Embed Size (px)

Citation preview

ARE INTEREST RATE SPREADS IN JAMAICA TOO LARGE? VIEWS FROM WITHIN THEFINANCIAL SECTORAuthor(s): David TennantSource: Social and Economic Studies, Vol. 55, No. 3 (September 2006), pp. 88-111Published by: Sir Arthur Lewis Institute of Social and Economic Studies, University of the WestIndiesStable URL: http://www.jstor.org/stable/27866472 .

Accessed: 15/06/2014 06:42

Your use of the JSTOR archive indicates your acceptance of the Terms & Conditions of Use, available at .http://www.jstor.org/page/info/about/policies/terms.jsp

.JSTOR is a not-for-profit service that helps scholars, researchers, and students discover, use, and build upon a wide range ofcontent in a trusted digital archive. We use information technology and tools to increase productivity and facilitate new formsof scholarship. For more information about JSTOR, please contact [email protected].

.

University of the West Indies and Sir Arthur Lewis Institute of Social and Economic Studies are collaboratingwith JSTOR to digitize, preserve and extend access to Social and Economic Studies.

http://www.jstor.org

This content downloaded from 195.78.109.66 on Sun, 15 Jun 2014 06:42:57 AMAll use subject to JSTOR Terms and Conditions

Social and Economic Studies 55:3 (2006): 88-111 ISSN: 0037-7651

ARE INTEREST RATE SPREADS IN

JAMAICA TOO LARGE? VIEWS FROM

WITHIN THE FINANCIAL SECTOR

David Tennant

ABSTRACT

The size of interest rate spreads, particularly for Jamaican commercial

banks, has been heavily debated in the media. This paper explores the issue

by highlighting results of a comprehensive survey analysis of key stakeholders in the Jamaican financial sector, as to whether interest rate

spreads are too large, reasons for the size of the spreads, and suggestions

for reducing them. It also seeks to ascertain whether the views highlighted can be validated by financial and economic data. It was found that while

most financial institution managers argue that the spreads are justified by current economic, regulatory and social conditions, a few others, along with the regulators and policy-advisors, are insistent that the spreads are

fuelled by inefficiency and greed. Greater macroeconomic stability, reduced

government borrowing on the local market, heightened competition within

the financial sector, and increased operational efficiency by financial institutions have been advocated.

The size of interest rate spreads, particularly for Jamaican commercial banks, has been heavily debated in the media. This

debate is, however, part of a broader analysis as to the importance of financial institutions' operational efficiency to a country's economic growth. It is generally accepted in the literature that a

more efficient financial system benefits the real economy by

allowing 'higher expected returns for savers with a financial

surplus, and lower borrowing costs for investing in new projects that need external finance' (Quaden 2004: 2). The spread between a

financial institution's lending and deposit rates is therefore a key indicator of that institution's efficiency, and, more importantly, of its

potential impact on economic growth.1 If this spread is large, it will

1 Ngugi (2001: 1) illustrates by noting that under perfect competition the interest

rate spread is narrower, composed only of the transaction cost, while in an

imperfect market, the spread is wider, reflecting inefficiency in market operation.

This content downloaded from 195.78.109.66 on Sun, 15 Jun 2014 06:42:57 AMAll use subject to JSTOR Terms and Conditions

Are Interest Rate Spreads In Jamaica Too Large? 89

discourage potential savers due to low returns on deposits, limit

financing for potential borrowers, and will reduce feasible investment opportunities, thus limiting future growth potential

(Ndung'u and Ngugi 2000). The size of the interest rate spread is therefore a critical

consideration for developing countries, many of which have

experienced low or stagnating economic growth rates in the past few decades. This is even more so, as Chirwa and Mlachila (2004:

98) note that interest rate spreads in developing countries have been

persistently high. Ngugi (2001:1) argues that this is because of two

pervasive features of LDC financial sectors ? high administrative

costs and low competition ? both of which are incentives for

financial institutions to unduly increase lending rates. Prominent

political and private sector stakeholders in the Jamaican economy have recently been expressing such concerns, and forcefully argue that the interest rate spreads of major financial institutions

operating in Jamaica are not justified by current economic

conditions, and are much larger than those of counterpart institutions in other countries.

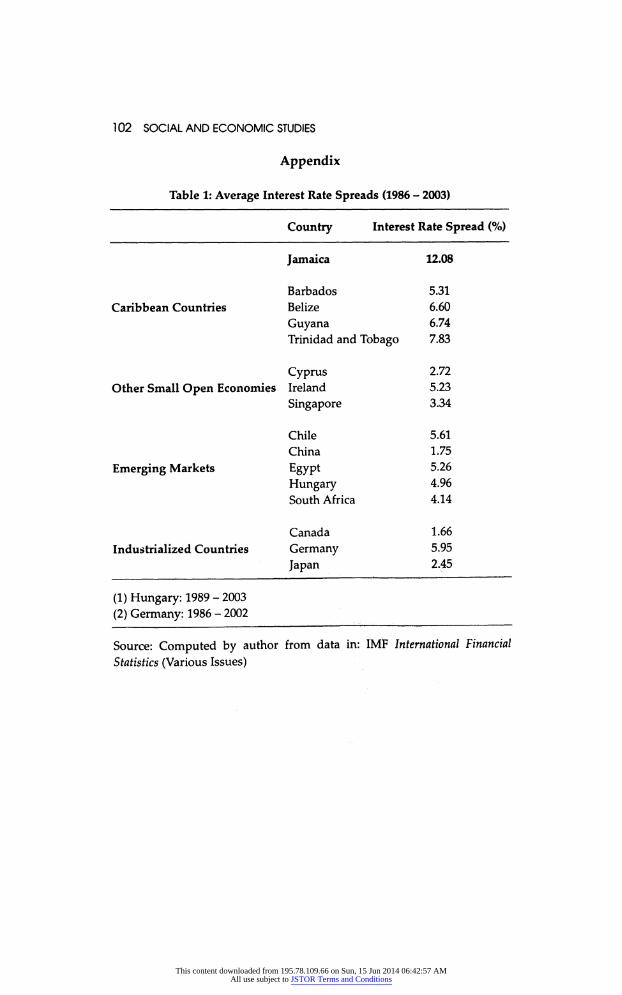

A cross-country comparison of interest rate spreads seems to

provide some support for this view. In Table 1 (see Appendix), IFS

data was used to calculate the average interest rate spreads in 15

countries for the period 1986-2003. The countries examined include

Caribbean territories, other small open economies, emerging market economies, and industrialized countries. The figures clearly show that Jamaica's average interest rate spread of 12.08% is

significantly higher than the spreads of any of the other countries.

