Embed Size (px)

Citation preview

AMEC

Homestead FundsApril 10th , 2018

Brian AllenInstitutional Sales Consultant

2Our People | homesteadfunds.com

v3-2017

We’d be pleased to provide more information about our strategies and welcome your call.

Business Development

Brian AllenInstitutional Sales Consultant

Experience

Brian has been providing investment guidance and client services to Homestead Funds shareholders for more than a decade. He holds FINRA Series 6 license (Investment Company and Variable Contracts), Series 63 (Uniform Securities Agent State Law) and Series 65 (Investment Advisor Representative).

Education

Brian is a graduate of King College, where he received a Bachelor’s degree in business administration. He received his MBA from Marymount University.

YEARS IN THE INDUSTRY:

Since 2000

Firm Overview

4Firm Overview| homesteadfunds.com

v3-2017

For Institutional or Advisor Use Only—Not for Public Distribution

Homestead Funds was established in 1990 by the National Rural Electric Cooperative

Association (NRECA), a not-for-profit organization that serves and represents the

nation’s consumer-owned rural electric cooperatives.

Based in Arlington, Virginia, we are a mutual fund company created to provide

high-quality, affordable investment products and services to rural electric

cooperatives.

We serve financial advisors, retirement plans, institutional clients as well as

individual investors.

We currently make eight investment strategies available through our no-load

mutual fund offering.

RE Advisers (REA), a wholly owned subsidiary of NRECA, provides investment

advisory and administrative services to Homestead Funds.

About Homestead

Built for Cooperatives | homesteadfunds.com

v6-2017

5

• A series of eight no-load mutual funds. Established by NRECA in 1990

for member systems and their employees.

• Open to the public. Created for co-ops, but others can invest.

Created by and for the Co-Op Community

“If you are an employee of a member co-op, you can think of Homestead Funds as a local business supporting you and your community.”

Brian AllenInstitutional Sales Consultant

Built for Cooperatives | homesteadfunds.com

v6-2017

6

More than $3.3 billion in assets as of 9/30/2017

• Rollover, Traditional and Roth IRA accounts

• Education Savings and UGMA/UTMA accounts for minors

• Individual & joint accounts

• Corporate and trust accounts

• Cooperative benefit plan accounts, including deferred compensation plan

assets

Assets Under Management

Helping investors in the co-op community reach their dreams

The Mutual Fund Company Built for Cooperatives

Built for Cooperatives | homesteadfunds.com

v6-2017

8

Our Funds

Money Market Fund

Short-Term: Investor’s time horizon is typically less than one year

Daily Income Fund

Bond Funds

Medium-Term: Investor’s time horizon is typically less than five years

Short-Term Government Securities Fund

Short-Term Bond Fund

Equity Funds

Long-Term: Investor’s time horizon is typically more than five years

Stock Index Fund

Value Fund

Growth Fund

Small-Company Stock Fund

International Equity Fund

Investing in mutual funds involves risk, including the possible loss of principal. You could lose money by investing in the Daily Income Fund. Although the Fund seeks to preserve the value of your investment at $1.00 per share, it cannot guarantee it will do so. An investment in the Fund is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. The Fund’s sponsor has no legal obligation to provide financial support to the Fund, and you should not expect that the sponsor will provide financial support to the Fund at any time.

Built for Cooperatives | homesteadfunds.com

v1-2017

9

Deferred Compensation Plan Accounts

— Homestead Funds may be used as the funding vehicles for these plans.

Designed to help members attract, retain and compensate directors, CEOs

and other highly compensated employees

Welfare Benefit Plan Trust (FAS-106) Accounts

— An account for covering future retiree medical costs

Corporate Accounts

— Regular investment accounts, which can be dedicated for specific purposes

Trust Accounts

— Unclaimed capital credits or scholarship monies can be held in trust

accounts

How We Help Co-Ops

Built for Cooperatives | homesteadfunds.com

v6-2017

10

Build retirement savings

Manage assets in retirement

Accounts types and investment options for other goals

— Save for education costs

— Build wealth

— Put money aside for a major purchase, like a house

Ways Investors Use Our Funds

Built for Cooperatives | homesteadfunds.com

v6-2017

11

Roth IRA

Traditional IRA

Spousal IRA

SEP IRA

Types of Retirement Accounts

* Homestead Funds does not offer tax advice. Please consult an appropriate professional for your individual circumstance.

Built for Cooperatives | homesteadfunds.com

v6-2017

12

Individual & Joint Accounts

— Can be used to build emergency funds, save for larger goals or establish a

rainy day account.

Trust Accounts

— Can be used as an estate planning tool.

Accounts for Minors

— Education Savings Accounts can be used to save for a child’s education.

