Embed Size (px)

Citation preview

BUSINESS

Philippine ANALYST August 2014

36BUBUBUBUSISISISINENENENESSSSSSSSBUSINESS

Aerospace, electric vehicles industry roadmaps revealedThe aerospace industry and electric vehicles industry revealed its roadmap during the Board of Investments’ forum held last July 24. The industry roadmaps aim to make the Philippines globally competitive by boosting sales and production targets and through increased government support.

The roadmaps were presented by the Aerospace Industries Association of the Philippines (AIAP) and the Electric Vehicle Association of the Philippines (EVAP). Aside from

these industries, 12 other industries have released their respective roadmaps with the goal of developing further investments in the Philippines. This includes: manufacturing, copper, iron and steel, cement, chemicals, creative industries, jewelry, furniture, paper, mass housing, rubber, and natural health products.

According to AIAP, the Philippine aerospace industry for 2013-2022 is envisioned to become “a major hub for manufacturing of original equipment manufacturer (OEM) parts and allied services for the global commercial aircraft industry.” The local industry is expected to become a $1.4 billion industry by 2022 from $385 million in 2013 – or an annual increase of approximately 29%. It is also expected to increase its employment generation to 8,300 (see chart).

Meanwhile, the electric vehicle industry roadmap for 2014-2024 aims to accelerate the country’s conversion from gas-powered to electric vehicles, and to develop a transportation landscape that is “one with the environment.” It also aims to increase domestic industry sales by almost 2000%, from P214 million in 2013 to P4.4 billion in 2015. EVAP executive director Roberto Cruz said the industry expects to produce 38,220 units this year and 69,145 units in 2017. Annual growth rate is targeted at 11-

13%. The roadmap presented by EVAP has 4 phases: the 1st phase will be implemented in 2014, the 2nd phase in 2015 to 2016, the 3rd phase in 2017 to 2019, and the 4th phase in 2020 to 2024 (see table).

Both the aerospace and electric vehicle industry called on government support to help them overcome the challenges faced by their respective industries and to achieve the targets stated in the roadmap (see table). At present, the 2 industries are still small

The aerospace industry is seen to become a $1.4 billion industry by 2022, while the electric vehicles industry aims to increase production to 69,145 units in 2017.

37BUSINESS

Philippine ANALYST August 2014

particularly when compared with other countries. In 2010, data from the World Trade Services shows that the Philippine aerospace industry had total investments of $150 million, whereas Singapore had $4.6 billion, Indonesia $234 million, and Malaysia $1 billion. Similarly, the electric vehicle industry produced only 168,000 units in the same year, well below Thailand’s 800,000 units, Indonesia’s 765,000 units, and Malaysia’s 605,000 units. The industry currently has 20 local e-vehicle manufacturers/importers and 8 foreign investments while employing 42,000 people.

The creation of a roadmap for the 2 industries may be the beginning of their continuous development. Both still face numerous challenges involving policies, bureaucracy, and training and development. They need stronger government support.

Source: EVAP

Source: AIAP, EVAP

4 PHASES OF THE ELECTRIC VEHICLE INDUSTRY ROADMAP

YEAR(S) DESCRIPTION PLANS

2014 Program development and approval

Formulation of electric vehicle development programa. Charting of implementing rules and regulationsb. Creation of incentives programc. Passing and approval of Executive Order

Program implementation/registration and monitoring

2015-2016 Local market buildup/ production capacity enhancement

Domestic market buildup: critical support from government Incentive program to strengthen auto parts industry Intensive investment promotion to attract foreign and domestic investment fl ows to the sector

2017-2019 Local and export markets expansion Increase in industry output and manufactures electric vehicles and more parts and components for

both domestic and export

Labor capacity building, skills and capital accumulation

2020-2024 Full integration of EV with auto industry / Technological advancement

Full integration of the automotive industry Complementation between EV industry, automotive industry, and all related industries Resources integration for established regional and global networks

GAPS MEASURES

Policy Include Aerospace Manufacturing as a pioneering industry with extension of Tax Holidays from 4-6 years to 6-8 years in the

2014 Investment Priority Plan (IPP) Maintain status of the Philippines as a Category 1 country by International Aviation Regulatory Standards.

Training and education Investments in training and development

Government programs and incentives Provide continuous review and improvement of policies and incentives that are supportive of the industry

Administrative bottlenecks Make government programs and incentives more attractive to entice investors Streamline import/export lead times and procedures for faster transaction processing

High costs and fi nancing Passage of SB 2856 (HB 5460) or the “Electric, Hybrid, and Other Alternative Fuel Vehicles Incentives Act” to bring down

the price given fi scal incentives Creation of special vehicle pollution control fund (P3.4 billion) to support electric vehicle manufacturing

Technological issues Establish standards and regulations for electric vehicles and charging stations Rigid education and training to overcome problem on social acceptance Device effi cient methods and systems to lower cost of battery replacement and improve waste disposal

Bureaucracy Update and systematize Land Transportation Offi ce’s registration process

0

200

400

600

800

1000

1200

1400

1600

PHILIPPINE AEROSPACE INDUSTRY (in USD Million)

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

AEROSPACE INDUSTRY PROJECTED EMPLOYMENT GENERATION

HOW THE GOVERNMENT CAN HELP THE AEROSPACE AND ELECTRIC VEHICLE INDUSTRY

Source: AIAP Source: AIAP

38 BUSINESS

Philippine ANALYST August 2014

Credit surety funds to help MSME’s bank credit access

A bill that will enhance bank credit access through the institutionalization of credit surety fund (CSF) cooperatives for micro, small and medium entrepreneurs (MSMEs) is being deliberated in the Congress.

Banks are hesitant to extend credit to MSMEs as the risk of default in the sector is high. Banks’ compliance with the requirement to provide loans to micro and small enterprises was only at 6.1% in 2013, below the mandated allocation of 8% under the Magna Carta for MSMEs. In particular, universal banks which compose 49% of total banks, have under-complied since 2008 (see table). Large banks normally opt to pay the P500,000 fi ne for under compliance rather than extending credit to MSMEs. Particularly discouraging are MSMEs’ lack of acceptable collateral, unstable income or cash fl ows, and lack of business experience or track record. House Bill 278 aims to increase credit availability for MSMEs especially those in the countryside through the establishment of CSF cooperatives.

HB 278 or the “Credit Surety Fund and CSF Coop Act”,would establish special cooperatives that will help MSMEs in the areas of credit evaluation, loan and risk management

ITEM 2008 2009 2010 2011 2012 2013*Net loan portfolio (P mil.) 1,637,533 1,728,628 1,881,139 2,303,436 2,912,347 3,070,505

Min. amount required to be set aside ** (P mil.) 163,753 172,863 188,114 230,344 291,235 307,050

Total funds set aside for MSMEs (P mil.) 310,882 309,357 308,554 348,915 387,681 384,579

Compliance for MSEs (%) 10.0 9.7 8.5 7.6 6.4 6.1

Universal and Commercial Banks 7.1 7.1 6.8 5.8 5.3 4.8

Thrift Banks 16.4 16.1 14.0 16.2 11.3 10.8

Rural and Cooperative Banks 51.8 41.1 34.1 29.6 22.3 26.5

Compliance for MEs (%) 9.0 8.2 7.8 7.6 6.9 6.4

Universal and Commercial Banks 8.3 7.9 7.7 7.4 6.7 6.2

Thrift Banks 12.9 8.9 8.6 8.0 7.8 7.7

Rural and Cooperative Banks 11.4 12.8 12.0 10.5 9.5 8.9

ME = medium-sized enterprise, MSE = micro and small enterprise, SME = small and medium-sized enterprise.Notes: Compliance required under the Republic Act No. 6977 (amended by RA No. 8289 and 9501).* as of June 2013* * 8% of net portfolio to micro and small enterprises and 2% to medium-sized enterprisesSource: Asia SME Finance Monitor 2013 by the Asian Developmental Bank.

