Embed Size (px)

Citation preview

Financial Report For the Fiscal Year Ended

June 30, 2014

Bedford County

Public Service

Authority

BEDFORD COUNTY PUBLIC SERVICE AUTHORITY

BEDFORD, VIRGINIA

FINANCIAL REPORT

For the Fiscal Year Ended June 30, 2014

PREPARED BY THE FINANCE DEPARTMENT

BEDFORD COUNTY PUBLIC SERVICE AUTHORITY

TABLE OF CONTENTS

FINANCIAL SECTION

Independent Auditor’s Report ............................................................................................................................. 1

Financial Statements

Exhibit 1 Statement of Net Position ............................................................................................................... 4

Exhibit 2 Statement of Revenues, Expenses, and Changes in Net Position ................................................................................................................................... 5

Exhibit 3 Statement of Cash Flows................................................................................................................. 6

Notes to Financial Statements ............................................................................................................................. 7

COMPLIANCE SECTION

Independent Auditor’s Report on Internal Control over Financial Reporting and onCompliance and Other Matters Based on an Audit of Financial Statements

Performed in Accordance with Government Auditing Standards ............................................................. 14

Schedule of Finding and Response ................................................................................................................... 16

FINANCIAL SECTION

Financial Section contains the Basic Financial Statements.

1Your Success is Our Focus

319 McClanahan Street, S.W. • P.O. Box 12388 • Roanoke, VA 24025-2388 • 540-345-0936 • Fax: 540-342-6181 • www.BEcpas.com

INDEPENDENT AUDITOR’S REPORT

To the Honorable Members of the Board of DirectorsBedford Regional Water AuthorityBedford, Virginia

Report on the Financial Statements

We have audited the accompanying financial statements of the Bedford County Public Service Authority (the “Authority”) as of and for the year ended June 30, 2014, and the related notes to the financial statements, which collectively comprise the Authority’s basic financial statements as listed in the table of contents. The prior year partial comparative information has been derived from the Authority’s 2013 financial statements and, in our report dated September 27, 2013, we expressed an unmodified opinion on the respective financial statements.

Management’s Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error.

Auditor’s Responsibility

Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States, and Specifications for Audits of Authorities, Boards and Commissions issued by the Auditor of Public Accounts of the Commonwealth of Virginia.Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the Authority’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Authority’s internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

2

Report on the Financial Statements (Continued)

Opinion

In our opinion, the financial statements referred to above present fairly, in all material respects, the respective financial position of the Bedford County Public Service Authority, as of June 30, 2014, and the respective changes in financial position and cash flows thereof for the year then ended in accordance with accounting principles generally accepted in the United States of America.

Change in Accounting Principle

As described in Note 6 to the financial statements, in 2014, the Authority adopted new accounting guidance, GASB Statement No. 65, Items Previously Reported as Assets and Liabilities. Our opinion is not modified with respect to this matter.

Emphasis of Matter

As discussed in Note 5 to the financial statements, the Authority ceased operations and transferred all assets, liabilities, and agreements to the Bedford Regional Water Authority effective July 1, 2013. Our opinion is not modified with respect to that matter.

Other Matters

Required Supplementary Information

Management has omitted management’s discussion and analysis that accounting principles generally accepted in the United States of America require to be presented to supplement the basic financial statements. Such missing information, although not a part of the basic financial statements, is required by the Governmental Accounting Standards Board, who considers it to be an essential part of financial reporting for placing the basic financial statements in an appropriate operational, economic, or historical context. Our opinion on the basic financial statements is not affected by this missing information.

Other Reporting Required by Government Auditing Standards

In accordance with Government Auditing Standards, we have also issued our report dated September __, 2014 on our consideration of the Authority’s internal control over financial reporting and on our tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements and other matters. The purpose of that report is to describe the scope of our testing of internal control over financial reporting and compliance and the results of that testing, and not to provide an opinion on internal control over financial reporting or on compliance. That report is an integral part of an audit performed in accordance with Government Auditing Standards in considering the Authority’s internal control over financial reporting and compliance.

