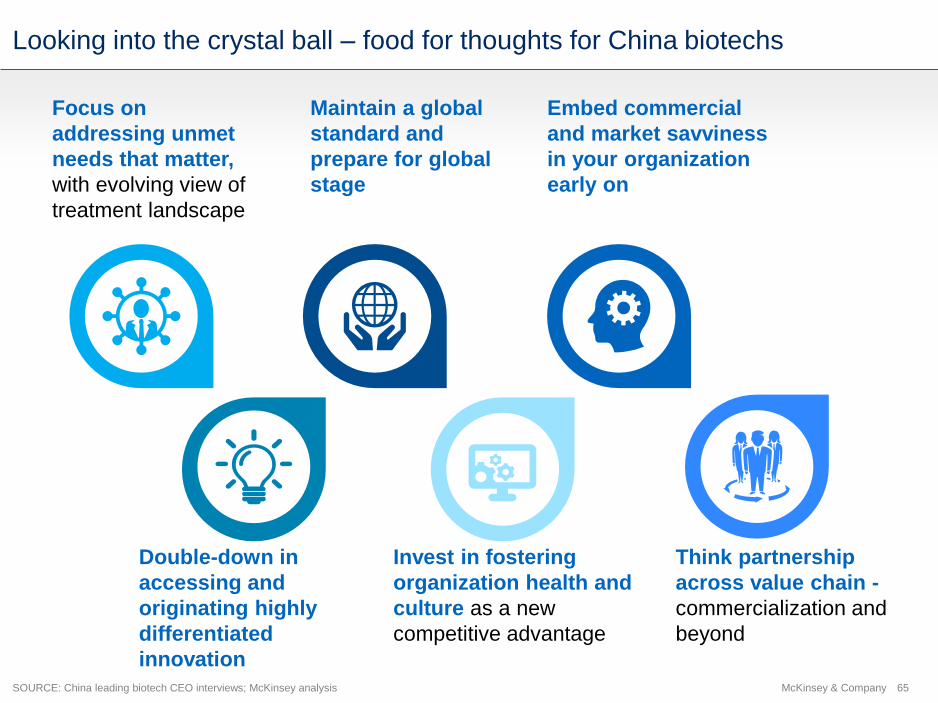

Looking into the crystal ball – food for thoughts for China biotechs

Double-down in

accessing and

originating highly

differentiated

innovation

Maintain a global

standard and

prepare for global

stage

Invest in fostering

organization health and

culture as a new

competitive advantage

Focus on

addressing unmet

needs that matter,

with evolving view of

treatment landscape

Think partnership

across value chain -

commercialization and

beyond

Embed commercial

and market savviness

in your organization

early on

SOURCE: China leading biotech CEO interviews; McKinsey analysis

66McKinsey & Company

4 key

questions to

explore …

Impact of Digital

and Analytics?

Momentum of the

innovation drive?

Speed of improvement

in market access?

Macro market

evolution? 01

02

03

04

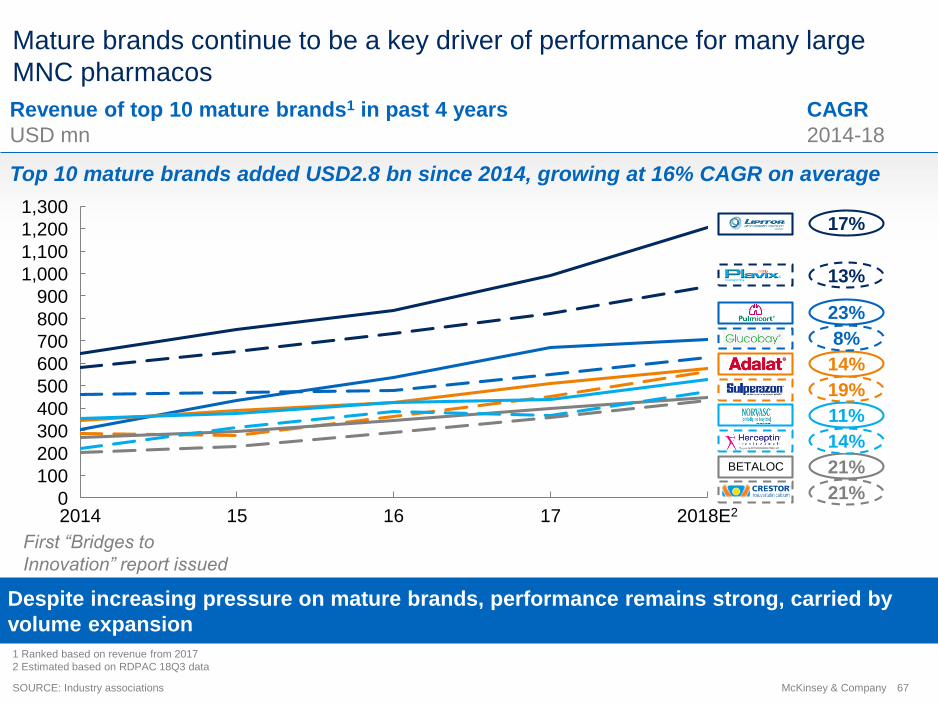

67McKinsey & Company

Mature brands continue to be a key driver of performance for many large

MNC pharmacos

172014 15 16

1,200

2018E20

100

200

300

400

500

600

700

800

900

1,000

1,100

1,300

Despite increasing pressure on mature brands, performance remains strong, carried by

