Embed Size (px)

Citation preview

4Brazilian Institute of Corporate Governance

Corporate Governance Handbooks

Sustainability Guide for CompaniesAn Overview for Directors and Senior Executives

Handbook 4 - Sustainability Guide for Companies.indd 1 16/05/2009 14:45:50

Handbook 4 - Sustainability Guide for Companies.indd 2 16/05/2009 14:45:50

Sustainability Guide for CompaniesAn Overview for Directors and Senior Executives

Foreword by Mervyn E. King

2008

Handbook 4 - Sustainability Guide for Companies.indd 3 16/05/2009 14:45:51

• • • • Brazilian Institute of Corporate Governance

The Brazilian Institute of Corporate Governance (IBGC, to use its Portuguese acronym) is dedicated exclusively to the promotion of corporate governance in Brazil. It is the country’s main advocate of corporate governance practices and debates, and has achieved national and international recognition.

Founded on November 27th, 1995, IBGC – a Brazilian non-profit organization – aims “to be a reference in corporate governance, contributing to the sustainability of organizations and influencing key agents in our society towards greater transparency, justice and responsibility”.

Chairman of Board of DirectorsJosé Guimarães Monforte

Vice-Presidents Gilberto Mifano and Mauro Rodrigues da Cunha

Board MembersCelso Giacometti, Eliane Lustosa, Fernando Mitri, Francisco Gros, João Pinheiro Nogueira Batista and Ronaldo Veirano.

Executive CommitteeEdimar Facco, Eliane Lustosa and Ricardo Veirano

General SecretaryHeloisa B. Bedicks

For further information on the Brazilian Institute of Corporate Governance, please visit the website: www.ibgc.org.br. To become an IBGC member please call: + 55 (11) 3043-7008.

B827s Brazilian Institute of Corporate Governance. Sustainability Guide for Companies: An Overview for Directors and Senior Executives / Brazilian Institute of Corporate Governance; coordination by Carlos Eduardo Lessa Brandão and Homero Luís Santos; foreword by Mervyn E. King; translation by Jodie Thorpe. São Paulo, SP: IBGC, 2008. (Corporate Governance Notebooks Series, 4).

48p.

Translated from: Guia de Sustentabilidade para Empresas, c2007. ISBN: 978-85-99645-08-06

1. Corporate Governance. 2. Sustainable Development. 3. Sustainability. I. Title. II Brandão, Carlos Eduardo Lessa, coord. III Santos, Homero Luís, coord. IV.Thorpe, Jodie, trans.

CDU – 658.4

Librarian in charge: Mariusa F. M. Loução – CRB-12/330

Handbook 4 - Sustainability Guide for Companies.indd 4 16/05/2009 14:45:51

• • • • Credits

This work was carried out by the Sustainability for Companies Study Group (GESE), established by the IBGC.

• • • • Acknowledgements

To Professor Mervyn King, who had the kindness to write the foreword for this document.

To the staff of IBGC, who gave their support to the GESE, and to Cristine Zanarotti Prestes Rosa, who, in addition to being secretary for the project, contributed so much to the content of this document.

To the GESE members who are also members of IBGC, who gave their time so generously for the development of corporate governance.

To the GESE members who, even without being IBGC members, worked in the spirit of collaboration and contributed their knowledge and experience to enrich the content of this document.

• • • • Contributions

Members Non-membersCibele de Macedo Salviatto Alvaro Plínio PurezaCláudio Pinheiro Machado Filho Antônio Carlos Lopes SimasFernando Foz Macedo Aron BelinkyHeloisa B. Bedicks Christina Carvalho PintoLeonardo Viegas Clarissa LinsPaulo Bellotti Diva Irene da Paz VieiraPaulo Conte Vasconcellos Elisabeth Barbieri LernerPaulo Vanca Fábio FeldmannRicardo Pinto Nogueira Giovanni BarontiniRoberto Sousa Gonzalez Luciana BrennerRogério Gollo Marina SchurrRogério Marques Patrícia de Caires SogayarSandra Guerra Tarcila Reis UrsiniSimone de Carvalho Soares

• • • • Coordination

Carlos Eduardo Lessa Brandão (IBGC’s Chief Knowledge Officer)Homero Luís Santos (Chairman of GESE)

Handbook 4 - Sustainability Guide for Companies.indd 5 16/05/2009 14:45:51

ContentsForeword by Mervyn E. King 6

Introduction 8

Context 10 1.1 The global context and its impact on companies 11 1.2 The connection with IBGC Corporate Governance Best Practice 12

Concepts 13 2.1 Sustainability 14 2.2 Sustainability in companies 15 2.2.1 An approach to doing business 15 2.2.2 Intangibles and externalities 16

Sustainability and business viability 18 3.1 Sustainability and the economic value of companies 19 3.2 Impact on reputation and license to operate 20 3.3 Correlation between sustainability and business success 20

The stages of sustainability in companies 22 4.1 The five stages 23 4.2 Transitions between stages 24

Application 25 5.1 Sustainability in institutional definitions and strategy 26 5.1.1 Embedding in institutional definitions 26 5.1.2 Connection with strategy 26 5.2 Sustainability and operations 27 5.2.1 Connection with operations 27 5.2.2 Setting goals and monitoring results 27 5.2.3 Compensation (remuneration) 28 5.3 Sustainability in corporate governance 28

4

3

21

5

Handbook 4 - Sustainability Guide for Companies.indd 6 16/05/2009 14:45:51

Annexes 30 6.1. Recent history of sustainability 31 6.2. Business initiatives 32 6.3. The Triple Bottom Line (TBL) and the five-capital model 34 6.4. Sustainability tools, standards and indicators 35 6.4.1 Principles-based standards 35 6.4.2 Performance standards 35 6.4.3 Process standards 36 6.4.4 Hybrid standards 36

References 39

Glossary 42

6

78

Handbook 4 - Sustainability Guide for Companies.indd 7 16/05/2009 14:45:51

There is a gap between the financial and economic value of a company. The price of any share

on any stock exchange in the world will not equal book value. This is because traditional accounting does

not take account of intangibles or the so-called non-financial aspects.

In the 21st Century, intangibles can be more valuable than tangible assets. One therefore has

an iceberg effect, where the tangibles are accounted for and what is really valuable is not even seen on

the balance sheet or on the profit and loss statement. Intangibles such as goodwill, brand, reputation, the

quality of governance, the quality of management, the human rights record of a company, social and labor

issues and a company’s treatment of the eco-systems in the community in which it operates have all become

material issues today.

There is growing public attention on key sustainability issues. The best example is climate

change. When companies are asked why they report on sustainability issues, their answers are varied. For

example, “we do it because our competitors are doing it”; “we have found that strategically we are able to

manage reputation and brand in a more informed manner”; “our stakeholders want it”; and perhaps most

importantly of all, “it improves our risk management”. The latter is probably the most significant because

sustainability issues can become huge risk issues for a company.

Sustainability issues can be grouped under the headings of Economic, Environmental and Social.

It is important for companies to be able to report on the economic impact which its operations have had, both

positively and negatively, on the community in which it operates during the year under review. The company

should also be able to report on how it intends to enhance the positive aspects and eradicate or ameliorate

the negative aspects of the company’s operations in the community in which it operates in the year ahead.

It should also report on the company’s impact on the community’s eco-systems. People, planet

and profit can no longer be separated.

Foreword

6 • Sustainability Guide for Companies

Handbook 4 - Sustainability Guide for Companies.indd 8 16/05/2009 14:45:51

Human rights and social issues are also significant sustainability issues. Thus, for example, in

regard to procurement contracts, a company needs to make sure that their suppliers are not discriminatory,

there is freedom of association and they do not use child labor. If they do, it can have material reputational

damage for the company. Likewise, a company should check whether its suppliers have in place proper

occupation, health and safety measures in producing the goods received by the company.

One of the principles of good governance is that a board of directors has a positive duty to give

strategic direction to a company. In developing a strategy for the company, both short- and long-term issues

have to be considered. In considering the latter, one has to take account of sustainability issues. It follows

as a matter of logic that governance, strategy and sustainability have become inseparable. One can no

longer plan strategically without having regard to sustainability issues.