PARTICIPANT BENEFIT

Well-Capitalized Cooperatives

Provide its members of good standing access to formal sources of credit like banks

Increased membership and capital

Additional income derived from surety fees

MSMEs

Access to broader sources of fi nancing

Lower cost of borrowing

Formal training on business management

Banks Avenue for complying with required lending allocation to MSMEs as mandated under theMagna Carta for MSMEs

Credit risks associated with extending loans to MSMEs are mitigated

LGUs Supports poverty-alleviation and economic programs

Contribution to the CSF will not be perceived as a dole-out

COMPLIANCE WITH MSME LOANS REQUIRED

BENEFITS OF THE CREDIT SURETY FUND (CSF)

Source: Bangko Sentral ng Pilipinas

as well as good governance. These special CSF cooperatives will manage its member-cooperatives’ CSF, which is pooled from contributions of the members, local government units and partner non-governmental institutions. The CSF is used by MSMEs as a substitute for collaterals normally accepted by banks. In case of a default from the MSME, the CSF guarantees to pay the claim of the lending bank.

Qualifi ed borrowers of the CSF include MSME members of a member-cooperative, member-cooperatives themselves, and member-NGOs (see table). In order to be a member of the CSF coop, cooperatives must have a minimum capital-to-assets ratio of 30% or a capital-to-risk assets ratio of 20% or higher.

The Philippine Exporters Confederation (PhilExport) supports the passage of the bill, saying it could determine the success or failure of MSMEs which are resorting more and more to informal lending for their funding requirements. The institutionalization of CSFs would address the issue of insuffi cient collateral for MSME loans, which is the main reason why banks decline credit requests from MSMEs, PhilExport added. PhilExport said that LGUs should allocate contributions to the CSF from taxes, licenses and registration fees generated from activities in their area.

The BSP has already established 29 CSFs across the country, with total loans given at P1.07 billion. This has improved from 26 CSFs in 2012 with P615.6 million worth

The establishment of CSFs supports poverty alleviation in municipalities.

39BUSINESS

Philippine ANALYST August 2014

PHILIPPINE CONSUMER CONFIDENCE AND INDICATORS (2005-2014)

of extended loans. It aims to build 7 more by the end of 2014 and another 6 by 2015. The BSP said that the establishment of CSFs supports poverty alleviation in municipalities through job creation and increased economic activities. To ensure the continuous fl ow of credit to the countryside, the BSP has allowed for rediscounting by banks of the CSF’s surety cover.

There were 816,759 MSMEs in the Philippines, comprising 99.6% of total businesses. MSMEs in the trade and repair sector comprised 47% of the total, followed by services with 38.5%. The sector also created 3.87 million jobs in 2011, up by 9.6% from 2010. However, MSMEs only contributed 35.7% of the total gross value added in the business sector in 2006.

PH consumer confi dence up in 2Q2014

Consumer confi dence for the 2nd quarter of 2014 remained robust, according to a global consumer survey. This was despite other Southeast Asian countries seeing a dip in their consumer confi dence scores.

The Philippines increased its consumer confi dence index to 120 in the Nielsen Global Survey of Consumer Confi dence and Spending for 2Q2014. This was 4 points ahead of its score in the 1st quarter. It was the 2nd highest score amongst Southeast Asian countries and 3rd globally (behind India and Indonesia) (see table). Most Southeast Asian countries recorded declines as political instability and food prices rose in the region. Only the Philippines and Malaysia were able to raise their scores among their neighbors.

The Philippines’ high consumer confi dence score means that Filipinos are willing to spend more in the short term and are confi dent in their personal fi nances and job prospects. All 3 indicators were on an uptrend and near record-highs (see chart), with 80% of Filipino respondents expressing confi dence about their personal fi nances (versus 79% last quarter) and 77% being confi dent about their job prospects (up from 71%). Meanwhile, 51% thought now is the opportune time to buy (up from 50%).

The rise in consumer confi dence is attributed mainly to the growing middle class population. According to the National Statistical Coordination Board, almost 25% of Filipinos belong to the middle class with per-capita incomes ranging from P66,000 to P805,000. The National Capital Region has the highest concentration of middle-class families at around 51-54%. The rise of the middle class is also supporting the continuous growth in the country’s retail sector.

The Nielsen survey also revealed that concerns of the Filipino consumer are more focused on the household rather than the country’s overall economic condition. Job security and work/life balance were the main concerns of the Filipino consumer (see box). Meanwhile, the overall economy was among the 2 main concerns for consumers in Indonesia, Malaysia, Thailand, Singapore and Vietnam. Political stability and war were also concerning consumers in Indonesia, Thailand and Vietnam. These results refl ect the Filipinos’ optimism in the country’s economic and political environment (the percentage of Filipinos thinking that the country is in recession has continuously dropped from 79% in 1Q2009 to 48% at present (see chart).

OVERALL RANK COUNTRY INDEX CHANGE FROM Q1

1 India 128 +7

2 Indonesia 123 -1

3 Philippines 120 +4

4 China 111 0

7 Thailand 105 -3

9 Hong Kong 103 -8

15 New Zealand 99 -1

16 Singapore 98 -1

18 Vietnam 98 -1

22 Malaysia 93 +1

27 Australia 85 -4

41 Taiwan 75 -1

43 Japan 73 -8

55 South Korea 53 +2

2Q 2014 RANKING OF CONSUMER CONFIDENCE AMONG ASIA-PACIFIC COUNTRIES

Source: Neilsen Global Survey of Consumer Confi dence & Spending Intentions, 2Q 2014

Legend: Blue=confi dence on personal fi nances: Gray=confi dence on job prospects; Orange= confi dence on short-term sendingSource: Nielsen Consumer Confi dence Trend Tracker.

40 BUSINESS

Philippine ANALYST August 2014

PHILIPPINE CONSUMER CONFIDENCE AND INDICATORS (2005-2014)

Legend: Green=percentage of consumers changing spending to save more; Red= percentage of consumers who feel their country is in recession Source: Nielsen Consuemr Confi dence Trend Tracker.

RANK CATEGORIES AD SPEND, IN MILLION PESOS1 Hair shampoos, rinses, treatments/hairdressing products 6,691

2 Detergents and laundry preparations 6,481

3 Communication/telecommunication 4,726

4 Other food products/other than biscuits and bakeshop 4,121

5 Powder milk 3,732

6 Skin care 3,170

7 Dentrifi ces, mouthwash and toothbrush 3,075

8 Proprietary drugs/other than vitamins and tonics 2,667

9 Flour, bakery products and bakeshop 2,400

10 Entertainment 2,313

New clothing

Gas and electricity

Technology upgrade

ITEMS WHERE FILIPINOS SAVE THE MOST

The survey showed 80% of Filipino consumers see their personal fi nances over the next 12 months as good or excellent (see chart). Meanwhile, savings remain an important part of the fi nances of Filipinos, with 80% rechanneling their spending to save on household expenses. Cutting expenses on clothing was the top way for Filipinos to handle their income (see box).

Although the income levels of Filipinos are expanding, consumers are still focused on saving for emergencies and the future as well as managing their long-term fi nancial goals. In order to tap the expanding Filipino middle class, Nielsen recommends producers to develop a wide range of products and services that will provide good value for the consumers’ money.

