Embed Size (px)

Citation preview

Presenting a live 90‐minute webinar with interactive Q&A

Additional Insured & Contractual Indemnity Additional Insured & Contractual Indemnity Coverage in Commercial & Construction Contracts Reconciling Contractual Obligations With Policy Terms to Maximize Coverage

T d ’ f l f

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

WEDNESDAY, OCTOBER 12, 2011

Today’s faculty features:

Joann M. Lytle, Partner, McCarter English, Philadelphia

Stephen D. Palley, Principal, Ober | Kaler, Washington, D.C.

Jenna Kirkpatrick Howard, Producer, Lockton Companies, Washington, D.C.

The audio portion of the conference may be accessed via the telephone or by using your computer's speakers. Please refer to the instructions emailed to registrants for additional information. If you have any questions, please contact Customer Service at 1-800-926-7926 ext. 10.

Conference Materials

If you have not printed the conference materials for this program, please complete the following steps:

• Click on the + sign next to “Conference Materials” in the middle of the left-hand column on your screen hand column on your screen.

• Click on the tab labeled “Handouts” that appears, and there you will see a PDF of the slides for today's program.

• Double click on the PDF and a separate page will open. Double click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

2

Continuing Education Credits FOR LIVE EVENT ONLY

For CLE purposes, please let us know how many people are listening at your location by completing each of the following steps:

• Close the notification box

• In the chat box, type (1) your company name and (2) the number of attendees at your location

• Click the SEND button beside the box

3

Tips for Optimal Quality

S d Q litSound QualityIf you are listening via your computer speakers, please note that the quality of your sound will vary depending on the speed and quality of your internet connection.

If the sound quality is not satisfactory and you are listening via your computer speakers, you may listen via the phone: dial 1-888-450-9970 and enter your PIN when prompted Otherwise please send us a chat or e mail when prompted. Otherwise, please send us a chat or e-mail [email protected] immediately so we can address the problem.

If you dialed in and have any difficulties during the call, press *0 for assistance.

Viewing QualityTo maximize your screen, press the F11 key on your keyboard. To exit full screen, press the F11 key againpress the F11 key again.

4

OTHER PEOPLE’S INSURANCE:INSURANCE:

Additional Insured Coverage

BByJoann M. Lytle, Esq.

McCarter & English, LLP

October 12, 2011

g ,BNY Mellon Center1735 Market Street, Suite 700Philadelphia, PA [email protected]

Information which is copyrighted by and proprietary to Insurance Services Office, Inc. ("ISO Material") is included in this publication. Use of the ISO Material is limited to ISO Participating Insurers and their Authorized Representatives. Use by ISO Participating Insurers is limited to use in those jurisdictions for which the insurer has an appropriate participation with ISO. Use of the ISO Material by Authorized Representatives is limited to use solely on behalf of one or more ISO Participating Insurers.

5

Wh t i Additi l I dWhat is Additional Insured Coverage?

Risk transfer method that allows one party Risk transfer method that allows one party to a business relationship to obtain coverage under another party’s policy .

6

Who Are The Players?

Additional Insured – the party seeking to take advantage of another party’s coverage.

Named Insured – the party whose policy is providing coverage to the Additional Insured.

7

Additi l I d Additi lAdditional Insured vs. Additional “Named Insured”

Not the same thing Not the same thing. “Additional Named Insured” has no generally

accepted meaning.p g

8

Additional Named Insured

“A person or organization, other than the first p g ,named insured, identified as an insured in the policy declarations or an addendum to the policy declarations ”declarations.

“A person or organization added to a policy after the policy is written with the status of named yinsured. This entity would have the same rights and responsibilities as an entity named as an insured in the policy declarations ”

9

insured in the policy declarations….

Irmi Online - Glossary of Insurance and Risk Management Terms

Additional Insured

“A person or organization notA person or organization not automatically included as an insured under an insurance policy, but for whom p y,insured status is arranged, usually by endorsement. …”

Irmi Online - Glossary of Insurance and Risk Management Terms

10

Benefits for Additional Insured

Coverage without premium. Doesn’t erode additional insured’s own limits

of liabilityof liability. No responsibility for deductibles. Particularly important for companies who are y p p

self-insured or who have retentions on their own policies.

11

Benefits for Additional Insured

Supports indemnity obligation, which only has value if the indemnitor has assets to fulfill it.

Defense coverage without having to wait for a Defense coverage, without having to wait for a resolution of the indemnity obligation.

Can be independent of, and provide broader p pprotection than, the indemnity obligation, i.e., for the additional insured’s negligence.

Important where applicable state’s law prohibits

12

– Important where applicable state s law prohibits indemnification for one’s own negligence.

Di d t f Additi lDisadvantages for Additional Insured:

No control over the defense No control over the defense.– Significant where both the Named Insured and Additional

Insured are sued. Limits must be shared among all insureds Limits must be shared among all insureds. Often no business relationship with carrier.

13

Implications for Named Insured

ProsAllows transfer of the obligation to defend and– Allows transfer of the obligation to defend and indemnify the indemnitee to the insurer.

Cons– Erosion of limits.– Limits shared by all insureds.

Limits used to pay claims for which the Additional– Limits used to pay claims for which the Additional Insured may be partly or entirely at fault.

– Responsibility for deductible.

14– Higher premiums down the road based on loss

experience.

R l ti hi Gi i Ri tRelationships Giving Rise to Additional Insured Coverage

Construction Construction– General contractor requires additional insured status on

subcontractors’ policies. Vendor/VendeeVendor/Vendee

– Vendor requires additional insured coverage on manufacturer’s policy.