Stakeholders want forward looking information to be given by the preparers of annual statements.

The balance sheet and the profit and loss statement are backward-looking and a photograph of a moment

in time of what is happening in the company. The stakeholders need to make a more informed assessment

of the true economic value of a company and the only way this can be done is ensuring that reports contain

enough information that stakeholders can make such an assessment.

It is appropriate that the IBGC has issued a Sustainability Guide for Companies, because the

three factors of people, planet and prosperity are interdependent in the 21st Century.

Mervyn E King SCChairman of the Board of GRI – Global Reporting Initiative, First Vice-President of the Institute of Directors, Southern Africa (IoD-SA) and member of the Private Sector Consultative Group of the GCGF – Global Corporate Governance Forum (World Bank). Professor King was a South African Supreme Court Judge and is the Chairman of the IoD-SA Committee responsible for the writing and revision of the King Report on Corporate Governance in South Africa.

Sustainability Guide for Companies • 7

Handbook 4 - Sustainability Guide for Companies.indd 9 16/05/2009 14:45:51

To celebrate its 10th Anniversary in 2005, the Brazilian Institute of Corporate Governance (or IBGC, to

use its Portuguese acronym) launched a series of publications entitled Corporate Governance Handbooks.

The object of this initiative is to bring practical information to the market which will help improve

corporate governance processes and help board members and other administrators perform their duties, thereby

contributing to improved business performance, increased investor trust, and the flow of financial resources to

the company.

IBGC’s Corporate Governance Handbooks are edited in three series according to their content:

Legal Governance Documents, Documents on Governance Structures and Processes, and Special Governance

Themes. They are the result of contributions, suggestions and recommendations made by the Institute’s

members, who make up its various working groups.

Because of the broad scope of the topic, this document was prepared by the Sustainability for

Companies Study Group (GESE), established for this purpose by IBGC’s Knowledge Center. Study groups permit

a greater participation of experts who are not necessarily associated with the Institute.

Introduction

8 • Sustainability Guide for Companies

Handbook 4 - Sustainability Guide for Companies.indd 10 16/05/2009 14:45:51

The present Sustainability Guide for Companies is part of the Special Governance Themes series. It

aims to present to directors and officers and other corporate governance agents the topic of sustainability from the

perspective of corporate governance, linking it to corporate philosophy and strategy. It is an effort to internalize

the new concepts and tools in management processes and to provide a decision-making model that takes into

account economic-financial and socio-environmental aspects, as well as the short- and long-term interests of

diverse stakeholders.

This document is directed primarily at for-profit organizations. However, corporate governance and

sustainability principles may be applied to a variety of organizations of different sizes, structures and objectives.

This initiative does not seek to provide detailed concepts and practices, but rather to promote a

minimum common language for both topics (corporate governance and sustainability), and to signal ways in which

organizations can understand sustainability as an element of management excellence. From a wider perspective,

we believe that ignorance of these topics will be unacceptable for organizations with a long-term vision.

Sustainability Guide for Companies • 9

Handbook 4 - Sustainability Guide for Companies.indd 11 16/05/2009 14:45:51

Context

1

1.1 The global context and its impact on companies 11 1.2 The connection with IBGC Corporate Governance Best Practice 12

Handbook 4 - Sustainability Guide for Companies.indd 12 16/05/2009 14:45:51

Sustainability Guide for Companies • 11

1.1 The global context and its impact on companies

a) Understanding the scope of corporate responsibility is becoming an inevitable priority for business leaders around the world. Society is increasingly scrutinizing the environmental, social and economic impacts of corporate activities.

b) Such scrutiny stems from increasing environmental and social degradation, which impacts all countries, regardless of income level, and which may jeopardize the very continuity of civilization. 1,2

c) For companies, this scrutiny can be seen as a source of opportunity, innovation and competitive advantage rather than of new costs and constraints to their activities. However, this requires a long-term, strategic focus, since social and environmental aspects will sooner or later be reflected in financial statements and companies’ economic and market value, and can have a decisive influence on their longevity.

d) From the social perspective, companies will be able to broaden the range of their

stakeholders, allowing them to identify risks and opportunities that had not been taken into account previously. From the environmental perspective, companies will be able to go beyond eco-efficiency initiatives and start to redesign products and services and re-assess management practices and business models. In terms of long-term economic value creation, companies will shift to seeking “optimum profits” rather than “maximum profits”, taking into account how results are obtained.

e) Investors, directors and officers face a new reality that demands an understanding of the broader role of companies in society, beyond their role as market agents. This requires the development of a broader vision, which recognizes that companies form part of society, and this, in turn, forms an integrated system with the natural environment.

1 - Since the 1980s, the growing human demand for natural resources is exceeding supply by more than 20%, impacting the quality of life of populations. See “One Planet Business: creating value within planetary limits”, WWF, 2007 - www.sustainability.com/insight/research-article.asp?id=941

2 - See “Living Planet Report” - http://assets.panda.org/downloads/living_planet_report.pdf

Handbook 4 - Sustainability Guide for Companies.indd 13 16/05/2009 14:45:51

12 • Sustainability Guide for Companies

1.2 The connection with IBGC Corporate Governance Best Practice

a) IBGC’s “Code of Best Practice of Corporate Governance” is based on four basic principles: Transparency, Fairness, Accountability and Corporate Responsibility.

b) These four principles are integrated in the various aspects of corporate sustainability, including long-term strategy, risk management, consideration of intangible aspects, quality of stakeholder relations and responsibility for actions and omissions that, sooner or later, may affect companies’ economic value.

c) According to the fourth principle, Corporate Responsibility, directors and officers must address the longevity of their organizations and therefore incorporate social and environmental concerns in defining their business and operations. This implies a broader vision of corporate strategy, which takes into account a wider range of corporate relationships.

d) Due to its direct management benefits and in order to facilitate access to capital, good corporate governance is being rapidly adopted by companies. It can therefore act as both a “gateway” for introducing sustainability into the corporate environment and a “guardian” of the company’s alignment with sustainability.

Handbook 4 - Sustainability Guide for Companies.indd 14 16/05/2009 14:45:51

Concepts

2

2.1 Sustainability 142.2 Sustainability in companies 15 2.2.1 An approach to doing business 15 2.2.2 Intangibles and externalities 16

Handbook 4 - Sustainability Guide for Companies.indd 15 16/05/2009 14:45:51

14 • Sustainability Guide for Companies

2 Concepts

2.1 Sustainability

a) In economic terms, sustainability means living on the “income” the planet provides rather than on its “capital”, the so-called natural capital. All economic activity depends on this capital. 3

b) Natural capital is responsible for providing environmental services, i.e. the benefits that human beings get from nature, produced by interactions within ecosystems such as oxygen production, carbon sequestration, soil formation, water, timber and fiber provision, climate regulation, and aesthetic, spiritual and leisure values. Many of these services are essential for human beings.

c) The notion of social capital4 used in this document is associated with the quality of relationships between people and groups within society, for which trust is an essential factor. Social capital influences the degree of stability and prosperity, and is crucial in the quest for sustainability.

d) Sustainable development is understood as development that meets the needs of the present without compromising the ability of future generations to meet their own needs. This definition makes it possible to balance the interests of environmental conservation and improving the quality of human life. It is the criterion based on which human impact on the environment must be assessed.5

e) The idea of sustainability has been gaining momentum in recent years. Because of the diversity of possible definitions and approaches, it is more effective to define “what sustainability is not” in the broadest sense. There are four basic conditions through which society may become unsustainable, i.e., undermine its own future viability:6

i) the systematic increase in nature in the concentration of substances extracted from the Earth’s crust;

3 - See “Ecological Footprint” in the Glossary.4 - Not to be confused with the Brazilian notion of corporate capital, reflected in currency, represented by the amount

invested by the shareholders of a company which is mentioned in the company´s By-laws or Articles of Association and divided in shares (in the corporations) or quotas (in the limited liability companies, cooperatives and other types of legal entities).

5 - WCED (1998).6 - See “The Natural Step” in the Glossary.