1. Job security

2. Work/life balance

3. Health

4. Increasing utility bills

5. Children’s education and/or welfare

MAJOR CONCERNS OF FILIPINO CONSUMERS IN THE NEXT 6 MONTHS

Source: Nielsen Global Survey of Consumer Confi dence & Spending Intentions, 2Q 2014

1. Savings

2. Paying off debts/credit cards/loans

3. Holidays

4. Investing in shares of stock/mutual funds

AREAS WHERE FILIPINO CONSUMERS ALLOCATE THEIR SPARE CASH

Source: Nielsen Global Survey of Consumer Confi dence & Spending Intentions, 2Q 2014

Source: Nielsen GCCSI 2Q 2014 and BSP Consumer Expectations Survey 2Q 2014

ITEMS WHERE ADVERTISERS SPEND THE MOST

Source: Nielsen Philippines.

41BUSINESS

Philippine ANALYST August 2014

Sales of cement industry increase in 1H2014

The cement industry recorded an increase in sales of 3.2% during the 2nd quarter and by 5.7% for the 1st half of the year as demand from the public and private sector continued to grow.

The Cement Manufacturers’ Association of the Philippines (CeMAP) said that cement sales grew by 3.2% in the 2nd quarter from 5.349 million metric tons (MT) in the same period last year to 5.519 million MT. Sales also grew in the 1st half of 2014, rising by 5.7% from 10.136 million in 2013 to 10.718 million. The cement industry recorded its highest sales growth in 15 years last 2012, with a 17.5% increase from 15.595 million MT in 2011 to 18.356 million MT in 2012.

The increase in sales of cement is attributed to the increased demand in the construction industry from both the public and private sector. BCI Asia, a construction market research fi rm, dubbed 2013 as the “birth of new construction” for the Philippines following the increase in government expenditure and the civil construction works on infrastructure. Data from the Department of Budget and Management (DBM) showed that government spending for infrastructure and capital outlay increased by 24.5% to P92.7 billion in the 1st 4 months of the year from the P75.2 billion in 2013. The devastation brought about by Category-5 Typhoon Haiyan in November 2013 to airports, seaports, power lines, hospitals, houses, cargo terminals, and other infrastructure triggered this increase in spending for the reconstruction and rehabilitation efforts.

Despite this, the cement industry sees fl at growth in sales this year because of the slow approval of infrastructure projects under the Aquino administration’s Public Private Partnership (PPP) scheme. According to CeMAP, the PPP projects “are not moving fast enough to start construction this year.” The program has had several delays in the bidding process, faced right-of-way (RoW) issues, and had numerous complaints from losing bidders. These hinder the steady progress of infrastructure projects. So far, only 8 projects have been awarded of the 57 in the pipeline, while 5 are still for bid submission. Improvement of the current system is necessary to aid the growth of the country’s industries. Managing director general of the Asian Development Bank Juan Miranda said that the PPP thrust of the Philippines “is not bad but can be better”, noting that “a good PPP is one where there are no disagreements between the 2 sectors, hence its title ‘public and private partnership.’” He added, ”To be better, Manila’s PPP program needs changes that will do away with legal hurdles, which are causing delays in building better infrastructure.”

In the Oxford Business Group’s “The Report: The Philippines 2014” which provides an outlook of various industries, it is stated that expansion of the cement industry this year is expected to remain within the range of 9-10%. CeMAP forecasted that consumption will reach P26.6 million MT in 2017, up 39% from 2013 records. CeMAP is composed of the Cemex Philippines Group of Companies, Holcim Philippines, Inc., Lafarge Associated Companies, Northern Cement Corp., Pacifi c Cement Philippines, Inc., and Taiheiyo Cement Philippines, Inc.

050000100000150000200000250000300000350000400000450000500000

2008 2009 2010 2011 2012 2013

GROSS VALUE OF CONSTRUCTION, 2008-2013 (in million peso at 2000 constant prices)

Public Private

The industry sees fl at growth in sales this year because of the slow approval of infrastructure projects under PPP.

MINING, OIL, & GAS

Source: CEMAP 2013 Annual Report.

PH-EITI transparency report to be released in December

The Philippines is set to release its 1st comprehensive report on transparency in the Philippine extractive industry. The report covers major companies in the industry and will provide information that is currently not accessible to the public.

National Coordinator of the Philippine Extractive Industries Transparency Initiative (PH-EITI) Marie Gay Ordones said the fi rst Philippine country report is set for release in December as a requirement for its application to be included in the global EITI list. Information that will be published in the report is based on 2012 records – a long 2 years ago – and will contain an overview of the Philippine extractive industry, the legal framework, contracts and permits, licenses and cadasteral system, processes involving indigenous people (IPs), payments and types of revenues (taxes, fees, royalties, etc.), identifi cation of discrepancies, and the reconciliation of these discrepancies (if applicable). According to Ms. Ordones, “Though all revenue records are with different government agencies, there is no unifi ed system bringing all the

42 BUSINESS

Philippine ANALYST August 2014

information together for easier analysis and comparison.” The report will do this, and also address the following questions:

How much is the company getting from the extractive industries?

How do local communities benefit from extractive operations in their area?

How much do companies pay IPs or local governments to mine in their domains?

How are special funds (environmental and social development funds) managed?

Does the government collection tally with company payments?

How are revenues allocated? The PH-EITI is an initiative for the extractive industries

(mining, oil, and gas) that has been pushed by the Chamber of Mines of the Philippines since 2005 “to let the public know how much they are contributing to the country.” The EITI is a globally developed standard – currently with 29 compliant

countries – that promotes the principles of “transparency, good governance, sustainable development practice, and the improvement of the country’s investment climate.” The Philippines has been a candidate country since May 2013, and the process offi cially began through the creation of Executive Order 147 signed in November 2013. A multi-stakeholder group (MSG) composed of people from government, civil society organizations (CSOs), and the business community is mandated to complete the requirements for the country’s candidacy.

Analysis of data obtained for the report was done by an Independent Administrator, Isla Lipana, which was contracted by the PH-EITI team through public bidding. Isla Lipana is the local arm of Price Waterhouse Coopers, the group which has done EITI reports of other countries. The report will also be translated into different languages and dialects, and will be discussed to local governments and communities. The transparency report will be made annually “to cure the perceived ills of the mining industry”. According to Tess Tabada of Bantay Kita, a coalition representing CSOs in the MSG, EITI is critical as “…there has always been a lack of transparency

There is no unifi ed system bringing all information together for easier analysis and comparison.

COMPANIES THAT ALLOWED THE BIR TO DISCLOSE THEIR TAX RECORDS FOR THE REPORT

Benguet Corporation / Benguet Nickel Mines, Inc.

Cagdianao Mining Corp.

Rio Tuba Nickel Mining Corp.

Hinatuan Mining Corp.

Taganito Mining Corp.

Carmen Copper Corp.

Filiminera Resources Corp.

Lepanto Consolidated Mining Co.

OceanaGold (Philippines), Inc.

Philex Mining Corp.

Philsaga Mining Corp.

Platinum Group Metals Corp.

TVI Resource Development

Zambales Diversifi ed Metals Corp.

CTP Construction and Mining Corp.

Berong Nickel Corp.

Eramen Minerals, Inc.

Apex Mining Co., Inc.

Philippine Mining Development Corporation (PMDC)

LNL Archipelago Minerals, Inc.

Rapu-Rapu Minerals, Inc.

SR Metals, Inc.

Leyte Iron Sand Mining Corp.

