Embed Size (px)

DESCRIPTION

Banco do Brasil 3Q08. 18.0. 17.8. 13.3. 11.3. 7.6. 5.7. 4.5. 3.1. Interest Rate Selic. Price Index - IPCA. Economic Environment. Ratio - %. 13.8. 11.2. 4.8. 3.0. 2004. 2005. 2006. 2007. 9M07. 9M08. Economic Environment. 383. 303. 304. 222. 192. 172. 206.5. - PowerPoint PPT Presentation

Citation preview

1

Banco do Brasil3Q08

2

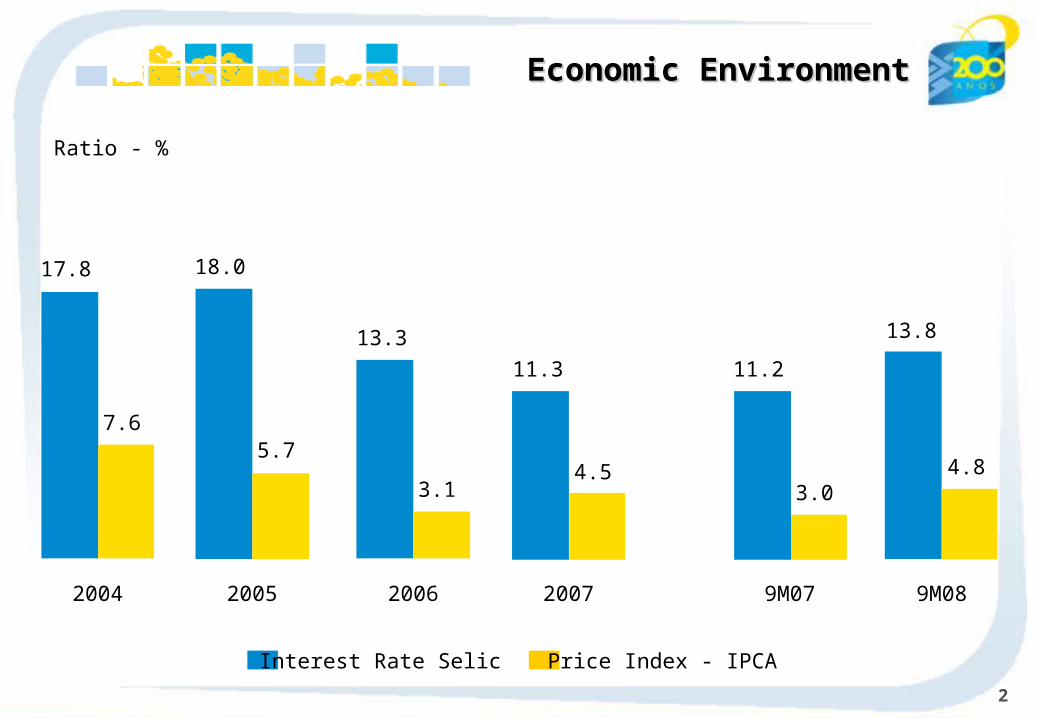

Economic EnvironmentEconomic Environment

Interest Rate Selic

Ratio - %

Price Index - IPCA

17.8

7.6

18.0

5.7

13.3

3.1

11.3

4.5

11.2

3.0

13.8

4.8

2004 2005 2006 2007 9M07 9M08

3

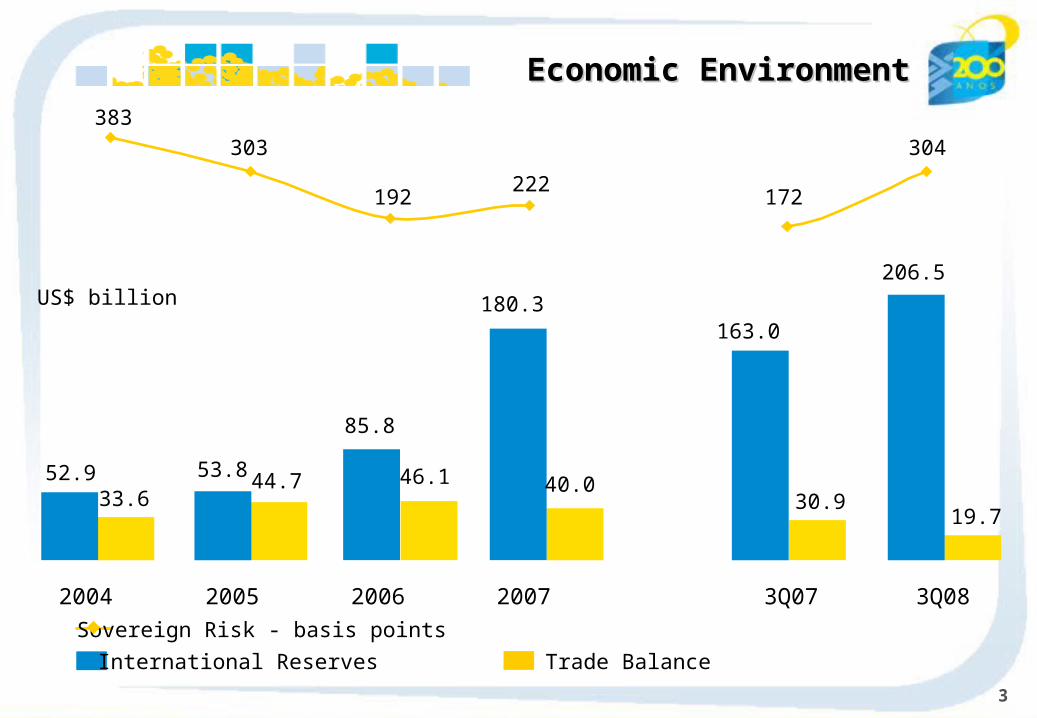

Economic EnvironmentEconomic Environment

International Reserves

Sovereign Risk - basis points

Trade Balance

US$ billion

33.644.7 46.1 40.0

30.919.7

52.9 53.8

85.8

180.3163.0

206.5

2004 2005 2006 2007 3Q07 3Q08

383

303

192222

172

304

4

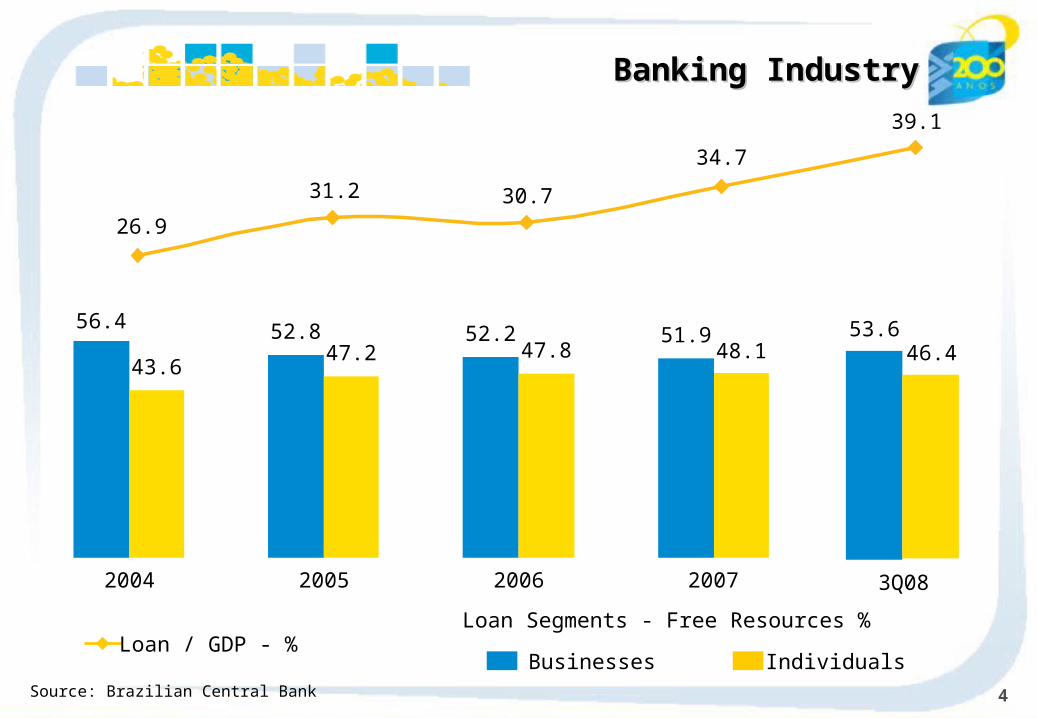

Banking IndustryBanking Industry

56.4

43.6

2004

52.847.2

2005

52.247.8

2006

51.948.1

2007

Businesses IndividualsLoan / GDP - %

53.646.4

3Q08

Loan Segments - Free Resources %

26.9

31.2 30.7

34.7

39.1

Source: Brazilian Central Bank

5

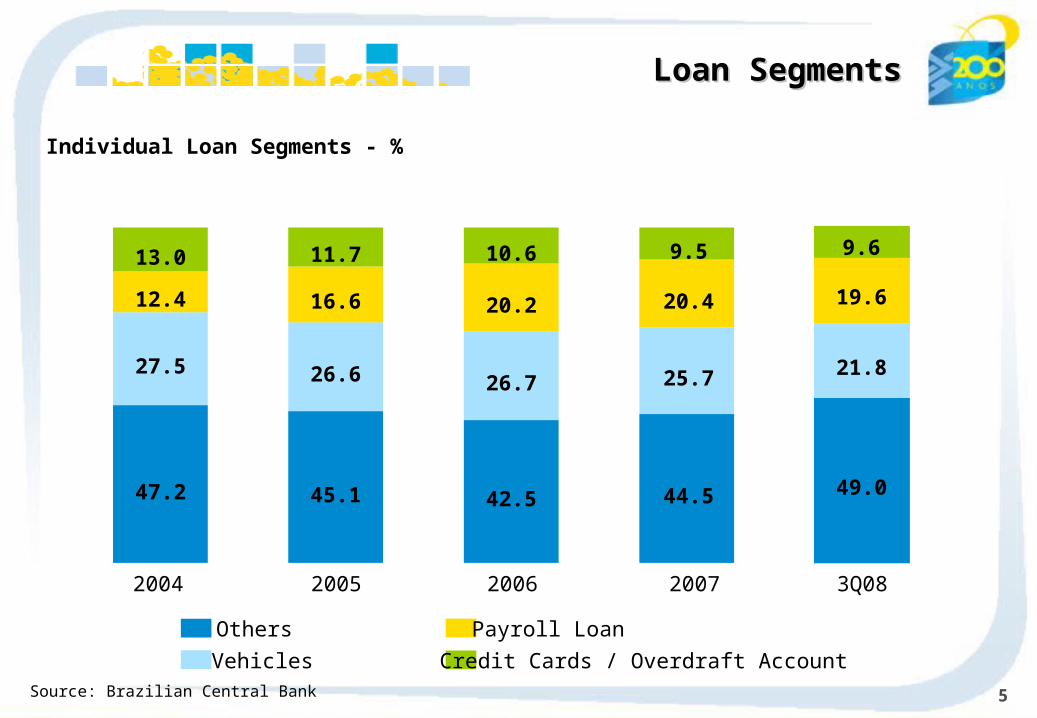

Others

Vehicles

Payroll Loan

Credit Cards / Overdraft Account

Loan SegmentsLoan Segments

2004 2005 2006 2007 3Q08

47.2

27.5

12.4

13.0

45.1

26.6

16.6

11.7

42.5

26.7

20.2

10.6

44.5

25.7

20.4

9.5

Individual Loan Segments - %

49.0

21.8

19.6

9.6

Source: Brazilian Central Bank

6

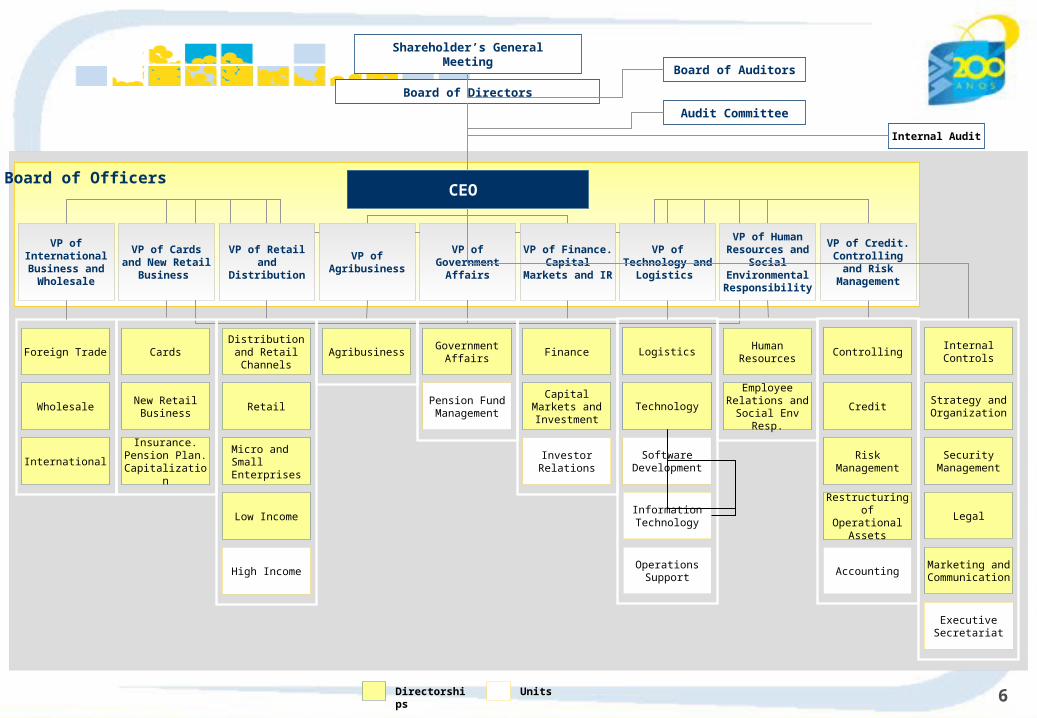

Board of Officers

Internal Audit

Board of Directors

Shareholder’s General Meeting

Board of Auditors

Directorships

Audit Committee

CEO

VP of International Business and

Wholesale

Foreign Trade

Wholesale

International

VP of Cards and New Retail Business

VP of Retail and Distribution

VP of Agribusiness

VP of Government

Affairs

VP of Finance. Capital Markets

and IR

VP of Technology and Logistics

VP of Human Resources and

Social Environmental Responsibility

VP of Credit. Controlling and

Risk Management

Cards

New Retail Business

Insurance. Pension Plan. Capitalization

Distribution and Retail Channels

Low Income

High Income

AgribusinessGovernment

Affairs

Pension Fund Management

Finance

Capital Markets and Investment

Investor Relations