— Uniform Gift/Transfer to Minor Accounts can be used to save for anything

benefiting the minor (including education).

Types of Non-Retirement Accounts

Built for Cooperatives | homesteadfunds.com

v6-2017

13

No sales commissions (loads)

Funds with a sales charges typically deduct the charge from the amount

invested.

Funds offered at no load, like Homestead Funds, do not deduct a sales

charge from the amount invested.

Low expense ratios

All funds have expenses, which cover the costs for needed services, like

portfolio management, accounting and recordkeeping.

These costs are deducted from fund assets, effectively lowering investors’

returns.

Funds with a relatively low expense ratio, allow investors to keep more of the

fund’s earnings.

Low Costs

Homestead Fund expense ratios are in line with or below peers according to Morningstar Direct, based on each fund’s Morningstar classification. The gross expense ratio shows the percentage of fund assets deducted annually to cover operating costs. For some funds, the investment advisor has agreed voluntarily or contractually (for at least the current fiscal year) to waive or reimburse a portion of expenses. The net expense ratio is the gross expense ratio minus the portion of expenses waived or reimbursed. Please see the current prospectus for additional details.

Built for Cooperatives | homesteadfunds.com

v6-2017

14

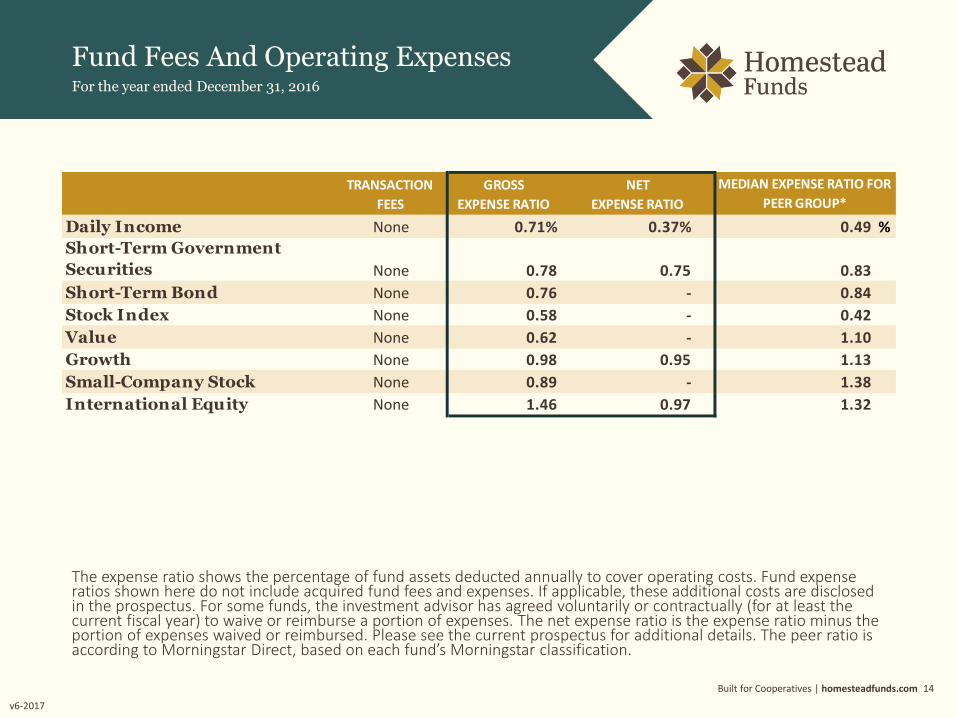

The expense ratio shows the percentage of fund assets deducted annually to cover operating costs. Fund expense ratios shown here do not include acquired fund fees and expenses. If applicable, these additional costs are disclosed in the prospectus. For some funds, the investment advisor has agreed voluntarily or contractually (for at least the current fiscal year) to waive or reimburse a portion of expenses. The net expense ratio is the expense ratio minus the portion of expenses waived or reimbursed. Please see the current prospectus for additional details. The peer ratio is according to Morningstar Direct, based on each fund’s Morningstar classification.

