Embed Size (px)

Citation preview

For Use at Unconstrained Fixed Income Summit Only. Not for Further Distribution.For Use at Unconstrained Fixed Income Summit Only. Not for Further Distribution.

Building a Resilient Fixed Income Portfolio

for all Stages of the Economic Cycle

For Use at Unconstrained Fixed Income Summit Only. Not for Further Distribution.

Matthew J. Eagan, CFA, Vice President and Portfolio Manager, Fixed Income, Loomis, Sayles & Company

Kevin P. Kearns, Vice President, Portfolio Manager & Senior Derivatives Strategist, Absolute Return and Credit, Loomis, Sayles &

Company

For Use at Unconstrained Fixed Income Summit Only. Not for Further Distribution.

2

Survey Question 1

What is the role of unconstrained fixed income in

a portfolio?

1. To outperform in a rising rate environment

2. To protect capital in a downturn

3. To provide attractive, uncorrelated return

For Use at Unconstrained Fixed Income Summit Only. Not for Further Distribution.

3

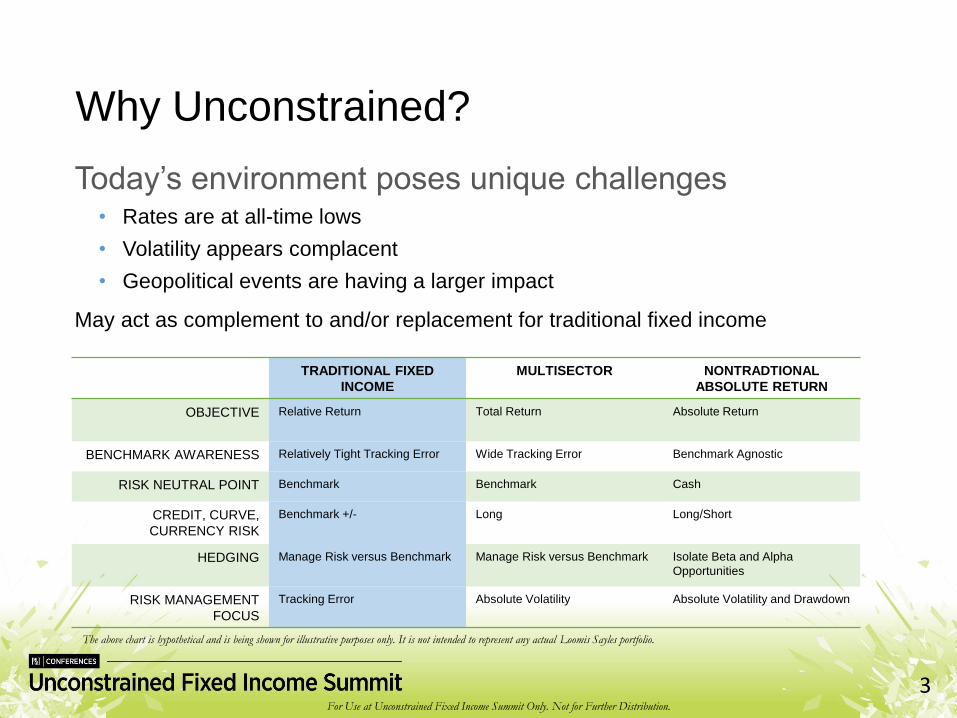

Why Unconstrained?

Today’s environment poses unique challenges • Rates are at all-time lows

• Volatility appears complacent

• Geopolitical events are having a larger impact

May act as complement to and/or replacement for traditional fixed income

TRADITIONAL FIXED

INCOME

MULTISECTOR NONTRADTIONAL

ABSOLUTE RETURN

OBJECTIVE Relative Return Total Return Absolute Return

BENCHMARK AWARENESS Relatively Tight Tracking Error Wide Tracking Error Benchmark Agnostic

RISK NEUTRAL POINT Benchmark Benchmark Cash

CREDIT, CURVE,

CURRENCY RISK

Benchmark +/- Long Long/Short

HEDGING Manage Risk versus Benchmark Manage Risk versus Benchmark Isolate Beta and Alpha

Opportunities

RISK MANAGEMENT

FOCUS

Tracking Error Absolute Volatility Absolute Volatility and Drawdown

The above chart is hypothetical and is being shown for illustrative purposes only. It is not intended to represent any actual Loomis Sayles portfolio.

