Embed Size (px)

DESCRIPTION

Monthly magazine for banking entrance exams in India

Citation preview

HIGHLIGHTS

Banking & Finance

Recent Banking Developments

Concept Briefs

Model Tests

J. S . INSTITUTE OF BANKING AND FINANCE PVT. LTD.Ramanashree Park View, 2nd Floor, 2462, 24th Cross Road,Banashankari 2nd Stage, Bangalore - 560 070.E-mail : [email protected] : www.jsinstitute.co.in

Vol. - IX May-2015 Issue - 9

J. S. DIGEST OFBANKING & FINANCE

Monthly Rs. 55/-SBI 2015 EXAMS

STP (PO/TO/JMG):

Please buy Banking Guide, MM Special Guide,and subscribe for 1 year Banking Digest (Aug14 to July 15.)

Please order immediately

Please do not postpone and avoid delay /

hassles like “out of stock”, last minute rush,

postal delay, etc.

The syllabus is vast and demands studious andcommitted preparation for a long time.

Please see our website

JS Digest of Banking and Finance May15 4 Contents

From the Editor’s Pen...

We have pleasure in placing

before our readers May 2015

Digest.

The issue contains the

latest developments in

Banking, Finance and

Economy, Recent Banking

Developments, Concept

Brief, Priority Sector

Lending and Model Tests.

We are sure these will be

found immensely useful by

the readers. We wish success

for our readers in the ensuing

exams and interviews.

- Editor

3

J.S. DIGEST OFBANKING AND FINANCE

Monthly Magazine

Vol.-IX May-15 Issue-9

Annual Subscription-Rs. 660/-

Single Copy - Rs. 55/-

Published byJ. S. INSTITUTE OF

BANKING AND FINANCEPVT. LTD.

Ramanashree Park View, 2ndFloor, 2462, 24th Cross Road,

Banashankari 2nd Stage,Bangalore-560 070.

Phone: 080-41307114Phone

E-MailPlease send messages inour new mail addresses

[email protected]@jsinstitute.co.in

Visit us at our newWebsite

www.jsinstitute.co.in

This issue consists of total124 pages including cover.

EditorG. Subramanian

CONTENTSVol. - IX May-15 Issue - 9

BANKING & FINANCE –May 2015

SBI:Rupay Platinum Debit Card ............... 7Deals with E-CommerceCompanies ................................................. 7New Cards ................................................. 7Online Overdraft Facility ...................... 7Results ........................................................ 7

RBI:3 Banks Penalised ................................... 8Liberalised Branch AuthorisationPolicy ........................................................... 8NBFCs Selling MFs ................................. 8Funds for Start-ups ................................ 8AFA Relaxed for SmallValue Transactions ................................. 8Resolution Period for StressedAssets .......................................................... 8Internal Ombudsman ............................ 9RBI on FDI Inflows ................................. 9Swap Transactions ................................. 9Resilience against Outflows ................. 9Trade Transaction Limit ....................... 9

Banking/Other Banks:Micro ATMs WithdrawalLimits .......................................................... 9Panel for Selecting Chairmenin PSBs ........................................................ 9Ping Pay ....................................................1 0Switching Fee ...........................................1 0Insurance Schemes ofGovernment ..............................................1 0Chequebook App ....................................1 0HDFC Bank’s SmartBuy ......................1 0ATM Transactions Decline ..................1 0Credit Cards .............................................1 0SC Notice for Hiring ofTop Executives in PSBs ........................1 0Voice Recognition Software ................1 1

Finance, SE:LIC’s Market Share ................................1 1Gold Monetisation Scheme ..................1 1

Insurance Policies in RuralSectors ........................................................1 12-Wheeler Insurance ..............................1 2Privatisation of ITDC Hotels .............1 2Insurance Schemes .................................1 2

Corporates:Capgemini’s Acquisition ofiGate ............................................................1 2Future-Bharti Pact .................................1 3Investment in India ................................1 3Nestle’s Maggi Unsafe ..........................1 3

Economy:Divestment ...............................................1 3Growth Forecast ......................................1 3Bad Loans .................................................1 3Table of Key Statistics ..........................1 3

National:Salman Khan Convicted .......................1 4India’s Largest Power Plant ...............1 4Earthquake in Andaman ......................1 4Social Security Schemes .......................1 4MoUs in Chhattisgarh ...........................1 4SC on Photos of Politicians .................1 5Black Money Bill .....................................1 5Urea Policy ...............................................1 5Credit to Mongolia .................................1 5Farmer Suicide .........................................1 5Cabinet clears Land BoundaryBill ................................................................1 5Lok Sabha Clears GST Bill ..................1 5Tamil Nadu’s Chief Minister ..............1 6Raju Out on Bail .....................................1 6Proposed GST Council .........................1 6Elections in Bihar ....................................1 6Environmental Clearance forMining Auctions .....................................1 6Pollution Violations ...............................1 6Heat Wave in AP, Telangana .............1 6AAP-LG Conflict in Delhi ...................1 6

International:Indian-Americans’ MedianIncome ........................................................1 7UK PM........................................................1 7

JS Digest of Banking and Finance May15

ADB Loan for WaterResource management ......................... 1 7Human Capital Index .......................... 1 7Pakistan Helicopter Crash ................. 1 7Sentence for Malala Attack ................ 1 7India-Japan Pact ................................... 1 7Kazakhstan President .......................... 1 7Disaster Losses ...................................... 1 7Morsi’s Death Sentence ........................ 1 8Air Pollution ............................................ 1 8FT Top 50 Executive EducationSchools ...................................................... 1 8Nepal Earthquake ................................. 1 8Banks Fined ............................................. 1 8US Economy ............................................ 1 8Japan’s Economy ................................... 1 8Kazakhstan Elections ........................... 1 8Japan’s Plan for AsianInfrastructure .......................................... 1 9

Technology:Motorola Patent Penalty ..................... 1 9Flipkart’s Acquisition ofAppiterate ................................................ 1 9Verizon’s Acquisition of AOL .......... 1 9Cognizant Results ................................. 1 9Job Cuts .................................................... 1 9

Dates, Anniversaries:. ....................... 1 9

Personalities:. ..........................................1 9

Sports:. ..................................................... 2 0

Awards/Recognitions:. ....................... 2 0

Appointments: . ................................... 2 0

Recent Banking Developments-Feb’15P B Business:Xpress Credit .......................................... 2 1The employees of reputed privateschools and colleges are now includedunder Xpress Credit Loan Scheme on theundernoted terms and conditions: ... 2 1Agri Business:Warehouse Receipt Financing withcollateral Management services:Improvement in Margin, CollateralSecurity and Rate of Interest: ............ 2 1Financing Agri Value Chain: NewScheme for Financing “Farmers

Producer Companies (FPCs) ..............2 2C & I Business:Industry Specific Benchmarks:Change in Loan Policy ............................ 2 4Foreign Exchange:Digitization of clearances –External Commercial Borrowings(ECB) and Trade Credit ............................. 2 5Foreign Exchange ManagementAt, 1999–Import of Goods into India ... 2 5Delay in utilization of advance receivedfor Exports .................................................. 2 5Risk Management and Inter BankDealings: Foreign Currency (FCY) –INR Swaps .................................................... 2 6Foreign Investment in India byForeign Portfolio Investors ..................... 2 6Human Resources:Project – Gratuity Automation:Payment of Gratuity in HRMS ................ 2 7Gene r al :Gold Banking – Import of Gold:Review / Restart of Gold BankingActivities ...................................................... 2 7Guidelines on Import of Gold byNominated Banks/Agencies ...................... 2 8

Recent Banking Developments-Mar’15P B Business:Personal Banking Advances ................. 2 9Real Estate, Habitat &Housing Development ............................ 2 9SBI Scholar Loan Scheme ................. 30Central Government Salary Package(CGSP) ................................................... 31Agri Business:Financial Inclusion:Business Correspondents (BCs) ..... 32Interest subvention scheme .............. 32Educational Loan Scheme:Obtaining Aadhaar details ofborrowers ............................................... 33Pradhan Mantri Jan-Dhan Yojana(PMJDY) ................................................. 34Agri Business-SBI Special OTS forTractor Loans 2014 -15 ..................... 36SME Business:SMECCC has bee renamed asSME Centre ............................................. 39C & I Business:Lending under Consortium /

Multiple Banking Arrangement .........3 9Advances:Metal Gold Loan (MGL) andSale of Gold ..............................................4 0Foreign Exchange:Acquisition / transfer ofimmovable property ..............................4 1NRI Services .............................................4 1Mandatory use of StructuredFinancial Messaging System(SFMS) .......................................................4 3Human Resources:Payment of Family Pension ................4 3General:Western Union Remittances ................4 4PPF A/C: ..................................................4 4Service Tax ................................................4 4

Recent Banking Developments-April’15P B Business:Providing key fact statement topersonal and education loanborrowers ....................................................4 5Car Loans ...................................................4 5Home Loan above Rs.10 lacs ................4 5Campaign for opening of savingsbank accounts with non-personalisedwelcome kits ..............................................4 5SME Business:. ......................................4 6Rice Mill Plus .............................................4 7Loans without CGTMSE cover .............4 7Agri Business:Interest Subvention Scheme (ISS) .........4 8Mandatory use of ‘AGRI LOS’ ..............4 8RuPay (DEBIT) card to FIcustomers ....................................................4 8Financial Inclusion ...................................4 9Advances:Non-Cooperative Borrowers ..................4 9Modification in Provisioning norms ...5 0Collection and Dissemination ofInformation on Wilful Defaulters .........5 1Online Loan against shares ....................5 2Follow up of Loan Accounts ..................5 5Foreign Exchange:Risk Management and Inter-bankDealings ......................................................5 5KYC Documents for opening of NRE /NRO / FCNR (B) and RFC Accounts ....5 6Export of Goods and Services –