Handbook 4 - Sustainability Guide for Companies.indd 16 16/05/2009 14:45:51

Sustainability Guide for Companies • 15

7 - Diamond (2005).8 - “Rio Declaration on the Environment and Development” (1992), Principle 15: www.unep.org/Documents.Multilingual/Default.asp?DocumentID=78&ArticleID=1163. 9 - In considering the Precautionary Principle, it is relevant to understand the concepts of risk (identified future events for

which the probability of occurrence can be estimated), uncertainty (identified future events for which the probability of occurrence cannot be estimated) and ignorance (future events which, at the time of analysis, cannot be identified, much less quantified). See Faber, Manstetten and Proops (1996, 209-11).

ii) the systematic increase in nature in the concentration of substances produced by society;

iii) the systematic weakening of biological diversity and of the cycles that sustain natural processes;

iv) the submission of people to conditions that systematically undermine their ability to meet their fundamental needs.

f) In the economy, industrial processes and logistics are based on a linear logic

(extraction – production – use – final disposal), while in nature processes are cyclical, non-linear and self-regulating through the interaction between eco-systems (zero waste).

g) The effects resulting from human action upon social and environmental systems are

often non-linear, irreversible and difficult to measure. Certain events may have their effects spread through time, due to a feedback cycle that amplifies the initial effects.7

h) In the face of events resulting from complex systems such as climate (the consequences of global warming, for example, may go beyond those predictable by science), the Precautionary Principle should be followed. The Principle states that “where there are threats of serious or irreversible damage, lack of full scientific certainty shall not be used as a reason for postponing cost-effective measures to prevent environmental degradation”. 8,9

2.2 Sustainability in companies

2.2.1 - An approach to doing business

a) From a corporate perspective, economic and financial viability is vital; without it the company does not survive. However, it is becoming imperative for the quality of corporate performance to seek alignment with a vision of sustainability in the broader sense.

b) For the private sector the concept of sustainability represents an innovative approach to doing business, in the sense of sustaining economic and financial viability while preserving environmental integrity for present and future generations, and building more harmonious societal relationships, resulting in a solid and positive reputation.

Handbook 4 - Sustainability Guide for Companies.indd 17 16/05/2009 14:45:51

16 • Sustainability Guide for Companies

c) This approach incorporates the best corporate governance practices and has strategic characteristics, since it facilitates the identification of risks and opportunities, enables the company to preserve and create value, increases the probability of business continuity (longevity) and, simultaneously, contributes to sustainable development.

d) As a result, the company will be able to improve the quality of social capital (by respecting cultural diversity and the interests of the various stakeholders directly or indirectly involved in the business or impacted by it) and reduce – or optimize – the use of natural resources and the company’s impact on the environment.

e) Approaching business in the light of sustainability allows companies to consider, in a more structured manner, the local and global aspects that are increasingly directly affecting their economic and financial results, and to respond to new societal expectations regarding environmental, social justice and generational issues.

f) These themes have the potential to affect the business environment because they are closely linked to the behavior of shareholders, financial investors, clients, suppliers, employees, communities and legislators who are involved, directly or indirectly, in the company’s activities.

g) Companies that are alert to sustainability issues develop the ability to anticipate environmental, social, legal and institutional trends, and benefit strategically as a result.

h) There still exists a certain juxtaposition regarding the various definitions of terms that refer, to a greater or lesser degree, to the scope of sustainability in companies, such as Corporate Social Responsibility, Social Responsibility and Corporate Sustainability.

i) The promotion or funding of philanthropic, cultural, social and environmental projects must be clearly related to the company’s social goals or contribute in a readily identifiable way to business value. If not, these activities can be considered a corporate governance problem, since the directors and officers would be exceeding their mandates.10

2.2.2 - Intangibles and externalities

a) The perspective of sustainability will require the company to face situations in which it will struggle to quantify certain impacts resulting from its actions with respect to their inclusion in financial accounts (intangibles) or their financial value (externalities).

10 - See Porter and Kramer (2006) for a structured approach directed to business strategy.

Handbook 4 - Sustainability Guide for Companies.indd 18 16/05/2009 14:45:51

Sustainability Guide for Companies • 17

b) Intangible assets are rights, with no physical representation, which give the company a unique or preferential position in the market, i.e. they contribute to a company’s economic value. Some aspects may be included in financial accounts (e.g.: expenditures related to brands and patents, public concessions, copyright, licenses) while others, despite their contribution to the value of the company, are not (e.g.: customer portfolio, company reputation).

c) Economic externalities are the effects of a transaction on third parties that did not consent to or participate in it. They result, therefore, from activities that involve the involuntary imposition of costs or benefits upon third parties who do not have the chance to prevent them, the obligation to pay for them or the right to compensation. Externalities may be positive (e.g.: increased property value due to better lighting and road paving) or negative (e.g.: decreased property value due to soil contamination from a neighboring property).

d) Many environmental services and social capital benefits are externalities, i.e., the company benefits but does not pay for them, which encourages their unsustainable use.

e) Responsibility for externalities places business ethics in a broader – even global – behavioral perspective, which impacts a company’s reputation.

Handbook 4 - Sustainability Guide for Companies.indd 19 16/05/2009 14:45:51

Sustainability and business viability

3

3.1. Sustainability and the economic value of companies 193.2. Impact on reputation and license to operate 203.3. Correlation between sustainability and business success 20

Handbook 4 - Sustainability Guide for Companies.indd 20 16/05/2009 14:45:51

Sustainability Guide for Companies • 19

3.1 Sustainability and the economic value of companies

a) From a financial perspective, the broader and more consistent a company’s understanding of the dynamics of the actors and systems that affect it, the greater its chances to remain profitable and in operation, i.e., of being economically viable.

b) Financial statements reflect tangible aspects from the point of view of accounting principles. Other, intangible, aspects will impact those statements. One example is the company’s reputation, which impacts its ability to generate revenues, both in the short and long term.

c) Situations involving sustainability will be reflected, sooner or later, in financial statements, in the economic and market value of the company.

d) Revenues, costs and expenses, capital invested and the cost of the capital used to finance the business are the main drivers of both the company’s economic value and of the financial valuation of investments and divestments.11

e) The following is a list of potential impacts on value drivers resulting from aspects linked to sustainability:

i) Revenues: reaction of the client base to the company’s position; identification of market opportunities due to a better understanding of stakeholders; anticipation of changes in the regulatory environment; eco-efficiency generating new products.

ii) Costs and expenses: efficiency in natural resource use in production processes; workforce retention and productivity; restrictions or preferences on the part of suppliers.

iii) Capital invested, understood as the working capital and fixed assets that generate the company’s operations: greater or lesser degree of efficiency in natural resource use; identification, in advance, of changes and restrictions in the supply of certain resources.

iv) Cost of capital, related to the perceived risk of the company: ease or difficulty in accessing either debt or equity capital.

11 - The value drivers are applied, for example, in the discounted cash flow (DCF) method used for the financial evaluation of business opportunities by the great majority of companies, financial analysts (including capital market analysts and investment banks), books and publications. See Bruner et al. (1998).

Handbook 4 - Sustainability Guide for Companies.indd 21 16/05/2009 14:45:51

20 • Sustainability Guide for Companies

f) Reassessing value drivers can inspire a strategic rethink of the company’s business model, leading to improvements or even its replacement with another more adequate model.

3.2 Impact on reputation and license to operate

a) Measuring economic and financial performance has been one of the main concerns of companies, and is based on diverse financial and accounting indicators such as return on investment, revenue growth, growth in profit margins and discounted cash flow, among others. On the other hand, “intangible assets” contribute decisively to the value of a company.

b) The company’s reputation, which is part of its economic value, is a consequence of its set of actions and positions through time.

c) The adoption by companies of a responsible approach results, in time, in tangible gains such as cost efficiency and effectiveness and greater productivity. Responsible practices produce additional stimuli for internal improvements, such as clarity and alignment of principles, purpose, policies and practices, with an impact on management quality.

d) Ultimately, every company needs a social license to initiate and maintain operations through time. Part of this license is formal (based on laws, regulations, etc.) and another broader and more intangible part is informal and reflects the degree of societal acceptance and approval of a company’s activities. It is the latter which is subject to a new focus of attention by directors and officers, in order to cultivate that license or avoid the risk of its erosion or loss.