SinoSteel Phils. H.Y. Mining Corp.

Cambayas Mining Corp.

Marcventures Mining and Development

Johson Gold Mining Corporation

Shenzhou Mining Group Corp.

Krominco, Inc.

Oriental Synergy Mining Corp.

Adnama Mining Resources, Inc.

Shuley Mine Incorporated

Carrascal Nickel Corporation

Ore Asia Mining and Development Corp.

Greenstone Resources Corp.

Shell Philippines Exploration B.V (SPEX)

Chevron Malampaya LLC

PNOC-Exploration Corporation

Nido Production Galoc. Pty. Ltd.

Galoc Production Company

COMPANIES THAT HAVE NOT YET SUBMITTED THEIR WAIVER FOR THE REPORT

Oriental Petroleum and Minerals Corp.

Alcorn Gold Resources Corp.

Trans Asia Oil and Energy Development Corp.

Semirara Mining Corporation

Pacifi c Nickels Philippines, Inc.

Mt. Sinai Mining Exploration and Development Corp.

Forum Energy Philippines Corp.

Forum Pacifi c, Inc.

Inclusion of the Philippines in the global EITI list is an important step towards government transparency.

Source: Various news clips

43BUSINESS

Philippine ANALYST August 2014

in the dealings of the mining companies with government and more so with the communities affected by their work.”

Of the 51 large-scale mining companies and major oil and gas companies (or those that reported total revenue/assets of more than $23 million each), 40 have already submitted a waiver allowing the Bureau of Internal Revenue (BIR) to disclose the company’s tax information for the report (see box). Three companies refused to disclose their fi nancial reporting, including Philodrill Corporation, AAM-PHIL Natural Resources Exploration and Development Corporation, and Citinickel Mines and Development Corporation.

Inclusion of the Philippines in the global EITI list is an important step towards the much-desired transparency in government, especially since countries that are already implementing EITI have reported improved revenue collection and economic growth. The Civil Society Organization-Multi Sectoral Group is currently crafting a draft bill that will mandate all companies in the extractive industry to divulge key information about their operations. Ms. Ordones said: “We want it to be mandatory… to make our report comprehensive, because what’s the point of coming up with a report that would only reveal a partial picture? We want to reap the full benefi ts of the process… So the ideal situation is to get 100% compliance.” She specifi cally highlighted the need for Semirara Mining Corporation to sign the waiver as it accounts for 94% of coal production. Finance Secretary Cesar Purisima has also been appealing for a 100% compliance rate, saying that there is a need to develop mining for the benefi t of the people.

I.T. UPDATETelevision white space technology to expand connectivity to rural areas

The Department of Science and Technology (DOST) is pushing for the Television White Space (TVWS) technology, which will expand internet connectivity to the Philippines’ isolated areas. Through the program, the DOST hopes to achieve a 99% internet penetration rate by 2015.

The TVWS program is one of the government’s leading programs which will develop and boost the country’s information and communications technology (ICT) infrastructure. The government will use the technology to provide internet connectivity and government services to people in the countryside. Among the government projects that can be supported by the TVWS include environmental sensor networks for project NOAH, educational content delivery for DepEd through the Cloud Top projects, as well as telemedicine by the University of the Philippines’ TeleHealth Center. Expanding the connectivity to far-fl ung areas will also help in maintaining the country’s lead in the IT-business process management sector.

Television white space refers to unused television frequencies in between broadcast TV channels. These frequencies can be used to accommodate internet band with connectivity. According to DOST, the technology is the preferred way to provide internet connectivity to the country’s isolated areas due to its long distance propagation characteristics and the ability of its signals to travel over water and through thick foliage like trees and mountains. The DOST added that it is cheaper and can be easily deployed.

The DOST-Information and Communications Technology Offi ce (ICTO) said that the nationwide rollout of the TVWS program will cost P3.5 billion, covering areas where commercial wired or wireless broadband service is lacking or totally non-existent.

A series of pilot testing were held in Bohol and Palo, Leyte by Filipino-Singaporean fi rm Nityo Infotech. Nityo Infotech was also tapped by DOST-ICTO to provide a TVWS system in Tacloban and Palo a week after the Super Typhoon Yolanda devastation. Nityo Infotech said they are ready to pour in additional investment for the expansion of the national broadband connectivity. Other partners for the pilot testing were Microsoft and Power Automation Co., a Singapore Power subsidiary.

44 BUSINESS

Philippine ANALYST August 2014

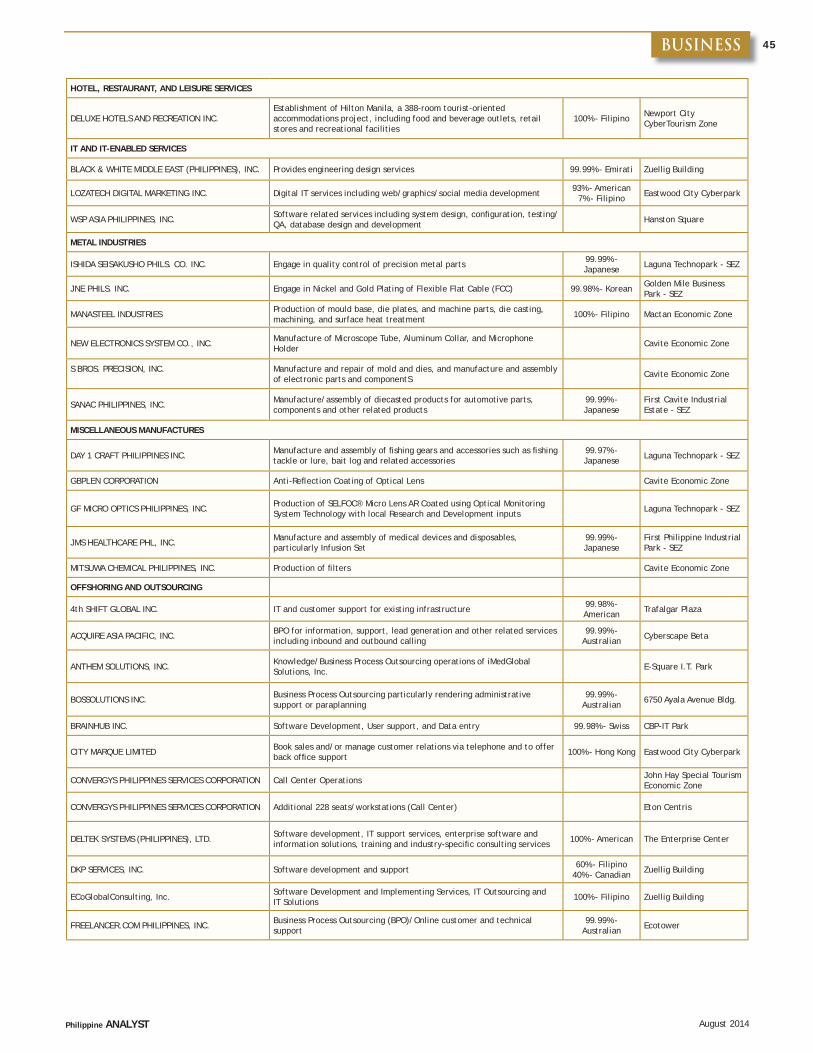

PEZA APPROVED PROJECTS

2nd Quarter 2014

INDUSTRY ACTIVITY EQUITY LOCAL/FOREIGN ZONE

APPAREL AND TEXTILE MANUFACTURES

FEEDER APPAREL CORPORATION Washing of Apparels and Auto-Cutting of Fabrics and Apparels Mactan Economic Zone

