Embed Size (px)

Citation preview

Modul ke:

Fakultas

Program Studi

Akuntansi Biaya Job Order Costing

Suryadharma Sim, SE, M. Ak

04 Ekonomi dan

Bisnis

S1 Manajemen

Job Order Costing

Overview of Job Order Costing In job order costing, or job costing, production costs are accumulated for each separate job; a job is the output identified to fill a certain customer order or to replenish an item of stock on hand. This differs from process costing, in which costs are accumulated for an operation or a subdivision of the company, such as department. For job costing to be effective, jobs must be separately identifiable. Details about a job are recorded on a job order cost sheet, or simply cost sheet, which can be in paper or electronic form. Although many jobs may be worked on simultaneously, each cost sheet collects details for one specific job.

Job Order Costing

The record keeping and cost assignment problems are more complex in a

job order costing system when a company sells many different products and

services than when it has only a single product or service. Since the products

are different, the costs are typically different. Consequently, cost records

must be maintained for each distinct product or job. For example an attorney

in a large criminal law practice would ordinarily keep separate records of the

costs of advising and defending each of her clients. And a clothing factory

would keep separate track of the costs of filling orders for particular styles,

sizes, and colors of jeans. A job order costing system requires more effort

than a process costing system. Companies classify manufacturing costs into

three broad categories: (1) direct materials, (2) direct labor, (3) manufacturing

overhead.

Job Order Costing

Accounting for Materials Materials Purchased Cost accounting for purchased materials is the same as it is for any perpetual inventory system. As materials are received, the account Materials is debited (rather than Purchases, in a periodic inventory system). Rayburn Company received a shipment of $25,000 of purchased materials on January 5. The journal entry is: Materials 25,000 Accounts Payable 25,000 Materials Used The flow of direct materials from storeroom to factory is accounted for as a transfer of cost from Materials to Work in Process. Often this is done in summary from at the end of a month or other period. A total of $31,000 of direct materials were requisitioned in January at Rayburn Company, consisting of $2,510 for Job 5574, $24,070 for Job 5575, and $4,420 for Job 5576. The summary entry is: Direct materials; Work in Process 31,000 Materials 31,000

Job Order Costing

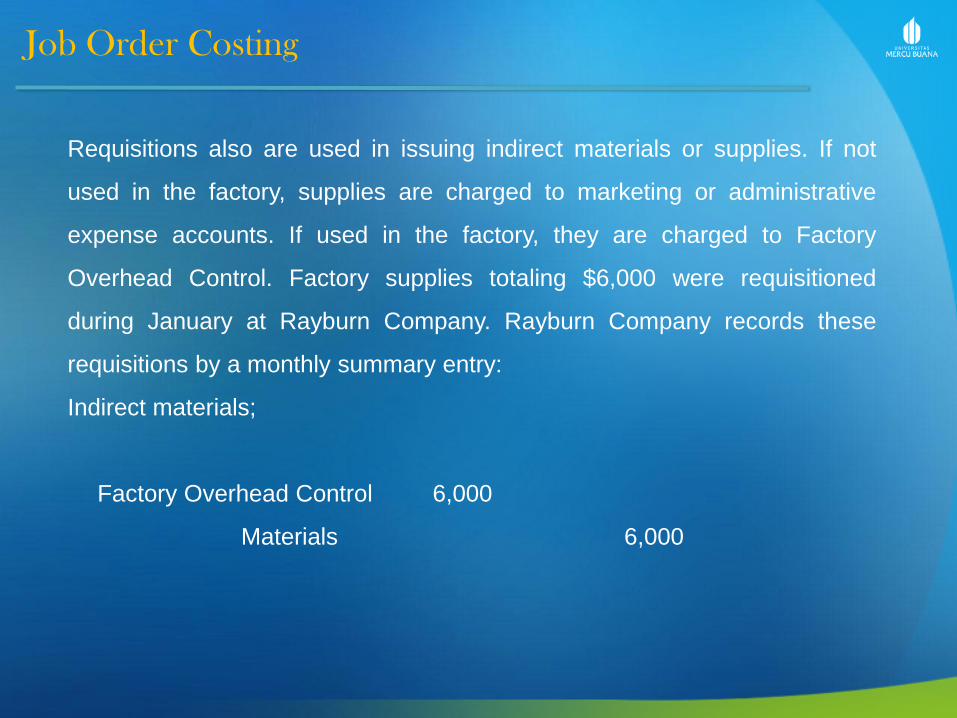

Requisitions also are used in issuing indirect materials or supplies. If not

used in the factory, supplies are charged to marketing or administrative

expense accounts. If used in the factory, they are charged to Factory

Overhead Control. Factory supplies totaling $6,000 were requisitioned

during January at Rayburn Company. Rayburn Company records these

requisitions by a monthly summary entry:

Indirect materials;

Factory Overhead Control 6,000

Materials 6,000

Job Order Costing

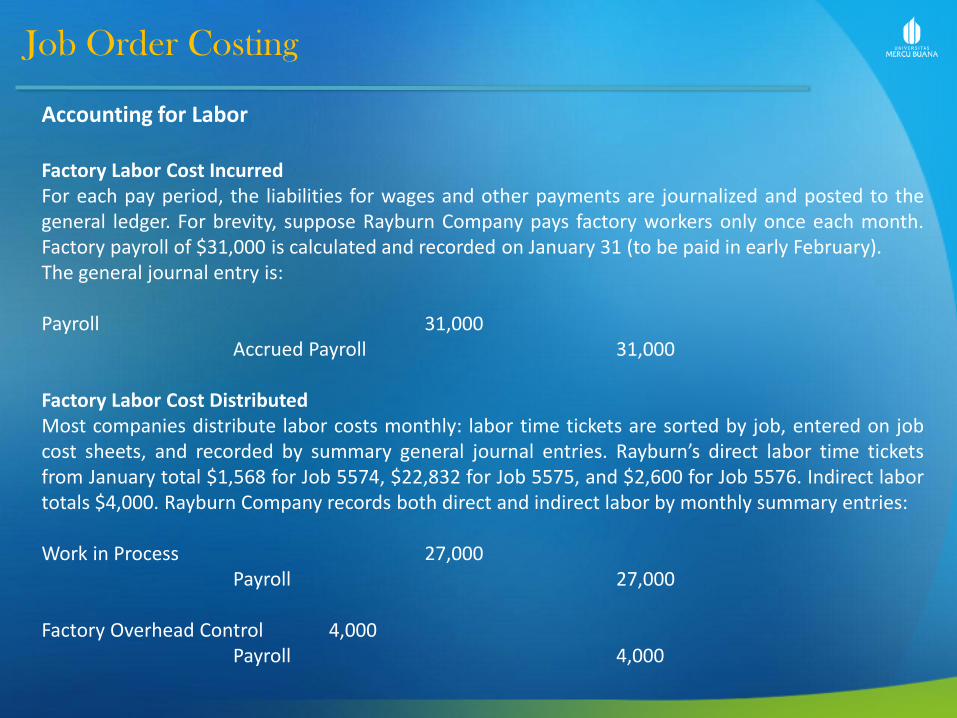

Accounting for Labor Factory Labor Cost Incurred For each pay period, the liabilities for wages and other payments are journalized and posted to the general ledger. For brevity, suppose Rayburn Company pays factory workers only once each month. Factory payroll of $31,000 is calculated and recorded on January 31 (to be paid in early February). The general journal entry is: Payroll 31,000 Accrued Payroll 31,000 Factory Labor Cost Distributed Most companies distribute labor costs monthly: labor time tickets are sorted by job, entered on job cost sheets, and recorded by summary general journal entries. Rayburn’s direct labor time tickets from January total $1,568 for Job 5574, $22,832 for Job 5575, and $2,600 for Job 5576. Indirect labor totals $4,000. Rayburn Company records both direct and indirect labor by monthly summary entries: Work in Process 27,000 Payroll 27,000 Factory Overhead Control 4,000 Payroll 4,000

