Embed Size (px)

Citation preview

ASHK_MedicalReform_PSC_RFC_20150417.pptx

Actuarial Society of Hong Kong

Better Use of Data for Health Insurance Management and VHIS Implementation

17 April 2015

Fred Choi FCAS, MASHK

1

ASHK_MedicalReform_PSC_RFC_20150417.pptx

Agenda

Overview

VHIS minimum requirement for standard plan

VHIS impact on pricing, Data use and refinement

Data Field Checklist

Questions and Answers

2

ASHK_MedicalReform_PSC_RFC_20150417.pptx

Overview

3

Food and Health Bureau issued the Voluntary Health Insurance Scheme (“VHIS”) Consultation Paper in December 2014.

Generally speaking, insurers are required to provide more comprehensive coverage with more restrictive terms and conditions after implementation of VHIS.

The bill and subsidiary legislation for VHIS is expected to be introduced in 2015/16. Actual implementation of VHIS will probably be a few years after that.

ASHK_MedicalReform_PSC_RFC_20150417.pptx

Overview

4

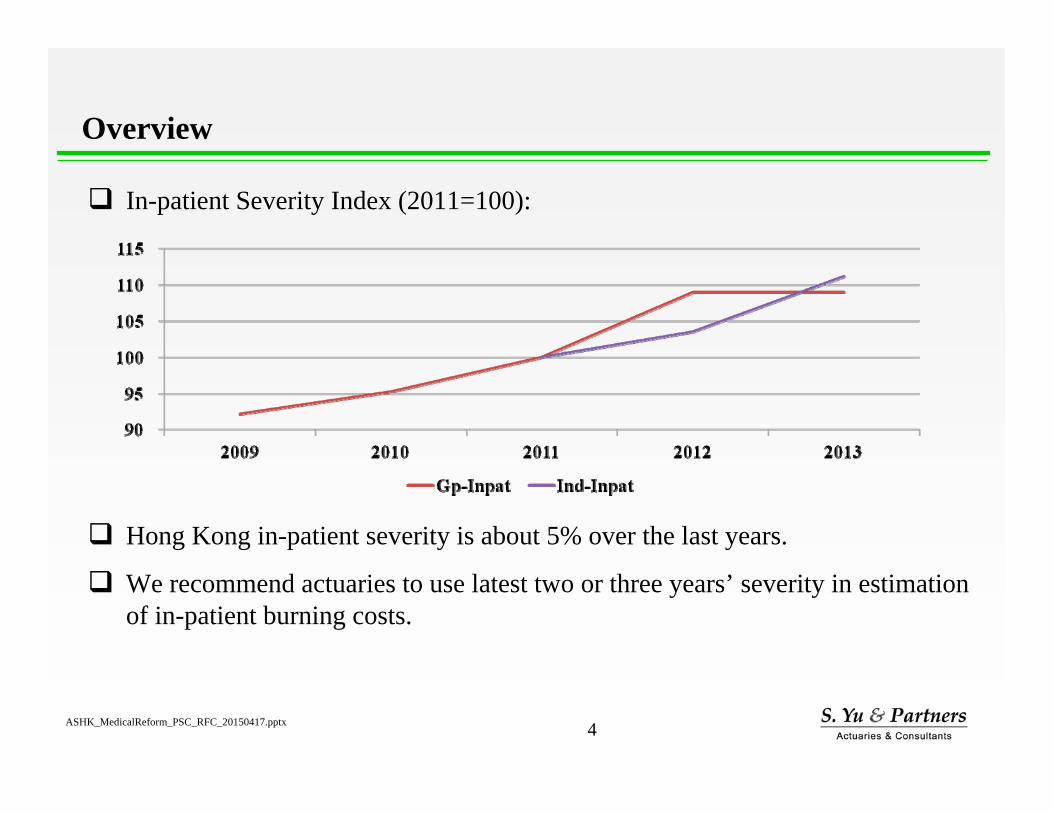

In-patient Severity Index (2011=100):

Hong Kong in-patient severity is about 5% over the last years.

We recommend actuaries to use latest two or three years’ severity in estimation of in-patient burning costs.

