Embed Size (px)

Citation preview

Page 1 of 12

AUDIT QUALITY, THE INDEPENDENCE OF AN AUDITOR AND

THE IMPLEMENTATION OF AUDIT STANDARD:

A SURVEY BASED STUDY

Hisar Pangaribuan

Adventist University of Indonesia – Bandung

Abstract

The purpose of this study is to obtain empirical evidence on the influence of independence auditor and implementation of audit standard on audit quality. The research was conducted

by purposive sampling and obtained the total sample of 77 respondent external auditors

who work in public accounting firm in Jakarta. Criteria of respondents as a sample in this study is that the respondent as a senior auditor has minimum experience of two years as

an auditor. The result of this study indicated that the independence of auditor and the implementation of audit standards can be as predictor variables in order to improve audit

quality.

Key words: audit quality, independence of auditor, audit standard.

1. Introduction

There are two important characteristics that must exist in financial statements,

that is relevant and reliable. Both characteristics are difficult to measure thus information

users need third party services that are independent auditors in public accountants to

provide assurance that the financial statements are both relevant and reliable and can

increase the confidence of all parties concerned with the company (Singgih & Bawono ,

2010).

In carrying out their profession, public accountants are required to produce

quality audits. Audit quality is any possibility that an auditor when auditing its’ client's

financial report can determine the violation that happened in the client's accounting system

and report it in an audited financial statement, where in performing its duty the auditor is

guided by auditing standards and ethical code of relevant public accountants (Rapina et al,

2010).

Auditing standards established by the Indonesian Institute of Certified Public

Accountants (IAPI) in 2013 describes the auditor's general principles and responsibilities,

risk assessment and response to assessed risks, audit evidence, use of other parties' work,

audit and reporting conclusions and specific areas. The general principles are a reflection of

the personal qualities that an auditor must possess that requires the auditor to have sufficient

technical skills and training in performing the audit procedures. While other standards set

the auditor in terms of data collection and other activities carried out during the audit and

require auditors to prepare a report on the audited financial statements as a whole (IAPI,

2013). While professional ethics codes governing the behavior of public accountants in

carrying out their professional practices both with members and with the general public are

about professional responsibility, competence and professional caution, confidentiality,

professional behavior and technical standards for an auditor in carrying out his profession

(Elfarini, 2007).

Page 2 of 12

Perceptions of the quality of audit services generated by KAP (Public

Accounting Firm) will be a great benefit to investors and users of financial statements

related to audit benefits in financial reporting. Therefore, the ability to provide high quality

audit services is an important focus to be considered by the Public Accounting Firm

(Yuniarti & Zumara, 2013).

Audit quality is influenced by the attitude of independent auditors in applying

the code of ethics of the public accounting profession. The code of ethics sets out the basic

principles and rules of professional ethics that every individual in a public accounting firm

(KAP) or KAP network, whether they are members of the IAPI or not members of the IAPI,

which includes assurance services and services other than assurance as set out in

professional standards and professional codes of ethics (IAPI, 2013). The presence of

professional code of ethics of public accountants, the public will be able to assess whether

an independent auditor has worked in accordance with the ethical standards established by

his profession.

DeAngelo defined audit quality as the probability the auditor is able to find (as

seen from the competence of auditors) and be willing to report violations (as seen from the

independence of the auditor) to the financial statements of their clients (DeAngelo, 1981).

The audit quality should be good, because good audit quality can reduce the

uncertainty and reduce noise in financial reporting (Balsam, 2002). Previous study also

found that good audit quality will have a positive influence on the disclosure and will

reduce the level of information asymmetry (Silveira & Barros, 2006). Conversely, audit

failure will provide great litigation problem opportunities, bad reputation, corporate value

will deteriorate, audit fee earnings will also decline. Quality audits adversely affect the

auditor and auditee (Taqi, 2013).

The reality is that the audit quality is still low, as the evidence, it is still very

necessary to improve audit quality in ASEAN countries: In Singapore and Malaysia, the

auditor does not have the ability to audit the handling of the law. In Brunei and Vietnam,

the auditor does not have a requirement for continuing professional education audit.

Especially for Indonesia and Malaysia, the auditors required more or better knowledge of

internal quality reviews to improve the audit quality result. It is still very necessary to

improve the audit quality (Favere-Marchesi, 2000).