In fact, Jamaica was the only country with a double-digit average interest rate spread, as the country with the next largest spread was

Trinidad and Tobago (7.83%). A comparison of average interest rate spreads across types of

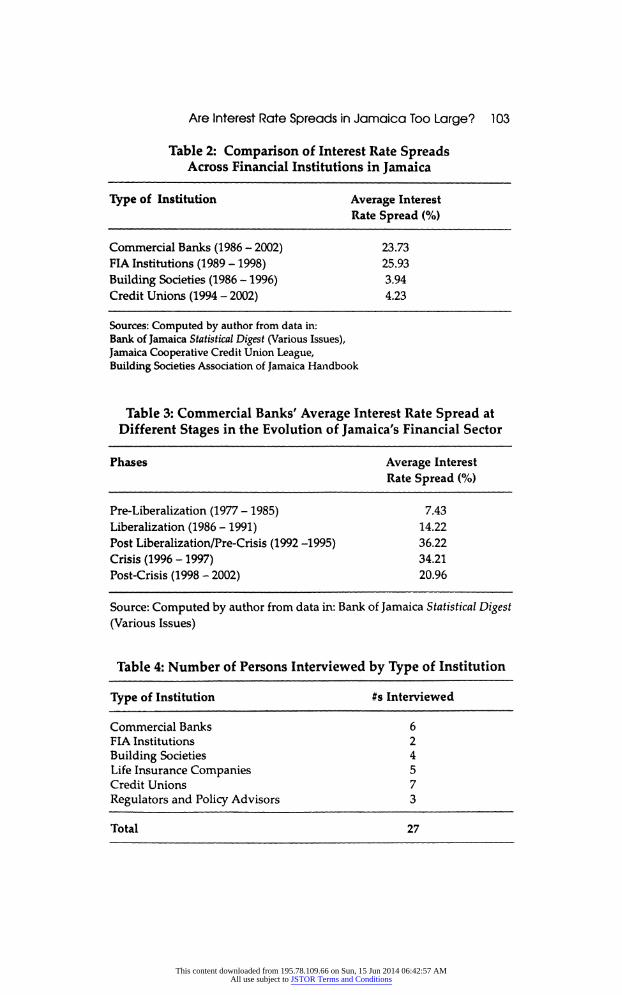

institutions within Jamaica also reveals interesting results. Table 2

shows that Jamaican building societies and credit unions were both

able to maintain significantly lower interest rate spreads (3.94% and

4.23%, respectively) than commercial banks (23.73%) and FIA

Institutions2 (25.93%), in the same economic environment. While it

may be argued that commercial banks are disadvantaged in this

respect because of their obligation to meet liquid asset reserve

2 Merchant banks, finance houses and trust companies.

This content downloaded from 195.78.109.66 on Sun, 15 Jun 2014 06:42:57 AMAll use subject to JSTOR Terms and Conditions

90 SOCIAL AND ECONOMIC STUDIES

requirements, one must question whether this can justify their

spread being approximately six times larger than that of building societies and credit unions.

Such data fuels the argument that the relatively high interest rate spreads of the dominant lending institutions in the Jamaican financial sector has had a stifling impact on real sector activities.

Barnes and Stewart (1996: 18) note that the resultant high cost of

loanable funds "presented an obstacle to productive investments

and is partly responsible for the poor performance of the productive sectors of the Jamaican economy." This, however, is only one side

of the story, as many financial institution managers have publicly

argued that their spreads are justified and should not be compared with those of financial institutions in other countries, as there are

numerous factors unique to the business environment in Jamaica that must be considered. While popular, this view is not

unanimously held even within the financial sector, as there are

some managers, who, along with the regulators and policy-makers, believe that unduly high levels of inefficiency and greed are

responsible for the current size of the interest rate spreads. This paper explores the issue further by highlighting the

results of a comprehensive survey analysis of the views of

managers, regulators and policy advisors in the Jamaican financial

sector, as to whether the interest rate spreads are indeed too large, the reasons for the size of the spreads, and their suggestions for

reducing the spreads in Jamaica. It also seeks to ascertain whether

the views highlighted can be validated by relevant data. The next

section provides the contextual background to this study by briefly

outlining the basic stages in the evolution of Jamaica's financial

sector and the corresponding changes in the interest rate structure.

This will be followed by a brief description of the methodology used. The analysis of the data will then be highlighted in three

sections: the managers' views about and explanations of the size of

interest rate spreads in Jamaica will be presented first; the

managers' suggestions for reducing the spreads will be highlighted next; and finally the views and responses of regulators and the

policy advisors to the Minister of Finance and Planning will be

summarized.

This content downloaded from 195.78.109.66 on Sun, 15 Jun 2014 06:42:57 AMAll use subject to JSTOR Terms and Conditions

Are Interest Rate Spreads In Jamaica Too Large? 91

Interest Rate Spreads and the Evolution of Jamaica's Financial

Sector

The Jamaican financial sector has undergone five distinct phases in

its development ?

pre-liberalization, liberalization, post-liberaliza

tion/pre-crisis, crisis, and post-crisis (Kirkpatrick and Tennant 2002:

1934). In each of these phases there were changes in the interest

rates being applied by the major financial institutions, as

determined by either the prevailing legislation or market

conditions. In the pre-liberalization phase, between the 1970s and early

1980s, financial repression was strong in Jamaica. The financial

system operated within a highly regulated environment aimed at

constraining the growth of the money supply (McBain 1997: 145). The average interest rate spread for commercial banks during this

period was therefore a relatively small 7.43% (See Table 3). This

figure, however, almost doubled (to 14.22%) during the years in

which the financial sector was being liberalized, as savings rates

were totally deregulated, with the commercial banks now being authorised to set their own rates (Lim 1991:12 & 38).

In the period immediately following financial liberalization in

Jamaica, there was 'rapid asset expansion and deepening within the

financial sector, with the operations of commercial banks and non

bank financial institutions (NBFIs) increasing significantly'

(Kirkpatrick and Tennant 2002: 1935).3 This expansion did not,

however, lead to a proportionate increase in competition in the

sector, because of the continued dominance of a few institutions,4 and the emergence of large financial conglomerates.5 The

combination of low competition and high demand for credit in the

3 The number of commercial bank branches increased from 154 in 1985 to 201 in

1993 (Peart 1995: 13), and their asset portfolio grew by an average 48.5% in the

early 19$0s (Stennett et al 1998:11). Additionally, the number of NBFIs increased from 8 in 1985 to 25 in 1993, with their assets increasing in nominal terms from

J$1.4 billion in 1986 to J$11.4 billion in 1993 (Peart 1995:15). 4 At the end of 1997, the assets of commercial banks totalled J$142.4 billion,

representing 50% of the total assets of the financial sector, and of this amount,

three large banks accounted for J$106.8 billion or 75% (Stennett et al 1998: 11).

5 These conglomerates were usually composed of a merchant bank, a commercial

bank, a building society, an insurance company and other business firms. They often had complex structures of inter-company share holdings, interlocking boards of directors, common management and extensive inter-group transactions

(Stennett et al 1998:12).

This content downloaded from 195.78.109.66 on Sun, 15 Jun 2014 06:42:57 AMAll use subject to JSTOR Terms and Conditions

92 SOCIAL AND ECONOMIC STUDIES

post-liberalization era fuelled further increases in the commercial

banks' interest rate spread, which averaged 36.22% between 1992

and 1995.

The inefficiencies in the financial sector eventually resulted in

illiquidity and insolvency problems for numerous financial

institutions. The consequent financial sector crisis of the mid to late

1990s, and government intervention to prevent a collapse of the

system, did not, however, immediately result in major changes to

the commercial banks' average interest rate spread. Between 1996

and 1997, the rate only marginally declined to 34.21%. More

significant reductions in the commercial banks' interest rate spreads were eventually realized in the post-crisis period, after the

government, through the Financial Sector Adjustment Company (FINSAC), introduced measures to restructure and consolidate the

sector. Between 1998 and 2002, commercial banks' average interest

rate spread declined to 20.96%. Questions, however, still remain as

to whether or not the spreads have now fallen to reasonable levels, or whether the calls for further reductions are justified.

Methodology The information used in the survey analysis was extracted from a

broader study on the impact of financial sector intermediation on

economic performance (Tennant 2004). Key stakeholders in the

Jamaican financial sector were interviewed. The target population consisted of managers and regulators of commercial banks, FIA

institutions, building societies, credit unions and life insurance

companies, and the policy-advisors to the Minister of Finance and

Planning (who has overall responsibility for the financial sector).

Attempts were made to interview the person with the highest position in each of the targeted institutions, as they have decision

making powers in the institutions and so would influence the path taken by the entities.

