Embed Size (px)

Citation preview

1www.metrostudy.com

Boulder Valley Real Estate ConferenceNovember 15, 2018

Denver Market

• Denver Post Article: ‘Major Cold Front Slams Denver Housing Market in September’ (Oct 3)

• Denver Post Article: ‘Metro Denver Housing Market Finds its Footing in October After Volatile September’ (Nov 5)

• Unemployment Rate up!....slightly

• 30-Year Mortgage Rates Bust Through 5% And Keep Rising!

• Denver Housing Costs Are High & Traffic Congestion is Worsening

• New Home Traffic and Sales Dropped Significantly in September

• Denver Metro Area Out of Running for Amazon HQ2

There’s A Lot Going on to Close Out the Year….

PAGE 2

Denver Market

• National Housing Permits Fall to Lowest Level in Two Years

• NAHB Builder Sentiment Index at Lowest Level of The Year

• Combined With Rising Interest Rates and Declining Affordability, The Outlook for Housing is Deteriorating

• Mid-Term Elections

• The Denver Broncos Are Not Going to Make the Playoffs….Again

There’s A Lot Going on to Close Out the Year….continued

PAGE 3

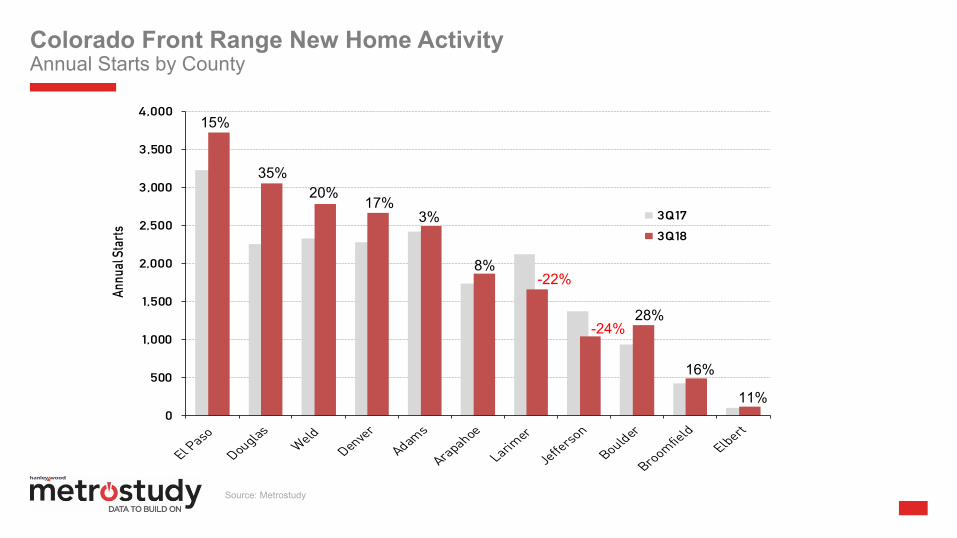

Colorado Front Range New Home ActivityAnnual Starts by County

PAGE 4

Source: Metrostudy

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000An

nual

Star

ts

3Q173Q18

15%

20%35%

17%3%

8%-22%

-24%28%

16%

11%

Denver Metro New Home ActivityAnnual Starts by County and Market Share

PAGE 5

Source: Metrostudy

2,492

1,866

1,191

544

2,669

3,053

1,042

0

250

500

750

1,000

1,250

1,500

1,750

2,000

2,250

2,500

2,750

3,000

3,250

Adams Arapahoe Boulder Broomfield Denver Douglas Jefferson

Annu

al St

arts

19%

14%

9%

4%

21%

23%

8%

Denver Metro New Home ActivityMarket Share Trend by County

PAGE 6

Source: Metrostudy

19%

14%

9%

21%

24%

8%

4%

0%

5%

10%

15%

20%

25%

30%

Adams Arapahoe Boulder Broomfield Denver Douglas Jefferson

Mar

ket S

hare

of A

nnua

l Sta

rts3Q13 3Q14 3Q15 3Q16 3Q17 3Q18

Denver Market Traffic & ContractsAverage Weekly Traffic Per Subdivision is Down -1% Compared to YTD 2017

