Embed Size (px)

Citation preview

This article was downloaded by: [The University of Manchester Library]On: 06 November 2014, At: 07:06Publisher: RoutledgeInforma Ltd Registered in England and Wales Registered Number:1072954 Registered office: Mortimer House, 37-41 Mortimer Street,London W1T 3JH, UK

The International Reviewof Retail, Distribution andConsumer ResearchPublication details, including instructions forauthors and subscription information:http://www.tandfonline.com/loi/rirr20

Beyond convenience: thefuture for independentfood and grocery retailersin the UKSteve Baron , Kim Harris , David Leaver &Brenda M. OldfieldPublished online: 15 Apr 2011.

To cite this article: Steve Baron , Kim Harris , David Leaver & Brenda M.Oldfield (2001) Beyond convenience: the future for independent food andgrocery retailers in the UK, The International Review of Retail, Distribution andConsumer Research, 11:4, 395-414

To link to this article: http://dx.doi.org/10.1080/09593960126381

PLEASE SCROLL DOWN FOR ARTICLE

Taylor & Francis makes every effort to ensure the accuracy of allthe information (the “Content”) contained in the publications on ourplatform. However, Taylor & Francis, our agents, and our licensorsmake no representations or warranties whatsoever as to the accuracy,completeness, or suitability for any purpose of the Content. Anyopinions and views expressed in this publication are the opinions andviews of the authors, and are not the views of or endorsed by Taylor& Francis. The accuracy of the Content should not be relied upon andshould be independently verified with primary sources of information.Taylor and Francis shall not be liable for any losses, actions, claims,proceedings, demands, costs, expenses, damages, and other liabilitieswhatsoever or howsoever caused arising directly or indirectly inconnection with, in relation to or arising out of the use of the Content.

This article may be used for research, teaching, and private studypurposes. Any substantial or systematic reproduction, redistribution,reselling, loan, sub-licensing, systematic supply, or distribution in anyform to anyone is expressly forbidden. Terms & Conditions of accessand use can be found at http://www.tandfonline.com/page/terms-and-conditions

Dow

nloa

ded

by [

The

Uni

vers

ity o

f M

anch

este

r L

ibra

ry]

at 0

7:06

06

Nov

embe

r 20

14

Beyond convenience: thefuture for independent foodand grocery retailers in theUK

Steve Baron, Kim Harris, David Leaver and BrendaM. Old� eld

Abstract

The UK’s independent food and grocery retail sector’s competitive advantage of‘convenience’ has been eroded in recent years as major retailers increase opening hoursand develop their own convenience trading formats. As a result, large numbers ofindependent retailers are closing. A UK-wide survey was undertaken to identify othersources of competitive advantages, and the changes needed to stop or reverse thedecline in this sector. Exploratory semi-structured interviews led to the developmentof a questionnaire on six major issues affecting the sector. ‘Snowball’ sampling, usingindustry partners, provided 142 respondents. The provision of a ‘social shoppingexperience’ emerged as a key competitive advantage that could be developed. Improv-ing vertical and horizontal trading alliances, and the wider use of informationtechnology, provided other options.

Keywords

Convenience retailing, competitive advantage, independent retailers, retail envi-ronment, social shopping experience.

Introduction

Recent reports on UK independent food and grocery retailers emphasize thedecline in their numbers over the last decade (Peston and Ennew 1998; Gordonand Walton 2000). For example the number of ‘non-af� liated independents’declined from 24 000 in 1996 to 22 000 by 1998 (Gordon and Wilson 1999).

Steve Baron, David Leaver and Brenda M. Old� eld, The Business School, ManchesterMetropolitan University, Aytoun Building, Manchester M1 3GH, UK; Tel: +44 (0)161247 3982; Fax: +44 (0)161 247 3996; E-mail: [email protected]; [email protected];b.m.old� [email protected]; Kim Harris, Shef� eld University Management School, 9Mappin Lane, Shef� eld S1 4DT, UK; Tel: +44 (0)114 222 3434; Fax: +44 (0)114 2223348; E-mail: k.cassidy@shef� eld.ac.uk.

The International Review of Retail, Distribution and Consumer ResearchISSN 0959-3969 print/ISSN 1466-4402 online © 2001 Taylor & Francis Ltd

http://www.tandf.co.uk/journalsDOI: 10.1080/09593960110073331

Int. Rev. of Retail, Distribution and Consumer Research 11:4 October 2001 395–414

Dow

nloa

ded

by [

The

Uni

vers

ity o

f M

anch

este

r L

ibra

ry]

at 0

7:06

06

Nov

embe

r 20

14

During the same period, the combined total of other trading formats servicingthe convenience food and grocery market rose by 1000 to 24 000. (Gordon andWilson 1999; Gordon and Walton 2000), and home shopping by Internet hasbecome accessible to most locations in the UK.

This article looks at some of the major issues affecting non-af� liated inde-pendent retailers, symbol group members and specialists such as CTNs and off-licenses. This grouping re� ects the new (year 2000) categorization of the UKgrocery market from the Institute of Grocery Distribution (IGD) into four mainsectors: ‘Convenience retailing’; ‘Traditional retailing/developing convenience’;‘Supermarkets and superstores’; and ‘Alternative channels’ (such as kiosks andmarket stalls). In the convenience retailing sector, non-af� liated retailers andsymbol group members are classi� ed as independent retailers, while in thetraditional retailing/developing convenience sector, specialists such as CTNs,grocers, off-licenses, greengrocers, butchers, � shmongers and bakers are classi-� ed as independents. As Gordon and Wilson state the convenience sector is‘notoriously dif� cult to pigeonhole’; however the grouping chosen for this studyis based loosely on store size of less than 3000 square feet, and a location closeto customers’ homes, within the case of the non-specialist independents, havinga product range that is wide and shallow. This de� nition aligns itself to that ofa convenience store format (Kirby 1987) and, as such, forms a part of a largerconvenience food sector which is serviced by this grouping, together with otherformats such as major multiples and petrol forecourt retailers.

It has been argued that the one major competitive advantage of the independ-ent food and grocery retailer – convenience – is being eroded (Peston and Ennew1998). According to the Institute of Grocery Distribution, convenience retailingoffers local shopping and long hours (Gordon and Walton 2000), while Morga-nosky and Cude (2000, p. 17) argue that retailers offer convenience ‘by enablingthe consumer to increase the number of tasks that can be accomplished duringa single visit to the retailer, or reduce the amount of time required to completethe shopping task’. Whether convenience involves location, opening hours or in-store ef� ciencies, it is no longer the case that these attributes are exclusive to theindependent food and grocery retailer. The erosion of the competitive advantageof convenience may be nearing completion by the start of the 21st century.

But do independent retailers have other competitive advantages? What chan-ges may have to be made to stop or reverse the decline in the number ofoutlets?

This article reports on a survey of independent retailers, carried out duringthe � rst half of the year 2000. In an attempt to answer the questions above, itaddresses the issues and opportunities for independent retailers that had beenidenti� ed from popular, trade and academic press and from prior qualitativeresearch.

The issues are:

c factors contributing to the success of independent retail businesses;c independent retailers’ responses to changes in the retail environment, with

speci� c reference to competition;c independent retailers’ views of their relationships with consumers;

396 The International Review of Retail, Distribution and Consumer Research

Dow

nloa

ded

by [

The

Uni

vers

ity o

f M

anch

este

r L

ibra

ry]

at 0

7:06

06

Nov

embe

r 20

14

c independent retailers’ reactions to technological developments within theindustry;

c factors constraining growth and succession within independent retail com-panies; and

c the range of skills currently perceived to be present within independent retailbusinesses.

