Embed Size (px)

DESCRIPTION

Audit de marketing

Citation preview

Journal of Marketing Management, 1996, 12, 99-112

Douglas Brownlie

Department of Marketing,

University of Stirling,

Scotland, UK

Marketing Audits andAuditing: Diagnosis ThroughIntervention

The marketing audit has a long and distinguished provenance as adiagnostic device in marketing planning. Indeed, as any goodmarketing student will tell you, the marketing audit should be thestarting-point for any considered course of managerial action inmarketing. Yet, in practice there is often confUsion about how toconduct a marketing audit to good effect.This paper argues that confusion does not arise out of uncertaintyabout what to do, for there is a wealth of accessible literature settingout the steps. Rather, this confusion is seen to be a product of animplicit bias towards means rather than ends in the existingliterature. This bias manifests itself in a clear emphasis on thecontent of marketing audits, i.e. the checklists and questionnaireswhich facilitate diagnosis. However, the purpose of the marketingaudit is not merely to diagnose, but to facilitate collective action in thelight of that diagnosis. Thus, if the end of the marketing audit islearning and change, then the auditing process is inevitably anorganizational intervention.

In this paper, the author attempts to redress the balance between themeans of marketing auditing, i.e. diagnosis, and its end, i.e.organizational change. It sets out an approach to the process ofmarketing auditing that places benchmarks and benchmarking at its

centre.

Introduction

Kotler et al. (1977) define the marketing audit as a systematic examination of anorganization's marketing objectives, strategies, organization and performance. Its primaiypurpose is then to identify under-utilized marketing resources and to generaterecommendations for ways in which these resources could be put to more effectiveuse.

Laudable aims you might agree. However, given the significance of those aims interms of the judgements the audit seeks to make about the conduct of marketingafiairs, it is rather naive to see it as a neutral analytiCcJ tool in the hands of theenlightened few. In practice, the passing of judgement on the conduct of marketingInevitably points the finger at someone whose responsibility is to manage particularelements of an oi^anization's marketing activities. Thus, the task of conducting amarketing audit is fraught with dangers and difficulties for the politically naive orinsensitive. The process has to be carefully managed, and in some cases stage-Correspondence to be addressed to: Department of Marketing, University of Stirling, Stirling FK94LA,Scotland, UK.

0267-257X/96/010099 +14 $12.00/0 ©19% The Dryden Press

100 DomgUu Browidie

managed, if the end of oigaiuzational change, desirable or otiierwise, is to beattained.

This paper sets out to consider those dangers and difficulties. It does so in the lightof a view of the marketing audit as an organizational device that when "in play"cannot be politically neutral, for by its very nature it seeks to intervene in theprocesses of the organization that are subjected to the audit. It reflects on the processof marketing auditing and hopes to offer insights on how auditors can bettermanage the intervention towards a successftal condusion.

Lessons from the Accounting Audit?

When defined in Kotler et al.'s (1977) terms, the marketing audit seems to serve asimilar purpose to the accoimting audit. However, unlike the accounting audit,which is an offidal examination and verification of a company's accounts andaccounting procedures relating to past financial performance, ihe marketing audit isalso said to be a dedsion-making tool (Naylor and Wood 1978).

An accounting audit is conduded in accordance with generally acceptedaccoimting prindples and is produced by the appointees of statutory bodies largelyfor external consumption. However, the procedures governing the conduct ofmarketing audits are not widely agreed or standardized; nor is their condud policedby a pubUdy recognized statutory institution. It is then impossible to deferjudgements to the "higher court" of the authority of an established governinginstitution. Those judgements are made by one group of people, the auditors, aboutthe activities of another group of {people within the same organization thatempowers both. Therefore, judgements are open to political interpretation ormanipulation and they can, £md should, often be contested.

In addition to examining pwsf performance, the marketing audit also has a role toplay in recommending how to go about improving future performance. Thus, themarketing audit is not orUy concerned with how effectively marketing pierfonns itsassigned fimctions in the areas of advertising or distribution. It also questions theorganization's choice of market position which is itself dictated by the broaderimperatives of top management's dedared corporate strategy. So, as McDonald cindLeppard (1991) assert, the marketing audit is not only a tool for exerdsingmanagement control, it also contributes to planning emd strategy-making throughsubjecting the activities of all to dose scrutiny.

There is also no statutory obligation to condud a marketing audit, or to employpardctilar people to conduct it. Indeed, as \Wlson (1992) notes, marketing audits canbe performed by persormel within an organization or outside it. As he suggests, aninterned auditor or consultemt may be a senior meinager, a senior managementcommittee, or a manager or group of managers from other sites, branches orfunctions. Although in the short term it may be more expensive to use externalconsultants, they do lend the outsider's perspective, imparticility, continuity andbreadth of experience to the audit (Turner 1^2). External consultants are usuallypreferred by organizations new to marketing, or with a naive approach to it,especially where the use of a consultant is linked to the award of an enterprise grant,or some other form of extenul support. More sophisticated organizations are likelyto employ internal consultants and to approach marketing auditing as a regular and

Marketing Audits and Auditing 101

integral part of the marketing-planning routine of setting targets and monitoringperformance towcirds those tcirgets. But, these organizations wUl often use externalconsultants where sensitive issues concerning the management of importantorganizationcd changes are anticipated.