For all the institutions except credit unions, the need for

sampling was obviated, as it was possible to conduct the survey on

the entire population. The response rate was high (87.5%), with

interviews being conducted with highly-ranked managers in all the

commercial banks and building societies, five of the six life

This content downloaded from 195.78.109.66 on Sun, 15 Jun 2014 06:42:57 AMAll use subject to JSTOR Terms and Conditions

Are Interest Rate Spreads in Jamaica Too Large? 93

insurance companies,6 three of the five FIA Institutions,7 and all the senior regulators and policy-advisors approached.8

Sampling was therefore only needed for credit unions, as with 55 registered credit unions scattered across the island, a census

survey was not possible. In selecting the sample for this study a

crucial criterion was the potential influence that the credit unions

could have on the broader economy, as represented by the breadth

of their membership. Credit union data clearly shows that the

distribution of the number of members across credit unions is

heavily skewed, with the largest three credit unions having 41.5% of

total membership as at December 2002. This is because many of the

small credit unions are bonded to serve very limited groups of

people in small organizations or communities. As such, a decision was taken to select from the sampling frame9 only those credit

unions with more than one branch office. This use of purposive

sampling limited the number of credit unions in the sample to seven

institutions.10 A 100% response rate was achieved, and in terms of

membership, the sample selected represented 46.83% of the total

number of credit union members.11

A total of 27 interviews were conducted with the most

influential stakeholders in the Jamaican financial sector. In

managing the data garnered from these interviews, processing errors were minimized by ensuring accuracy in recording the

respondents' responses, and by exercising extreme care in

analyzing these responses. The answers to each question were

carefully coded, and SPSS was used to analyze the data. Data entry was independently verified so as to ensure accuracy.

6 Which currently offer life insurance products.

7 The manager of one of these FIA institutions is also the manager of the

commercial bank within the group of companies, and he noted that the

operations of the merchant bank were basically subsumed under that of the

commercial bank, even though the merchant bank is still registered with the BOJ. As such, the responses of only two FIA institution managers will be reported.

8 Table 4 outlines the number of persons interviewed from each type of institution.

9 The Yellow Pages Listing in the national telephone directory.

10 The use of purposive sampling for the credit unions precludes the traditional

tests of significance, and implies that the study is limited in terms of its ability to

precisely represent the population of credit union managers.

11 Figures were taken from The Jamaica Co-Operative Credit Union League Ltd.

Annual Report (2002), and the St. Ann Co-Operative Credit Union Ltd. Annual

Report (2003).

This content downloaded from 195.78.109.66 on Sun, 15 Jun 2014 06:42:57 AMAll use subject to JSTOR Terms and Conditions

94 SOCIAL AND ECONOMIC STUDIES

Attempts were also made to ascertain whether any claims

made by the respondents could be validated by relevant data.

Whenever factors were highlighted by the respondents for which

reliable data was available, such data was analyzed and conclusions

made as to the veracity of the claims. The Bank of Jamaica's Statistical Digest was the primary source for data on financial and

macroeconomic indicators.

Managers' Views About and Explanations of the Size of Interest

Rate Spreads in Jamaica

The interest rate spreads of financial institutions has recently been

a heavily debated topic in Jamaican society. The Minister of Finance

and Planning and the Head of the Jamaica Manufacturers'

Association have repeatedly called for financial institutions to

reduce their spreads, but many managers of such institutions feel

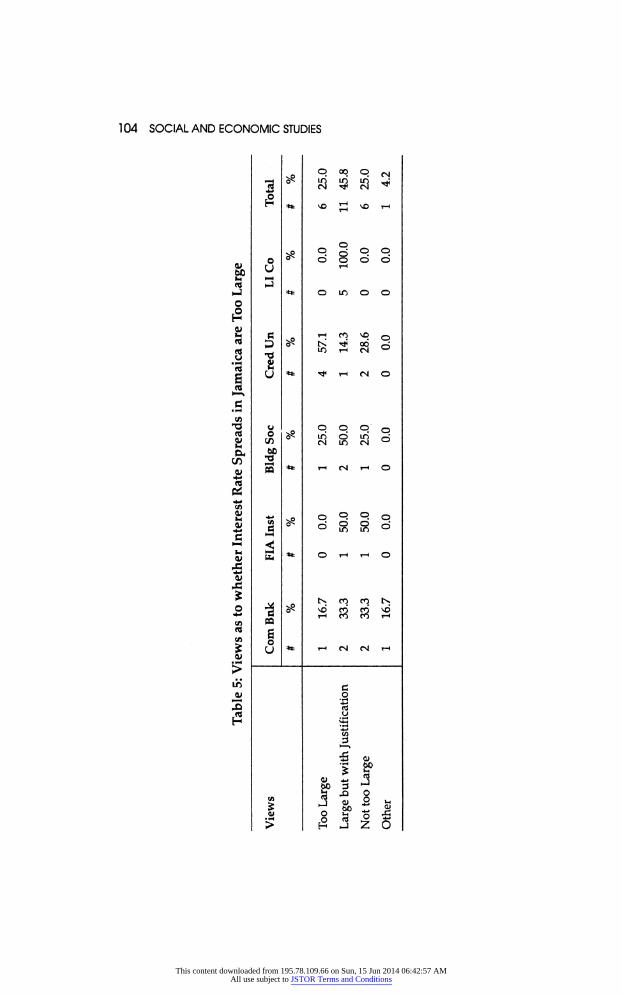

that this is an unreasonable request. The controversy surrounding this issue is highlighted when the managers' views as to whether

the interest rate spreads in Jamaica are indeed too large, are

summarized (see Table 5). Whilst 25% of the managers believe that

the spreads, while not large for all institutions, are generally too

large in the sector as a whole, an equal number of managers hold

the opposite view, insisting that the spreads are not too large. Almost half (45.8%) of the managers however, have taken the

middle ground by asserting that while large, the spreads are

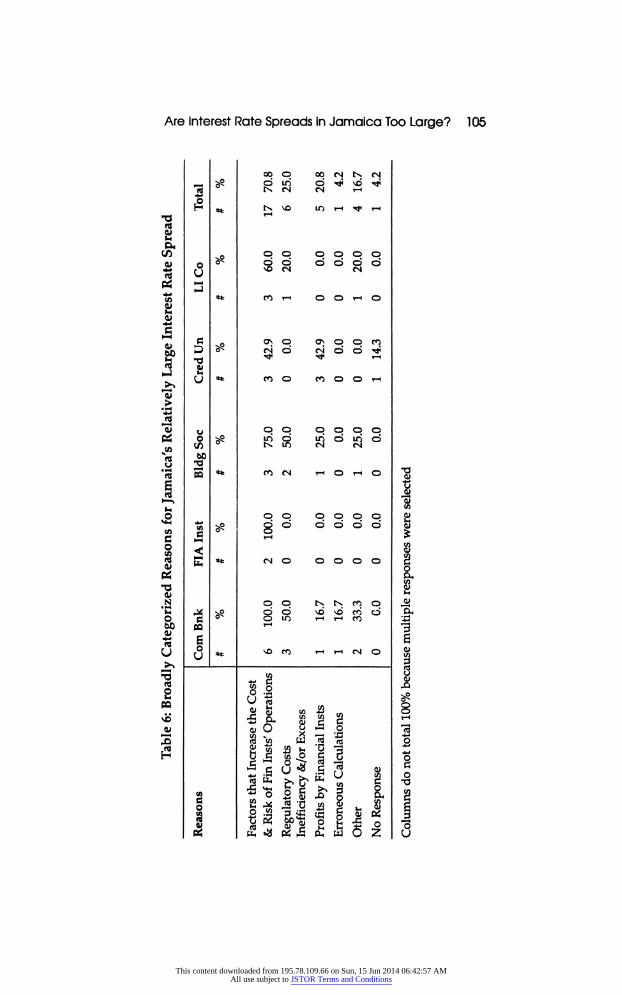

justifiable. When the reasons given for the Jamaican financial institutions'

relatively large spreads are broadly categorized (see Table 6), it is

interesting to note that 70.8% of the managers believe that the

financial institutions' spreads are simply a reflection of a plethora of

factors that increase the cost and risk of their operations, and a

further 25% identify various regulatory costs as factors

necessitating the large spreads. Only 20.8% of the managers

(representing three credit unions, one building society and one

commercial bank) accepted that the size of the spreads is reflective

of the operational inefficiency and at times excessive profits by financial institutions.