The way to improve audit quality is that the auditor is required to understand and

use the applicable audit standards in accordance with the set requirements, and the auditor

must be independent in carrying out his / her engagement duties.

With the existence of auditing standards, the auditor is required to perform its

engagement duties in order to refer to the existing audit standards. Based on that, the

resulting audit reflects the economic events that occur and the financial records presented

under applicable accounting standards, so that the quality will be better.

Independent attitude and mentality must be owned by an auditor in carrying out

its duties, both independent in fact and in appearance. The independent attitude of the

auditor will bring the auditor to act more objectively, resulting in an objective audit opinion

which results in better audit quality.

This study will focus on knowing how audit quality can be influenced by the

independence of auditors and the implementation of standard audits.

2. Literature review and hypotheses development

Auditing standards are guidelines for auditors in carrying out their professional

responsibilities. The audit standards (SPAP) in Indonesia issued by IAPI (2013) is an

adoption of the International Standard on Auditing issued by the International Auditing and

Page 3 of 12

Assurance Standards Board which will be applied by public accountants to audit the

financial statements for periods beginning on or after 1 January 2013. This adoption is

performed as part of the process to fulfill one of the Statement of Membership Obligation

of the International Federation of Accountants, which must be complied with by the Public

Accounting profession in Indonesia. (IAPI, 2013)

The Audit Standards (PSAP) issued by IICAP consist of (a). General principles

and auditor responsibilities (SA 200 - 265), (b). Risk assessment and response to the rated

risk (SA 300-450), (c). audit evidence (SA 500-560), (d). use of the work of others (SA

600-620), (e). Audit and reporting conclusions (SA 700-720) and (f). special areas (SA

800-810).

On the other hand, it should be noted that users of the financial statements,

especially the shareholders, will make decisions based on reports made by the auditor

regarding the financial statements of a company. This means that auditors have an

important role in approving a company's financial statements. Therefore, the quality of

audit is an important thing that must be considered by the auditors in the auditing process

(Agoes, 2017).

Meutia (2004) stated that the auditor's report contains the interests of the three

groups of audited company managers, shareholders of the company; and third parties or

outside parties such as potential investors, creditors and suppliers.

Independence of Auditor and Audit Quality

The presence of auditors through its audit report is expected to boost the

confidence of investors and financial information users to increase public trust. Qualified

audit opinion and understanding in utilizing of the company's audited financial information

really be an important key for many parties, including for investors and creditors. Guidance

book for auditor and internal control guidance over financial reporting, as well as educating

the reader who is not well versed on the financial statements is an example of efforts to

increase the use of audited financial statement correctly. The quality of information through

an audit over financial statement is very highly required, even in the situation of financial

crisis, the use of audited financial information in effort to improve their trust over financial

information remains high (Murphy, 2014).

Audit quality included in the audit topics are the most spacious and warmly

discussed. Audit quality is the possibility that the auditor able to find and be willing to

report violations on their client's financial statements (DeAngelo, 1981). This definition

was adopted by many other researchers into the ability (regarding expertise) and

willingness (independent) auditor to express an event at the company in accordance with

the occurrence of actual (Johnson et al., 2002; Carey & Simnett, 2006; Velnampy et al.,

2014; Evelyn, and Christine, 2001; Hapsoro, 2012; Kane & Velury, 2005).

Previous research has found that auditor independence significantly affects the

quality of the resulting audit (Tepalagul & Lin, 2015; Saputra, 2015; Agoes & Sarwoko,

2014).

On other occasions, the results of studies in banking companies in Indonesia

found that auditor independence has a positive relationship with audit quality generated,

although significant influence was not found. This finding says that independence issues

for the auditor have become an inherent requirement for the auditor itself (Pangaribuan et

al., 2016). Tjun, et al., (2012) also said auditor independence has no significant effect on

audit quality.

H1: Independence of auditors significantly impact audit quality

Page 4 of 12

Implementation of Audit Standard and Audit Quality

In carrying out its profession, public accountants are required to produce good

quality audit. Audit quality is any possibility that an auditor when auditing its client's

financial report can determine the violation that happened in client accounting system and

report it in the audited financial report, where in performing its duty the auditor is guided

by auditing standard and ethical code of relevant public accountant (Rapina et al., 2010).