Kotler et al. (1977) have written that the marketing audit has value as a one-off,freestanding exercise. However, they add that its potential has a far greater chanceof being reailized as part of a regular auditing process which is itself driven by theorganization's meirkedng-plamung process. In this way, comparison can be madebetween the restilts of each audit so that performance trends can be monitored. Mththis data, it is possible to empower staff to take responsibility for dearly definedtasks. Accotintability for those tasks can then be dearly assigned. So, the marketingaudit also has the potential to provide the basis for target-setting appraisal andreward schemes, tfius linking htiman resource considerations to the cyde ofmarketing planning.

So, like an accountitig audit, a marketing audit should be conducted regularly andnot only when some aspect of marketing activities is thought to be out of control.The auditor, whether intemal or external, has the opportunity not merely to conducta one-off audit for a client at a time of crisis, but to demonstrate the value of makingit a regular part of the organization's planning process. This paper argues that to doso requires skills in organizationcd intervention as well as analytical skiUs.

The inescapable implication of a marketing audit is that action of some kind isgoing to be taken to change something, and this will mean making an interventionof some sort in the processes, structures, systems and procedtires of the organization.Indeed, the audit itself is an intervention. Its announcement and subsequent conductwiU signed to the staff concerns about something that is happening, and that mayhave been predpitated by intemal or external drctimstances. It may also come tosymbolize the organization galvanizing itself for change.

Any organization looking to employ an external consultant to perform amarketing audit should, therefore, look for intervention capabilities too. Therein liesanother demger of one-off marketing audits—they can become associated in theminds of employees as signalling serious management concerns, or as weaponswhich management use to jtistify a course of action it has already dedded to pursueanyway. The audit can become a blunt and divisive ideological weapon in the handsof the tinwary or ill-prepared. However, the regular conduct of marketing audits canhelp to make them less threatening and to position them correctly as anotherinstrtiment of collective management control and dedsion-making which subjects allaspects of jin organization's marketing activities to scrutitiy.

Marketing Auditing

Much that is written about the marketing audit draws on the seminal work of Kotleret al. (1977), as well as that of Naylor and Wood (1978) and MacDonald (1982). Thisbody of work describes a rather mechaniccd approach to the collection andinterpretation of data that seems to have tiniversal applicability, even if the authorsnever intended it to be so. Whilst applauding this early work, the author'sexperience leads him to believe that there is no single set of procedtires that worksbest for all marketing audits in all organizations, at all points in time and space. The

102 Douglas BrownUe

exerdse does commit the auditing consultants, whether internal or external, todelivering to the dient a comprehensive audit document, as well as makingpresentations to senior management, and increasingly these days, to middle andjunior management too. The document and the presentations would provide thefollowing information, p>erhaps tailoring the delivery and the content to suit theneeds and expedations of the different audiences.

— An inventory of the client organization's existing marketing resources, assets,skills and competences.

— A statement of the client's marketing needs and problem areas as defined byits client group, which is tj^ically top or middle management, but should takeinto account the perspectives of op)erationctl staff.

— A review of the client's position with resptect to its customers, competitors,suppliers and other external stakeholder groups that exert an influence on it.

—An ancilysis of the client's strengths and weaknesses in the area ofmarketing.

—An evaluation of the client's current marketing activities.—An inventory of the marketing resotirces, assets, skills and competences which

the consultant believes to be desirable for the client to obtain.—Recommendations as to a course of action by means of which the dient could

go about acquiring the desired marketing approach and expertise and to whatexpeded effed.

This is not an exhaustive Ust of dient expedations by any means. But it is indicativeof the committment made by clients to the outcomes of the marketing audit, even ifthey are unsure as to the process by means of which those outcomes are to beachieved.

Clearly, before proceeding with the marketing audit, the consultant requires aknowledge of the client organization, its produds, services, markets, systems,procedures and personnel However, the reason for this has less to do with acquiringa farruliarity with the drcumstances and operating details of the business. It is moreimportant in terms of helping the auditors to develop a sensitivity to the agendas ofthe various interest groups, or coalitions operating within the company. For thoseagendas will ultimately determine staff perceptions of the audit and what theybelieve it is really tr3dng to achieve—which may be very different from the dedaredaims of the audit. They will also irrfluence staff attitudes to partidpating in itsprocesses and may colour what they choose to tell the auditors about that part of thebusiness they are held accountable for. It is also important to be sensitive to thelabour relations context when proceeding with an audit, the findings of which mayultimately have ramifications for staff in the organization. For all these reasons, theclient will rarely be disinterested in the process by means of which the audit is to beconduded. Most astute managers are alert to the political sensitivities that anyorganization intervention can upset. The author believes that four additionalrequirements should also be borne in mind:

—Dedding which issues are relevant.— Knowing where or from whom to obtain information on those issues.— Interpreting the data coUeded in the light of client needs.—Translating findings into condusions and recommendations for action.