The article is structured as follows. A brief background to set the history andcontext of the offer of convenience to food and grocery shoppers in the 21stcentury is followed by a description of the methodology employed for theprimary research. The survey results related to the six issues above are reported,and the interpretation and discussion of the results are focused on the potentialcompetitive advantages of independent food and grocery retailers, and the stepsto be taken by them to increase the likelihood of successful future trading.

Background

History and context

Academic research on the independent retail sector can be traced back to the1930s, where McGarry (1930) and Nystrom (1930) identi� ed the high failurerates of US independents. Later work by Smith (1937) and Collin (1937) in theUK concentrated on strategic and � nancial aspects of the sector. These studiessuggested that the key factors resulting in the high failure rates amongstindependent retailers were the ease of entry into the sector without either thenecessary � nancial support or acumen, and the rise of multiple retailers. In the1950s, there was a move to a more positive approach, centring on howindependent retailers might successfully accommodate the increasing challengessuch as self-service in multiple retailers (Channing 1960). The services providedby independent retailers in locational and social contexts also received increasedattention (Burns 1954; Moss 1958). Locational studies continued during the1960s and 1970s (Berry 1963; Maroney 1976), but these were augmented bystudies focusing on the social role of the independent sector (Dixon andMcLaughlin 1968), impact studies on the effect of multiple retailers on thesector (Labat 1972), and the operational characteristics of independent retailers(McClelland 1966).

Dawson and Kirby (1979) pulled together the strands above to provide anoverview of the issues relating to the independent retail sector, and to assess waysforward for independent retailers. They identi� ed problems in the independentretail sector stemming from complexities and inconsistencies in the supplychain, a lack of suf� cient capital for investment, a lack of business experience,the levels of rent and rates, the administrative burdens associated with ValueAdded Tax (VAT), and low operating margins. They suggested a number of waysto overcome these problems. These included re-organizing the independentretailers’ supply chain, increasing the size of their business through capitalinvestment, increasing the product range, and an increase in governmentallobbying on issues affecting the sector.

Baron et al.: Beyond convenience 397

Dow

nloa

ded

by [

The

Uni

vers

ity o

f M

anch

este

r L

ibra

ry]

at 0

7:06

06

Nov

embe

r 20

14

The traditional advantages of independent retailers lay in their convenience inlocation and opening hours, home delivery, friendly and personal service, andinformal � nancial services such as extended credit and Christmas clubs. Theseadvantages were offset by higher prices. Dawson and Kirby suggested thatcompetition from multiples was not considered a problem by the independentretailers. The prevailing view was that of a polarization of the shoppinglandscape (Bates 1976), with multiple retailer stores at one end of the spectrumand independent retailers at the other, and that this landscape effectively met thevarious needs of the consumer.

In the 1980s, the polarization view was consolidated (Brown 1987), and in1985 it was reported that there was an increase in the use of convenienceconsiderations in consumers’ decisions as to where to shop (Kirby 1987). Thesmall independent food and grocery retailer was well placed to meet theseconsumer convenience needs. Kirby suggested that it was not until the mid1980s that a convenience store format – ‘a self-service store usually between 1000and 3000 sq. ft located close to housing with some parking facilities, offering awide range of goods including grocery and CTN products, chemist sundries,alcohol and possibly other lines including video hire, fast foods or petrol,opening long hours including Sundays – could be identi� ed in the UK’s retailsystem.

By the late 1980s, ‘three planks’ for a thriving independent retail business hadbeen identi� ed: product specialization; service; and location (Davies and Harris1990). Location is a recognized element of convenience. In the food and grocerysector, product specialization was linked then to the offer of ‘healthier’ foods.The service factor included the provision of an open, friendly and personalizedenvironment, retailer expertise, and the ‘open all hours’ philosophy (the latteragain being an element of convenience).

Changes in the 1990s

Changes in the 1990s, in particular, suggest that the degree of polarization ismuch less. Indeed, retailers from both ends of the spectrum seemed to begravitating towards the centre to offer ‘convenience’ to food and groceryshoppers.

Many specialist and independent retailers in the UK diversi� ed towardsconvenience store retailing in the 1990s. As a result, some of the traditionalindependent retail businesses (such as CTNs, bakers, grocers and off-licences)were classi� ed by the Institute of Grocery Distribution as being in a grocerymarket sector known as ‘Traditional retailing/developing convenience’ (Gordonand Walton 2000, p. 19). It has been observed by industry commentators that‘convenience provides a niche for small retailers that, until recently, the largesupermarkets have found dif� cult to match’ (Gordon and Walton 2000, p. 8, ouremphasis). However, the large UK supermarket groups, and fuel companiesbegan to enter the convenience retailing market in a substantial way in the late1990s, recognizing the convenience food sector as a major business opportunity.Sainsbury’s began testing their c-store ‘Local’ format in early 1999, and the fulllaunch of ‘Local’ took place in summer 1999, when the company announced the

398 The International Review of Retail, Distribution and Consumer Research

Dow

nloa

ded

by [

The

Uni

vers

ity o

f M

anch

este

r L

ibra

ry]

at 0

7:06

06

Nov

embe

r 20

14

intention to open 200 convenience stores over the next three years and about1000 in the long term. They also planned a mini-store format for small towns tocompete with Tesco ‘Metro’ stores. Safeway stated the aim to operate 45 petrolforecourt shops (in conjunction with BP Amoco) by the end of 1999, while Tescointroduced 17 Express forecourt stores (in conjunction with Esso) (FinancialMail on Sunday 1999). Changes in consumer pro� les with the emergence of timepoor/cash rich consumers, the rise of single-person households requiring less ofa ‘big shop’, and the increasing mobility of consumers have meant that‘convenience’ had become a highly attractive sector. The latest estimate (HenleyCentre 2001) suggests that over 70% of the UK’s £32 billions convenience foodretail sector is serviced by multiple retailers. The lessening polarization hasresulted in the multiple retailers having store formats in a range of sizes andlocation (Weller 2001). According to ‘Super Marketing’ (1998), it is specialistretailers such as butchers, � shmongers and greengrocers who will be affectedmost by such initiatives.

Also, the strategies and tactics of the large supermarkets have had an effect onindependent food and grocery retailers, irrespective of whether they havetargeted the niche of convenience retailing. According to a Verdict report, ‘out-of-town superstores are likely to kill off more than 20 000 small retailers by2001’, the most likely being butchers, bakers and grocers (Daily Mail 1999). ADepartment of Environment, Transport and the Regions (DETR) reportestimated that large food stores opening in edge-of-centre or out-of-centrelocations had had an impact on market share ‘of 13%–50% on principal foodretailers in market towns and district centres’ (DETR 1998). Hallsworth andWorthington (2000), in a study of a UK market town, examined how locationalstrategies of large food retailers affected retail trade in the market towncommunity, and concluded that, ‘Through time it emerges that the communityhas not been able to sustain its trading opposition to a large format intruder’(p. 207).

Small independent food and grocery retailers had, until the 1990s, been ableto claim that the offer of long opening hours distinguished them from the largeformat operators. However, that distinction is quickly being eroded in the UK.Many outlets of the large supermarket groups are now open 24 hours a day, fromMonday to Saturday, and a further six hours on a Sunday – a total of 150 hoursa week. Smith and Sparks (2000), in a study of independent small shops inScotland found that the longest opening hours for such independent shops werein neighbourhood centres, with a mean of 81 hours per week, and the longestindividual opening hours was 109 hours per week, in an isolated rural area.