PAGE 7

Source: Metrostudy

0

5

10

15

20

25

J F M A M J J A S O N D

Aver

age W

eekly

Tra

ffic P

er Su

bdivi

sion

2018

2015

2017

2016

Denver HBA Parade of Homes

Traffic Down -17% Aug-Oct

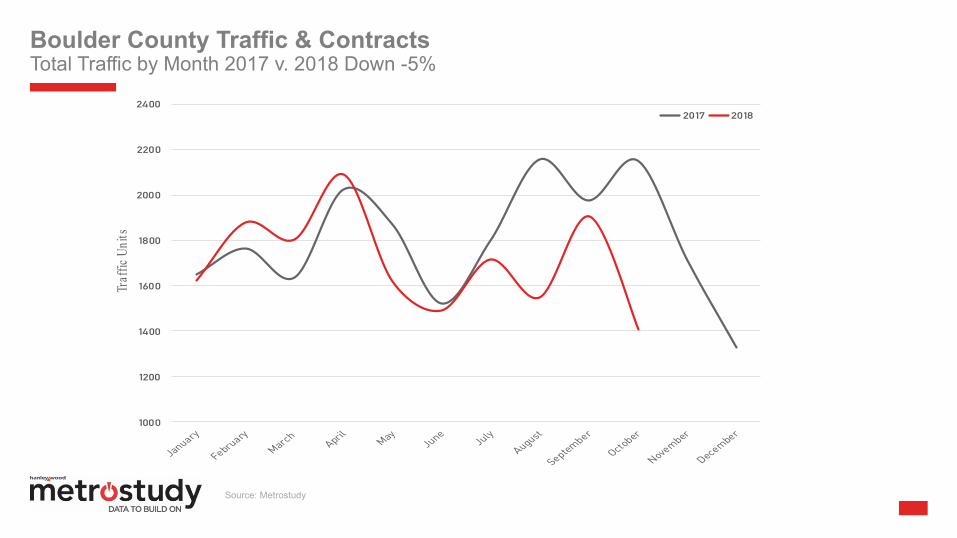

Boulder County Traffic & ContractsTotal Traffic by Month 2017 v. 2018 Down -5%

PAGE 8

Source: Metrostudy

1000

1200

1400

1600

1800

2000

2200

2400

Traf

fic U

nits

2017 2018

Denver Market Traffic & ContractsTotal Traffic by Base Price Range 2014-2018

PAGE 9

Source: Metrostudy

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

$0-$299 $300-$ 399 $400-$499 $500-$ 599 $600-$ 699 $700-$799 $800+

Traf

fic U

nits

(Jan

-Oct

)

20142015201620172018

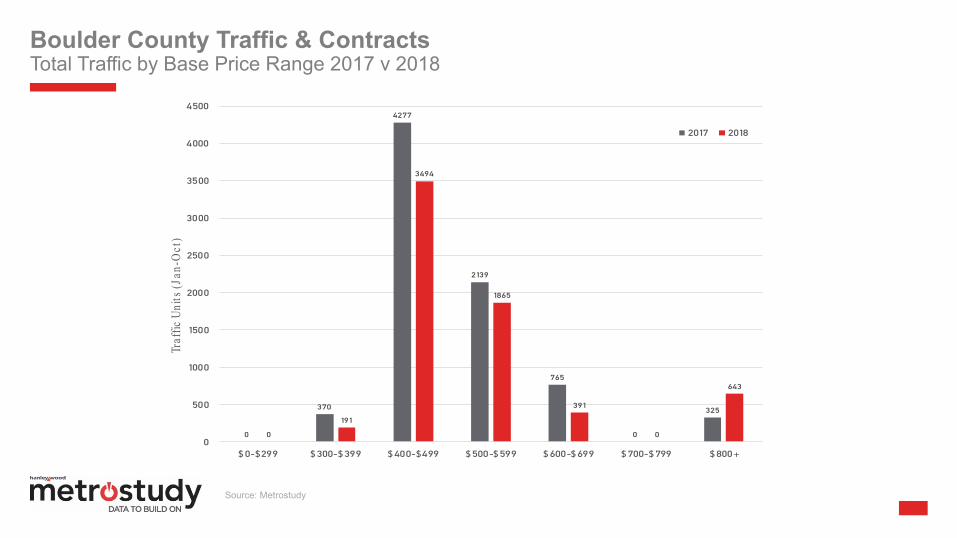

Boulder County Traffic & ContractsTotal Traffic by Base Price Range 2017 v 2018

PAGE 10

Source: Metrostudy

0

370

4277

2139

765

0

325

0

191

3494

1865

391

0

643

0

500

1000

1500

2000

2500

3000

3500

4000

4500

$ 0-$299 $ 300-$ 399 $ 400-$499 $ 500-$ 599 $ 600-$ 699 $ 700-$ 799 $ 800+

Traf

fic U

nits

(Jan

-Oct

)