Marketing Audits and Auditing 103

Relevance

At the earliest possible time, clear objectives for the marketing audit should beagreed between the dient and the auditors. Those objectives represent a key elementof the context within which the audit is to be conducted and its findingssubsequently given meaning and import. They also represent an essential part of abriefing document which would detail a step-by-step plan to be followed by theauditors in executing their task.

The broad framework of an appropriate plan should be devised, but rarely set bythe auditors alone. The audit plan will establish which issues to investigate, how tocollect data and from whom, in what time-span, at what cost, and what managementneeds to do to set the context for the audit through communicating its purpose to thestaff. The details of the plan should arise from discussions between the client and theauditors in which they both set out to paint a verbal picture of the broad contextwithin which the marketing audit has to be seen. Therefore, the context of the auditis negotiated and not simply dictated by the client. Similar discussions should alsotake place about the audit process, i.e. the way in which the intervention is to takeplace. This discussion should lead to an agreed strategy that will set out how theaudit is to be conducted by the auditors, and the respective roles to be played by theauditors and the various organizational participants. A version of this vision willneed to be communicated to the staff concerned, typically by means of formalannouncement setting out the reasons for the audit, its aims and the consultativeprocess it will employ.

Qecirly, it is not enough for the auditors to take everything the client says aboutthe context of the marketing audit at face value. To do so would be tantamount to adereliction of their duty to unearth painful realities that the client might be unawareof, or may not have been facing up to. Discussions between the client and theauditors about the audit context should become increasingly searching andrevealing to both parties as the process unravels.

Kotler (1977), Davidson (1987), McDonald and Leppard (1991), and VWlson (1992)advocate that their audit process should be based on the auditors administering aseries of questionnaires to a sample of the organization's ptersonnel. Wilson (1992)advises that these questionnaires should be developed carefully to ensure that theaudit focuses on the "right" issues. Decisions about this will, in practice, involveboth client and auditors, although in theory you might expect it to be at thediscretion of the latter. It follows then that checklists of "off-the-shelf questions",such as those offered by McDonald and Leppard (1991) and Wilson (1992), must bemixed and matched to suit the particular organization, the audit context and thecircumstances that surround it. Wilson (1992) believes that the marketing auditshould draw the client's attention to both the obvious and the esoteric, and that theywill mean different things for each organization and marketing memager. Thus, somediagnostic questions may seem simple and even naive for one organization ormanager, while the same questions in another context may provide new insights.

Identifying Participants

Another area of the audit plan for discussion between the auditors and the client

104 Douglas BrownUe

concerns the selection of audit partidpants, typically questionnedre respondents andinterviewees. Thus, the auditors also require an ability to obtain cooperation frombusy and sometime sceptical, disingenuous, inscrutable or even unwillingpartidpants. This may be achieved through the early communication of the purposeof the audit to staff, particularly those from whom help wiU be sought.

Experience shows that when interviewing personnel, the auditors should try totalk with as diverse a group of pieople in the organization as possible. They shouldexped to have some discretion over which managers to interview and shouldalways call on staff outside marketing. However, this discretion will sometimes beseverely curtailed until some degree of rapport and trust is established between theauditors, the dient and the interviewees. The auditing consultants must meet withheadcjuarters staff, visit field oi^anizations, interview customers and, if possible,competitors, and analyse interned information on the marketing environment andperformance. It takes time and some sensitivity to establish the trust and reapedwhich makes this degree of access possible and lends the audit, as well as theauditors, legitimacy within the dient organization. Enis and Garfein (1993) foundthat their computer-driven approach to the collection of auditing information helpedin some of those matters, particularly in generating ownership of the audit processand in facilitating partidpation and the cross-fertilization of ideas.

In politically sensitive situatiorts, it may be advisable to have different auditorsinterviewing staff at different levels, or staJEf from different parts of the organization.This helps to ensure reasonably uncontaminated access to personnel of variouslevels and fimctions. Otherwise the auditors shotdd focus on the organization's topmanagement initially, and then move down through the orgemizational hierarchybefore revisiting senior staff.

The auditors should actively seek out different points of view within the variousdepartments of the organization, or a mismatch between the customers' andcompany's percejrtion of the produd. Such differences can signify conflid andtension within the organization, and between it and its ctistomers, distributors andsuppliers. In many ways, the auditors must proted their impartiality and even-handedness. They must be seen to be taking the impartial viewpoint of the outsiderand to be Ustening to all views. The asstuance of confidentiality can help in thisregard. However, in their actions the corisultants must embody this impartiality andthis offen means that interim reports are shared with aU the interest groujjs in theorganization and that promises of confidentiality are met.