For Use at Unconstrained Fixed Income Summit Only. Not for Further Distribution.

4

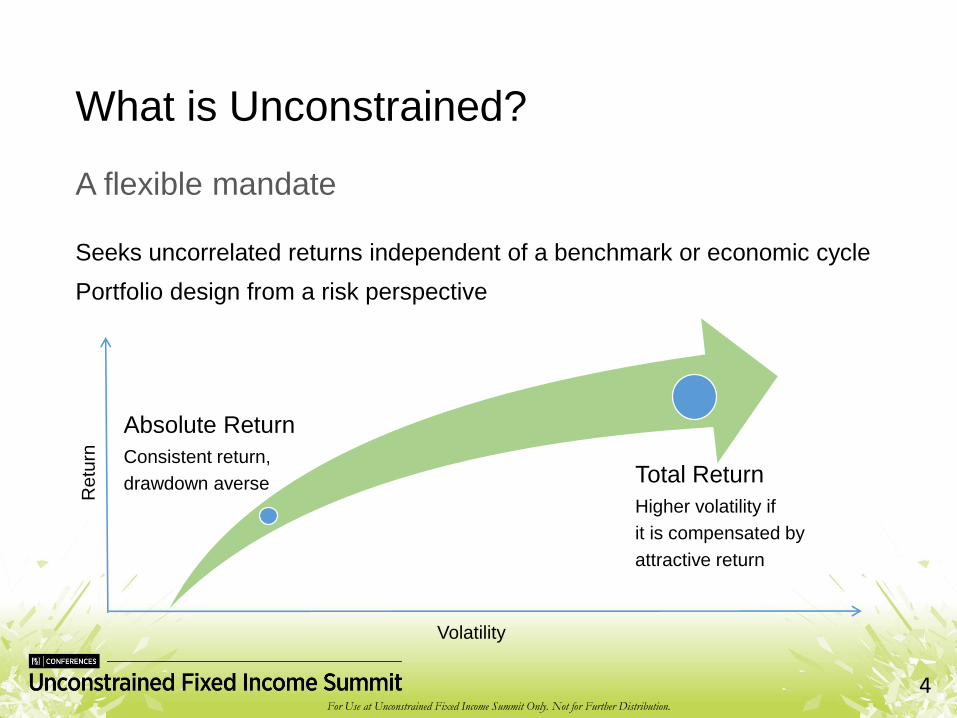

What is Unconstrained?

A flexible mandate

Seeks uncorrelated returns independent of a benchmark or economic cycle

Portfolio design from a risk perspective

Absolute Return

Consistent return,

drawdown averse Total Return

Higher volatility if

it is compensated by

attractive return

Re

turn

Volatility

For Use at Unconstrained Fixed Income Summit Only. Not for Further Distribution.

5

Alpha Generation

Three legs of the stool

1) Beta Selection

2) Idiosyncratic Selection with better information or a better process

• Fundamental research

• Quantitative analysis

• Technical analysis

3) Exploit Structural Inefficiencies

• Illiquidity

• Seasonality

• Basis or pair trades

For Use at Unconstrained Fixed Income Summit Only. Not for Further Distribution.

6

Survey Question 2

What stage of the economic cycle are we currently in?

1. Downturn

2. Credit Repair

3. Recovery

4. Expansion / Late Cycle

For Use at Unconstrained Fixed Income Summit Only. Not for Further Distribution.