Audit standards established by the Indonesian Institute of Certified Public

Accountants in 2013, namely general principles and auditor responsibilities, risk

assessment and response to assessed risks, audit evidence, use of other party work, audit

and reporting conclusions and areas special. Where the general principles are a reflection

of the personal qualities that an auditor must possess that requires the auditor to have

sufficient technical skills and training in performing the audit procedures. While other

standards set the auditor in terms of data collection and other activities carried out during

the audit and require auditors to prepare a report on the audited financial statements as a

whole (IAPI, 2013). Furthermore, professional codes of conduct governing the behavior of

public accountants in carrying out their professional practices both with their fellow

members and with the general public (Elfarini, 2007).

Arens (2008: 42) states that auditing standards are general guidelines to help

auditors fulfill their professional responsibilities in auditing historical financial statements.

Implementation of good audit standards can significantly affect audit quality

generated by auditors (Khadafi et al., 2014). This is because there are auditing standards as

the auditor's foundation or foundation in planning, conducting audit engagement work and

reporting audit findings. This audit standard also serves as a guide to what auditors can and

should not do in the conduct of an audit engagement.

H2: Implementation of audits of standard significantly impact audit quality

3. Research Method

This study is conducted on the basis of the writer's deep curiosity on the factors

that may affect the improvement of audit quality, especially those likely caused by the

independence of auditors and the implementation of audit standards in the assignment of

the audit. Furthermore, this study also tries to elaborate from both predictor variables that

which elements give the biggest contribution in influencing audit quality.

This study was conducted with a quantitative approach, with partial least square

statistic. Testing with partial least square approach suggests that if t arithmetic > t critical

(1.96) then Ho is rejected, if otherwise Ha is rejected (Kline, 2010).

The data was collected with questioners distributed to 77 respondents, external

auditors who work in public accounting firms in Jakarta. Criteria of respondents as a sample

in this study is that the respondent as a senior auditor and has minimum experience of two

years as an auditor.

1. Results and discussion

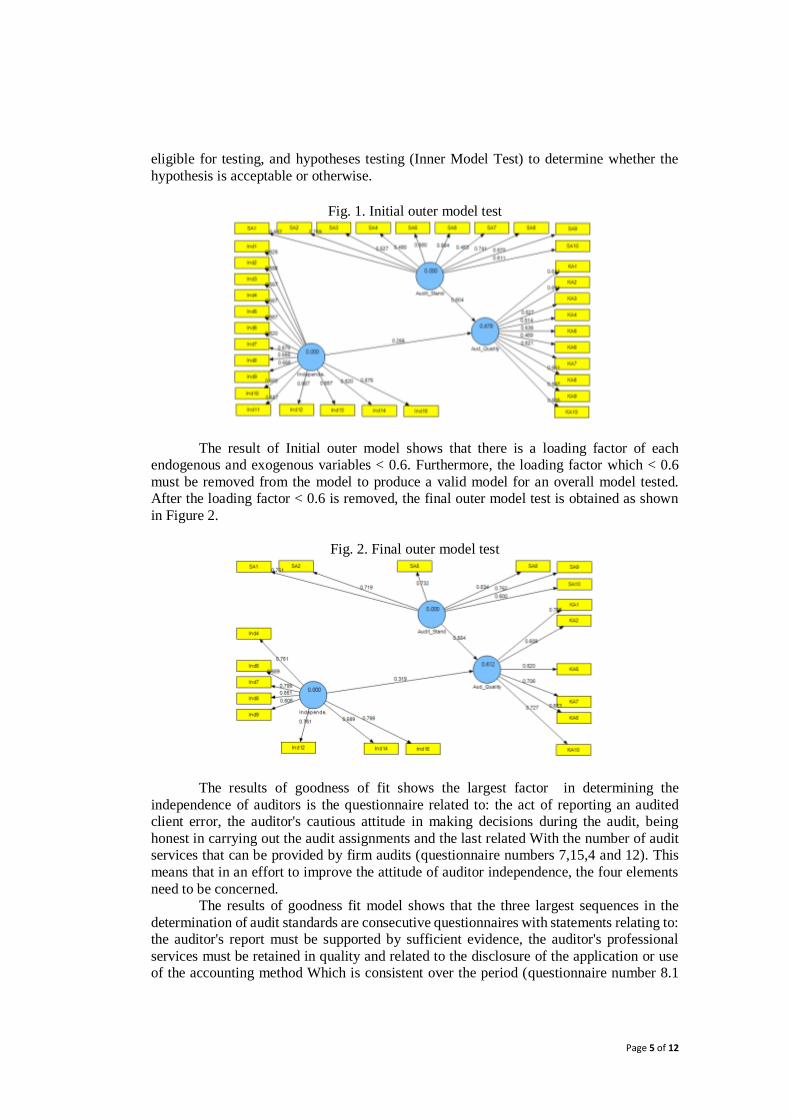

4.1 Outer Model Test

PLS approach in testing the hypotheses is done through two stages, that is

Goodness of fit model (Outer Model Test) to determine whether the model is already

Page 5 of 12

eligible for testing, and hypotheses testing (Inner Model Test) to determine whether the

hypothesis is acceptable or otherwise.