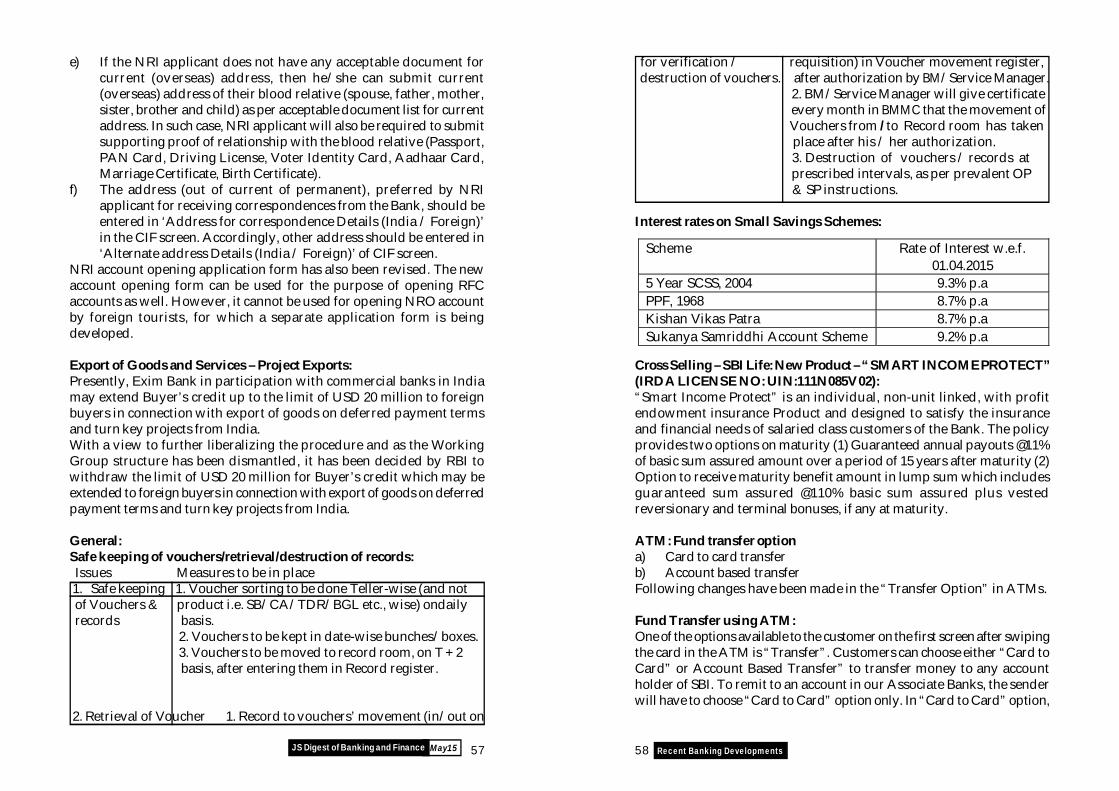

Project Exports ........................................5 7Gene r al :Safe keeping of vouchers/retrieval/destruction of records .............5 7Cross Selling – SBI Life: .........................5 8Fund Transfer using ATM .......................5 8Time of Credit ...........................................5 9Solvency Certificate ................................5 9RFIA / Credit Audit ...................................5 9Composite Rating Introduced ................6 0

Recent Banking Developments-April and May’15Human Resources:Mandatory Leave for Employees .........6 2Forex:Merchanting Trade to Nepal andBhutan Foreign Currency(Non-Resident) Account .........................6 2Foreign Currency(Non-Resident)Account (Banks)(FCNR(B)) Scheme ...6 3Deposits:Rights of transgender persons ................6 4Advances:Loan frauds in banks ................................6 5Early Warning Signals (EWS) andRed Flagged Accounts (RFA) ..................6 5Technology:Security and Risk mitigation Measuresfor Card Present and ElectronicPayment Transactions ............................6 7Gene r al :Dispension with ‘No Due Certificate’(NDC) for lending by Banks ..................6 7Simplified procedure for openingof Currency Chests ...................................6 8Calendar of Reviews .................................6 9Critical themes in board deliberations ..6 9Card Payments - Relaxation ..................7 0Mandatory issue of acknowledgementto Pensioners .............................................7 1

CONCEPT BRIEF - IndianEconomy Roundup – May 2015 ...........7 2MODEL TEST (BASED ON MAY2015 INFORMATION) .........................7 6PRIORITY SECTORADVANCES (Changes–April2015) Model Test – II ............................7 8Model Test-I (for STP aspirants)(MM II Confirmation Exam) ..............9 2SBI Results (2014-15) ......................... 121

65 Contents

JS Digest of Banking and Finance May15

BANKING & FINANCE–May 2015

SBI: Rupay Platinum Debit Card: SBI has launched a Rupay

Platinum debit card along with National Payment Corporationof India (NPCI). This card may be used at ATMs and Point ofSale (PoS) or merchant terminals as well as for e-commercetransactions. It also offers other benefits like 5% cash back onutility bills, complimentary airport lounge access, personalaccident death and permanent total disability insurance coverof Rs.2 lakh.

Deals with E-Commerce Companies: SBI has signed an MoUwith American e-commerce company Amazon to offer paymentsolutions to its customers. It has also tied up with India’s e-commerce company Snapdeal to enable sellers on the site to getassistance in raising collateral-free loans with favourable interestrates. Snapdeal’s data analytics will also help it gauge thecreditworthiness of sellers. It has also entered a pact withAmerican online payment system company PayPal to facilitateinternational trade and overseas funding for the GOI’s initiativeslike Swachh Bharat and Clean Ganga. Customers will also haveaccess to PayPal’s secure payment solutions as well as be able touse it to make payments for purchases made from overseaswebsites.

New Cards: SBI has launched two new cards – SBI INTOUCHcontactless Debit Card and SBI Signature Contactless Credit Card.Contactless cards use Near Field Communication (NFC)technology; customers may make payments by merely wavingthe card near the contactless reader. Since the card does not haveto be swiped, it is more secure.

Online Overdraft Facility: SBI has started an online overdraftfacility against fixed deposits (FD), wherein customers can availof an overdraft against fixed deposits, held in a single name, upto 90% of the FD amount. Special interest rate for the introductoryperiod: 0.5% above the TDR rate.

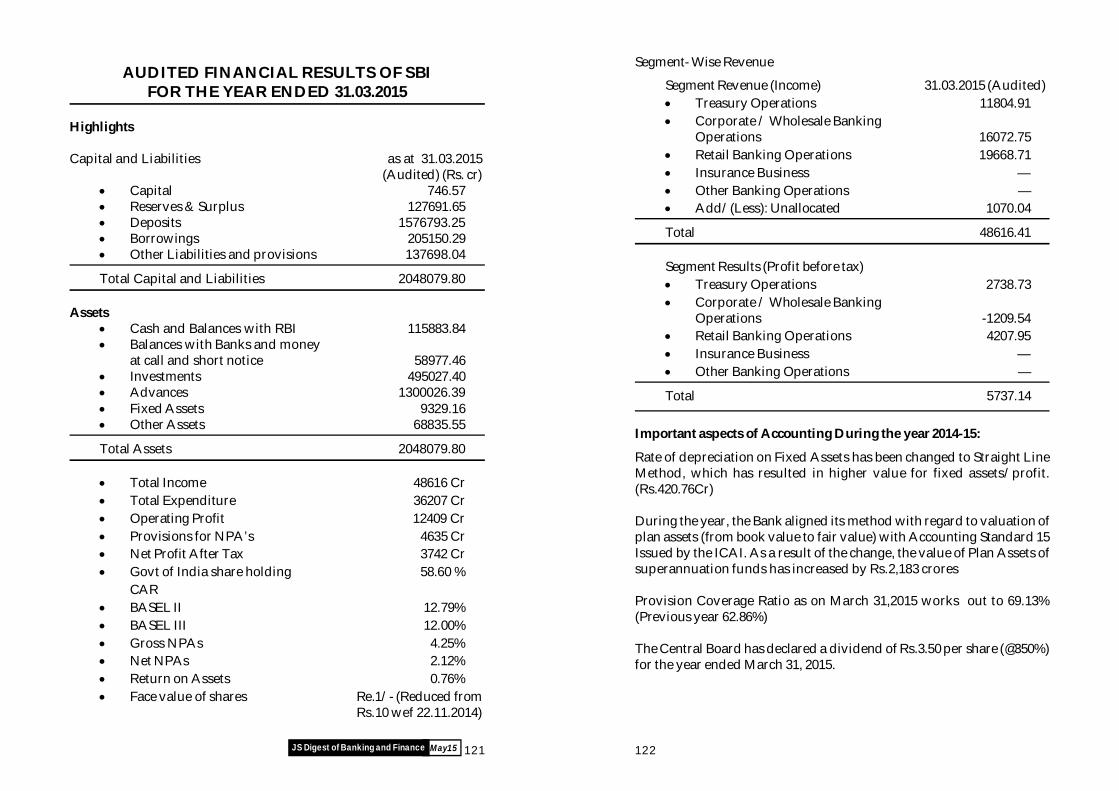

Results: State Bank of India (SBI)’s net profit for the year endedMar’15 increased by 23% to Rs.3,742 crore as compared to theprevious year. Gross Non-Performing Assets (GNPAs) were4.25%, down from 4.95% in the previous year while Net Non-Performing Assets (NNPA) reduced from 2.57% to 2.12%. It hasrestructured advances of Rs.71,229 crore in total.

RBI: 3 Banks Penalised: RBI has fined Dena Bank, Bank of

Maharashtra and Oriental Bank of Commerce (OBC) Rs.1.5 croreeach for not complying with regulatory guidelines that led to thefixed deposits fraud case. Fraudsters forged Fixed Deposit receiptsof these banks and availed of cash credit based on those receipts.Further, the central bank has cautioned some other banks namelyCentral Bank of India, Bank of India, Punjab and Sind Bank,Punjab National Bank, State Bank of Bikaner & Jaipur, UCO Bank,Union Bank of India and Vijaya Bank, in this regard.

Liberalised Branch Authorisation Policy: As part of its policystance to relax norms for opening branches, RBI has now statedthat banks need not report disputes in relation to leased premiseson a periodic basis. But they must ensure that the leased premisesare not illegal. Also, commercial banks except Regional RuralBanks (RRBs) need not seek RBI’s approval each time they openbranches anywhere in the country.

NBFCs Selling MFs: RBI has allowed all Non-Banking FinanceCompanies (NBFCs) to sell Mutual Funds (MFs) – there are nominimum eligibility criteria or approvals required from the apexbank. Earlier, NBFCs needed to have net owned funds of Rs.100crore and less than 3% net bad loans.

Funds for Start-ups: RBI has allocated Rs.10,000 crore to SmallIndustries Development Bank of India (SIDBI) to set up a VentureCapital (VC) fund. This is to attract private capital for start-upsby making available equity and other forms of risk capital.

AFA Relaxed for Small Value Transactions: To increasecustomer convenience, RBI has done away with the AdditionalFactor of Authentication (AFA) for small value card presenttransactions – i.e. of value lesser than Rs.2,000 across allmerchant categories. Banks may decide how often customerscan undertake such transactions. RBI has also stated that fromSeptember 2015, all banks must issue only Europay MasterCardVisa (EMV) chip – or PIN-enabled credit and debit cards to reducethe chance of fraud. RBI has also asked banks to put in placeearly warning systems for accounts over Rs.50 crore. Accountsthat have suspicious activity like bounced high value chequesor raid by tax officials may become Red Flagged Accounts (RFA).Banks are required to make full provision for the amount of thefraud once detected.