Fund Fees And Operating ExpensesFor the year ended December 31, 2016

TRANSACTION

FEES

GROSS

EXPENSE RATIO

NET

EXPENSE RATIO

Daily Income None 0.71% 0.37% 0.49 %

Short-Term Government

Securities None 0.78 0.75 0.83

Short-Term Bond None 0.76 - 0.84

Stock Index None 0.58 - 0.42

Value None 0.62 - 1.10

Growth None 0.98 0.95 1.13

Small-Company Stock None 0.89 - 1.38

International Equity None 1.46 0.97 1.32

MEDIAN EXPENSE RATIO FOR

PEER GROUP*

Built for Cooperatives | homesteadfunds.com

v6-2017

15

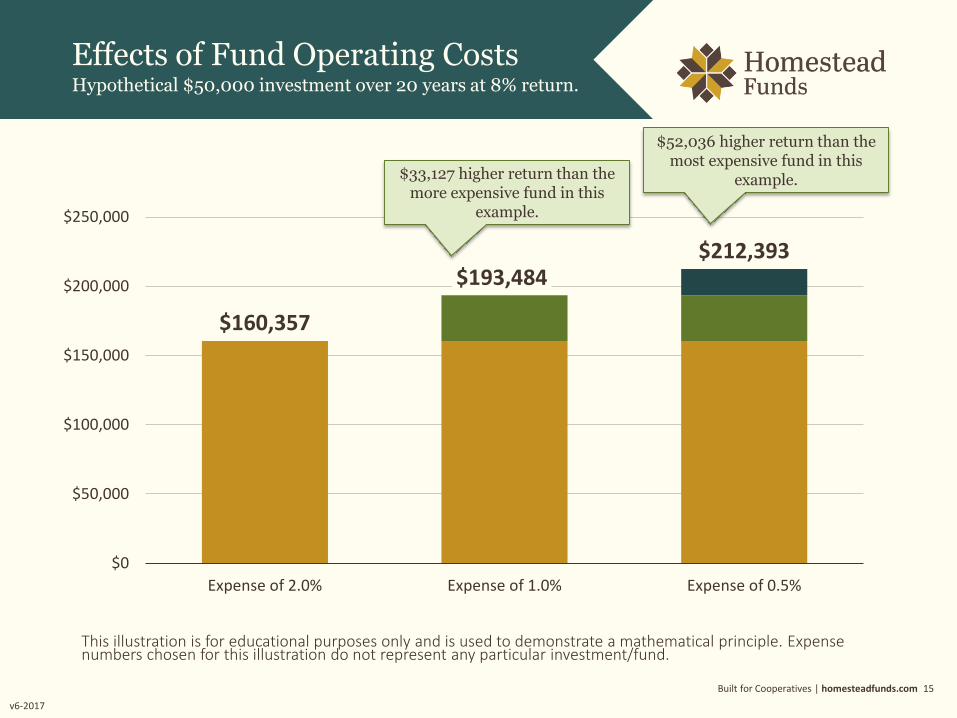

$160,357

$193,484$212,393

$0

$50,000

$100,000

$150,000

$200,000

$250,000

Expense of 2.0% Expense of 1.0% Expense of 0.5%

Effects of Fund Operating CostsHypothetical $50,000 investment over 20 years at 8% return.

This illustration is for educational purposes only and is used to demonstrate a mathematical principle. Expense numbers chosen for this illustration do not represent any particular investment/fund.

$52,036 higher return than the most expensive fund in this

example.$33,127 higher return than the more expensive fund in this

example.

Built for Cooperatives | homesteadfunds.com

v6-2017

16

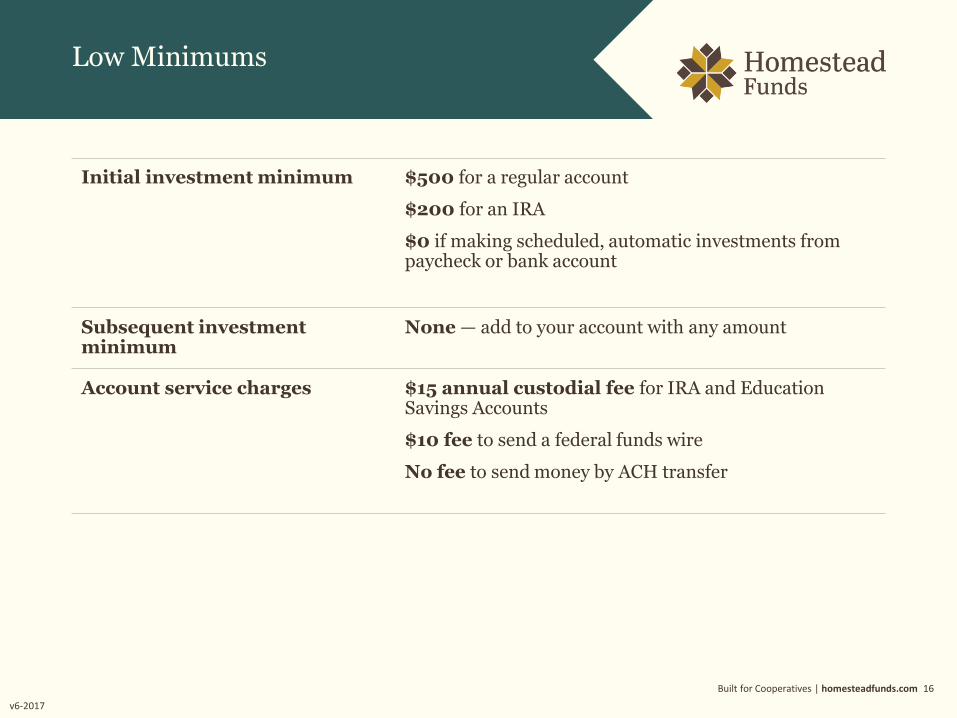

Initial investment minimum $500 for a regular account

$200 for an IRA

$0 if making scheduled, automatic investments from paycheck or bank account

Subsequent investmentminimum

None — add to your account with any amount

Account service charges $15 annual custodial fee for IRA and Education Savings Accounts