CERTIFIED PUBLIC ACCOUNTANTS

Roanoke, VirginiaOctober 8, 2014

3

FINANCIAL STATEMENTS

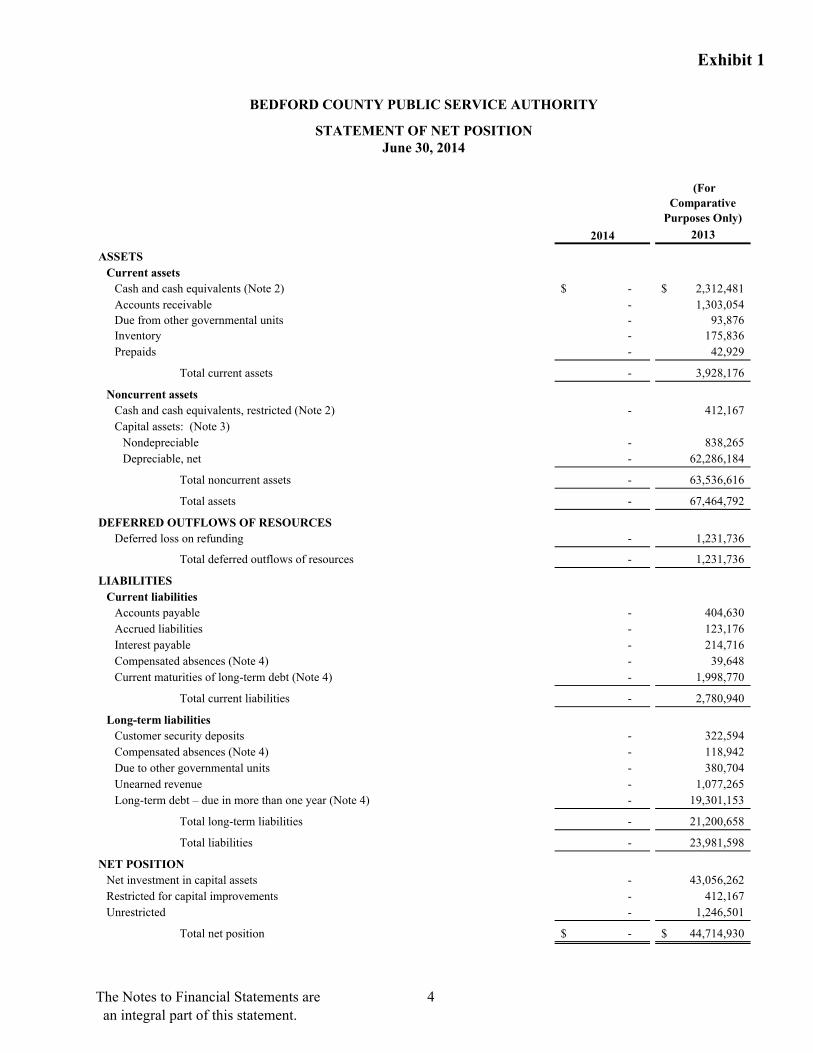

Exhibit 1

(For

Comparative

Purposes Only)

2013

ASSETS

Current assets

Cash and cash equivalents (Note 2) -$ 2,312,481$

Accounts receivable - 1,303,054

Due from other governmental units - 93,876

Inventory - 175,836

Prepaids - 42,929

Total current assets - 3,928,176

Noncurrent assets

Cash and cash equivalents, restricted (Note 2) - 412,167

Capital assets: (Note 3)

Nondepreciable - 838,265

Depreciable, net - 62,286,184

Total noncurrent assets - 63,536,616

Total assets - 67,464,792

DEFERRED OUTFLOWS OF RESOURCES

Deferred loss on refunding - 1,231,736

Total deferred outflows of resources - 1,231,736

LIABILITIES

Current liabilities

Accounts payable - 404,630

Accrued liabilities - 123,176

Interest payable - 214,716

Compensated absences (Note 4) - 39,648

Current maturities of long-term debt (Note 4) - 1,998,770

Total current liabilities - 2,780,940

Long-term liabilities

Customer security deposits - 322,594

Compensated absences (Note 4) - 118,942

Due to other governmental units - 380,704

Unearned revenue - 1,077,265

Long-term debt – due in more than one year (Note 4) - 19,301,153

Total long-term liabilities - 21,200,658

Total liabilities - 23,981,598

NET POSITION

Net investment in capital assets - 43,056,262

Restricted for capital improvements - 412,167

Unrestricted - 1,246,501

Total net position -$ 44,714,930$

BEDFORD COUNTY PUBLIC SERVICE AUTHORITY

STATEMENT OF NET POSITIONJune 30, 2014

2014

The Notes to Financial Statements are an integral part of this statement.

4

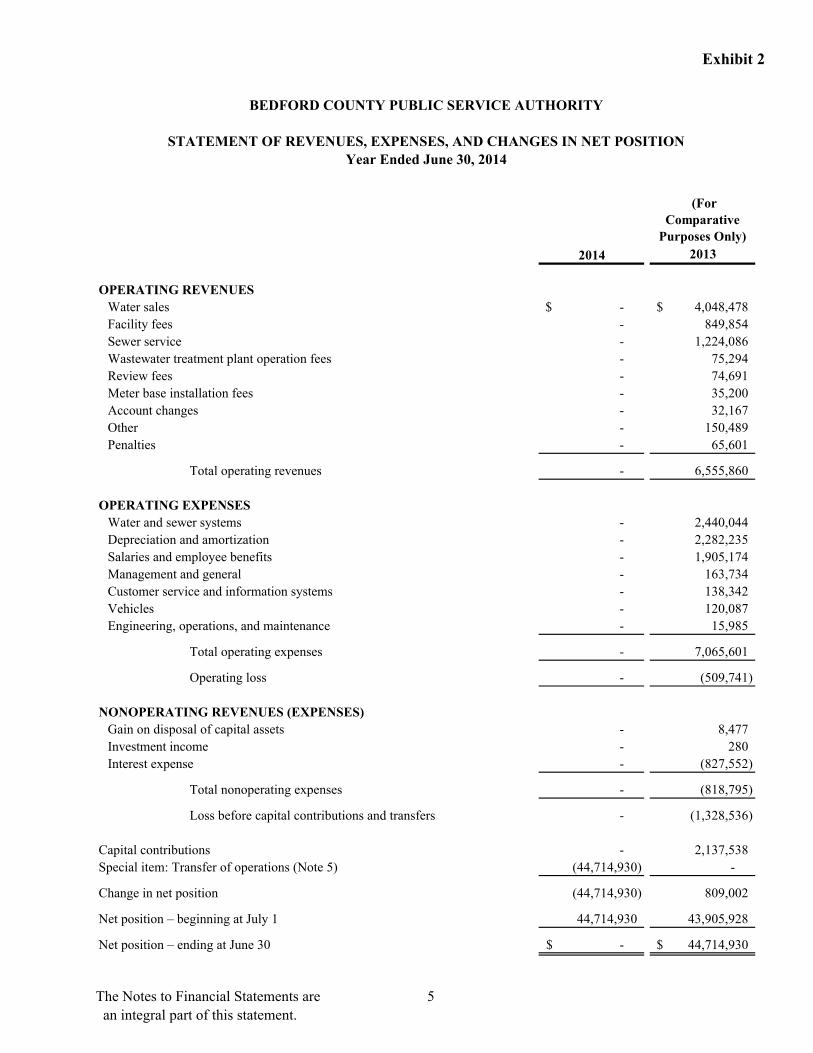

Exhibit 2

(For

Comparative

Purposes Only)