Service AgreementService Agreement– Customer requires additional insured status on service

provider’s policy. Building maintenance

15 Cafeteria operation

Relationships Giving Rise to Additional Insured Coverage

Equipment Lease

– Lessor requires additional insured status on lessee’s insurance.

16

R l Lif E lReal Life Example

Manufacturer leases equipment to Customer. Customer installs equipment in its plant and uses equipment to q p p q p

manufacture insulation. Explosion on one of the lines. Very serious injuries to Customer’s employees, including

multiple deathsmultiple deaths. Customer’s employees sue Manufacturer. Manufacturer has multi-million dollar retention for products

claims on its own policy, and Manufacturer’s policy does not fimpose a duty to defend.

Manufacturer makes claim as an Additional Insured against Customer’s policy for both defense and indemnification.

17

H D O B AHow Does One Become An Additional Insured?

Generally requires both contract between the parties and an additional insured provision in anparties and an additional insured provision in an insurance policy.

18

The Contract

An obligation to indemnify does not confer additional insured statusadditional insured status.

Does the contract contain an insurance provision?p

– Does it require that the other party name your client as an additional insured?

– Does it specify the type and amount of insuranceDoes it specify the type and amount of insurance coverage to be provided? CGL, Umbrella? Primary or Excess?

19

Primary or Excess? Limits?

The Insurance Policy

A contractual obligation to provide insurance is ineffective unless the Named Insured’s policy contains an Additional Insured Clause.

Usually in an endorsement Usually in an endorsement.

20

T f Additi l I dTypes of Additional Insured Endorsements

Both ISO endorsements and manuscript endorsementsTwo varieties– Two varieties Blanket additional insured endorsements – grant

additional insured status to categories of Additional Insureds or to those whom the NamedAdditional Insureds or to those whom the Named Insured has a contractual obligation to insure.– Sometimes called automatic additional

insuredsinsureds.– If the contract does not specifically require

insurance, the endorsement is ineffective.Sched led additional ins red endorsements lists

21

Scheduled additional insured endorsements – lists the name of the additional insured.

Verifying Additional InsuredVerifying Additional Insured Coverage

A certificate of insurance is not proof of iinsurance

The Acord form specifically states that dditi l i d iadditional insured coverage requires an

endorsement

22

23

Verifying Additional InsuredVerifying Additional Insured Coverage

Ideally, request a full copy of the Named I d’ liInsured’s policy.

May not be that simple.– For some large companies, the extent of their

insurance program, including limits and deductibles, is a closely-guarded secret., y g

– In that situation, review the additional insured endorsement(s), at a minimum.

24– Review the Other Insurance Clause, if possible.

Additional InsuredAdditional Insured –Timely Notice Obligation?

A typical CGL policy will generally state that i d t i tian insured must give notice as soon as

“practicable” of an occurrence that may result in a claim under the policyin a claim under the policy.

25

Additional InsuredAdditional Insured –Timely Notice Obligation?

In some jurisdictions, a named insured’s timely notice will also constitute adequate

ti th dditi l i d’ b h lfnotice on the additional insured’s behalf.

26

Additional InsuredAdditional Insured –Timely Notice Obligation?

In Casualty Insurance Co. v. E.W. Corrigan Construction Co., Inc., 247 Ill. App. 3d 326 (Ill. App. Ct. 1993), the court rejectedInc., 247 Ill. App. 3d 326 (Ill. App. Ct. 1993), the court rejected the carrier’s attempts to argue that notice to the workers’ compensation department is insufficient to provide adequate notice to the liability department for the same carrier.y p

“[I]f an insured notifies its insurer of an occurrence and references its workers’ compensation policy, it should bereferences its workers compensation policy, it should be considered notice in regards to any general liability policy the insured might have with the same insurer. Consequently, it should also be adequate notice to the insurer for any

27

yadditional insured named on the general liability policy.” Id. at 333.

Additional InsuredAdditional Insured –Timely Notice Obligation?

In some jurisdictions, however, the additional insured must provide notice on its own behalf i i t t ith th li ’in a manner consistent with the policy’s specific terms and conditions.

28

Additional InsuredAdditional Insured –Timely Notice Obligation?

In Liberty Ins Underwriters Inc v Great American Ins In Liberty Ins. Underwriters Inc. v. Great American Ins. Co., No. 09 Civ. 4912(DLC), 2010 WL 3629470 (S.D.N.Y. Sept. 17, 2010), the court determined an additional insured has an implied duty to provide its own notice toinsured has an implied duty to provide its own notice to the insurance carrier even if the policy does not explicitly require separate notice by the additional insured or the i i d t l ti f th l i f thinsurer received actual notice of the claim from the named insured or a separate source.

29

Additional InsuredAdditional Insured –Timely Notice Obligation?