7

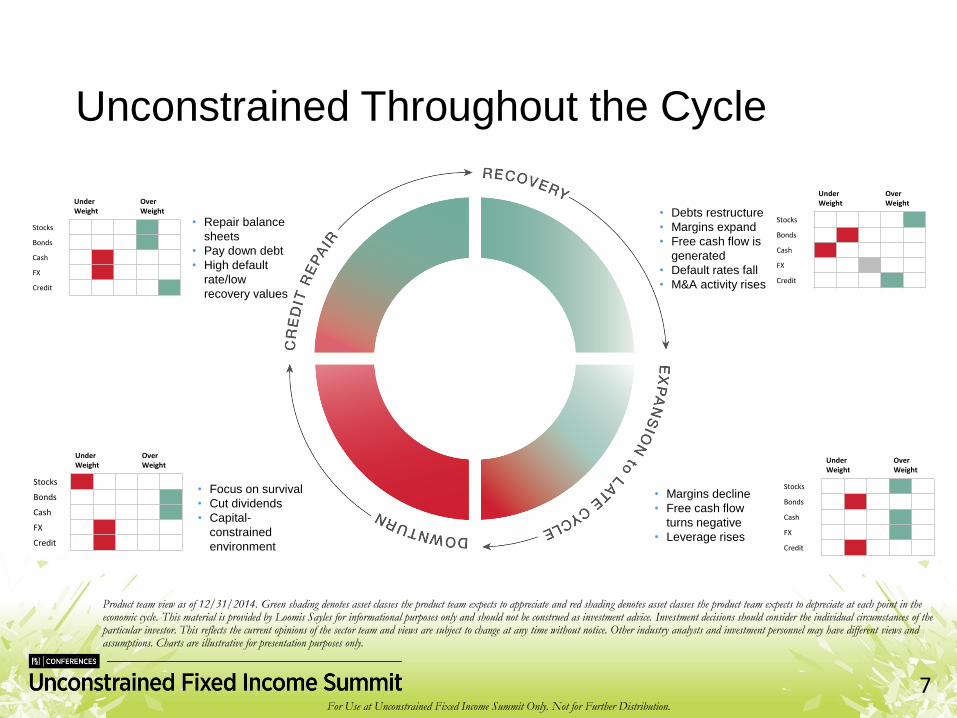

Under Weight

OverWeight

Stocks

Bonds

Cash

FX

Credit

Under Weight

OverWeight

Stocks

Bonds

Cash

FX

Credit

Under Weight

OverWeight

Stocks

Bonds

Cash

FX

Credit

Under Weight

OverWeight

Stocks

Bonds

Cash

FX

Credit

Product team view as of 12/31/2014. Green shading denotes asset classes the product team expects to appreciate and red shading denotes asset classes the product team expects to depreciate at each point in the economic cycle. This material is provided by Loomis Sayles for informational purposes only and should not be construed as investment advice. Investment decisions should consider the individual circumstances of the particular investor. This reflects the current opinions of the sector team and views are subject to change at any time without notice. Other industry analysts and investment personnel may have different views and assumptions. Charts are illustrative for presentation purposes only.

Unconstrained Throughout the Cycle

• Margins decline

• Free cash flow

turns negative

• Leverage rises

• Focus on survival

• Cut dividends

• Capital-

constrained

environment

• Repair balance

sheets

• Pay down debt

• High default

rate/low

recovery values

• Debts restructure

• Margins expand

• Free cash flow is

generated

• Default rates fall

• M&A activity rises

For Use at Unconstrained Fixed Income Summit Only. Not for Further Distribution.