Job Order Costing

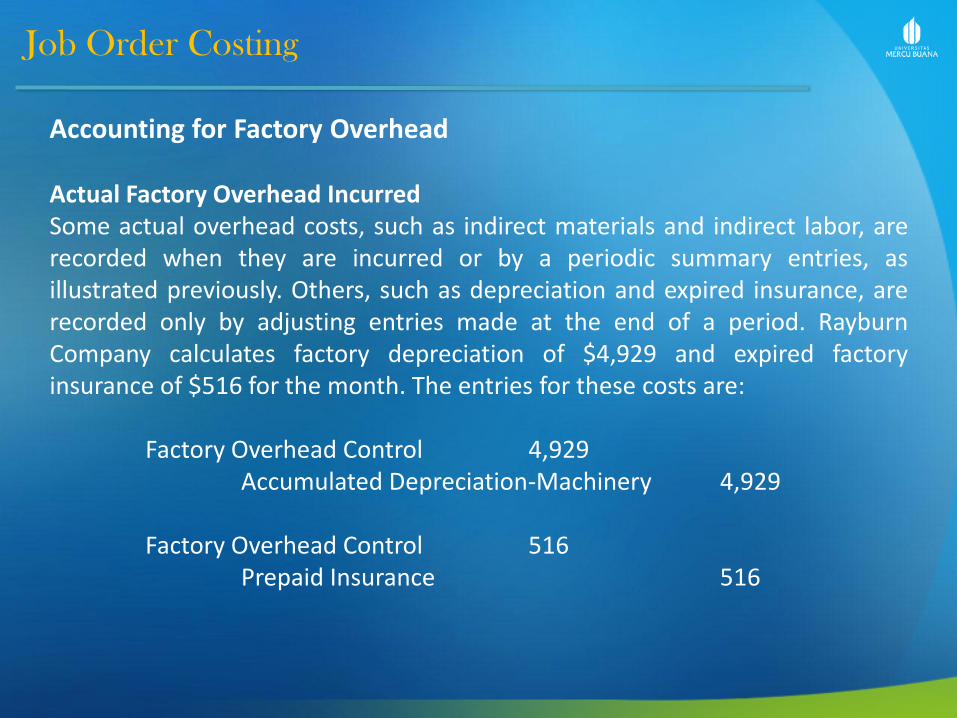

Accounting for Factory Overhead Actual Factory Overhead Incurred Some actual overhead costs, such as indirect materials and indirect labor, are recorded when they are incurred or by a periodic summary entries, as illustrated previously. Others, such as depreciation and expired insurance, are recorded only by adjusting entries made at the end of a period. Rayburn Company calculates factory depreciation of $4,929 and expired factory insurance of $516 for the month. The entries for these costs are: Factory Overhead Control 4,929 Accumulated Depreciation-Machinery 4,929 Factory Overhead Control 516 Prepaid Insurance 516

Job Order Costing

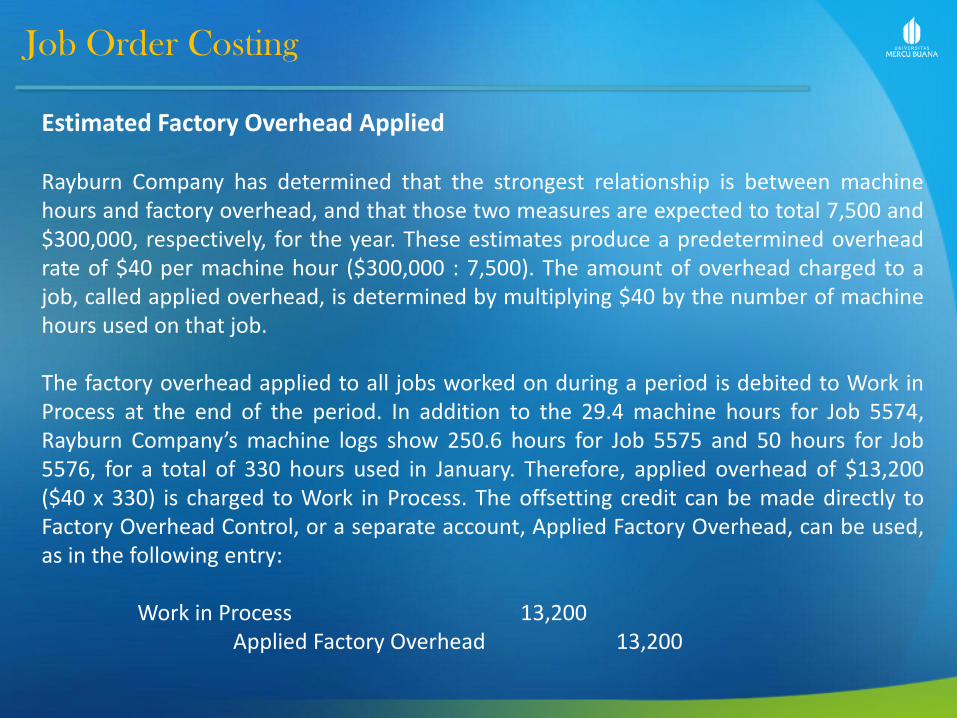

Estimated Factory Overhead Applied Rayburn Company has determined that the strongest relationship is between machine hours and factory overhead, and that those two measures are expected to total 7,500 and $300,000, respectively, for the year. These estimates produce a predetermined overhead rate of $40 per machine hour ($300,000 : 7,500). The amount of overhead charged to a job, called applied overhead, is determined by multiplying $40 by the number of machine hours used on that job. The factory overhead applied to all jobs worked on during a period is debited to Work in Process at the end of the period. In addition to the 29.4 machine hours for Job 5574, Rayburn Company’s machine logs show 250.6 hours for Job 5575 and 50 hours for Job 5576, for a total of 330 hours used in January. Therefore, applied overhead of $13,200 ($40 x 330) is charged to Work in Process. The offsetting credit can be made directly to Factory Overhead Control, or a separate account, Applied Factory Overhead, can be used, as in the following entry: Work in Process 13,200 Applied Factory Overhead 13,200