Why is this a problem? Why is this a problem?– In many cases, the only policy information an additional

insured has is a Certificate of InsuranceE i it t i t li i f ti it’– Even assuming it contains current policy information, it’s unlikely to contain the policy’s specific notice requirements

30

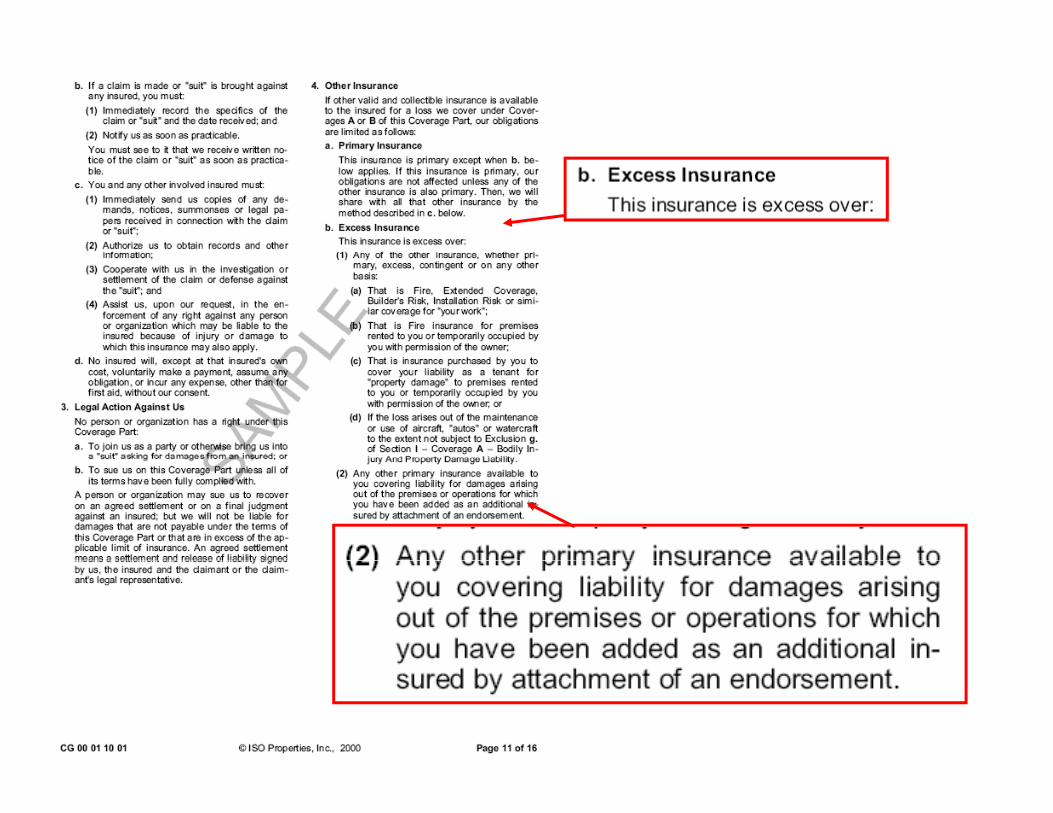

Whose Coverage is Primary?

Formerly a hotly-disputed issue. ISO attempted to resolve the dispute in the CGL

policy itself.Th 2001 d l t i f th ISO CGL The 2001 and later versions of the ISO CGL Policy (CG 00 01 10 01) contain an amended Other Insurance Clause (Section IV).( )

31

32

ISO Other Insurance Clause

• States that the Named Insured’s policy is excess over any other policy on which “You” have beenover any other policy on which “You” have been added as an additional insured by way of endorsement.

• Issues still arise when the other party’s insurance purports to provide only excess coverage.coverage.

• Issues also arise concerning whose policy pays after the limits of the policy providing additional insured coverage are exhausted

33

insured coverage are exhausted.

S Of Additi l I dScope Of Additional Insured Coverage

How broad is it? Does it essentially back-stop the Named Insured’s

contractual indemnity obligation?– Which clause appears first in the contract – indemnity or pp y

insurance? Does it cover more than the Additional Insured would be

able to recover under the Indemnity Agreement?– What if the indemnity agreement contains a monetary cap?– What if the insurance provision states that the Additional

Insured will receive coverage in the minimum amount of $ ?

34$________?

Scope of Additional InsuredScope of Additional Insured Coverage

What if the indemnity agreement is f bl ?unenforceable?

– For example, an agreement that purports to indemnify the indemnitee for its own negligence?indemnify the indemnitee for its own negligence?

– In a state where such an agreement is void as against public policy?

35

Gilbane Building Co. v. Empire Steel Erectors, L.P., No. H-08-

1707, 691 F. Supp. 2d 712 (S.D.Tex. 2010)

Parr, an employee of Empire Steel, a , p y p ,Subcontractor, fell off a ladder at a construction site and sued Gilbane Building Co., the General Contractor.

– Admiral Ins. Co. argued that because the indemnity agreement in the Trade Contractor Agreement was unenforceable under TX law, Gilbane was not covered as an additional insured.

– Court rejected this argument and noted that the indemnity and insurance provisions were separate clauses that do not reference each other are not intertwined or interrelated and on their face

36

each other, are not intertwined or interrelated, and on their face stand independently as separate obligations.

Norfolk & Dedham Mut. Fire Ins. Co. v. Morrison, 456 Mass.

463, 924 N.E.2D 260 (2010)

Dr. Beverly Shafer rented office space from C iCummings.– The lease agreement required Dr. Shafer to

indemnify Cummings against liability to thirdindemnify Cummings against liability to third parties and to purchase insurance adding Cummings as an additional insured.

37

Norfolk & Dedham Mut Fire InsNorfolk & Dedham Mut. Fire Ins. Co. v. Morrison

One of Dr. Shafer’s patients tripped in the ki l t d d b th D Sh f dparking lot and sued both Dr. Shafer and

Cummings.Cummings (landlord) demanded that both Dr– Cummings (landlord) demanded that both Dr. Shafer and Norfolk (Shafer’s insurer) indemnify it.

– Norfolk refused, citing a Massachusetts statute , gvoiding a tenant’s obligation to indemnify a landlord.