8

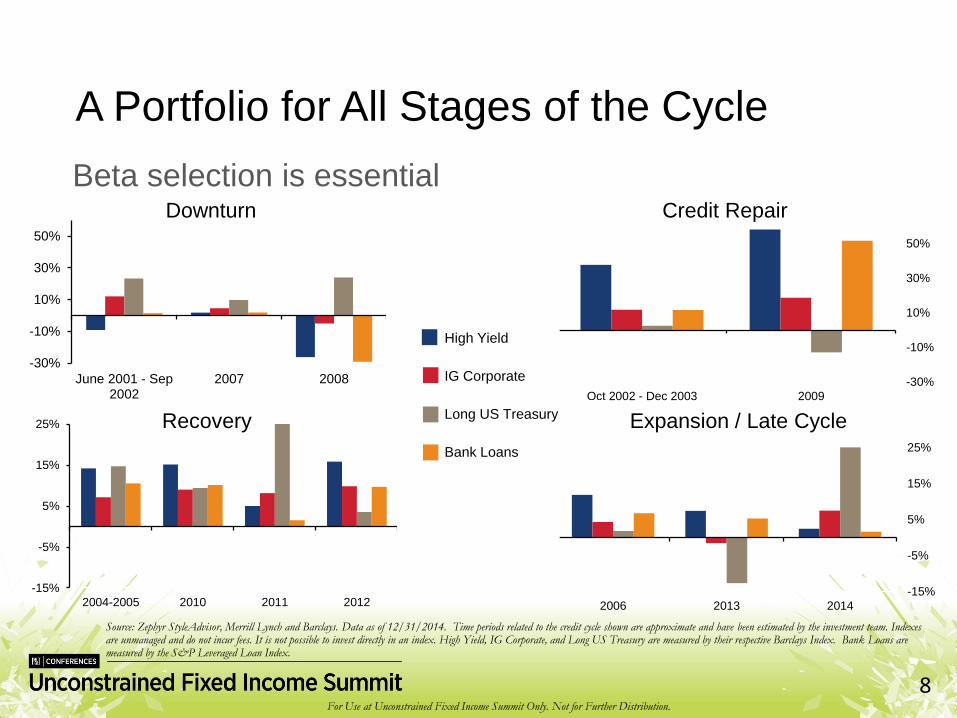

-15%

-5%

5%

15%

25%

2006 2013 2014

-15%

-5%

5%

15%

25%

2004-2005 2010 2011 2012

-30%

-10%

10%

30%

50%

Oct 2002 - Dec 2003 2009

-30%

-10%

10%

30%

50%

June 2001 - Sep2002

2007 2008

Beta selection is essential

A Portfolio for All Stages of the Cycle

Source: Zephyr StyleAdvisor, Merrill Lynch and Barclays. Data as of 12/31/2014. Time periods related to the credit cycle shown are approximate and have been estimated by the investment team. Indexes are unmanaged and do not incur fees. It is not possible to invest directly in an index. High Yield, IG Corporate, and Long US Treasury are measured by their respective Barclays Index. Bank Loans are measured by the S&P Leveraged Loan Index.

Downturn Credit Repair

Expansion / Late CycleRecovery

High Yield

IG Corporate

Long US Treasury

Bank Loans

For Use at Unconstrained Fixed Income Summit Only. Not for Further Distribution.