2017 2018

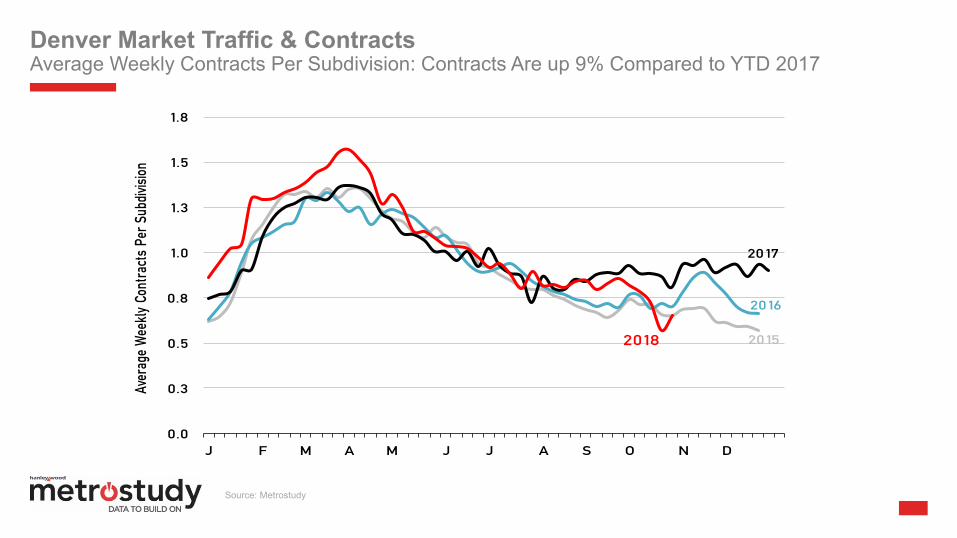

Denver Market Traffic & ContractsAverage Weekly Contracts Per Subdivision: Contracts Are up 9% Compared to YTD 2017

PAGE 11

Source: Metrostudy

0.0

0.3

0.5

0.8

1.0

1.3

1.5

1.8

J F M A M J J A S O N D

Aver

age W

eekly

Con

tracts

Per

Subd

ivisio

n

2016

2017

2018 2015

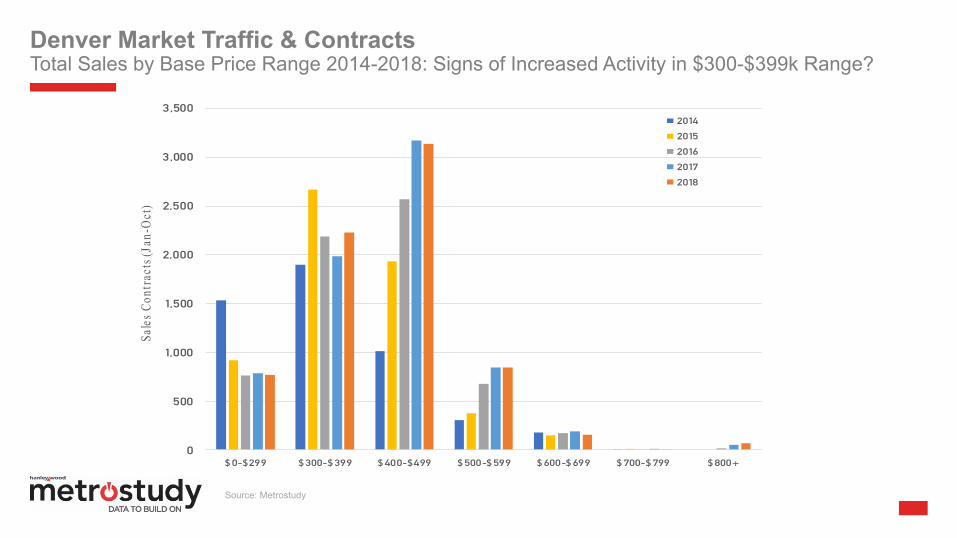

Denver Market Traffic & ContractsTotal Sales by Base Price Range 2014-2018: Signs of Increased Activity in $300-$399k Range?