38

Norfolk & Dedham Mut Fire InsNorfolk & Dedham Mut. Fire Ins. Co. v. Morrison

The Court held that the statutory prohibition i t i d it t did t lagainst indemnity agreements did not apply

to the insurance provision of the lease agreement:agreement:– “An agreement in a lease that the tenant

indemnify or hold harmless the landlord is distinct yfrom an agreement to purchase insurance on the landlord’s behalf, which covers the liability of both in the event of a negligently caused injury ”

39

in the event of a negligently caused injury.

Impact of Anti Indemnity StatutesImpact of Anti-Indemnity Statutes on Additional Insured Coverage

Recently some states (e g California Colorado Kansas Recently, some states (e.g., California, Colorado, Kansas, Louisiana and New Mexico) have enacted legislation prohibiting coverage for the additional insured’s own negligence where that negligence could not be transferred via an indemnitythat negligence could not be transferred via an indemnity agreement

In states where additional insured status is within the jurisdiction of the anti-indemnity statute, an additional insured’sjurisdiction of the anti indemnity statute, an additional insured s coverage cannot be broader than its protection as an indemnitee

40

Kansas Stat. S. 16-121

For example, Kansas Stat. S. 16-121 (2011) in relevant part provides:part provides:

– (b) “An indemnification provision in a contract which requires the promisor to indemnify the promisee for the promisee’s negligence or intentional acts or omissions ispromisee s negligence or intentional acts or omissions is against public policy and is void and unenforceable.”

– (c) “A provision in a contract which requires a party to provide liability coverage to another party as anprovide liability coverage to another party, as an additional insured, for such party’s own negligence or intentional acts is against public policy and is void and unenforceable.”

41

unenforceable.

Kansas Stat. S. 16-121

S. 16-121(f) indicates, “This section applies l t i d ifi ti i i donly to indemnification provisions and

additional insured provisions entered into after January 1 2009 ”after January 1, 2009.

42

New Mexico Stat. Ann. S. 56-7.1

New Mexico Stat. Ann. S. 56-7.1 (2011) similarly provides:A A provision in a construction contract that requires one party to– A. A provision in a construction contract that requires one party to the contract to indemnify, hold harmless, insure or defend the other party to the contract, including the other party’s employees or agents, against liability, claims, damages, losses or expenses, including attorney fees, arising out of bodily injury to person or damage to property caused by or resulting from, in whole or in part, the negligence, act or omission of the indemnitee, its officers, employees or agents, is void, unenforceable and againstofficers, employees or agents, is void, unenforceable and against the public policy of the state.

43

New Mexico Stat. Ann. S. 56-7.1

Section 56-7.1(B) states further:– B. A construction contract may contain a provision that, or shall beB. A construction contract may contain a provision that, or shall be

enforced only to the extent that, it: (1) requires one party to the contract to indemnify, hold harmless or

insure the other party to the contract, including its officers, employees or agents against liability claims damages losses or expensesor agents, against liability, claims, damages, losses or expenses, including attorney fees, only to the extent to that the liability, damages, losses or costs are caused by, or arise out of, the acts or omissions of the indemnitor or its officers, employees or agents.

Section 56-7.1(F) indicates “indemnify” or “hold harmless” “includes any requirement to name the indemnified party as an additional insured in the indemnitor’s insurance coverage for the purpose of providing indemnification for any liability not otherwise allowed in this

44

providing indemnification for any liability not otherwise allowed in this section.

Typical Additional Insured Claim

Contract requiring that general contractor

Subcontractor’sInsuranceCompany

Contract requiring that general contractorbe added as additional insured. Subcontractor

(Named Insured)General Contractor(Additional Insured)

Does additional insured’s liability to named insured’sInjured Employee

45

Does additional insured s liability to named insured semployee “arise out of” named insured’s ongoingoperations?

C f Additi l I d’Coverage for Additional Insured’s Own Negligence

Prior to 2004, a number of ISO additional insured endorsements provided coverage for liabilityendorsements provided coverage for liability “arising out of” the Named Insured’s operations for the Additional Insured.

A number of courts construed “arising out of” to be the same as “but for” causation.If the liability would not have arisen “but for” the If the liability would not have arisen “but for” the named insured’s involvement, the additional insured has coverage.

46

C f Additi l I d’Coverage for Additional Insured’s Own Negligence

Township of Springfield v. Ersek, 660 A.2d 672 (Pa. Commw. 1995) (to nship as added to pro shop’s polic as additional1995) (township was added to pro shop’s policy as additional insured “with respect to liability arising out of operations performed by” pro shop; policy covered damages for injuries to pro shop’s employee, caused by township’s negligence, because p p p y y p g g“arising out of” means causally connected with, not proximately caused by).

Aetna Cas. & Surety Guar. Corp. v. Ocean Acc. & Guarantee C 386 F 2d 413 (3d Ci 1967) ( id d f i j iCorp., 386 F.2d 413 (3d Cir. 1967) (coverage provided for injuries to named insured’s employee, caused by additional insured’s sole negligence, where the additional insured’s liability would not have arisen “but for” its engagement by or association with the

47

g g ynamed insured).

Coverage for Additional Insured’sCoverage for Additional Insured’s Own Negligence

Mid-Continent Cas. Co. v. Swift Energy Co., 206 F.3d 487 (5th Cir. 2000) (finding that injuries to named insured’s employee “arose out2000) (finding that injuries to named insured’s employee “arose out of” named insured’s operations, even if the cause of the injuries was the sole negligence of the additional insured).