3.3 Correlation between sustainability and business success

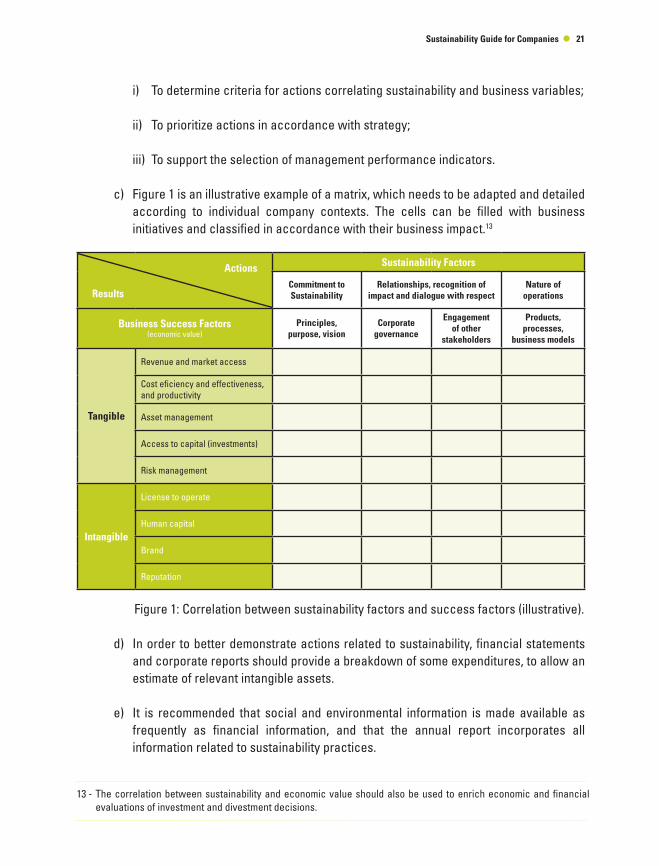

a) By considering environmental aspects and stakeholder interests broadly, the company can establish a structured agenda of issues relevant for identifying risks and opportunities associated, directly or indirectly, with the economic performance of the business, enriching strategic discussions and fostering innovation.

b) The relationship between the main factors that influence the company’s economic value and sustainability factors may be illustrated using a matrix:12

12 - Inspired by “Developing Value: The business case for sustainability in emerging markets”, published jointly by SustainAbility, IFC and the Ethos Institute. See www.sustainability.com/developing-value.

Handbook 4 - Sustainability Guide for Companies.indd 22 16/05/2009 14:45:51

Sustainability Guide for Companies • 21

13 - The correlation between sustainability and economic value should also be used to enrich economic and financial evaluations of investment and divestment decisions.

i) To determine criteria for actions correlating sustainability and business variables;

ii) To prioritize actions in accordance with strategy;

iii) To support the selection of management performance indicators.

c) Figure 1 is an illustrative example of a matrix, which needs to be adapted and detailed according to individual company contexts. The cells can be filled with business initiatives and classified in accordance with their business impact.13

Figure 1: Correlation between sustainability factors and success factors (illustrative).

d) In order to better demonstrate actions related to sustainability, financial statements and corporate reports should provide a breakdown of some expenditures, to allow an estimate of relevant intangible assets.

e) It is recommended that social and environmental information is made available as frequently as financial information, and that the annual report incorporates all information related to sustainability practices.

Actions

Results

Sustainability Factors

Commitment to Sustainability

Relationships, recognition of impact and dialogue with respect

Nature of operations

Business Success Factors (economic value)

Principles, purpose, vision

Corporate governance

Engagement of other

stakeholders

Products, processes,

business models

Tangible

Revenue and market access

Cost eficiency and effectiveness, and productivity

Asset management

Access to capital (investments)

Risk management

Intangible

License to operate

Human capital

Brand

Reputation

Handbook 4 - Sustainability Guide for Companies.indd 23 16/05/2009 14:45:52

The stages of corporate sustainability

4

4.1 The five stages 234.2 Transitions between stages 24

Handbook 4 - Sustainability Guide for Companies.indd 24 16/05/2009 14:45:52

Sustainability Guide for Companies • 23

4.1 The five stages

a) There are diverse systems to map the alignment of companies with respect to sustainability, each with its own nomenclature and language.14

b) Companies can be classified in stages based on their treatment of sustainability in relation to external factors (current legislation and regulation) and to internal ones (integration with strategy or with company principles and purpose):

i) Legal pre-compliance: in this stage the company sees profit as its sole purpose, ignores sustainability and stands against any related regulation, as this would mean additional expense.

ii) Legal Compliance: the company manages its liabilities by complying with labor, environmental, and health and safety legislation. Social and environmental actions are treated as costs and sustainability is paid lip service.

iii) Beyond legal compliance: the company takes a proactive approach, understanding it can save costs through eco-efficiency initiatives, and recognizing that social and environmental investments can minimize operational uncertainties and risks, improve reputation and have a positive impact on economic value. Sustainability initiatives are concentrated within specialized departments instead of being institutionalized.

iv) Integrated strategy: the company re-brands itself and integrates sustainability in its key business strategies. The board of directors is the main forum for dealing with sustainability. The company creates economic value through differentiated initiatives that benefit stakeholders. Instead of costs and risks, it perceives investments and opportunities, develops clean products and services, understands the life cycle of its products and services, and benefits from sustainability initiatives.

v) Purpose & passion: the company adopts sustainability practices because it understands that it does not make sense to contribute to an unsustainable world. Sustainability initiatives are not presented to the board of directors, they emanate from it.

14 - See Willard (2005). For an evaluation of the stages of responsible business practices in 108 countries, see “The state of responsible competitiveness”, in the study “Making sustainable development count in global markets”.

www.accountability21.net/publications.aspx?id=878&terms=Making+sustainable+development+count+in+ global+markets

Handbook 4 - Sustainability Guide for Companies.indd 25 16/05/2009 14:45:52

24 • Sustainability Guide for Companies

4.2 Transitions between stages

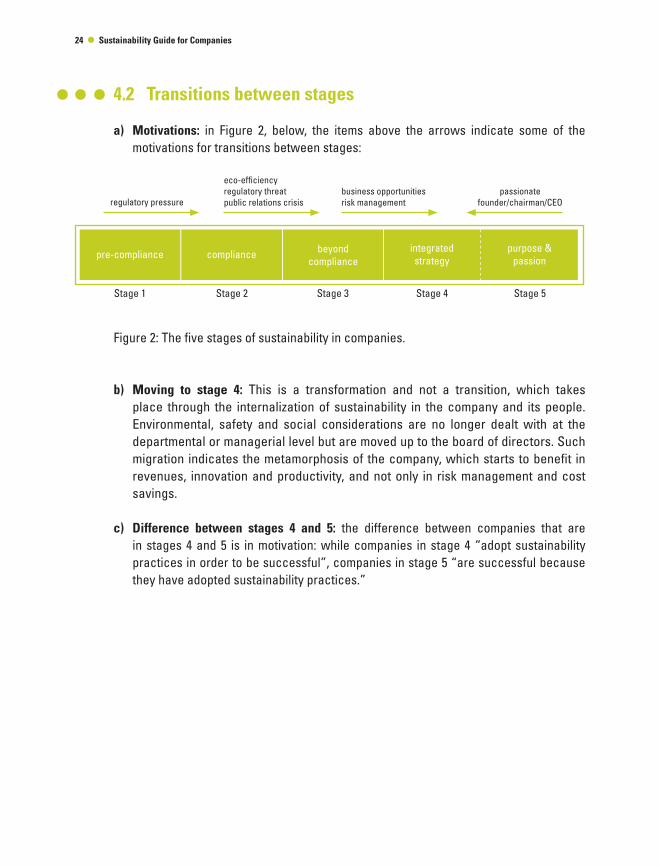

a) Motivations: in Figure 2, below, the items above the arrows indicate some of the motivations for transitions between stages:

Figure 2: The five stages of sustainability in companies.

b) Moving to stage 4: This is a transformation and not a transition, which takes place through the internalization of sustainability in the company and its people. Environmental, safety and social considerations are no longer dealt with at the departmental or managerial level but are moved up to the board of directors. Such migration indicates the metamorphosis of the company, which starts to benefit in revenues, innovation and productivity, and not only in risk management and cost savings.

c) Difference between stages 4 and 5: the difference between companies that are in stages 4 and 5 is in motivation: while companies in stage 4 “adopt sustainability practices in order to be successful”, companies in stage 5 “are successful because they have adopted sustainability practices.”