PAGE 12

Source: Metrostudy

0

500

1,000

1,500

2,000

2,500

3,000

3,500

$0-$299 $300-$ 399 $400-$499 $500-$599 $600-$699 $700-$ 799 $800+

Sales

Con

tract

s (Ja

n-Oc

t)

20142015201620172018

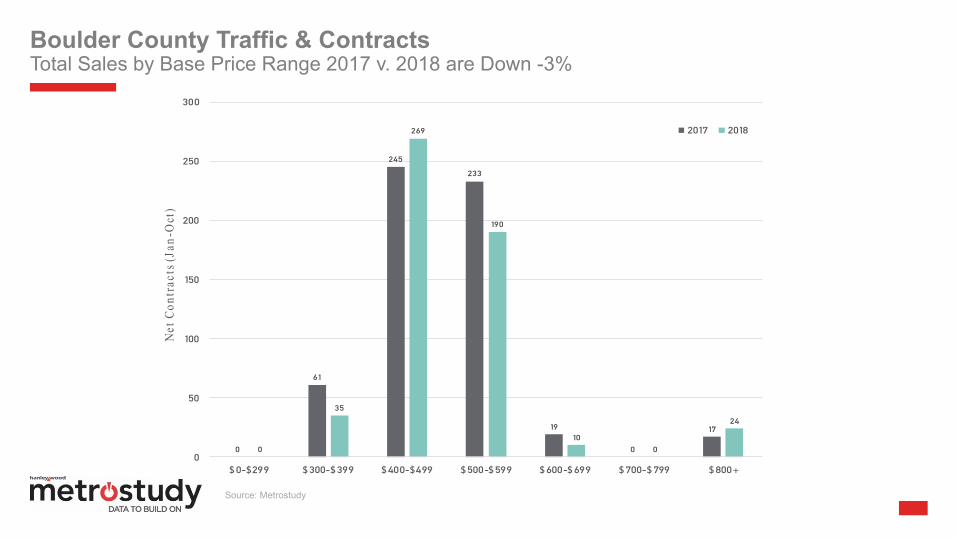

Boulder County Traffic & ContractsTotal Sales by Base Price Range 2017 v. 2018 are Down -3%

PAGE 13

Source: Metrostudy

0

61

245

233

19

0

17

0

35

269

190

100

24

0

50

100

150

200

250

300

$0-$299 $ 300-$ 399 $ 400-$499 $ 500-$ 599 $ 600-$ 699 $ 700-$ 799 $ 800+

Net

Con

trac

ts (J

an-O

ct)

2017 2018

Denver Market Traffic & ContractsAverage Weekly Conversion Rate – Sept ’18 was 7.4% v. Sept ‘17 of 5.3%

PAGE 14

Source: Metrostudy

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

J F M A M J J A S O N D

Axis Title

Aver

age W

eekly

Con

vers

ion R

ate

Axis Title

3.245

2016

2017

2018

2015

Denver Market Traffic & ContractsTraffic Conversion Rate by Month 2014-2018

PAGE 15

Source: Metrostudy

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%Co

nver

sion R

ate (

Jan-

Oct)

20142015201620172018

Denver Market Traffic & ContractsTraffic Conversion Rate by Base Price Range 2014-2018

PAGE 16

Source: Metrostudy

0%

2%

4%

6%

8%

10%

12%

14%

16%

$0-$299 $300-$399 $400-$499 $500-$ 599 $600-$ 699 $700-$799 $800+

Conv

ersio

n Rat

e (Ja

n-Oc

t)20142015201620172018

Boulder New Home Activity3Q Starts & Closings Stats (All Product)

PAGE 17

Source: Metrostudy

DENVER METRO Type 3Q17 3Q18 % Change

Qtr Starts Condominium 194 78 -59.8%Townhome/Duplex 797 891 11.8%Detached 2255 2353 4.3%