Fig. 1. Initial outer model test

The result of Initial outer model shows that there is a loading factor of each

endogenous and exogenous variables < 0.6. Furthermore, the loading factor which < 0.6

must be removed from the model to produce a valid model for an overall model tested.

After the loading factor < 0.6 is removed, the final outer model test is obtained as shown

in Figure 2.

Fig. 2. Final outer model test

The results of goodness of fit shows the largest factor in determining the

independence of auditors is the questionnaire related to: the act of reporting an audited

client error, the auditor's cautious attitude in making decisions during the audit, being

honest in carrying out the audit assignments and the last related With the number of audit

services that can be provided by firm audits (questionnaire numbers 7,15,4 and 12). This

means that in an effort to improve the attitude of auditor independence, the four elements

need to be concerned.

The results of goodness fit model shows that the three largest sequences in the

determination of audit standards are consecutive questionnaires with statements relating to:

the auditor's report must be supported by sufficient evidence, the auditor's professional

services must be retained in quality and related to the disclosure of the application or use of the accounting method Which is consistent over the period (questionnaire number 8.1

Page 6 of 12

and 9). This means in the effort to use a good audit standard, the three elements must be

given special attention.

The result of goodness fit model also show that the three largest sequences in

determining audit quality are consecutively related to: the audit report should find

explanation of the result of the examination, the setting of the audit objectives from the

beginning of the acceptance of the assignment and that the report should also disclose issues

that can’t be completed until the end of the examination (questionnaire number 10, 1 and

7). These three elements should be given special attention in relation to the formation of

the audit quality.

4.2 Inner Model Test and Result

The test results show that there is a positive path between audit standard with audit

quality, with a path of 0.553715. This means by establishing and applying a good audit

standard by the auditor, the quality of the audit will be better. The use of standard audits

also make the auditor perform better engagement duties, supervise for better junior auditors

and perform audit reporting better so the resulting audit quality will be better.

Table 1. Path Coefficients

Aud_Quality

Aud_Quality

Audit_Stand 0.553715

Independence 0.318880

It also found that there is a positive path between independence and audit quality,

with a path of 0.318880. This means that the presence of an independent auditor in engaging

the audit engagement will result good audit quality, since the auditor will be more objective

in performing the engagement duties.

Table 2. Overview

Composite

Reliability

R

Square

Cronbachs

Alpha Communality Redundancy

Aud_Quality 0.834334 0.612218 0.763309 0.457429 0.226739

Audit_Stand 0.874477 0.828078 0.539492

Independence 0.896506 0.871366 0.522006

Overall it was found that the model was valid to be tested, it is proved that all the

values of composite reliability and cronbachs alpha have been > 0.7. It is also found that

the R square value of the model is 61.22%, which means that the model shows the

contribution of auditing standard and independence of auditor in determining audit quality

is 61.22%. Other factors that can determine audit quality for 38.78% is auditor quality

control standard, professional code of ethics and other factors outside of this study.

Fig. 3. Inner Model Test

Page 7 of 12

The result of hypothesis testing shows that t statistics of each exogenous variable

to endogenous variable > 1.96 means the auditing standard application and auditor

independence (exogenous variable) effect audit quality (endogen variable) significantly.

Based on the prerequirement, if t arithmetic > t critical (1.96) then Ho is rejected, if on the

contrary then Ha is rejected (Kline, 2010).

Table 3. Total Effects (Mean, STDEV, T-Values)

Original

Sample (O)

Standard

Deviation

(STDEV)

Standard

Error

(STERR)

T Statistics

(|O/STERR|)

Audit_Stand -> Aud_Quality 0.553715 0.072791 0.072791 7.606942

Independence -> Aud_Quality 0.318880 0.101795 0.101795 3.132575

Testing result show that the application of auditing standards in auditing

engagement Have a significant effect on audit quality. The testing result also show that the

independence of the auditor will improve the quality of the audit result. The attempts to

generate audit quality through these two predictors are very important to be concerned in

the practice of the audit profession in the field.