Interpreting Data

There is an assmnption underpirming much of the existing literature on marketingaudits that the data coUeded by the auditor is neutral and objective. In the author'sexperience, there is nothing hks conducting a marketing audit to teetch the lessonthat data about the activities of organizations is never neutral or objective. Auditstypically colled opinions or accoimts of circumstances, situations and outcomesfrom informants located in various parts of an organization. What those informantschoose to tell the auditor is already influenced by their perceptions of what the auditis really trying to achieve and for whom. Some informants may feel threatened bythe audit, others may see it eis an opportunity to grind an axe. The auditors have

Marking Audits and Auditing 105

little control over this and rely on top management to set a context that encouragesan open and frank exchange of views.

Moreover, the data the auditor collects is already an interpretation, whether it isprovided in the form of accounts of previotis actions and dedsions, or opinions onwhat should have been done. Thtas the author is already two degrees removed fromthe cut and thrust of everyday marketing conduct within the client organization. Ifyou accept this as a fact of organizational life, then the view that the marketing auditcan ever be a neutral analytical tool is not tenabk.

The auditors are then placed in the diffictilt position of having to make theirinterpretations of the collected data as transparent as possible. It is in this regard thatthe issue of objectivity is relevant, for the authors must be seen to be taking thedisinterested, if well-informed, outsider's perspective and to be consistent in thisapproach. The technique of triangulation can be useful here in searching for somecommon ground on which to base interpretations. The opinions and accoimts ofinformants will differ in emphasis, if not substance. But through analysing theirdifferences and sinulaiities, it is possible for the auditors to offer a fcdr interpretationthat can withstand the scrutiny of the dient, even if he or she is not comfortable withit. It is at this jtmcture that the idea of benchmarks can fadlitate the interpretiveprocess.

Benchmarks and Benchmarking

Authoritative writers on the marketing audit, induding Kotler et al. (1977), Naylorand Wood (1978), Kotler (1977), McDonald and Leppard (1991), and Wilson (1992),typically view it ets an instrument by means of which to judge an organization'soverall commitment to a marketing orientation; to measure the extent to whichmarketing objectives have been achieved; to indicate whether the route chosen(marketing strategy) was the most effective and profitable; and to indicate whetherparticulctr marketing activities are better intensified, adjusted or dropped. Thisfocuses on the outcomes and content of the marketing audit.

More recently, writers such as Enis and Garfein (1992) and Enis (1993) haveemphctsized the interactive informational gathering role of the marketing audit.However, once again the marketing audit is portrayed as a technique, as aninstrument in the hands of marketing management. The instrumental approach thatis typically taken to describe the "how tos" of marketing auditing does overlooksome important facets of the audit as an organizational intervention.

The thinking process that underlies the auditing methodology needs to beclarified. It is based on an essentially comparative methodology which findswidespread application in marketing in the context of developing frameworkswithin which to make managerial judgements about matters such as the diagnosis ofcompetitive strengths and weaknesses p a y and Wensley 1988). In the case of themaiiceting audit, the dient and the auditors must agree a broad set of organizationalparameters and a specific set of derivative and meastirable benchmarks. A way ofmeasuring those benchmarks must also be agreed.

It is indeed a great pity that, unlike medical sdence, marketing does not yet havea definitive set of concepts, benchmarks, measures and instruments by means ofwhich we can both describe and analyse the anatomy of an organization in order to