volume expansion

Revenue of top 10 mature brands1 in past 4 years

USD mn

SOURCE: Industry associations

1 Ranked based on revenue from 2017

2 Estimated based on RDPAC 18Q3 data

CAGR

2014-18

21%

21%

14%

11%

19%

14%

8%

23%

13%

17%

First “Bridges to

Innovation” report issued

Top 10 mature brands added USD2.8 bn since 2014, growing at 16% CAGR on average

BETALOC

68McKinsey & Company

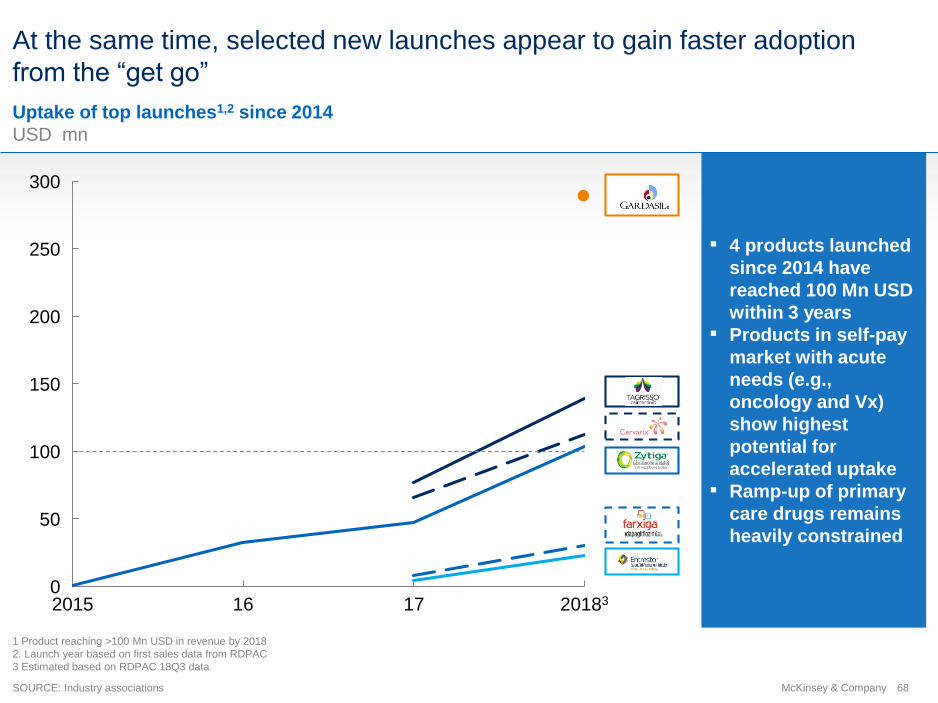

At the same time, selected new launches appear to gain faster adoption

from the “get go”

Uptake of top launches1,2 since 2014

USD mn

1 Product reaching >100 Mn USD in revenue by 2018

2. Launch year based on first sales data from RDPAC

3 Estimated based on RDPAC 18Q3 data

SOURCE: Industry associations

2015 1716 201830

50

100

150

200

250

300

▪ 4 products launched

since 2014 have

reached 100 Mn USD

within 3 years

▪ Products in self-pay

market with acute

needs (e.g.,

oncology and Vx)

show highest

potential for

accelerated uptake

▪ Ramp-up of primary

care drugs remains

heavily constrained

69McKinsey & Company

In this context of evolving access environment, two key questions for the

biopharma industry

Do we believe 2019 will be the year of the

“reckoning” for mature brands given

convergence of new procurement rules,

pricing pressure and GQCE roll-out?

Do we believe that access is expanding fast

enough to support the wave of ~100

innovative drugs hitting the market since

2016, in addition to those included in NRDL??Innovative

portfolio

?Mature

portfolio

1

2

70McKinsey & Company

# of new drug approvals1 in the past 3 years

# of products Examples

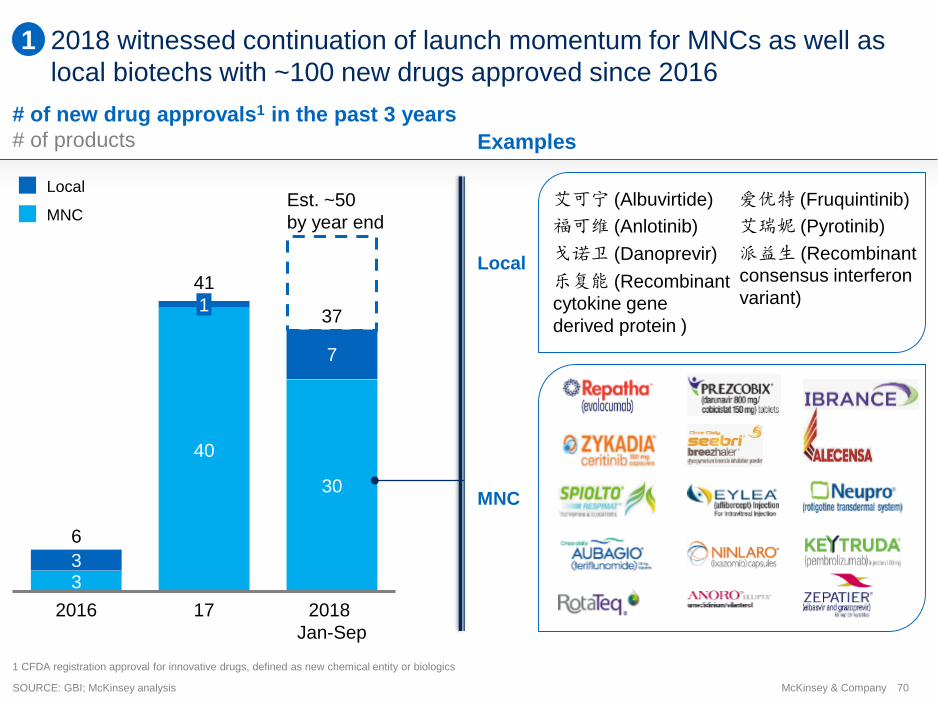

2018 witnessed continuation of launch momentum for MNCs as well as

local biotechs with ~100 new drugs approved since 2016

SOURCE: GBI; McKinsey analysis

1 CFDA registration approval for innovative drugs, defined as new chemical entity or biologics

3

40

30

3

7

172016

1

41

2018

Jan-Sep

6

37

MNC

Local

Local

MNC

戈诺卫 (Danoprevir)

乐复能 (Recombinant

cytokine gene

derived protein )

艾可宁 (Albuvirtide)

艾瑞妮 (Pyrotinib)福可维 (Anlotinib)

爱优特 (Fruquintinib)

派益生 (Recombinant

consensus interferon

variant)