Logistics

Technology

Software Development

Information Technology

Operations Support

Human Resources

Employee Relations and

Social Env Resp.

Controlling

Credit

Risk Management

Restructuring of Operational

Assets

Accounting

Internal Controls

Strategy and Organization

Security Management

Legal

Marketing and Communication

Executive Secretariat

Units

Micro and Small Enterprises

Retail

7

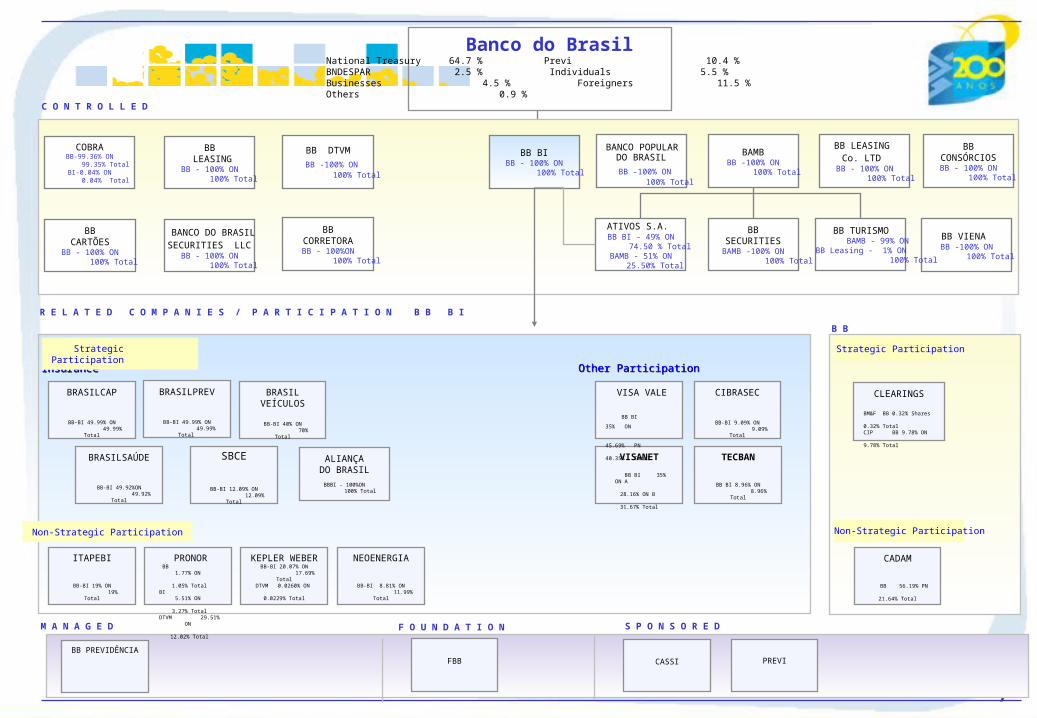

COBRABB-99.36% ON

99.35% TotalBI-0.04% ON

0.04% Total

BB LEASING

BB - 100% ON 100% Total

BB VIENA BB -100% ON

100% Total

BBCARTÕES

BB - 100% ON 100% Total

BB LEASING Co. LTD

BB - 100% ON 100% Total

BB DTVM

BB -100% ON 100% Total

BBCORRETORA

BB - 100%ON 100% Total

BAMBBB -100% ON

100% Total

BBCONSÓRCIOS

BB - 100% ON 100% Total

BB BIBB - 100% ON

100% Total

BANCO DO BRASIL

SECURITIES LLC BB - 100% ON

100% Total

BBSECURITIES

BAMB -100% ON 100% Total

BB TURISMO BAMB - 99% ONBB Leasing - 1% ON

100% Total

ATIVOS S.A. BB BI - 49% ON

74.50 % TotalBAMB - 51% ON 25.50% Total

BRASILPREV

BB-BI 49.99% ON 49.99% Total

CIBRASEC

BB-BI 9.09% ON 9.09% Total

SBCE

BB-BI 12.09% ON 12.09% Total

BRASILSAÚDE

BB-BI 49.92%ON 49.92% Total

VISANET

BB BI 35% ON A 28.16% ON B 31.67% Total

InsuranceInsurance

ITAPEBI

BB-BI 19% ON 19% Total

BRASILCAP

BB-BI 49.99% ON 49.99% Total

KEPLER WEBER

BB-BI 20.07% ON 17.69% TotalDTVM 0.0260% ON

0.0229% Total

VISA VALE

BB BI 35% ON

45.69% PN 40.35% Total

PRONORBB 1.77% ON

1.05% TotalBI 5.51% ON

3.27% Total DTVM 29.51% ON

12.02% Total

Strategic Participation

Non-Strategic Participation

BRASIL VEÍCULOS

BB-BI 40% ON 70% Total

NEOENERGIA

BB-BI 8.81% ON 11.99% Total

TECBAN

BB BI 8.96% ON 8.96% Total

CLEARINGS

BM&F BB 0.32% Shares 0.32% Total CIP BB 9.78% ON 9.78% Total

B B

Strategic Participation

CADAM

BB 56.19% PN 21.64% Total

Non-Strategic Participation

M A N A G E D

BB PREVIDÊNCIA

S P O N S O R E D

CASSI PREVIFBB

Other ParticipationOther Participation

R E L A T E D C O M P A N I E S / P A R T I C I P A T I O N B B B I

C O N T R O L L E D

BANCO POPULAR DO BRASIL

BB -100% ON 100% Total

F O U N D A T I O N

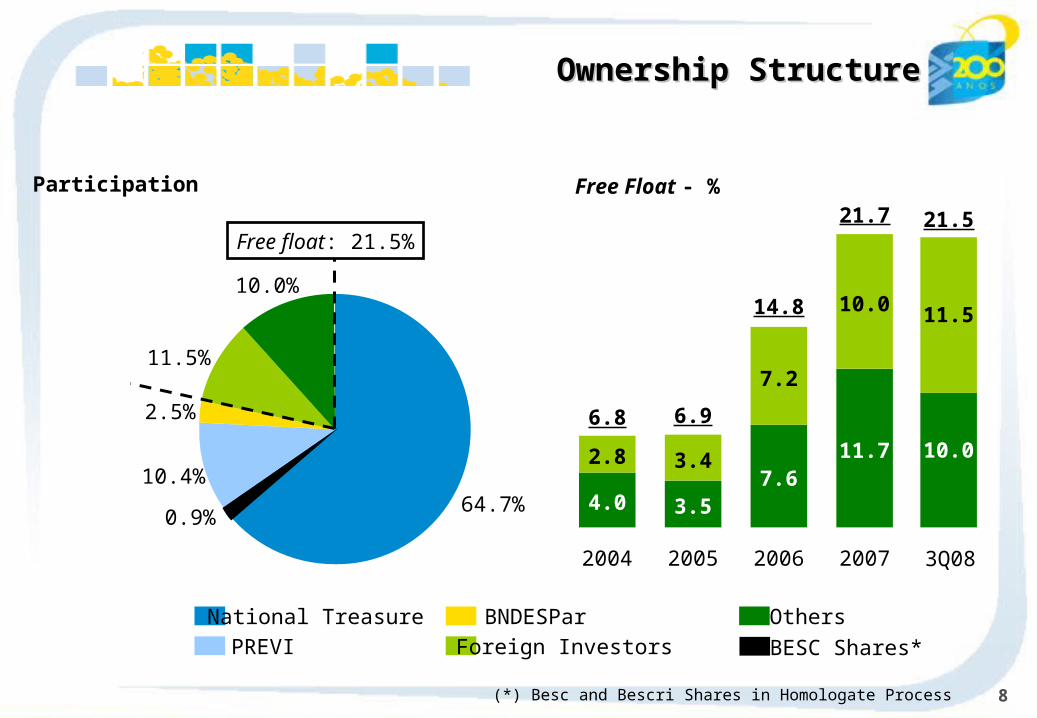

Banco do BrasilNational Treasury 64.7 % Previ 10.4 %BNDESPAR 2.5 % Individuals 5.5 %Businesses 4.5 % Foreigners 11.5 %Others 0.9 %