Total 3246 3322 2.3%

Annual Starts Condominium 505 896 77.4%Townhome/Duplex 2795 3207 14.7%Detached 8158 8865 8.7%

Total 11458 12968 13.2%

Qtr Closings Condominium 77 104 35.1%Townhome/Duplex 546 841 54.0%Detached 1912 2193 14.7%

Total 2535 3138 23.8%

Annual Closings Condominium 175 420 140.0%Townhome/Duplex 2206 2861 29.7%Detached 7844 8407 7.2%

Total 10225 11688 14.3%

BOULDER COUNTY Type 3Q17 3Q18 % Change

Qtr Starts Condominium 12 0 -100.0%Townhome/Duplex 39 89 128.2%Detached 195 206 5.6%

Total 246 295 19.9%

Annual Starts Condominium 53 166 213.2%Townhome/Duplex 178 324 82.0%Detached 701 701 0.0%

Total 932 1191 27.8%

Qtr Closings Condominium 27 22 -18.5%Townhome/Duplex 28 61 117.9%Detached 144 161 11.8%

Total 199 244 22.6%

Annual Closings Condominium 82 135 64.6%Townhome/Duplex 150 192 28.0%Detached 574 726 26.5%

Total 806 1053 30.6%

Boulder New Home ActivityCounty Above Previous Cycle Peak for Home Starts

PAGE 18

Source: Metrostudy

0%

2%

4%

6%

8%

10%

12%

0

200

400

600

800

1,000

1,200

1,400

3Q05 3Q06 3Q07 3Q08 3Q09 3Q10 3Q11 3Q12 3Q13 3Q14 3Q15 3Q16 3Q17 3Q18

Mark

et Sh

are

Annu

al St

arts

Boulder County Annual StartsBoulder % Share of Metro Area

Boulder County New Home ActivityHas a 14.4 Month Supply of Vacant Developed Lots and VDL Count is up +3% From 3Q17

PAGE 19

Source: Metrostudy

0

20

40

60

80

100

120

140

160

180

0

500

1,000

1,500

2,000

2,500

3Q05 3Q06 3Q07 3Q08 3Q09 3Q10 3Q11 3Q12 3Q13 3Q14 3Q15 3Q16 3Q17 3Q18

Mon

ths o

f Sup

ply

Vaca

nt D

evel

oped

Lots

Boulder County VDL InventoryBoulder County VDL Months of Supply

Boulder County New Home ActivityTotal Housing Inventory is up, Months of Supply Remains Balanced

PAGE 20

Source: Metrostudy

0

2

4

6

8

10

12

14

16

18

20

0

200

400

600

800

1,000

1,200

3Q05 3Q06 3Q07 3Q08 3Q09 3Q10 3Q11 3Q12 3Q13 3Q14 3Q15 3Q16 3Q17 3Q18

Mont

hs of

Supp

ly

Inven

tory U

nits

Total Housing Inventory

Total INV Months of Supply

Boulder County New Home ActivityFinished Vacant Home Inventory Months of Supply is Below Equilibrium

PAGE 21

Source: Metrostudy

1.6

0

1

2

3

4

5

6

7

8

9

10

11

12

0

50

100

150

200

250

300

350

400

450

3Q05 3Q06 3Q07 3Q08 3Q09 3Q10 3Q11 3Q12 3Q13 3Q14 3Q15 3Q16 3Q17 3Q18

Mon

ths o

f Sup

ply

Fini

shed

Vaca

nt U

nits

Finished Vacant Finished MOS

Boulder County New Home Activity64% of New Home Starts are Above $500k Base Price v. Denver Market 35% (All Housing)

PAGE 22

Source: Metrostudy

5.9%

9.2%

16.4%

18.4%

15.6%

18.1%

8.7%7.8%

3.1%

8.6%

6.8%

9.2% 8.6%

28.5%

19.1%

16.1%

0%

5%

10%

15%

20%

25%

30%

< $299 $300-$349 $350-$399 $400-$449 $450-$499 $500-$599 $600-$ 699 $700 +

Denver Metro Area

Boulder County

6.9%

24.7%

4.3%

2.2%

7.5%

21.7%20.4%

7.1%

1.8%

3.4%

13.9%

27.2%

0.2%

3.1% 2.7%

18.6%

25.2%

3.0% 3.3%2.9%

0%

5%

10%

15%

20%

25%

30%

% S

hare

of A

nnua

l Sta

rts by

Lot

Fron

tage

Denver Metro AreaBoulder County

Boulder County New Home ActivityAttached Product (41%) and 50-60’ lots (44%) Are the Predominant Size

