Embed Size (px)

Citation preview

Budget, 2011 & Draft Taxation Laws Amendment Bills –

Personal Income Tax & Savings: Institute of Retirement Funds

5 July 2011

National Treasury

2

Summary

• Consultation process for TLAB

• Changes after the Budget, 2011: Discussion documents

• Tax proposals: Peripheral matters

• Tax proposals: Retirement & long-term insurance

• Conclusion

3

Consultation process for TLAB

• The Taxation Laws Amendment Bills give effect to the tax proposals announced in 2011 February (as contained in Chapter 5 and Annexure C of the Budget Review).

• Bills were published for public comment 2 June 2011:

– SCOF briefing 15 June; hearings 21 & 22 June– Treasury deadline for public comments: 4 July 2011– Treasury workshops with the public: Mid-July– Response document for SCOF in August– Formal introduction of Bill in late August/September

4

Changes after the Budget, 2011

• Retirement tax proposals – discussion documents pending:

– Uniform Retirement Contribution base– Provident funds

• Other peripheral matter – discussion document on medical credit (partial) published

5

• As per the Budget, 2011 the current retirement savings tax incentive will be amended within the broader retirement reform framework regarding:

– The tax treatment of an employer’s contribution on behalf of an employee (inclusion as a fringe benefit).

– Uniform deduction limits for retirement savings (for employees and small business owners).

– Limited deductions for high income earners.

Uniform retirement contribution base

6

• Different options (including the Budget, 2011 option of 22.5%/R200 000) will be presented for public discussion (pending July/August 2011).

Uniform retirement contribution base

7

• Currently, pension and retirement annuity funds allow the retiring member to take 1/3rd as a lump sum and purchase an annuity with the rest.

• Provident funds however, allow the member to take the full amount as a lump sum upon withdrawal.

• To allow this practice to continue will not be in line with Government’s drive to increase household savings.

Uniform retirement withdrawals (ie. provident funds)

8

• Pending discussion document (July 2011):

– To create uniformity and to ensure that retired individuals have sustained sources of income during their retirement years, it is being considered that provident funds be subject to the same withdrawal rules as pension and retirement annuity funds.

– Transitional measures will be provided to protect established rights.

Uniform retirement withdrawals (ie. provident funds)

9

Tax proposals - Peripheral matters

• Introduction of a third rebate of R2000 for individuals 75 years and older.

• Introduction of a medical credit (also refer to the discussion document).

• Adjustments to medical scheme and tax free interest monetary thresholds.

• Amendments to the rates and thresholds for individuals.

10

Tax proposals - Retirement & long-term insurance

• The retirement lump sum & severance benefit tax table

• Transition from a Living Annuity to a RIDDA

• Transfers from a provident or a provident preservation fund to a pension preservation fund.