ALIANÇADO BRASIL

BBBI - 100%ON 100% Total

8

National Treasure

PREVI

BNDESPar

Foreign Investors

Others

Participation

64.7%10.4%

2.5%

11.5%

10.0%

Free float: 21.5%

Ownership StructureOwnership Structure

4.0

2.8

2004

6.8

3.5

3.4

2005

6.9

7.6

7.2

2006

14.8

11.7

10.0

2007

21.7Free Float - %

(*) Besc and Bescri Shares in Homologate Process

0.9%

BESC Shares*

3Q08

21.5

10.0

11.5

9

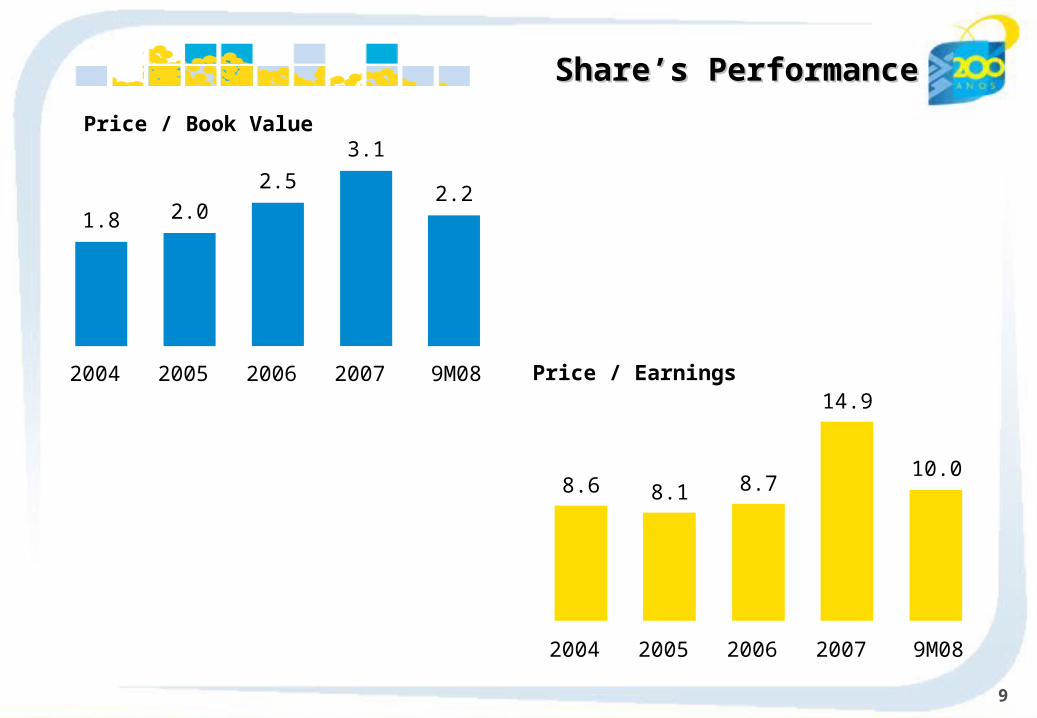

Price / Book Value

Price / Earnings

1.8

2004

2.0

2005

2.5

2006

3.1

2007

2.2

9M08

8.6

2004

8.1

2005

8.7

2006

14.9

2007

10.0

9M08

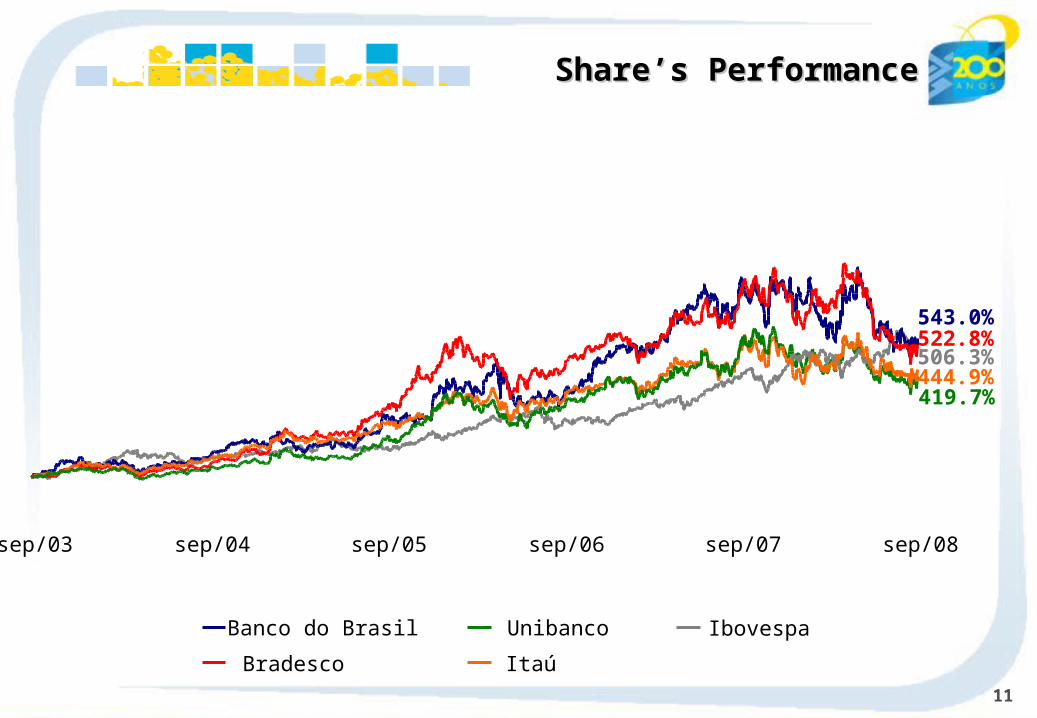

Share’s PerformanceShare’s Performance

10

Earnings / Share – R$

Dividends and Interest on Own Capital / Share – R$

1.3

2004

1.7

2005

2.4

2006

2.0

2007

2.3

9M08

0.4

2004

0.6

2005

1.0

2006

0.8

2007

0.9

9M08

Share’s PerformanceShare’s Performance

11

sep/03 sep/04 sep/05 sep/06 sep/07

IbovespaBanco do Brasil

Bradesco Itaú

Unibanco

Share’s PerformanceShare’s Performance

sep/08

543.0%

506.3%522.8%

444.9%419.7%

12

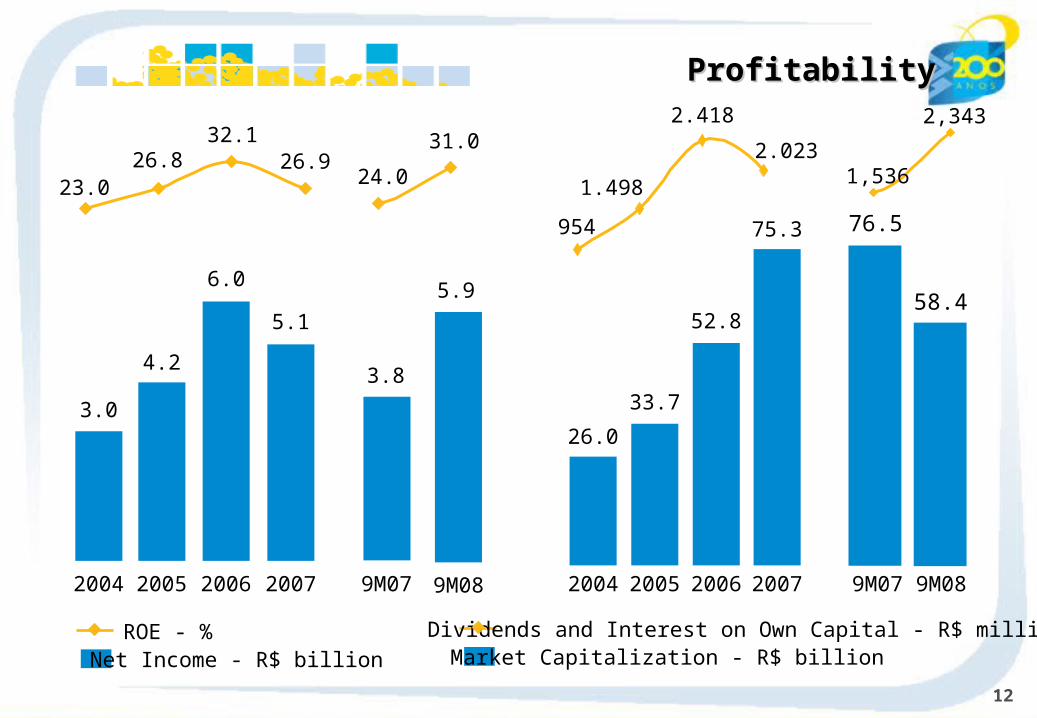

ProfitabilityProfitability

3.0

2004

4.2

2005

6.0

2006

5.1

2007 9M07 9M08

26.0

2004

33.7

2005

52.8

2006

75.3

2007 9M07 9M08

2.023

2.418

1.498

954

Net Income - R$ billionROE - %

Market Capitalization - R$ billionDividends and Interest on Own Capital - R$ million