Stage 1

regulatory pressure

eco-efficiencyregulatory threatpublic relations crisis

business opportunitiesrisk management

passionatefounder/chairman/CEO

pre-compliance compliance beyondcompliance

integratedstrategy

purpose &passion

Stage 2 Stage 3 Stage 4 Stage 5

Handbook 4 - Sustainability Guide for Companies.indd 26 16/05/2009 14:45:52

Application

5

5.1 Sustainability in institutional definitions and strategy 26 5.1.1 Embedding in institutional definitions 26 5.1.2 Connection with strategy 26

5.2 Sustainability and operations 27 5.2.1 Connection with operations 27 5.2.2 Setting goals and monitoring results 27 5.2.3 Compensation (remuneration) 28

5.3 Sustainability in corporate governance 28

Handbook 4 - Sustainability Guide for Companies.indd 27 16/05/2009 14:45:52

26 • Sustainability Guide for Companies

5 Application

5.1 Sustainability in institutional definitions and strategy

5.1.1 - Embedding in institutional definitions

a) The mission and vision of the organization and its business must express the concept of sustainability formally and unequivocally.

b) The formal declaration of the organization’s values and code of conduct must provide guidance for directors and officers and be a tool for communicating to society the decision to adopt the principles of sustainability.

c) In mergers, acquisitions and associations, the principles and practices that rule sustainability must be preserved in the institutional definitions of the resulting entities.

d) Conglomerates should strive to ensure coherence of principles and consistency of sustainability practices across their various businesses and corporate activities.

5.1.2 - Connection with strategy

a) Sustainability values and practices should be sources of inspiration in the formulation of business strategies.

b) The principles of sustainability should be applied to the business model, of which they should be part, and not only to peripheral activities.

c) Embedding sustainability in business strategies, right from project conception or product and service development, allows companies to maximize opportunities and strengthen the long-term economic value of the organization.

d) Possible negative externalities generated by the organization must be studied with a view to internalizing them in business strategies, seeking to reduce potential or real risks and contribute to long-term economic value.

Handbook 4 - Sustainability Guide for Companies.indd 28 16/05/2009 14:45:52

Sustainability Guide for Companies • 27

e) Initiatives to align business activities with sustainability must be evaluated for their long-term economic and financial viability (business case), taking into account the interests of partners and other stakeholders.

f) Sustainability practices adopted by the company must be disseminated throughout the entire value chain, both upstream (in the activities that precede the company’s direct participation, linked, for instance, to suppliers) and downstream (in the activities that follow the company’s direct participation, related, for example, to clients), through formal mechanisms duly registered in contracts or partnership agreements.

5.2 Sustainability and operations

5.2.1 - Connection with operations

a) The directives fixed by the strategy must be converted into business processes.

b) Attention must be given to situations that involve physical or geographic expansion of activities, technological innovation, creation of new products and services, or modification of those already existing (involving life cycle assessment of the products and services).

c) When adjusting processes to align with strategies that incorporate the principles of sustainability, positive and negative economic externalities must be considered. These externalities must be balanced by taking into account both the expectations of stakeholders (internal to the company or located in the company’s economic and social environment) and the impacts on the environment and future generations.

d) Contracts or agreements with those in the value chain must be monitored to ensure their alignment with the company’s social and environmental practices.

5.2.2 - Setting goals and monitoring results

a) Any system of indicators must ensure that institutional discourse and actions are duly aligned (“walk the talk”). In this sense, it is recommended that initiatives are submitted to independent third-party verification, which should not only verify the execution of proposed actions and the accuracy of resource allocation, but also the actual results obtained versus stated objectives.

b) Indicators must exist that allow the quantification and specification of actual impacts related to the dimensions of sustainability contained in strategies and operational processes.

Handbook 4 - Sustainability Guide for Companies.indd 29 16/05/2009 14:45:52

28 • Sustainability Guide for Companies

c) Quantification allows long-term goals to be set and monitored and allows verification at the end of the process as to whether or not the agreed result was achieved.

d) The efforts of the company (such as “the number of people trained by a project”) should not be treated as “outcomes”; the real outcomes are the benefits actually obtained (for example, the extent to which the training provided by the project improved, or not, the lives of those who received it).

5.2.3 - Compensation (remuneration)

a) If the results agreed upon by the directors, officers and other managers are achieved, it is essential that they are recognized, since they involve the application of a new paradigm.

b) The performance appraisal system for directors, officers and other managers must show a coherent alignment between business strategy, short-, medium- and long-term goals and remuneration.

c) Ensuring a financial reward for directors, officers and other managers for achieving expected results will determine the success of the practice of management for sustainability.

d) The remuneration system must reflect the degree of insertion of sustainability in institutional definitions and its relation with business strategy, operational processes and management indicators.

e) By relating remuneration to performance appraisals which include social and environmental aspects, directors, officers and managers should also be rewarded for short-term actions for which results will be only seen in the medium and long term.

f) For the effectiveness of these remuneration measures, the benefits offered for good social and environmental performance must be motivating, even compared to those related to economic performance. For example: nothing is achieved by offering $ 1 to “keep trees standing” if the executive will earn a $ 2 bonus for cutting them down.

5.3 Sustainability in corporate governance

a) It is at the highest administrative levels that management values and philosophy are addressed, of which sustainability principles must form a part.

Handbook 4 - Sustainability Guide for Companies.indd 30 16/05/2009 14:45:52

Sustainability Guide for Companies • 29

b) It is essential that the board of directors and the CEO are convinced of the strategic importance of sustainability, assuring the leadership and commitment necessary to address the issue within the organization.

c) Sustainability may form part of the scope of a specific board committee, as a temporary measure to support its integration in the organization’s daily activities, until it is naturally embedded in activities connected to strategy and operations.

d) The board of directors should support and back up management in the process of attaining long-term goals and in reducing negative externalities, taking care that management does not hasten short-term actions that could generate negative externalities in the medium and long term.

e) Emphasis should be placed on training board members on the issues that are relevant to embedding sustainability in the organization.

f) The board of directors must be aware of the changes taking place in the responsibility of companies, shareholders, directors and officers, including with respect to fiduciary duty.15

g) There are an increasing number of tools available to guide companies in incorporating sustainability in management processes. It falls to the board of directors to guide the process of defining tools to be adopted so that they have a connection with strategic priorities. The tools may be grouped in accordance with their approaches: based on principles, on performance, on processes, or hybrid standards.16

15 - See Annex 6.2.a.16 - See Annex 6.4.

Handbook 4 - Sustainability Guide for Companies.indd 31 16/05/2009 14:45:52

Annexes

6

6.1 Recent history of sustainability 316.2 Business initiatives 326.3 The Triple Bottom Line (TBL) and the five-capital model 346.4 Sustainability tools, standards and indicators 35 6.4.1 Principles-based standards 35 6.4.2 Performance standards 35 6.4.3 Process standards 36 6.4.4 Hybrid standards 36

Handbook 4 - Sustainability Guide for Companies.indd 32 16/05/2009 14:45:52

Sustainability Guide for Companies • 31

6.1 Recent history of sustainability

The nuclear weapons used in World War II led the world to think collectively, because the consequences could affect everyone. The creation of the United Nations (UN), in 1945, was one of the results of such concern.

In addition to nuclear weapons, other potential global impacts have been identified. The Club of Rome, created in 1970 by an international group of executives, scientists and leaders of governmental and non-governmental organizations, led a study to understand the interconnection between different aspects that could put humankind at risk, such as population growth, pollution, economic limits and social conflicts. In 1972 The limits to growth17 was published, indicating that environmental limits (resource use and waste generation) could have a significant impact on global development.