E-commerce transactions are expected to represent 4% of GDP in 2002(Guardian 1999). The UK Government is set to include Internet shopping in thecalculation of the Retail Price Index as at present online shopping accounts forabout 0.2% of total retail spending (The Observer 1999). Morganosky and Cude(2000), in a study of consumer response to online grocery shopping in the USA,reported that over 70% of their sample gave ‘convenience and saving time’ astheir main reason for purchasing groceries on-line. Furthermore, almost 20% oftheir sample claimed to be buying all their groceries from on-line food chan-nels. Home shopping may be seen as ‘the ultimate time-saving convenience’(Morganosky and Cude 2000, p. 17). Tesco.com has been particularly successful

Baron et al.: Beyond convenience 399

Dow

nloa

ded

by [

The

Uni

vers

ity o

f M

anch

este

r L

ibra

ry]

at 0

7:06

06

Nov

embe

r 20

14

and is now the world’s leading on-line grocery retailer with 70 000 orders a weekand an annual turnover of £250 million.

Challenges for the independent food and grocery retailer in the 21st century

All of the above casts much doubt on whether convenience alone represents asustainable source of competitive advantage for the small independent food andgrocery retailer in the year 2001.

Some recent studies have urged for consideration of government interventionto maintain a healthy independent retail sector. Pickering et al. (1998) empha-sized that independent retailers contribute signi� cantly to the preservation oflocal communities, while Peston and Ennew (1998, p. vi), summarizing focusgroup research on neighbourhood shopping, pointed out that ‘consumers andretailers agreed on one thing . . . that there was a social need for their (‘cornershops’) existence. Whatever (remedial) action is taken, however, needs to bebetter informed by a consideration of what consumers and society wish to be thefunction of independent retailers’ (Smith and Sparks 2000).

The social and community services provided by independent retailers can beviewed as a positive function. There is growing concern among various com-mentators about the negative impact of e-commerce on the quality of theconsumer shopping experience (Piercy 1999). Many are anxious that, in this ageof advanced technology, efforts are made to preserve the positive social elementsof shopping that are still valued by many consumers. The traditional independ-ent retailer has always scored well here. The owner/manager of the independentstore is often on � rst-name terms with customers, and can converse naturallyand frequently about service issues as and when they occur. In the currentclimate, the independent retailer’s ability to provide positive, interpersonalcomponents of the retail experience could be viewed as a real strength andexploited to the full (Baron et al. 1999).

Additionally, independent retailers are still being urged to develop verticalalliances with wholesalers and suppliers, and horizontal alliances, such asfranchizing arrangements, buying groups, or working together with neighbour-ing retailers to enhance the shopping attractiveness of a location (Pickering et al.1998). Peston and Ennew (1998) argued strongly that independent retailers mustimprove their technology and management systems to satisfy consumer desires,and that they must consider their roles in the provision of delivery services forhome shoppers. Some factors which contribute to a successful independent foodand grocery retail operation have been identi� ed by the DETR (1999). Theyinclude opening long hours, being accessible for local customers with a visiblelocation, having a good range of products and services, and offering a friendlyand ef� cient service.

Given the very fast changing retail environment in which independentretailers must trade, and the question-mark over their competitive position onconvenience, primary research was carried out with independent food andgrocery retailers during 1999 and 2000 to address their opportunities andconstraints in the year 2000. The methodology is now described.

400 The International Review of Retail, Distribution and Consumer Research

Dow

nloa

ded

by [

The

Uni

vers

ity o

f M

anch

este

r L

ibra

ry]

at 0

7:06

06

Nov

embe

r 20

14

Methodology

The research was carried out to provide a snapshot of the views of independentfood and grocery retailers on the issues facing them at the start of the 21stcentury. A positivist approach to data collection, via a sample survey, wasdeemed appropriate in order to gain an up-to-date breadth of views on a domainthat is clearly de� ned by academics and practitioners alike. Some of the richnessof qualitative data (which could have been obtained, for example, from detailedcase studies) has been sacri� ced in order to attempt to uncover some potentiallygeneralizable � ndings.

The identi� cation of the issues facing independent food and grocery retailersresulted from a synthesis of three sources of information:

c the academic literature on independent retailers;c an electronic search of trade and popular press coverage of the UK retail

environment and small business issues in 1999; andc the outcomes of personal interviews with owners of 18 small retail businesses

in the North West of England.

For the latter, all the interviews were semi-structured, and were designed toencourage the interviewees to talk openly about the strengths of their business,the constraints on growth, their training needs and what they felt they couldlearn from large retailers. Unsurprisingly, the owners took the opportunity toarticulate some of the dif� culties that independent retailers face, with speci� cstories of constraints on growth, of obtaining advice, and on � nance andproperty.

As a result of the synthesis of information, the issues were divided into the sixcategories speci� ed in the introduction in order to add a respondent-friendlystructure to the intended questionnaire. The particular statements in eachcategory were tested for relevance and content validity by seeking opinions fromsenior people in organizations closely associated with the well-being of inde-pendent food and grocery retailers, viz. the British Institute of Retailing, theAssociation of Convenience Stores, the Distributive National Training Organiza-tion and the Bakery National Training Organization. As a result, some state-ments were amended, added or deleted, and all statements were examined fortheir meaningfulness to the respondents. We were assured that some of the moretechnical terms, such as ‘catchment area’, would be familiar to respondents.Sometimes, precision in the wording had to be sacri� ced in order to ensure asmooth negotiation through the questionnaire. For example, the use of adjectivessuch as ‘adequate’ (as in adequate car parking, or adequate provision) or‘sizeable’ (as in sizeable population), was regarded as a means of capturing anon-apathetic response, although it was acknowledged that they were liable tosubjective interpretations. Temporal responses to some questions were mademore speci� c by forcing respondents to express their views as to what hadhappened ‘in the last two years’. The � nal set of statements that were used onthe questionnaire is presented in Table 3.

The questionnaire was designed to be completed by a sample of owners and/or managers of independent retail businesses that operate in the grocery marketsector. Data on attitudes and opinions of the respondents were captured through

Baron et al.: Beyond convenience 401

Dow

nloa

ded

by [

The

Uni

vers

ity o

f M

anch

este

r L

ibra

ry]

at 0

7:06

06

Nov

embe

r 20

14

the use of statements requiring answers on a � ve-point Likert scale, with5 5 strongly agree through to 1 5 strongly disagree. The questionnaire waspiloted with � ve small retailers, who advised that the completion time would beapproximately 15 minutes. Some questions were re-worded as a result, and 550copies of the revised questionnaire (available from the � rst-named author onrequest) were distributed at the Convenience Retailing Trade Fair at the NationalExhibition Centre in Birmingham on 20 March 2000. Only seven retailersreturned completed questionnaires. The fact that they answered all the questionscon� rmed that the revised wording had worked. However, the extremely lowresponse rate meant that we needed help from industry partners to encouragevery busy people to spend time completing a questionnaire.

The choice of the sampling frame was complicated by the changing categor-ization models of ‘convenience’ in retailing. The new (year 2000) model of theInstitute of Grocery Distribution (IGD) divides the UK grocery market intofour main sectors: ‘Convenience retailing’, Traditional retailing/developingconvenience’, ‘Supermarkets and superstores’ and ‘Alternative channels’, such askiosks and market stalls. The � rst two sectors were relevant to the focus of thestudy. In the convenience retailing sector, non-af� liated retailers and symbolgroup members are classi� ed as independent retailers, while in the traditionalretailing/developing convenience sector, specialists such as CTNs, grocers, off-licenses, greengrocers, butchers, � shmongers and bakers are classi� ed as in-dependents. Therefore, the sampling frame consisted of non-af� liated retailers,symbol group members and specialists.