3.8

5.9

31.0

24.026.9

32.126.8

23.0

76.5

58.4

1,536

2,343

13

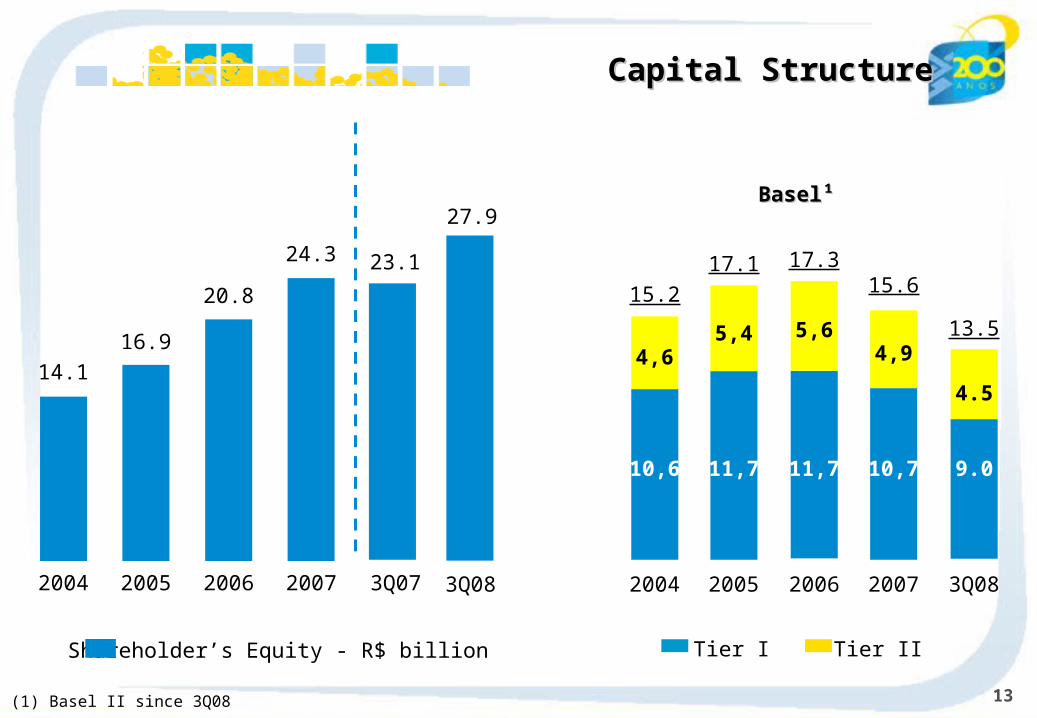

Shareholder’s Equity - R$ billion

14.1

2004

16.9

2005

20.8

2006

24.3

2007

23.1

3Q07

Capital StructureCapital Structure

27.9

3Q08

Tier IITier I

15.2

2004

17.1

2005

17.3

2006

15.6

2007

13.5

3Q08

9.0

4.5

(1) Basel II since 3Q08

Basel¹Basel¹

10,6

4,6

11,7

5,4

11,7

5,6

10,7

4,9

14

239.0

2004

253.0

2005

296.4

2006

357.8

2007

Market Share % Assets - R$ billions

AssetsAssets

(**) Economic-Financial Consolidated

458.9**

9M08

CAGR: 19.0%CAGR: 19.0%

19.5%17.7% 17.2% 16.4% 16.6%*

(*) Until Jun/08 - Source: Brazilian Central Bank

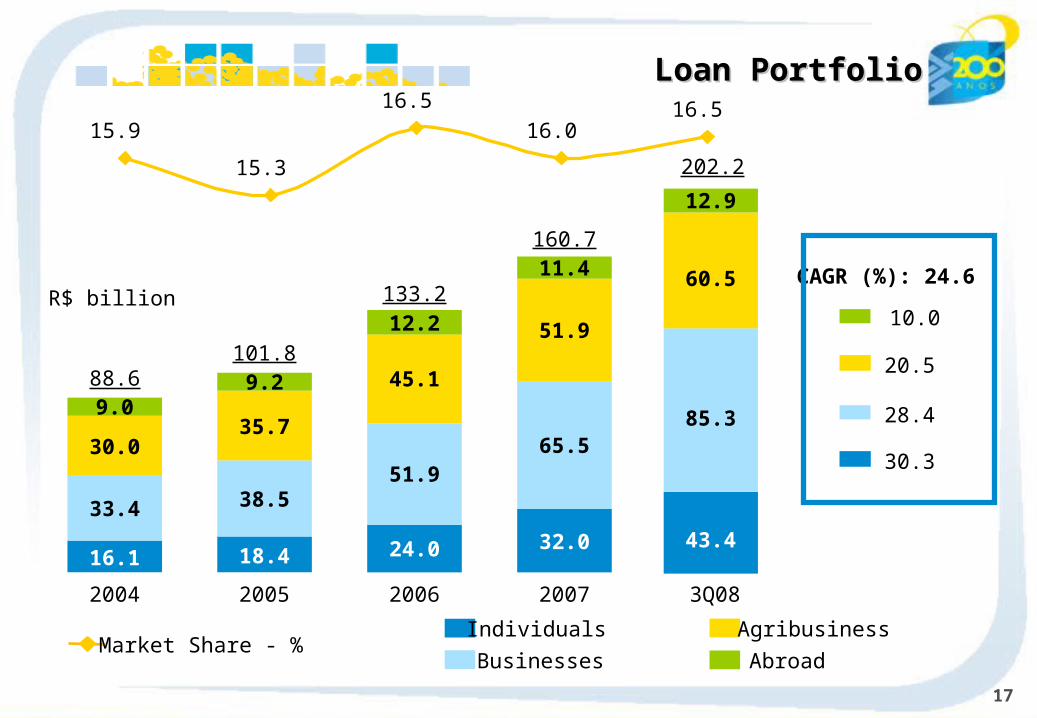

15

2004

49.7

44.5

29.0

31.15.8

160.1

2005

63.5

30.5

35.8

32.85.5

168.2

2006

76.9

49.3

40.1

36.7

5.2

208.1

2007

85.5

72.3

51.3

45.8

5.6

260.6

CAGR (%): 19.9

3.4

15.1

11.1

R$ billion

19.0

28.7

3Q08

315.7

FundingFunding21.1

19.819.619.1

21.9

127.8

85.6

43.0

52.7

6.6

Money Market Borrowing

Demand Deposits

Saving Deposits

Others

Market Share - %

Time Deposits

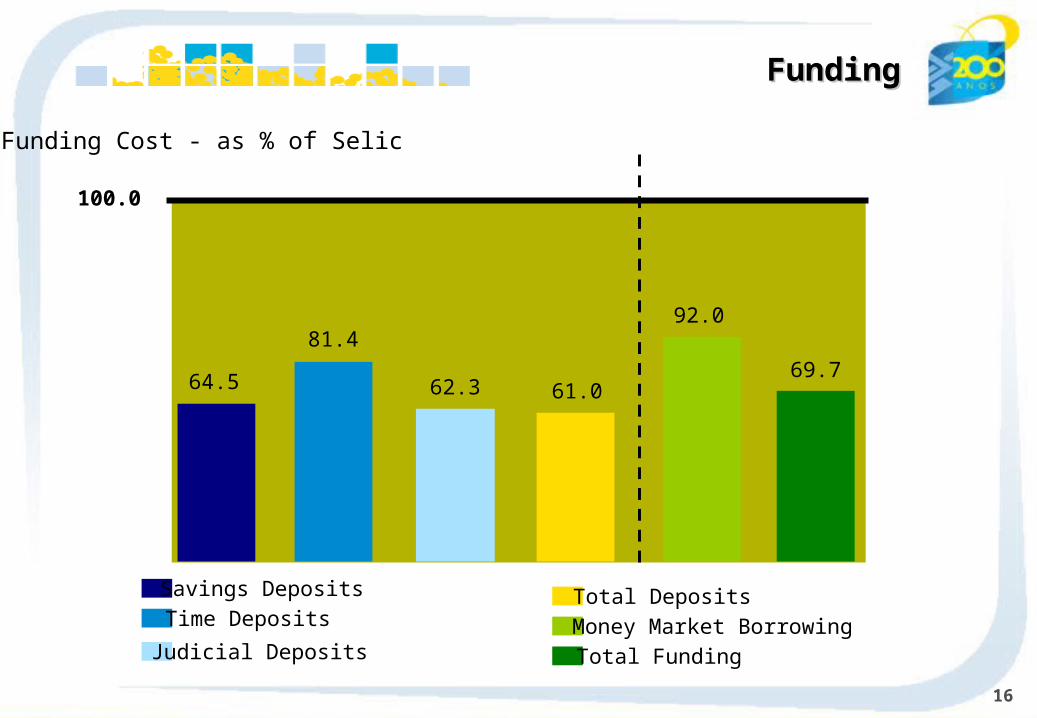

16

64.5

81.4

62.3

92.0

61.069.7

100.0

Funding Cost - as % of Selic

FundingFunding

Savings Deposits

Time Deposits

Judicial Deposits

Total Deposits

Money Market Borrowing

Total Funding

17

Individuals

Businesses

Agribusiness

Abroad

2004

16.1

33.4

30.0

9.088.6

2005

18.4

38.5