Resolution Period for Stressed Assets: RBI has extended theresolution period for Asset Reconstruction Companies (ARCs)

87 Banking & Finance

JS Digest of Banking and Finance May15

to restructure stressed assets to beyond 8 years. Internal Ombudsman: RBI has directed all Public Sector Banks

(PSBs) and some private and foreign banks, based on their assetsize and business mix (ICICI Bank Ltd., HDFC Bank Ltd., AxisBank Ltd., Kotak Mahindra Bank Ltd., IndusInd Bank Ltd.,Standard Chartered Bank, Citi Bank N.A. and HSBC Ltd.) toappoint an internal ombudsman – a Chief Customer ServiceOfficer (CCSO). This is to ensure that customers’ grievances aregiven due priority and attention.

RBI on FDI Inflows: RBI has issued a clarification that ForeignDirect Investment (FDI) inflow does not require its approval atany stage. FDI may flow into an Indian company through theautomatic route and the approval route. In the former, noapproval is required for FDI inflow while the approval of theForeign Investment Promotion Board (FIPB) is required in thelatter.

Swap Transactions: To enable foreign lenders to lend in Rupeesto Indian entities, RBI has allowed them to enter into swaptransactions with their overseas banks; these banks will thenenter into back-to-back swap transactions with Indian banks.

Resilience against Outflows: RBI Governor Raghuram Rajanhas expressed confidence in India’s ability to withstand suddencapital outflow because of its improved economic fundamentalslike foreign exchange reserves (US$ 353.87 billion as of May 152015) and Current Account Deficit (CAD).

Trade Transaction Limit: RBI has increased the tradetransactions limit under the Rupee Drawing Agreement fromRs.5 lakh to Rs.15 lakh per transaction.

Banking/Other Banks:Micro ATMs Withdrawal Limits: Banks have fixed thewithdrawal limit for micro ATMs at Rs.10,000. Up to Rs.2,000,there will be an interchange fee of Rs.2 per financial transactionwhile between Rs.5,000 and Rs.10,000, it will increase to Rs.15per transaction. Non-financial transactions will not be charged.Switching fees have been exempted till December 2015. A microATM is a hand-held device that Business Correspondents (BCs)use to accept deposits and dispense cash. They are less expensivethan ordinary ATMs. Of the 124,000 micro ATMs in the market,54,000 are Aadhaar-enabled and 8,000 Rupay card-enabled.Panel for Selecting Chairmen in PSBs: The Government hasappointed RBI Governor Raghuram Rajan as the head of a new

panel that will select non-executive Chairmen in Public SectorBanks (PSBs); the panel will set rules regarding eligibility criteriaand age limits.Ping Pay: Axis Bank’s mobile-based application Ping Pay willenable customers to make payments using different platformssuch as WhatsApp, Facebook, Twitter, email and SMS.Switching Fee: The National Payments Corporation of India(NPCI) has reduced the switching fee by 10% to 45 paise forATM transactions effective May 1, 2015.Insurance Schemes of Government: Central Bank of India (CBI)has signed an MoU with The New India Assurance Co. Ltd. tooffer the Pradhan Mantri Suraksha Bima Yojana (PMSBY). Thiswas announced in the Union Budget 2015-16.Chequebook App: ICICI Bank has launched ‘eftCheque’ mobileapplication. This will help customers, who are not conversantwith electronic modes of payment, transfer funds to beneficiarieswhose bank details are not required. The app replicates the lookand feel of a cheque.HDFC Bank’s SmartBuy: HDFC Bank plans to allow customersto buy products like groceries, clothes and other retail goodsthrough a platform called SmartBuy; customers will get discountsand facilities as a one-stop shop. This is to earn fee income bypartnering with various e-tailers to offer these products andservices.ATM Transactions Decline: According to the Confederation ofATM Industry (CATMI), the number of average daily ATMtransactions have declined from 137 to 108 between December2012 and December 2014. In this period, the number of ATMswent up from 1.05 lakhs to 1.76 lakhs and the number of debitcards also increased from 314.4 million to 500 million. The declinehas been attributed to the limited number of free transactions inATMs as well as the Direct Benefit Transfer (DBT) scheme nottaking off as anticipated.Credit Cards: The number of outstanding credit cards at the endof December was 20.29 million, according to data from RBI.SC Notice for Hiring of Top Executives in PSBs: The SupremeCourt has issued a notice to the Union Government based on aPublic Interest petition that claims that the top posts in PublicSector Banks (PSBs) must be filled from the pool of executivesserving in the banks rather than from other private banks. TheGovernment had issued an advertisement seeking candidatesfor the posts of Managing Director (MD) and Chief Executive

109 Banking & Finance

JS Digest of Banking and Finance May15

Officer (CEO) of Bank of Baroda (BoB), Bank of India (BoI), CanaraBank, IDBI Bank and Punjab National Bank (PNB). The petitionhas stated that seeking candidates from outside is againstbanking regulations.Voice Recognition Software: ICICI Bank has introduced a voicerecognition software at its call centres. Customers no longer needto validate their identities by typing in their card numbers orPINs as the technology will recognise their voice and authenticatethem; this is for the special convenience of those who use smartphones.

Finance, SE: LIC’s Market Share: The market share of Life Insurance

Corporation of India (LIC), in terms of first-year premium income,has reduced to 69.21% from 75% as a result of new regulationswherein it had to stop selling ULIP products.

Gold Monetisation Scheme: The Government has released adraft gold monetisation scheme. This seeks to optimally utilisethe idle gold reserves held by banks. Some of the proposalsinclude:o Interest earned on gold deposits will be exempted from all forms of taxation.o The minimum gold that can be deposited in gold schemes will be 30 grams, down from 500 grams.o Interest to the depositors will be valued in gold. Depositors may also receive the maturity amount in gold.o Banks may use the deposited gold for lending to jewellers, selling to customers and generating foreign currency.o There will be 350 hallmarking centres that will test the purity of the gold. These centres will also issue purity and weight certificates.

Insurance Policies in Rural Sectors: The Insurance RegulatoryDevelopment Authority of India (IRDAI) has stated that insurersmust increase the number of policies sold to rural sectors. As perrecently released draft guidelines, life insurers have to ensurethat they sell:

7% of the total policies written direct to rural areas inthe first financial year,

9% in the second financial year, 12% in the 3rd year 14% in the 4th year 16% in the 5th year

18% in the 6th and 7th year 19% in the 8th and 9th year 20% between the 10th to the 15th years and 25% from the 16th financial year onwards

General insurers have to ensure that they sell: 2% of the total gross premium income written direct in

the 1st financial year 3% in the 2nd year 5% between the 3rd and 7th years 6% in the 8th year 7% in the 9th year.

The rural obligations of stand-alone health insurers is half of thegeneral insurers’ obligations. In the social sector, for all insurersthe rural obligation begins at 0.5% in the 1st year and goes up to5% from the 19th year onwards. It is a percentage of the totalbusiness in the preceding financial year.

2-Wheeler Insurance: The Insurance Regulatory DevelopmentAuthority (IRDA) has stated that almost 75% of two-wheelers inIndia do not have insurance. The Supreme Court has set up acommittee on road safety to make a report with methods to identifythese vehicles in 3 months.

Privatisation of ITDC Hotels: The GOI has plans to privatisehalf of the 16 India Tourism Development Corporation (ITDC)hotels that are not performing well. This is part of the GOI’splans to offload sick units.

Insurance Schemes: The Union Budget had announced 2insurance schemes to provide social security to all Indians. Thisis valid for the period between June 1 2015 and May 31 2016 andhas to be renewed annually. Customers need not get a medicalcheck-up done.

PMJBY (Pradhan Mantri Jeevan Jyoti Bima Yojana) - Thisprovides a life insurance cover of Rs.2 lakh for an annualpremium of Rs.330 for those between 18 and 50 years ofage.

PMSBY (Pradhan Mantri Suraksha Bima Yojana) - Thisprovides an accident insurance cover of Rs.2 lakh for anannual premium of Rs.12/- for those between 18 and 70years of age.

Corporates:o Capgemini’s Acquisition of iGate: France-based software

company Capgemini has acquired US-based software company

1211 Banking & Finance

JS Digest of Banking and Finance May15

iGate for US$ 4 billion. Its employee base will increase to 90,000post acquisition.

o Future-Bharti Pact: Future Retail and Bharti Retail have decidedto merge their operations; the joint venture will have a turnoverof Rs.15,000 crore with 570 stores in 243 cities.

o Investment in India: US automobile company Ford Motors plansto invest Rs.5,000 crore in its R&D centre in Chennai.

o Nestle’s Maggi Unsafe: Authorities in Uttar Pradesh havedetected a higher- than-permissible limit of lead and monosodiumglutamate in Nestle’s Maggie noodles. While furtherinvestigations are underway, Nestle has refuted the claims thatits product is unsafe for consumption.

Economy: Divestment: The Cabinet has approved a 10% stake sale for

Indian Oil and 5% sale for National Thermal Power Corporation(NTPC) and expects to garner an aggregate revenue of overRs.13,500 crore.

Growth Forecast: A UN World Economic Situation and Prospects(WESP) update expects India to grow by 7.6% in 2015 and 7.7%in 2016; it expects China to grow by 7% in 2015 and 6.8% in2016.

Bad Loans: According to data from RBI, there has been an increaseof 90% in the restructured loans that have been classified asfailed to Rs.56,995 crore as of March 31 2015 compared to theyear-ago period. The total value of restructured loans as of March31 2015 was Rs.2.86 lakh crore.

Table of Key Statistics:CRR 4%SLR 21.5%REPO 7.5%REVERSE REPO 6.5%MSF 8.5%BANK RATE 8.5%INFLATION (WPI)* -2.65%FDI** US$ 28.81 bnFII *** (into equity) US$ 17.2 bnSENSEX@ 27564NIFTY@ 8334RS/$@ 64.01GOLD/10 g@ 26,875

SILVER/kg @ 38,320Forex Reserves# US$ 353.87 bnCurrent Account Deficit asa % of GDP^ 1.6Industrial Output^^ 2.1%

* April 2015** April 2014 to February 2015*** FY 2014-15 up to mid-March 2015@ As on May 27 2015# As on May 15 2015^ October-December 2014^^ March 2015

National: Salman Khan Convicted: Hindi film actor and producer Salman

Khan has been convicted for culpable homicide not amountingto murder for driving under the influence of alcohol and killing1 person and injuring 4 others in 2002. He has received a sentenceof 5 years Rigorous Imprisonment (RI). Currently, he is out onbail pending appeal.