The subsequent distribution and response rates, of questionnaires, are shownin Table 1. With each distribution link, a mailing list of independent food/grocery retailers was obtained and a self-completion postal questionnaire, withreply envelope, was sent to all the addresses supplied. In the case of thedistribution of questionnaires via the link with the Association of ConvenienceStores, one of the mailing lists was subsequently provided by a regionalsubgroup operating mainly in Wales and the South West of England. Thedecision to use this form of snowball sampling was made in order to increase thevolume of responses. A total of 142 respondents completed the questionnaire,which is a relatively large sample size in the context of small business research.However, in comparison with IGD statistics on store numbers, there was anover-representation of responses from symbol group members. Therefore, wecannot rule out the possibility of non-response bias in relation to the samplingframe, brought about by this form of sampling. For this reason, we arerestricting ourselves to reporting descriptive summaries and categorizationsarising from the data, given that the assumptions underpinning conventionalstatistical hypothesis testing are unlikely to hold.

Pro� le of respondents

Some 59% of respondents described themselves as independent owners (ofwhich 19% owned more than one shop). The remaining 41% were members ofa symbol group. Their roles in the business are owners (44%), owner/managers(44%) or managers (12%). Almost 75% of their shops have been trading for over10 years, with 15.5% trading less than 6 years. Just below 46% of their stores

402 The International Review of Retail, Distribution and Consumer Research

Dow

nloa

ded

by [

The

Uni

vers

ity o

f M

anch

este

r L

ibra

ry]

at 0

7:06

06

Nov

embe

r 20

14

were convenience stores, almost 20% were off licence or general stores, and over11% were bakers shops. The majority of the stores (61%) had 600 sq. ft or moreof selling space, although 13.5% had 300 sq. ft or less of selling space. Only 21%of their main shops had less than 500 product lines; 63% had 1000 or moreproduct lines.

The majority of the respondents employed between one and � ve full-timestaff (68%), and between one and � ve part-time staff (52%), although asigni� cant minority (21%) employed 10 or more part-time staff. Only sixrespondents dealt with a sole supplier. The number of suppliers varied con-siderably; 2–5 suppliers (37%), 6–10 suppliers (25%), and more than 10suppliers (33%).

Replies were received from respondents across the UK with the greatestnumber of replies coming from Wales (34%), North West of England (17%),London and the South East (15%) and East/West Midlands (15%). Almost68% of their stores open seven days a week, with a further 30% open fromMonday to Saturday. The opening hours per week of the main store were: lessthan 54 hours (21%), 55–74 hours (26%), 75–99 hours (26%), and 100 hours ormore (27%).

The � ndings

Apart from the section on technological developments, there are between 10 and26 statements for respondents to rate. To systematically identify important state-ments (and hence important issues), statements have been categorized accordingto the means and standard deviations of the rating scores (see Table 2).

Table 1 Distribution links and response rates of questionnaires

Distribution linkNumber of questionnaires

distributed Response rate (%)

via Bakery National Trainingorganization

350 4.6

via Hyndburn Borough Council 110 9.1via Association of ConvenienceStores Newsletter and networks 924 11.8

Overall 1384 9.75

Table 2 Categorizing responses to statements according to means and standard devia-tions (S.D.)

S.D.Mean Low ( , 0.9) Medium (0.9–1.1) High ( . 1.1)

Low ( , 2.5) b d eMedium (2.5–3.5) f f eHigh ( . 3.5) a c eKey: a 5 consistently high level of agreement with a statement; b 5 consistently highlevel of disagreement with a statement; c 5 generally high level of agreement with astatement; d 5 generally high level of disagreement with a statement; e 5 wide variabilityin responses to a statement; and f 5 neutral responses to a statement

Baron et al.: Beyond convenience 403

Dow

nloa

ded

by [

The

Uni

vers

ity o

f M

anch

este

r L

ibra

ry]

at 0

7:06

06

Nov

embe

r 20

14

Tables 3a, 3b, 3c, 3e and 3f show the means and standard deviations of theratings on the statements, and the corresponding categories for each statement.The section on changing technology is summarized using appropriate per-centage frequency tables relating to the responses to statements in Table 3d,made by retailers with and without experience of selling via the Internet.

Interpretation

Factors contributing to the success of independent retail businesses

The respondents claimed that they were offering a friendly service, with asmooth operation (fully stocked shop and a speedy service). They were servingthe community, and would generally know many customers by name. Many werefortunate to have a ‘sizeable’ catchment population. If the self-evaluations wererealistic, then the offers of many of the independent retailers are not easilyreplicated by the multiple food and grocery retailers. However, the number ofcompetitors within a one mile radius, and visibility to passing traf� c variedconsiderably. Customer car-parking was ‘adequate’ for many of the larger stores,but the lack of adequate car parking, especially having double yellow linesoutside the shop, was clearly of great concern to many small shopkeepers.Finally, the relative lack of discussion, by some retailers, with neighbouringindependent retailers, was surprising. Many issues are common to all traders inthe same high street or precinct, and opportunities for combined voices may bebeing missed.

Independent retailers’ responses to changes in the retail environment, with speci� creference to competition

There was a strong feeling that services provided by Local and RegionalGovernment Agencies could be improved and made less bureaucratic. Similarly,

Table 3a Statements on ‘factors contributing to the success of independent retailbusinesses’

Mean S.D. Category

There is a sizeable population living within the retailcatchment area 3.94 0.93 c

My shop is highly visible to passing traf� c 3.77 1.13 eThere is limited competition within a radius of 1 mile of the

shop 3.22 1.35 eI know a lot of my customers by name 3.89 0.98 cI often discuss trade with other independent retailers in the

immediate vicinity 2.95 1.04 fMy staff give friendly service 4.38 0.58 aI can offer speed of service to minimize queues 4.23 0.67 aMy store is fully stocked most of the time 4.25 0.72 aThere is adequate car parking for my customers 3.28 1.29 eI demonstrate my commitment to the local community 3.92 0.84 a

404 The International Review of Retail, Distribution and Consumer Research

Dow

nloa

ded

by [

The

Uni

vers

ity o

f M

anch

este

r L

ibra

ry]

at 0

7:06

06

Nov

embe

r 20

14

there was a view that local Chambers of Commerce do not provide adequatesupport for small retailers. There was also a generally held view that local/regional enterprise boards are not providing adequate support. There was a farfrom consistently positive view about the provision of help by local tradeassociations. The feeling came across very strongly that many small retailersperceived themselves to be � ghting to survive without much support from localand national bodies.

Table 3b Statements on ‘retailers’ responses to changes in the retail environment’

Mean S.D. Category

Large supermarkets opening near me have reduced myturnover 3.77 1.33 e

I feel that I can survive the competition from the largesupermarkets 3.49 1.09 f

The opening of convenience stores by large retailers will havelittle effect on my trade 2.56 1.16 e

I believe that the large retailers’ convenience store formatswill be successful for them 3.73 0.75 a

It is important to visit a large retailer’s convenience store tosee what I can learn 3.85 0.91 c

I know how I can increase my catchment area 3.00 1.04 fI am prepared to increase my opening hours if necessary 3.03 1.11 fMy current range of merchandise is much the same as it was

2 years ago 2.69 1.10 fMy current range of customer services is much the same as

it was 2 years ago 2.85 1.09 fIt would be relatively easy for me to sell products or services

which I do not currently offer 3.18 1.00 fIn general, new product/service ideas come from customers

or suppliers, rather from my staff 3.46 0.88 fI frequently discuss consumer needs with my main

supplier(s) 3.51 0.95 cMy supplier(s) share(s) my views of consumer needs 3.49 0.84 fMy supplier(s) ask(s) my opinion on the packaging of goods 2.40 0.94 dMy supplier(s) ask(s) my opinion on the display of goods 2.65 1.03 fI believe that an EPOS system enhances supplier-retailer

relationships 3.53 1.01 cI feel that knowing more about category management would

help my business 3.57 0.88 aI feel that knowing more about ef� cient response systems

would help my business 3.63 0.87 aI am aware of the role of Regional Enterprise Boards 2.51 1.07 fI believe there is adequate provision of support by my local