Although it was received with skepticism, the Club of Rome’s report was a contributing factor which led the United Nations to organize, in 1972, the UN Conference on the Human Environment, known as the Stockholm Conference, with the participation of more than 100 countries, including Brazil. The resulting Stockholm Declaration brought the impact of the use of natural resources in the current model of economic growth to the international political agenda.

In 1983 the Vienna Convention was signed, the first instrument designed to foster actions to deal with a global environmental problem: the preservation of the ozone layer, essential for life on Earth. The deterioration of the ozone layer is due mainly to the use of CFC (chlorofluorocarbon) gases. At the time, the issue was not yet a priority: only 20 countries participated. In 1989, however, the Montreal Protocol came into force, after it was ratified by 29 nations plus the European Union, which together produced 89% of the substances that harm the ozone layer. The goal of the Protocol is to eliminate the use of products harmful to ozone by 2010.

In 1987, the World Business Academy was founded as a forum to deal with the role and responsibility of business in the face of moral, environmental and social challenges. In 1993 the Club of Budapest, a humanistic association of scientists, writers, businessmen and political and spiritual leaders, was founded with a similar objective.

Also in 1987 the document Our common future - known as the “Brundtland Report”18 – was produced, the result of the UN’s World Commission on Environment and Development. It was in this report that one of the best known definitions of sustainable development was first published: “development that meets the needs of the present without compromising the ability of future generations to meet their own needs”.

17 - See Meadows et al. (1972).18 - See WCED (1998).

Handbook 4 - Sustainability Guide for Companies.indd 33 16/05/2009 14:45:52

32 • Sustainability Guide for Companies

The 1990s also witnessed international agreements regarding sustainability. In 1992, in the United Nations Conference on Environment and Development, held in Rio de Janeiro (Rio Earth Summit), Agenda 21 was developed - a broad plan signed by 178 UN member countries involving global, regional and local actions. It is an ambitious agenda for sustainable development – and not just the environment.

In 1997 the Kyoto Protocol was signed, within the United Nations Framework Convention on Climate Change. It addresses the issue of global warming and changes to the climate caused by human activity in recent centuries, involving principally the burning of fossil fuels, with significant consequences for human beings and other forms of life on Earth.

The first UN proposal dealing with the theme of corporate sustainability was the Global Compact, launched in 2000 as a personal initiative of the then secretary-general Kofi Annan, aiming at putting a human face on globalization. In that same year, during the Millennium Summit in New York, with 147 heads of state and governments and representatives from 189 countries present, the Millennium Development Goals were established, encompassing 18 targets related to eight global sustainable development goals. The Earth Charter, which the United Nations approved in 2002 during the World Summit on Sustainable Development in Johannesburg, has the same breadth as the Universal Declaration of Human Rights, with reference to sustainability, equity and justice.

6.2 Business initiatives

Several initiatives that relate access to capital to the degree of a company’s alignment with sustainability are being developed. Investors are increasingly taking into account quality of governance and social and environmental impacts on the business as important elements of their risk evaluation process.19

A list of initiatives with their respective links appears below. Some of these are also listed in 6.4.

a) Corporate governance and climate change/corporate responsibilitySustainability and risk: climate change and fiduciary duty for the 21st century trustee (CERES/Harvard University)http://216.235.201.250/netcommunity/Document.Doc?id=106

The changing landscape of liability (SustainAbility/Swiss Re)www.sustainability.com/insight/liability-article.asp?id=180

19 - See ‘Who cares wins’: one year on – a review of the integration of environmental, social and governance value drivers in asset management, financial research and investment processes, IFC - Global Compact - www.ifc.org/ifcext/home.nsf/AttachmentsByTitle/Who_Cares_Wins/$FILE/Who_Cares_Wins.pdf

Handbook 4 - Sustainability Guide for Companies.indd 34 16/05/2009 14:45:52

Sustainability Guide for Companies • 33

Corporate governance and climate change: making the connection (CERES)http://216.235.201.250/netcommunity/Document.Doc?id=90

b) Institutional investors/multilateral institutionsShow me the money: linking environment, social and governance issues to company valuewww.unepfi.org/fileadmin/documents/show_me_the_money.pdf

Principles for Responsible Investment (PRI)www.unpri.org/

c) Credit providersEquator Principleswww.equator-principles.com/principles.shtml

d) Corporate reportsSustainability Reports: Global Reporting Initiative (GRI)www.globalreporting.org

Climate Governance: The Carbon Disclosure Project (CDP)www.cdproject.net

e) Stock Exchange IndexesDJSI – Dow Jones Sustainability Indexeswww.sustainability-indexes.com/

FTSE4Good - Financial Times Stock Exchangewww.ftse.com/Indices/FTSE4Good_Index_Series/index.jsp

ISE - Corporate Sustainability Index – Bovespa www.bovespa.com.br/Mercado/RendaVariavel/Indices/FormConsultaApresentacaoP.asp?Indice=ISE

JSE SRI Index – Johannesburg Stock Exchangewww.jse.co.za/sri/

f) AccountantsSustainability: the role of accountants (ICAEW)www.icaew.co.uk/index.cfm?route=117128

Handbook 4 - Sustainability Guide for Companies.indd 35 16/05/2009 14:45:52

34 • Sustainability Guide for Companies

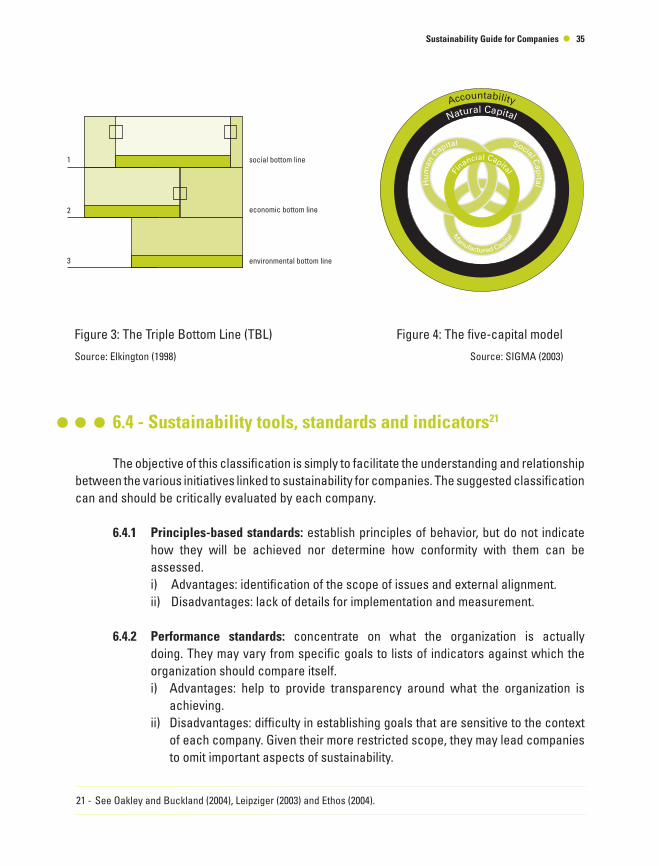

6.3 - The Triple Bottom Line (TBL) and the five-capital model20

The concept of the TBL is widely used to describe sustainable development in an organizational context, placing such performance in terms of the economic, social and environmental bottom lines. It is a popular and powerful concept. The SIGMA (Sustainability - Integrated Guidelines for Management) principles are based on the TBL idea and have developed it, offering the concept of protecting and improving five types of capital: natural, social, human, manufactured and financial.

These capitals are the basis on which the bottom lines are generated and are placed under the umbrella of organizational accountability. This approach is aimed at illustrating the dynamic nature of sustainable development.

Both approaches – TBL and the five-capital model – are complementary, since manufactured and financial capital are reflected in economic bottom line, human and social capital are reflected in the social bottom line and natural capital in the environmental bottom line.

By using the five-capital model it is possible to overcome some of the limitations of the TBL concept, such as, for instance, the temptation to make concessions among the social, economic and environmental factors as if they were equivalent or interchangeable (environmental integrity is, in fact, a pre-requisite for society and for the economy) and could be treated independently (whereas they are actually interrelated facets of a single reality).