2013

OPERATING REVENUES

Water sales -$ 4,048,478$

Facility fees - 849,854

Sewer service - 1,224,086

Wastewater treatment plant operation fees - 75,294

Review fees - 74,691

Meter base installation fees - 35,200

Account changes - 32,167

Other - 150,489

Penalties - 65,601

Total operating revenues - 6,555,860

OPERATING EXPENSES

Water and sewer systems - 2,440,044

Depreciation and amortization - 2,282,235

Salaries and employee benefits - 1,905,174

Management and general - 163,734

Customer service and information systems - 138,342

Vehicles - 120,087

Engineering, operations, and maintenance - 15,985

Total operating expenses - 7,065,601

Operating loss - (509,741)

NONOPERATING REVENUES (EXPENSES)

Gain on disposal of capital assets - 8,477

Investment income - 280

Interest expense - (827,552)

Total nonoperating expenses - (818,795)

Loss before capital contributions and transfers - (1,328,536)

Capital contributions - 2,137,538

Special item: Transfer of operations (Note 5) (44,714,930) -

Change in net position (44,714,930) 809,002

Net position – beginning at July 1 44,714,930 43,905,928

Net position – ending at June 30 -$ 44,714,930$

2014

BEDFORD COUNTY PUBLIC SERVICE AUTHORITY

STATEMENT OF REVENUES, EXPENSES, AND CHANGES IN NET POSITION

Year Ended June 30, 2014

The Notes to Financial Statements are

an integral part of this statement.

5

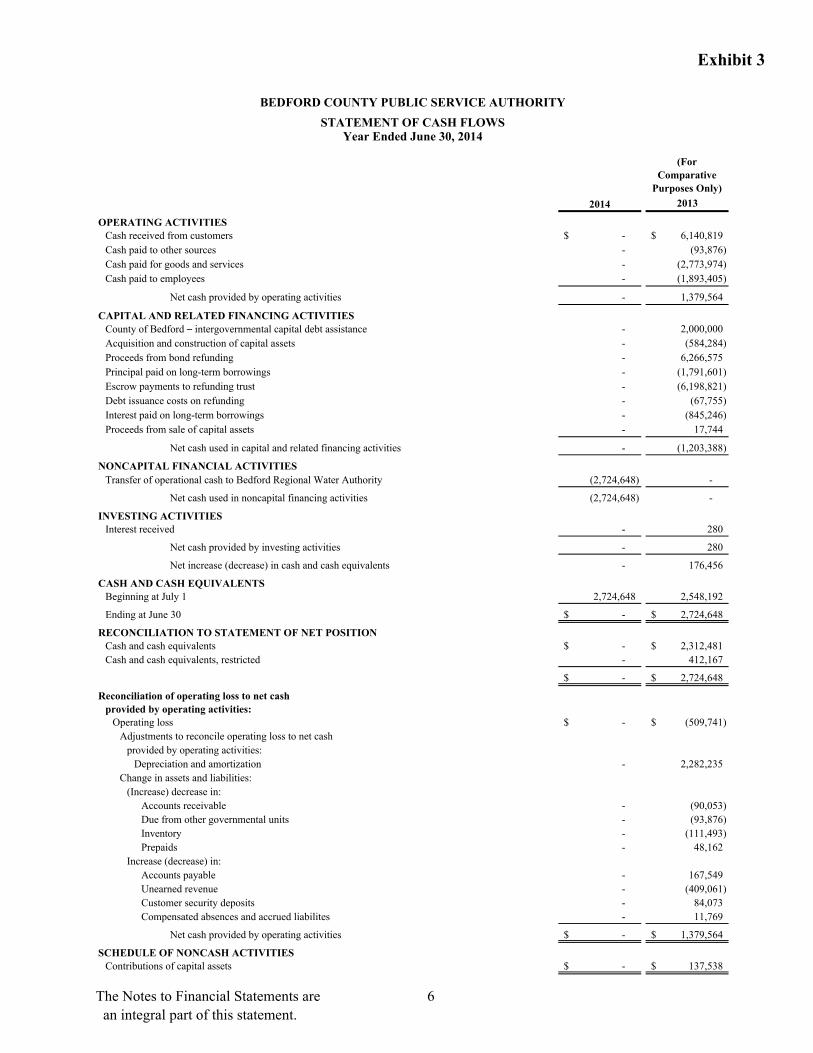

Exhibit 3

(For

Comparative

Purposes Only)

2013

OPERATING ACTIVITIESCash received from customers -$ 6,140,819$

Cash paid to other sources - (93,876)

Cash paid for goods and services - (2,773,974)

Cash paid to employees - (1,893,405)

Net cash provided by operating activities - 1,379,564

CAPITAL AND RELATED FINANCING ACTIVITIES

County of Bedford – intergovernmental capital debt assistance - 2,000,000

Acquisition and construction of capital assets - (584,284)