In fact, when the managers' more specific explanations for the

relatively large spreads are detailed (see Table 7), the most popular

explanation is that it is more expensive and risky to do business in

This content downloaded from 195.78.109.66 on Sun, 15 Jun 2014 06:42:57 AMAll use subject to JSTOR Terms and Conditions

Are Interest Rate Spreads in Jamaica Too Large? 95

Jamaica than in some other countries. It was noted that costs have

been increasing, many of which the financial institutions do not

have complete control over. These costs include security (because of the crime and violence prevalent in Jamaica), utilities (because of

the rising price of oil), and wages (because of the unionized environment in which financial institutions operate).

Some managers (29.2%) also argued that spreads have to be

large so as to protect financial institutions from risks associated

with operating in an unstable macroeconomic environment. Many

specifically identified volatility of interest rates as a factor which

forces them to maintain large spreads, as they are never completely sure of the direction being taken by the Central Bank. The added

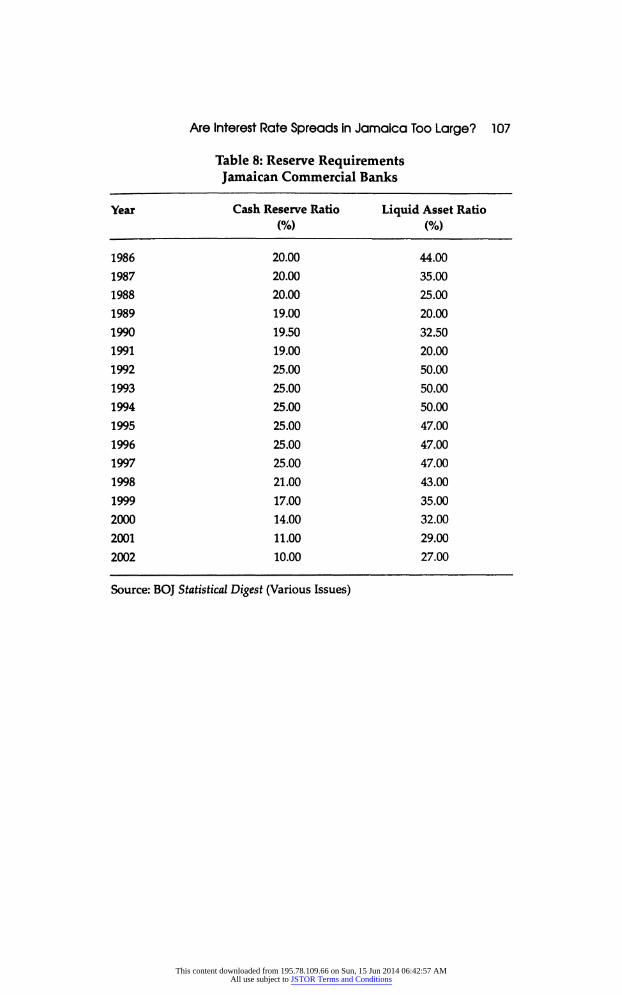

cost of high reserve requirements was also highlighted by 25% of the managers as one of the reasons for the large interest rate

spreads. This was, however, rejected as a non-issue by a commercial

bank manager and a building society manager, who both noted that

the reserve requirements are now much lower than they were in the

past. This seems to be supported by figures extracted from the Bank

of Jamaica's Statistical Digest, which show that commercial banks'

cash reserve ratio fell significantly from a maximum of 25%

between 1992 and 1997, to 10% in 2002, as did the liquid asset ratio,

from 50% between 1992 and 1994, to 27% in 2002 (see Table 8). The other controversial and relatively unpopular reasons

given for the large spreads include excessive profiteering by some

financial institutions (12.5%), and the high levels of operational

inefficiency within some financial institutions (12.5%). The issue of

operational efficiency was investigated further, as managers were

specifically questioned as to whether operational costs have been

increasing. All but two of the managers noted that such costs have

increased, but in spite of this, 37.5% of the institutions reported

improved efficiency/productivity ratios. It was noted that the types of costs that have been increasing are varied, but amongst the most

prevalent are staff and administrative costs (identified by 45.8% of

managers), and utilities (29.2%). A few other managers, however,

identified reasons for the relative inefficiency of Jamaican financial

institutions that were completely out of their control, including the

lack of economies of scale (caused by the small market size), the

customers' demand for inefficient services (such as passbooks and

personalized service), and the absence of infrastructure to aid in the

This content downloaded from 195.78.109.66 on Sun, 15 Jun 2014 06:42:57 AMAll use subject to JSTOR Terms and Conditions

96 SOCIAL AND ECONOMIC STUDIES

efficient assessment of loan applications (particularly credit

bureaus).

Managers7 Suggestions for Reducing Interest Rate Spreads in

Jamaica

The reasons for the size of interest rate spreads that were identified

by the managers have led to numerous suggestions as to how they should be reduced. When broadly categorized these suggestions are instructive as to who the managers believe should bear the

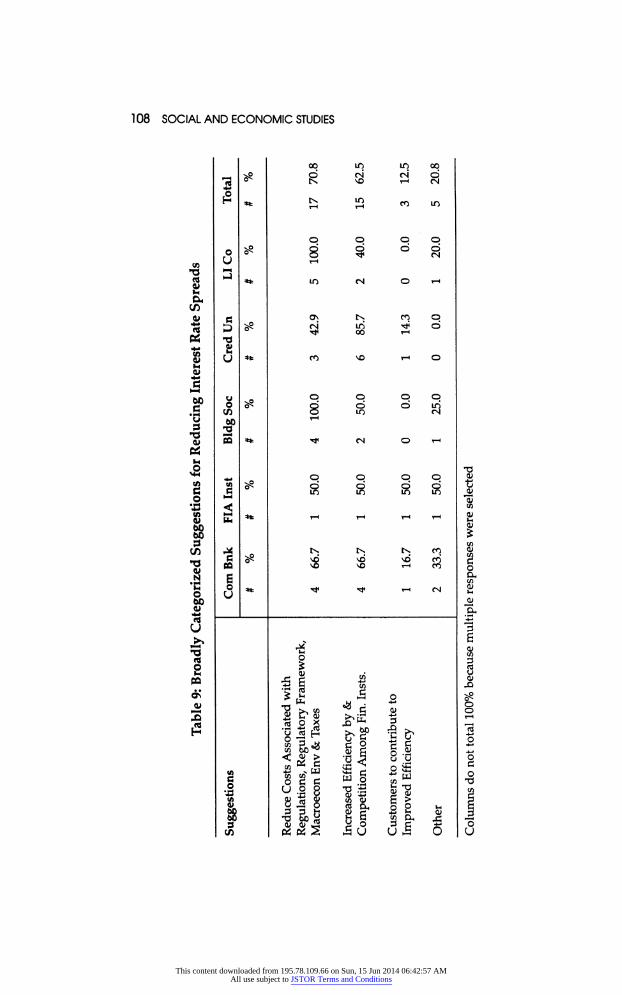

responsibility for reducing the spreads in Jamaica (see Table 9). Over two-thirds (70.8%) of the managers noted that if interest rate

spreads in Jamaica are to be narrowed, the government would first have to reduce a variety of costs associated with the regulations and

regulatory framework, the macroeconomic environment, and

taxation. Interestingly though, a fairly large number of managers

(62.5%), although reluctant to admit much responsibility for the size

of the spreads, accepted that the reduction of the spreads would

also require increased operational efficiency by and competition

amongst financial institutions. A few managers further noted that

the customers would have to bear some of the responsibility for the

eventual lowering of the interest rate spreads in Jamaica. When the more detailed breakdown of the managers' specific