• Long-term insurance: Employer contributions as a taxable fringe benefit

• Long-term insurance: Taxation of proceeds

• Long-term insurance: Employer key person plans

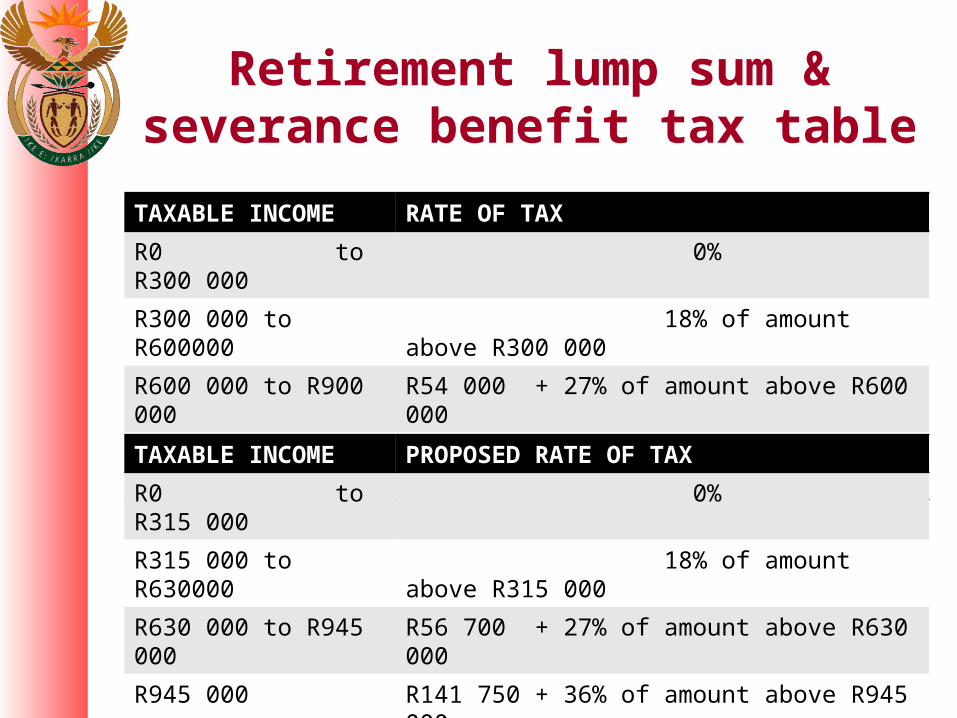

Retirement lump sum & severance benefit tax table

TAXABLE INCOME RATE OF TAX

R0 to R300 000 0%

R300 000 to R600000 18% of amount above R300 000

R600 000 to R900 000 R54 000 + 27% of amount above R600 000

R900 000 R135 000 + 36% of amount above R900 000

11

TAXABLE INCOME PROPOSED RATE OF TAX

R0 to R315 000 0%

R315 000 to R630000 18% of amount above R315 000

R630 000 to R945 000 R56 700 + 27% of amount above R630 000

R945 000 R141 750 + 36% of amount above R945 000

12

• Upon retirement, members of a retirement annuity or pension fund must use 2/3rds of their retirement interest to acquire a guaranteed life annuity or a living annuity – either from the fund or from a long-term insurer.

• For tax purposes, still viewed as a retirement product, and subject to the same rules as retirement fund monies.

Living Annuity background

13

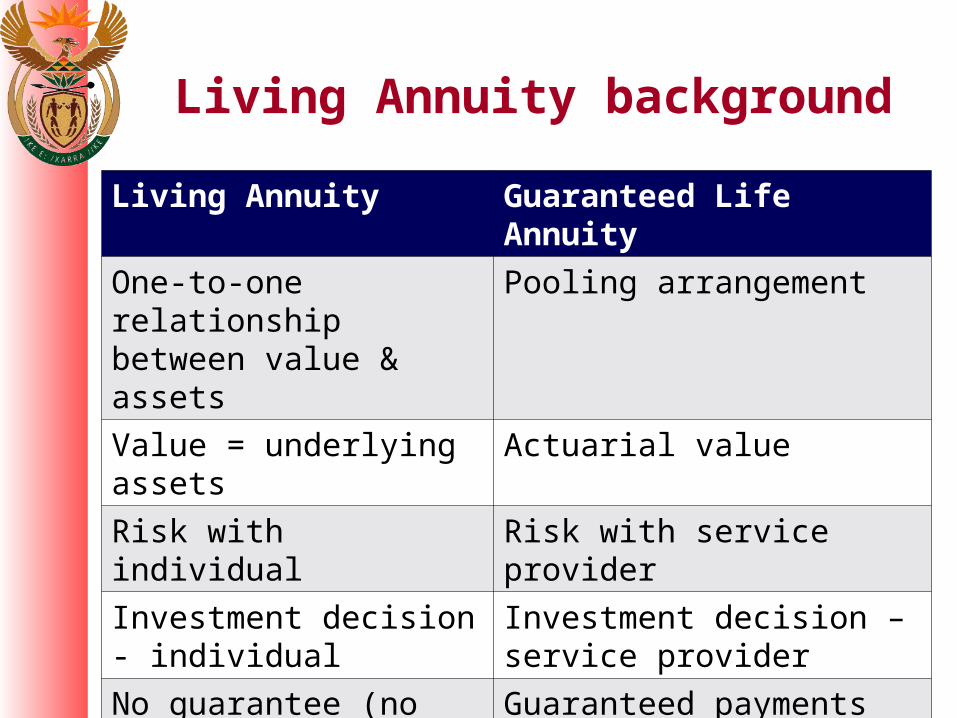

Living Annuity background

Living Annuity Guaranteed Life Annuity

One-to-one relationship between value & assets

Pooling arrangement

Value = underlying assets Actuarial value

Risk with individual Risk with service provider

Investment decision - individual

Investment decision – service provider

No guarantee (no ‘insurance’ element)