Est. ~50

by year end

1

71McKinsey & Company

NSCLC

Prices of 17 oncology drugs post 2018 NRDL negotiation

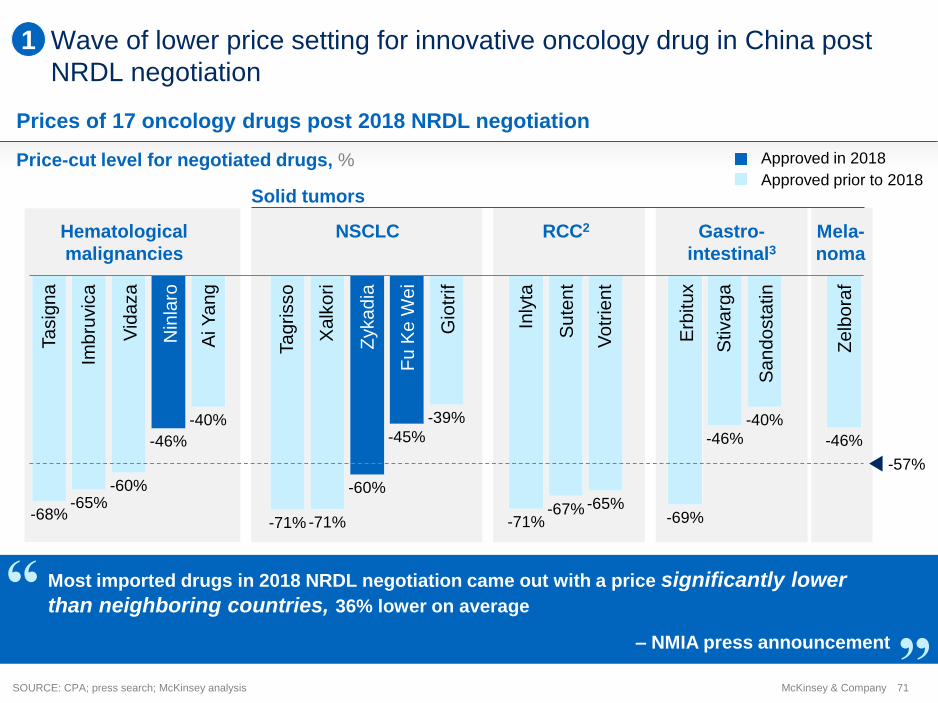

Wave of lower price setting for innovative oncology drug in China post

NRDL negotiation

SOURCE: CPA; press search; McKinsey analysis

1

Price-cut level for negotiated drugs, %

-46%

-68%

-57%

-65%

-46%

-60%

-40%

-71% -71%

-60%

-45%

-67%

-39%

-71%-65%

-69%

-46%-40%

Ta

sig

na

Imb

ruvic

a

Vid

aza

Nin

laro

Ai Y

an

g

Ta

grisso

Xa

lko

ri

Gio

trif

Inly

ta

Su

ten

t

Vo

trie

nt

Erb

itu

x

Stiva

rga

Sa

nd

osta

tin

Zelb

ora

f

Approved in 2018

Approved prior to 2018

Hematological

malignancies

Solid tumors

RCC2 Gastro-

intestinal3

Most imported drugs in 2018 NRDL negotiation came out with a price significantly lower

than neighboring countries, 36% lower on average

– NMIA press announcement

Zyka

dia

Fu

Ke

We

i

Mela-

noma

72McKinsey & Company

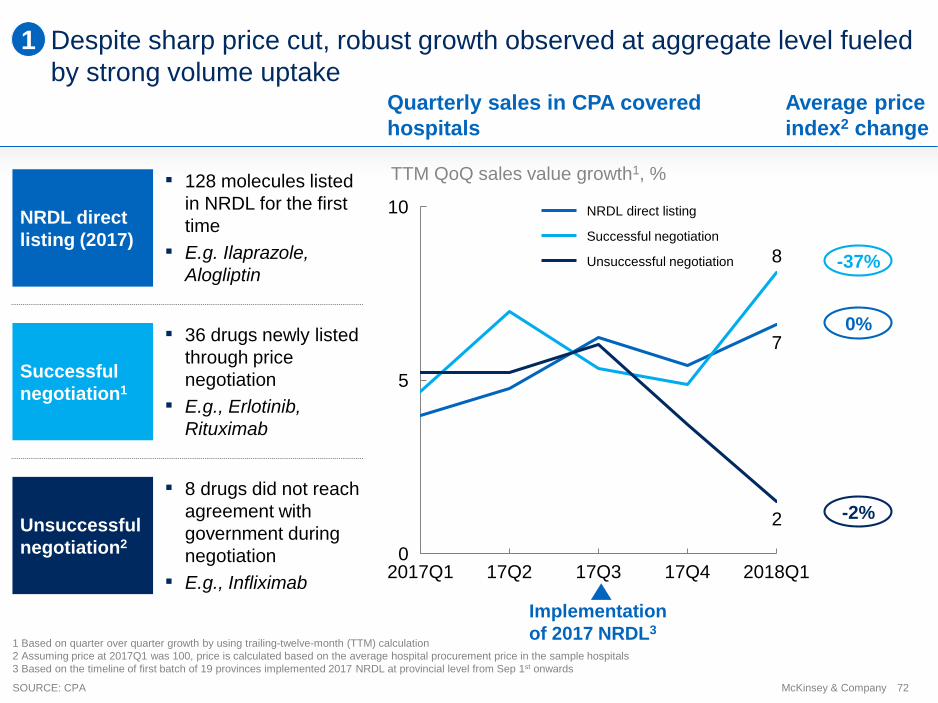

NRDL direct

listing (2017)

▪ 128 molecules listed

in NRDL for the first

time

▪ E.g. Ilaprazole,

Alogliptin

Successful

negotiation1

▪ 36 drugs newly listed

through price

negotiation

▪ E.g., Erlotinib,

Rituximab

Unsuccessful

negotiation2

▪ 8 drugs did not reach

agreement with

government during

negotiation

▪ E.g., Infliximab

Despite sharp price cut, robust growth observed at aggregate level fueled

by strong volume uptake

7

8

2

0

5

10

2018Q117Q32017Q1 17Q2 17Q4

NRDL direct listing

Successful negotiation

Unsuccessful negotiation -37%

1 Based on quarter over quarter growth by using trailing-twelve-month (TTM) calculation

2 Assuming price at 2017Q1 was 100, price is calculated based on the average hospital procurement price in the sample hospitals