McIntosh v. Scottsdale Ins. Co., 992 F.2d 251 (10th Cir. 1993) (festival patron injured on fairgrounds brought suit against township/additional insured. Festival operator’s insurer obligated to cover township, even though township stipulated that it was 100% negligent, since injuries “arose out of” Festival’s operations).eg ge t, s ce ju es a ose out o est a s ope at o s)

Allen-Stevenson School v. Burlington Ins. Co., 2008 N.Y. Misc. LEXIS 10587 (N.Y. Sup. Ct. Mar. 31, 2008) (“The additional insured language…defines coverage…based on the scope of the named insured’s work As long as the claim against the additional insured

48

insured’s work. As long as the claim against the additional insured arises out of the named insured’s work, coverage is provided under the Endorsement.”).

Th 2004 A d t t ISO’The 2004 Amendments to ISO’s Endorsements

In response to these cases, in 2004, ISO amended some of its most commonly-used additional insured endorsements to make clear that the additional insured’s sole negligence isthat the additional insured s sole negligence is not covered.

Additional Insured only has coverage with respect to liability for BI or PD caused, in whole or in part, by the Named Insured’s conduct.

49

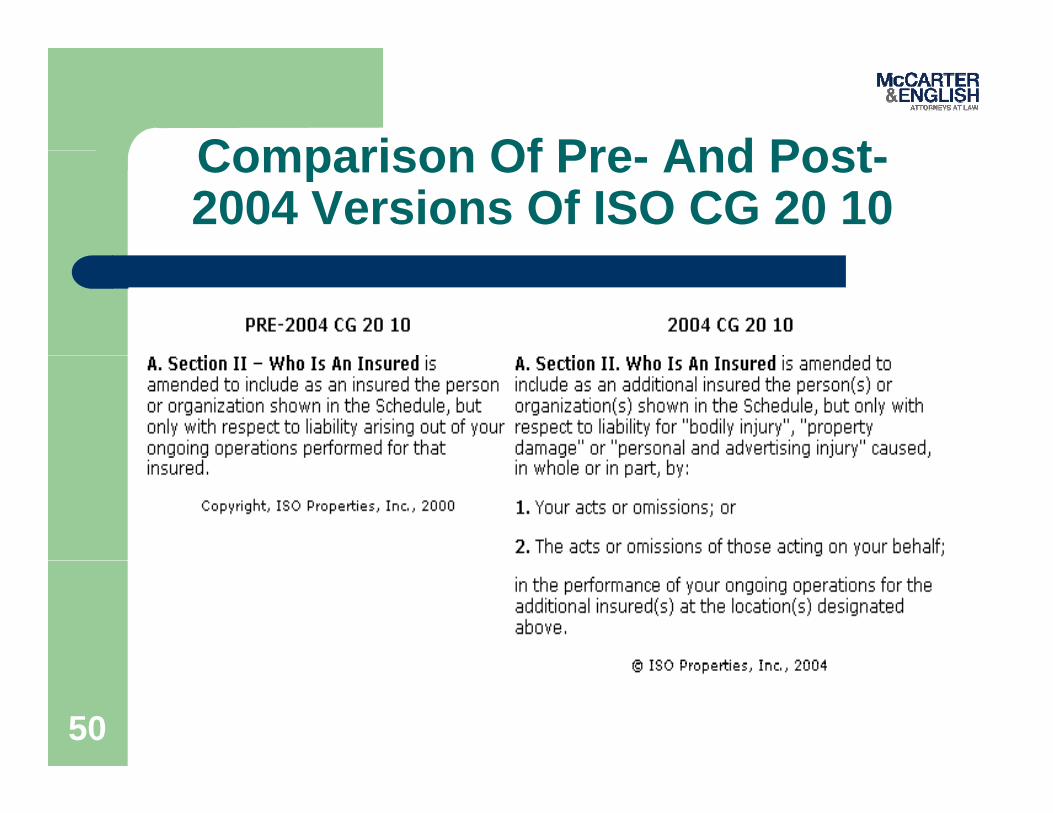

Comparison Of Pre And PostComparison Of Pre- And Post-2004 Versions Of ISO CG 20 10

50

Did ISO’s Amendment ResolveDid ISO’s Amendment Resolve The Issue?

Maybe not. In the Gilbane Building Co. case, Admiral

argued that since the complaint contained no ll ti f li th t fallegations of negligence on the part of

Empire (the Subcontractor/Named Insured) or anyone acting on its behalf the Generalor anyone acting on its behalf, the General Contractor was not covered.

51

Gilbane Building Co v EmpireGilbane Building Co. v. Empire Steel Erectors

Court rejected Admiral’s argument and sided ith th G l C t twith the General Contractor:

– Parr (the employee) was statutorily barred from naming his employer the Subcontractor as anaming his employer, the Subcontractor, as a liable party because of the Workers’ Compensation bar.

– Under Texas’s comparative responsibility statute, Parr’s own negligence is at issue, even if not pled. Parr while acting in the scope of his employment for

52

Parr, while acting in the scope of his employment for Empire (and thus acting on behalf of Empire), was potentially responsible for his own injuries.