Guaranteed payments over life of individual

14

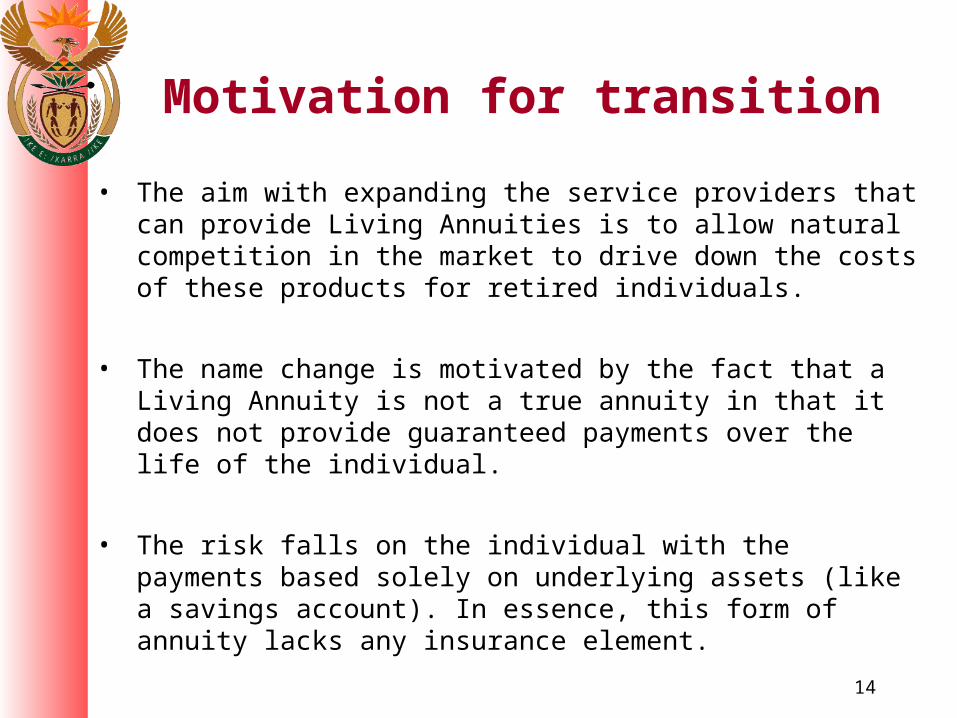

• The aim with expanding the service providers that can provide Living Annuities is to allow natural competition in the market to drive down the costs of these products for retired individuals.

• The name change is motivated by the fact that a Living Annuity is not a true annuity in that it does not provide guaranteed payments over the life of the individual.

• The risk falls on the individual with the payments based solely on underlying assets (like a savings account). In essence, this form of annuity lacks any insurance element.