3 Based on the timeline of first batch of 19 provinces implemented 2017 NRDL at provincial level from Sep 1st onwards

Implementation

of 2017 NRDL3

SOURCE: CPA

Average price

index2 change

0%

1

-2%

Quarterly sales in CPA covered

hospitals

TTM QoQ sales value growth1, %

73McKinsey & Company

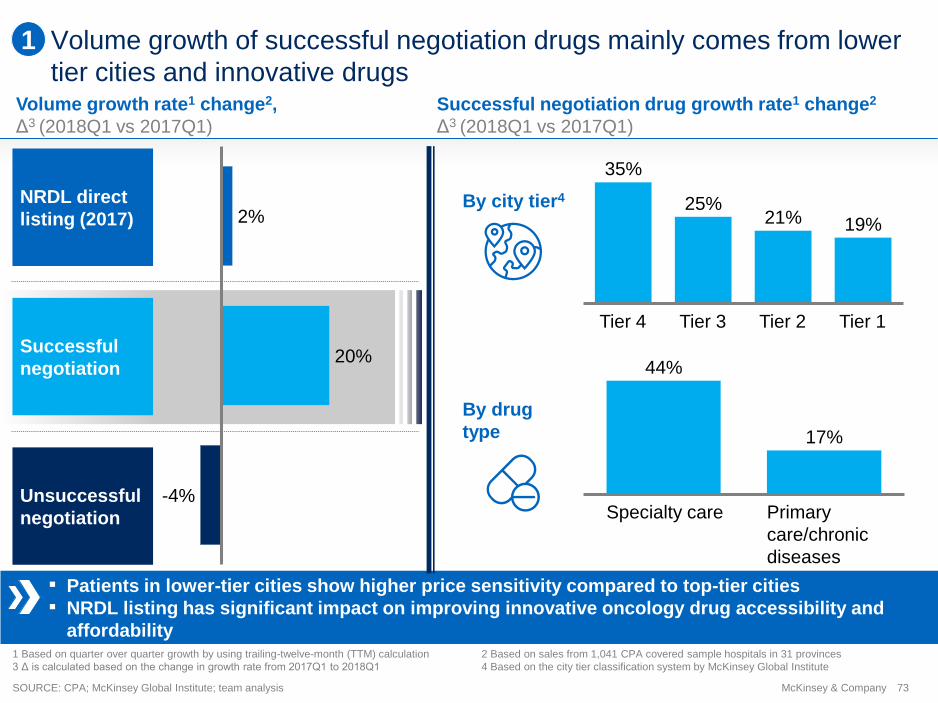

Volume growth of successful negotiation drugs mainly comes from lower

tier cities and innovative drugs

▪ Patients in lower-tier cities show higher price sensitivity compared to top-tier cities

▪ NRDL listing has significant impact on improving innovative oncology drug accessibility and

affordability

2%

20%

-4%

19%

Tier 2Tier 4 Tier 1Tier 3

21%25%

35%

Specialty care Primary

care/chronic

diseases

44%

17%

By city tier4

By drug

type

Volume growth rate1 change2,

Δ3 (2018Q1 vs 2017Q1)

Successful negotiation drug growth rate1 change2

Δ3 (2018Q1 vs 2017Q1)

SOURCE: CPA; McKinsey Global Institute; team analysis

1

NRDL direct

listing (2017)

Successful

negotiation

Unsuccessful

negotiation

1 Based on quarter over quarter growth by using trailing-twelve-month (TTM) calculation 2 Based on sales from 1,041 CPA covered sample hospitals in 31 provinces

3 Δ is calculated based on the change in growth rate from 2017Q1 to 2018Q1 4 Based on the city tier classification system by McKinsey Global Institute

74McKinsey & Company

2017 NRDL national negotiation is on track for local implementation

SOURCE: Literature research; PDB Database; McKinsey analysis

1

Implementation

timeline

Local reimbursement

Procurement

Clinical use

▪ By December 2017, all 31

provinces had included

negotiated drugs under

PRDL list B

▪ 14 provinces set up OOP

from 20% to 50%

▪ Rest of provinces allowed

city/county gov’t to set OOP

by their own

▪ Guangzhou and Beijing

also offer coverage for

outpatient reimbursement

▪ 12+ provinces (i.e.

Guangdong, Tianjin,

Chongqing) removed

restriction of drug sales

ratio for negotiated drugs

▪ Strong supervision to

ensure rational

prescription in line with

indication restriction for

reimbursement

▪ Negotiated

drugs are

eligible for

direct online

procurement

in most regions

(e.g. Shaanxi,

Anhui, Jilin)

75McKinsey & Company

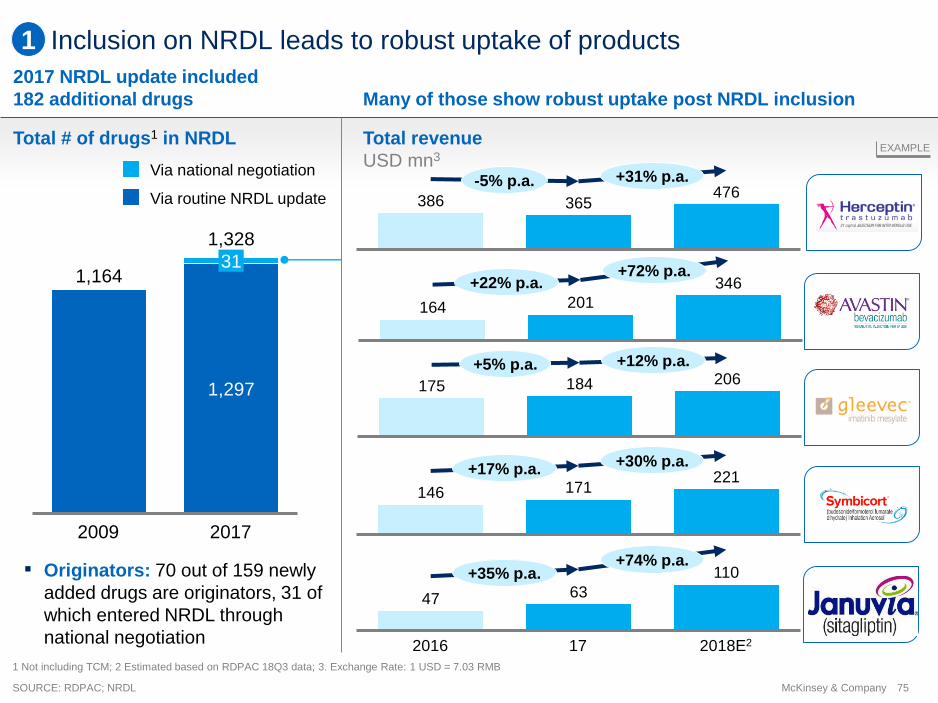

Inclusion on NRDL leads to robust uptake of products

SOURCE: RDPAC; NRDL

Many of those show robust uptake post NRDL inclusion

386 365476

-5% p.a. +31% p.a.

47 63

110

2018E22016 17

+35% p.a.+74% p.a.

164 201

346+22% p.a.+72% p.a.

Total revenue

USD mn3

175 184 206+5% p.a. +12% p.a.

146 171221

+17% p.a.+30% p.a.

