Embed Size (px)

Citation preview

Modul ke:

Fakultas

Program Studi

Akuntansi Biaya Costing By-Products and Joint Products

Suryadharma Sim, SE, M. Ak

09 Ekonomi dan

Bisnis

S1 Manajemen

Costing By-Products and Joint Products

By-Products and Joint Products Defined

The term by-product is generally used to denote a product of relatively small total value

produced simultaneously with a product of greater total value.

Joint products are produced simultaneously by a common process or series of processes,

with each product possessing more than nominal value in the form in which it is produced.

Many industrial concerns are confronted with the difficult and often rather complicated

problem of assigning costs to their by-products and joint products. Chemical companies,

coke manufacturers, refineries, flour mills, coal mines, lumber mills, gas companies,

dairies, canners, meat packers, and many others produce in their manufacturing or

conversion processes a multitude of products to which some cost must be assigned.

Assignment of costs of these various products enhances equitable inventory costing for

income determination and financial statement purposes. An even more important aspect of

by product and joint product costing is that it furnishes management with data for use in

planning maximum profit potentials and evaluating actual profit performance.

Costing By-Products and Joint Products

Difficulties / Problems in Costing by Products and Joint Products:

By products and joint products are difficult to cost because a true joint cost is

indivisible. For example, an ore might contain both lead and Zink. In the raw

state, these minerals are joint products, and until they are separated by

reduction of the ore, the cost of finding mining, and processing is a joint cost;

neither lead nor Zink can be produced without the other prior to the split-off

point.

The cost accumulated to the split-off point must be born by the difference

between the selling price and the cost to complete and sale each mineral after

the split-off point.

Costing By-Products and Joint Products

Joint Products and Joint Product Cost:

Definition and Explanation of Joint Products:

Joint products are produced simultaneously by a common process or

series of processes, with each product processing more than a

nominal value in the form in which it is produced. The definition

emphasizes the point that the manufacturing process creates

products in a definite quantitative relationship. An increase in one

product's output will bring about an increase in the quantity of the

other products, or vice versa, but not necessarily in the same

proportion.

Costing By-Products and Joint Products

Definition and explanation of Joint Product Cost:

A joint product cost cay be defined as that cost which arises from the common processing or

manufacturing of products produced from a common raw material. Whenever two or more

different products are created from a single cost factor, a joint product cost results. A joint cost

is incurred prior to the point at which separately identifiable products emerge from the same

process.

Example:

For example, the production of coke, for which coal is the original raw material. In addition to

coke as its major product, the process produces sulfate of ammonia, light oil, crude tar and

gas. The greater quantity of gas is not sold but is used to fire the coke ovens and the boilers

in the power plant. The coke ovens are the split-off point for cost assignments. The cost of

each product consists of a pro rata share of the joint cost plus any separable or subsequent

costs incurred in order to put the products into saleable condition.