Chamber of Commerce 2.45 0.88 bI believe there is adequate provision of support by local trade

associations 2.60 0.91 fI believe there is adequate provision of support by local

enterprise boards 2.37 0.91 dI am aware of Government initiatives which support

independent retailers 2.30 1.04 dLocal and regional Government agencies are too bureaucratic 4.01 0.92 cThe services provided by Government agencies could be

improved 4.15 0.76 a

Baron et al.: Beyond convenience 405

Dow

nloa

ded

by [

The

Uni

vers

ity o

f M

anch

este

r L

ibra

ry]

at 0

7:06

06

Nov

embe

r 20

14

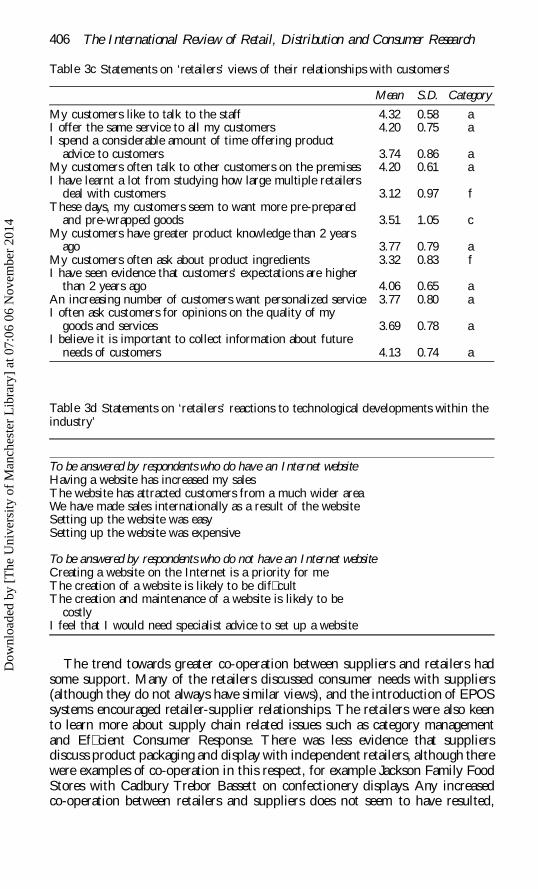

The trend towards greater co-operation between suppliers and retailers hadsome support. Many of the retailers discussed consumer needs with suppliers(although they do not always have similar views), and the introduction of EPOSsystems encouraged retailer-supplier relationships. The retailers were also keento learn more about supply chain related issues such as category managementand Ef� cient Consumer Response. There was less evidence that suppliersdiscuss product packaging and display with independent retailers, although therewere examples of co-operation in this respect, for example Jackson Family FoodStores with Cadbury Trebor Bassett on confectionery displays. Any increasedco-operation between retailers and suppliers does not seem to have resulted,

Table 3c Statements on ‘retailers’ views of their relationships with customers’

Mean S.D. Category

My customers like to talk to the staff 4.32 0.58 aI offer the same service to all my customers 4.20 0.75 aI spend a considerable amount of time offering product

advice to customers 3.74 0.86 aMy customers often talk to other customers on the premises 4.20 0.61 aI have learnt a lot from studying how large multiple retailers

deal with customers 3.12 0.97 fThese days, my customers seem to want more pre-prepared

and pre-wrapped goods 3.51 1.05 cMy customers have greater product knowledge than 2 years

ago 3.77 0.79 aMy customers often ask about product ingredients 3.32 0.83 fI have seen evidence that customers’ expectations are higher

than 2 years ago 4.06 0.65 aAn increasing number of customers want personalized service 3.77 0.80 aI often ask customers for opinions on the quality of my

goods and services 3.69 0.78 aI believe it is important to collect information about future

needs of customers 4.13 0.74 a

Table 3d Statements on ‘retailers’ reactions to technological developments within theindustry’

To be answered by respondents who do have an Internet websiteHaving a website has increased my salesThe website has attracted customers from a much wider areaWe have made sales internationally as a result of the websiteSetting up the website was easySetting up the website was expensive

To be answered by respondents who do not have an Internet websiteCreating a website on the Internet is a priority for meThe creation of a website is likely to be dif� cultThe creation and maintenance of a website is likely to be

costlyI feel that I would need specialist advice to set up a website

406 The International Review of Retail, Distribution and Consumer Research

Dow

nloa

ded

by [

The

Uni

vers

ity o

f M

anch

este

r L

ibra

ry]

at 0

7:06

06

Nov

embe

r 20

14

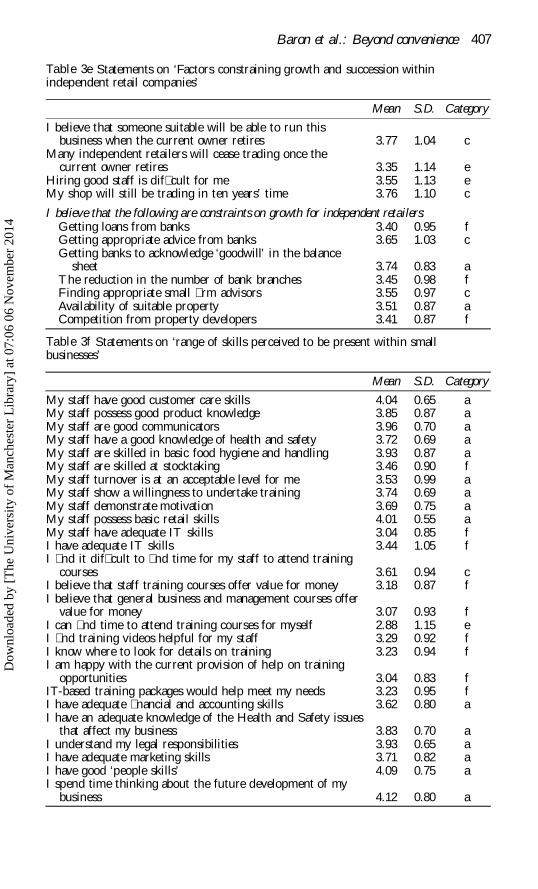

Table 3e Statements on ‘Factors constraining growth and succession withinindependent retail companies’

Mean S.D. Category

I believe that someone suitable will be able to run thisbusiness when the current owner retires 3.77 1.04 c

Many independent retailers will cease trading once thecurrent owner retires 3.35 1.14 e

Hiring good staff is dif� cult for me 3.55 1.13 eMy shop will still be trading in ten years’ time 3.76 1.10 c

I believe that the following are constraints on growth for independent retailers:Getting loans from banks 3.40 0.95 fGetting appropriate advice from banks 3.65 1.03 cGetting banks to acknowledge ‘goodwill’ in the balance

sheet 3.74 0.83 aThe reduction in the number of bank branches 3.45 0.98 fFinding appropriate small � rm advisors 3.55 0.97 cAvailability of suitable property 3.51 0.87 aCompetition from property developers 3.41 0.87 f