$10 fee to send a federal funds wire

No fee to send money by ACH transfer

Low Minimums

2017 Understanding Investing | homesteadfunds.com

v3

17

Financial Fragility and the $400 Question

47% of Americans could not come up with $400 in an emergency

55% of households don’t have enough liquid savings to replace a month’s worth of income

56%of Americans worried about finances in the last year

62%of Americans could not cover a $1,000 ER visit or $500 car repair with savings

Source: Gabler, Neal. “The Secret Shame of Middle-Class Americans.” The Atlantic. May 2016.

Built for Cooperatives | homesteadfunds.com

v6-2017

18

Representatives have backgrounds in banking, brokerage and insurance.

Each has passed FINRA Series 6 (Investment Company and Variable

Contracts) and 63 (Uniform Securities State Law) securities exams.

Daily interaction with shareholders via telephone, emails and written

correspondence.

In-depth knowledge of different account structures and processing

requirements.

The Team

19Our People | homesteadfunds.com

v3-2017

Business Development and Client Relations

Brian Allen

Institutional Sales

Consultant

Dim a Awam leh

Senior Institutional

Client Services

Associate

Will Cunningham ,

CFP®

Senior Client

Relationship Advisor

Kara Gardner

Senior Operations

Specialist

Darry l Keeton,

CIMA®

Head of Distribution

Nancy Jacobs

Senior Client Services

Associate

Megan McFarland,

CFP®

Senior Client

Relationship Advisor

Alaina Schrager,

CFP®

Senior Client

Relationship Advisor

John Scott

Senior Client Services

Associate

Ray m ond Scott,

CFP®

Client Relationship

Advisor

Makia T illm an

Mutual Funds

Operations Specialist

Built for Cooperatives | homesteadfunds.com

v6-2017

20

Discuss your financial goals

Provide personalized investment guidance

Provide investment education

Assist with opening and funding accounts

How We Can Help

Built for Cooperatives | homesteadfunds.com

v1-2017

21

One-on-one financial planning help and account service

— Detailed assessment of your financial planning goals, budget, risk

tolerance

— Guidance for structuring your portfolio for an appropriate risk/return

trade off

— Help maintaining your target asset mix over time

How We Help Our Shareholders

Economy and Markets| homesteadfunds.com 22

v1

Investing by Life Stage: Early Career

Investor Profile- Age 19 – 35

Investment Considerations- Build an emergency fund

Investment Goals- Provide for family- Pay off student loans- Buy a home- Save for retirement

Start saving now for a more secure financial future.

Economy and Markets| homesteadfunds.com 23

v1

Investing by Life Stage: Mid Career

Reassess your investment goals and consider rebalancing, if necessary.

Investor Profile- Age 36 – 51

Investment Considerations- Continue growing emergency fund- Prioritizing financial goals- Continue investing for retirement- Make catch-up contributions, if necessary

Investment Goals- Save for a child’s education- Pay off mortgage- Taking care of elderly parents- Save for retirement

Rebalancing can entail transaction costs and tax consequences that should be considered when determining a rebalancing strategy.

Economy and Markets| homesteadfunds.com 24

v1

Investing by Life Stage: Late Career

Investor Profile- Age 52-65

Investment Considerations- Estimate your retirement income needs- Evaluate your portfolio- Continue investing for retirement- Make catch-up contributions, if necessary

Investment Goals- Eliminate debt- Save for retirement

Plan your retirement income strategy.

Economy and Markets| homesteadfunds.com 25

v1

Investing by Life Stage: Retirement

Investor Profile- Age 65+

Investment Considerations- Make a decision about Social Security benefits- Transition asset allocations- Learn about Required Minimum Distributions

(RMDs)

Investment Goals- Financial security- Leaving money to heirs

Optimize your retirement experience.