2. Conclusions and recommendations

Audit quality is one of the most important concerns for users of financial statements,

wherein financial statements are presented by management and verified through audits into

reliable financial information in assisting users to make decision.

The results of this study indicate that the existence of auditing standards as the

foundation of auditors in planning audits, executing audits and reporting audit findings can

improve the audit quality. The auditor will do the job of engagement better with obvious

guidance. Users of financial information will be more confident in using the information

because of the presence of good audit quality.

Independence of auditor is another important concern in an effort to improve audit

quality. The existence of an independent auditor (in attitude and appearance) within the

audit engagement will result an objective audit report in accordance with the audit findings

that result better audit quality. Further study is needed to know the impact of good audit

Page 8 of 12

quality. The impact can be on the internal company, regulator or government and also to

investors and creditors.

References

Agoes, S. (2017). Auditing: Petunjuk Praktis Pemeriksaan Akuntan oleh Akuntan Publik.

Edisi Kelima. Penerbit Salemba Empat.

Agoes, S. & Sarwoko, I. (2014). An empirical analysis of auditor’s industry specialization,

auditor’s independence and audit procedures on audit quality: Evidence from

Indonesia. International Conference on Accounting Studies 2014, 18-19 August

2014, Kuala Lumpur, Malaysia.

Balsam, S. (2002). Accrual Management, Investor Sophisticated, and Equity Valuation:

Evidence from 10-Q Fillings. Journal of Accounting Research, vol. 40, no. 4, pp.

987-1012.

Carey, P. & Simnett, R. (2006). Audit Partner Tenure and Audit Quality. The Accounting

Review 81, 2006.

DeAngelo. L.E. (1981). Auditor independence, “low balling” and disclosure regulation.

Journal of Accounting and Economics. 3.

Elfarini, Eunike Christina. 2007. Pengaruh Kompetensi dan Independensi Auditor

Terhadap Kualitas Audit. Semarang: Universitas Negeri Semarang.

Evelyn, Y., & Christine, A. J. (2001). Governance and Audit Quality: Is There an Association? Australian Accounting Standards Board & International

Federation of Accountants Public Sector Committee. Dikunjungi dari

http://aaahq.org/audit/midyear/ 02midyear/papers/yeoh&jubb.htm.

Favere-Marchesi, M. (2000). Audit Quality in ASEAN. International Journal of

Accounting. vol. 35, no. 1. Accounting and Regulatory Issues. Association for

Investment Management and Research.

Hapsoro, D. (2012). Pengaruh Kualitas Corporate Governance , Kualitas Audit, Dan

Earnings Management Terhadap Kinerja Perusahaan. Jurnal Ekonomi dan Bisnis,

Vol. 6, No. 3 November 2012 Hal. 203-214.

Institut Akuntan Publik Indonesia (IAPI). 2013. Standar Profesional Akuntan Publik.

Penerbit Salemba Empat. Jakarta.

_________________________________. 2013. Standar Pengendalian Mutu. Penerbit

Salemba Empat. Jakarta.

Johnson, V.E., Khurana, I.K. & Reynolds, J.K. (2002). Audit Firm Tenure and the Quality

of Financial Reports. Contemporary Accounting Research 19.

Kane, G.D. & Velury, U. (2005). The impact of managerial ownership on the likelihood of

provision of high quality auditing services. Review of Accounting & Finance. 4

(2), 86.

Khadafi, M., Nadirsyah, A., & Syukriy. (2014). Pengaruh Independensi, Etika dan Standar

Audit terhadap Kualitas Audit Inspektorat Aceh. Jurnal Akuntansi, Volume 3,

No. 1, Februari 2014.Kline, R.B., (2010). Principles and Practice of Structural

Equation Modeling. 3rd edition. the Guilford Press. New York London.

Meutia, I. (2004), Pengaruh Independensi Auditor Terhadap Manajemen Laba untuk KAP

Big-5 dan Non Big-5. Jurnal Riset Akuntansi Indonesia. 7(3), 333-350.