35.7

9.2101.8

2006

24.0

51.9

45.1

12.2133.2

2007

32.0

65.5

51.9

11.4160.7

Loan PortfolioLoan Portfolio

CAGR (%): 24.6

10.0

20.5

28.4

30.3

R$ billion

Market Share - %

3Q08

202.2

15.9

15.3

16.5

16.016.5

43.4

85.3

60.5

12.9

202.2

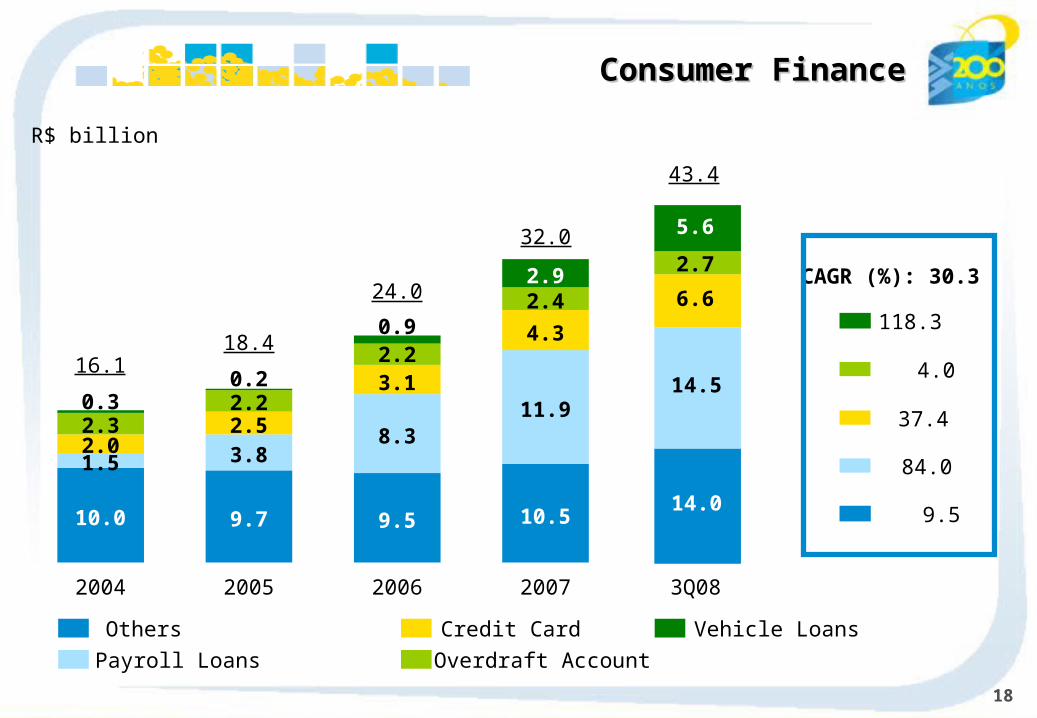

18

Others

Payroll Loans Overdraft Account

Credit Card Vehicle Loans

CAGR (%): 30.3

4.0

118.3

37.4

9.5

84.0

Consumer FinanceConsumer Finance

R$ billion

16.1

10.0

1.52.02.30.3

2004

18.4

9.7

3.82.52.20.2

2005

24.0

9.5

8.3

3.12.20.9

2006

32.0

10.5

11.9

4.3

2.42.9

2007

43.4

3Q08

14.0

14.5

6.6

5.6

2.7

19

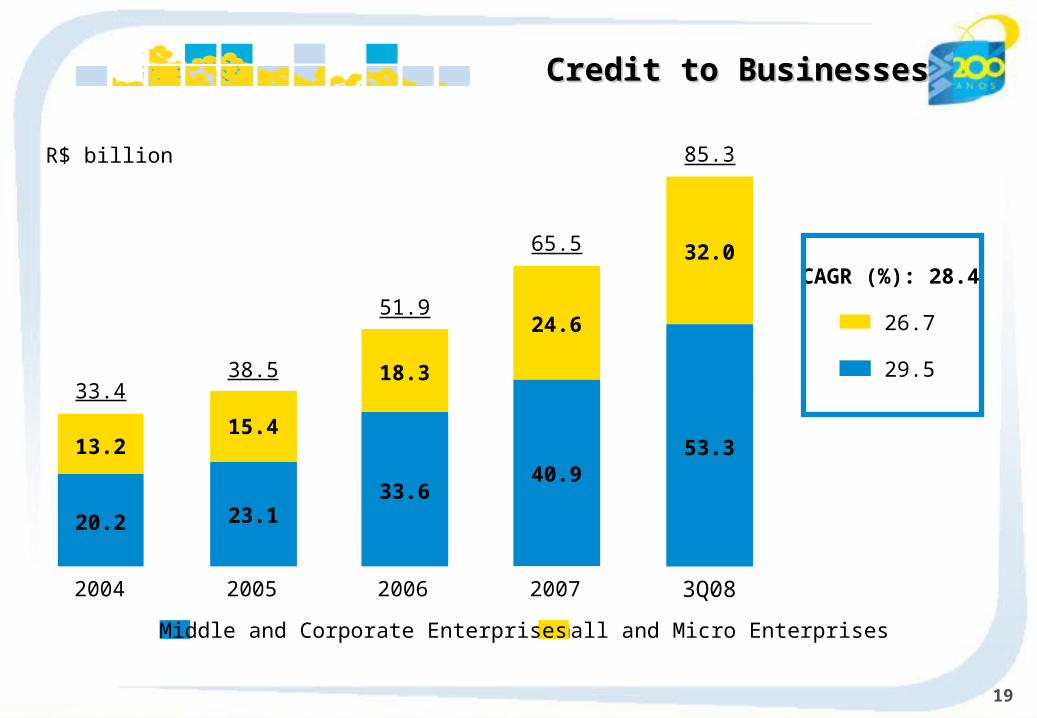

Small and Micro EnterprisesMiddle and Corporate Enterprises

2004

33.4

2005

38.5

2006

51.9

2007

65.5

CAGR (%): 28.4

26.7

29.5

Credit to BusinessesCredit to Businesses

R$ billion

3Q08

85.3

20.2 23.133.6

40.953.313.2

15.4

18.3

24.6

32.0

20

BusinessesIndividuals

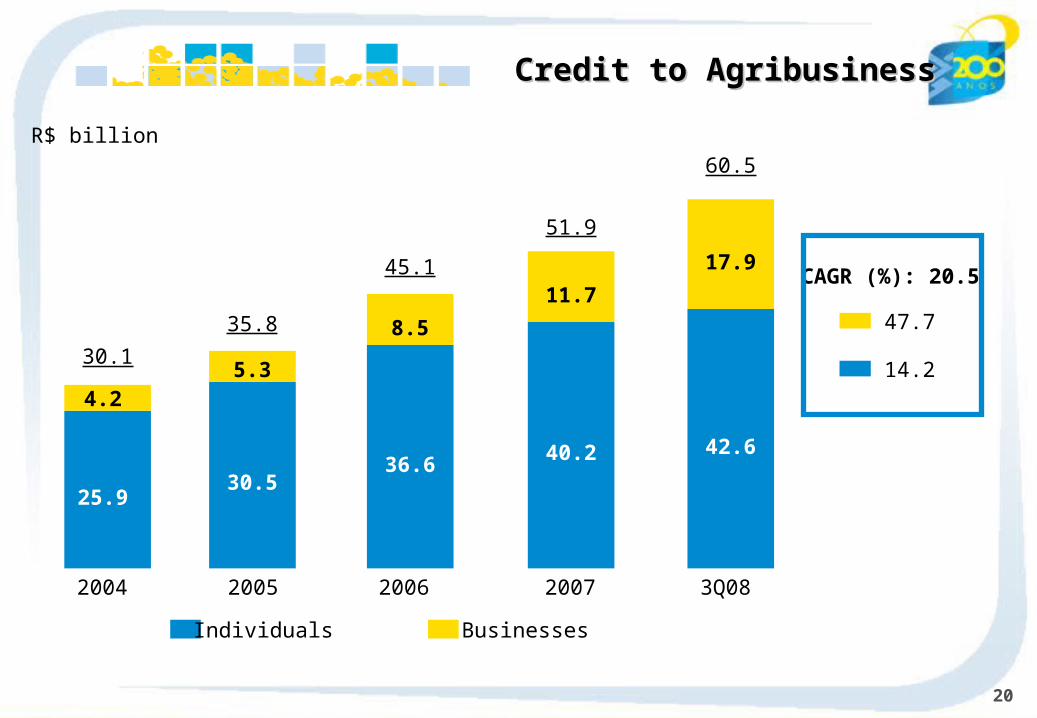

CAGR (%): 20.5

47.7

14.2

Credit to AgribusinessCredit to Agribusiness

R$ billion

2004

30.1

2005

35.8

2006

45.1

2007

51.9

3Q08

60.5

25.930.5

36.640.2 42.6

4.25.3

8.5

11.7

17.9

21

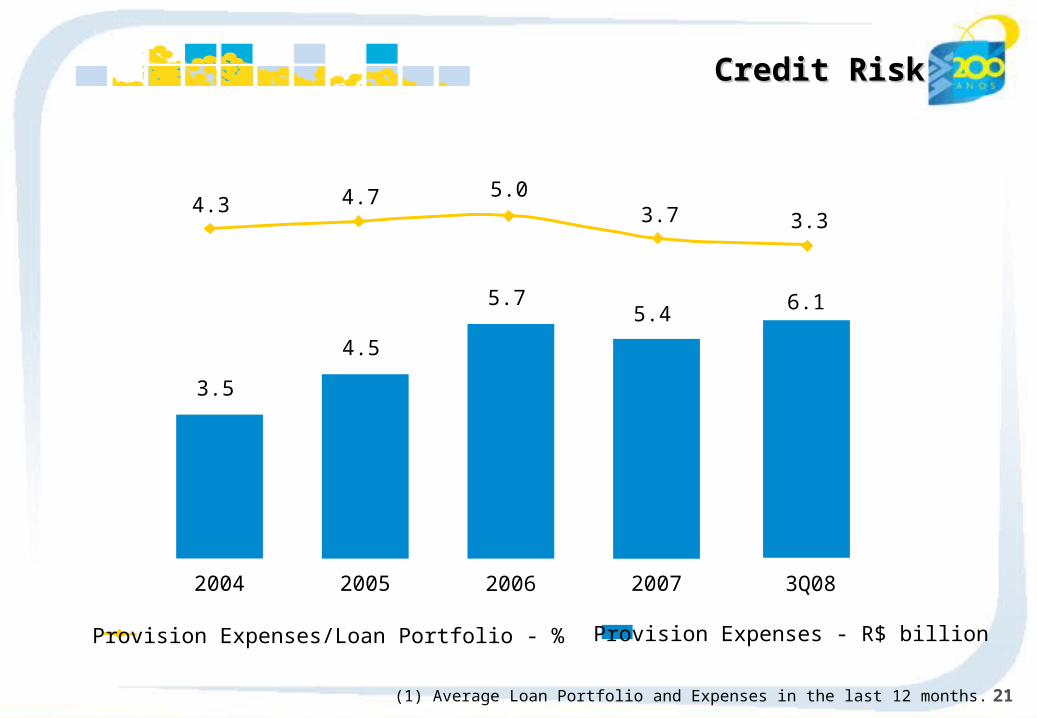

2004

3.5

2005

4.5

2006

5.7

2007

5.4

3Q08

6.1

Credit RiskCredit Risk

4.3 4.73.7 3.3

5.0

Provision Expenses - R$ billionProvision Expenses/Loan Portfolio - %

(1) Average Loan Portfolio and Expenses in the last 12 months.