Built for Cooperatives | homesteadfunds.com

v6-2017

26

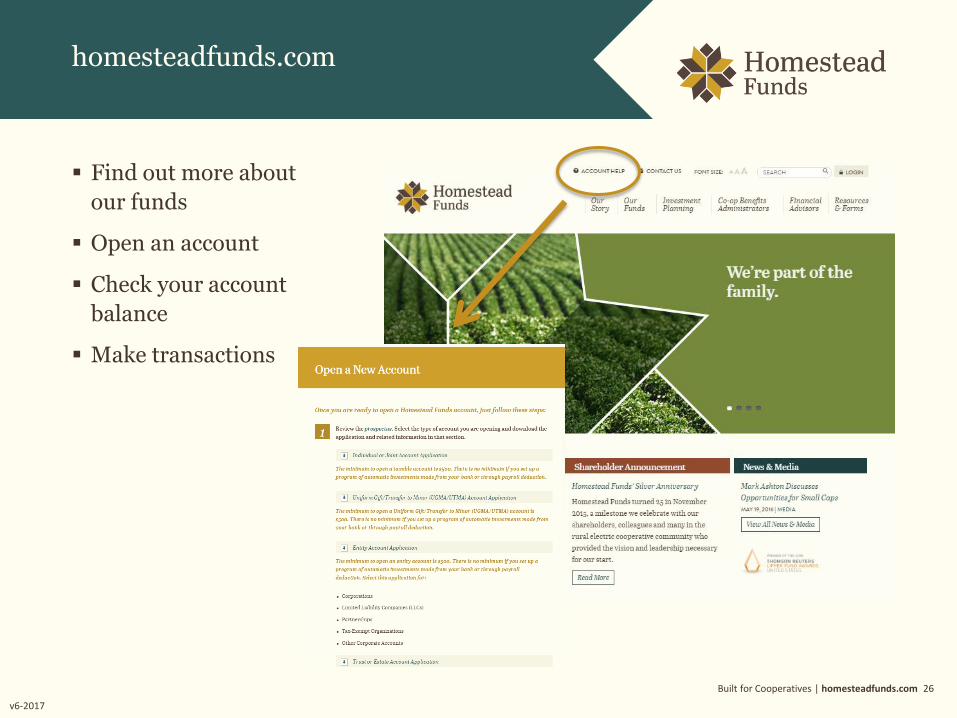

Find out more about

our funds

Open an account

Check your account

balance

Make transactions

homesteadfunds.com

Built for Cooperatives | homesteadfunds.com

v1-2017

27

Others Can Invest

Homestead Funds was created for the rural electric cooperative community, but you don’t have to be a co-op employee or director to invest. Family and friends of NRECA member system employees and the general public can open accounts.

Built for Cooperatives | homesteadfunds.com

v6-2017

28

• We’re part of the NRECA family!