Job Order Costing

Applied Factory Overhead usually is closed to Factory Overhead

Control at year-end, but for illustrative purposes assume Rayburn Company closes Applied Factory Overhead monthly. If the preceding $13,200 journal entry is the only application of overhead for the month, the closing entry is: Applied Factory Overhead 13,200 Factory Overhead Control 13,200

Job Order Costing

Accounting for Jobs Completed and Products Sold As jobs are completed, their cost sheets are moved from the in-process category to a finished work file. Rayburn Company completed Jobs 5574 and 5575 during January at costs of $5,254 and $56,926, respectively. A job for a specific customer can be shipped when completed and thus never enter finished goods inventory; Sales and Cost of Goods Sold are recorded when the job is transferred from Work in Process. Because Job 5574 was shipped immediately to Lawrenceville Construction Company on January 18, it is not included in the entry transferring completed work to Finished Goods. Only Job 5575 is transferred to Finished Goods, and the completion of Job 5574 is recorded by the following entries: Accounts Receivable 7,860 Sales 7,860 Cost of Goods Sold 5,254 Work in Process 5,254 Job 5575 was transferred to Finished Goods to replenish stock, and the entry recording the transfer was made at month-end as follows: Finished Goods 56,926 Work in Process 56,926

Job Order Costing

Rayburn Company shipped finished goods costing $52,300,

consisting of a portion of Job 5575 and portions of various jobs that were completed in the preceding year. The sales price was $70,000, and the entries are: Account Receivable 70,000 Sales 70,000 Cost of Goods Sold 52,300 Finished Goods 52,300

Job Order Costing

Non-manufacturing Costs:

In addition to manufacturing costs, companies also incur marketing and selling costs. These

costs should be treated as period expenses and charged directly to the income statement

and therefore should not go into the the manufacturing overhead account. To illustrate the

correct treatment of non-manufacturing costs, assume that the company (in this example)

incurred $30,000 in selling and administrative salary costs during a months, the following

entry records these salaries.

Salaries expense 30,000 Dr

Salaries and wages payable 30,000 Cr

Depreciation on factory equipment is debited to manufacturing overhead account but

depreciation on office equipment is considered a period expense and is not included in

manufacturing overhead. Assume that depreciation of office equipment during the month

was $7,000. The entry is as follows.

Depreciation expense 7,000 Dr

Accumulated depreciation 7,000 Cr

Job Order Costing

Finally assume that advertising was $42,000 and that other selling and administrative

expenses during the month was $8,000. The following journal entry records these items:

Advertising expenses 42,000 Dr.

Other selling and administrative expense 8,000 Dr.

Accounts payable 50,000 Cr.

Since the amounts in entries above all go directly into expense accounts, they will have no

effect on the costing of the company's production for the month. The same will be true of any

other selling and administrative expenses incurred during the month including sales

commission, depreciation on sales equipment, rent on office facilities, insurance on office

facilities, and related costs.

Job Order Costing

Job Order Costing in Service Businesses In service businesses where jobs differ from each other and cost information is desired for individual jobs, several varieties of job order costing are used. These service businesses include tailors, lawn service companies, temporary-help companies, repair shops, and professional services such as legal, medical, architectural, engineering, accounting, and consulting. In these businesses, direct labor and labor-related costs are usually larger than any other cost, often by a wide margin, so the predetermined overhead rate typically is based on direct labor cost. It is also common to combine labor cost with the predetermined overhead rate, so the amount charged to a job for each hour of direct labor represents both labor and overhead. Job order costing is also used in service organizations such as law firms, movie studios, hospitals, and repair shops, as well as manufacturing companies. In a law firm, for example, each client represents a "job," and the costs of that job are accumulated day by day on a job cost sheet as the client's case is handled by the firm. Legal forms and similar inputs represent the direct materials for the job; the time expended by attorneys represents the direct labor; and the costs secretaries, clerks, rent, depreciation, and so forth, represent the overhead.

Job Order Costing

In a movie studio, each film produced is a "job," and costs for direct materials (customs,

props, film, etc.) and direct labor (actors, directors and extras) are accounted for and

charged to each film's job cost sheet. A share of the studio's overhead costs, such as

utilities, depreciation of equipment, wages of maintenance workers, and so forth, is also

charged to each film. However, the method used by some studios to distribute overhead

costs among movies are controversial and sometimes result in lawsuits.

In sum, the reader should be aware that Job order costing is a versatile and widely used

costing method, and may be encountered in virtually any organization that provides diverse

products or services.

Terima Kasih Suryadharma Sim, SE, M. Ak