India’s Largest Power Plant: National Thermal PowerCorporation (NTPC) plans to set up a power plant withJharkhand State Electricity Board with a generation capacity of6,400 megawatt (mw) annually. This will be India’s largest powerplant.

Earthquake in Andaman: An earthquake measuring 5.4 on theRichter scale hit Andaman and Nicobar Islands without anycasualties.

Social Security Schemes: Prime Minister Narendra Modi haslaunched 3 social security schemes - Pradhan Mantri SurakshaBima Yojana (PMSBY), Pradhan Mantri Jeevan Jyoti Bima Yojana(PMJJBY) and Atal Pension Yojana (APY) with the objective ofproviding social security protection, insurance cover and oldage income needs to all. He said that in the week since its launch,55 million people have been covered by these schemes.

MoUs in Chhattisgarh: On a visit to Chhattisgarh, PM NarendraModi signed 4 MoUs for infrastructure development in the stateannouncing investments worth Rs.24,000 crore includingRs.18,000 crore for a steel plant. Chhattisgarh has been besetwith Naxalite issues - Naxalites held 300 farmers hostage duringPM’s visit but released them later; however, one person was killed.

1413 Banking & Finance

JS Digest of Banking and Finance May15

SC on Photos of Politicians: The Supreme Court (SC) has statedthat the photos of politicians must not be used in mediaadvertisements connecting them to Government policy with theexception of those of the Prime Minister, President and the ChiefJustice of India.

Black Money Bill: The Parliament has passed the Black Money(Undisclosed Foreign Income and Assets) and Imposition of TaxBill, 2015.o The Government has opened a compliance window for

offenders with undeclared taxable income to come forwardand state their overseas assets/income and pay tax pluspenalty of 60%.

o This will be applicable to residents and not non-residentsand professionals working abroad; it is meant to unearthforeign assets of residents.

o In 2017, the automatic global information exchange will come into effect.o Those with amounts equivalent to Rs.5 lakh in bank accounts abroad will not be targeted as they could be students.o The penalty for non-disclosure will be 120% tax plus penalty and 10 years imprisonment.

Urea Policy: The Cabinet has passed a new urea policy effectivefrom 2015-16 for 4 years; this will incentivise domesticmanufacturers based on their annual consumption of energyand allow free transportation of phosphorous and potassiumfertilisers.

Credit to Mongolia: India has extended a line of credit of US$ 1billion to Mongolia for infrastructure development. Indian PrimeMinister Narendra Modi was on a 2-day visit there.

Farmer Suicide: Gajendra, a farmer committed suicide at an AAPrally allegedly to protest against the Land Bill – he was unable tomeet loans due to a failed crop season caused by unseasonalrains. His death became a political hot potato as the ChiefMinister of Delhi and AAP’s head, Arvind Kejriwal even issuedan apology for continuing with his rally after the unfortunateevent occurred.

Cabinet clears Land Boundary Bill – The Cabinet has passedthe Land Boundary Bill that covers area that will be transferredto Bangladesh from the states of Assam, Tripura and West Bengaland vice versa.

Lok Sabha Clears GST Bill: The Goods and Services Tax (GST)

Bill has been passed by the Lok Sabha. Needs to go through theRajya Sabha.

Tamil Nadu’s Chief Minister: Tamil Nadu’s former ChiefMinister J Jayalalithaa has replaced O Panneerselvam as CMafter the Karnataka High Court found her not guilty of possessingassets disproportionate to her income. The case has been in courtfor 19 years. She had resigned her post as CM 7 months ago, aftera Bengaluru special court convicted and sentenced her to 4 yearsin prison and fined her Rs.100 crore.

Raju Out on Bail: Satyam’s Ramalinga Raju and 9 others are outof prison on bail as his 7-year sentence has been suspended.They were convicted and sentenced for manipulating Satyam’sbooks of accounts to the tune of Rs.7,000 crore.

Proposed GST Council: The Union Finance Minister, Arun Jaitleywill be the Chairman of the Goods and Services Tax (GST)Council. The other members will include the Union Minister ofState for Finance and other state finance ministers or tax ministersnominated by the states. The Council will take calls on tax rates,exemption and threshold limits. According to the proposed GSTcouncil, the Centre will have one-third voting rights while thestates will have two-thirds voting rights. Regardless of their size,all states will have an equal vote. Any proposal needs 75% votesto be passed.

Elections in Bihar: Bihar will have assembly elections inSeptember-October 2015, according to Chief ElectionCommissioner (CEC) Nasim Zaidi.

Environmental Clearance for Mining Auctions: The Centre hasstated that states need not get environmental clearance beforethey auction mining projects. States had argued that the CentralGovernment or the mining company must obtain these clearances.It is still not clear as to who will be responsible for obtainingthese clearances.

Pollution Violations: A 5-star hotel in Haridwar, Radisson Bluhas been closed for not conforming to rules as set by the NationalGreen Tribunal; it has allegedly released untreated sewage waterinto the Ganga.

Heat Wave in AP, Telangana: The severe heat wave in AndhraPradesh (AP) and Telangana has led to the death of 500 peoplein a matter of days. Other cities across the country also registeredrecord high temperatures.

AAP-LG Conflict in Delhi: There has been a conflict regardingposting and transfer of bureaucrats in Delhi between the Delhi

1615 Banking & Finance

JS Digest of Banking and Finance May15

Government and the Lieutenant General (LG) Najeeb Jung. Bothparties have applied to the President seeking a resolution to theirclaims that they should have such powers. The Centre has issueda notification stating that the LG has the final powers.

International:Indian-Americans’ Median Income: According to the US CensusBureau, the median household income of Indian Americans isover US$ 100,000 as compared to the national median income ofUS$ 51,000 per annum. This is even higher than the medianincome of white, native-born Americans.UK PM: David Cameron has been re-elected as the Prime Minister(PM) of United Kingdom (UK). This is the first time a ConservativeGovernment has won a majority in 20 years. India-born PritiPatel has become minister of state for employment. ConservativeParty Member of Parliament (MP), British-Indian Rishi Sunak,son-in-law of Infosys co-founder Narayana Murthy, also wonfrom his constituency.ADB Loan for Water Resource management: AsianDevelopment Bank (ADB) has given a loan of US$ 31 million toKarnataka to enhance water availability in its river basins andimprove irrigation.Human Capital Index: India has been ranked 100 out of 124nations in the Human Capital Index compiled by the WorldEconomic Forum (WEF). Finland was ranked first. The indexmeasures how well human capital is developed and deployed.Pakistan Helicopter Crash: A military helicopter in Pakistanwas allegedly shot down by the Taliban. 2 foreign ambassadorswere among the 7 that died.Sentence for Malala Attack: 10 persons, held responsible forattacking Pakistani Nobel Peace prize awardee MalalaYousafzai, have been sentenced to life imprisonment by aPakistan court.India-Japan Pact: India and Japan have signed an agreement todouble Japan’s investment in India over the next 5 years as wellas to boost bilateral trade. The investment is for developingtownships in India and for other projects in infrastructuredevelopment.Kazakhstan President: Nursultan Nazarbayev won theKazakhstan presidential elections.Disaster Losses: According to a report by the United NationsOffice for Disaster Risk Reduction, India loses US$ 9.8 billion

annually due to disasters occurring because more than 58% ofland in India is prone to earthquakes and 8.5% of land is proneto cyclones.Morsi’s Death Sentence: Egypt’s former President MohammedMorsi and over 100 others were sentenced to death for the massprison break uprising in 2011. He was the first freely-electedhead of state of Egypt. Morsi was ousted from power in 2013 bythe military. He has been succeeded by Abdel-Fattah el-Sisi, themilitary chief who also won the elections last year.Air Pollution: According to a report by the World HealthOrganisation (WHO), air pollution has led to 4 times more deathsin the last 10 years around the world. India and China accountedfor two-thirds of the 4.3 million deaths due to indoor air pollution- 1.5 million deaths were in China and 1.3 million in India.FT Top 50 Executive Education Schools: The Indian Institute ofManagement, Bangalore (IIMB) has been ranked 48th on theFinancial Times (FT) Executive Education 2-15 Top 50 schools;it is the only Indian business school on the list.Nepal Earthquake: Nepal’s Prime Minister (PM) Sushil Koiralahas estimated that the death toll from the 7.6 on the Richter scalestrong earthquake that hit the country may cross 10,000. Theofficial toll is at over 6,000. 22 Mount Everest climbers died whilemany others went missing; the toll in India rose to 62. Indiaextended its support airlifting the needy from Nepal during thistime. Another earthquake measuring 7.3 on the Richter scalestruck Nepal again – 76 people were killed while thousandswere injured. There was also an earthquake in Afghanistan thatadded to the aftershocks that India suffered.Banks Fined: 4 major global banks – US banks JPMorgan Chaseand Citigroup, British banks Barclays Plc and Royal Bank ofScotland (RBS) have pleaded guilty to US criminal charges ofmanipulating foreign exchange rates. They have, in all, been finedUS$ 5.7 billion. Swiss bank UBS is also expected to plead guiltyto similar charges.US Economy: The US economy grew by 0.2% in the January-March 2015 quarter; in the year-ago period, it contracted by 2.1%.In the December 2014 quarter, it grew by 2.2%.Japan’s Economy: Japan’s economy grew by 2.4% annualisedrate in the March 2015 quarter and by 0.6% Quarter-on-Quarter(QoQ); in the December 2014 quarter, it increased by 1.5% QoQ.Kazakhstan Elections: Nazarbayev has won the elections to

1817 Banking & Finance

JS Digest of Banking and Finance May15

continue his term as President of Kazakhstan; he has been inpower since 1989.Japan’s Plan for Asian Infrastructure: Japan will invest US$110 billion over the next 5 years in developing infrastructure inAsia. The Asian Infrastructure Investment Bank (AIIB), that has57 nations on board, is also expected to have a capital base ofUS$ 100 billion.

Technology: Motorola Patent Penalty: Motorola Mobility, a US mobile device

subsidiary of Chinese technology company Lenovo, has beenpenalised US$ 10.2 million by a US jury for using technology,patented by Japan’s Fujifilm Corp, in its phone.

Flipkart’s Acquisition of Appiterate: E-commerce companyFlipkart has acquired mobile engagement and marketingautomation company Appiterate to strengthen its mobileofferings.

Verizon’s Acquisition of AOL: US-based wireless providerVerizon Communications plans to acquire US mass mediacompany AOL for US$ 4.4 billion.