22

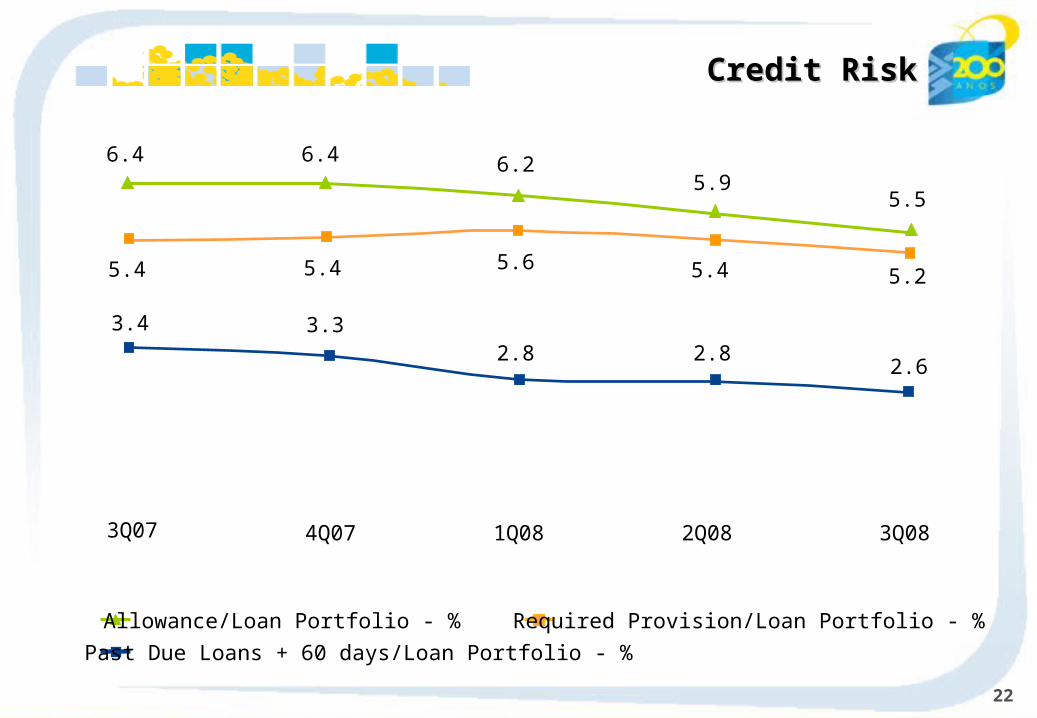

Credit RiskCredit Risk

3Q07 4Q07 1Q08 2Q08 3Q08

3.4 3.32.8 2.8

2.6

5.55.9

6.26.46.4

5.25.45.65.45.4

Past Due Loans + 60 days/Loan Portfolio - %

Allowance/Loan Portfolio - % Required Provision/Loan Portfolio - %

23

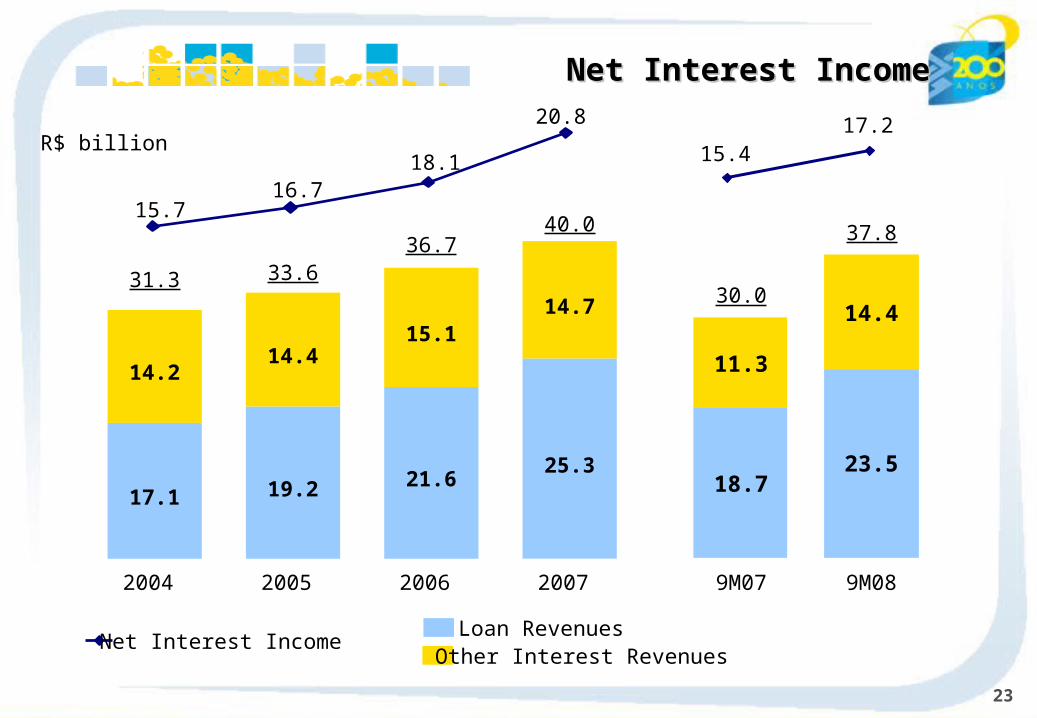

Net Interest IncomeNet Interest Income

Loan Revenues

15.716.7

18.1

20.8

Net Interest Income

R$ billion

17.1

14.2

2004

31.3

19.2

14.4

2005

33.6

21.6

15.1

2006

36.7

25.3

14.7

2007

40.0

9M07

30.0

9M08

37.8

15.417.2

18.723.5

11.3

14.4

Other Interest Revenues

24

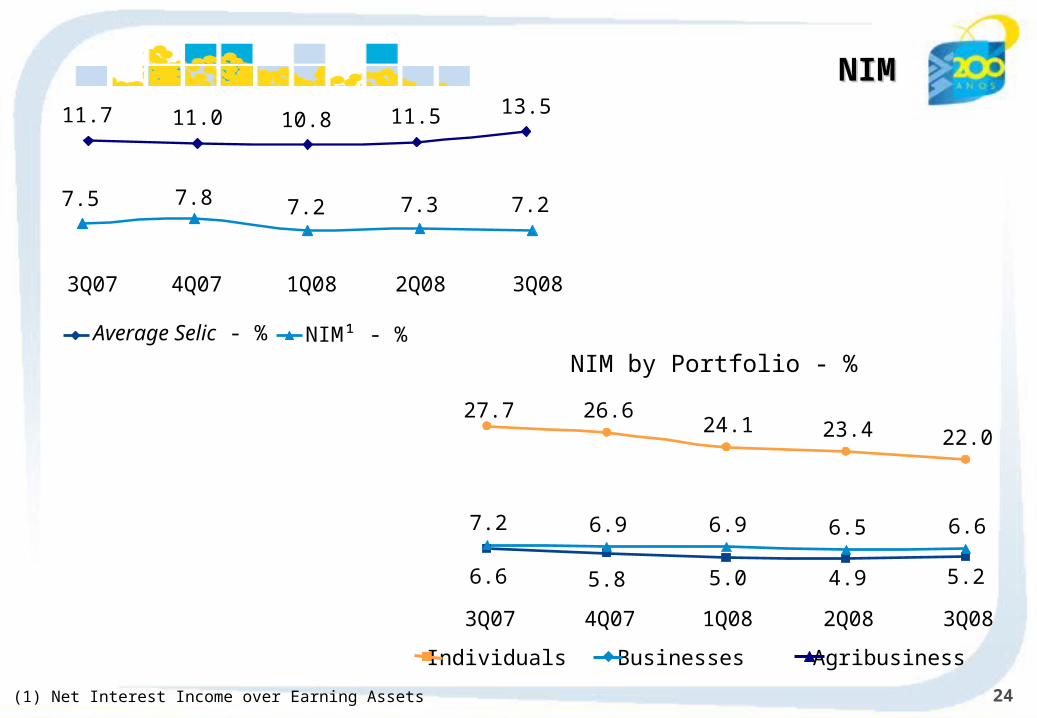

NIMNIM

3Q07 4Q07 1Q08 2Q08 3Q08

6.6 5.8 5.0 4.9 5.2

7.2 6.9 6.9 6.5 6.6

27.7 26.624.1 23.4 22.0

3Q07 4Q07 1Q08 2Q08 3Q08

7.27.37.27.87.5

11.7 11.0 10.8 11.5 13.5

(1) Net Interest Income over Earning Assets

Average Selic - % NIM¹ - %

NIM by Portfolio - %

Individuals Businesses Agribusiness

25

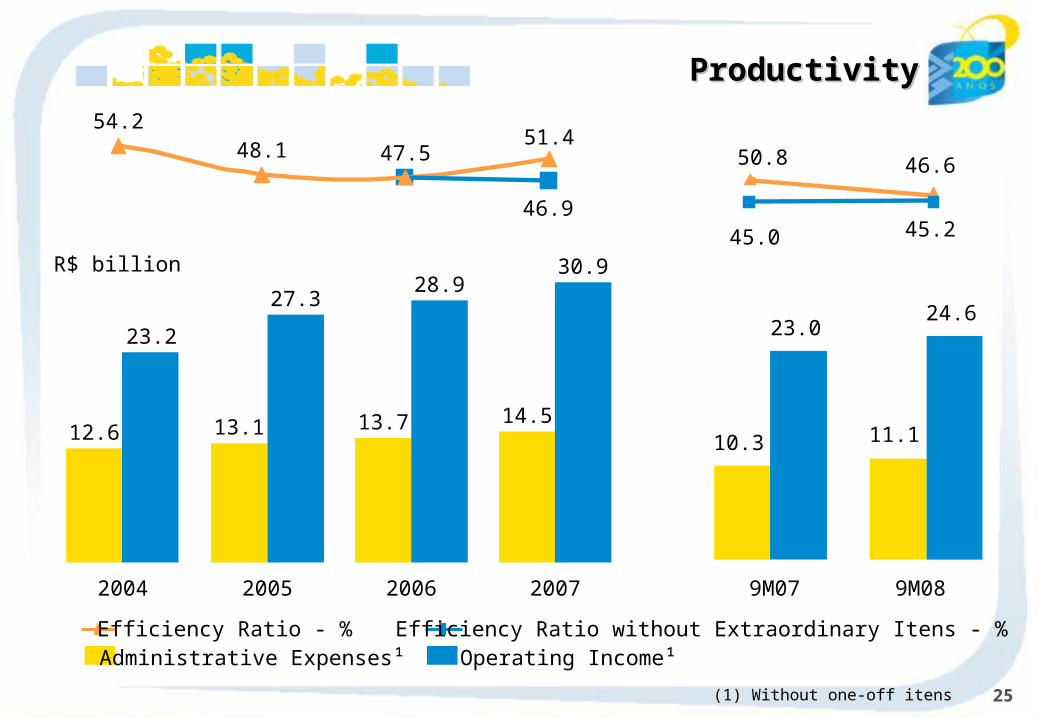

ProductivityProductivity

2004

12.6

23.2

2005

13.1

27.3

2006

13.7

28.9

2007

14.5

30.9

54.248.1 47.5

51.4

46.9

R$ billion

(1) Without one-off itens

9M07 9M08

10.3 11.1

23.024.6

50.8 46.6

45.245.0

Efficiency Ratio - %Administrative Expenses¹

Efficiency Ratio without Extraordinary Itens - %Operating Income¹

26

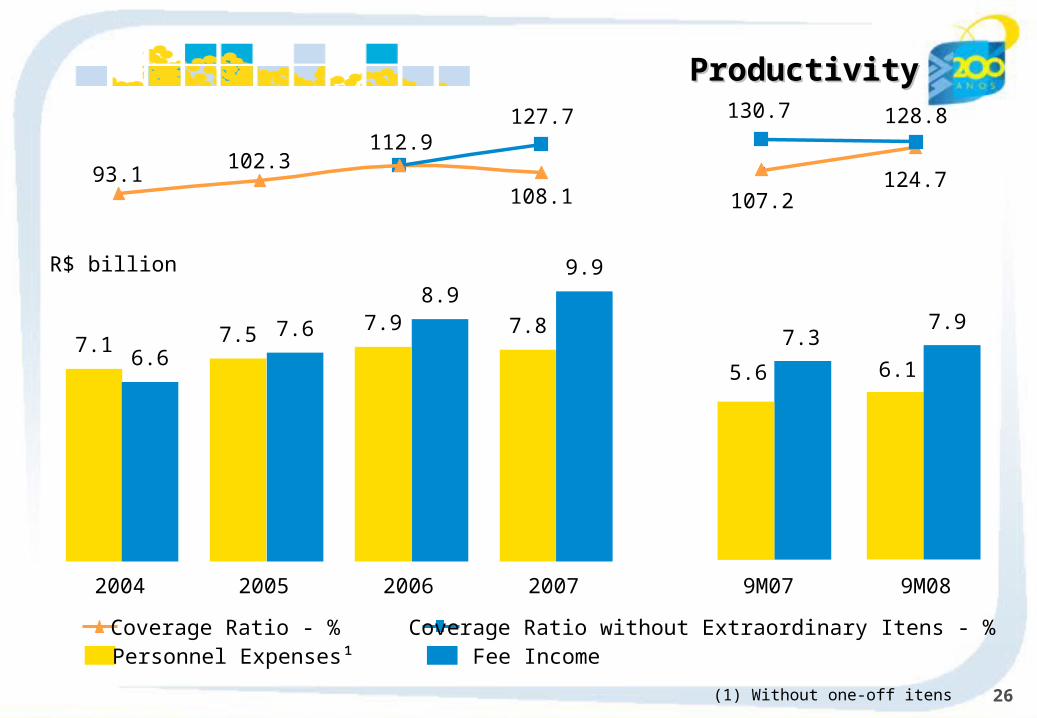

ProductivityProductivity

2004 2005 2006 2007

7.16.6

7.5 7.6 7.98.9

7.8

9.9

102.3

108.1

127.7

93.1

112.9

R$ billion

9M07 9M08

5.6 6.1

7.37.9

128.8130.7

107.2124.7

Coverage Ratio - %Personnel Expenses¹

Coverage Ratio without Extraordinary Itens - %Fee Income

(1) Without one-off itens