Motivation for transition

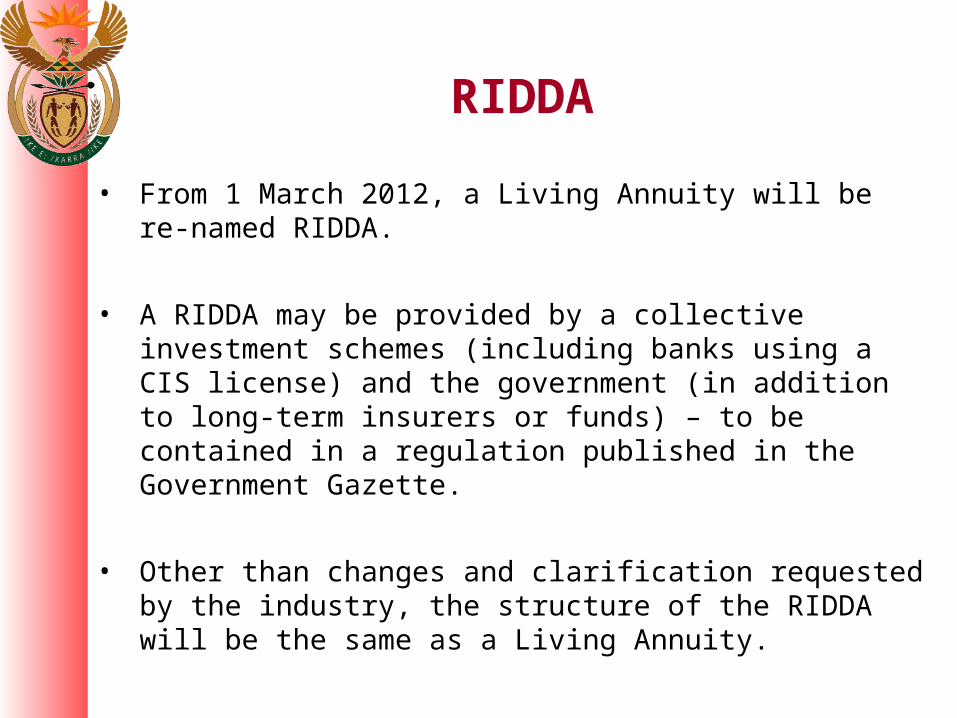

• From 1 March 2012, a Living Annuity will be re-named RIDDA.

• A RIDDA may be provided by a collective investment schemes (including banks using a CIS license) and the government (in addition to long-term insurers or funds) – to be contained in a regulation published in the Government Gazette.

• Other than changes and clarification requested by the industry, the structure of the RIDDA will be the same as a Living Annuity.

RIDDA

16

• Total value of the RIDDA must be linked to the value of the assets/retirement savings used to acquire the RIDDA – no change.

• The drawdown level chosen by the recipient must be set between up to a maximum of 17.5% per annum – the 2.5% floor falls away.

• Can choose draw down percentage and frequency only once per annum – no change except when combining accounts, see hereunder.

RIDDA features

17

• Once the total value of the assets or savings falls to R75 000 or less, the total amount may be withdrawn as a lump sum – no change.

• The amount of the annuity cannot be guaranteed by the service provider – no change

• When the recipient dies, the remaining savings may be withdrawn by his/her nominee as a lump sum or continued as an annuity, or as a combination of both – previously only one option available.

RIDDA features continue

18

• When the recipient dies, the remaining savings may only be continued as an annuity by his/her nominee if that nominee is a natural person – previously legal entities could continue with an annuity.

RIDDA features continue

19

Industry questions around the application of the legislation (and regulations) that applied when combining accounts clarified:•Combining of RIDDAs is encouraged – clarified. •In the event that two or more RIDDA’s are combined, the payment frequency and draw down percentage can be set by the recipient at the date of the anniversary of the combining – previously no direction provided.•When a RIDDA is transferred to another provider, it must remain intact, and cannot be split into two or RIDDAs – no change.