Cognizant Results: Cognizant Technology Solutions (CTS)’snet profits increased by 9.7% to US$ 382.9 million in the March2015 quarter as compared to the year-ago period.

Job Cuts: Engineering company Siemens plans to cut 4,500 jobsthis year. It has already announced that 7,400 jobs will be cut outof 340,000 employees worldwide.

Dates, Anniversaries:May 3 - World Laughter DayMay 9 - Victory Day - 70th Anniversary of victory over the NazisPersonalities:

o Dave Goldberg: The Chief Executive Officer (CEO) of poll-takingcompany SurveyMonkey has passed away after an accident at agymnasium. He was the husband of Facebook Chief OperatingOfficer (COO), Sheryl Sandberg.

o Alexandre Lamfalussy (86): One of the founding fathers of theEuro currency as a single currency for Europe has passed away.He was an economist and the first president of the EuropeanMonetary Institute, predecessor of the European Central Bank(ECB).

o Mrinal Datta Chaudhuri (82): The economist and former directorof the Delhi School of Economics has passed away; he was also

a visiting professor at the universities of Harvard and Minnesota.He was awarded Padma Bhushan in 2005 in the field of tradeand industry.

o John Nash (86): The Economics Nobel Prize winning Americanmathematician has passed away in a car crash. He won theNobel prize in 1994 for his various contributions to economicscience - game theory, Nash equilibrium and Nash embeddingtheorems. Oscar award-winning movie A Beautiful Mind wasbased on his life.

Sports: Boxing: American professional boxer, Floyd Mayweather beat

Filipino Manny Pacquiao in boxing’s most expensive fight takinghis record of unbeaten fights to 48. He has won 11 world titles sofar.

Tennis: India’s Rohan Bopanna and Romania’s Florin Mergeahave won the Madrid Open Men’s Doubles title, an ATP 1000Masters Series event.

Shooting: Indian shooter Gagan Narang won a bronze medal inthe ISSF World Cup in the US in the 50 m Rifle Prone Event. Withthis, he has earned a quota place in the 2016 Olympics to be heldin Rio de Janeiro.

Formula One: Nico Rosberg, of Germany, driving the Mercedeswon the 2015 Spanish and Monaco Grand Prix.

Cricket: Mumbai Indians beat Chennai Super Kings to becomethe champions of Indian Premier League (IPL) – 8.

Awards/Recognitions: Jnanpith Award: Marathi litterateur Bhalchandra Nemade

received the 50th Jnanpith Award for 2014. He has written bookssuch as Hindu and Kosala.

Appointments: BRICS Bank Chief: K V Kamath, Chairman of ICICI Bank, has

been appointed the first President of New Development Bank(NDB), the new bank of the BRICS (Brazil, Russia, India, Chinaand South Africa) nations.

Chief Statistician: T C A Anant’s term as the Chief Statisticianand principal secretary of the Ministry of Statistics andProgramme Implementation has been extended till January 2016.

2019 Banking & Finance

JS Digest of Banking and Finance May15

RECENT BANKING DEVELOPMENTS –Feb’ 2015

PB Business:Xpress Credit:Presently only employees of State / Central Govt-run schools/colleges,by virtue of being State/Central Govt. employees, are eligible for ExpressCredit Loans. The employees of Educational Institutions of NationalRepute (defined as Institutions covered under SBI Scholar Loan Scheme)are also eligible under the scheme.

The employees of reputed private schools and colleges are now includedunder Xpress Credit Loan Scheme on the undernoted terms andconditions:i) These Private Schools and Colleges should not be government aided.ii) They should be at least 15 years old and should be affiliated to

CBSE/ICSE/UGC/AICTE etc.iii) They must have 5 years of Banking Relationship with us.iv) The number of employees (teaching and non-teaching) of such

Institutes should not be less than 50.v) There should not be any default in contribution towards EPFO

pertaining to the employees.vi) The Xpress Credit Loans will be sanctioned and disbursed through

only one Branch where the Salary accounts of the employees aremaintained for proper monitoring and follow up.

Agri Business:Warehouse Receipt Financing with collateral Management services:Improvement in Margin, Collateral Security and Rate of Interest:Now, improvement in margin, collateral security and rate of interest hasbeen made when services of Collateral Managers are utilized for lending.Improvements are:i) Margin:Category Existing RevisedA 40% 25% Of the Market Value – Lower of

the:a) Current Market Price of thecommodityb) Price prevailing at the time of harvestof the commodity

B 40% 20% Of Minimum Support Price –Wherever declaredHigher of the A or B above.

ii) Collateral Security: No Collateral SecurityExisting RevisedUp to Rs.10 lac Up to Rs.50 lac

iii) Rate of Interest: For loans up to Rs.50 lac per farmer.

Tenure of loan Existing RevisedUp to 6 months 200 bps to 400 bps 50 bps above BR-

Above BR (Card Rate) Effective Rate: 10.50%Above 6 months 200 bps to 400 bps 75 bps above BR –& up to 1 year above BR (Card Rate) Effective 10.75%

Stipulations:i) The improvement in margin, collateral security and rate of interest

will be applicable only for the loans granted against warehousereceipts under Produce Marketing Loan scheme where stocks aremanaged by bank’s approved Collateral Managers.

ii) Important roles of Collateral Managers under the scheme are asunder:

- Do sampling, testing, grading, assaying and certification of thecommodities.

- Perform storage/preservation (like pest control, insurance,fidelity etc)

- Provide MIS on market-related value movement of thecommodities.

- Place requests for margin top-up to the borrowers in case of need.- Provide sale and settlement support in case of default in the

loan.- Facilitate periodical inspection and verification of the stock.

The margin, collateral security and rate of interest for loans grantedagainst warehouse receipts under Produce Marketing Loan scheme issuedby Private Warehouses remain unchanged.

Financing Agri Value Chain: New Scheme for Financing “FarmersProducer Companies (FPCs):‘Farmer Producer Company (FPC)’ is a legal entity established underSection-581 of the Companies Act, 1956. These companies wereestablished to overcome the constraints face by the small size of farmers’landholding to leverage collective strength and bargaining power toaccess financial and non-financial input, services and appropriate

2221 Recent Banking Developments

JS Digest of Banking and Finance May15

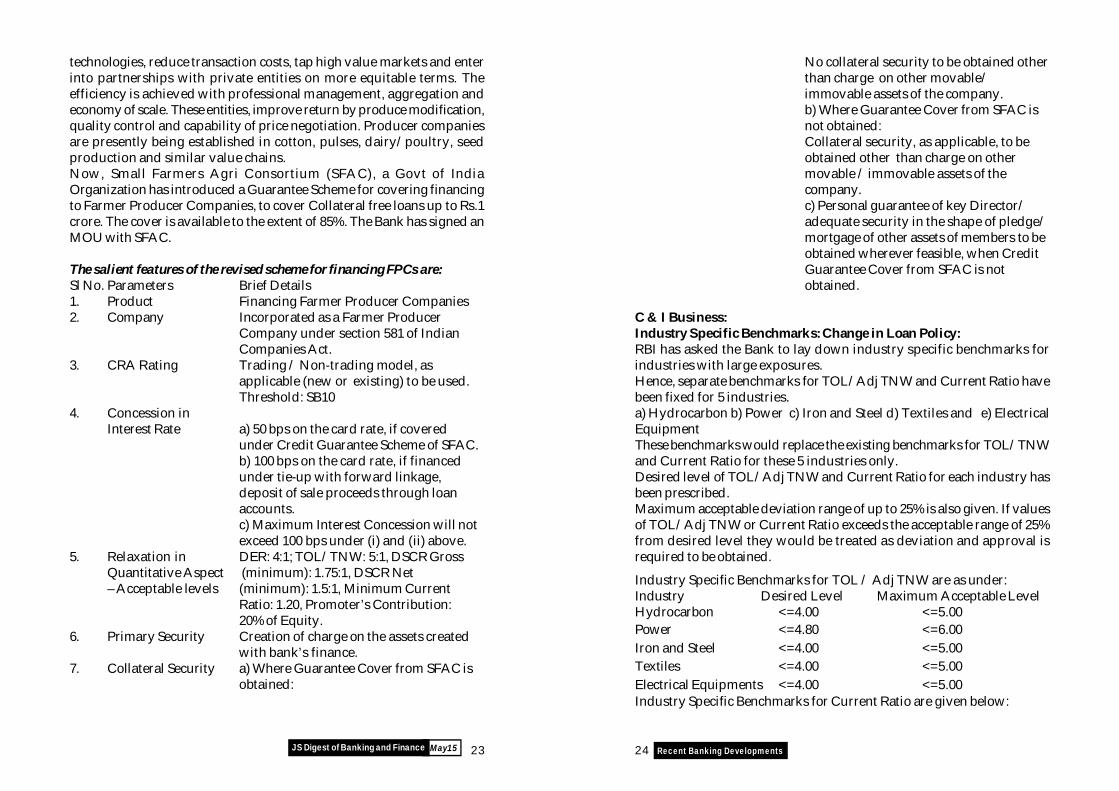

technologies, reduce transaction costs, tap high value markets and enterinto partnerships with private entities on more equitable terms. Theefficiency is achieved with professional management, aggregation andeconomy of scale. These entities, improve return by produce modification,quality control and capability of price negotiation. Producer companiesare presently being established in cotton, pulses, dairy/poultry, seedproduction and similar value chains.Now, Small Farmers Agri Consortium (SFAC), a Govt of IndiaOrganization has introduced a Guarantee Scheme for covering financingto Farmer Producer Companies, to cover Collateral free loans up to Rs.1crore. The cover is available to the extent of 85%. The Bank has signed anMOU with SFAC.

The salient features of the revised scheme for financing FPCs are:Sl No. Parameters Brief Details1. Product Financing Farmer Producer Companies2. Company Incorporated as a Farmer Producer

Company under section 581 of IndianCompanies Act.

3. CRA Rating Trading / Non-trading model, asapplicable (new or existing) to be used.Threshold: SB10

4. Concession inInterest Rate a) 50 bps on the card rate, if covered

under Credit Guarantee Scheme of SFAC.b) 100 bps on the card rate, if financedunder tie-up with forward linkage,deposit of sale proceeds through loanaccounts.c) Maximum Interest Concession will notexceed 100 bps under (i) and (ii) above.

5. Relaxation in DER: 4:1; TOL/TNW: 5:1, DSCR GrossQuantitative Aspect (minimum): 1.75:1, DSCR Net– Acceptable levels (minimum): 1.5:1, Minimum Current

Ratio: 1.20, Promoter’s Contribution:20% of Equity.