27

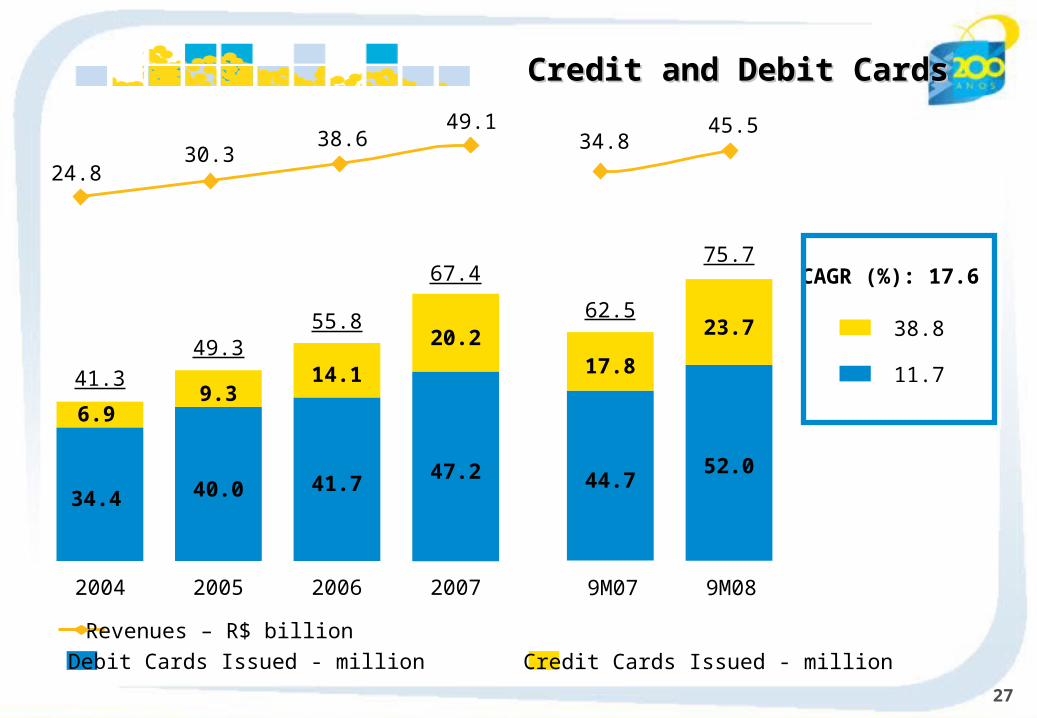

Credit and Debit CardsCredit and Debit Cards

CAGR (%): 17.6

38.8

11.7

2004

34.4

6.9

41.3

2005

40.0

9.3

49.3

2006

41.7

14.1

55.8

2007

47.2

20.2

67.4

9M07

44.7

17.8

62.5

52.0

23.7

9M08

75.7

Debit Cards Issued - million

Revenues – R$ billion

Credit Cards Issued - million

34.845.549.1

38.630.3

24.8

28

Individuals Businesses

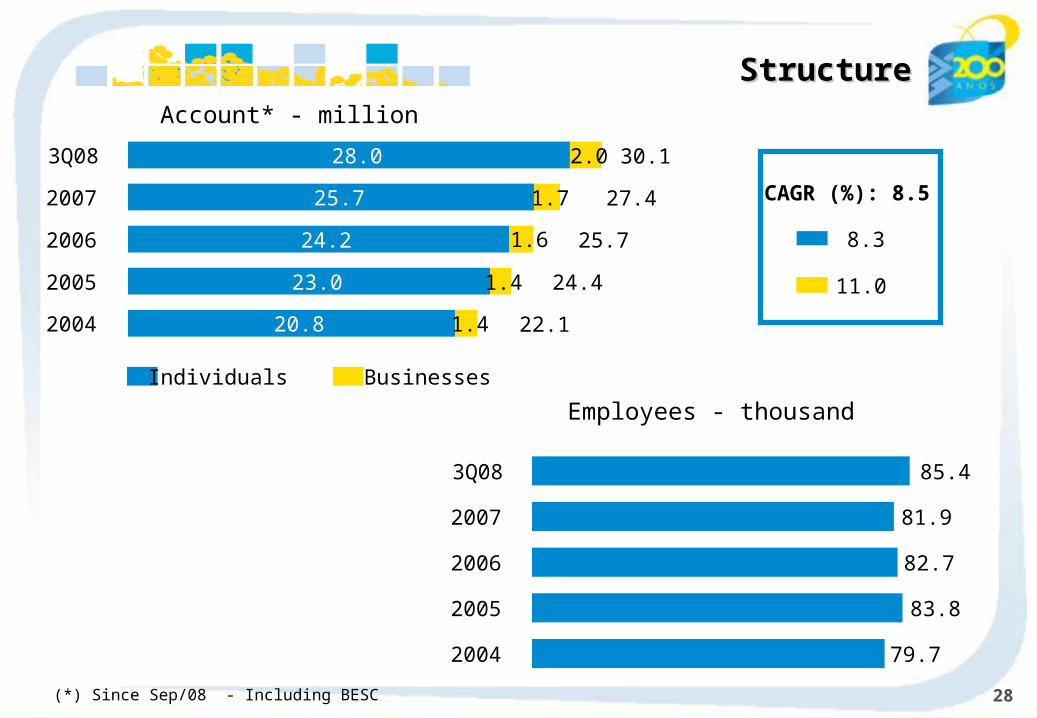

Account* - million

CAGR (%): 8.5

8.3

11.0

StructureStructure

Employees - thousand

2004 22.120.8 1.4

2005 24.423.0 1.4

2006 25.724.2 1.6

2007 27.425.7 1.7

3Q08 30.128.0 2.0

2004 79.7

2005 83.8

2006 82.7

2007 81.9

3Q08 85.4

(*) Since Sep/08 - Including BESC

29

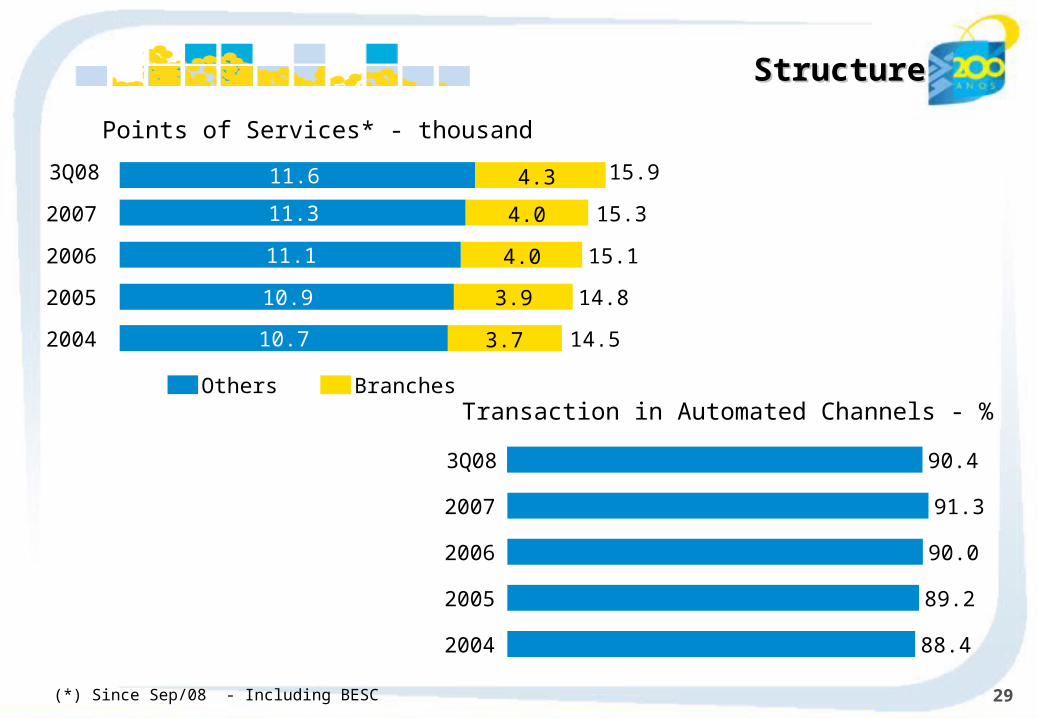

Others Branches

Points of Services* - thousand

88.42004

89.22005

90.02006

91.32007

Transaction in Automated Channels - %

StructureStructure

90.43Q08

2004 14.510.7 3.7

2005 14.810.9 3.9

2006 15.111.1 4.0

2007 15.311.3 4.0

3Q08 15.911.6

(*) Since Sep/08 - Including BESC

4.311.6

30

StructureStructure

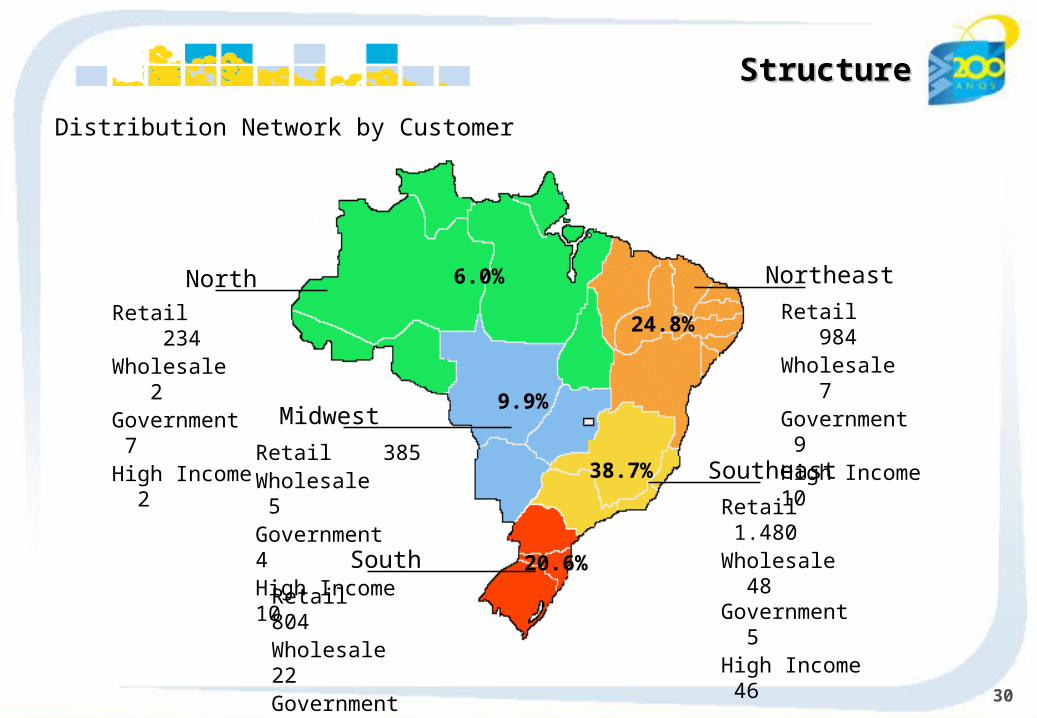

Distribution Network by Customer

Northeast

Retail 984Wholesale 7Government 9High Income 10

Retail 1.480Wholesale 48 Government 5High Income 46Retail 804

Wholesale 22Government 3High Income 9

Retail 385Wholesale 5Government 4High Income 10

Retail 234Wholesale 2Government 7High Income 2

North

Midwest

South

Southeast

6.0%

9.9%

24.8%

38.7%

20.6%

31

StructureStructure

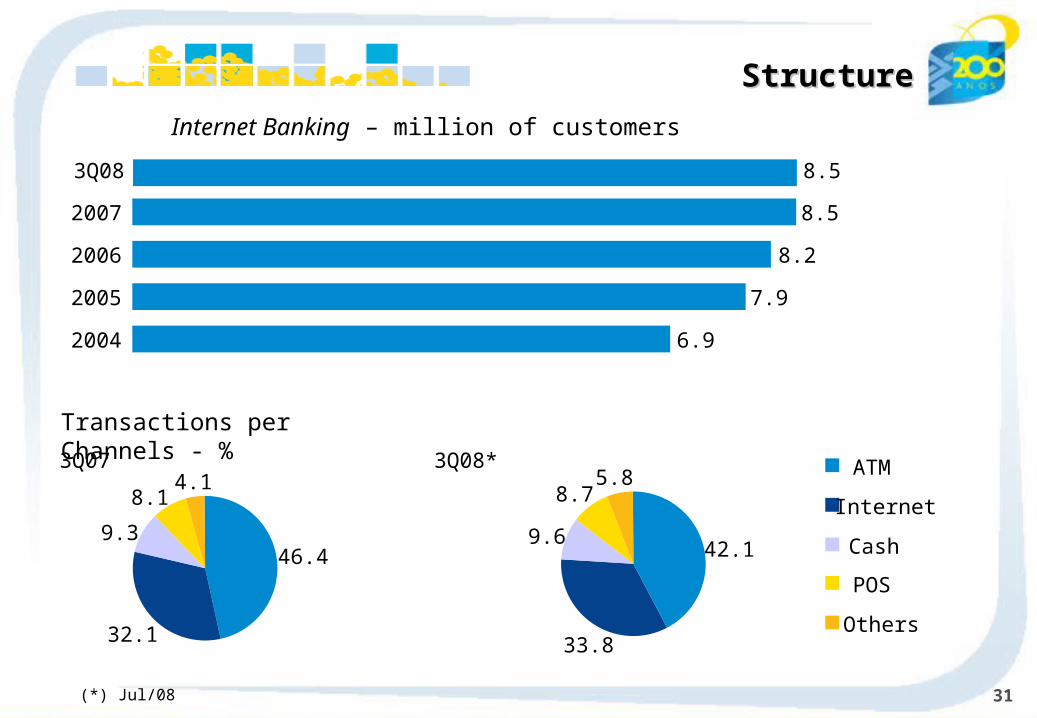

Transactions per Channels - %

ATM

Internet

Cash

POS

Others

Internet Banking – million of customers

6.92004