HP FASHION AND APPAREL MANUFACTURING CORP. Manufacture of wearing apparel for ladies/women and men 100% - Filipino Golden Mile Business Park - SEZ

MANILA OKABE APPAREL CORPORATION Manufacture of apparel 99.99% - Japanese

Carmelray Industrial Park I - SEZ

MOON DAE CORPORATION Manufacture of Knitted and Woven Tops, and Back Pack Bags and Pouch 100% - Filipino Victoria Wave - SEZ

AUTOMOTIVE TRADE

FURUKAWA ELECTRIC AUTOPARTS PHILIPPINES, INC. Manufacture of steering roll connectors (SRC) Laguna Technopark - SEZ

TRP, INC. Manufacture of automotive switches Toyota Sta. Rosa - SEZ

CHEMICAL AND CHEMICAL PRODUCTS

VISAYAS ACTIVATED CARBON INC. Manufacture of activated carbon from coconut shells 100% - Filipino New Jubilee Agro-Industrial Economic Zone

ELECTRICITY, WATER, AND GAS

FPIP UTILITIES, INC. Establishment, operation and maintenance of a power distribution facility

First Philippine Industrial Park II - SEZ

FPIP UTILITIES, INC. Establishment, operation and maintenance of a water distribution facility

First Philippine Industrial Park II - SEZ

ELECTRONICS

GF MICRO OPTICS PHILIPPINES, INC. Production of Waterproof Passive WDM Cassette using Optical Monitoring System Technology Laguna Technopark - SEZ

IONICS EMS, INC. Manufacture of Light Cure Device using its full design process with local Research and Development inputs

Light Industry & Science Park I - SEZ

IONICS EMS, INC. RMA or importation of defective fi nished goods manufactured by IEI, i.e., Wireless Broadband Access Unit, Hi-Focus Asymmetrical Digital Subscriber Line (ADSL) Broadband Access System, etc.

Light Industry & Science Park I - SEZ and Light Industry & Science Park II - SEZ

MAXIM PHILIPPINES OPERATING CORPORATION Assembly and Test (A & T) procedures and Test and Reel (T & R) activities Gateway Business Park - SEZ

MICROSEMI SEMICONDUCTORS-MANILA (PHILIPPINES), INC. Assembly and Test of Power Modules Food Terminal Inc. - SEZ

MOATECH MANUFACTURING PHILS., INC. Manufacture of Brushless DC (BLDC) Motor, Damper Unit, Pinion-type Stepping Motor (SP Motor), and Gear-type Stepping Motor (GSP Motor)

First Philippine Industrial Park - SEZ

NISSEN PHILIPPINES, INC. Manufacture and assembly of Network Communication Cable, Electric Fuse and Network Communication Optical Fiber Cable with Connector

99.99% - Japanese

Daiichi Industrial Park - SEZ

PV TECH PTE. LTD. Manufacture of Mono Crystalline Module Cavite Economic Zone II

ROHM ELECTRONICS PHILIPPINES, INC. Manufacture of Transistor and Diode Wideline Package People's Technology Complex - SEZ

SOUHATSU PHILIPPINES, INC. Manufacture of plug part of AC adapter Greenfi eld Automotive Park - SEZ

STMICROELECTRONICS, INC. Manufacture of CB6 Light Industry & Science Park II - SEZ

SUNAUTOMOTIVE TECHNOLOGY, INC. Engage in electrical assembly (automotive security and accessory) 99.9% - Japanese Light Industry & Science Park III - SEZ

TSUKIDEN ELECTRIC INDUSTRIES PHILIPPINES, INC. Power Plant Control System Assembly; and Automotive Engine Control System Assembly

99.99% - Hong Kong Laguna Technopark - SEZ

WELGAO ELECTRONIC TECHNOLOGY (PHILIPPINES) INCORPORATED PCB Manufacturing / PCB Assembly 99.99% - Chinese First Cavite Industrial

Estate - SEZ

WARREN AND BROWN TECHNOLOGIES FIBER SYSTEMS CORPORATION

Manufacture of optical fi ber ducting raceway production system and its installation in Telecommunication System

Laguna International Industrial Park - SEZ

FOOD AND BEVERAGE MANUFACTURES

EAU DE COCO, INC. Production of stabilized coconut water and manufacture of secondary products such as frozen young coconut meat and outer shell residues

99.99% - British Virgin Islander

Lima Technology Center - SEZ

PRIMEX COCO PRODUCTS, INC. Manufacture of desiccated coconut and coconut milk powder 100% - Filipino Candelaria Agri Special Economic Zone

45BUSINESS

Philippine ANALYST August 2014

HOTEL, RESTAURANT, AND LEISURE SERVICES

DELUXE HOTELS AND RECREATION INC.Establishment of Hilton Manila, a 388-room tourist-oriented accommodations project, including food and beverage outlets, retail stores and recreational facilities

100% - Filipino Newport City CyberTourism Zone

IT AND IT-ENABLED SERVICES

BLACK & WHITE MIDDLE EAST (PHILIPPINES), INC. Provides engineering design services 99.99% - Emirati Zuellig Building

LOZATECH DIGITAL MARKETING INC. Digital IT services including web/graphics/social media development 93% - American 7% - Filipino Eastwood City Cyberpark

WSP ASIA PHILIPPINES, INC. Software related services including system design, confi guration, testing/QA, database design and development Hanston Square

METAL INDUSTRIES

ISHIDA SEISAKUSHO PHILS. CO. INC. Engage in quality control of precision metal parts 99.99% - Japanese Laguna Technopark - SEZ

JNE PHILS. INC. Engage in Nickel and Gold Plating of Flexible Flat Cable (FCC) 99.98% - Korean Golden Mile Business Park - SEZ

MANASTEEL INDUSTRIES Production of mould base, die plates, and machine parts, die casting, machining, and surface heat treatment 100% - Filipino Mactan Economic Zone

NEW ELECTRONICS SYSTEM CO., INC. Manufacture of Microscope Tube, Aluminum Collar, and Microphone Holder Cavite Economic Zone

S BROS. PRECISION, INC.

Manufacture and repair of mold and dies, and manufacture and assembly of electronic parts and componentS Cavite Economic Zone

SANAC PHILIPPINES, INC. Manufacture/assembly of diecasted products for automotive parts, components and other related products

99.99% - Japanese

First Cavite Industrial Estate - SEZ

MISCELLANEOUS MANUFACTURES

DAY 1 CRAFT PHILIPPINES INC. Manufacture and assembly of fi shing gears and accessories such as fi shing tackle or lure, bait log and related accessories

99.97% - Japanese Laguna Technopark - SEZ

GBPLEN CORPORATION Anti-Refl ection Coating of Optical Lens Cavite Economic Zone

GF MICRO OPTICS PHILIPPINES, INC. Production of SELFOC® Micro Lens AR Coated using Optical Monitoring System Technology with local Research and Development inputs Laguna Technopark - SEZ

JMS HEALTHCARE PHL, INC. Manufacture and assembly of medical devices and disposables, particularly Infusion Set

99.99% - Japanese

First Philippine Industrial Park - SEZ

MITSUWA CHEMICAL PHILIPPINES, INC. Production of fi lters Cavite Economic Zone

OFFSHORING AND OUTSOURCING

4th SHIFT GLOBAL INC. IT and customer support for existing infrastructure 99.98% - American Trafalgar Plaza

ACQUIRE ASIA PACIFIC, INC. BPO for information, support, lead generation and other related services including inbound and outbound calling

99.99% - Australian Cyberscape Beta

ANTHEM SOLUTIONS, INC. Knowledge/Business Process Outsourcing operations of iMedGlobal Solutions, Inc. E-Square I.T. Park

BOSSOLUTIONS INC. Business Process Outsourcing particularly rendering administrative support or paraplanning

99.99% - Australian 6750 Ayala Avenue Bldg.