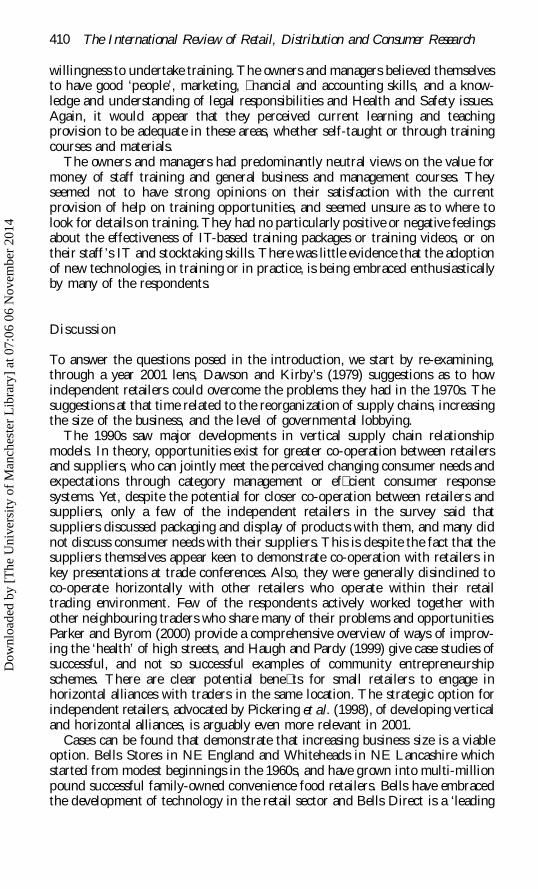

Table 3f Statements on ‘range of skills perceived to be present within smallbusinesses’

Mean S.D. Category

My staff have good customer care skills 4.04 0.65 aMy staff possess good product knowledge 3.85 0.87 aMy staff are good communicators 3.96 0.70 aMy staff have a good knowledge of health and safety 3.72 0.69 aMy staff are skilled in basic food hygiene and handling 3.93 0.87 aMy staff are skilled at stocktaking 3.46 0.90 fMy staff turnover is at an acceptable level for me 3.53 0.99 aMy staff show a willingness to undertake training 3.74 0.69 aMy staff demonstrate motivation 3.69 0.75 aMy staff possess basic retail skills 4.01 0.55 aMy staff have adequate IT skills 3.04 0.85 fI have adequate IT skills 3.44 1.05 fI � nd it dif� cult to � nd time for my staff to attend training

courses 3.61 0.94 cI believe that staff training courses offer value for money 3.18 0.87 fI believe that general business and management courses offer

value for money 3.07 0.93 fI can � nd time to attend training courses for myself 2.88 1.15 eI � nd training videos helpful for my staff 3.29 0.92 fI know where to look for details on training 3.23 0.94 fI am happy with the current provision of help on training

opportunities 3.04 0.83 fIT-based training packages would help meet my needs 3.23 0.95 fI have adequate � nancial and accounting skills 3.62 0.80 aI have an adequate knowledge of the Health and Safety issues

that affect my business 3.83 0.70 aI understand my legal responsibilities 3.93 0.65 aI have adequate marketing skills 3.71 0.82 aI have good ‘people skills’ 4.09 0.75 aI spend time thinking about the future development of my

business 4.12 0.80 a

Baron et al.: Beyond convenience 407

Dow

nloa

ded

by [

The

Uni

vers

ity o

f M

anch

este

r L

ibra

ry]

at 0

7:06

06

Nov

embe

r 20

14

generally, in changes in the range of products and services being offered over thelast two years. This supports � ndings of the Convenience Tracking Programme2000, jointly carried out by the Institute of Grocery Distribution and HarrisInternational Marketing, which highlighted differences of opinion betweenretailers and suppliers regarding implementation.

The retailers’ strongly believed that the convenience store formats of largeretailers, such as Sainsbury, Tesco and Safeway will be successful (although thelarge retailers themselves are, at the time of writing, re-evaluating their conveni-ence store strategies). Most small retailers did believe that they could learn fromthe large retailers’ convenience store operations. Also, although there was a largeamount of variability in the responses, almost two-thirds of respondents felt thatlarge supermarkets opening nearby had affected their turnover.

It has been suggested previously, that the measures which small retailers cantake to remain competitive include increasing opening hours, increasing thecatchment population, and diversifying the range of goods/services on offer.The largely neutral responses, regarding the knowledge and willingness ofrespondents to take such measures, is of concern. This survey, however, has notcaptured the reasons for the neutrality.

Independent retailers’ views of their relationships with consumers

The statements about customers liking to talk to staff, and to other customers,were in the top � ve most high-scoring statements across the whole survey. Theseresponses con� rm the social value being given by independent retailers. Therewere also consistently held views by respondents that the provision of productadvice is integral to the service offer, and there was a strongly consistent viewthat staff of small retail businesses aim to offer friendly service.

There was widespread agreement amongst the respondents that customershave greater product knowledge and higher expectations than two years ago. Inaddition, a greater number of customers appeared to want personalized service.This con� rms the � ndings of the secondary research, where innovations in thepast are becoming the norms of the present. Small retailers are aware of thesechanges in consumer attitudes and behaviours, and are clearly monitoring thefuture needs of consumers, although there is scope for more of them toincorporate a system for seeking consumer opinions on the quality of goods andservices. In this respect, and others, there is a need for small retailers to keep upwith modern technology. Also, the strong belief that the same service is/shouldbe offered to each customer may need to be challenged.

Independent retailers’ reactions to technological developments within the industry

Some 47% of respondents had EPOS systems, but only 15% had an Internetwebsite. The respondents who have a website did not express particularly strongviews about ease or expense of setting up a website, either negatively orpositively. While most of the retailers were neutral regarding whether the sitehad increased sales, there was general disagreement that sales had been madeinternationally as a result of the website, although for 28% of them, the website

408 The International Review of Retail, Distribution and Consumer Research

Dow

nloa

ded

by [

The

Uni

vers

ity o

f M

anch

este

r L

ibra

ry]

at 0

7:06

06

Nov

embe

r 20

14

had attracted customers from a much wider area. Of the 85% of respondentswho do not have a website, only 16% of them agreed, or strongly agreed, thatsetting up a website was a priority. A total of 71% of respondents were locatedin areas where neighbouring supermarkets offer home shopping, and 28% ofthese respondents had noticed the effect on their own business.

There is a lack of prioritization given to setting up websites, despite the manyUK government statements and initiatives, in 1999 and 2000, on making internetaccess a priority for small businesses. In general, the respondents who have notset up a website believed that setting up a website would be dif� cult and wouldrequire specialist advice, and that the creation and maintenance of the site wouldbe costly. This is in contrast to the experiences of those who have actually set upa website. There is, therefore, an identi� ed need for training and information onhow to set up a website (and the values of so doing).

Factors constraining growth and succession within independent retail companies

The two main constraints on growth of independent retailers, consistentlyvoiced, were the inability to get banks to acknowledge goodwill in their balancesheets, and the (lack of) availability of suitable property. There was also agenerally held view that lack of success with obtaining advice from banks, or in� nding appropriate small � rm advisors can constrain growth. Interestingly, thehighly publicized potential constraints on growth – getting a loan from a bank,and the closure of bank branches – did not appear to be as critical as getting thebanks to give advice or to acknowledge ‘goodwill’.

Regarding succession and the future trading potential of independent re-tailers, while there was general agreement that their own shop will be trading in10 years time, there are mixed views on whether many independents will ceasetrading when the current owner retires, and on the dif� culties of hiring goodstaff. Hiring and retaining good staff, who see retailing as a career, was an issuewhich affected all retailers, regardless of size, as emphasized in a report by theDepartment of Trade and Industry (2000). As might be expected, members ofsymbol groups were more optimistic about the survival of their main store in 10years time, than the other independent retailers.