106 Douglas BroumUe

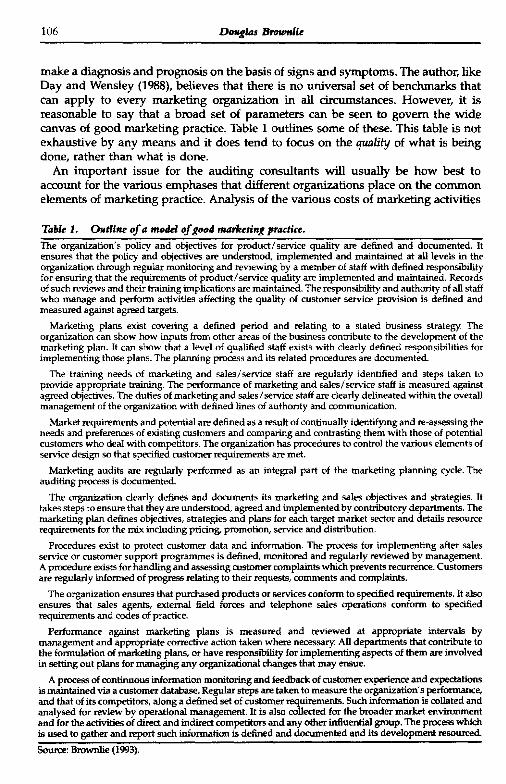

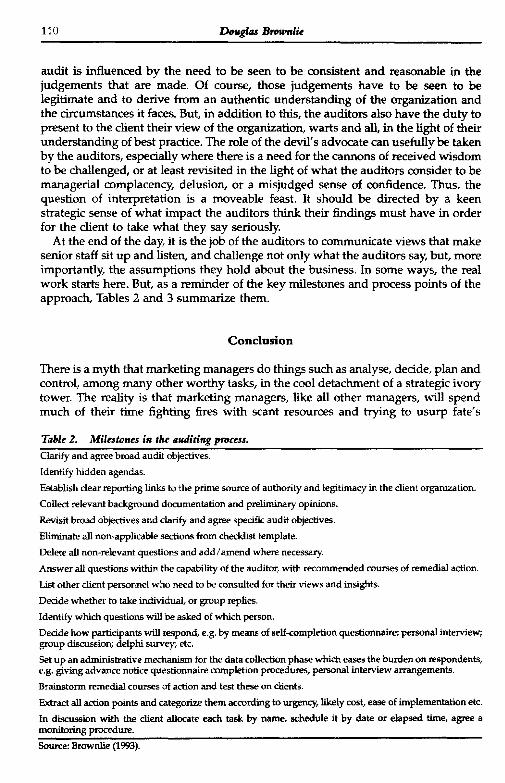

mctke a diagnosis and prognosis on the basis of signs and sjmptoms. The author, likeDay and Wensley (1988), believes that there is no universal set of benchmarks thatcan apply to every marketing organization in aU drctimstances. However, it isreasonable to say that a broad set of parameters can be seen to govern the widecanvas of good marketing practice. Table 1 outlines some of these. This table is notexhaustive by any means and it does tend to focus on the qtiality of what is beingdone, rather than what is done.

An important issue for the auditing consultants will usually be how best toaccount for the various emphases that different orgarvizations place on the commonelements of marketing practice. Analysis of the veuious costs of marketing activities

Table 1. Outline of a model of good marketing practice.

The organizahon's policy and objectives for product/service quality are defined and documented. !tensures that the policy and objectives are understood, implemented and maintained at all leveis in theorganization through regular monitoring and reviewing by a member of staff with defined responsibilityfor ensuring that the requirements of product/service quality are implemented and maintained. Recordsof such reviews and their training implications are maintained. The responsibility and authority of all staffwho manage and perform activities affecting the quality of customer service provision is defined andmeasured against agreed targets.

Marketing plans exist covering a defined period and relating to a stated business strategy. Theorganization can show how inputs from other areas of the business contribute to the development of themarketing plan. It can show that a level ol qualified staff exists with clearly defined responsibilities forimplementing those plans. The planning process and its related procedures are documented.

The training needs of marketing and sales/service staff are regularly identified and steps taken toprovide appropriate training. The performance of marketing and sales/service staff is measured againstagreed objectives. The duties of marketing and sales/service staff are dearly delineated within the overallmanagement of the organization with defined lines of authority and communication.

Market requirements and potential are defined as a result of continually identifying and re-assessing theneeds and preferences of existing customers and comparing and contrasting them with those of potentialcustomers who deal with competitors. The organization has procedures to control the various elements ofservice design so that specified customer requirements are met.

Marketing audits are regularly performed as an integral part of the marketing planning cycle. Theauditing process is documented.

The organization clearly defines and documents its marketing and sales objectives and strategies. Ittakes steps to ensure that they are understood, agreed and implemented by contributory departments. Themarketing plan defines objectives, strategies and plans for each target market sector and details resourcerequirements for the mix including pricing, promotion, service and distribution.

Procedures exist to protect customer data and information. The process for implementing after salesservice or customer support programmes is defined, monitored and regularly reviewed by management.A procedure exists for handling and assessing customer complaints which prevents recurrence. Customersare regularly informed of progress relating to their requests, comments and complaints.

The organization ensures that purchased products or services conform to specified requirements. It alsoensures that sales agents, external field forces and telephone sales operations conform to specifiedrequirements and codes of practice.

Performance against marketing plans is measured and reviewed at appropriate intervcds bymanagement and appropriate corrective action taken where necessary. All departments that contribute tothe formulation of marketing plans, or have responsibility for implementing aspects of them are involvedin setting out plans for managing any organizational change that may ensue.

A process of continuous infonnation monitoring and feedback of customer experience and expectationsis maintained via a customer database. Regular steps are taken to measure the organization's performance,and that of its competitors, along a defined set of customer requirements. Such infonnation is collated andanalysed for review by operational management. It is also collected for the broader market environmentand for the activities of d i « * and indirect competitors and any other influential group. The process whichis used to gather and rq>ort such icformation is defined and documented and its development resourced.

Source: Brownlie (1993).

Marketing Audits and Auditing 107

and their assodated trends and outcomes clearly provides valuable data that willcontribute to the overall diagnosis. Therefore, techniques in this area mustsupplement other forms of data collection. Day and Wensley (1988), Thomas (1986),emd Stasch and Lanktree (1980), among many others, have described procedures foranalysing various marketing activities that would contribute to the marketingaudit.

At a general level, these broad parameters do provide guidelines about theelements of good marketing practice. Clearly they will be informed by the findingsof the numerous empirical studies relating marketing practice to organizationalperformance. At the detailed level of an individual organization, they may need tobe modified to account for the idios)mcrades of mairkets, relationships andmarketing operations that seem to apply in a specific business. Of course, this is notto say that the auditors must be blinded by what they find. They have the importantrole to play of questioning why things are done in a particular way and to whatmeasurable effect. This charges the auditors with the responsibility to be well-informed on current ideas about the nature of best marketing practice and itsrelationship to broader organizational practices and outcomes, wherever it lies. Theymust also be able to translate the findings of more esoteric marketing research intoa language that managers can understand so that they can grasp its practicalsignificance.