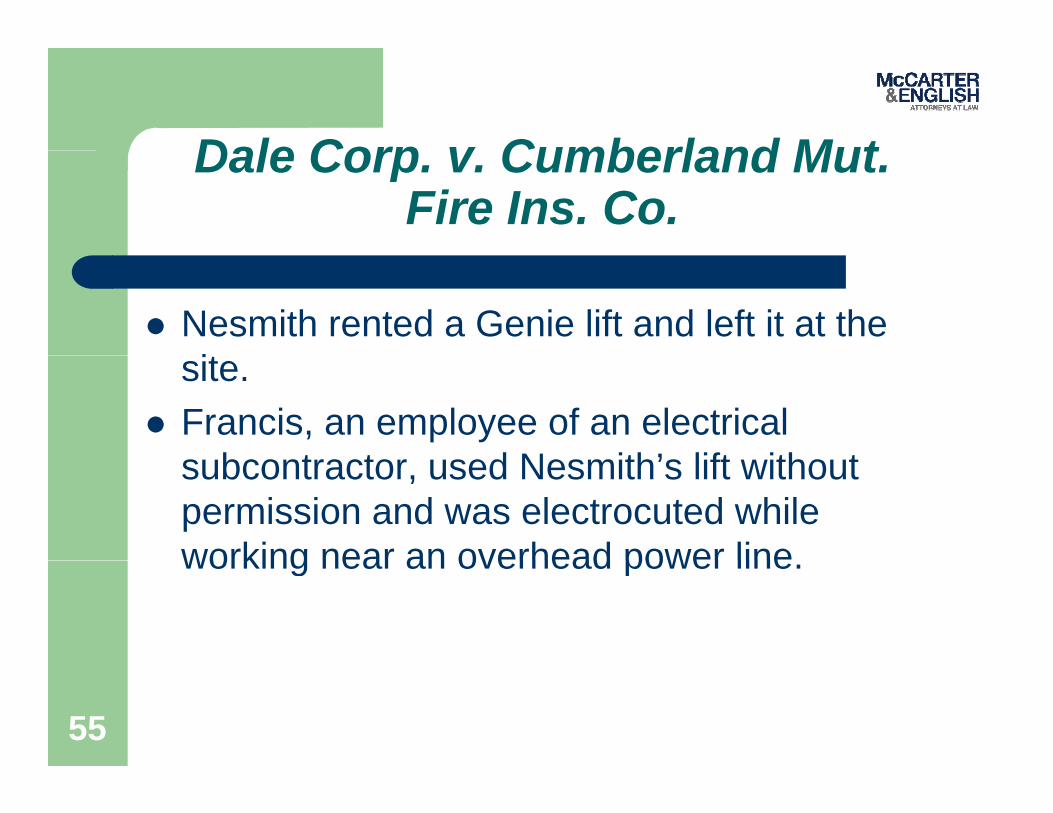

Dale Corp v Cumberland MutDale Corp. v. Cumberland Mut. Fire Ins. Co.

Dale Corp. v. Cumberland Mut. Fire Ins. Co., N 09 1115 2010 U S Di t LEXIS 65052No. 09-1115, 2010 U.S. Dist. LEXIS 65052 (E.D. Pa. June 30, 2010) (Pennsylvania law)

Another construction injury case– Another construction injury case.– Dale Corp. was hired as a construction manager

for the Brewerytown construction project in y p jPhiladelphia.

53

Dale Corp v Cumberland MutDale Corp. v. Cumberland Mut. Fire Ins. Co.

Dale retained Nesmith as a subcontractor– The Dale/Nesmith subcontract required Nesmith

to add Dale as an additional insured on Nesmith’s CGL Policy, issued by Cumberland.CGL Policy, issued by Cumberland.

– The Cumberland Policy contained the 2004 ISO Additional Insured Endorsement.

54

Dale Corp v Cumberland MutDale Corp. v. Cumberland Mut. Fire Ins. Co.

Nesmith rented a Genie lift and left it at the itsite.

Francis, an employee of an electrical b t t d N ith’ lift ith tsubcontractor, used Nesmith’s lift without

permission and was electrocuted while working near an overhead power lineworking near an overhead power line.

55

Dale Corp v Cumberland MutDale Corp. v. Cumberland Mut. Fire Ins. Co.

Francis sued Dale and Nesmith.– Dale sought coverage as an additional insured

under the Cumberland policy issued to Nesmith.Cumberland refused to defend or indemnify– Cumberland refused to defend or indemnify, alleging that Francis’ injuries did not arise “in whole or in part” out of Nesmith’s acts or

i iomissions.

56

Dale Corp v Cumberland MutDale Corp. v. Cumberland Mut. Fire Ins. Co.

Court held that Cumberland was obligated to d f d D l b F i ’ l i tdefend Dale because Francis’ complaint alleged that Nesmith was negligent in failing to secure the lift and keysto secure the lift and keys.

However, Cumberland was not obligated to indemnify Dale for its settlement with Francisindemnify Dale for its settlement with Francis.

57

Dale Corp v Cumberland MutDale Corp. v. Cumberland Mut. Fire Ins. Co.

Duty to indemnify was based on facts known t D l t ti f ttl tto Dale at time of settlement.

Was Nesmith the proximate cause of the id t?accident?

– No, because it was undisputed that Nesmith did not give permission to anyone to use the liftnot give permission to anyone to use the lift.

58

Revised CG 20 10 Does Not LimitRevised CG 20 10 Does Not Limit Coverage To Vicarious Liability

American Empire Surplus Lines Ins. Co. v. C & F t S i lt I C N H 06Crum & Forster Specialty Ins. Co., No. H-06-004, 2006 U.S. Dist. LEXIS 33556 (S.D. Tex. May 23 2006) (language of endorsementMay 23, 2006) (language of endorsement requiring that Additional Insured’s liability arise, in whole or in part, out of Named , p ,Insured’s conduct, does not limit coverage to vicarious liability, but provides coverage

59where both Named Insured and Additional Insured are negligent).

Final Thoughts

Additional insured coverage may provide more – or less coverage than the parties anticipatedless – coverage than the parties anticipated.