BRAINHUB INC. Software Development, User support, and Data entry 99.98% - Swiss CBP-IT Park

CITY MARQUE LIMITED Book sales and/or manage customer relations via telephone and to offer back offi ce support 100% - Hong Kong Eastwood City Cyberpark

CONVERGYS PHILIPPINES SERVICES CORPORATION Call Center Operations John Hay Special Tourism Economic Zone

CONVERGYS PHILIPPINES SERVICES CORPORATION Additional 228 seats/workstations (Call Center) Eton Centris

DELTEK SYSTEMS (PHILIPPINES), LTD. Software development, IT support services, enterprise software and information solutions, training and industry-specifi c consulting services 100% - American The Enterprise Center

DKP SERVICES, INC. Software development and support 60% - Filipino 40% - Canadian Zuellig Building

ECoGlobalConsulting, Inc. Software Development and Implementing Services, IT Outsourcing and IT Solutions 100% - Filipino Zuellig Building

FREELANCER.COM PHILIPPINES, INC. Business Process Outsourcing (BPO)/Online customer and technical support

99.99% - Australian Ecotower

46 BUSINESS

Philippine ANALYST August 2014

GUMI ASIA PTE. LTD. (PHILIPPINES BRANCH)Provides customer and technical support, social network services management, quality assurance, and server application maintenance and development for mobile social games

50% - Japanese 50% - Singaporean One Corporate Centre

HCCA HEALTH CONNECTIONS INC. Business Process Outsourcing and Call Center operations CBP-IT Park

IBM SOLUTIONS DELIVERY, INC. IT Application Management services Eastwood City Cyberpark

IMEDGLOBAL SOLUTIONS, INC.IT-Enabled Knowledge Process Outsourcing in areas of life sciences / Provision of Clinical, Pharmacovigilance, regulatory and technology services to life science companies

96% - American 4% - Indian E-Square I.T. Park

INFOSYS BPO LIMITED - PHILIPPINE BRANCH Business Process Outsourcing (BPO) Services Northgate Cyberzone

LEARNASIA PHILS. INC. Business Process Outsourcing Services – Online Tutorial 98% - Japanese 2% - Filipino CBP-IT Park

LITTELFUSE PHILS., INC..Technical Support Services; Product Evaluation; Production Planning; Product Development; Sourcing; Global Logistics; Sales Reporting; Sales Review

Lima Technology Center - SEZ

LOCALPHONE LIMITED Call Center Operations 100% - British RCBC Savings Bank Corporate Center

NORTHERN LIGHTS TECHNOLOGY DEVELOPMENT (PHILIPPINES) CORPORATION

Technology services including development, consultation, service, use and transfer of software technologies, products and related information operations

Cebu I.T. Park

ORANGENOSE STUDIO PHILIPPINES INC. Mobile Games Application Development as outsourced services 99.96% - Singaporean The Enterprise Center

PANASIATIC CALL CENTERS, INC. Call Center Operations Villa Angela Techno Park

PSG GLOBAL SOLUTIONS, INC. Business Process Outsourcing (BPO) Services Multinational Bancorporation Centre

QBE GROUP SHARED SERVICES LIMITED IT-enabled Business Process Outsourcing operations W Fifth Avenue

REERACOEN BPO INC. Business Process Outsourcing activities and Call center operations 99.5% - Singaporean GAGFA IT Center

REPRISK PHILIPPINES, INC. Provides analytical and other data gathering, monitoring and processing services 99.99% - Swiss E-Square I.T. Park

RMH TELESERVICES ASIA PACIFIC, INC. Provides inbound and outbound call center services Eton Centris

RS800 GROUP INC. Online English Tutorial services 99.8% - Australian Crown 7 I.T. Center

STARTEK PHILIPPINES, INC. Call Center operations Iloilo Business Park

TATA CONSULTANCY SERVICES (PHILIPPINES) INC. Information Technology (IT), business solutions and outsourcing services operations E-Square I.T. Park

TATA CONSULTANCY SERVICES (PHILIPPINES) INC. Information Technology (IT) and Business Process Outsourcing services PANORAMA

TELETECH CUSTOMER CARE MANAGEMENT - PHILIPPINE BRANCH Offer the lease of its facility to Telstra International Philippines, Inc. Cebu I.T. Park

THOUSAND CRANE PHILIPPINES, INC. Business Process Outsourcing activities and Call center operations 70% - Japanese 30% - Singaporean GAGFA IT Center

UNITEDHEALTH GROUP GLOBAL SERVICES, INC. Collocation Space to lease and occupy six (6) rack spaces Vitro Internet Data Center Building

UNITEDHEALTH GROUP GLOBAL SERVICES, INC. Information technology services, call centre and back offi ce operations UP Science and Technology Park (North)

UNITEDHEALTH GROUP GLOBAL SERVICES, INC."Collocation Agreement" with ePLDT, Inc. for the REGISTRANT's Collocation Space to lease and occupy six (6) rack spaces in ePLDT's Vitro Internet Data Center site

Vitro Internet Data Center Building

WELLS FARGO ENTERPRISE GLOBAL SERVICES, LLC-PHILIPPINES Business Process Outsourcing activities and Call center operations 100% - American McKinley Hill Cyberpark

WELLS FARGO ENTERPRISE GLOBAL SERVICES, LLC-PHILIPPINES

Provision of administrative, back offi ce, call center, information technology, support, training and other allied services related to the foregoing services

McKinley Hill Cyberpark

PAPER AND PAPER PRODUCTS

HEAVY DUTY PACKAGING CORPORATION Manufacture of heavy duty cartons and allied/similar packaging systems Carmelray Industrial Park II - SEZ

PLASTIC PRODUCTS

D&L POLYMER & COLOURS, INC. Manufacture of New Generation, Eco-Friendly Specialty Polymer and Colour Compounds