ASHK_MedicalReform_PSC_RFC_20150417.pptx

Overview

5

As VHIS is generally more comprehensive and restrictive than current practice, migration to VHIS implied that existing system may be inadequate for the challenge.

In this presentation, we would like to:

Identify impact on health insurance cost and pricing due to VHISimplementation

Discuss what and how data can be use to prepare for VHIS pricing

Propose data adjustment and judgment

Propose additional data field and possible data refinement

ASHK_MedicalReform_PSC_RFC_20150417.pptx

Agenda

Overview

VHIS Minimum Requirement for Standard Plan

VHIS Impact on Pricing, Data Use and Refinement

Data Field Checklist

Questions and Answers

6

ASHK_MedicalReform_PSC_RFC_20150417.pptx

VHIS Minimum Requirement for Standard Plan

7

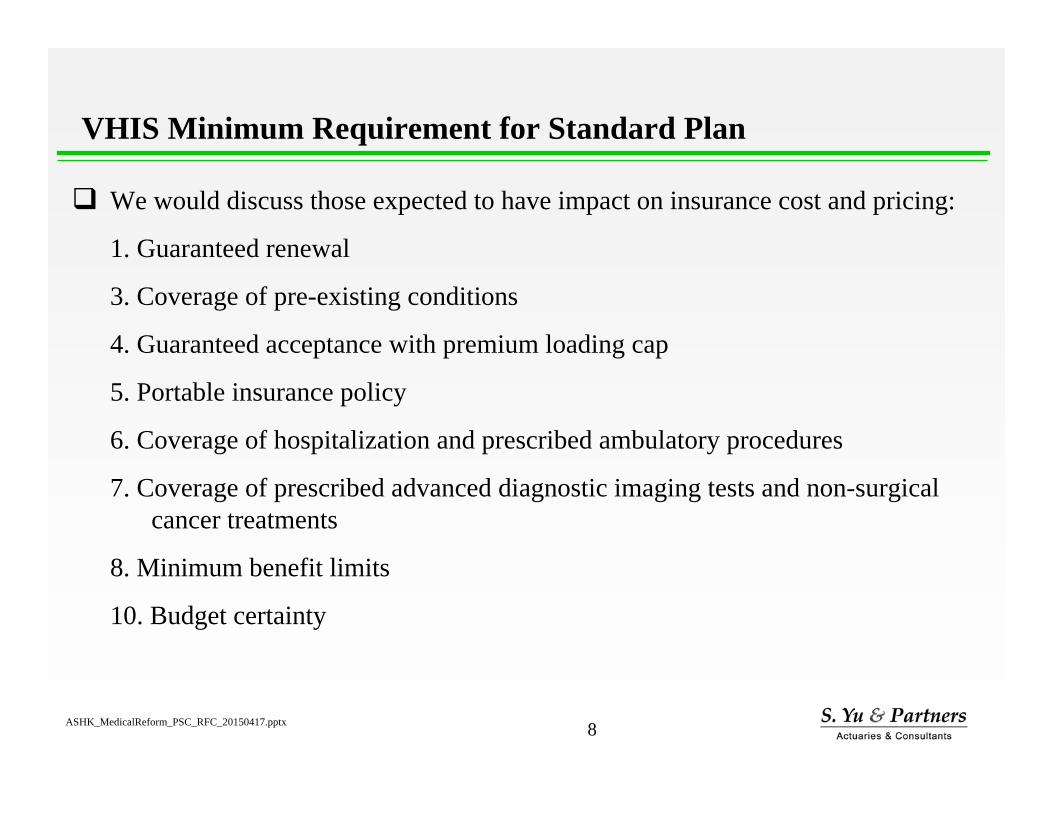

There are 12 minimum requirements proposed for VHIS Standard Plan:

ASHK_MedicalReform_PSC_RFC_20150417.pptx

VHIS Minimum Requirement for Standard Plan

8

We would discuss those expected to have impact on insurance cost and pricing:

1. Guaranteed renewal

3. Coverage of pre-existing conditions

4. Guaranteed acceptance with premium loading cap

5. Portable insurance policy

6. Coverage of hospitalization and prescribed ambulatory procedures

7. Coverage of prescribed advanced diagnostic imaging tests and non-surgical cancer treatments

8. Minimum benefit limits

10. Budget certainty

ASHK_MedicalReform_PSC_RFC_20150417.pptx

Agenda

Overview

VHIS Minimum Requirement for Standard Plan

VHIS Impact on Pricing, Data Use and Refinement

Data Field Checklist

Questions and Answers

9

ASHK_MedicalReform_PSC_RFC_20150417.pptx

VHIS impact on pricing – Pre-Existing Condition, Guaranteed acceptance and renewal

10

Coverage of pre-existing conditions:

Increase claim cost

Actuaries need to determine additional premium loading.