The five types of capital are interrelated and thus must be managed, protected and improved in an integrated manner. The five capitals emphasize the fundamental nature of natural capital, as well as the fact that financial capital is just an expression of the value of the other capitals.

The five-capital approach assumes that these distinctions are useful for organizations, particularly when they are developing a vision and principles for acting in alignment with sustainable development.

Many companies are managing the three elements of the TBL separately. However, they increasingly need to be managed so that their interrelations are recognized. A strategic approach such as this is important in order to generate significant changes rather then incremental ones. Fewer and better integrated standards may encourage initiatives in companies where the plethora of standards has been an obstacle for action.

The following Figures illustrate both approaches.

20 - Based on GRI (2002), SIGMA (2003) and Oakley and Buckland (2004).

Handbook 4 - Sustainability Guide for Companies.indd 36 16/05/2009 14:45:52

Sustainability Guide for Companies • 35

6.4 - Sustainability tools, standards and indicators21

The objective of this classification is simply to facilitate the understanding and relationship between the various initiatives linked to sustainability for companies. The suggested classification can and should be critically evaluated by each company.

6.4.1 Principles-based standards: establish principles of behavior, but do not indicate how they will be achieved nor determine how conformity with them can be assessed.i) Advantages: identification of the scope of issues and external alignment.ii) Disadvantages: lack of details for implementation and measurement.

6.4.2 Performance standards: concentrate on what the organization is actually doing. They may vary from specific goals to lists of indicators against which the organization should compare itself.i) Advantages: help to provide transparency around what the organization is

achieving.ii) Disadvantages: difficulty in establishing goals that are sensitive to the context

of each company. Given their more restricted scope, they may lead companies to omit important aspects of sustainability.

21 - See Oakley and Buckland (2004), Leipziger (2003) and Ethos (2004).

1

2

3

social bottom line

economic bottom line

environmental bottom line

Figure 3: The Triple Bottom Line (TBL)

Source: Elkington (1998)

Figure 4: The five-capital model

Source: SIGMA (2003)

Handbook 4 - Sustainability Guide for Companies.indd 37 16/05/2009 14:45:52

36 • Sustainability Guide for Companies

6.4.3 Process standards: describe processes that the organization should follow to improve its performance. They may include processes to identify appropriate goals.i) Advantages: provide practical guidelines and help establish processes

and behaviors.ii) Disadvantages: they do not indicate levels of performance and can be

very bureaucratic.

6.4.4 Hybrid standards: combine elements of the three previous approaches, aiming to establish a degree of consensus before measuring performance and impact. They provide an architecture to extract the best out of each approach and provide a framework of principles, some practical guidance about what should be done and the possibility to measure performance.

A list with some examples of initiatives, with relevant links, appears below.22

a) Principles-based standards

Agenda 21www.unep.org/Documents.Multilingual/Default.asp?DocumentID=52

Code of Best Practice of Corporate Governance - IBGCwww.ibgc.org.br/CodigoMelhoresPraticas.aspx

Earth Charterwww.earthcharter.org/

Global Compactwww.unglobalcompact.org/

Millennium Development Goalswww.un.org/millenniumgoals/

OECD Guidelines for Multinational Enterpriseswww.oecd.org/department/0,2688,en_2649_34889_1_1_1_1_1,00.html

OECD Principles of Corporate Governancewww.oecd.org/dataoecd/32/18/31557724.pdf

22 - See also “Tool Compatibility Guide” www.ethos.org.br/_Rainbow/Documents/Guia_Compat_ING.pdf

Handbook 4 - Sustainability Guide for Companies.indd 38 16/05/2009 14:45:52

Sustainability Guide for Companies • 37

PRI – Principles for Responsible Investmentwww.unpri.org/

Universal Declaration of Human Rightswww.un.org/Overview/rights.html

b) Performance standards

CDP – Carbon Disclosure Projectwww.cdproject.net

DJSI – Dow Jones Sustainability Indexeswww.sustainability-indexes.com/

Ecological Footprintwww.footprintnetwork.org/gfn_sub.php?content=footprint_overview

Ethos Indicators on Corporate Social Responsibilitywww.ethos.org.br/_Rainbow/Documents/indicators_2003.pdf

FTSE4Good – Financial Times Stock Exchangewww.ftse.com/Indices/FTSE4Good_Index_Series/index.jsp

GRI – Global Reporting Initiativewww.globalreporting.org

ISE – Corporate Sustainability Index - Bovespawww.bovespa.com.br/Mercado/RendaVariavel/Indices/ FormConsultaApresentacaoP.asp?Indice=ISE

JSE SRI Index – Johannesburg Stock Exchangewww.jse.co.za/sri/

NBC T 15 - Brazilian Accounting Norms – Information of a Social and Environmental Nature www.portaldecontabilidade.com.br/nbc/t15.htm

Social Balance – Ibase www.balancosocial.org.br/cgi/cgilua.exe/sys/start.htm?sid=2

Handbook 4 - Sustainability Guide for Companies.indd 39 16/05/2009 14:45:52

38 • Sustainability Guide for Companies

c) Process standards

AA1000www.accountability21.net/default.aspx?id=42

Equator Principleswww.equator-principles.com/principles.shtml

FSC – Forest Stewardship Councilwww.fsc.org/en/

ISO 9000www.iso.org

ISO 14000www.iso.org

ISO 26000www.iso.org/sr

MSC – Marine Stewardship Councilwww.msc.org

NBR 16000www.abnt.org.br

OHSAS 18001www.osha-bs8800-ohsas-18001-health-and-safety.com

SA 8000www.sa-intl.org/index.cfm?fuseaction=Page.viewPage&pageId=473

d) Hybrid standards

The Natural Stepwww.naturalstep.org

The SIGMA Projectwww.projectsigma.co.uk

Triple Bottom Line (TBL)See Elkington (1998)

Handbook 4 - Sustainability Guide for Companies.indd 40 16/05/2009 14:45:52

References

7

Handbook 4 - Sustainability Guide for Companies.indd 41 16/05/2009 14:45:52

40 • Sustainability Guide for Companies

7 References

BRUNER, R., EADES, K., HARRIS, R., HIGGINS, R. (1998) “Best practices in estimating the cost of capital: survey and synthesis”, Financial Practice and Education, Vol. 8, No. 1, Spring/Summer, pp. 13-28

DIAMOND, J. (2005) Collapse: How societies choose to fail or survive, New York: Penguin

ELKINGTON, J. (1998) Cannibals with forks: the triple bottom line of 21 century business, Gabriola Island: New Society Publishers

ETHOS, Instituto (2004) “Tool Compatibility Guide”, São Paulo: Ethos Institute

FABER, M., MANSTETTEN, R., PROOPS, J. (1996) Ecological economics: concepts and methods, Cheltenham: Edward Elgar

HENRIQUES, A., RICHARDSON, J. (eds.) (2004) The triple bottom line: does it all add up? Assessing the sustainability of business and CSR, London: Earthscan

IBGC - Brazilian Institute of Corporate Governance (2004) “Code of Best Practices of Corporate Governance”, São Paulo: IBGC

LEIPZIGER, D. (2003) The corporate responsibility code book, Sheffield: Greenleaf

MEADOWS, D.H., MEADOWS, D.L., RANDERS, J., BEHRENS III, W. (1972) The limits to growth: a report for the Club of Rome’s project on the predicament of mankind, 2nd ed., Washington, DC: Potomac Associates Book

MEADOWS, D.H., MEADOWS, D.L., RANDERS, J. (1992) Beyond the limits: confronting global collapse – envisioning a sustainable future, White River Junction: Chelsea Green

MEADOWS, D.H., RANDERS, J., MEADOWS, D.L. (2004) Limits to growth: the 30 year update, White River Junction: Chelsea Green

OAKLEY, R., BUCKLAND, I. (2004) “What if business as usual won’t work?”, in: HENRIQUES and RICHARDSON (eds.) (2004), pp. 131-141

st

Handbook 4 - Sustainability Guide for Companies.indd 42 16/05/2009 14:45:52

Sustainability Guide for Companies • 41

PORTER, M.E., KRAMER, M.R. (2006) “Strategy and society: the link between competitive advantage and corporate social responsibility”, Harvard Business Review, Vol. 84, No. 12, December, pp. 78-92

SIGMA PROJECT (2003) “The sigma guidelines: putting sustainable development into practice – a guide for organizations”, London: BSI

WCED - World Commission on Environment and Development (1987) Our Common Future, Oxford: Oxford University Press

WILLARD, B. (2005) The next sustainability wave: building boardroom buy-in, Gabriola Island: New Society Publishers

Handbook 4 - Sustainability Guide for Companies.indd 43 16/05/2009 14:45:53

Glossary

8

Handbook 4 - Sustainability Guide for Companies.indd 44 16/05/2009 14:45:53

Sustainability Guide for Companies • 43

Board (of Directors)Governing body elected by the subscribers of the organization concerned with providing business direction, with overseeing and controlling the executive actions of management, according to the organization charter and the law. Though all its members might not be engaged in the organization’s day-to-day operations, the entire board is held liable for the consequences of the organization’s policies, actions, and failures to act.