PAGE 23

Source: Metrostudy

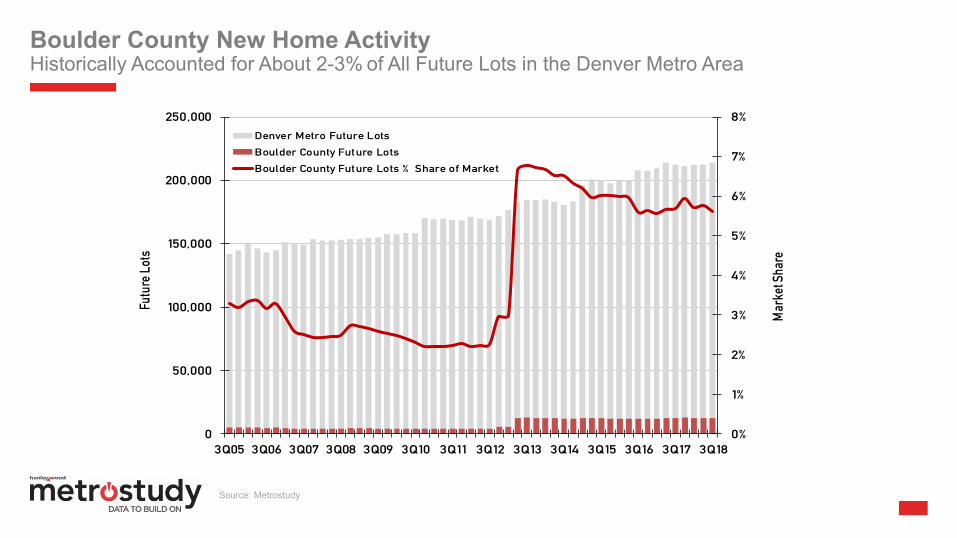

Boulder County New Home ActivityHistorically Accounted for About 2-3% of All Future Lots in the Denver Metro Area

PAGE 24

Source: Metrostudy

0%

1%

2%

3%

4%

5%

6%

7%

8%

0

50,000

100,000

150,000

200,000

250,000

3Q05 3Q06 3Q07 3Q08 3Q09 3Q10 3Q11 3Q12 3Q13 3Q14 3Q15 3Q16 3Q17 3Q18

Mar

ket S

hare

Futu

re Lo

tsDenver Metro Future LotsBoulder County Future LotsBoulder County Future Lots % Share of Market

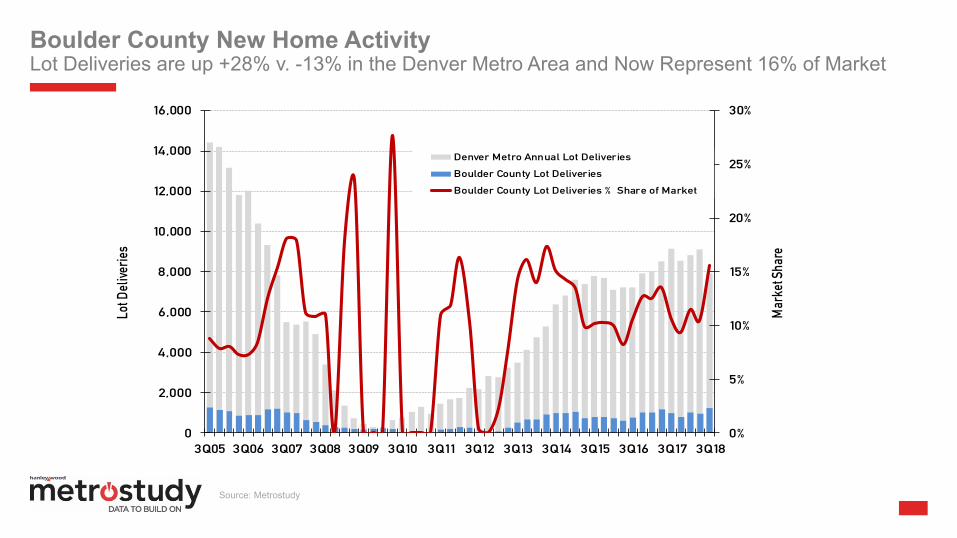

Boulder County New Home ActivityLot Deliveries are up +28% v. -13% in the Denver Metro Area and Now Represent 16% of Market