Page 9 of 12

Murphy, M.L. (2014). Improving Audit Quality: An Interview with Cynthia M. Fornelli,

an Executive Director of the Center for Audit Quality. The CPA Journal (February 2014).

Pangaribuan, H., Simbolon, R.F., & Simbolon, D., (2016). Kualitas Audit Berdasarkan

Persepsi Auditor Independen. Ekonomis; Jurnal Ekonomi dan Bisnis. Vol. 10,

No. 1. Maret 2016.

Silveira, A.D.M.D. & Barros, L.A.B.D.C. (2006). Correlate Governance Quality and Firm

Value in Brazil. Journal of Financial Economics. at:

http://ssrn.com/abstract=923310

Rapina, Saragi, L.W., & Carolina (2010), Pengaruh Independensi Eksternal Auditor

Terhadap Kualitas Pelaksanaan Audit (Studi Kasus pada beberapa KAP di

Bandung). Akurat Jurnal Ilmiah Akuntansi , No 2 .

Saputra, W. (2015). The Impact Of Auditor‘s Independence On Audit Quality: A

Theoretical Approach. International Journal of Scientific & Technology

Research Volume 4, Issue 12, December 2015.

Singgih, E. M., & Bawono, I.R. (2010). Pengaruh Independensi Pengalaman,Due

Professional Care dan Akuntabilitas terhadap Kualitas Audit.SNA XIII. UJSP.

Purwokerto.

Taqi, M. (2013). Consequences of Audit Quality in Signaling Theory Perspective. GSTF

International Journal on Business Review (GBR). Vol.2 No.4, July 2013.

Tepalagul, N. & Lin L. (2015). Auditor Independence and Audit Quality; A literature

review. Journal of Accounting, Auditing and Finance. Vol. 30, issue 1, 2015.

Tjun, L.T., Marpaunt, E.I. & Setiawan (2012). Pengaruh Kompetensi dan Independensi

Auditor Terhadap Kualitas Audit. Jurnal Akuntansi. Vol.4 No.1 Mei 2012: 33-

56

Velnampy, T., Sivathaasan, N., Tharanika, R. & Sinthuja, M. (2014). Board Leadership

Structure, Audit Committee and Audit Quality: Evidence from Manufacturing

Companies in Sri Lanka. International Journal of Business and Management;

Vol. 9, No. 4. Yuniarti, R., & Zumara, W.M. (2013). Audit Quality Attributes and Audit Client

Satisfaction. International Journal of Humanities and Management Sciences. Volume 1,

issue 1 (2013).

QUESTIONAIRES

A. INDEPENDENCE OF AUDITOR

Please give tick mark () in columns (1 to 5), according to the scale which best suits you.

Variable X Independence Questionnaire No Statement Strongly

Agree

(5)

Agree

(4)

Neither

Agree or

Disagree

(3)

Disagree

(2)

Strongly

Disagree

(1)

Length of Relationship with Client (Audit Tenure)

1 An auditor should have a

relationship with the same

client for at least 3 years

2 I make an effort to stay

independent when auditing

3 I do not report all the

violations that has been done

by my client because of the

Page 10 of 12

length of relationship with my

client

Pressure from the client

4 Sometimes I must act

dishonestly as to not lose my

client

5 If I do not conduct audit well, I

may receive sanctions from

my client

6 I do not report all the

violations that my client has

because I received an

exhortation from my client

7 I am not brave enough to

report my clients violation

because my client may replace

me with another auditor

8 If the audit fee from a client is

a large part of the total revenue

of an accounting firm, then

this will damage the

independence of public

accountants

9 The facilities that I receive

from the client make me hesitant and limits me in

conducting audit

Review of the auditors’ peers (peer review)

10 I do not need reviews from my

peers to assess my auditing

procedure because it there are

no benefits in it

11 I act honestly to avoid

assessment from peers (auditor

peers) in the team

Non-audit services

12 Other than conducting audit

services, an accounting firm

may conduct other services to

the same client

13 I do not easily believe the

clients statements while

conducting audit

14 Non-audit services conducted

to clients may damage the

independence of a public

accountants’ appearance

15 I always make an effort to be

careful in making decisions

while auditing.