Guaranteed acceptance and renewal:

Cannot reject poor insureds, e.g. with pre-existing conditions

Cannot refine the insurance pool by non-renewing poor insureds

Increase risks to insurers

ASHK_MedicalReform_PSC_RFC_20150417.pptx

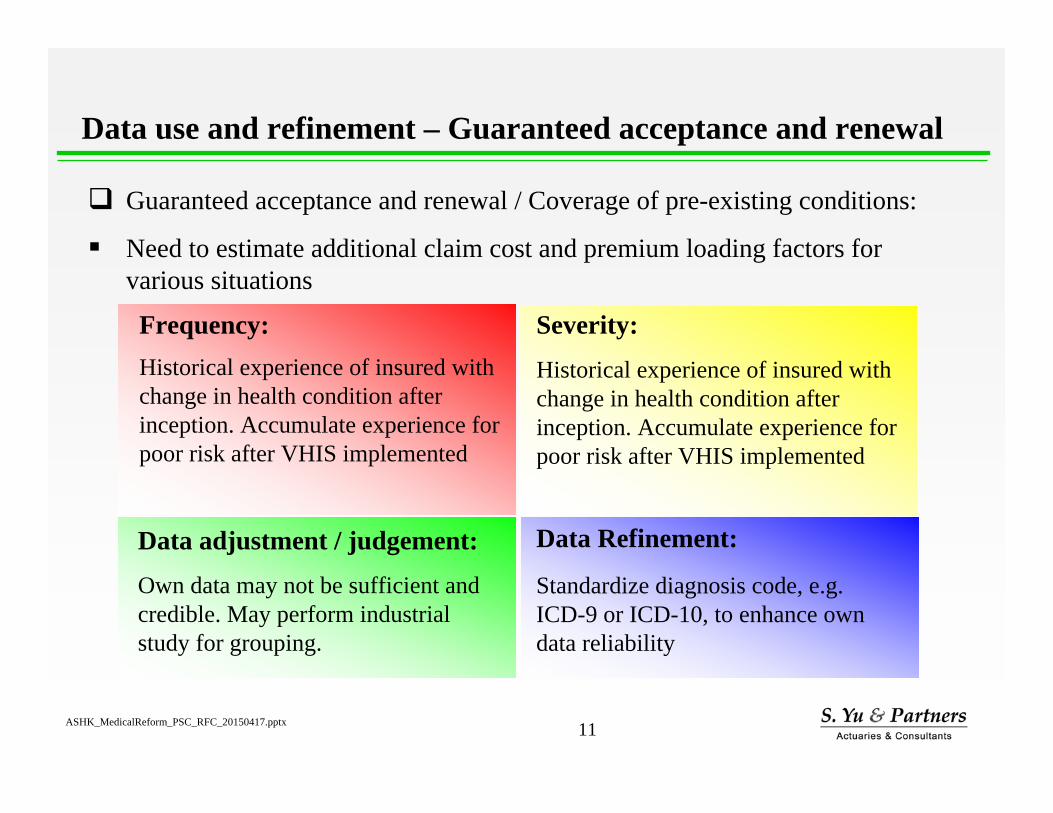

Data use and refinement – Guaranteed acceptance and renewal

11

Frequency:Historical experience of insured with change in health condition after inception. Accumulate experience for poor risk after VHIS implemented

Severity:

Historical experience of insured with change in health condition after inception. Accumulate experience for poor risk after VHIS implemented

Data adjustment / judgement:

Own data may not be sufficient and credible. May perform industrial study for grouping.