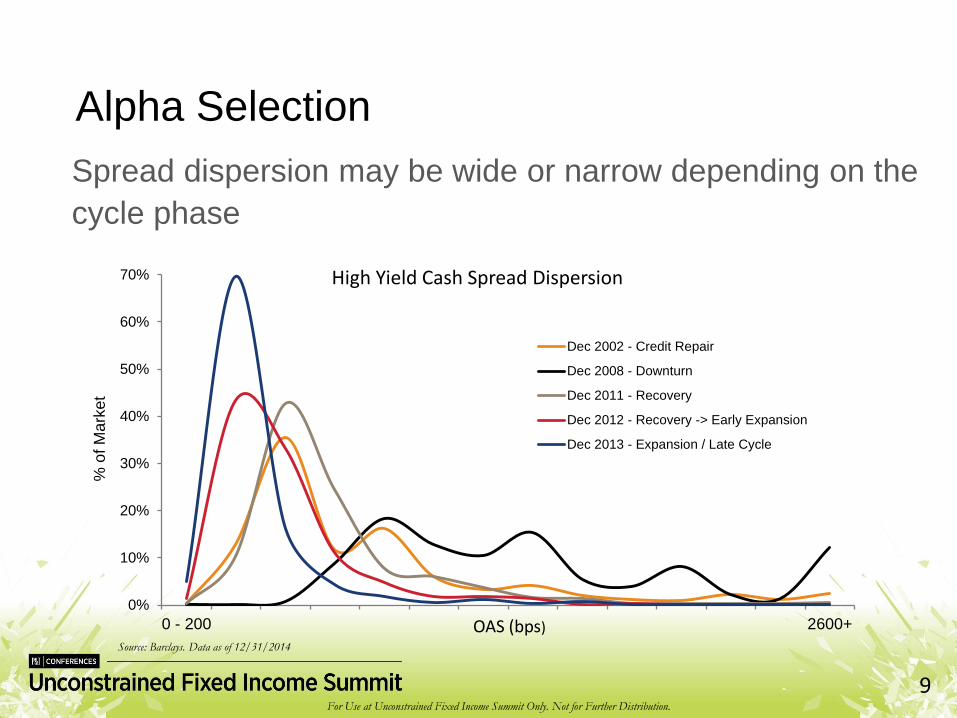

9

Alpha Selection

Spread dispersion may be wide or narrow depending on the

cycle phase

0%

10%

20%

30%

40%

50%

60%

70%

0 - 200 2600+

Dec 2002 - Credit Repair

Dec 2008 - Downturn

Dec 2011 - Recovery

Dec 2012 - Recovery -> Early Expansion

Dec 2013 - Expansion / Late Cycle

OAS (bps)

% o

f M

ark

et

High Yield Cash Spread Dispersion

Source: Barclays. Data as of 12/31/2014

For Use at Unconstrained Fixed Income Summit Only. Not for Further Distribution.

10

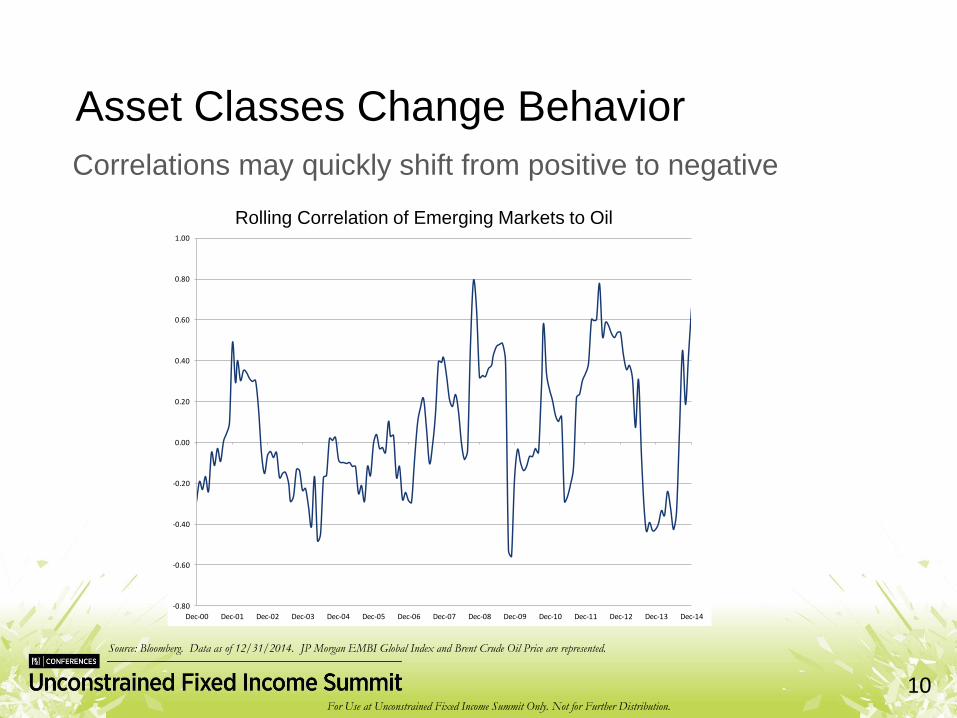

-0.80

-0.60

-0.40

-0.20

0.00

0.20

0.40

0.60

0.80

1.00

Dec-00 Dec-01 Dec-02 Dec-03 Dec-04 Dec-05 Dec-06 Dec-07 Dec-08 Dec-09 Dec-10 Dec-11 Dec-12 Dec-13 Dec-14

Asset Classes Change Behavior

Correlations may quickly shift from positive to negative

Source: Bloomberg. Data as of 12/31/2014. JP Morgan EMBI Global Index and Brent Crude Oil Price are represented.

Rolling Correlation of Emerging Markets to Oil

For Use at Unconstrained Fixed Income Summit Only. Not for Further Distribution.