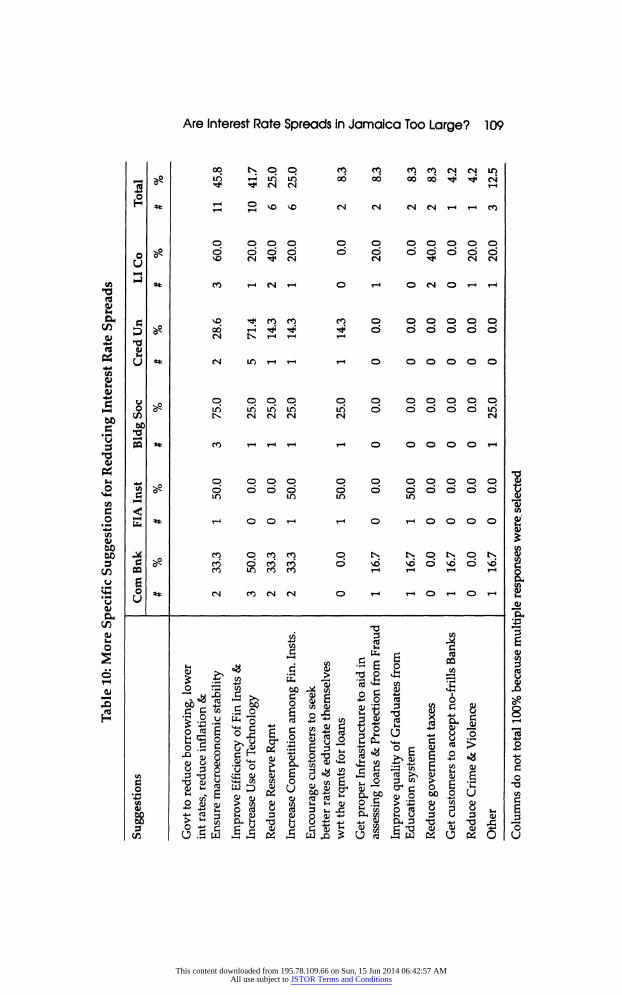

suggestions was examined (Table 10), it was evident that the

solution most commonly identified (by 45.8% of the managers) was

for the government to take measures to improve the

macroeconomic environment. This included reducing its borrowing on the local market, lowering interest and inflation rates, and

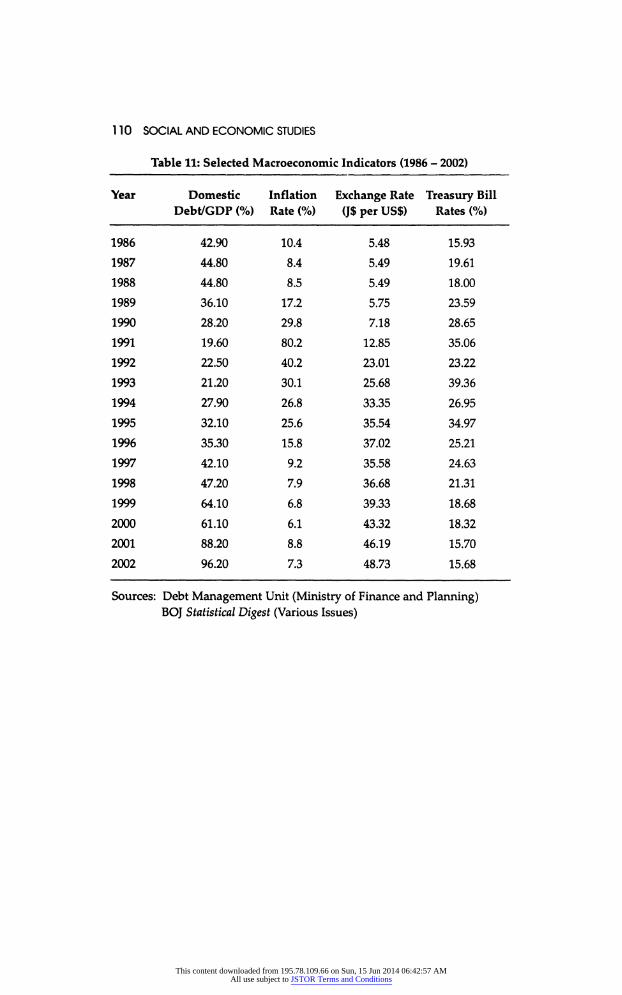

ensuring stability of the major macroeconomic variables. An

examination of a few key macroeconomic variables for Jamaica (see Table 11) confirms that the country's domestic debt to GDP ratio has

been increasing and was almost 100% in 2002. It, however, was also

evident that exchange rates have been reasonably stable in the past few years, and, more importantly, that Treasury Bill and inflation

rates have been consistently and significantly reduced since 1995.

Commercial bank managers would argue though that they have

decreased their spreads in line with the reductions in the Treasury Bill rates, as between 1995 and 2002, commercial bank interest rate

spreads declined by 57%, while Treasury Bill rates fell by 55%. This

would seem to support the managers' argument that a further

This content downloaded from 195.78.109.66 on Sun, 15 Jun 2014 06:42:57 AMAll use subject to JSTOR Terms and Conditions

Are Interest Rate Spreads in Jamaica Too Large? 97

lowering of interest rates would foster greater narrowing of their

spreads.

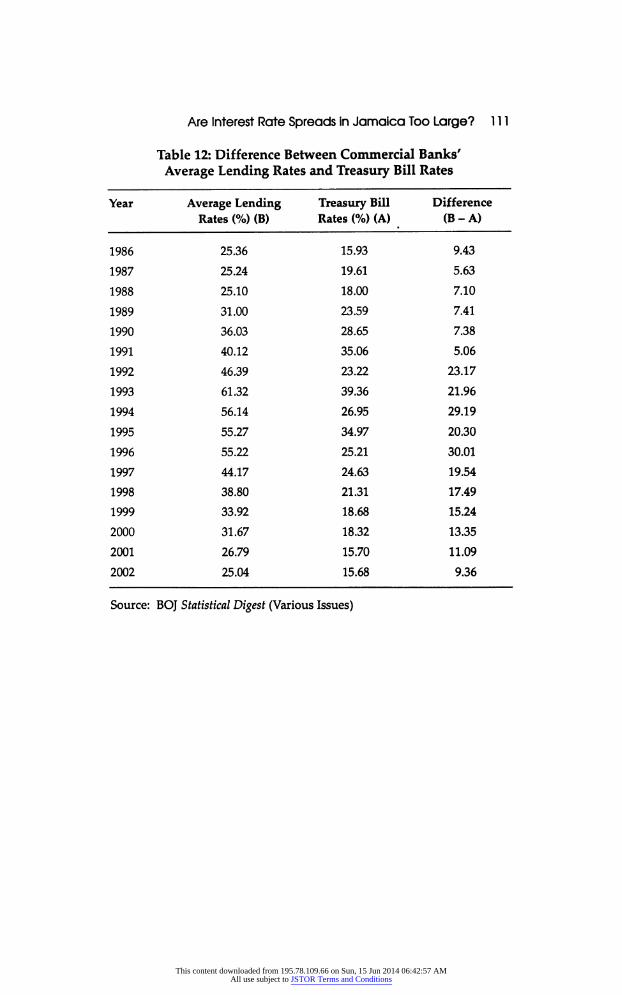

It, however, does not provide an adequate explanation as to

why, in an environment of relative macroeconomic stability and low

interest cost of funds, the commercial banks' average lending rate is

consistently much higher than the governments' Treasury Bill rate.