Review the actual insurance policy or the additional insured endorsements.

Review indemnity and insurance provisions before contracts are signed.

Consider any applicable legislation which may impact the additional insured’s right to coverage.

Caution the business units about signing contracts

60

Caution the business units about signing contracts containing indemnity and/or additional insured clauses.

Additi l I d CAdditional Insured Coverage

Jenna Kirkpatrick Howard

L O C K T O N C O M P A N I E S , L L C

[email protected] | 202-414-2607

The Insurance Coverages Where Additional Insureds Status is requested?

Commercial Property / Builders Risk

General Liability Policy

Auto Liability

Umbrella/Excess Liability

Workers Compensation – not possible

Professional Liability – should not request

Pollution Liability – only in unique circumstancesPollution Liability only in unique circumstances

62

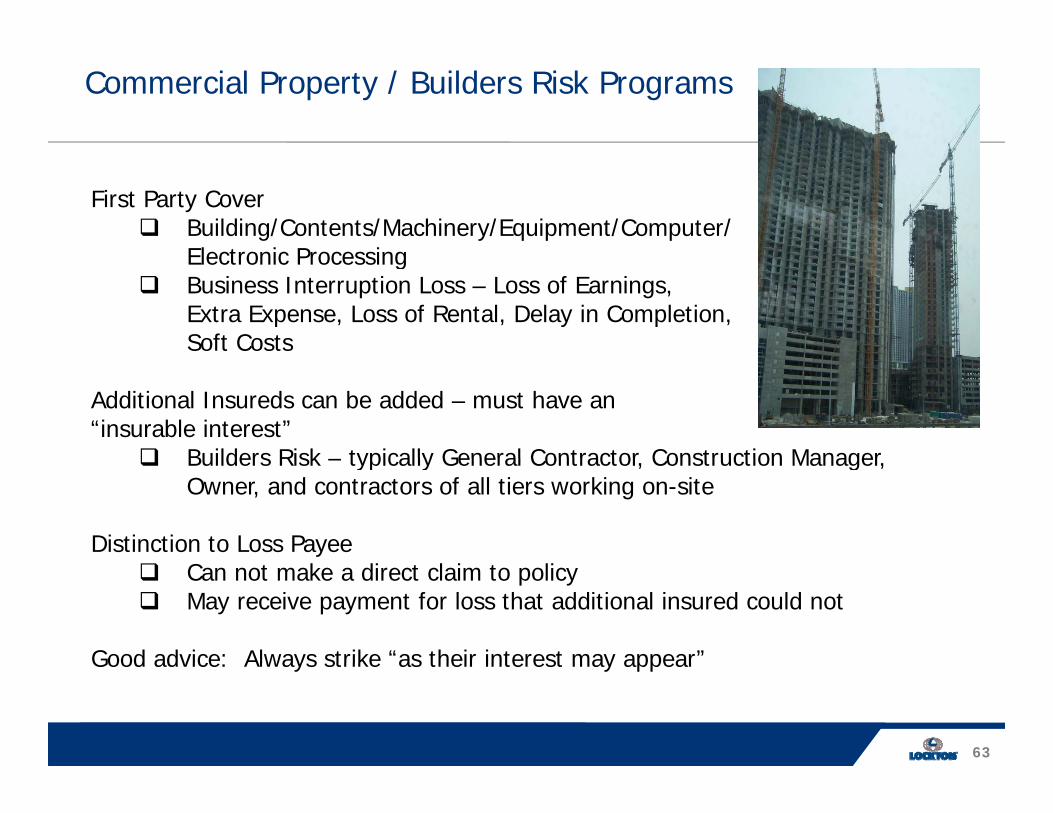

Commercial Property / Builders Risk Programs

First Party Cover Building/Contents/Machinery/Equipment/Computer/

Electronic ProcessingElectronic Processing Business Interruption Loss – Loss of Earnings,

Extra Expense, Loss of Rental, Delay in Completion, Soft Costs

Additional Insureds can be added – must have an “insurable interest”

Builders Risk – typically General Contractor Construction Manager Builders Risk – typically General Contractor, Construction Manager, Owner, and contractors of all tiers working on-site

Distinction to Loss Payee Can not make a direct claim to policy May receive payment for loss that additional insured could not

Good advice: Always strike “as their interest may appear”

63

Good advice: Always strike as their interest may appear

General Liability PolicyThe Highlights

Loss must be attributable to bodily injury, sickness, disease, or death or damage to tangible property

Two major coverages: Premises/Ongoing Operations Products/Completed Operations

Policy has multiple types of insureds: “named insured” “additional named insured” “ dditi l i d” “additional insured” “insured”

The intent is not the same for each nor are their definitions within the policy.definitions within the policy.

ISO – 34 additional insured forms available – which is appropriate for the contact?

Certain forms (CG 10 11 85) are requested in contracts but not available in the

64

Certain forms (CG 10 11 85) are requested in contracts but not available in the insurance marketplace. So what now?

Common Additional Insured FormsConstruction Agreements

CG 20 10 11 85 Liability arising out of “your work” for that insured by or for you.

CG 10 07 04Liability for “bodily injury”, “property damage” or “personal and advertising

injury” caused, in whole or in part by:The insured’s acts or omissions; orThe insured s acts or omissions; orThe acts or omissions of those acting on the insured’s behalf; In the performance of the insured’s “ongoing “operations for the additional

insured

Does not apply to “bodily injury” or “property damage” occurring after all work for the additional insured has been completed or has been put to its intended use.use.