Proceeds from bond refunding - 6,266,575

Principal paid on long-term borrowings - (1,791,601)

Escrow payments to refunding trust - (6,198,821)

Debt issuance costs on refunding - (67,755)

Interest paid on long-term borrowings - (845,246)

Proceeds from sale of capital assets - 17,744

Net cash used in capital and related financing activities - (1,203,388)

NONCAPITAL FINANCIAL ACTIVITIES

Transfer of operational cash to Bedford Regional Water Authority (2,724,648) -

Net cash used in noncapital financing activities (2,724,648) -

INVESTING ACTIVITIESInterest received - 280

Net cash provided by investing activities - 280

Net increase (decrease) in cash and cash equivalents - 176,456

CASH AND CASH EQUIVALENTSBeginning at July 1 2,724,648 2,548,192

Ending at June 30 -$ 2,724,648$

RECONCILIATION TO STATEMENT OF NET POSITIONCash and cash equivalents -$ 2,312,481$

Cash and cash equivalents, restricted - 412,167

-$ 2,724,648$

Reconciliation of operating loss to net cash

provided by operating activities:Operating loss -$ (509,741)$

Adjustments to reconcile operating loss to net cash

provided by operating activities:

Depreciation and amortization - 2,282,235

Change in assets and liabilities:

(Increase) decrease in:

Accounts receivable - (90,053)

Due from other governmental units - (93,876)

Inventory - (111,493)

Prepaids - 48,162

Increase (decrease) in:

Accounts payable - 167,549

Unearned revenue - (409,061)

Customer security deposits - 84,073

Compensated absences and accrued liabilites - 11,769

Net cash provided by operating activities -$ 1,379,564$

SCHEDULE OF NONCASH ACTIVITIESContributions of capital assets -$ 137,538$

2014

BEDFORD COUNTY PUBLIC SERVICE AUTHORITY

STATEMENT OF CASH FLOWSYear Ended June 30, 2014

The Notes to Financial Statements are

an integral part of this statement.

6

BEDFORD COUNTY PUBLIC SERVICE AUTHORITY

NOTES TO FINANCIAL STATEMENTSJune 30, 2014

(Continued) 7

Note 1. Summary of Significant Accounting Policies

Reporting entity:

The Bedford County Public Service Authority (the “Authority”) was chartered June 8, 1970 under the Water and Sewer Authorities Act of 1950 of the Commonwealth of Virginia. The Authority primarily served water and sewer needs of the Smith Mountain Lake, Forest, Montvale, Stewartsville, New London, and Boonsboro areas of Bedford County, Virginia. The Authority operated on a Board-administrator form of government. The Board consisted of a Chairman and six other Board members, who were appointed by the Bedford County Board of Supervisors. The Authority was not a component unit of the County of Bedford, since it was neither fiscally dependent on nor governed by the County. The Authority ceased operations effective July 1, 2013 (Note 5).

Measurement focus and basis of accounting:

The Authority’s financial statements are reported using the accrual basis of accounting. Revenues are recorded when earned and expenses are recorded when a liability is incurred, regardless of the timing of related cash flows.

The Authority distinguishes operating revenues and expenses from nonoperating items. Operating revenues and expenses generally result from providing services and producing and delivering goods in connection with the Authority’s principal ongoing operations. The principal operating revenues of the Authority are charges to customers for sales and services. The Authority also recognizes as operating revenue the portion of facility fees intended to recover the cost of connecting new customers to the system. Operating expenses include the cost of sales and services, administrative expenses, and depreciation on capital assets. All revenues and expenses not meeting this definition are reported as nonoperating revenues and expenses.

When both restricted and unrestricted resources are available for use, it is the Authority’s policy to use restricted resources first, then unrestricted resources as they are needed.

Cash and cash equivalents:

The Authority’s cash and cash equivalents are considered to be cash on hand, demand deposits, and short-term investments with original maturities three months or less from the date of acquisition.

Capital assets:

Capital assets are stated at cost, except for donated assets, which are recorded at fair market value at the date of acquisition. The threshold for recording capital assets is $1,000. Depreciation of property and equipment is computed using the straight-line method over useful lives as follows:

Transmission/distribution lines 50-66 yearsSewer system 50-66 yearsReservoirs, standpipes, and source of supply structures 50-66 yearsMotor vehicles 5-7 yearsOffice furniture, fixtures, and equipment 5-7 yearsMaintenance and engineering equipment 5-10 years

BEDFORD COUNTY PUBLIC SERVICE AUTHORITY

NOTES TO FINANCIAL STATEMENTSJune 30, 2014

(Continued) 8

Note 1. Summary of Significant Accounting Policies (Continued)

Capital assets: (Continued)

Leasehold improvements include administrative and other facilities constructed and additions affixed to those facilities on land leased from Bedford County. These leasehold improvements are depreciated over the shorter of the useful life of the asset or the remaining term of the lease. The lease term includes all reasonably assured renewals.

Capitalization of interest:

Interest expense applicable to indebtedness used to construct new facilities is capitalized during the period of construction as part of the cost of such facilities. Other interest costs of the Authority are treated as nonoperating expenses.