6. Primary Security Creation of charge on the assets createdwith bank’s finance.

7. Collateral Security a) Where Guarantee Cover from SFAC isobtained:

No collateral security to be obtained otherthan charge on other movable/immovable assets of the company.b) Where Guarantee Cover from SFAC isnot obtained:Collateral security, as applicable, to beobtained other than charge on othermovable / immovable assets of thecompany.c) Personal guarantee of key Director/adequate security in the shape of pledge/mortgage of other assets of members to beobtained wherever feasible, when CreditGuarantee Cover from SFAC is notobtained.

C & I Business:Industry Specific Benchmarks: Change in Loan Policy:RBI has asked the Bank to lay down industry specific benchmarks forindustries with large exposures.Hence, separate benchmarks for TOL/Adj TNW and Current Ratio havebeen fixed for 5 industries.a) Hydrocarbon b) Power c) Iron and Steel d) Textiles and e) ElectricalEquipmentThese benchmarks would replace the existing benchmarks for TOL/TNWand Current Ratio for these 5 industries only.Desired level of TOL/Adj TNW and Current Ratio for each industry hasbeen prescribed.Maximum acceptable deviation range of up to 25% is also given. If valuesof TOL/Adj TNW or Current Ratio exceeds the acceptable range of 25%from desired level they would be treated as deviation and approval isrequired to be obtained.

Industry Specific Benchmarks for TOL / Adj TNW are as under:Industry Desired Level Maximum Acceptable LevelHydrocarbon <=4.00 <=5.00Power <=4.80 <=6.00Iron and Steel <=4.00 <=5.00Textiles <=4.00 <=5.00Electrical Equipments <=4.00 <=5.00Industry Specific Benchmarks for Current Ratio are given below:

2423 Recent Banking Developments

JS Digest of Banking and Finance May15

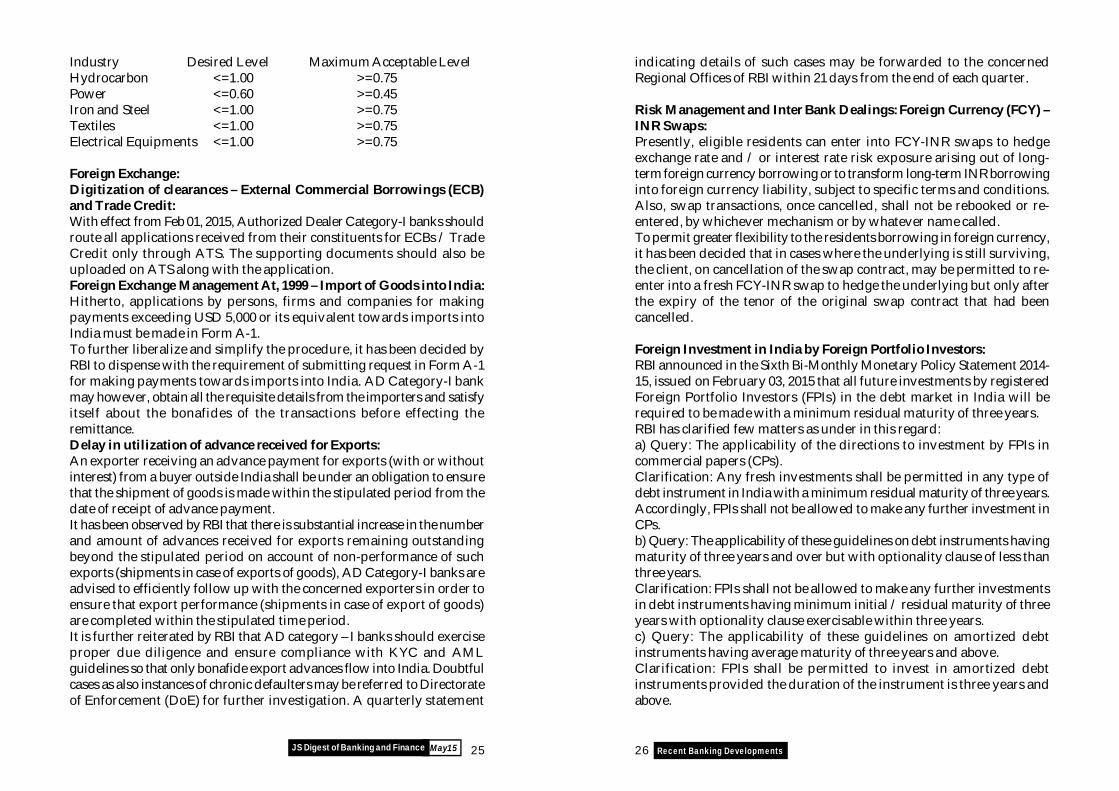

Industry Desired Level Maximum Acceptable LevelHydrocarbon <=1.00 >=0.75Power <=0.60 >=0.45Iron and Steel <=1.00 >=0.75Textiles <=1.00 >=0.75Electrical Equipments <=1.00 >=0.75

Foreign Exchange:Digitization of clearances – External Commercial Borrowings (ECB)and Trade Credit:With effect from Feb 01, 2015, Authorized Dealer Category-I banks shouldroute all applications received from their constituents for ECBs / TradeCredit only through ATS. The supporting documents should also beuploaded on ATS along with the application.Foreign Exchange Management At, 1999 – Import of Goods into India:Hitherto, applications by persons, firms and companies for makingpayments exceeding USD 5,000 or its equivalent towards imports intoIndia must be made in Form A-1.To further liberalize and simplify the procedure, it has been decided byRBI to dispense with the requirement of submitting request in Form A-1for making payments towards imports into India. AD Category-I bankmay however, obtain all the requisite details from the importers and satisfyitself about the bonafides of the transactions before effecting theremittance.Delay in utilization of advance received for Exports:An exporter receiving an advance payment for exports (with or withoutinterest) from a buyer outside India shall be under an obligation to ensurethat the shipment of goods is made within the stipulated period from thedate of receipt of advance payment.It has been observed by RBI that there is substantial increase in the numberand amount of advances received for exports remaining outstandingbeyond the stipulated period on account of non-performance of suchexports (shipments in case of exports of goods), AD Category-I banks areadvised to efficiently follow up with the concerned exporters in order toensure that export performance (shipments in case of export of goods)are completed within the stipulated time period.It is further reiterated by RBI that AD category – I banks should exerciseproper due diligence and ensure compliance with KYC and AMLguidelines so that only bonafide export advances flow into India. Doubtfulcases as also instances of chronic defaulters may be referred to Directorateof Enforcement (DoE) for further investigation. A quarterly statement

indicating details of such cases may be forwarded to the concernedRegional Offices of RBI within 21 days from the end of each quarter.

Risk Management and Inter Bank Dealings: Foreign Currency (FCY) –INR Swaps:Presently, eligible residents can enter into FCY-INR swaps to hedgeexchange rate and / or interest rate risk exposure arising out of long-term foreign currency borrowing or to transform long-term INR borrowinginto foreign currency liability, subject to specific terms and conditions.Also, swap transactions, once cancelled, shall not be rebooked or re-entered, by whichever mechanism or by whatever name called.To permit greater flexibility to the residents borrowing in foreign currency,it has been decided that in cases where the underlying is still surviving,the client, on cancellation of the swap contract, may be permitted to re-enter into a fresh FCY-INR swap to hedge the underlying but only afterthe expiry of the tenor of the original swap contract that had beencancelled.

Foreign Investment in India by Foreign Portfolio Investors:RBI announced in the Sixth Bi-Monthly Monetary Policy Statement 2014-15, issued on February 03, 2015 that all future investments by registeredForeign Portfolio Investors (FPIs) in the debt market in India will berequired to be made with a minimum residual maturity of three years.RBI has clarified few matters as under in this regard:a) Query: The applicability of the directions to investment by FPIs incommercial papers (CPs).Clarification: Any fresh investments shall be permitted in any type ofdebt instrument in India with a minimum residual maturity of three years.Accordingly, FPIs shall not be allowed to make any further investment inCPs.b) Query: The applicability of these guidelines on debt instruments havingmaturity of three years and over but with optionality clause of less thanthree years.Clarification: FPIs shall not be allowed to make any further investmentsin debt instruments having minimum initial / residual maturity of threeyears with optionality clause exercisable within three years.c) Query: The applicability of these guidelines on amortized debtinstruments having average maturity of three years and above.Clarification: FPIs shall be permitted to invest in amortized debtinstruments provided the duration of the instrument is three years andabove.

2625 Recent Banking Developments

JS Digest of Banking and Finance May15

Human Resources:Project – Gratuity Automation: Payment of Gratuity in HRMS:Application for Payment of Gratuity:Members/employees will apply for Payment of Gratuity in HRMS Portal.In case of Normal Retirement, they can apply three months prior to dateof retirement whereas in other cases i.e resignation, voluntary retirementetc., they can apply one month prior to date of separation, if their date ofseparation is marked in the HRMS system.In addition, there is a facility for Branch Head, Recommending authority/ designated (maker) official at LHO to apply on behalf of employeethrough Manger Self Service (MSS) (maker can apply from the linkavailable in ES), if employee is not able to apply through HRMS system.After submitting the application through HRMS Portal, applicant has totake the print of application and submit, duly signed and witnessed, tonext authority for recommendation / approval.On approval the intermediary account opened at CAO for the purposewill be debited on the next date of retirement/separation, or if alreadyretired/separated then next day of approval. Branch System SuspenseAccounts will be credited. The head of the Branch/OAD has to obtainnecessary documents viz stamped receipts etc before disbursement ofthe Gratuity amount by reversing the entry parked in System SuspenseAccount. The Branch/OAD officials can also generate Gratuity PaymentAdvice through HRMS Portal.

Based on the report generated through SAP, the designated Officer atCAO Kolkata will check the payments made during the day and zeroisethe intermediary account by reversing the entries and debiting the sameto Gratuity Trust Fund account.