• A range of fund choices

• Experienced portfolio managers

• An affordable way to invest—No loads, low account minimums

• Personalized shareholder service and investment guidance

Summary

Questions? Just call 800-258-3030

29Firm Overview | homesteadfunds.com

v1-2018

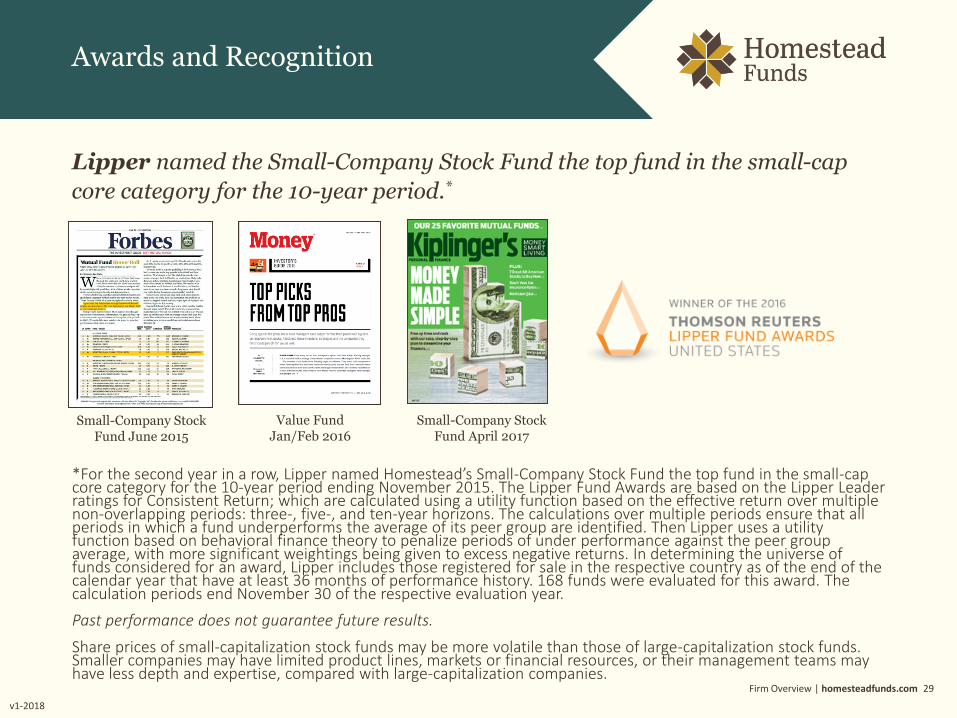

Lipper named the Small-Company Stock Fund the top fund in the small-cap

core category for the 10-year period.*

Awards and Recognition

*For the second year in a row, Lipper named Homestead’s Small-Company Stock Fund the top fund in the small-cap core category for the 10-year period ending November 2015. The Lipper Fund Awards are based on the Lipper Leader ratings for Consistent Return; which are calculated using a utility function based on the effective return over multiple non-overlapping periods: three-, five-, and ten-year horizons. The calculations over multiple periods ensure that all periods in which a fund underperforms the average of its peer group are identified. Then Lipper uses a utility function based on behavioral finance theory to penalize periods of under performance against the peer group average, with more significant weightings being given to excess negative returns. In determining the universe of funds considered for an award, Lipper includes those registered for sale in the respective country as of the end of the calendar year that have at least 36 months of performance history. 168 funds were evaluated for this award. The calculation periods end November 30 of the respective evaluation year.

Past performance does not guarantee future results.

Share prices of small-capitalization stock funds may be more volatile than those of large-capitalization stock funds. Smaller companies may have limited product lines, markets or financial resources, or their management teams may have less depth and expertise, compared with large-capitalization companies.

Small-Company Stock Fund June 2015

Value FundJan/Feb 2016

Small-Company Stock Fund April 2017

30Firm Overview | homesteadfunds.com

v1-2018

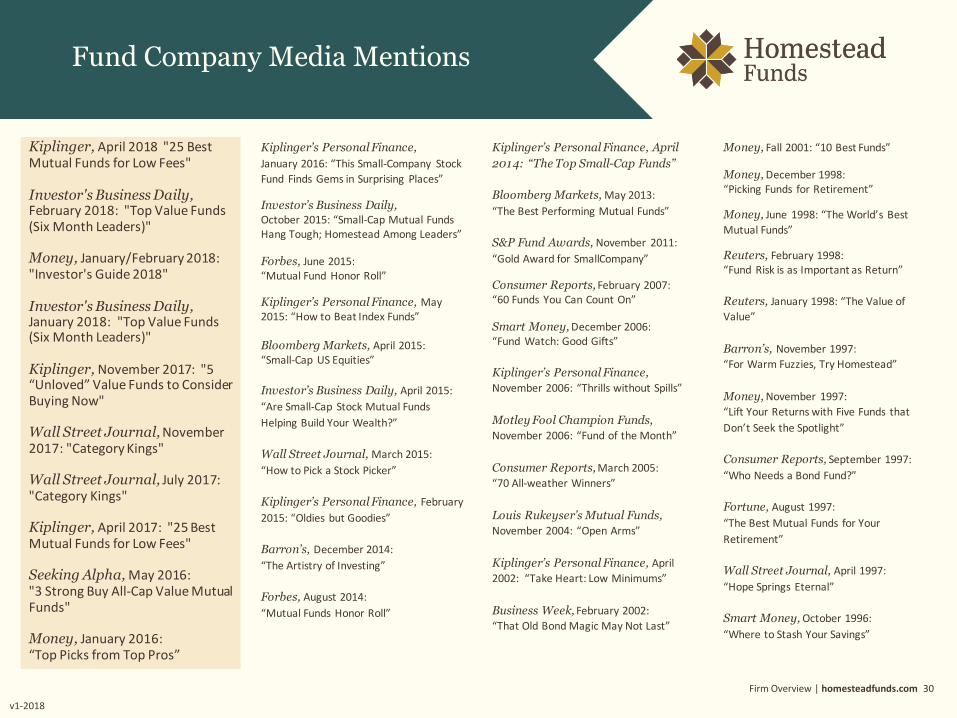

Fund Company Media Mentions

Money, Fall 2001: “10 Best Funds”

Money, December 1998: “Picking Funds for Retirement”

Money, June 1998: “The World’s Best

Mutual Funds”

Reuters, February 1998: “Fund Risk is as Important as Return”

Reuters, January 1998: “The Value of

Value”

Barron’s, November 1997:

“For Warm Fuzzies, Try Homestead”

Money, November 1997:

“Lift Your Returns with Five Funds that

Don’t Seek the Spotlight”

Consumer Reports, September 1997:

“Who Needs a Bond Fund?”