7.92005

8.22006

8.52007

8.53Q08

3Q08*

42.1

33.8

9.6

8.75.8

3Q07

46.4

32.1

9.3

8.14.1

(*) Jul/08

32

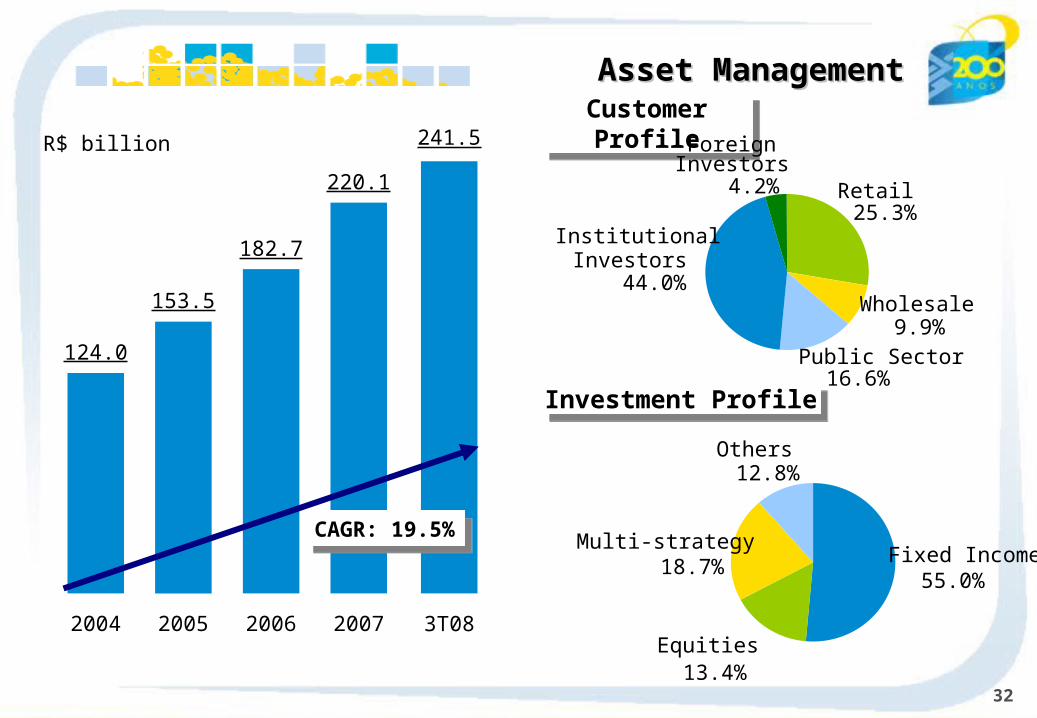

241.5

3T08

Asset ManagementAsset Management

124.0

2004

153.5

2005

182.7

2006

220.1

2007

CAGR: 19.5%CAGR: 19.5%

Customer ProfileCustomer Profile

Retail25.3%

Wholesale 9.9%

Public Sector16.6%

Institutional Investors

44.0%

Foreign Investors

4.2%

Investment ProfileInvestment Profile

Fixed Income55.0%

Equities13.4%

Multi-strategy18.7%

Others12.8%

R$ billion

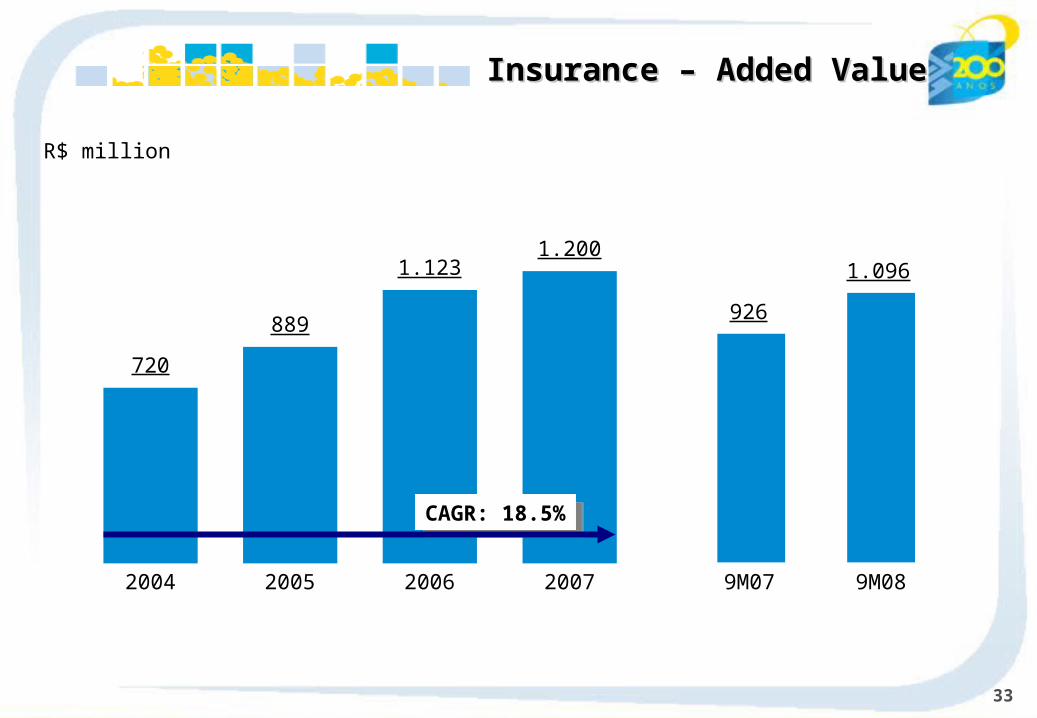

33

720

2004

889

2005

1.123

2006

1.200

2007 9M07 9M08

CAGR: 18.5%CAGR: 18.5%

R$ million

Insurance – Added ValueInsurance – Added Value

926

1.096

34

Investor Relations UnitSCN - Quadra 2 - Bloco A - 6th floor - Room 602

Ed. Corporate Financial Center70712-900 - Brasília (DF)Phone: 55 (61) 3101.8781

Fax: 55 (61) 3101.8793

DisclaimerDisclaimer - This presentation contains references and statements. planned synergies, increasing estimates, projections of results and future strategy for Banco do Brasil, it’s Associated and Affiliated Companies and Subsidiaries. Although these

references and statements reflect the management’s belief, it also involves imprecision and high difficult risks to be foreseen, consequently, it may conduct to a different result than the one anticipated here. These expectations are highly depended on market conditions, on the Brazilian economic performance, on the sector and the international market. Banco do Brasil is not

responsible for bringing up to date any estimate in this presentation.

For further information access www.bb.com.br/ir