In recent years, the idea of benchmarking has come to some prominence in theplanning literature (Pryor 1989; Shetty 1993; Watson 1993; Leppard and Molyneux1994), largely because of the pioneering efforts of the Xerox Corporation. Essentiallythe process involves comparing one firm's performance on a set of measurableparameters of strategic importance against that of the firms known to have achievedbest jjerformance on those indicators. Sources of best practice need not be found inthe same sector as the firm that is the subject of the audit, for as Shetty (1993) cirgues,non-competing firms can provide valuable insights and information on bestpractices that may stiU have to find their way into the sector in question.

Advocates of benchmarking describe it as a continuous comparative process thatcan be appUed to all areas of an organization's activities, from strategic development(Watson 1993) to operations (Shetty 1993) to customer service and satisfaction(Leppard and Molyneux 1994). Essentially the process works to the extent thatbenchmarks can be agreed, and stiitable comparators found, for which measure-ments are also available. Thus, the benchmarker must have detailed access toinformation about best practice, regardless of the industry or sector in which it isfound.

Authors recognize that it is a formidable task to collect information about thepractices of leading-edge firms, who may in some instcuices be competitors.However, they do suggest that some firms may be willing to share the necessaryinformation that leads to a better understanding of the elements of improvedpractice, if not the detailed actions that can lead to its attainment. Indeed, Watson(1993) advocates that firms that are keen to develop a strategic approach tobenchmarking shoxild consider developing long-standing relationships with alimited ntimber of companies that will serve as a network for sharing ittformationabout benchmarks and benchmarking methodology.

In the context of marketing auditing, benchmarking may create a new role for theauditor in terms of identifying parameters and suitable organizations against which

108 Douglas BrowidU

comparisons can be made. The auditing consultants may also take a leading role inestablishing relationships with other organizatioi« which share an interest inbenchmarking and the benefits it can bring.

Checklisting

Although the language of "benchmarking" is currently in vogue, the concept hasalways been an integral, if implicit, part of the marketing audit methodology.However, contemporary discussions of benchmarking do add an interesting "spin"to what used to be known as "checklisting", whereby a checklist of diagnosticquestions would be developed as a means of focusing on key issues for theorganization undergoing the marketing audit. The answers to those questions wouldthen provide data on specific elements of the marketing operations of theorganization. This data would then be compared and contrasted with a pre-conceived set of standards, or benchmarks, which would typically be derived frommanagement expectations or objectives.

Of course, as the advocates of this approach have always argued, impUcit to theasking of each question is the expectation that particular answers will signify eithergood or bad marketing practice (Wlson 1992) when compjired to given standards.So, the questions themselves will be derived from a prior view (a theory) of what theelements of good marketing practice should be for the organization in its sector. Thismodel can be derived from the literature, especially that which offers what Baker(1992) calls currently useful generalizations: the views of management; the manage-ment of other firms; customers; competitors; industry commentators; sales andservice staff; etc. What the language of "benchmarking" adds is a focus on theprocess of seetrching for appropriate stemdards of best practice against which tocompare measures of the client organization's practice and performance.

Advocates of benchmarking are cleat that the development of benchmarks is aniterative and ongoing process that is likely to involve sharing information with otherorganizations and working with them towards an agreeable metrology (Brownlie1993). On the other hand, advocates of the cheddistitig approach seem moreconcerned to develop a comprehensive listing of diagnostic questions that can beapplied to all areas of marketing activity for all times and places. This is driven bythe worthy goal of providing a reliable ready-reckoner for assembling diagnosticinformation about key elements of marketing practice. Furthermore, as Wilson(1992) claims, having access to a comprehensive checklist of diagnostic questionshelps to ensure the possibility of a detailed mapping of marketing resources andtheir various flows both within and without the organization.

However, as Wilson (1992) also notes, checklists can inhibit original thinking and,in the hands of the unwary, can produce an unconsidered acceptance of benchmarksof performance that may be inappropriate to the dncuinstances at lumd. Wilson(1992) provides a very comprehensive series of checklists which can be consulted asa resource in develofring em inventory of diagnostic questions to suit a particular setof circumstances. Readers who are interested in checklists that could be used areencouraged to consult the work of Wilson (1992), Naylor and Wood (1978),MacDonald (1982), and McDonald and Leppard (1991). Qearly, those off-the-shelfchecklists must be screened, re-orientated and supjdemented to meet the specific

Marketing Audits and Auditing 109

needs of the auditor, as well as the activities and ambitions of the clientorganization.

Whatever approach is used to establish benchmarks of good marl^ting practice,the auditors must have a clear view of why they sire asking particular questions; andimpoifemtly this view should also be shared by the client organization. The auditormust also keep a weather-eye on the legitimacy and authenticity of thosebenchmarks in the mind of the client. Moreover, the auditors should be clear aboutwhat interpretation it will be possible to place on particular answers.