2017 NRDL update included

182 additional drugs

1 Not including TCM; 2 Estimated based on RDPAC 18Q3 data; 3. Exchange Rate: 1 USD = 7.03 RMB

EXAMPLE

1,164

1,297

2009

1,328

31

2017

Via national negotiation

Via routine NRDL update

▪ Originators: 70 out of 159 newly

added drugs are originators, 31 of

which entered NRDL through

national negotiation

Total # of drugs1 in NRDL

1

76McKinsey & Company

First EDL update since 2012, with many target therapies/ non-NRDL listed

drugs included, revealing authorities’ priority shifting toward clinical value

317

417

203

268

2018

EDL

2012

EDL

520

TCM

685

Western

Medicine

▪ 187 newly added drugs

▪ 22 drugs removed

Highlight of newly added drugs# of drugs included in EDL

Non-NRDL listed

drugs included

11 drugs not

reimbursable

currently were picked

up

Targeted

therapies

included

12 oncology drugs

listed, incl. 6 TKIs

CVS and Metabolic

drugs count for

25% of all newly

added drugs

Better aligned

with disease

burden

SOURCE: National Health Commission

1

77McKinsey & Company

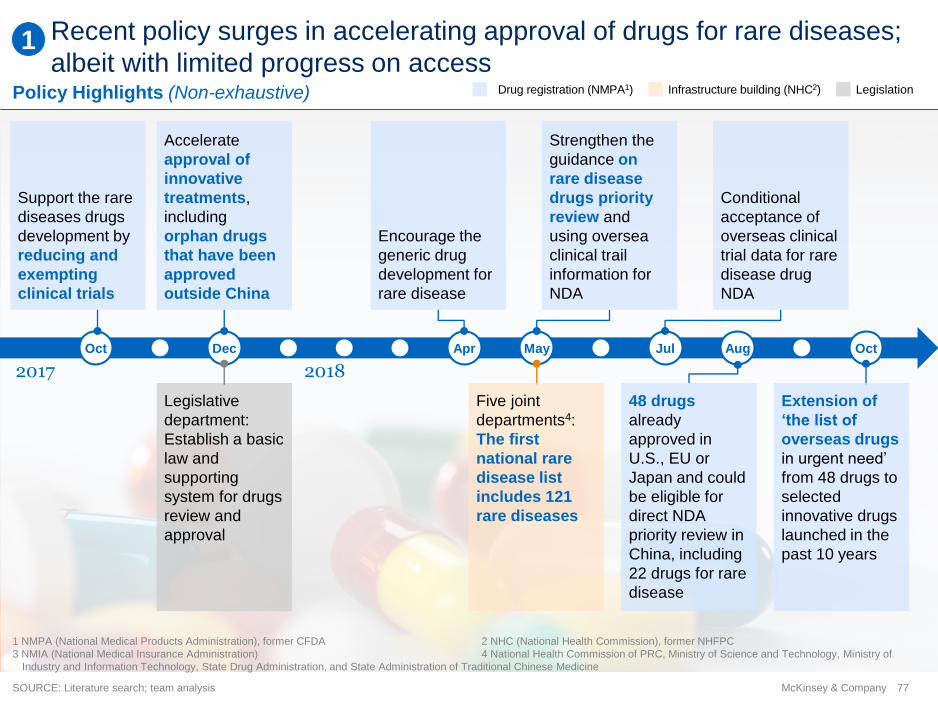

Recent policy surges in accelerating approval of drugs for rare diseases;

albeit with limited progress on access

1 NMPA (National Medical Products Administration), former CFDA 2 NHC (National Health Commission), former NHFPC

3 NMIA (National Medical Insurance Administration) 4 National Health Commission of PRC, Ministry of Science and Technology, Ministry of

Industry and Information Technology, State Drug Administration, and State Administration of Traditional Chinese Medicine

SOURCE: Literature search; team analysis

Infrastructure building (NHC2) Legislation Drug registration (NMPA1)Policy Highlights (Non-exhaustive)

Support the rare

diseases drugs

development by

reducing and

exempting

clinical trials

Accelerate

approval of

innovative

treatments,

including

orphan drugs

that have been

approved

outside China

Encourage the

generic drug

development for

rare disease

Strengthen the

guidance on

rare disease

drugs priority

review and

using oversea

clinical trail

information for

NDA

Conditional

acceptance of

overseas clinical

trial data for rare

disease drug

NDA

Legislative

department:

Establish a basic

law and

supporting

system for drugs

review and

approval

2017 2018

Oct Dec Apr May Jul Aug Oct

1

48 drugs

already

approved in

U.S., EU or

Japan and could

be eligible for

direct NDA

priority review in

China, including

22 drugs for rare

disease

Extension of

‘the list of

overseas drugs

in urgent need’

from 48 drugs to

selected

innovative drugs

launched in the

past 10 years

Five joint

departments4:

The first

national rare

disease list

includes 121

rare diseases

78McKinsey & Company

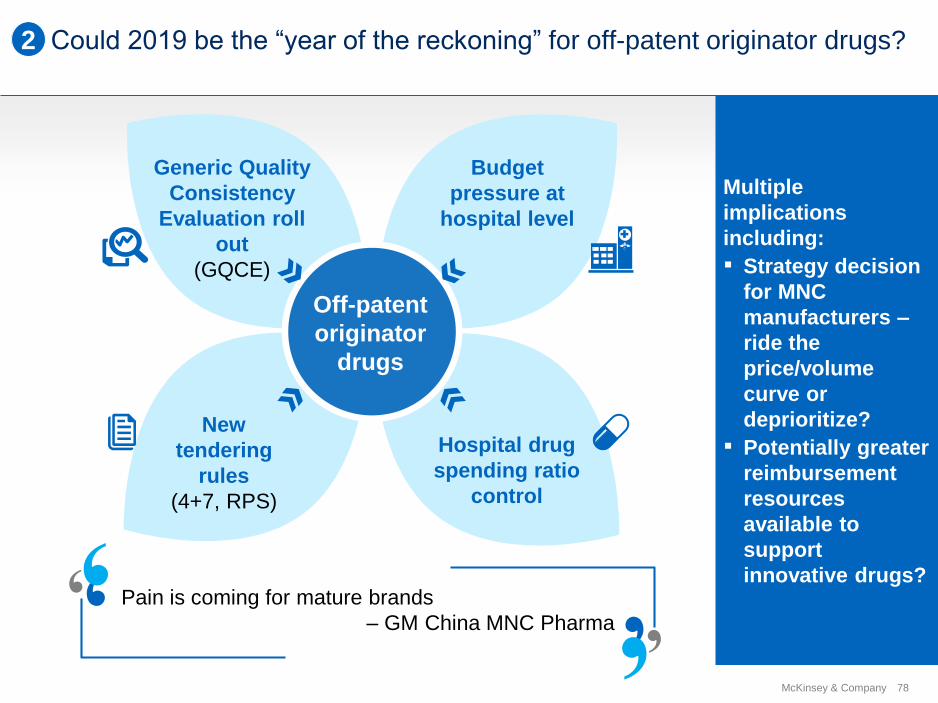

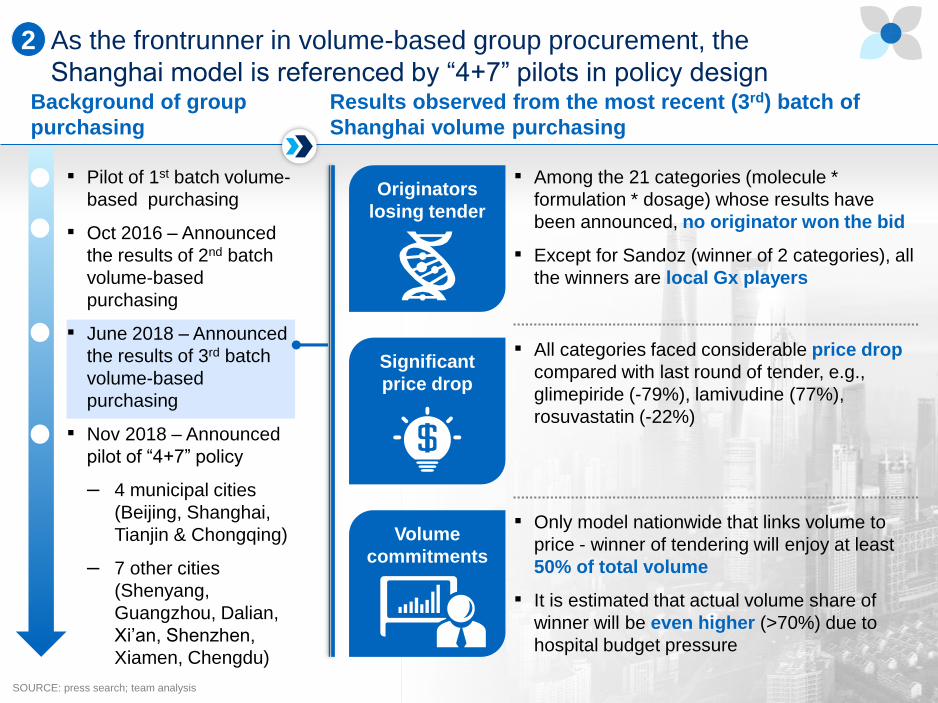

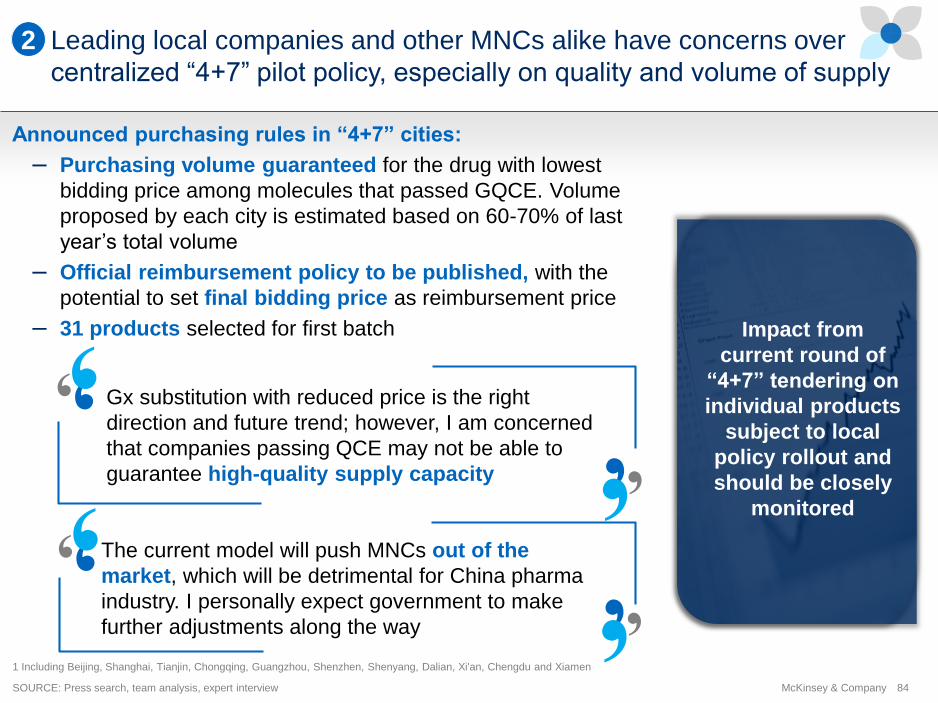

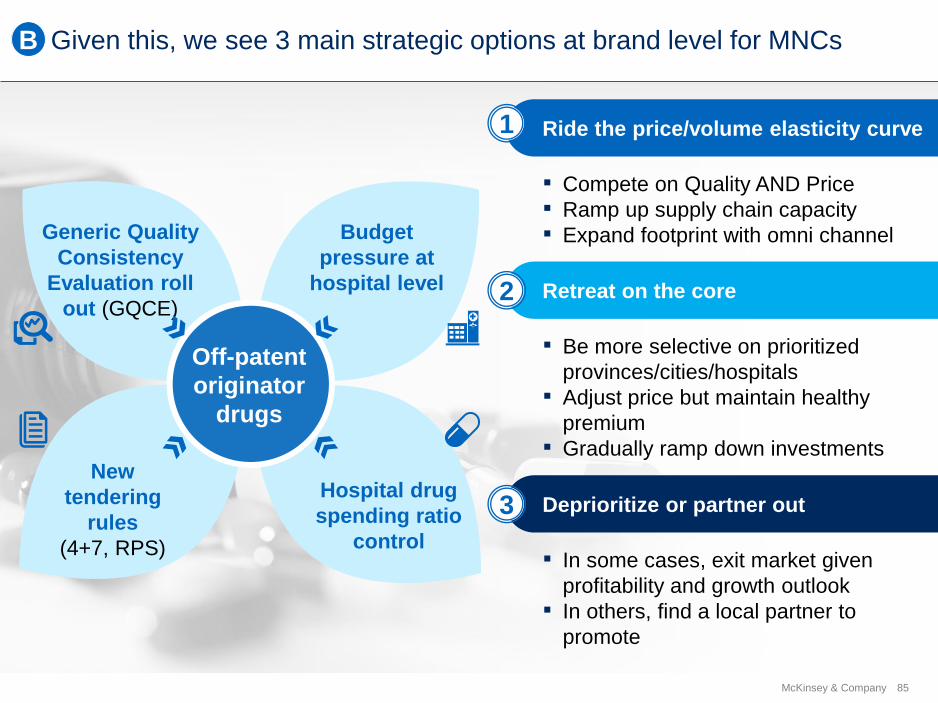

Could 2019 be the “year of the reckoning” for off-patent originator drugs?