Page 11 of 12

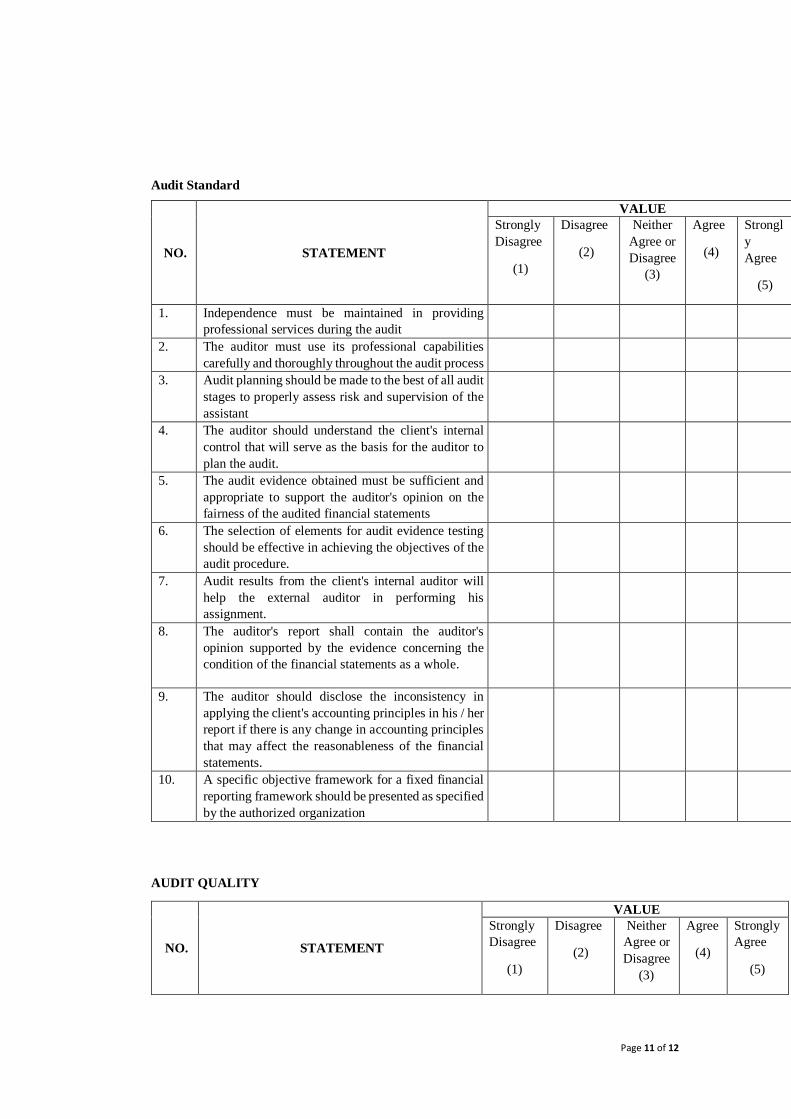

Audit Standard

NO. STATEMENT

VALUE

Strongly

Disagree

(1)

Disagree

(2)

Neither

Agree or

Disagree

(3)

Agree

(4)

Strongl

y

Agree

(5)

1. Independence must be maintained in providing

professional services during the audit

2. The auditor must use its professional capabilities

carefully and thoroughly throughout the audit process

3. Audit planning should be made to the best of all audit

stages to properly assess risk and supervision of the

assistant

4. The auditor should understand the client's internal

control that will serve as the basis for the auditor to

plan the audit.

5. The audit evidence obtained must be sufficient and

appropriate to support the auditor's opinion on the

fairness of the audited financial statements

6. The selection of elements for audit evidence testing

should be effective in achieving the objectives of the

audit procedure.

7. Audit results from the client's internal auditor will

help the external auditor in performing his

assignment.

8. The auditor's report shall contain the auditor's

opinion supported by the evidence concerning the

condition of the financial statements as a whole.

9. The auditor should disclose the inconsistency in

applying the client's accounting principles in his / her

report if there is any change in accounting principles

that may affect the reasonableness of the financial

statements.