Between 1995 and 2002, the commercial banks' lending rate was on

average 17.05 percentage points higher than the governments'

Treasury Bill rate (see Table 12). It must be noted though that this

difference has also been trending downwards, ranging from a

maximum of 30.01% in 1996 to a minimum of 9.36% in 2002.

Another popular suggestion for reducing interest rate spreads

(identified by 41.7% of the managers) was that financial institutions

should make efforts to improve their own efficiency, particularly by

seeking technological means of reducing costs. In this respect, the

measures already being utilized by some of the managers include

encouraging increased usage of ATMs and e-financial services so as

to cut down on staff costs, and using the intranet and emails so as

to reduce telephone and stationery costs. The utilization of

technology has also been useful in facilitating cost reductions

through rationalization of facilities, practices and service delivery methods. Here a few of the managers noted that cash points (ATMs) were used to replace full service branches in areas where the

customer base was not large enough to justify continued operations, and certain functions (such as accounting) were centralized so as to

preclude the need for each branch to have their own specialized staff. One manager however cautioned that institutions should

resist the temptation of going overboard with this, as there will be

serious economic and social implications if technology is used to

replace significant numbers of staff in a labour-abundant society. It was also argued (by 25% of the managers) that increased

operational efficiency would automatically result from heightened

competition amongst the financial institutions, especially if more

international players enter the market. Such competition would

force the institutions to reduce costs by employing a number of

cost-containing and cost-reducing measures. In this regard, almost

half of the managers noted that they were already taking the basic

step of carefully monitoring expenses and reducing wastage. One

manager however insisted that this measure will only yield sustained positive results if conscientiously applied to all expenses.

This content downloaded from 195.78.109.66 on Sun, 15 Jun 2014 06:42:57 AMAll use subject to JSTOR Terms and Conditions

98 SOCIAL AND ECONOMIC STUDIES

A mistake commonly made is to focus only on the large items of

expenditure, but it was argued that simple things such as

conserving on electricity and stationery, and cutting canteen

expenses can yield significant results. It was also noted that for any of these measures to be successful the commitment of the staff was

essential. In order to ensure that the staff implemented the planned measures, productivity-based salary incentives and profit-share schemes were seen as essential, as was an effective communication

system. Other innovative means by which operational efficiency can

be improved included the attempts by some managers to achieve

economies of scale by merging with other institutions thereby

making the customer base bigger, outsourcing parts of the business

to independent service providers so as to reduce administrative

costs, and the appointment of a conservation officer/committee to

focus solely on identifying areas in which costs can be reduced.

A quarter of the managers also strongly argued for a reduction

of the reserve requirement as a means of reducing the interest rate

spread, noting that financial institutions have a history of reducing their interest rates when the requirements were previously

dropped. The data however suggests that this rate of reduction is

less than proportional, as even though between 1995 and 2002 the

cash reserve and liquid assets ratios fell by 60% and 43%,

respectively, the commercial banks' interest rate spread declined by

only 57%.

A few managers also noted that their customers could

contribute to the lowering of the interest rate spreads by shopping around for better rates instead of blindly continuing with the

traditional institutions, and by accepting financial institutions that

offer quality low-cost services without the 'extra frills' (such as posh branch offices and large numbers of tellers) that are now

commonplace in Jamaica. It was also argued that the customers

could contribute to the lowered cost of assessing loan applications

by familiarizing themselves with the standard loan requirements. Also important in this respect is the need to have the proper infrastructure (such as credit bureaus) to aid in assessing loan

applications, thereby improving the efficiency of the sector and

reducing the need to maintain large spreads to buffer against the

risks of bad debt and fraud.

This content downloaded from 195.78.109.66 on Sun, 15 Jun 2014 06:42:57 AMAll use subject to JSTOR Terms and Conditions

Are Interest Rate Spreads In Jamaica Too Large? 99

Views and Responses of the Regulators and Policy-Advisors

The regulators and policy-advisors all firmly hold the view that interest rate spreads charged by many local financial institutions are too high and do not reflect the downward trending inflation rates. They either rejected or minimized the significance of all the

justifications highlighted by the managers, and insisted that the

spreads should be reduced. For example, one* respondent within

this group noted that volatility in the economy has been high, but

argued that it can only explain a small percentage of the margins, while another insisted that such volatility has long since been

reduced and should no longer be a factor. The regulators and policy advisors were also adamant that the managers' argument that the

spreads are high because of high reserve requirements is critically weakened by the fact that even though these requirements had been

significantly reduced, spreads were not appreciably impacted. Furthermore, while they concede that the cost of doing business in

Jamaica may be relatively high and is exacerbated by the lack of

economies of scale, they note that this can only explain a small

portion of the spreads being charged. One respondent within the regulatory and advisory group

instead argued that the large spreads are being driven by administrative inefficiencies, largely caused by the huge wage and

salary bills incurred by many institutions. It was noted that the ratio

of administration costs to total assets for some Jamaican financial

institutions is considerably higher than their counterparts elsewhere in the world. This respondent did not agree with the

view that the financial institutions are making super-profits, but

confirmed that they are viable, and asserted that their means of

achieving that viability without having improved their operational

efficiency is by charging high lending rates. Other regulators and

policy advisors, however, were not as charitable and insisted that

greed and the desire to make excessive profits was also one of the

factors driving the size of the spreads. The regulators and policy advisors were therefore unwavering

in their insistence that the Jamaican borrowers are being

overcharged. Their suggestions for reducing the spread included

the need for financial institutions to reduce their administrative

costs (particularly wages and salaries), and for heightened

competition in the sector (which has to be balanced with the need

for ensuring the safety of depositors' funds).

This content downloaded from 195.78.109.66 on Sun, 15 Jun 2014 06:42:57 AMAll use subject to JSTOR Terms and Conditions

100 SOCIAL AND ECONOMIC STUDIES

Conclusion

There is wide divergence between the views of some of the financial

institution managers, and the regulators and policy advisors on the issue of interest rate spreads in Jamaica. Whilst most managers

strongly argue that the spreads being applied are justified by current economic, regulatory and social conditions, a few others,

along with the regulators and policy advisors, are insistent that the

spreads are being fuelled by inefficiency and greed. The most

common justifications given for the commercial banks' relatively

large interest rate spreads include the uniquely high costs and risks

associated with conducting business in Jamaica, macroeconomic

instability, and high reserve requirements. These factors, however, are downplayed by a few managers, and regulators and policy advisors as being exaggerated or simply irrelevant.

This study has shown that whereas there is no imminent

resolution to the debate as to whether or not interest rate spreads in

Jamaica are justifiable, there is agreement on some of the measures

that can be taken to reduce these spreads. Most respondents

suggested that greater macroeconomic stability, reduced

government borrowing on the local market, heightened

competition within the financial sector, and increased operational

efficiency by the respective financial institutions, should be

pursued. More innovative means of reducing interest rate spreads were also suggested. These include the introduction of a credit

bureau to reduce risks and costs associated with bad debt and

fraud, and concerted efforts to increase public acceptance of

financial institutions that offer core services, without added costly frills.