PAGE 25

Source: Metrostudy

0%

5%

10%

15%

20%

25%

30%

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

3Q05 3Q06 3Q07 3Q08 3Q09 3Q10 3Q11 3Q12 3Q13 3Q14 3Q15 3Q16 3Q17 3Q18

Mar

ket S

hare

Lot D

elive

ries

Denver Metro Annual Lot Deliveries

Boulder County Lot Deliveries

Boulder County Lot Deliveries % Share of Market

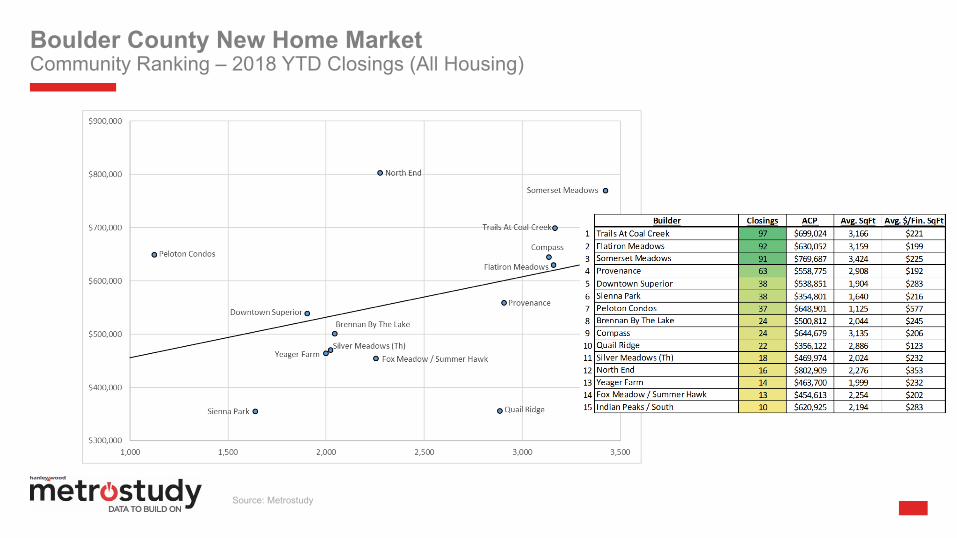

Boulder County New Home MarketCommunity Ranking – 2018 YTD Closings (All Housing)

PAGE 26

Source: Metrostudy

Boulder Housing Market

• High home prices coupled with rising mortgage rates have caused some market turbulence. Prospective buyers are recalibrating. Traffic and sales are down slightly in higher price points (generally), but Metrostudy expects housing demand to remain strong in 2019 and builders to start more homes.

• Fundamentals of Denver & Boulder economy remain very strong with steady in-migration, strong employment gains, low unemployment, healthy resale activity and low inventory. Denver’s population has grown by approximately 500,000 since 2008 fueling the undersupply of housing, thus creating opportunities for development for the next several years.

• Lot deliveries are up and vacant developed lot supplies are down, but with such strong demand to live in Boulder County, expect lot supplies to remain very tight for the foreseeable future.

• The market may have finally hit the price ceiling. But housing production should still grow in 2019. With the market ‘recalibrating’, now is the time to focus on the things you can control, not those you can’t:

ü Re-evaluate existing and future projects – a strong market has a way of covering up mistakes

ü Plan for continued product and price shifts – how are you communicating with your prospective buyers?

ü Look for operational efficiencies including internal, on-site, trade partners, etc. to combat margin compression

ü Re-evaluate and retrain sales team - complacency can erode sales and market share

3Q 2018 Conclusions

PAGE 27

28www.metrostudy.com

Thank You!Now you know…