10. A specific objective framework for a fixed financial

reporting framework should be presented as specified

by the authorized organization

AUDIT QUALITY

NO. STATEMENT

VALUE

Strongly

Disagree

(1)

Disagree

(2)

Neither

Agree or

Disagree

(3)

Agree

(4)

Strongly

Agree

(5)

Page 12 of 12

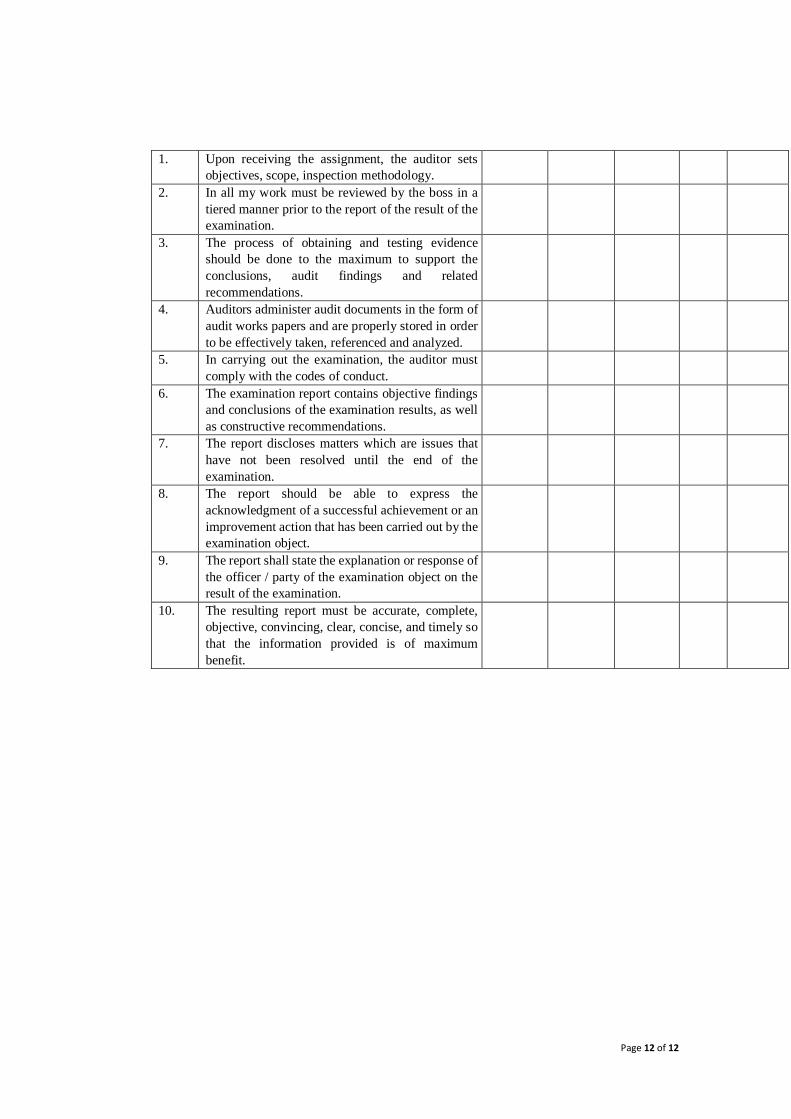

1. Upon receiving the assignment, the auditor sets

objectives, scope, inspection methodology.

2. In all my work must be reviewed by the boss in a

tiered manner prior to the report of the result of the

examination.

3. The process of obtaining and testing evidence

should be done to the maximum to support the

conclusions, audit findings and related

recommendations.

4. Auditors administer audit documents in the form of

audit works papers and are properly stored in order

to be effectively taken, referenced and analyzed.

5. In carrying out the examination, the auditor must

comply with the codes of conduct.

6. The examination report contains objective findings

and conclusions of the examination results, as well

as constructive recommendations.

7. The report discloses matters which are issues that

have not been resolved until the end of the

examination.

8. The report should be able to express the

acknowledgment of a successful achievement or an

improvement action that has been carried out by the

examination object.

9. The report shall state the explanation or response of

the officer / party of the examination object on the

result of the examination.

10. The resulting report must be accurate, complete,

objective, convincing, clear, concise, and timely so

that the information provided is of maximum

benefit.

![AUDiToR inDEPEnDEnCE 9 - ANU Presspress-files.anu.edu.au/downloads/press/p127531/pdf/ch0921.pdf · AUDiToR inDEPEnDEnCE 9 [T] ... most debated aspects in the maintenance of auditor](https://img.dokumen.tips/doc/110x75/5b4fed8a7f8b9a166e8d6686/auditor-independence-9-anu-presspress-filesanueduaudownloadspressp127531pdf.jpg)

![[2009] Audit Committee and Auditor Independence - Banker's Perception](https://img.dokumen.tips/doc/110x75/557213bc497959fc0b92e493/2009-audit-committee-and-auditor-independence-bankers-perception.jpg)