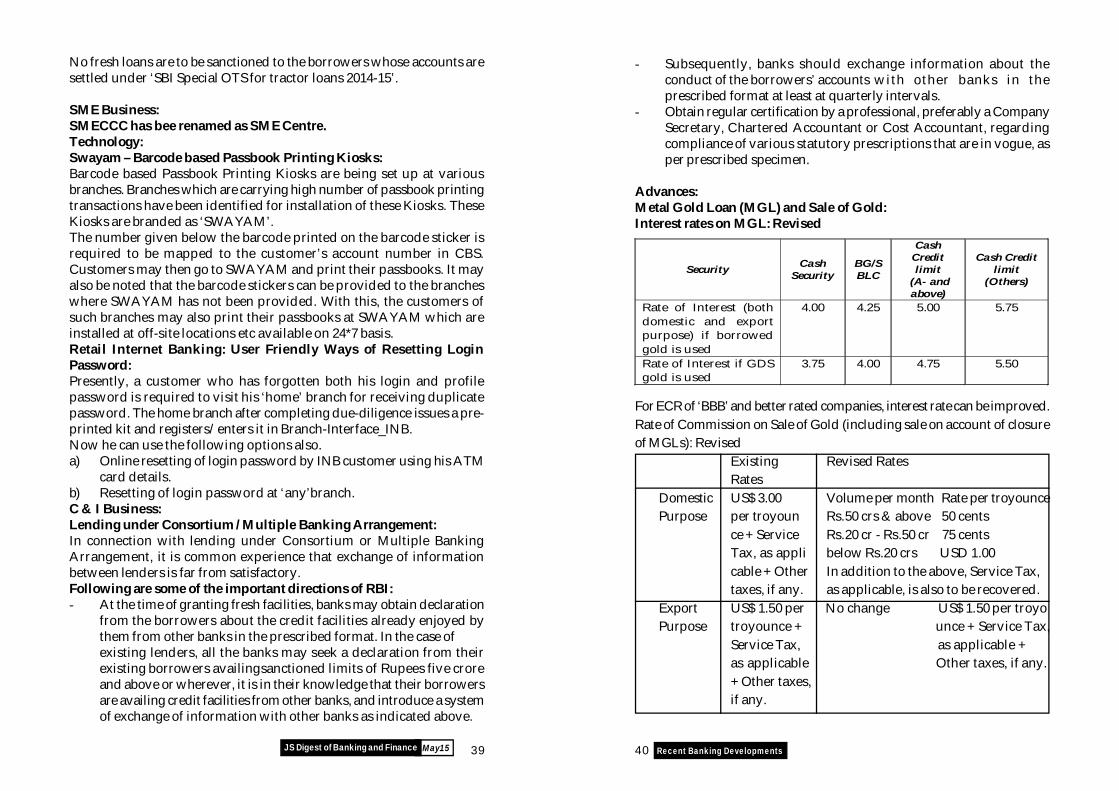

General:Gold Banking – Import of Gold: Review / Restart of Gold BankingActivities:Now, Designated Branches (DBs) can start activity of Sale of Gold(Wholesale) on outright basis to domestic jewellers and also grant MetalGold Loan to domestic jewellers from consignment gold stock.

RBI has issued clarificatios as under:a) Nominated banks are now permitted to import gold on consignmentbasis,b) All sale of gold domestically will be against upfront payment only,c) Banks are free to grant Metal Gold Loans,

d) The obligation to export under the 20:80 scheme will continue to applyin respect of unutilized gold imported before November 28,2014 i.e thedate of abolition of the 20:80 scheme.Indenting for import of gold by the DBs for the purpose of outright saleshould be on back to back basis only. Gold will be supplied to our DBsfor outright sale on the basis of firm commitment from their customersby depositing the money, equivalent to applicable customs duty, withthe branch at the time of indent. All sale of gold will be against upfrontpayment only.

Guidelines on Import of Gold by Nominated Banks/Agencies:RBI Clarifications:i) The obligation to export under the 20:80 scheme will continue to applyin respect of unutilized gold imported before November 28, 2014 i.e thedate of abolition of the 20:80 scheme.ii) Nominated banks are now permitted to import gold on consignmentbasis. All sale of gold domestically will, however, be against upfrontpayments. Banks are free to grant gold metal loans.iii) Star and Premier Trading House (STH/PTH) can import gold on DPbasis as per entitlement without any end use restrictions.iv) While the import of gold coins and medallions will no longer beprohibited, pending further review, the restrictions on banks in sellinggold coins and medallions are not being removed.

Rationale:1. BPR branches have to submit ECS mandate in respect of Auto Loans tothe concerned RACPC immediately on disbursement and not wait for themigration of document.R: Corporate Centre has observed that there is a strong correlation amongNPA, frauds, non-migration of auto loan documents and timely activationof ECS mandate at BPR branches. Prompt submission of ECS mandatewill enable RACPC to activate the mandate and follow up recovery.

2827 Recent Banking Developments

JS Digest of Banking and Finance May15

RECENT BANKING DEVELOPMENTS – Mar’ 2015

PB Business:Personal Banking Advances: Obtention of Report from CreditInformation Companies (CICs):Presently, operating units have to obtain Credit Information Report fromtwo of the four Credit Information Companies viz Credit InformationBureau (India) Limited (CIBIL), Equifax Credit Information Services PvtLtd (ECISPL), Experian Credit Information Company of India Ltd(ECICIPL) and Highmark Credit Information Services Pvt Ltd (HMCISPL)as follows:Particulars Report from one Report from two

Credit Bureau Credit BureausI) P Seg Secured Loans*Car Loans Limit upto Rs. 5 Lacs Limit > Rs. 5 LacsAll other Secured loans Limit upto Rs. 1 lac Limit > Rs. 5 lacs(including Education Loans,Two Wheeler & Super BikeLoans)II) P Seg unsecured LoansPersonal Loans Limit upto Rs. 1 Lac Limit > Rs. 1 LacEducation Loans Limit upto Rs. 4 Lacs Limit > Rs. 4 LacAll other Loans Limit upto Rs. 3 Lacs Limit > Rs. 3 Lac*Not applicable for Loans against Specified SecuritiesIn future CIC reports have to be obtained from the following two CICsonly for all the PBBU Segment for Loans above the threshold limitprescribed.i. Credit Information Bureau (India) Limited (CIBIL)ii Equifax Credit Information Services Pvt Ltd (ECISPL)It should be noted that CIBIL CIC report would be primary report andEquifax CIC report would be secondary report.

Real Estate, Habitat & Housing Development: Tab Banking: HomeLoan in Principle Approval (HLIPA):The maiden mobile client application has been designed and developedby GITC Belapur on Kony Mobile Application Development Platform(MADP). The features of the Application are as under: The Application will enable Field Staff to source a credit proposal

from a potential customer even when they are on move without theneed to carry and fill in any physical document.

The Application has been integrated with Lead management System(LMS).

Allows the field staff to access and process the leads assigned tohim or her by LMS. Also create a new lead of his own based onmarketing efforts / other channels.

Helps in meeting the potential Home Loan borrower on theirmarketing drive, collect the relevantdata, calculate the eligible loanamount based on all parameters and submit the application for inprinciple approval.

The application based on inputs, will also be sending email andSMS to the prospective customer informing his eligibility, rate ofinterest, EMI and other relevant details.

Through the application the Marketing executives are able to capturephotographs of the applicant, KYC documents, and geo locationsof the property along with its photographs.

The data captured through the application is integrated with LOSso that data up to QDE level in LOS could be captured and requiresno repetition.

The application will help in collecting the required documents andphotographs in one go and reduce the turnaround time in sourcingof Home Loan applications.

SBI: Scholar Loan Scheme:Hitherto, there were 3 types of Classification of eligible institutions: Now,reclassified into 4 groups (List AA, List A, List B and List C).List AA : 3 institutes - IIM Ahmedabad, ISB Hyderabad , ISB

Mohali.List A : 35 institutesList B : 12 institutesList C : 43 institutesTotal 93

Securities, Max Loan Amt:List Security Stipulated Maximum Loan AmountList AA without Tangible Collateral Rs. 30 lacsList A without Tangible Collateral Rs. 20 lacs

with Tangible Collateral Rs. 30 lacsList B without Tangible Collateral Rs. 20 lacsList C without Tangible Collateral Rs. 7.5 lacs

with Tangible Collateral Above Rs. 7.5 lacs & up to Rs. 30 lacsSome instructions have been excluded from the SBI Scholar Scheme; also,eligible Courses have been restricted in a few institutes. If loan cannot be

3029 Recent Banking Developments

JS Digest of Banking and Finance May15

taken up under the SBI Scholar Loan scheme, it may be considered underSBI Student Loan Scheme.Home Loans:Process for Online approval of Builder Tie-ups (OPAS)The extant process for according approval to residential projects underBank’s Builder Tie-up norm involves (i) approval of the Project by theApproving Authority and (ii) uploading of Project details, on Bank’sBuilder Tie-up site. This two stage approval process has been replacedwith a ‘Online Project Approval Solution’ (OPAS).

Personal Loans: modification in standing instructions in CBS forstanding instruction (S.I) between Deposit and Loan Account:The Recovery of EMIs in Personal Loans are generally done by setting upof Standing Instructions (S.I) between the Deposit (salary) and Loanaccount at the time of opening of the loan account. This is particularlytrue for Xpress Credit and Pension Loans.Now, “Hold Required” has been made mandatory i.e., there will be nooption of choosing Yes/No, whenever an SI is to be created for recoveryof EMI (Loan Servicing) between a Deposit and Loan account. Themandatory “Hold” will be applicable for both SI creation and amendmenttransaction; also the chase period has been increased from existing 30days to 32 days. The extra two days of chase will help the system toprocess at least two SIs, if these are not older then 32 days.

SI is to be set with the actual tentative date of salary payment. Theoperating units should also be advised to choose “100: Loan Servicing”as ‘Purpose of SI’ in the Screen No.SCR:000900 as this would be requiredto activate the above mentioned functionality of automatic Hold andchase period of 32 days in case SI is set up for recovery of EMIs fromDeposit A/c to Loan A/c.

Central Government Salary Package (CGSP) Inclusion of Employeesof Autonomous bodies / academics/councils etc. under union ministries,under CGSP:Currently, CGSP is restricted to employees of various Union ministriesand their departments, Election Commission, CBDT, CBEC. But there arehost of other establishments coming under Union Government whichare not included under CGSP. These include employees of Autonomousbodies, Academies, Institutions, Statutory Bodies, Commissions,Committees, Councils, like ESIC, AIIMS, AIR, IGNOU, IITs, IIMs, KendriyaVidhyalaya, Port Trust, Universities, CVCs, etc. Employees of these

establishments are having salary accounts with us, but are not coveredunder the structured package. Now, employees of autonomous bodiesetc are also eligible.Agri Business:Financial Inclusion: Business Correspondents (BCs): appointment ofnon-deposit taking NBFCs (NBFC-ND) as BC’s:The Reserve Bank of India has permitted Banks to appoint NBFCs (Non-Deposit taking) (NBFC-ND) as BCs.Eligibility Criteria:1. RBI registered NBFCs-ND with asset size of Rs. 50 crore and above

and considered by RBI as Systemically Important (NBFC-NDSI)shall be considered to be eligible for engagement as BCs.

2. Such NBFC-NDSI should not be defaulters with any bank and theloan account with the bankshould have remained as StandardAssets all through.

3. The names of NBFC-NDSI and /or any of its promoters / directors/trustees etc should not be in the CIBIL defaulter’s list.