Fortune, August 1997:

“The Best Mutual Funds for Your

Retirement”

Wall Street Journal, April 1997:

“Hope Springs Eternal”

Smart Money, October 1996:

“Where to Stash Your Savings”

Kiplinger’s Personal Finance, April

2014: “The Top Small-Cap Funds”

Bloomberg Markets, May 2013:

“The Best Performing Mutual Funds”

S&P Fund Awards, November 2011:

“Gold Award for SmallCompany”

Consumer Reports, February 2007: “60 Funds You Can Count On”

Smart Money, December 2006: “Fund Watch: Good Gifts”

Kiplinger’s Personal Finance,

November 2006: “Thrills without Spills”

Motley Fool Champion Funds,

November 2006: “Fund of the Month”

Consumer Reports, March 2005:

“70 All-weather Winners”

Louis Rukeyser’s Mutual Funds,

November 2004: “Open Arms”

Kiplinger’s Personal Finance, April

2002: “Take Heart: Low Minimums”

Business Week, February 2002:

“That Old Bond Magic May Not Last”

Kiplinger’s Personal Finance,

January 2016: “This Small-Company Stock

Fund Finds Gems in Surprising Places”

Investor’s Business Daily,

October 2015: “Small-Cap Mutual Funds Hang Tough; Homestead Among Leaders”

Forbes, June 2015: “Mutual Fund Honor Roll”

Kiplinger’s Personal Finance, May 2015: “How to Beat Index Funds”

Bloomberg Markets, April 2015: “Small-Cap US Equities”

Investor’s Business Daily, April 2015:

“Are Small-Cap Stock Mutual Funds

Helping Build Your Wealth?”

Wall Street Journal, March 2015:

“How to Pick a Stock Picker”

Kiplinger’s Personal Finance, February

2015: “Oldies but Goodies”

Barron’s, December 2014:

“The Artistry of Investing”

Forbes, August 2014:

“Mutual Funds Honor Roll”

Kiplinger, April 2018 "25 Best Mutual Funds for Low Fees"

Investor's Business Daily, February 2018: "Top Value Funds (Six Month Leaders)"

Money, January/February 2018: "Investor's Guide 2018"

Investor's Business Daily, January 2018: "Top Value Funds (Six Month Leaders)"

Kiplinger, November 2017: "5 “Unloved” Value Funds to Consider Buying Now"

Wall Street Journal, November 2017: "Category Kings"

Wall Street Journal, July 2017: "Category Kings"

Kiplinger, April 2017: "25 Best Mutual Funds for Low Fees"

Seeking Alpha, May 2016: "3 Strong Buy All-Cap Value Mutual Funds"

Money, January 2016: “Top Picks from Top Pros”

Glossary | homesteadfunds.com

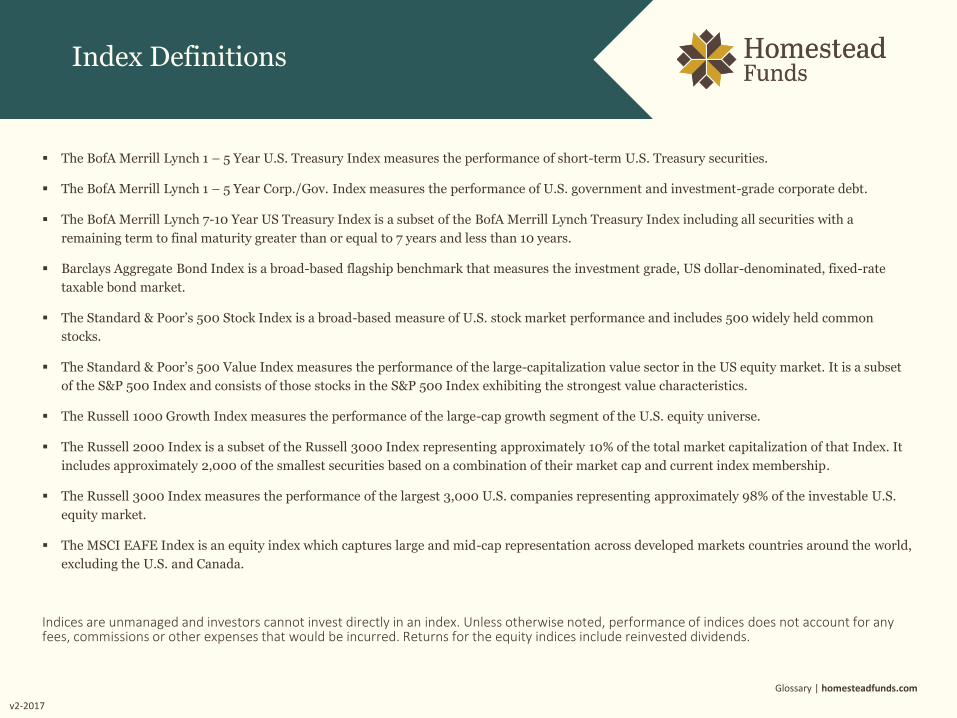

The BofA Merrill Lynch 1 – 5 Year U.S. Treasury Index measures the performance of short-term U.S. Treasury securities.