11

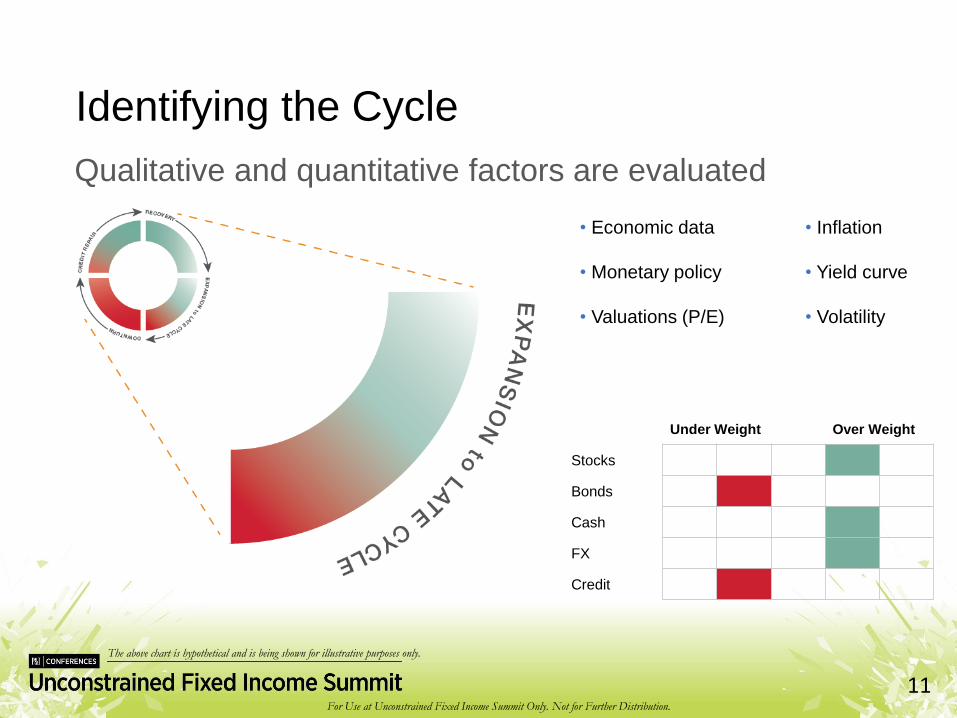

Identifying the Cycle

Qualitative and quantitative factors are evaluated

• Economic data

• Monetary policy

• Valuations (P/E)

• Inflation

• Yield curve

• Volatility

Under Weight Over Weight

Stocks

Bonds

Cash

FX

Credit

The above chart is hypothetical and is being shown for illustrative purposes only.

For Use at Unconstrained Fixed Income Summit Only. Not for Further Distribution.

12

Europe

High Yield

EMBI Global HY

ABS US Large Cap Value

Japan

US Small Cap

Europe IG

Bank Loans

US IG Corp

Convertibles

-10.0

-7.5

-5.0

-2.5

0.0

2.5

5.0

7.5

10.0

12.5

15.0

17.5

20.0

22.5

25.0

27.5

-26.0-24.0-22.0-20.0-18.0-16.0-14.0-12.0-10.0-8.0-6.0-4.0-2.00.02.04.06.0

Valuation tools help identify asset classes with favorable

asymmetric return/risk profiles

Acting on the Cycle

High Yield (491.88)

Targets CurrentInput Date

Downside: 600.00 -1.63 -1.08

Base: 385.00 8.90 9.45

Upside: 325.00 12.05 12.60

Attribution Score (Base/Down): 5.00 5.00

Team “Beta”: 1.00 0.90

Chart is illustrative for presentation purposes only as a sampling of risk management tool output. The information is not intended to represent any actual portfolio.

For Use at Unconstrained Fixed Income Summit Only. Not for Further Distribution.