Findings

In theory, suggestions for change should emerge from the marketing audit. Theymay lack the elegemce of sophisticated marketing strategies and systems. But, theycan have the advantage of being practical and relevant to the context as themanagers of the client organization understand it. Random, disconnected ideasoften arise during the audit which may well test the efficacy of the existingmarketing systems and their organization, as well as the assumptions underl3ringdeclared marketing plans. So the marketing audit should also be a creative force, andthe auditing process must embrace and facilitate such creativity. Checklists andother such tools are merely a means to this end and not ends in themselves. It is theauditors' job to conduct the audit in a way that empowers staff to contribute,criticize, and offer alternative perspectives on what may be the received wisdom inthe organization. Often middle and junior operational staff Ccin spot problems thatare invisible to senior staff. Indeed they may have to live with those problems on aday-to-day basis; and they can often suggest simple modifications to systems andprocedures which cjm help address the problems.

The reasons why marketing resources may not be fully exploited are often notdifficult to imderstand. Indeed, many organizations do not know what metrketingresources are within their gambit, or their quality. Frequently, because of thereceived wisdom, old worldng practices and sometimes despair, managers areconstrained, or constrain themselves, from introducing simple changes which wouldrelease much of the currently imder-exploited resources, energy and commitmentwithin the organization.

Completing a marketing audit does not automatically imply that what theauditors consider to be the appropriate actions will be taken by the client. Furtheradvocacy may be required in order to get a commitment to making changes which,to a greater or lesser extent, will be pairiful and resisted. This will becomeparticularly difficult for the internal consultant who has been drawn from localmanagement. To be certain that the marketing resources will be fully realized, it isimjxjrtant to ensure that every action decided upon is allocated to an individual orgroup; that the time for its completion is scheduled and commimicated; and thatsomeone monitors that the task is satisfactorily completed by the due date. Allocate,schedule and monitor are the key words for facilitating action.

So, if the desired outcome is change of some sort, and both the client and theauditors are clear on this, then the auditors have to grapple with the problem of howto present their interpretations in such a way that managers will listen and hear whatis being said. Thus the task of interpreting the data that is coUected by means of the

110 Douglas Broumlie

audit is influenced by the need to be seen to be consistent and reasonable in thejudgements that are made. Of course, those judgements have to be seen to belegitimate and to derive from an authentic understanding of the organization etndthe drcumstances it faces. But, in addition to this, the auditors also have the duty topresent to the dient their view of the organization, warts and all, in the light of theirunderstanding of best practice. The role of the devil's advocate can usefully be takenby the auditors, especially where there is a need for the cannons of received wisdomto be challenged, or at least revisited in the light of what the auditors consider to bemanagerial complacency, delusion, or a misjudged sense of confidence. Thus, thequestion of interpretation is a moveable feast. It should be directed by a keenstrategic sense of what impact the auditors think their findings must have in orderfor the client to take what they say seriously.

At the end of the day, it is the job of the auditors to communicate views that makesenior staff sit up and listen, and challenge not only what the auditors say, but, moreimportantly, the assumptions they hold about the business. In some ways, the realwork starts here. But, as a reminder of the key milestones and process points of theapproach. Tables 2 and 3 summarize them.

Conclusion

There is a myth that marketing managers do things such as ctnalyse, decide, plan andcontrol, among many other worthy tasks, in the cool detachment of a strategic ivorytower. The reality is that marketing managers, like all other managers, will spendmuch of their time fighting fires with scant resources and trying to usurp fate's

Table 2. Milestones in the atUliting process.

Clarify and agree broad audit objectives.

Identify hidden agendas.

Establish dear reporting links to the prime source of authority and legitimacy in the client organization.

Collect relevant background documentaticm and preliminary opinions.

Revisit broad objectives and clarify and agree specific audit objectives.

Eliminate ail non-applicable sections from checklist template.

Delete all non-relevant questions and add/amend where necessary.

Answer all questions within the capability of the auditor, with recommended courses of remedial action.

List other dient personnel who need to be consulted for their views and insights.

Dedde whether to t£ike individual, or group replies.

Identify which questions will be asked of which person.

Dedde how participants will respond, e.g. by means of self-completion questionnaire; personal interview;group discussion; delphi survey; etc.

Set up an administrative mechanism for the data collection phase which eases the burden on respondents,e.g. giving advance notice questionnaire completion procedures, personal interview arrangements.

Brainstorm remedial courses of action and test these on clients.

Extract all action points and categorize them according to urgency, likely cost, ease of implementation etc.

In discussion with the dient allocate each task by name, scheciule it by date or elapsed time, agree amonitoring procedure.

Source: Brownlie (1993).

Marketing Audits and Auditing 111

Table 3. Process considerations.

Initial visit to the client organization to meet top management, and discuss how you plan to go about themarketing audit and what commitn:\ent is needed from the hosts.

Further visits to record marketing activities and procedures and to establish perceived marketing needs,etc.

Interviews with managers to establish marketing effectiveness using checklists and questionnaires.