Carmelray Industrial Park I - SEZ

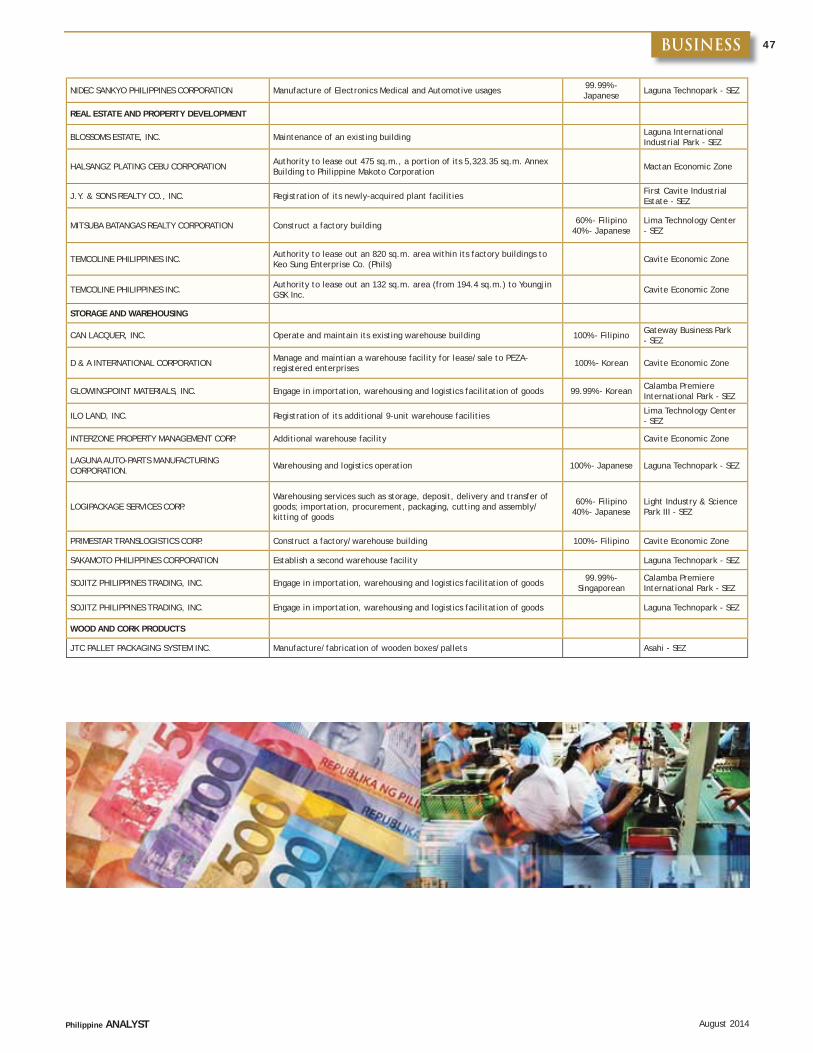

47BUSINESS

Philippine ANALYST August 2014

NIDEC SANKYO PHILIPPINES CORPORATION Manufacture of Electronics Medical and Automotive usages 99.99% - Japanese Laguna Technopark - SEZ

REAL ESTATE AND PROPERTY DEVELOPMENT

BLOSSOMS ESTATE, INC. Maintenance of an existing building Laguna International Industrial Park - SEZ

HALSANGZ PLATING CEBU CORPORATION Authority to lease out 475 sq.m., a portion of its 5,323.35 sq.m. Annex Building to Philippine Makoto Corporation Mactan Economic Zone

J.Y. & SONS REALTY CO., INC. Registration of its newly-acquired plant facilities First Cavite Industrial Estate - SEZ

MITSUBA BATANGAS REALTY CORPORATION Construct a factory building 60% - Filipino 40% - Japanese

Lima Technology Center - SEZ

TEMCOLINE PHILIPPINES INC. Authority to lease out an 820 sq.m. area within its factory buildings to Keo Sung Enterprise Co. (Phils) Cavite Economic Zone

TEMCOLINE PHILIPPINES INC. Authority to lease out an 132 sq.m. area (from 194.4 sq.m.) to Youngjin GSK Inc. Cavite Economic Zone

STORAGE AND WAREHOUSING

CAN LACQUER, INC. Operate and maintain its existing warehouse building 100% - Filipino Gateway Business Park - SEZ

D & A INTERNATIONAL CORPORATION Manage and maintian a warehouse facility for lease/sale to PEZA-registered enterprises 100% - Korean Cavite Economic Zone

GLOWINGPOINT MATERIALS, INC. Engage in importation, warehousing and logistics facilitation of goods 99.99% - Korean Calamba Premiere International Park - SEZ

ILO LAND, INC. Registration of its additional 9-unit warehouse facilities Lima Technology Center - SEZ

INTERZONE PROPERTY MANAGEMENT CORP. Additional warehouse facility Cavite Economic Zone

LAGUNA AUTO-PARTS MANUFACTURING CORPORATION. Warehousing and logistics operation 100% - Japanese Laguna Technopark - SEZ

LOGIPACKAGE SERVICES CORP.Warehousing services such as storage, deposit, delivery and transfer of goods; importation, procurement, packaging, cutting and assembly/kitting of goods

60% - Filipino 40% - Japanese

Light Industry & Science Park III - SEZ

PRIMESTAR TRANSLOGISTICS CORP. Construct a factory/warehouse building 100% - Filipino Cavite Economic Zone

SAKAMOTO PHILIPPINES CORPORATION Establish a second warehouse facility Laguna Technopark - SEZ

SOJITZ PHILIPPINES TRADING, INC. Engage in importation, warehousing and logistics facilitation of goods 99.99% - Singaporean

Calamba Premiere International Park - SEZ

SOJITZ PHILIPPINES TRADING, INC. Engage in importation, warehousing and logistics facilitation of goods Laguna Technopark - SEZ

WOOD AND CORK PRODUCTS

JTC PALLET PACKAGING SYSTEM INC. Manufacture/fabrication of wooden boxes/pallets Asahi - SEZ

48 BUSINESS

Philippine ANALYST August 2014

LIST OF BOI REGISTERED PROJECTS

JULY 2014

INDUSTRY ACTIVITY PROJECT COST (IN PHP MILLION)

EQUITY LOCAL/FOREIGN

AUTOMOTIVE TRADE

QSJ Motors Phils., Inc. Producer of Commercial Vehicles 408.47 60% Filipino 40% Chinese

ELECTRICITY, WATER, AND GAS

Balayan Distillery Inc. Renewable Energy Developer of Biomass Resources (Manufacturer of Bio-Ethanol) 125.84 100% Filipino

Green Innovations for Tomorrow Corporation Renewable Energy Developer of 12 MW Biomass Power Plant under RA 9513 (Renewable Energy Act of 2008) 1,134.07 100% Filipino

DMCI Power Corporation Operator of 15MW Bunker-Fired Power Plant 1,001 100% Filipino

Solar Philippines Commercial Rooftop Projects, Inc.

Renewable Energy Developer of 0.7 MW Solar Power Plant under RA 9513 (Renewable Energy Act of 2008) 42.23 100% Filipino

Panay Energy Development Corporation Operator of 150MW CFB Coal-Fired Power Plant 15,577.72 100% Filipino

ELECTRONICS

Grand Asia Electrical Light Corp. Producer of Decorative LED Light 7.82 100% Taiwanese

MISCELLANEOUS MANUFACTURE

CosmoMedical Inc. Producer of Disposable Medical Devices such Syringes 36.93 100% Korean

OFFSHORING AND OUTSOURCING

Martom Enterprises Non-Voice Business Processing Operations 2.64 100%Filipino

PAPER AND PAPER PRODUCTS

Duraboard Packaging Corporation Producer of Multilayer Kraft Paper Bags 20.37 100% Filipino

REAL ESTATE AND PROPERTY DEVELOPMENT

8990 Housing Development Corporation Developer of Low Cost Mass Housing Project (Deca Homes Resort Residences Phase 9 Subdivision) 521.73 100% Filipino

City and Land Developers, Incorporated Developer of Low-Cost Mass Housing Project (North Residences) 561.26 99.64% Filipino 0.36% Foreign

City and Land Developers, Incorporated Developer of Low-Cost Mass Housing Project (One Taft Residences) 1,082.81 99.64% Filipino 0.36% Foreign

Johndorf Ventures Corporation Developer of Low-Cost Mass Housing Project (Astana Subdivision) 448.25 100% Filipino

HLC Construction and Development Corporation Developer of Low-Cost Mass Housing Project (Oakwood Residences) 116.21 100% Filipino

HLC Construction and Development Corporation Developer of Low-Cost Mass Housing Project (Excellent Living Residences) 200.31 100% Filipino

TRANSPORT SERVICES

NMC Container Lines, Inc. Domestic/Inter-island Shipping Operator (One General Cargo Vessel - MV Knock, 4,450 GT) 225 100% Filipino