13

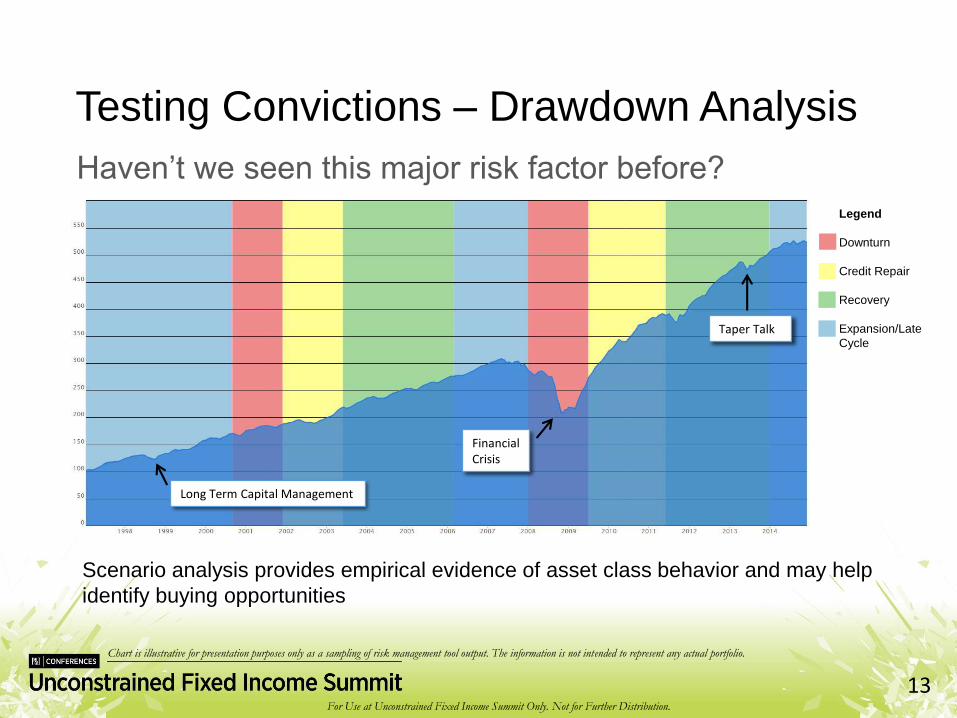

Testing Convictions – Drawdown Analysis

Haven’t we seen this major risk factor before?

Scenario analysis provides empirical evidence of asset class behavior and may help

identify buying opportunities

Long Term Capital Management

Financial Crisis

Taper Talk

Legend

Downturn

Credit Repair

Recovery

Expansion/Late

Cycle

Chart is illustrative for presentation purposes only as a sampling of risk management tool output. The information is not intended to represent any actual portfolio.

For Use at Unconstrained Fixed Income Summit Only. Not for Further Distribution.