The development of a suitable battery of benchmarks against which to judge marketing procedures.

Analysis of marketing procedures on the basis of those benchmarks.

Development of alternatives for improving the organization's marketing and the formulation of a draftreport.

Discussion of the preliminary findings with the client and the recording of feedback and recycling wherenecessary.

Preparation of the final report and presentation of findings to the top management of the dientorganization, and sometimes to middle management too.

Source: Brownlie (1993).

greatest efforts to thwart their best laid plans. Clearly, there is a need to providemanagers with a breathing space every now and then, to take some time to reflecton the organization's position, and where it is going and why, before commiting itto a course of action that may prove to be iU-conceived. Tbe marketing auditfacilitates this thinking.

However, there is another myth that the marketing audit is a neutral analyticaldevice which somehow escapes the manipulation of people within organizationswho seek to advance their interests in the light of their own perceptions. This paperhas attempted to show that this can never be so for various reasons, but mostimportantly because the auditing process does not end with diagnosis. This issimply the beginning. Ultimately organizations go through the pain and expense ofthe marketing audit either because they already seek to change things, or becausethey have a sneaking suspidon that something may need to be changed. Rarely is anaudit commissioned just so that senior managers can say "yes, we have done amarketing audit"; although for some oiganizations who seek only to be able to talka good marketing story, such display behaviour is a motivator. Rarely is a marketingaudit commissioned through the self-deluding vanity of needing to reaffirm whatthe organization already knows, or to congratulate itself on what it thinks it alreadydoes well.

The point of the marketing audit is to impel action, to fadlitate it in the light of adiagnosis that emei^es through intervention in the dient organization's processes atvarious levels. The audit is a way of creating awareness of the need for change andof identifying the various camps that may resist or fadlitate change. In doing so, itcan help the organization towards a more effective approach to the management ofthe change process. But, for the auditors this means that the process is just asimportant as dever diagnosis. At the end of the day, the organization has to actcollectively in the light of that diagnosis. This means bringing its staff on board; theyhave to be involved and consulted if they are ever to be empowered towards change.Thus, the real diagnosis, the one that facilitates change, the one that bonds stafftowards a common goal, emerges through intervention.

112 Douglas BroumUe

References

Baker, M.J. (1992), Marketing Strategy and Management 2nd Edition, London, TheMacmUlan I^ss .

Brownlie, D.T. (1993), "The Marketing Audit: A Metrology and Explanation",Marketing Intelligence and Planning, 11, No.l, pp.4-12.

Davidson, H. (1987), Offensive Marketing: Or Haw to Make Your Competitors Followers2nd Edition, London, Penguin Books.

Day, G.S. and Wensley, R. (1988), "Assessing Advantage: A Framework forDiagnosing Competitive Superiority", Journal of Marketing, 52, April, pp . l -^ .

Enis, B.M. (1993), The Marketing Audit: Practical Guidelines for Improving MarketingStrategy, Boston, AUyn and Bacon.

Enis, B.M. and Garfein, S.J. (1992), "The Computer-Driven Marketing Audit: AnInteractive Approach to Strategy Development", Journal of Management Inquiry, 1,No.4, pp.306-317.

Kotler, P. (1977), "From Sales Obsession to Marketing Effectiveness", HarvardBusiness Review, November/December 1977, pp.67-75.

Kotler, P., Gregor, W. and Rogers, W. (1977), "The Marketing Audit comes of Age",Slmn Management Review, Winter, pp.25-44.

Leppard, J. and Molynetix, L. (1994), Auditing Your Customer Service, London,Routledge.

MacDonald, C.R. (1982), The Marketing Audit Workbook, London, Englewood Cliffs,NJ, Prentice Hall.

McDonald, M. and Leppard, J. (1991), The Marketing Audit: Translating MarketingTheory into Practice, Oxford, Butterworth, Heinemann.

Naylor, J. and Wood, A. (1978), Practical Marketing Audits: A Guide to IncreasedProfitability, New York, Wiley & Sons.

Pryor, L. (1989), "Benchmarking: A Self-Improvement Strategy", Journal of BusinessStrategy, 10, No.6, pp.28-32.

Shetty, Y. (1993), "Aiming High: Competitive Benchmarking for Superior Perform-ance", Long Range Planning, 26, No.l, pp.39-44.

Stasch, S.F. and Lanktree, P. (1980), "Can Your Marketing Planning Procedures BeImproved?", Journal of Marketing, 44, Summer, pp.79-90.

Thomas, M.J. (1986), "Does your Marketing Pay", Management Dedsion, 24, pp.41-45.

Turner, A. (1982), "Consulting is More than Giving Advice", Harvard Business Review,September/October 1982, pp.l2(>-129.

Watson, G. (1993), Strategic Benchmarking: How to Rate your Company's PerformanceAgainst the World's Best, New York, Wiley & Sons.

Wilson, A. (1992), Aubrey Wilson's Marketing Audit Checklists: A Guide to EffectiveMarketing Resource Realization, 2nd Edition, London, McGraw Hill.