The BofA Merrill Lynch 1 – 5 Year Corp./Gov. Index measures the performance of U.S. government and investment-grade corporate debt.

The BofA Merrill Lynch 7-10 Year US Treasury Index is a subset of the BofA Merrill Lynch Treasury Index including all securities with a

remaining term to final maturity greater than or equal to 7 years and less than 10 years.

Barclays Aggregate Bond Index is a broad-based flagship benchmark that measures the investment grade, US dollar-denominated, fixed-rate

taxable bond market.

The Standard & Poor’s 500 Stock Index is a broad-based measure of U.S. stock market performance and includes 500 widely held common

stocks.

The Standard & Poor’s 500 Value Index measures the performance of the large-capitalization value sector in the US equity market. It is a subset

of the S&P 500 Index and consists of those stocks in the S&P 500 Index exhibiting the strongest value characteristics.

The Russell 1000 Growth Index measures the performance of the large-cap growth segment of the U.S. equity universe.

The Russell 2000 Index is a subset of the Russell 3000 Index representing approximately 10% of the total market capitalization of that Index. It

includes approximately 2,000 of the smallest securities based on a combination of their market cap and current index membership.

The Russell 3000 Index measures the performance of the largest 3,000 U.S. companies representing approximately 98% of the investable U.S.

equity market.

The MSCI EAFE Index is an equity index which captures large and mid-cap representation across developed markets countries around the world,

excluding the U.S. and Canada.

Indices are unmanaged and investors cannot invest directly in an index. Unless otherwise noted, performance of indices does not account for any fees, commissions or other expenses that would be incurred. Returns for the equity indices include reinvested dividends.

Index Definitions

v2-2017

Investing in mutual funds involves risk, including the possible loss of principal.

You could lose money by investing in the Daily Income Fund. Although the fund seeks to preservethe value of your investment at $1.00 per share, it cannot guarantee it will do so. An investment inthe fund is not insured or guaranteed by the Federal Deposit Insurance Corporation or any othergovernment agency. The fund’s sponsor has no legal obligation to provide financial support to thefund, and you should not expect that the sponsor will provide financial support to the fund at anytime.Investments in fixed-income funds are subject to interest rate, credit and inflation risk. Interest rate risk is risk that a change in rates willnegatively affect the value of the securities in the fund’s portfolio. Equity funds, in general, are subject to style risk, the chance that returnson stocks within the style category in which the fund invests will trail returns of stocks representing other styles or the market overall. Shareprices of small-capitalization stock funds may be more volatile than those of large-capitalization stock funds. Smaller companies may havelimited product lines, markets, financial resources or their management teams may have less depth and expertise compared with large-capitalization companies. International investing involves special risks such as currency fluctuation and political instability. Index funds aresubject to tracking risk, the risk that the fund’s return will not closely track the return of the index.

The preceding document is designed to be presented in its entirety to the intended audience. Please do not distribute without permission.This material represents an assessment of the market and economic environment at a specific point in time and is not intended to be aforecast of future events, or a guarantee of future results. Forward-looking statements are subject to certain risks and uncertainties. Actualresults, performance, or achievements may differ materially from those expressed or implied. Information is based on data gathered fromwhat we believe are reliable sources. It is not guaranteed as to accuracy, does not purport to be complete and is not intended to be used asa primary basis for investment decisions.

The information provided herein is not directed at any investor or category of investors and is provided solely as general information aboutour products and services and to otherwise provide general investment education. No information contained herein should be regarded as asuggestion to engage in or refrain from any investment-related course of action as none of Homestead Funds, RE Advisers, nor any of itsaffiliates is undertaking to provide investment advice, act as an adviser to any plan or entity subject to the Employee Retirement IncomeSecurity Act of 1974, as amended, individual retirement account or individual retirement annuity, or give advice in a fiduciary capacity withrespect to the materials presented herein. If you are an individual retirement investor, contact your financial advisor or other fiduciary aboutwhether any given investment idea, strategy, product or service described herein may be appropriate for your circumstances.

Homestead Funds investment advisor, RE Advisers Corporation, and distributor, RE Investment Corporation, are indirect wholly-ownedsubsidiaries of NRECA. 05/17

v3-2017

Past performance is no guarantee of future results.

Investors are advised to consider fund objectives, risks, charges and expenses before investing. The prospectus contains this and other information and should be read carefully before you invest. To obtain a prospectus, call 800.258.3030 or download a PDF at homesteadfunds.com.