References

Bank of Guyana, Statistical Bulletin, Various Issues.

Bank of Jamaica, Statistical Digest, Various Issues.

Barnes, Ainsworth and Stewart, Robert (1996). "Financial Sector

Developments and Economic Performance: The Jamaica Experience."

Paper Presented at the XXVIII Annual Conference on Monetary Studies, Trinidad and Tobago, October 28 - November 1,1996.

Central Bank of Barbados, Annual Statistical Digest, Various Issues.

Central Bank of Belize, Statistical Digest, Various Issues.

This content downloaded from 195.78.109.66 on Sun, 15 Jun 2014 06:42:57 AMAll use subject to JSTOR Terms and Conditions

Are Interest Rate Spreads in Jamaica Too Large? 101

Central Bank of Trinidad and Tobago, Statistical Digest, Various Issues.

Chirwa, Ephraim W. and Milachila, Montfort (2004). "Financial reforms and interest rate spreads in the commercial banking system in Malawi." IMF Staff Papers, v. 51(1): 96-117.

Green, Pauline M. (1999). "Preserving the integrity of the Jamaican financial

system: The challenges." Paper prepared for the Central Bank

responsibility for financial stability workshop.

International Monetary Fund, International Financial Statistics, Various Issues.

Jamaica Co-Operative Credit Union League (2002). Annual Report, Jamaica

Co-Operative Credit Union League: Kingston.

Kirkpatrick, Colin and Tennant, David (2002). "Responding to financial crisis: The case of Jamaica." World Development, v. 30(11): 1933-1950.

Lim, Gail Lue (1991). "Jamaica's financial system: Its historical

development." Paper presented at the Meeting of the Regional Programme of Monetary Studies.

McBain, Helen (1997). "Factors influencing the growth of financial services in Jamaica." Social and Economic Studies v. 46(2&3): 131-167.

Ndung'u, Njuguna and Ngugi, Rose W. (2000). "Banking sector interest rate spread in Kenya." www.kippra.org/Download/interest.doc.

Ngugi, Rose W. (2001). "An Empirical Analysis of Interest Rate Spread in

Kenya." www.aercafrica.org/documents/rpl06.pdf.

Peart, Kenloy (1995). "Financial system reform and financial sector

development in Jamaica." Social and Economic Studies, v. 44:1-22.

Quaden, Guy (2004). "Efficiency and stability in an evolving financial

system." www.bnb.be/Sg/En/Contact/pdf/2004/sp040517en.pdf.

St. Ann Co-Operative Credit Union Ltd. (2003). Annual Report, St. Ann Co

operative Credit Union Ltd: St. Ann.

Stennett, Robert R., Batchelor, Pauline M. and Foga, Camille S. (1998). "Stabilization and the Jamaican Financial Sector 1991-1997." Mimeo, Bank of Jamaica.

Tennant, David (2004). "The effect of financial sector intermediation on economic growth: The case of Jamaica (1986-2002)." PhD Thesis,

unpublished.

World Bank (2003). "Jamaica: The road to sustained growth ?

Country Economic Memorandum." Washington DC: World Bank.

This content downloaded from 195.78.109.66 on Sun, 15 Jun 2014 06:42:57 AMAll use subject to JSTOR Terms and Conditions

102 SOCIAL AND ECONOMIC STUDIES

Appendix

Table 1: Average Interest Rate Spreads (1986 - 2003)

Country Interest Rate Spread (%)

Jamaica 12.08

Barbados 5.31

Caribbean Countries Belize 6.60

Guyana 6.74 Trinidad and Tobago 7.83

Cyprus 2.72

Other Small Open Economies Ireland 5.23

Singapore 3.34

Chile 5.61 China 1.75

Emerging Markets EgvP* 5.26

Hungary 4.96

South Africa 4.14

Canada 1.66

Industrialized Countries Germany 5.95

Japan 2.45

(1) Hungary: 1989-2003

(2) Germany: 1986 - 2002

Source: Computed by author from data in: IMF International Financial

Statistics (Various Issues)

This content downloaded from 195.78.109.66 on Sun, 15 Jun 2014 06:42:57 AMAll use subject to JSTOR Terms and Conditions

Are Interest Rate Spreads in Jamaica Too Large? 103

Table 2: Comparison of Interest Rate Spreads Across Financial Institutions in Jamaica

Type of Institution Average Interest Rate Spread (%)

Commercial Banks (1986 -

2002) 23.73 FIA Institutions (1989 -1998) 25.93

Building Sodeties (1986 -1996) 3.94 Credit Unions (1994

- 2002) 4.23

Sources: Computed by author from data in:

Bank of Jamaica Statistical Digest (Various Issues),

Jamaica Cooperative Credit Union League,

Building Sodeties Association of Jamaica Handbook

Table 3: Commercial Banks' Average Interest Rate Spread at Different Stages in the Evolution of Jamaica's Financial Sector

Phases Average Interest Rate Spread (%)

Pre-Liberalization (1977 -1985) 7.43 Liberalization (1986

- 1991) 14.22

Post Liberalization/Pre-Crisis (1992 -1995) 36.22 Crisis (1996 -1997) 34.21 Post-Crisis (1998

- 2002) 20.96

Source: Computed by author from data in: Bank of Jamaica Statistical Digest (Various Issues)

Table 4: Number of Persons Interviewed by Type of Institution

Type of Institution #s Interviewed

Commercial Banks 6 FIA Institutions 2

Building Societies 4 Life Insurance Companies 5 Credit Unions 7

Regulators and Policy Advisors 3

Total 27

This content downloaded from 195.78.109.66 on Sun, 15 Jun 2014 06:42:57 AMAll use subject to JSTOR Terms and Conditions

g co >

Table 5: Views as to whether Interest Rate Spreads in Jamaica are Too Large

o g D

Views

Com Bnk

FIA Inst

Bldg Soc

Cred

Un

LI Co

%

%

%

%

Total

#

/ /

Too Large

Large but

with

Justification

Not too Large

Other

16.7 33.3

33.3 16.7

0 0.0 1 50.0

1 50.0

0 0.0

1 25.0 2 50.0 1 25.0 0 0.0

4 57.1

1 14.3 2 28.6

0 0.0

0 0.0 5 100.0 0 0.0 0 0.0

6 25.0 11 45.8

6 25.0 1 4.2

This content downloaded from 195.78.109.66 on Sun, 15 Jun 2014 06:42:57 AMAll use subject to JSTOR Terms and Conditions

Table 6: Broadly Categorized Reasons for Jamaica's Relatively Large Interest Rate Spread

> ? en ) ? 3" CO q a ? 3 * ?

* E <3 -

Reasons

Com Bnk

FIA Inst

Bldg Soc

Cred

Un

LI Co

%

%

%

%

%

Total

%

Factors that Increase the Cost

& Risk of

Fin Insts' Operations

Regulatory Costs

Inefficiency &/or Excess

Profits by Financial Insts Erroneous Calculations

Other

No

Response

6 3 1 1 2 0

100.0 50.0 16.7 16.7 33.3

CO

100.0

0.0 0.0 0.0

0.0 0.0

3 2 1 0 1 0

75.0 50.0

25.0 0.0

25.0 0.0

42.9 0.0 42.9

0.0 0.0

14.3

60.0 20.0

0.0 0.0 20.0 0.0

17 70.8 6 25.0 20.8 4.2

16.7 4.2

Columns do not total 100% because multiple responses were selected

s

This content downloaded from 195.78.109.66 on Sun, 15 Jun 2014 06:42:57 AMAll use subject to JSTOR Terms and Conditions

Table 7: More Specific Reasons for Jamaica's Relatively Large Interest Rate Spread

to 8 > r? > m 2

Reasons

ComBnk FIA Inst BldgSoc CredUn

LI Co

%

%

%

%

Total %

Cost & Risk of Doing Business

in Jamaica

Macroeconomic Instability & Volatility

of the Interest Rate

Reserve Requirement Inefficiency of Fin. Insts.