Lorenzo Shipping Corporation Domestic/Inter-island Shipping Operator under Infrastructure – Water Transport (One Container Cargo Vessel - MV Greetsiel) 225 99.88% Filipino

TOTAL 21,737.65

49BUSINESS

Philippine ANALYST August 2014

DATA INDEX

YEAR-ON-YEAR

GROWTH

YEAR-TO-DATE

GROWTH

(2000=100)

Volume of Production Index (VoPI) (2000=100) 126.3 13.3 0.0

a. Food 141.9 13.1 3.2

b. Beverage 129.7 12.9 22.0

c. Tobacco 5.6 -9.7 -23.4

d. Textile 38.0 15.5 13.2

e. Footwear and Wearing Apparel 29.3 -14.3 -12.5

f. Wood and Wood Products 69.8 6.7 2.6

g. Furniture & Fixtures 902.7 26.7 14.4

h. Basic Metals 149.0 24.5 -2.7

i. Iron and Steel 114.4 18.4 13.2

j. Non-ferrous Metals 231.5 30.3 -23.9

k. Fabricated Metal Products 292.1 39.8 40.7

l. Machinery Excluding Electrical 44.1 26.7 29.4

m. Electrical Machinery 92.3 4.3 0.5

n. Transport Equipment 110.6 19.8 -1.0

o. Other Mfg Industries 99.2 -6.3 -2.0

p. Paper & Paper Products 67.7 -3.6 -5.0

q. Publishing & Printing 126.4 153.8 112.4

r. Leather Products 4.2 40.0 6.2

s. Rubber Products 266.4 7.6 11.0

t. Chemical Products 248.3 2.3 -31.4

u. Petroleum Products 57.3 7.7 3.5

v. Non-Metallic Mineral Products 119.5 -21.2 -10.5

w. Glass & Glass Products 124.6 -2.6 3.9

x. Cement 156.2 4.3 -0.6

y. Misc. Non-Metalic Mineral Products 41.8 -74.6 -55.2

DATA YEAR-AGOLEVEL

GROWTH RATE (%)

MOTOR VEHICLE SALES 69,737 57,128 22

PASSENGER CAR SALES 24,824 18,702 327

COMMERCIAL VEHICLE SALES 44,913 38,426 16.8

BUSINESS CLIMATE INDEX

UNIVERSAL AND COMMERCIAL BANK’S LOANS OUTSTANDING TO THE REAL ESTATE SECTOR (P Bn)MARCH 2014

MAR-14 % TO TOTALRE: LOAN DEC-2012 % TO TOTAL

RE: LOAN

RESIDENTIAL 196.28 28.5 173.46 30.5

COMMERCIAL 492.28 71.5 394.95 69.9

MOTOR VEHICLE SALESJULY 2014

000

500

0

500

000

500

000

500

000

FDI:BOP CONCEPT US$ Million

INDUSTRIAL PERFORMANCE (2000=100) JULY 2014

FOREIGN DIRECT INVESTMENTBalance of Payments Concept*; JANUARY- APRIL 2014

LEVEL (US$ million)

SOURCE CURRENT YEAR AGO YEAR-ON-YEAR% CHANGE

TOTAL FDI 1,377 1,829 -24.74

Equity Capital 357.26 791.33 -54.85

Reivested Earnings 131.42 146.33 -10.19

Debt Instruments 887.99 891.64 -0.41

* The BSP adopted the Balance of Payment, 6th edition (BPM6) compilation framework effective 22 March 2013 with the release of the full-year 2012 and revised 2011 BOP statistics. In BPM6, net FDI fl ows refer to non-residents’ equity capital (i.e., placements less withdrawals) + reinvestment of earnings + debt instruments, net (i.e.,net intercompany borrowings).

50 BUSINESS

Philippine ANALYST August 2014

BUSINESS CLIMATE INDEX

SURVEY ON THE MONTHLY OCCUPANCY RATES & LENGTH OF STAY

67.2% HOTEL OCCUPANCY RATE IN 2013

The comparative average occupancy rates of hotels in Metro Manila hit 67.2% in 2013. The occupancy rate for accredited hotels hit 67.4% while non-accredited hotels posted a 54.85% occupancy rate. Deluxe hotels were the most popular with 70.82% occupancy. The guest’s length of stay averaged at 2.49 nights in 2013. On the average, guests preferred to stay longer on non-accredited hotels at 4.31 nights.

1 STRIKE IN JUNE 2013

A strike was recorded in June 2013 which involved 400 workers equivalent to 1,200 man-days lost. Meanwhile, there is a total of 83 notices of strike/lockouts since January 2014. In 2012, 3 strikes were recorded involving 209 workers, which is equivalent to 797 man-days lost. Meanwhile, 184 notices of strike were fi led that year.

LABOR STRIKES

STRIKES DECLARED WORKERS INVOLVED MAN-DAYS LOST (000)

2014 2013 2014 2013 2014 2013

JAN 0 0 - - - -

FEB - - - - - -

MAR - - - - - -

APR - - - - - -

MAY - - - - - -

JUN - 1.00 - 400 - 1,200

JUL - - - - - -

AUG - - - - - -

SEP - - - - - -

OCT - - - - - -

NOV - - - - - -

DEC - - - - - -

TOTAL 0 1 0 400 0 1,200

0

500

1000

1500

2000

2500

3000

3500

4000

MAN-DAYS LOST

0

2

4

6

8

10

12

STRIKES DECLARED

VISITOR ARRIVALS SLIGHTLY UP IN JUNE

Total visitor arrivals registered in June is 372,293, up by only 0.87% from 369,073 in the same month in 2013. Of this, 4.15% or 15,642 visitors were Filipinos residing abroad.

Korea remained the top source market followed by the U.S. and China. From January to June, visitors coming from Korea amounted to 585,282 (22.52% share of the 2.38 million total visitors for 2014). The U.S. market tallied 389,432 visitors (16%) while the Chinese market recorded 226,163 visitors (9.29%).

0

100

200

300

400

500

TOURISM ARRIVALS

VISITOR ARRIVALSJANUARY-JUNE 2014

COUNTRY 2014 2013 % CHANGE RANK

KOREA 547,971 585,282 -6.37 1

USA 389,432 364,506 6.84 2

CHINA 226,163 199,157 13.56 3

JAPAN 220,366 209,812 5.03 4

AUSTRALIA 111,687 103,286 8.13 5

SINGAPORE 91,692 86,290 6.26 6

CANADA 75,677 68,430 10.59 7

UNITED KINGDOM 68,593 60,234 13.88 8

TAIWAN 67,213 86,076 -21.91 9

MALAYSIA 66,796 54,154 23.34 10

HONGKONG 57,470 65,696 -12.52 11

GERMANY 38,642 37,025 4.37 12

OVERSEAS FILIPINO 106,088 109,029 -2.70

OTHERS 365,638 351,616 3.99

TOTAL 2,435,442 2,382,606 2.22

JANUARY - DECEMBER 2014 2012 2011 2012/2011

JAN TO DEC JAN TO DEC GROWTH RATE

De Luxe Hotels

Occupancy Rates 70.82 71.49 -0.94

Length of Stay 2.87 2.92 -1.71

First Class Hotels

Occupancy Rates 60.14 58.05 3.59

Length of Stay 2.20 2.30 -4.17

Standard Hotels

Occupancy Rates 65.34 64.82 0.80

Length of Stay 2.46 2.38 3.47

Economy Hotels

Occupancy Rates 52.15 53.44 -2.41

Length of Stay 1.87 2.13 -12.44

Overall Average 67.20 67.25 -0.07