Deferred outflows/inflows of resources:

In addition to assets, the statement of net position reports a separate section for deferred outflows of resources. This separate financial statement element, deferred outflows of resources, represents a consumption of net position that applies to future periods and so will not be recognized as an outflow of resources (expense) until then. The Authority only has one item that qualifies for reporting in this category, deferred loss on refunding. A deferred loss on refunding results from the difference in the carrying value of refunded debt and its reacquisition price. This amount is deferred and amortized over the shorter of the life of the refunded or refunding debt. Due to the relationship with outstanding debt, these deferred outflows are included in the calculation of net position, net investment in capital assets.

In addition to liabilities, the statement of financial position reports a separate section for deferred inflows of resources. This separate financial statement element, deferred inflows of resources, represents an acquisition of net position that applies to future periods and so will not be recognized as an inflow of resources (revenue) until that time. The Authority has no items that qualify for reporting in this category.

Unearned revenue:

Unearned revenue consists of monies or tangible assets given to the Authority under prescribed conditions by developers in exchange for credit vouchers to be used to pay facility fees (both water and sewer) in order to connect to the Authority’s system. These amounts are deferred and recognized as an inflow of resources in the period that the amounts become earned. The Authority recognized the revenue when the credit voucher is redeemed.

Compensated absences:

The paid-time-off (PTO) policy of the Authority provides for up to 296 hours per year of earned vacation leave, depending on years of service. Employees may carry over an unlimited amount of PTO hours to the succeeding year. Upon termination, the first 200 hours of accumulated PTO is 100% payable and the next 200 hours is 50% payable. Compensated absences are accrued when incurred.

BEDFORD COUNTY PUBLIC SERVICE AUTHORITY

NOTES TO FINANCIAL STATEMENTSJune 30, 2014

(Continued) 9

Note 1. Summary of Significant Accounting Policies (Continued)

Net position:

Net position is the difference between assets, deferred outflows of resources, liabilities, and deferred inflows of resources. Net investment in capital assets represents capital assets, less accumulated depreciation, less any outstanding debt and related deferred inflows or outflows of resources related to the acquisition, construction, or improvement of those assets. Net investment in capital assets excludes unspent debt proceeds. Net position is reported as restricted when there are limitations imposed on itsuse either through the enabling legislation adopted by the Authority or through external restrictions imposed by creditors, grantors, or laws or regulations of other governments.

Comparative information:

The basic financial statements include certain prior year summarized comparative information in total,but not at the level of detail required for a presentation in conformity with generally accepted accounting principles. Accordingly, such information should be read in conjunction with the Authority’s financial statements for the prior year from which the summarized information was derived.

Estimates:

Management uses estimates and assumptions in preparing its financial statements. Actual results could differ from those estimates.

Note 2. Cash and Investments

Deposits:

Deposits with banks are covered by the Federal Deposit Insurance Corporation (FDIC) and collateralized in accordance with the Virginia Security for Public Deposits Act (the “Act”) Section 2.2-4400 et. seq. of the Code of Virginia. Under the Act, banks and savings institutions holding public deposits in excess of the amount insured by the FDIC must pledge collateral to the Commonwealth of Virginia Treasury Board. Financial institutions may choose between two collateralization methodologies and depending upon that choice, will pledge collateral that ranges in the amounts from 50% to 130% of excess deposits. Accordingly, all deposits are considered fully collateralized.

Investments:

Statutes authorize the Authority to invest in obligations of the United States or agencies thereof; obligations of the Commonwealth of Virginia or political subdivisions thereof; obligations of the International Bank, the African Development Bank, “prime quality” commercial paper and certain corporate notes, banker’s acceptances, repurchase agreements, and the State Treasurer’s Local Government Investment Pool (LGIP).

The fair value of the positions in the external investment pool (Local Government Investment Pool) is the same as the value of the pool shares. As these pools are not SEC registered, regulatory oversight of the pools rests with the Virginia State Treasury. Local Government Investment Pool maintains a policy to operate in a manner consistent with SEC Rule 2a-7.

Due to the nature of LGIP, it is considered a cash and cash equivalent on the statement of net position.