14

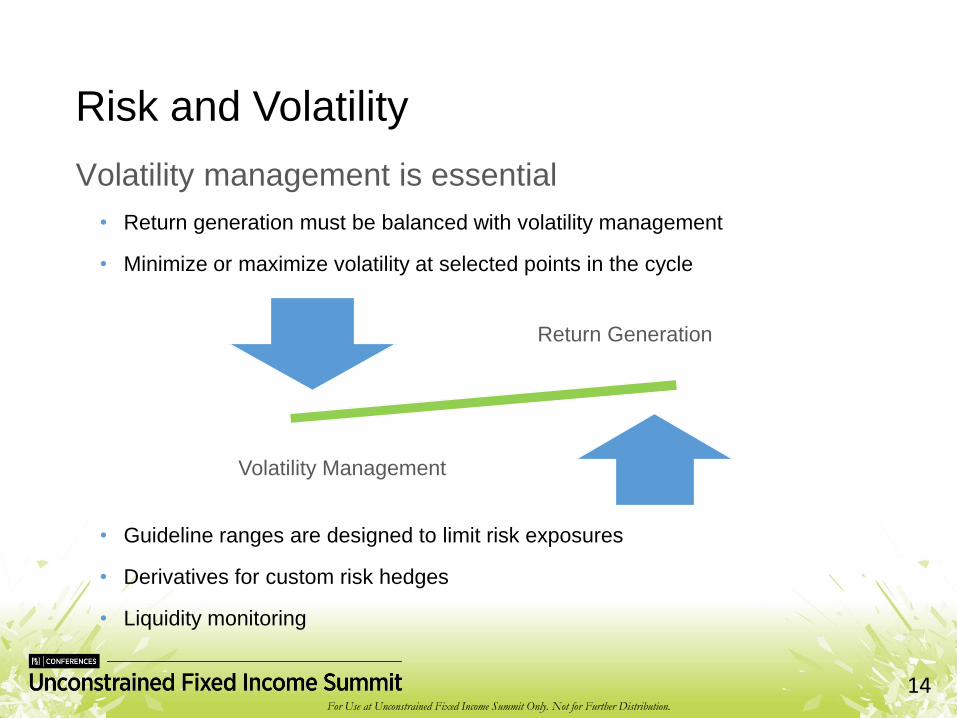

Risk and Volatility

Volatility management is essential

• Return generation must be balanced with volatility management

• Minimize or maximize volatility at selected points in the cycle

• Guideline ranges are designed to limit risk exposures

• Derivatives for custom risk hedges

• Liquidity monitoring

Return Generation

Volatility Management

For Use at Unconstrained Fixed Income Summit Only. Not for Further Distribution.

15

Survey Question 3

What are your risk and return expectations for an

unconstrained mandate?

1. Low volatility, consistent return

2. Moderate volatility, moderate return

3. Higher volatility, higher return

For Use at Unconstrained Fixed Income Summit Only. Not for Further Distribution.

16

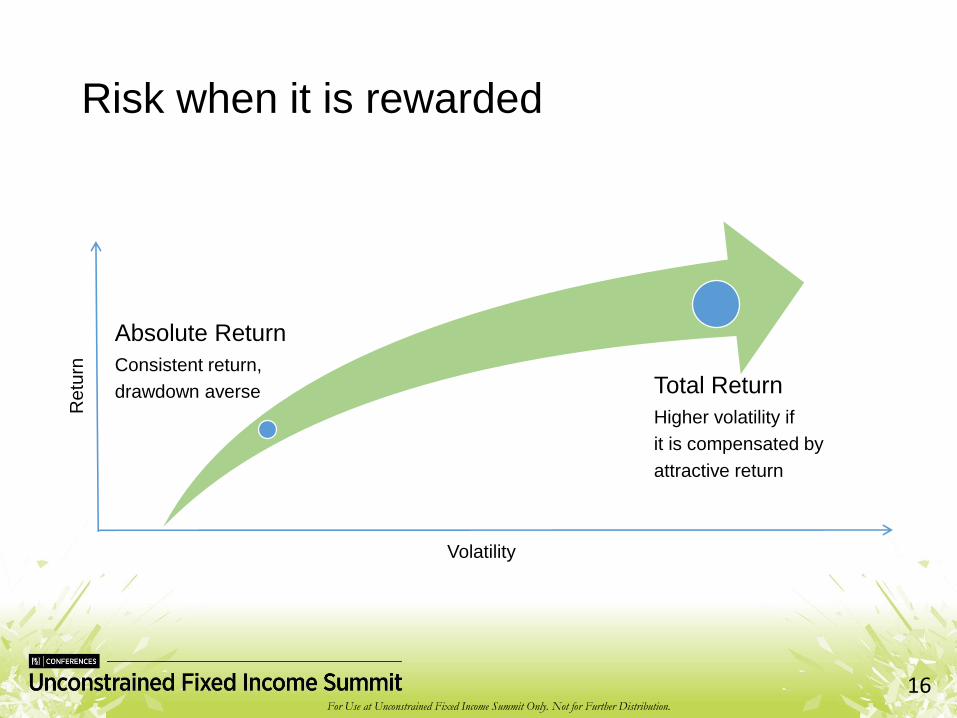

Risk when it is rewarded

Absolute Return

Consistent return,

drawdown averse Total Return

Higher volatility if

it is compensated by

attractive return

Re

turn

Volatility

For Use at Unconstrained Fixed Income Summit Only. Not for Further Distribution.

17

This material is provided for informational purposes only and should not be construed as investment advice. Investment decisions should consider the individual circumstances of the particular investor. Any opinions or forecasts contained herein reflect subjective judgments and assumptions of the author, and do not necessarily reflect the views of Loomis, Sayles & Company, L.P. or any portfolio manager. Investment recommendations may be inconsistent with these opinions. There can be no assurance that developments will transpire as forecasted and actual results will be different. Data and analysis does not represent the actual or expected future performance of any investment product. We believe the information, including that obtained from outside sources, to be correct, but we cannot guarantee its accuracy. Opinions reflect the views of the authors on the date made and are subject to change at any time without notice.