Excess Profits by Fin. Insts. Lack of Economies of Scale

Customers' Demand for Inefficient

Services e.g. passbooks

Cost of Deposit Insurance Erroneous Cale, of Spreads Lack Infrastructure to efficiently

assess Loan Applications

Other

No Response

2 3 1 0 2 2 0 1 0 2 0

66.7 33.3 50.0 16.7 0.0

33.3 33.3 0.0

16.7 0.0 33.3 0.0

1 50.0

1 0 0 0 0 0 0 0 1 0 0

50.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

50.0 0.0 0.0

1 2 1 0 0 0 1 0 0 1 0

50.0 25.0

50.0 25.0 0.0

0.0 0.0 25.0

0.0 0.0 25.0

0.0

1 0 1 3 0 0 0 0 0 0 1

28.6 14.3 0.0

14.3 42.9

0.0 0.0 0.0

0.0 0.0 0.0 14.3

20.0 40.0 20.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 20.0

0.0

10 41.7

7 6 3 3 2 2 1 1 1 4 1

29.2 25.0

12.5 12.5

8.3 8.3 4.2 4.2 4.2

16.7 4.2

Columns do not total 100% because multiple responses were selected

This content downloaded from 195.78.109.66 on Sun, 15 Jun 2014 06:42:57 AMAll use subject to JSTOR Terms and Conditions

Are Interest Rate Spreads in Jamaica Too Large? 107

Table 8: Reserve Requirements Jamaican Commercial Banks

Year

1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002

Cash Reserve Ratio

(%)

20.00

20.00

20.00

19.00

19.50

19.00

25.00

25.00

25.00

25.00

25.00

25.00

21.00

17.00

14.00

11.00

10.00

Liquid Asset Ratio

(%)

44.00

35.00

25.00

20.00

32.50

20.00

50.00

50.00

50.00

47.00

47.00

47.00

43.00

35.00

32.00

29.00

27.00

Source: BOJ Statistical Digest (Various Issues)

This content downloaded from 195.78.109.66 on Sun, 15 Jun 2014 06:42:57 AMAll use subject to JSTOR Terms and Conditions

Table 9: Broadly Categorized Suggestions for Reducing Interest Rate Spreads

Suggestions

ComBnk FIA Inst BldgSoc

CredUn LI Co

Total

# % # %

% # % # % # %

Reduce Costs Associated with Regulations,

Regulatory Framework,

Macroecon Env & Taxes Increased Efficiency by &

Competition Among Fin. Insts. Customers to contribute to

Improved Efficiency

Other

4 66.7 1 50.0 4 100.0 3 42.9 5 100.0 17 70.8 4 66.7 1 50.0 2 50.0 6 85.7 2 40.0 15 62.5

1 16.7 1 50.0 0 0.0 1 14.3 0 0.0 3 12.5 2 33.3 1 50.0 1

25.0

0 0.0 1 20.0 5 20.8

Columns do not total 100% because multiple responses were selected

This content downloaded from 195.78.109.66 on Sun, 15 Jun 2014 06:42:57 AMAll use subject to JSTOR Terms and Conditions

Table 10: More Specific Suggestions for Reducing Interest Rate Spreads

Suggestions

ComBnk FIA Inst Bldg Soc CredUn

LI Co

Total

/ /

%

%

%

#

/ /

%

Govt to reduce borrowing, lower

int rates, reduce inflation &

Ensure macroeconomic stability Improve Efficiency of Fin Insts &

Increase Use of Technology

Reduce Reserve Rqmt

Increase Competition among Fin. Insts.

Encourage customers to seek

better rates & educate themselves

wrt the rqmts for loans

Get proper Infrastructure to aid in

assessing loans & Protection from Fraud

Improve quality of Graduates from

Education system

Reduce government taxes

Get customers to accept no-frills Banks

Reduce Crime & Violence

Other

33.3 50.0 33.3 33.3 0 0.0 1

16.7 16.7 0.0

16.7 0.0

16.7

0 0 1 1 0 0 0 0

50.0 0.0

0.0

50.0 1 50.0 0 0.0

50.0

0.0 0.0 0.0 0.0

0 0 0 0 1

75.0 25.0 25.0 25.0 1 25.0 0 0.0 0.0

0.0 0.0

0.0 25.0

28.6 71.4 14.3

14.3 1 14.3 0 0.0 0.0

0.0 0.0 0.0 0.0

60.0 20.0 40.0

20.0 0 0.0 1 20.0 0.0 40.0 0.0 20.0 20.0

11 45.8 10 41.7 6 25.0 6 25.0 2 8.3 2 8.3

2 2 1 1 3

8.3 8.3 4.2 4.2 12.5

Columns do not total 100% because multiple responses were selected

This content downloaded from 195.78.109.66 on Sun, 15 Jun 2014 06:42:57 AMAll use subject to JSTOR Terms and Conditions

110 SOCIAL AND ECONOMIC STUDIES

Table 11: Selected Macroeconomic Indicators (1986 - 2002)

Year Domestic Inflation Exchange Rate Treasury Bill Debt/GDP (%) Rate (%) (J$ per US$) Rates (%)

1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002

42.90

44.80

44.80

36.10

28.20

19.60

22.50

21.20

27.90

32.10

35.30

42.10

47.20

64.10

61.10

88.20

96.20

10.4

8.4

8.5

17.2

29.8

80.2

40.2

30.1

26.8

25.6

15.8

9.2

7.9

6.8

6.1

8.8

7.3

5.48

5.49

5.49

5.75

7.18

12.85

23.01

25.68

33.35

35.54

37.02

35.58

36.68

39.33

43.32

46.19

48.73

15.93

19.61

18.00

23.59

28.65

35.06

23.22

39.36

26.95

34.97

25.21

24.63

21.31

18.68

18.32

15.70

15.68

Sources: Debt Management Unit (Ministry of Finance and Planning) BOJ Statistical Digest (Various Issues)

This content downloaded from 195.78.109.66 on Sun, 15 Jun 2014 06:42:57 AMAll use subject to JSTOR Terms and Conditions

Are Interest Rate Spreads in Jamaica Too Large? 111

Table 12: Difference Between Commercial Banks'

Average Lending Rates and Treasury Bill Rates

Year

1986 1987 1988 1989 1990 1991

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002

Average Lending Rates (%) (B)

25.36

25.24

25.10

31.00

36.03

40.12

46.39

61.32

56.14

55.27

55.22

44.17

38.80

33.92

31.67

26.79

25.04

Treasury Bill Rates (%) (A)

15.93

19.61

18.00

23.59

28.65

35.06

23.22

39.36

26.95

34.97

25.21

24.63

21.31

18.68

18.32

15.70

15.68

Difference (B-A)

9.43

5.63

7.10

7.41

7.38

5.06

23.17

21.96

29.19

20.30

30.01

19.54

17.49

15.24

13.35

11.09

9.36

Source: BOJ Statistical Digest (Various Issues)

This content downloaded from 195.78.109.66 on Sun, 15 Jun 2014 06:42:57 AMAll use subject to JSTOR Terms and Conditions