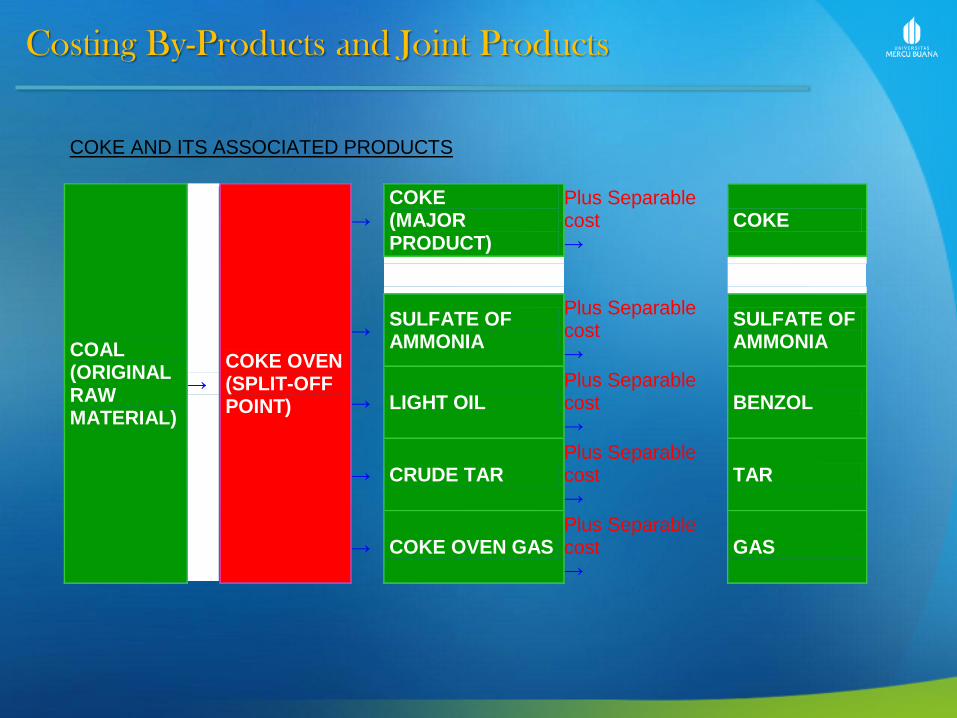

Costing By-Products and Joint Products

COKE AND ITS ASSOCIATED PRODUCTS

COAL (ORIGINAL RAW MATERIAL)

→ COKE OVEN (SPLIT-OFF POINT)

→ COKE (MAJOR PRODUCT)

Plus Separable cost →

COKE

→ SULFATE OF AMMONIA

Plus Separable cost →

SULFATE OF AMMONIA

→ LIGHT OIL Plus Separable cost →

BENZOL

→ CRUDE TAR Plus Separable cost →

TAR

→ COKE OVEN GAS Plus Separable cost →

GAS

Costing By-Products and Joint Products

Characteristics of Joint Products and Joint Cost:

Many products or services are linked together by physical relationships which

necessitate simultaneous production. To the point of split-off or to the point

where these several products emerge as individual units, the cost of the

products forms a homogeneous whole.

The classic example of joint products is found in the meat packing industry,

where various cuts of meet and numerous by products are processed from one

original carcass with one lump-sum cost. An other example of joint products

manufacturing is the production of gasoline, where the derivation of gasoline

inevitably results in the production of such items as naphtha, kerosene, and

distillate fuel oils.

Costing By-Products and Joint Products

Other examples of joint products manufacturing are the simultaneous

production of various grads of glue and the processing of soybeans into oil and

meal. Joint product costing is also found in industries that must grade raw

materials before it is processed. Tobacco manufacturers (except in cases

where graded tobacco is purchased) and virtually all fruit and vegetables

canners face the problem of grading. In fact, such manufacturers have a dual

problem of joint cost allocation:

1. Materials cost is applicable to all grades

2. Subsequent manufacturing costs are incurred simultaneously for all the

different grads.

Costing By-Products and Joint Products

By-Products:

Definition and Explanation of By Products:

The term "by product" is generally used to denote one or more products of

relatively small total value that are produced simultaneously with a product of

greater total value. The product with the greater value, commonly called the

"main product", is usually produced in greater quantities than the by products.

Ordinarily, the manufacturer has only limited control over the quantity of the by

product that comes into existence. However, the introduction of more advanced

engineering methods, such as in the petroleum industry, has permitted greater

control over the quantity of residual products. In fact, one company, which

formerly paid a trucker to haul away and dump certain waste materials,

discovered that the waste was valuable as fertilizer, and this by product is now

an additional source of income for the entire industry.

Costing By-Products and Joint Products

Nature of By-Products:

The accounting treatment of by-products necessitates a reasonably complete knowledge of

the technological factors underlying their manufacture, since the origins of by products may

vary. By-products arising from the cleansing of the main product, such as gas and tar from

coke manufacture, generally have a residual value. In some cases, the by product is left

over scrap or waste, such as sawdust in lumber mills. In other cases, the by product may

not be the result of any manufacturing process but may arise from preparing raw materials

before they are used in the manufacture of the main product. The separation of cotton seed

from cotton, cores and seeds from apples, and shells from coca beans are examples of this

type of product.

By product can be classified into the following two groups according to their marketable

condition at the split-off point:

1. Those sold in their original form without need of further processing.

2. Those which require further processing in order to be saleable.

Costing By-Products and Joint Products

Methods of Costing By-Products

Recognition of Gross Revenue Method-By Products Costing:

This method is typical non-cost procedure in which the final inventory cost of the

main product is overstated to the extent that some of the cost belongs to the by

product.