Multiple

implications

including:

▪ Strategy decision

for MNC

manufacturers –

ride the

price/volume

curve or

deprioritize?

▪ Potentially greater

reimbursement

resources

available to

support

innovative drugs?

2

Hospital drug

spending ratio

control

Generic Quality

Consistency

Evaluation roll

out

(GQCE)

Budget

pressure at

hospital level

New

tendering

rules

(4+7, RPS)

Off-patent

originator

drugs

Pain is coming for mature brands

– GM China MNC Pharma

79McKinsey & Company

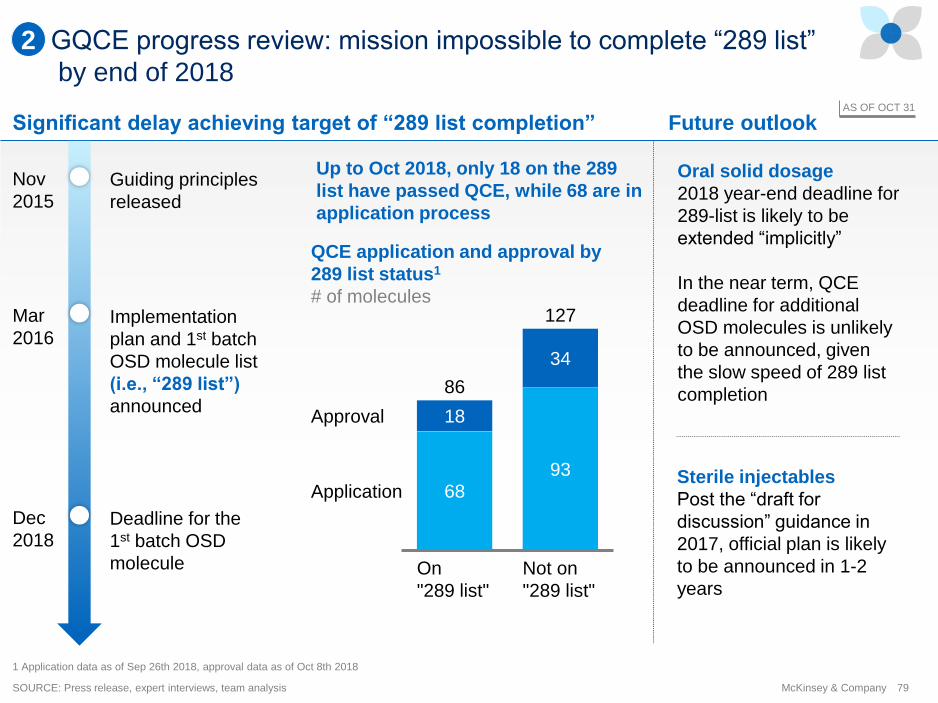

GQCE progress review: mission impossible to complete “289 list”

by end of 2018

QCE application and approval by

289 list status1

# of molecules

Up to Oct 2018, only 18 on the 289

list have passed QCE, while 68 are in

application process

Significant delay achieving target of “289 list completion” Future outlook

1 Application data as of Sep 26th 2018, approval data as of Oct 8th 2018

Oral solid dosage

2018 year-end deadline for

289-list is likely to be

extended “implicitly”

In the near term, QCE

deadline for additional

OSD molecules is unlikely

to be announced, given

the slow speed of 289 list

completion

Sterile injectables

Post the “draft for

discussion” guidance in

2017, official plan is likely

to be announced in 1-2

years

Deadline for the

1st batch OSD

molecule

Dec

2018

Mar

2016Implementation

plan and 1st batch

OSD molecule list

(i.e., “289 list”)

announced

Nov

2015

Guiding principles

released

2

6893

18

34

127

On

"289 list"

Not on

"289 list"

Approval

86

Application

SOURCE: Press release, expert interviews, team analysis

AS OF OCT 31

80McKinsey & Company

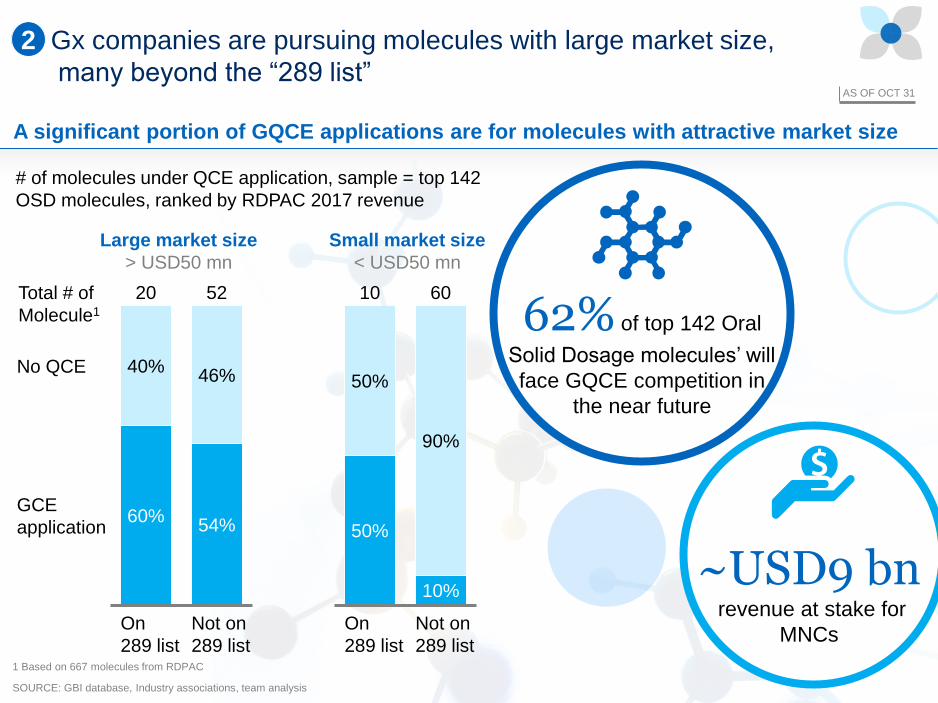

Gx companies are pursuing molecules with large market size,

many beyond the “289 list”