Book ValueCalculated by following accounting prin–ciples. It is retrospective (focus on historical data) and incorporates fiscal and legal questions. It is the basis for calculating Economic Value.

Company Value May be divided into three types: Book Value, Economic Value and Market Value.

CEOChief Executive Officer.

ChairmanChairman of the board of directors.

Directors and OfficersBoard members and top executives.

Eco-efficiencyRelationship between the value of the product or service and its environmental impact.

Ecological FootprintA resource management tool that measures the amount of land and water that a human population requires to produce the resources it consumes and have its waste absorbed, using prevailing technology. The concept makes it possible to establish benchmarks for comparisons between individuals, cities and nations. Its calculation takes into account the area of arable land and pasture (to fulfill the population’s needs for food and other products), forests (to supply timber, its derivatives and other products), urbanized area and the land needed to absorb excess CO2 from the burning of fossil fuels. It is being used by many institutions, such as the European Community. See www.footprintnetwork.org.

Economic ValueThe intrinsic value of the company. It is prospective (based on projections of the company’s performance) and takes into account the value of money in time and the risk associated with the company’s activities with respect to the return on investment. It has a managerial approach, and allows a correlation between company performance and compensation, both of capital providers and employees.

Handbook 4 - Sustainability Guide for Companies.indd 45 16/05/2009 14:45:53

44 • Sustainability Guide for Companies

Fiduciary DutyDirectors have a responsibility to act diligently and honestly while executing the tasks which are required for the good development of the company, considering its business operations, acting in good faith and in the interest of the organization as a whole, acting in accordance with its statutes or social contract, avoiding conflicts of interest and not making inappropriate use of the goods, opportunities and information of the company or the position being exercised.

IndicatorsTools that enable access to information about a particular situation, which have the main characteristics of being able to synthesize different pieces of information, keeping only the essential meaning of the aspects analyzed. To fulfill its purpose, an indicator must be transparent, complete, relevant, precise, neutral, comparable and auditable.

ManagementActivities under the responsibility of the CEO or equivalent.

ManagersInclude the board of directors and other managers.

Market ValueRepresents the vision of market agents, reflected at the time of an acquisition and sale transaction. It is directly linked to current and projected performance and to the company’s reputation.

Open SystemsA set of interconnected elements to which is attributed an explicit purpose, making up a whole that interacts with the environment of which it is part, importing from it material, energy and information, processing them in accordance to its own standards and, in consequence, exporting products.

Social license to operateA social contract which is not formalized, but through which stakeholders’ vote of confidence in the operations of the company is maintained. It is obtained by understanding how the company’s actions affect stakeholders. Relations between companies and society are based on a “social contract” that evolves along with changes in society and in societal expectations. In this contract society legitimates the company’s existence, recognizing its activities and obligations, as well as establishing legal limits for its actions.

StakeholdersRelevant individuals with interests pertinent to the company, or individuals or entities that take some kind of risk, direct or indirect, vis-a-vis the company, such as: shareholders, employees, clients, financial investors, suppliers, creditors, environmental organizations, government, and communities involved directly or indirectly with the company’s activities. For the purposes of this document, stakeholders also include parties affected by the company which are not organized and cannot be engaged, such as the environment, other living beings, children, future generations, etc.

Handbook 4 - Sustainability Guide for Companies.indd 46 16/05/2009 14:45:53

Sustainability Guide for Companies • 45

The Natural StepA conceptual approach based on widely-held scientific principles, which is intended to provide a common language to address how human societies can act in such a way as to avoid making their future on the planet unviable. See: www.naturalstep.org

Triple Bottom LineA model based not only on the economic point of view (a single bottom line vision), but also on the social and environmental aspects, all of them in an integrated manner.

ValueExpression of an organization’s achievement of its social objectives, which can be translated into monetary (company value) or non-monetary aspects, such as in the case of non-profit organizations.

Handbook 4 - Sustainability Guide for Companies.indd 47 16/05/2009 14:45:53

46 • Sustainability Guide for Companies

Handbook 4 - Sustainability Guide for Companies.indd 48 16/05/2009 14:45:53

Sustainability Guide for Companies • 47

Over the past decade, sustainability has moved from the fringes of the business world to the top of shareholders’ agenda. The concept of sustainability has gained trac-tion among corporate employees, regulators, and customers, too. Consequently, any miscalculation or misjudgement of matters related to sustainability can have serious repercussions on how the world judges your company and values its shares.

For corporate management, finding the right balance among competing economic, social, and environmental goals is the essence of “responsible leadership.” In prac-tice, responsible leadership means integrating ethical considerations into company decision-making, and managing on the basis of personal integrity and widely-held organisational values. Responsible leaders manage for the common good and gain authority and legitimacy in direct proportion to their success in serving others.

Is that kind of leadership readily achievable? Clearly, a perfect balance of all com-peting interests is difficult to achieve and managers are bound to make missteps in the attempt. Nevertheless, most stakeholders are adamantly in favour of companies dealing with sustainability issues in an honest and open fashion. So, as a first step to-ward demonstrating responsible leadership, companies must establish trust between themselves and their various stakeholder communities. Sometimes, the process of establishing trust can be painstakingly slow. But it starts by understanding stake-holders’ concerns and acknowledging their legitimacy. Only after you’ve mapped the spectrum of stakeholder issues can you start to prioritise them and develop suitable responses and outreach programmes.

Sponsored by:

Handbook 4 - Sustainability Guide for Companies.indd 49 16/05/2009 14:45:53

48 • Sustainability Guide for Companies

Handbook 4 - Sustainability Guide for Companies.indd 50 16/05/2009 14:45:53

Handbook 4 - Sustainability Guide for Companies.indd 51 16/05/2009 14:45:53

Sustainability Guide for CompaniesAn Overview for Directors and Senior Executives

Corporate Governance Handbooks

The Brazilian Institute of Corporate Governance (IBGC, to use its Portuguese acronym) is dedicated exclusively to the promotion of corporate governance in Brazil. It is the country’s main advocate of corporate governance practices and debates, and has achieved national and international recognition.

Founded on November 27th, 1995, IBGC – a Brazilian non-profit organization – aims “to be a reference in corporate governance, contributing to the sustainability of organizations and influencing key agents in our society towards greater transparency, justice and responsibility”.

IBGC - Instituto Brasileiro de Governança CorporativaAv. das Nações Unidas, 12.551 - 2508World Trade CenterSão Paulo, SP 04578-903 Brazil

Tel.: +55 (11) 3043-7008

IBGC Paraná – Tel.: +55 (41) 3022-5035IBGC Rio – Tel.: +55 (21) 2223-9651IBGC Sul – Tel.: +55 (51) 3328-2552www.ibgc.org.br

Handbook 4 - Sustainability Guide for Companies.indd 52 16/05/2009 14:45:53

![Corporate Governance Manualpaisalo.in/pdf/corporate-governance-en.pdf · [ 1 ] DEFINITIONS Corporate Governance Corporate Governance is the system of internal controls and procedures](https://img.dokumen.tips/doc/110x75/60457b037dc32d128b177c66/corporate-governance-1-definitions-corporate-governance-corporate-governance.jpg)