BEDFORD COUNTY PUBLIC SERVICE AUTHORITY

NOTES TO FINANCIAL STATEMENTSJune 30, 2014

(Continued) 10

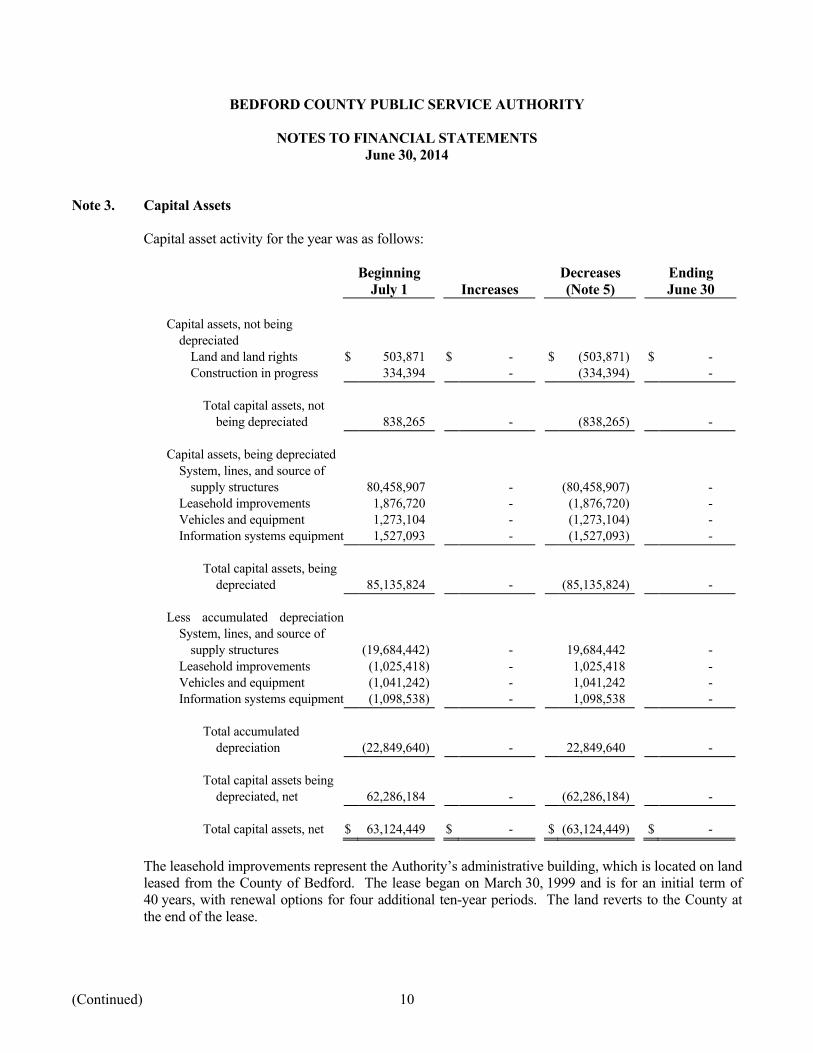

Note 3. Capital Assets

Capital asset activity for the year was as follows:

Beginning July 1 Increases

Decreases(Note 5)

Ending June 30

Capital assets, not beingdepreciated

Land and land rights $ 503,871 $ - $ (503,871) $ - Construction in progress 334,394 - (334,394) -

Total capital assets, notbeing depreciated 838,265 - (838,265) -

Capital assets, being depreciatedSystem, lines, and source of

supply structures 80,458,907 - (80,458,907) - Leasehold improvements 1,876,720 - (1,876,720) - Vehicles and equipment 1,273,104 - (1,273,104) - Information systems equipment 1,527,093 - (1,527,093) -

Total capital assets, beingdepreciated 85,135,824 - (85,135,824) -

Less accumulated depreciation for:System, lines, and source of

supply structures (19,684,442) - 19,684,442 - Leasehold improvements (1,025,418) - 1,025,418 - Vehicles and equipment (1,041,242) - 1,041,242 - Information systems equipment (1,098,538) - 1,098,538 -

Total accumulateddepreciation (22,849,640) - 22,849,640 -

Total capital assets beingdepreciated, net 62,286,184 - (62,286,184) -

Total capital assets, net $ 63,124,449 $ - $ (63,124,449) $ -

The leasehold improvements represent the Authority’s administrative building, which is located on land leased from the County of Bedford. The lease began on March 30, 1999 and is for an initial term of 40 years, with renewal options for four additional ten-year periods. The land reverts to the County at the end of the lease.

BEDFORD COUNTY PUBLIC SERVICE AUTHORITY

NOTES TO FINANCIAL STATEMENTSJune 30, 2014

(Continued) 11

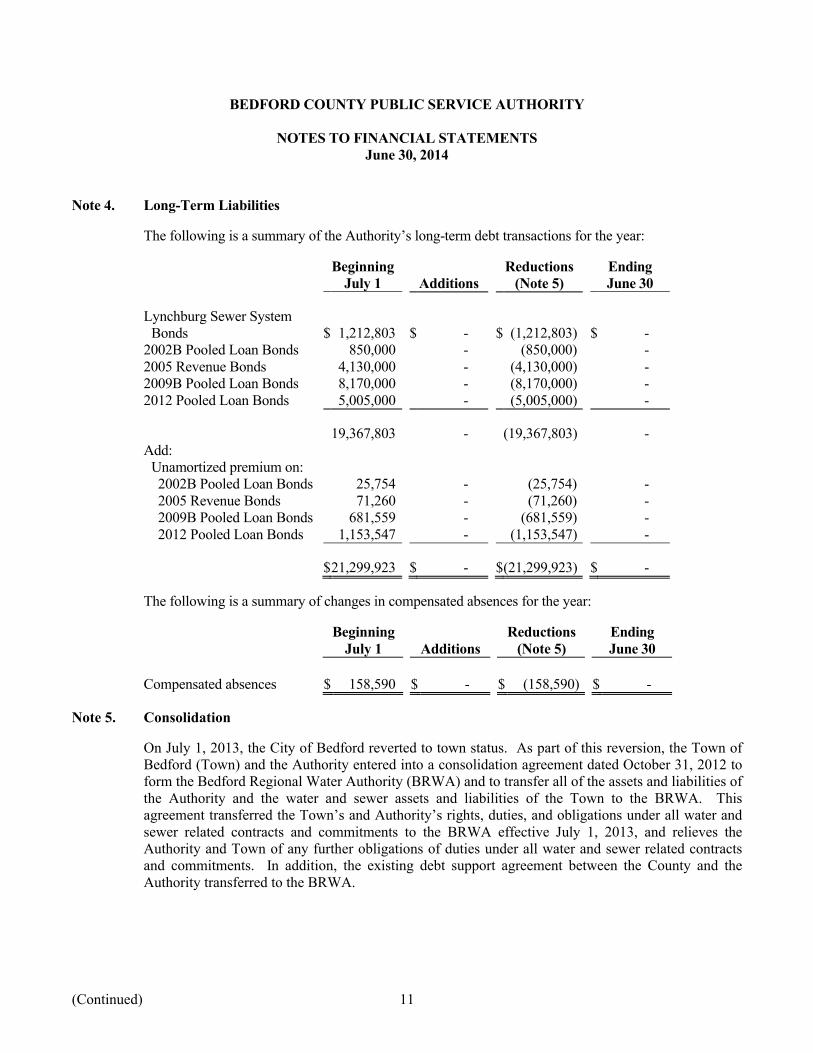

Note 4. Long-Term Liabilities

The following is a summary of the Authority’s long-term debt transactions for the year:

BeginningJuly 1 Additions

Reductions(Note 5)

Ending June 30

Lynchburg Sewer System Bonds $ 1,212,803 $ - $ (1,212,803) $ -

2002B Pooled Loan Bonds 850,000 - (850,000) - 2005 Revenue Bonds 4,130,000 - (4,130,000) - 2009B Pooled Loan Bonds 8,170,000 - (8,170,000) - 2012 Pooled Loan Bonds 5,005,000 - (5,005,000) -

19,367,803 - (19,367,803) - Add:

Unamortized premium on:2002B Pooled Loan Bonds 25,754 - (25,754) - 2005 Revenue Bonds 71,260 - (71,260) - 2009B Pooled Loan Bonds 681,559 - (681,559) - 2012 Pooled Loan Bonds 1,153,547 - (1,153,547) -

$21,299,923 $ - $(21,299,923) $ -

The following is a summary of changes in compensated absences for the year:

BeginningJuly 1 Additions

Reductions(Note 5)

EndingJune 30

Compensated absences $ 158,590 $ - $ (158,590) $ -

Note 5. Consolidation

On July 1, 2013, the City of Bedford reverted to town status. As part of this reversion, the Town of Bedford (Town) and the Authority entered into a consolidation agreement dated October 31, 2012 to form the Bedford Regional Water Authority (BRWA) and to transfer all of the assets and liabilities of the Authority and the water and sewer assets and liabilities of the Town to the BRWA. This agreement transferred the Town’s and Authority’s rights, duties, and obligations under all water and sewer related contracts and commitments to the BRWA effective July 1, 2013, and relieves the Authority and Town of any further obligations of duties under all water and sewer related contracts and commitments. In addition, the existing debt support agreement between the County and the Authority transferred to the BRWA.

BEDFORD COUNTY PUBLIC SERVICE AUTHORITY

NOTES TO FINANCIAL STATEMENTSJune 30, 2014

12

Note 5. Consolidation (Continued)

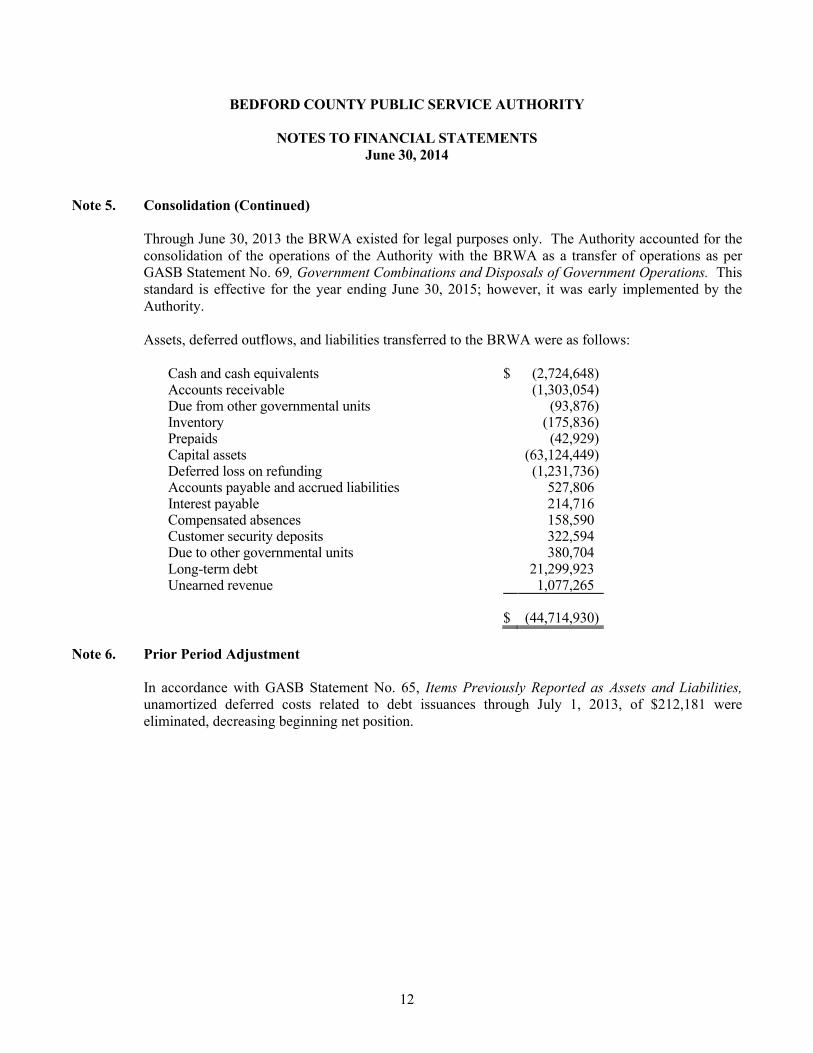

Through June 30, 2013 the BRWA existed for legal purposes only. The Authority accounted for the consolidation of the operations of the Authority with the BRWA as a transfer of operations as per GASB Statement No. 69, Government Combinations and Disposals of Government Operations. This standard is effective for the year ending June 30, 2015; however, it was early implemented by the Authority.