Data Refinement:

Standardize diagnosis code, e.g. ICD-9 or ICD-10, to enhance own data reliability

Guaranteed acceptance and renewal / Coverage of pre-existing conditions:

Need to estimate additional claim cost and premium loading factors for various situations

ASHK_MedicalReform_PSC_RFC_20150417.pptx

VHIS impact on pricing – Portable

12

Portable insurance policy:

Cannot reject poor risk / with pre-existing conditions for Standard Plan

Cannot re-underwrite if no claims were made in a certain period

Increase risk for insurers

We suggest insurers to capture and record underwriting classes of previous insurer or other existing insurers when they accept new policies

ASHK_MedicalReform_PSC_RFC_20150417.pptx

VHIS impact on pricing – Hospitalization & ambulatory procedures

13

Coverage of hospitalization and prescribed ambulatory procedures:

Encourage ambulatory procedures, reduce unnecessary hospitalization

Reduction in severity and claim cost

Severity become more certain and stable

ASHK_MedicalReform_PSC_RFC_20150417.pptx

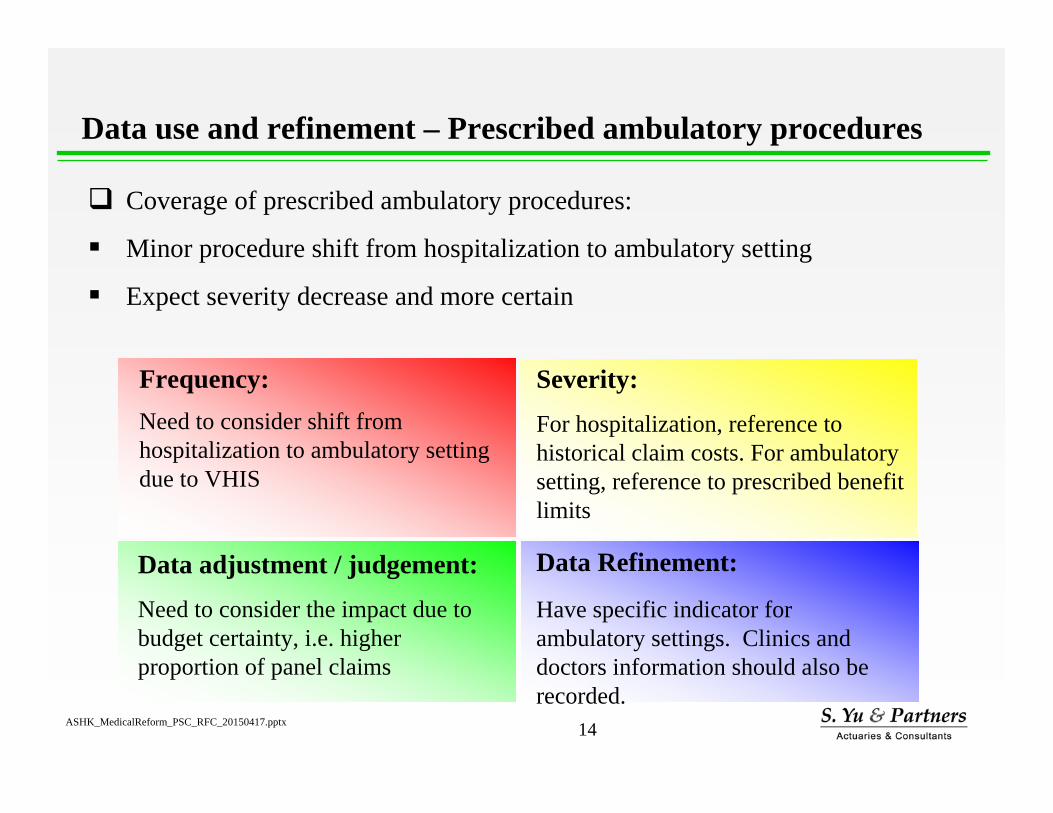

Data use and refinement – Prescribed ambulatory procedures

14

Coverage of prescribed ambulatory procedures:

Minor procedure shift from hospitalization to ambulatory setting

Expect severity decrease and more certain

Frequency:Need to consider shift from hospitalization to ambulatory setting due to VHIS

Severity:

For hospitalization, reference to historical claim costs. For ambulatory setting, reference to prescribed benefit limits

Data adjustment / judgement:

Need to consider the impact due to budget certainty, i.e. higher proportion of panel claims

Data Refinement:

Have specific indicator for ambulatory settings. Clinics and doctors information should also be recorded.