The range of skills currently perceived to be present within independent retailbusinesses

Despite possible dif� culties in hiring good staff, there was strong and consistentagreement that the staff, who are employed, have good basic retail and customercare skills, good knowledge of products and health and safety issues, and skills inbasic food hygiene and handling. Admittedly, these are the perceptions of theowners and managers, but they appear to believe that staff currently receive goodtraining, by one form or another, on the above skills and knowledge factors.Owners and managers are unlikely to be receptive to new training methods inthese areas, given these beliefs, and a generally held view that it was dif� cult to� nd the time for staff to attend courses. It should be noted, however, that staffwere perceived to be good communicators, who demonstrate motivation and a

Baron et al.: Beyond convenience 409

Dow

nloa

ded

by [

The

Uni

vers

ity o

f M

anch

este

r L

ibra

ry]

at 0

7:06

06

Nov

embe

r 20

14

willingness to undertake training. The owners and managers believed themselvesto have good ‘people’, marketing, � nancial and accounting skills, and a know-ledge and understanding of legal responsibilities and Health and Safety issues.Again, it would appear that they perceived current learning and teachingprovision to be adequate in these areas, whether self-taught or through trainingcourses and materials.

The owners and managers had predominantly neutral views on the value formoney of staff training and general business and management courses. Theyseemed not to have strong opinions on their satisfaction with the currentprovision of help on training opportunities, and seemed unsure as to where tolook for details on training. They had no particularly positive or negative feelingsabout the effectiveness of IT-based training packages or training videos, or ontheir staff ’s IT and stocktaking skills. There was little evidence that the adoptionof new technologies, in training or in practice, is being embraced enthusiasticallyby many of the respondents.

Discussion

To answer the questions posed in the introduction, we start by re-examining,through a year 2001 lens, Dawson and Kirby’s (1979) suggestions as to howindependent retailers could overcome the problems they had in the 1970s. Thesuggestions at that time related to the reorganization of supply chains, increasingthe size of the business, and the level of governmental lobbying.

The 1990s saw major developments in vertical supply chain relationshipmodels. In theory, opportunities exist for greater co-operation between retailersand suppliers, who can jointly meet the perceived changing consumer needs andexpectations through category management or ef� cient consumer responsesystems. Yet, despite the potential for closer co-operation between retailers andsuppliers, only a few of the independent retailers in the survey said thatsuppliers discussed packaging and display of products with them, and many didnot discuss consumer needs with their suppliers. This is despite the fact that thesuppliers themselves appear keen to demonstrate co-operation with retailers inkey presentations at trade conferences. Also, they were generally disinclined toco-operate horizontally with other retailers who operate within their retailtrading environment. Few of the respondents actively worked together withother neighbouring traders who share many of their problems and opportunities.Parker and Byrom (2000) provide a comprehensive overview of ways of improv-ing the ‘health’ of high streets, and Haugh and Pardy (1999) give case studies ofsuccessful, and not so successful examples of community entrepreneurshipschemes. There are clear potential bene� ts for small retailers to engage inhorizontal alliances with traders in the same location. The strategic option forindependent retailers, advocated by Pickering et al. (1998), of developing verticaland horizontal alliances, is arguably even more relevant in 2001.

Cases can be found that demonstrate that increasing business size is a viableoption. Bells Stores in NE England and Whiteheads in NE Lancashire whichstarted from modest beginnings in the 1960s, and have grown into multi-millionpound successful family-owned convenience food retailers. Bells have embracedthe development of technology in the retail sector and Bells Direct is a ‘leading

410 The International Review of Retail, Distribution and Consumer Research

Dow

nloa

ded

by [

The

Uni

vers

ity o

f M

anch

este

r L

ibra

ry]

at 0

7:06

06

Nov

embe

r 20

14

edge’ food e-retailer in 2001. In addition, the use of the Internet on the supplychain, in areas such as transportation, order processing, purchasing and procure-ment, customer service and inventory management, is becoming more wide-spread (Graham and Hardaker 2000). However, a large majority of the retailersin the survey did not have their own website, and were unsure of the value ofother technology-related initiatives. The growth potential through e-tailing iscurrently beyond the technical expertise of many independent food and groceryretailers who would need specialist courses in these areas, and clearer guidelinesas to costs and effort associated with implementation.

A response to Dawson and Kirby’s pleas for governmental lobbying on behalfof the independent food and grocery retailer can be seen in the work of theAssociation of Convenience Stores (ACS), which was formed in 1995. The ACSaims:

To pro-actively develop the whole of the professional convenience store sector,for the current and future bene� t of retailers, wholesalers and suppliers,through acting as the voice of the sector with Government and policy makers;campaigning on key issues to give members a voice in discussion on matterswhich effect them; providing bene� ts and services to help members developtheir businesses; providing a forum for the exchange of ideas and relevantinformation.

(ACS: http://cstoreretailing.co.uk/about.html)

It is particularly effective in lobbying on issues such as alcohol and tobaccosmuggling, tax relief for security measures, Sunday trading legislation and raterelief for village stores. Given the very strongly and widely held views ofindependent retailers that national and local government bodies are too bureau-cratic and of little help, organizations such as the ACS may play an increasinglyimportant role. There is an opportunity to change these views through the SmallBusiness Service, set up by the Chancellor of the Exchequer in the UK Budgetspeech of March 1999, but the effects of this initiative were not known at thetime of the survey. By gaining support of major suppliers such as Procter andGamble, Imperial Tobacco and Bass, the ACS is also helping to address thevertical supply chain relationships discussed above. But, otherwise, most of itsefforts are directed at preventing any increases in the costs of running itsmembers’ businesses, rather than identifying competitive advantages for them.

Dawson and Kirby’s suggestions were made at a time when there was generalagreement about the polarization of the retail landscape. However the lesseningof the gap between the offer of ‘convenience’ by the independent and multiplefood and grocery retailers has resulted in a retail environment, starting in thelate 1990s, where independent retailers do not necessarily have a competitiveadvantage through convenience alone. While owners and managers of independ-ent retail businesses perceive that they and their staff are competent in generalretail skills, customer care, health and safety, hygiene and store operations, theymay no longer be able to compete with the multiple grocery retailers on openinghours, location and serving the catchment population – key elements ofconvenience retailing.

Beyond convenience, the survey has con� rmed once again a key strength ofthe independent food and grocery retailer – the ability and willingness to

Baron et al.: Beyond convenience 411

Dow

nloa

ded

by [

The

Uni

vers

ity o

f M

anch

este

r L

ibra

ry]

at 0

7:06

06

Nov

embe

r 20

14

provide a social shopping experience for their consumers. The provision of thesesocial bene� ts for customers is an essential component of the service offers ofindependent retailers, which is not easily replicated by the competing multipleretailers. This constitutes a key source of potential competitive advantage forthem, and can be enhanced proactively, rather than being offered as a case forgovernment intervention. Current training provision fails to recognize theimportance of this feature of their offer. Advanced social skills would be requiredto preserve and enhance this aspect of retail provision that is valued so highly byconsumers. To build on this strength, owners and staff should invest in means ofmaintaining and enhancing the social element of their service. Rather thanspending more money and time on employees for them to acquire general retailor selling skills (which, in any case, are believed to be generally high), retailerscould look to improve the facilitation and improvization skills of staff, with aprimary focus on creating a friendly, social environment in their shops andstores.

According to Berry (2001), in the context of US retailing:

Today’s shoppers want the total consumer experience: superior solutions totheir needs, respect, an emotional connection, fair prices and convenience.Offering four out of the � ve pillars isn’t enough; a retailer must offer all ofthem.

(Berry 2001, p. 132)

The survey of UK independent food and grocery retailers shows that they maybe able to satisfy the four non-convenience pillars, and move beyond conveni-ence, as long as they are open to technological innovations to provide superiorsolutions to shoppers’ needs, and continue to develop the social settings whichpromote respect and an emotional connection with the customers.