RIDDA features continue

20

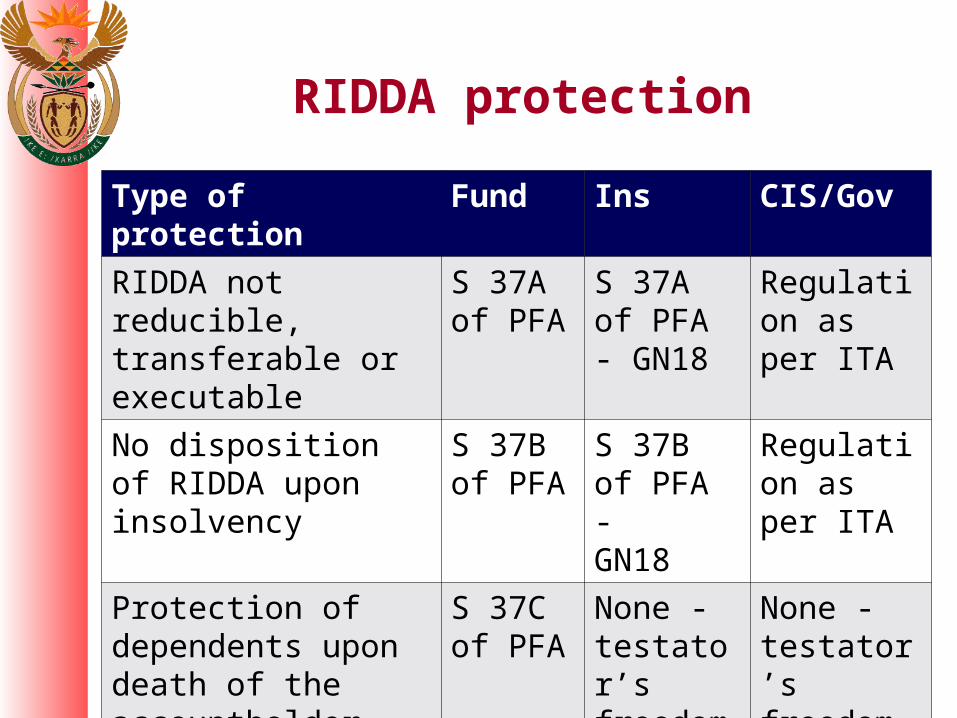

RIDDA protection

Type of protection Fund Ins CIS/Gov

RIDDA not reducible, transferable or executable

S 37A of PFA

S 37A of PFA - GN18

Regulation as per ITA

No disposition of RIDDA upon insolvency

S 37B of PFA

S 37B of PFA - GN18

Regulation as per ITA

Protection of dependents upon death of the accountholder

S 37C of PFA

None - testator’s freedom

None - testator’s freedom

21

Transfers to a pension preservation fund

• The TLAB is proposing that the definition of “pension preservation fund” be amended to allow it to accept a transfer from former members of a provident or a provident preservation fund, pursuant to:

– The winding up or partial winding up of a provident or a provident preservation fund; or

– If the member elected to have any lump sum benefit transferred to the pension preservation fund and made this election whilst he/she was a member.

22

• Employers acquire life cover for the benefit of employees and/or their dependents and pay the contributions on their behalf – typically offered through a group plan.

• The general rule is that any payment made for the benefit of an employee and/or their dependents is treated as a taxable fringe benefit.

• This rule should equally apply to long-term insurance but questions exist as to how far this rule can be applied.

Employer contributions as a taxable fringe benefit

23

• Under the proposed amendment, the fringe benefit treatment will be made explicit.

• Employees will therefore be taxed on any premiums paid by an employer in respect of a risk policy (life cover) that is intended directly or indirectly for the benefit of the employees and/or their dependents.

• Link to the taxation of long-term insurance proceeds – relevance of the 1 January 2011 transition assistance.

Employer contributions as a taxable fringe benefit

24

• Long-term insurance policies provide risk cover for life, disability, etc. and can be structured to provide pure risk, investment or a combination cover.

• Most payouts should be exempt (as capital in nature).

Long-term insurance: Taxation of proceeds

25

• Consistent with SARS practice, a two-fold system is proposed – (part 1) :

– If the premiums were paid with after-tax money, the proceeds will be tax-free in the hands of the beneficiary.

Examples: The policyholder could not deduct the premiums, or the employee paid tax on the premiums as a fringe benefit.

Long-term insurance: Taxation of proceeds

26

• Consistent with SARS practice, a two-fold system is proposed – (part 2):

– If the premiums were paid with pre-tax money, the proceeds will be taxable in the hands of the beneficiary.

Examples: The policyholder or the employee deducted the premiums paid for tax purposes.

Long-term insurance: Taxation of proceeds

27

• Employers take out key person policies to protect the business against the loss of profits (loss of clients, hiring/replacement costs, etc.).

• Generally, employers prefer a tax-free payout and are willing to give up an upfront deduction for the premiums.

Long-term insurance: Employer key person plans

28

• Based on consultation with industry, the legislation will allow the employer a one-off election per policy to choose the deduction (and receive taxable proceeds).

• Default: If no election is made, no deduction may be claimed and the proceeds will be tax-free.

• Because the amendments seek to address the current practical difficulties, special transitional relief will exist for pre-existing policies.

Long-term insurance: Employer key person plans

29

Questions