However this shortcoming is somewhat removed in procedure 4 (by product

revenue deducted from the production cost), although a sales value rather than a

cost is deducted from the production cost of the main product.

1. By-Product Revenue as Other Income:

2. By-Product Revenue as Additional Sales Revenue:

3. By-Product Revenue as a Deduction from the Cost of Goods Sold:

4. By-Product Revenue deducted from Production Cost:

Costing By-Products and Joint Products

Recognition of Net Revenue Method--By Product Costing:

This method recognizes the need for assigning some cost to the by-product. It does not

attempt, however, to allocate any main product cost to the buy product. Any expenses

involved in further processing or marketing the by-product are recorded in separate accounts.

All figures are shown on the income statement, following one of the procedures described at

recognition of gross revenue method page.

Journal entries in this method would involve charges to by-product revenue for the additional

work required and perhaps for factory overhead. The marketing and administrative expenses

might also be allocated to the by product on some predetermine basis. Some firms carry an

account called by-product to which all additional expenses are debited and all income is

credited. The balance of this account would be presented in the income statement, following

one of the procedures out lined at recognition of gross revenue method page. However,

accumulated manufacturing costs applicable to by product inventory should be reported on

the balance sheet.

Costing By-Products and Joint Products

Replacement Cost Method-By Product Costing:

Replacement cost method ordinarily is applied by firms whose by-products are

used within the plant, thereby avoiding the necessity of purchasing materials

and supplies from outside suppliers. The production cost of the main product is

credited for such materials, and the offsetting debit is to the department that

uses the by product. The cost assigned to the by product is the purchase or

replacement cost existing in the market. This method is common in the steel

industry. Although many by-products are sold in the open market, other

products, such as blast furnace gas and coke oven gas, are mixed and used

for heating in open hearth furnaces. The waste heat from open hearths is used

again in the generation of steam needed by the various producing

departments. The resourceful use of these by-products and their accounting

treatment are indicated by the following procedure used by a steel company:

Costing By-Products and Joint Products

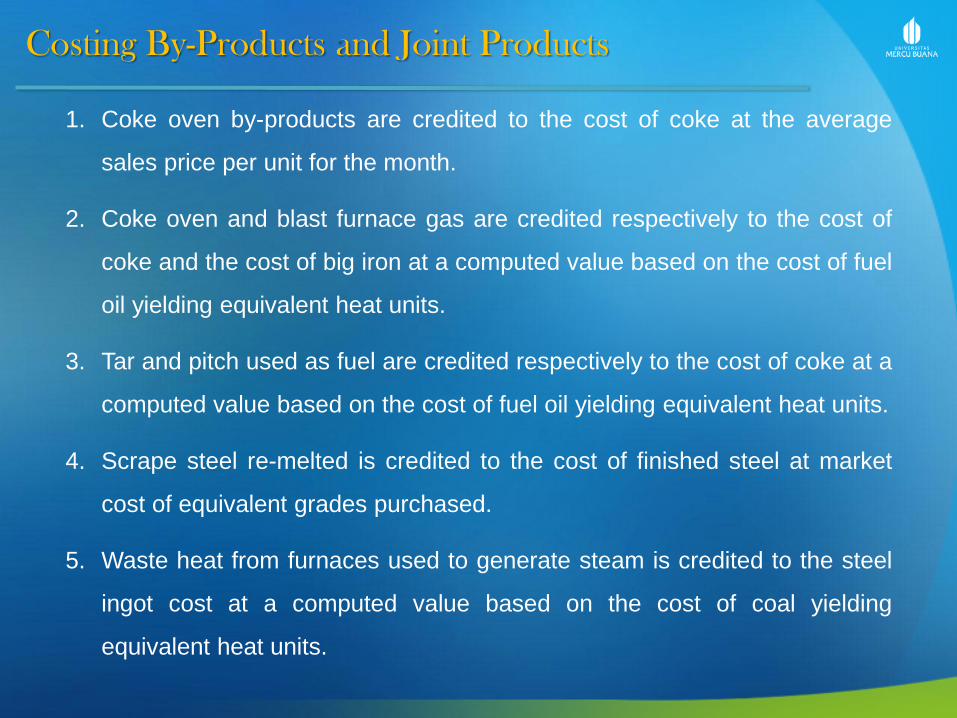

1. Coke oven by-products are credited to the cost of coke at the average

sales price per unit for the month.