SOURCE: GBI database, Industry associations, team analysis

2

Large market size

> USD50 mn

Small market size

< USD50 mn

# of molecules under QCE application, sample = top 142

OSD molecules, ranked by RDPAC 2017 revenue

A significant portion of GQCE applications are for molecules with attractive market size

60%54%

40%46%

Total # of

Molecule1

Not on

289 list

On

289 list

No QCE

GCE

application

20 52

50%

10%

50%

90%

Not on

289 list

On

289 list

10 60

1 Based on 667 molecules from RDPAC

AS OF OCT 31

62% of top 142 Oral

Solid Dosage molecules’ will

face GQCE competition in

the near future

~USD9 bnrevenue at stake for

MNCs

81McKinsey & Company

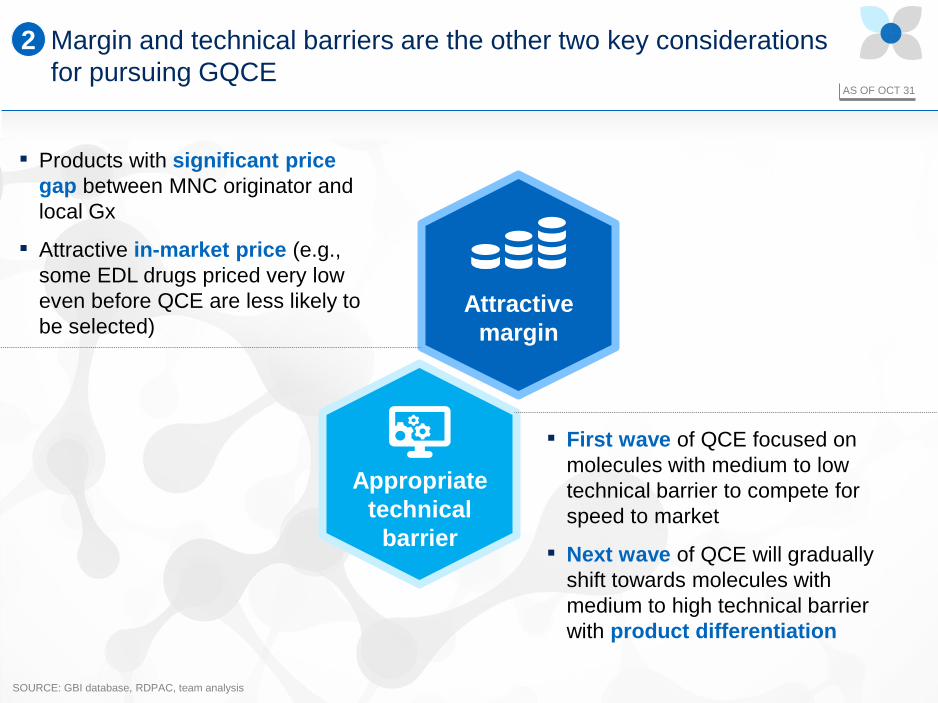

Margin and technical barriers are the other two key considerations

for pursuing GQCE

SOURCE: GBI database, RDPAC, team analysis

2

▪ Products with significant price

gap between MNC originator and

local Gx

▪ Attractive in-market price (e.g.,

some EDL drugs priced very low

even before QCE are less likely to

be selected)

▪ First wave of QCE focused on

molecules with medium to low

technical barrier to compete for

speed to market

▪ Next wave of QCE will gradually

shift towards molecules with

medium to high technical barrier

with product differentiation

AS OF OCT 31

Attractive

margin

Appropriate

technical

barrier

82McKinsey & Company

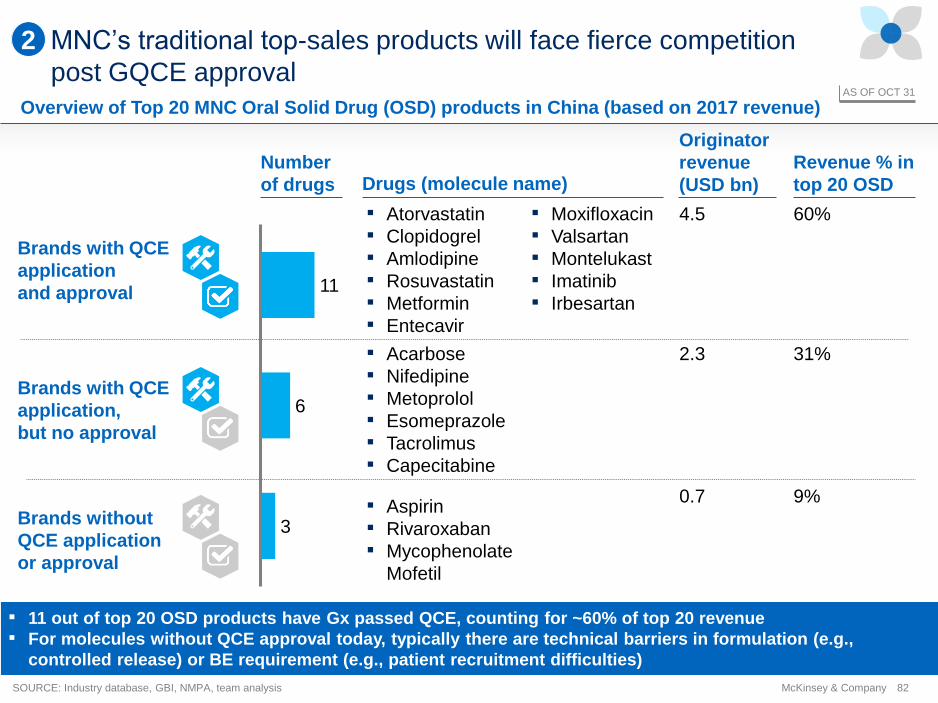

MNC’s traditional top-sales products will face fierce competition

post GQCE approval

2

AS OF OCT 31

Number