Assets, deferred outflows, and liabilities transferred to the BRWA were as follows:

Cash and cash equivalents $ (2,724,648)Accounts receivable (1,303,054)Due from other governmental units (93,876)Inventory (175,836)Prepaids (42,929)Capital assets (63,124,449)Deferred loss on refunding (1,231,736)Accounts payable and accrued liabilities 527,806Interest payable 214,716Compensated absences 158,590Customer security deposits 322,594Due to other governmental units 380,704Long-term debt 21,299,923Unearned revenue 1,077,265

$ (44,714,930)

Note 6. Prior Period Adjustment

In accordance with GASB Statement No. 65, Items Previously Reported as Assets and Liabilities, unamortized deferred costs related to debt issuances through July 1, 2013, of $212,181 were eliminated, decreasing beginning net position.

13

COMPLIANCE SECTION

14Your Success is Our Focus

319 McClanahan Street, S.W. • P.O. Box 12388 • Roanoke, VA 24025-2388 • 540-345-0936 • Fax: 540-342-6181 • www.BEcpas.com

INDEPENDENT AUDITOR’S REPORT ON INTERNAL CONTROL OVER FINANCIAL REPORTING AND ON COMPLIANCE AND OTHER MATTERS BASED ON AN AUDIT OF

FINANCIAL STATEMENTS PERFORMED IN ACCORDANCE WITH GOVERNMENT AUDITING STANDARDS

To the Honorable Members of the Board of DirectorsBedford Regional Water AuthorityBedford, Virginia

We have audited, in accordance with auditing standards generally accepted in the United States of America, the standards applicable to financial audits contained in Government Auditing Standards,issued by the Comptroller General of the United States; and Specifications for Audits of Authorities, Boards, and Commissions issued by the Auditor of Public Accounts of the Commonwealth of Virginia, the financial statements of the Bedford County Public Service Authority (the “Authority”), as of and for the year ended June 30, 2014, and the related notes to the financial statements, which collectively comprise the Authority’s basic financial statements, and have issued our report thereon dated October 8, 2014.

Internal Control over Financial Reporting

In planning and performing our audit of the financial statements, we considered the Authority’s internal control over financial reporting (internal control) to determine the audit procedures that are appropriate in the circumstances for the purpose of expressing our opinion on the financial statements, but not for the purpose of expressing an opinion on the effectiveness of the Authority’s internal control. Accordingly, we do not express an opinion on the effectiveness of the Authority’s internal control.

Our consideration of internal control was for the limited purpose described in the preceding paragraph and was not designed to identify all deficiencies in internal control that might be material weaknesses or, significant deficiencies and therefore, material weaknesses or significant deficiencies may exist that were not identified. However as described in the accompanying schedule of finding and response, we identified a certain deficiency in internal control that we consider to be a material weakness.

A deficiency in internal control exists when the design or operation of a control does not allow management or employees, in the normal course of performing their assigned functions, to prevent, or detect and correct misstatements on a timely basis. A material weakness is a deficiency, or a combination of deficiencies, in internal control such that there is a reasonable possibility that a material misstatement of the entity’s financial statements will not be prevented, or detected and corrected on a timely basis. A significant deficiency is a deficiency, or a combination of deficiencies, in internal control that is less severe than a material weakness, yet important enough to merit attention by those charged with governance. We consider the deficiency described in the accompanying schedule of finding and response, as item 08-1, to be a material weakness.

15

Compliance and Other Matters

As part of obtaining reasonable assurance about whether the Authority’s financial statements are free of material misstatement, we performed tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements, noncompliance with which could have a direct and material effect on the determination of financial statement amounts. However, providing an opinion on compliance with those provisions was not an objective of our audit, and accordingly, we do not express such an opinion. The results of our tests disclosed no instances of noncompliance or other matters that are required to be reported under Government Auditing Standards.

Management’s Response to Finding

The Authority’s response to the finding identified in our audit is described in the accompanying schedule of finding and response. The Authority’s response was not subjected to the auditing procedures applied in the audit of the financial statements and, accordingly, we express no opinion on the response.

Purpose of this Report

The purpose of this report is solely to describe the scope of our testing of internal control and compliance and the results of that testing, and not to provide an opinion on the effectiveness of the Authority’s internal control or on compliance. This report is an integral part of an audit performed in accordance with Government Auditing Standards in considering the Authority’s internal control and compliance. Accordingly, this communication is not suitable for any other purpose.

CERTIFIED PUBLIC ACCOUNTANTS

Roanoke, VirginiaOctober 8, 2014

16

BEDFORD COUNTY PUBLIC SERVICE AUTHORITY

SCHEDULE OF FINDING AND RESPONSEYear Ended June 30, 2014

A. FINDING – FINANCIAL STATEMENT AUDIT

08-1: Segregation of Duties (Material Weakness)

Condition:

A fundamental concept of internal controls is the separation of duties. No one employee should have access to both physical assets and the related accounting records or to all phases of a transaction. A proper segregation of duties has not been established in functions related to cash receipts, accounts receivable, cash disbursements, and accounts payable.

Recommendation:

Steps should be taken to eliminate performance of conflicting duties where possible or to implement effective compensating controls.

Management’s Response:

Management understands this concern; however, the current staff size limits the separation of duties in regards to these functions.