CG 20 37 07 04Provides completed operations coverage

65

General Liability PolicyInsured Contracts

Standard CGL form (CG 00 01) excludes coverage for Contractual Liability –Exclusion 2(b) but craves back over through an exception.

C GO S O S CO C SCATEGORIES OF INSURED CONTRACTS

Lease of premises, except with respect to an obligation to indemnify for fire damage to the leased premisesfire damage to the leased premises

A sidetrack agreement Any easement or license agreement, except with respect to construction

or demolition operations on or within 50 feet of a railroad A bli ti d it di t i d if i i lit t An obligation under a city ordinance to indemnify a municipality, except

in connection with work for a municipality An elevator maintenance agreement That part of any other contract related to the insured's business p y

operations in which the insured assumes the tort liability of another party with respect to third-party "bodily injury" or "property damage" (This item is referred to herein as part f. of the definition.)

66

IRMI publication date: May 2004

General Liability PolicyInsured Contracts

NOT COVERED UNDER DEFINITION OF INSURED CONTRACT

The Contractor's Work Breach of Contract Third-Party Beneficiary Claims Railroad Indemnification Agreements Assumptions of Professional Design Liability Personal Injury

IRMI publication date: May 2004

There are ISO endorsements that amend the standard General Liability policy’sThere are ISO endorsements that amend the standard General Liability policy s contractual liability wording.

67

General Liability PolicyAdditional Insured vs. Indemnitee

Indemnify1. to secure against future loss, damage, or liability; give security for; insure2. to compensate for loss, injury, expense, etc; reimburse C lli E li h Di ti C l t & U b id d 10th Editi 2009

Additional Insured Indemnitee

By endorsement Coverage within Hold Harmless

Collins English Dictionary - Complete & Unabridged 10th Edition 2009

By endorsement Coverage within Hold Harmless Agreement

Defined in policy Defined in “insured contract”

Defense included outside of limits Treatment of defense costs by insurance related to the supplementary

payments provision in policypayments provision in policy

Payment directed to Additional Insured Payment directed to Named Insured

68

Case in point: Long Island Lighting Co. v . American Employers Insurance Co. 131 A.D.2d 733,517 N.Y.S.2d 44 (N.Y. App. Div. 1987)

General Liability PolicyLimitation of Additional Insured

How does it impact the insured granting the additional insured status to others:

Sharing of policy limits Sharing of policy limits Lack of Completed Operations “Other Insurance Clause”

Obvious Statement: Additional Insured status does not replace anObvious Statement: Additional Insured status does not replace an indemnity/hold harmless agreement.

Second Obvious Statement: Do not confuse indemnity and insurance obligations

69

– they are separate issues.

Automobile Liability

Vicarious Auto Liability – anyone liable for the conduct of an insured but only to the extent of that liability

Automatic additional insured status if the indemnitee is an entity liable for named insured’s conduct, and the request for additional insured status does not specify coverage for more than vicarious liability.

ISO created form – CA 20 48 – Designated Insured EndorsementISO created form CA 20 48 Designated Insured Endorsement It is a scheduled form.

Many carriers have also created their own forms.

Secret: Designated Insured on ISO form has exactly some status as the insured with or without the ISO endorsement.

70

Umbrella/Excess Liability

Buyer beware – forms are not ystandard.

Is coverage truly “follow form”Is coverage truly follow form language

Understand “who is insured” wording – does it match ALL underlying policies

71

Admitted vs. Excess/Surplus Lines Coverage

ISO forms – admitted and approved by state insurance commissioners

Some carriers have admitted forms that are not ISO – sometimes called “broad forms”

Excess/Surplus Lines Policy wording not approved by state insurance commissioner Policy wording not approved by state insurance commissioner Not “tried and true” wording; can be more or less stringent No access to state guarantee funds

Excess/Surplus Lines Additional Insured status Coverage can be triggered in various ways:

• By written contract or written agreement that is “in effect”• By certificateBy certificate• By extent of contractual requirement

72

Cost of Coverage

Premium charge – not typical to add additional insured by endorsement, but it does happen.

Defense Costs – shares defense costs with all additional insureds. Are defense costs inclusive or exclusive of policy limits?

Need for higher limits – potentiallyNeed for higher limits – potentially

Contracts typically requirement notification of cancellation or nonrenewal of coverage – who is response for tracking and notifying – broker, insurer, insured, no one?

“Notice of material change” in contracts - not in insurance policy and undefined in contractand undefined in contract

73

The Claim Scenario

O Subcontractor agrees to indemnify General Contractor and name

the General Contractor as Additional Insured Third party sues General Contractor

Occurrence

d pa ty sues Ge e a Co t acto General Contractor submits claim to subcontractor’s insurer General Contractor also seeks indemnification from subcontractor.

Subcontractor submits indemnity claim to its insurer.

Obtain copies of contract, General Contractor’s insurance policies, Subcontractor’s certificates of insurance, and Subcontractor’s insurance

Best Practices

,policies including endorsements

Place subcontractor’s insurer on notice – not just general liability Place General Contractor insurer on notice, as a CYA measure

Acknowledge tender under reservation of rights within time period Investigate facts

Working relationships - insured, broker, outside attorney and insurers

74

Determine duty to defend and decide to reserve rights Tender all Subcontractor’s insurers

Our MissionTo be the worldwide value and service leader in insurance brokerage, employee benefits, and risk management

Our GoalTo be the best place to do business and to workp

www lockton com

75

www.lockton.com

© 2011 Lockton, Inc. All rights reserved.Images © 2011 Thinkstock. All rights reserved.