4. The NBFC-NDSI should not have Negative Net Owned Fund (NOF).5. The NBFC-NDSI should have been in existence for at least 3 years.Financial Inclusion: Business Correspondent channel: Issue of barcodebased Pass Book to FI Customers:Hitherto, passbooks were issued to customers at BC channel only by thelink branch and in no case can a passbook be issued at the BC/CSPoutlet by the CSP operator.As FI a/cs have been increasing steadily and as the Govt has directedbanks to issue PBs to all FI Customers, it has been decided to issue barcodebased passbook to all FI customers maintaining balance in the account.Interest Subvention Scheme - 2014-15:Based on the GOI guidelines, RBI has advised Banks to continue theinterest subvention scheme @2% for the year 2014-15.Details:A-Interest Subvention at 2% to Banks:i) Interest subvention of 2% p a will be made available to PSBs and PrivateSector Scheduled Commercial Banks (in respect of loans given by theirrural and semi-urban branches) on their own funds used for short-termcrop loans up to Rs.3.00 lacs per farmer provided the lending institutionsmake available short term credit at the ground level at @ 7% p a to farmers.ii) 2% interest subvention will be calculated on the crop loan amountfrom the date of its disbursement / drawal up to the date of actualrepayment of the crop loan by the farmer or up to the due date of the loanfixed by the bank, whichever is earlier, subject to a maximum period ofone year.

3231 Recent Banking Developments

JS Digest of Banking and Finance May15

iii) The benefit of interest subvention will also be available to small andmarginal farmers having Kisan Credit Card for a further period of up tosix months post harvest on the same rate as available to crop loan againstnegotiable warehouse receipt for keeping their produce in warehouses.iv) To provide relief to farmers affected by natural calamities, the interestsubvention of two percent will continue to be available to banks for thefirst year on the restructured amount. Such restructured loans may attractnormal rate of interest from the second year onwards as per the policylaid down by the RBI.B-Additional Interest Subvention of 3% to prompt paying farmers:Additional interest subvention @ 3% p a will be available to the promptpaying farmers from the date of disbursement of the crop loan up to theactual date of repayment by farmers or up to the due date fixed by thebank for repayment of crop loan, whichever is earlier, subject to amaximum period of one year from the date of disbursement. This alsoimplies that the prompt paying famers would get short term crop loans @4% per annum during the year 2014-15. This benefit would not accrue tothose farmers who repay after one year of availing such loans.2. Interest Subvention Claim process: Interest subvention claims are to besubmitted in two stages in prescribed claim formats as under:- Unaudited half-yearly claim as at September 30, 2014.- Audited claim as at March 31, 2015.3. Restoration of normal lending rate after the end of subvention period:After expiry of the interest subvention period subject to a maximum periodof one year, normal lending rate has to be restored in these accounts toplug income leakage.Subvention details like subvention start date and subvention end dateare to be entered by the branches at the time of account opening for eligibleaccounts so that CBS can automatically restore the normal lending rateafter the expiry of the interest subvention period.This scheme is valid up to 31st March 2015.Education Loan Scheme: Obtaining Aadhaar details of borrowers:PAN card of the student and the Parent / Guardian was made a requireddocument for all new Education Loans w.e.f 18.02.2012.Now, CIBIL has introduced Aadhaar as one of the key identifiers inaddition to others based on which account details of the borrower will beaccepted in CIBIL database. Also, GOI has advised that Banks shouldendeavour to link loan/interest subsidy with Aadhaar Card for propertracking of students in the larger interest of all.Hence, Aadhaar details of the borrower should also be obtained whereveravailable, in addition to PAN and other identifiers prescribed by CIBIL.

However, no application will be rejected for mere want of Aadhaar detailsand the borrower will be advised to submit Aadhaar before the secondscheduled disbursement as being done hitherto in case of non-availabilityof PAN.In cases, where the borrower is not in possession of either PAN orAadhaar with him/her, obtaining Aadhaar details will be preferred asAadhaar is being used for administration of subsidies by the Govt. andis also a proof of identity and address anywhere in India. Moreover, it isbased on biometric system for identification of an individual and is morereliable.In cases, where the student has already submitted PAN, Aadhaar detailsshould also be obtained during the course of the study period.Pradhan Mantri Jan-Dhan Yojana (PMJDY):Claim Procedure for Life Insurance Cover of Rs.30,000/- provided byLIC.A life cover of Rs.30,000/- was announced by the PM for all those whosubscribe to a bank account for the fist time during the period 15th August,2014 to 26th January, 2015. The scheme aims to provide security to thosefamilies who cannot afford direct insurance, namely the urban poor andrural poor and who are not covered under social security scheme.The life cover of Rs.30,000/- will be payable on death of the accountholder due to any cause, subject to fulfillment of the eligibility conditionsas under:i) Person opening Bank account for the first time, with RuPay Card in

addition, during the period from 15-08-2014 to 26-01-2015.ii) The person should normally be head of the family or an earning

member of the family and should be in the age group of 18 to 59 (i.eperson should be at least 18 years old and should not havecompleted 60 years of age). In case the head of family is 60 years ormore of age, the second earning person of the family in the abovementioned age group will be covered, subject to eligibility.

iii) Person must have a RuPay Card and Bio-Metric Card (Aadhaar)linked to bank account or in process of being linked to bank accountif not already there.

iv) The account can be any bank account including a small account.v) For the coverage to be effective, the RuPay Card should be valid and

in force at the time of the death of the member.vi) Only one person in the family will be covered. In case of the person

having multiple cards/accounts the benefit will be allowed onlyunder one card i.e one person per family will get a single cover ofRs.30,000/-, subject to the eligibility conditions.

3433 Recent Banking Developments

JS Digest of Banking and Finance May15

vii) The life cover of Rs.30,000/- under the scheme will be initially for aperiod of 5 years, i.e till the close of financial year 2019-20. Thereafter,the scheme will be reviewed.

viii) In case the PMJDY Account is held jointly, the first account holderi.e primary account holder will be eligible for cover subject to theeligibility conditions.

Ineligible Categories:i) Central Govt and State Govt employees (in service or retired) and

their families.ii) Employees (in service or retired) of Public Sector Undertakings,

Public Sector Banks, any entity owned by Central Govt, any entityowned by a State Govt or any entity owned by the Central Govt andany State Govt and their families.

iii) Persons whose income is taxable under IT Act 1961 or are filing theyearly Income Tax return or in whose case TDS is being deductedfrom the income, and their families.

iv) Persons who are included in the AamAadmiBimaYojana covering48 occupations defined under the scheme and their families.

v) Otherwise eligible account holders, who have life cover on accountof any other scheme of the Bank against the account, shall have tochoose between the two schemes and derive benefit from only one.

vi) All persons who do not fulfill the basic eligibility conditions of thescheme.

Claim Settlement Procedure:a) The claim is payable to nominee(s) / legal heirs of the account

holder. The nominee will be the person having nomination in theBank account. In the absence of nominee or if the nominee pre-deceases the insured member or if the nominee is not spouse, childor parent, the legal heirs of account holder should submit IndemnityBond to dispense with legal evidence of title in the prescribed format.

b) The claim will be credited to Bank account of nominee/legal heirsthrough APBS i.e the amount will be credited to account linked toAadhaar Card number.

c) The branch maintaining account of deceased account holder willforward the claim along with requisite documents to nearestPension and Group Scheme Unit (P & GS unit) of LIC designated forthis purpose for processing of claims.

d) The documents to be attached with claim forms will be self-attestedby claimant/legal heirs. However, Death Certificate has to be dulyverified/attested by the bank.

SBI Asset Backed Loan (Commercial Real Estate) – (ABL-CRE):Changes in prepayment penalty:- In case of pre-payment / pre-closure from internal accruals pre-

payment / pre-closure penalty will not be levied.- As per RBI Circular no-RBI/2014-15/72, Floating rate term loans

sanctioned to individual borrowers are exempted from levy offoreclosure charges.

- 2% of the drawing power.

Agri Business – SBI Special OTS for tractor loans 2014-15.Frequently Asked Questions (FAQs):

Sl No

Queries Clarification / response

1. Under the same CIF, one account is Sub Standard and other accounts are doubtful or loss assets or in the same CIF different IRAC status exists. What is the rate of waivers to be allowed?

Generally, all accounts in single CIF should have the same asset classification. If for any reason IRAC status is not the same, the worst IRAC among all the accounts would be taken for the purpose of calculation of OTS amount. For example, if one account is under D1 category and other is in D2 asset category, then both the accounts should be taken as D2 for calculation of OTS amount. If the assets value of securities in the borrower’s accounts is less than 10% of outstanding, all facilities will be treated as loss assets.

2. Whether standard accounts of same borrower which became NPA due to ‘one account NPA all account NPA’ norms in CCDP can be covered.

Yes, Standard accounts of the same borrower will also be covered which became NPA due to ‘one account NPA all account NPA’ norms in CCDP, as IRAC classification is borrower wise and not account wise.

3. Date of disbursement in The related linked accounts

3635 Recent Banking Developments

JS Digest of Banking and Finance May15

3. Date of disbursement in case of tractor loans should be 31.03.2011 or before. What disbursement criteria is to be taken for related linked accounts in the same CIF?

The related linked accounts would be eligible even if sanctioned/disbursed after 31-03-2011, if they satisfy other eligibility criteria.

4. Same borrower is having multiple CIFs. Whether accounts opened in other CIF can be considered for OTS, if otherwise eligible.

Yes, if the accounts are in the same borrower’s name and capacity as of tractor loan NPA account.

5. In case a borrower having a tractor loan (NPA) and KCC (standard) though both the accounts are treated as NPAs as per IRAC norms (classification is borrower wise and not account wise) – whether it is necessary to close the KCC account though the account individually is standard. In case it is required to be closed whether any waiver can be given (say, in the accrued interest till the date of closure).

Generally, all accounts in single CIF should have the same asset classification as classification is borrower-wise and not account wise. Even through KCC is standard in CBS, it is NPA as per IRAC norms and may be considered eligible under the OTS. Waivers as applicable to tractor loan NPA account may be extended to KCC also. But both the accounts need to be closed.

6. In case a borrower is willing to settle the dues in tractor loan and want to continue the KCC as standard account. Whether the KCC account can be allowed to be continued?

No, as per the scheme, all accounts of the same borrower are to be settled concurrently under the OTS and need to be closed. As such the borrower has to close the KCC account also.

7. If there is shortfall in provision or sufficient provision is not available

Generally, provisions should be available as per IRAC status of account. The write off amount is

provision is not available for writing off the amount, what needs to be done?