2. Coke oven and blast furnace gas are credited respectively to the cost of

coke and the cost of big iron at a computed value based on the cost of fuel

oil yielding equivalent heat units.

3. Tar and pitch used as fuel are credited respectively to the cost of coke at a

computed value based on the cost of fuel oil yielding equivalent heat units.

4. Scrape steel re-melted is credited to the cost of finished steel at market

cost of equivalent grades purchased.

5. Waste heat from furnaces used to generate steam is credited to the steel

ingot cost at a computed value based on the cost of coal yielding

equivalent heat units.

Costing By-Products and Joint Products

Market Value Method or Reversal Cost Method:

Market value method or reversal cost method is similar to the last technique (By Product

Revenue deducted from Production Cost) illustrated at recognition of gross revenue method

page. However it reduces the manufacturing cost of the main product , not by the actual

revenue received, but by an estimate of the by products value at the time of recovery. This

estimate must be made prior to split-off from the main product. Dollar recognition depends

on the stability of the market as to price and stability of by product; however, control over

quantities is important. The by product account is charged with this estimated amount and

the production (manufacturing) cost of the main product is credited. Any additional costs of

materials, labor, or factory overhead incurred after the by-product is separated from the main

product are charged to the by product. The marketing and administrative expenses might

also be allocated to the by product on some equitable basis. The proceeds from sales of the

by product are credited to the by-product account. The balance in this account can be

presented on the income statement in one of the ways outlined for recognition of gross

revenue method except that the manufacturing cost applicable to by product inventory

should be reported in the balance sheet.

Costing By-Products and Joint Products

Methods of Allocating Joint Production Cost to

Joint Products

Market or Sales Value Method-Allocation of Joint Cost:

Market or sales value method enjoys great popularity because of the

argument that market value of any product is a manifestation of the cost

incurred in its production. The contention is that if one product sells for more

than another, it is because more cost was expended to produce it. Therefore,

the way to prorate the joint cost is on the basis of the respective market

values of the items produced. The method is really a weighted market value

basis using the total market or sales value of each unit (quantity sold times

the unit sales price).

Costing By-Products and Joint Products

Quantitative or Physical Unit Method-Allocating Joint Product Cost:

Quantitative or physical unit method attempts to distribute the total joint cost

on the basis of some unit of measurement, such as pounds, gallons, tons, or

board feet. Of course, the unit products must be measurable by the basic

measurement unit. If this isn't possible, the joint units must be converted to a

denominator common to all units produced, For example, in the manufacture

of coke, products such as coke, coal tar, benzol, sulfate of ammonia, and gas

are measured in different units. The yield of these recovered units is

measured on the basis of the quantity of product extracted per ton of coal.

Costing By-Products and Joint Products

Average Unit Cost Method-Allocating Joint Product Cost:

Average unit cost method attempts to apportion total joint production cost

to the various products on the basis of a predetermined standard or index

of production. An average unit cost is obtained by dividing the total

number of units produced into the total joint production cost. As long as all

units produced are measured in terms of the same unit and do not differ

greatly, the method can be used without too much misgiving. When the

units produced are not measured in like terms, the method cannot be

applied.

Costing By-Products and Joint Products

Joint Cost Analysis for Managerial Decisions and Profitability Analysis

Joint cost allocation methods indicate that the amount of the cost to be apportioned to the

various products emerging at the split-off point is difficult to establish for any purpose.

Furthermore, the acceptance of an allocation method for the apportionment of joint cost does

not solve the problem. The idea has been advanced that no attempt should be made to

determine the cost of individual products up to the split-off point; rather, it seems important to

calculate the profit margin in terms of total combined units. Of course, costs incurred after the

split-off provide management with information needed for decisions relating to the desirability

of any further processing.

For profit planning, management should consider a joint product’s contribution margin after

separable costs-those incurred after split-off- are deducted from sales. This contribution

margin allows management to predict the amount that a segment or product line will add to or

subtract from company profits.

Terima Kasih Suryadharma Sim, SE, M. Ak