Conclusion

This study is timely in providing some areas for further development of the UKindependent food and grocery retailer sector which, despite the many challengesits faces, can continue to be a signi� cant feature of the retail landscape.

The polarization of the landscape, which characterized the sector in the 1970sand 1980s, became less apparent in the 1990s, and the offer of convenienceretailing became part of the strategies of large supermarket groups and forecourtretailers, and therefore was no longer a competitive advantage, per se, forindependent retailers. The independent retail sector has responded, in variousdegrees, to the suggestions for survival and success made by Dawson and Kirbyin 1979. However, the suggestions made in the late 1990s – for small independ-ent retailers to adopt the new technologies, and strengthen both vertical andhorizontal alliances – are not, according to the survey reported here, beingembraced widely. They may be essential to embrace, in order to keep up with thetimes and the rising consumer expectations.

Perhaps the strongest feature to emerge from the survey is the con� rmation ofthe small retail store as a centre for social and community activity (Davies andHarris 1990). Rather than being taken for granted, and indeed underplayed as a

412 The International Review of Retail, Distribution and Consumer Research

Dow

nloa

ded

by [

The

Uni

vers

ity o

f M

anch

este

r L

ibra

ry]

at 0

7:06

06

Nov

embe

r 20

14

consumer bene� t, we suggest that this role can be re-af� rmed as a competitiveadvantage. A concentration on the training of higher-level interpersonal skills forthe staff can be a relatively low cost way of increasing customer retention andfrequency of visit.

The research has limitations, especially in relation to the non-randomsampling methods employed. Future research could concentrate on a smallersampling frame, for example non-af� liated independent retailers only, and focuson a single issue such as the adoption of new technology, or the creation ofconsumer experiences. This could provide greater insights into the readiness ofthe group to adopt such ideas.

References

Baron, S., Leaver, D., Old� eld, B.M.and Cassidy, K. (1999) ‘Economic andsocial trends and the non-af� liatedindependent retailer’. Available on-line:http: www.man-bus.mmu.ac.uk/retmark/reports/rmesftrends.htm

Bates, P. (1976) The Independent GroceryRetailer, Manchester: ManchesterBusiness School.

Berry, B.J.L. (1963) ‘Commercialstructure and commercial blight’,University of Chicago, Department ofGeography, Research Paper No. 85.

Berry, L.L. (2001) ‘The old pillars ofnew retailing’, Harvard BusinessReview, April: 131–7.

Brown, S. (1987) ‘An integratedapproach to retail change: the multi-polarization model’, The ServicesIndustries Journal, 7(2): 153–64.

Burns, W. (1954) ‘The despised cornershop’, The Surveyor, 113: 823–4.

Channing, W. (1960) ‘Retaildevelopment in Europe’, EuropeanProductivity, 36: 16–24.

Collin, F. (1937) ‘Rapport sur les classesmoyennes artisanales et commerciales’,Commission du Commerce, Brussels.

Davies, G. and Harris, K. (1990) SmallBusiness: The Independent Retailer,Basingstoke: MacMillan Education.

Dawson, J.A. and Kirby, D.A. (1979)Small Scale Retailing in the UK,Farnborough: Saxon House.

Daily Mail (1999) ‘Toys and shoeshopsnext in the high street wipeout’, 10March.

DETR (1998) The Impact of LargeFoodstores on Market Towns and District

Centres, London: The StationeryOf� ce.

DETR (1999) The Survival of the LocalShop, Retail and Consumer ServicesForesight Panel, London: TheStationery Of� ce.

Dixon, D.F. and McLaughlin, D.J.(1968) ‘Do the inner city poor paymore for food?’ Temple UniversityEconomic and Business Bulletin, 20:6–12.

DTI (2000) Bridging the Gap: Building aPartnership Between Retail andEducation, Retail and ConsumerServices Foresight Panel. Availablefrom Department of Trade andIndustry, 1 Victoria Street, LondonSW1H 0ET.

Financial Mail on Sunday (1999) ‘Storegiants think small’, 25 July.

Gordon, D. and Walton, J. (2000)Convenience Retailing 2000: TheMarket Review, Letchmore Heath:IGD Business Publication.

Gordon, D. and Wilson, S. (1999)Convenience Tracking Programme:Market Review 1999, LetchmoreHeath: IGD Business Publication.

Graham, G. and Hardaker, G. (2000)‘Supply-chain management across theInternet’, International Journal ofPhysical Distribution and LogisticsManagement, 30(3): 286–95.

Guardian (1999) ‘Time Britain ended E-commerce lip-service’, 14 September.

Hallsworth, A.G. and Worthington, S.(2000) Local resistance to largerretailers: the example of market townsand the food superstore in the UK,International Journal of Retail and

Baron et al.: Beyond convenience 413

Dow

nloa

ded

by [

The

Uni

vers

ity o

f M

anch

este

r L

ibra

ry]

at 0

7:06

06

Nov

embe

r 20

14

Distribution Management, 28(4/5):207–16.

Haugh, H.M. and Pardy, W. (1999)Community entrepreneurship in NorthEast Scotland, International Journal ofEntrepreneurial Behaviour and Research,5(4): 163–72.

Henley Centre (2001) ConvenienceMarketing Conference, London, 23January.

Kirby, D. (1987) ‘Convenience stores’, inMcFadyen, E. (ed.), The Changing Faceof British Retailing, London: Newman,pp. 94–102.

Labat, G. (1972) ‘Contribution a l’etudede la modernisation du commerce: lecas d’hypercosmos’, University ofBordeaux, Institute of BusinessStudies.

McClelland, W.G. (1966) Costs andCompetition in Retailing. London:Macmillan.

McGarry, E.D. (1930) ‘Retail trademortality’, University of Buffalo,Bureau of Business and SocialResearch Studies in Business, No. 4.

Maroney, A. (1976) ‘The decline ofsmall shops in Liverpool and theproblems involved in providing newfacilities’, in Jones, P. and Oliphant, R.(eds) Local Shops: Problems andProspects, Reading: URPI, pp. 33–43.

Morganosky, M.A. and Cude, B.J.(2000) Consumer response to onlinegrocery shopping, International Journalof Retail and Distribution Management,28(1): 17–26.

Moss, L. (1958) The Consumer’s FoodBuying Habits, Paris: OEEC.

Nystrom, P. (1930) Economics ofRetailing, New York: Ronald Press.

The Observer (1999) ‘Internet shoppingto be included in retail price index’, 10October.

Parker, C. and Byrom, J. (eds) (2000)Towards a ‘Healthy High Street’:Training the Independent Retailer,Manchester: Manchester MetropolitanUniversity.

Peston, L. and Ennew, C.T. (1998)Neighbourhood shopping in themillennium, University of NottinghamBusiness School Discussion Paper1998, XII, October.

Pickering, J.F., Greene, F.J. andCockerill, T.A.J. (1998) The Future ofthe Neighbourhood Store, UK: DurhamUniversity Business SchoolPublications, September.

Piercy, N. (1999) Cases in Market-LedStrategic Change, Oxford: Heinemann.

Smith, A. and Sparks, L. (2000) ‘Therole and function of the independentsmall shop: the situation in Scotland,The International Review of Retail,Distribution and Consumer Research,10(2): 205–26.

Smith, H. (1937) Retail Distribution,London: Oxford University Press.

Super Marketing (1998) ‘Multiples putsmall businesses at risk’, 21 August.

Weller, S. (2001) ‘Staying ahead of yourcompetitors’, Retail Week Conference,London, 5–6 March.

414 The International Review of Retail, Distribution and Consumer Research

Dow

nloa

ded

by [

The

Uni

vers

ity o

f M

anch

este

r L

ibra

ry]

at 0

7:06

06

Nov

embe

r 20

14