ASHK_MedicalReform_PSC_RFC_20150417.pptx

VHIS impact on pricing – Diagnostic tests and cancer treatments

15

Coverage of prescribed advanced diagnostic imaging tests and non-surgical cancer treatments:

Typically included in hospital expense or with very low benefit limits

Coverage significantly enhanced in VHIS

Increase claim cost, perhaps materially

ASHK_MedicalReform_PSC_RFC_20150417.pptx

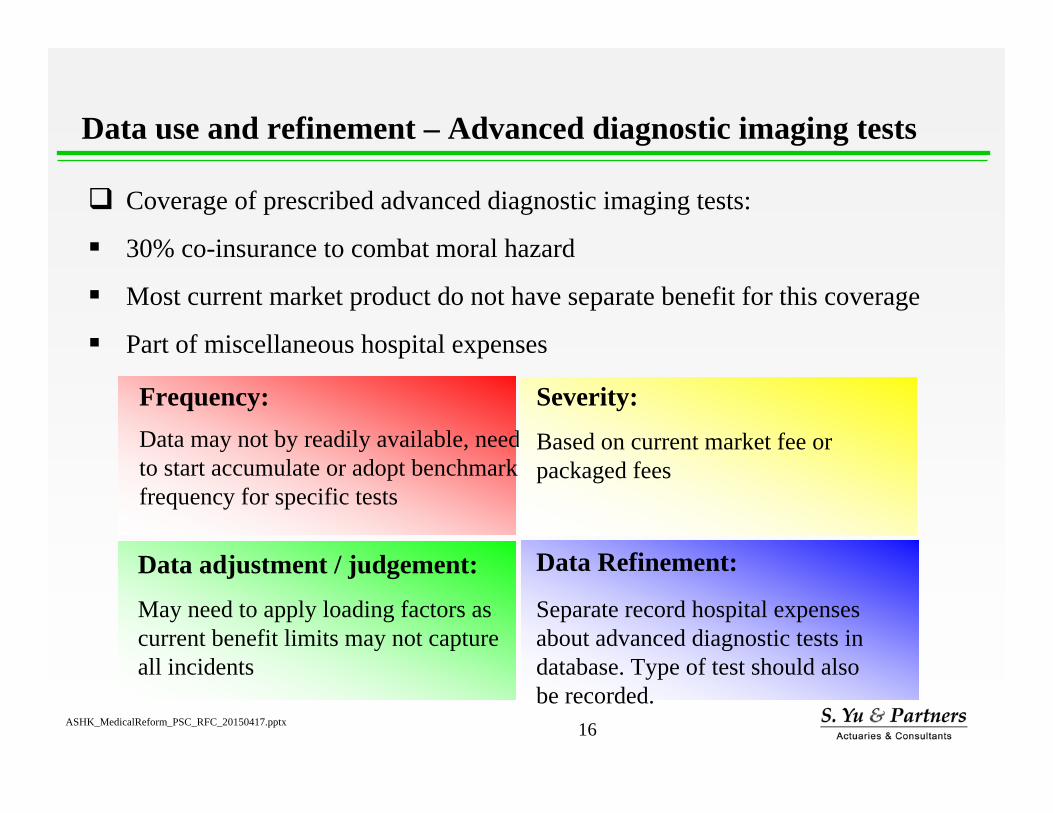

Data use and refinement – Advanced diagnostic imaging tests

16

Coverage of prescribed advanced diagnostic imaging tests:

30% co-insurance to combat moral hazard

Most current market product do not have separate benefit for this coverage

Part of miscellaneous hospital expenses

Frequency:Data may not by readily available, need to start accumulate or adopt benchmark frequency for specific tests

Severity:

Based on current market fee or packaged fees

Data adjustment / judgement:

May need to apply loading factors as current benefit limits may not capture all incidents

Data Refinement:

Separate record hospital expenses about advanced diagnostic tests in database. Type of test should also be recorded.

ASHK_MedicalReform_PSC_RFC_20150417.pptx

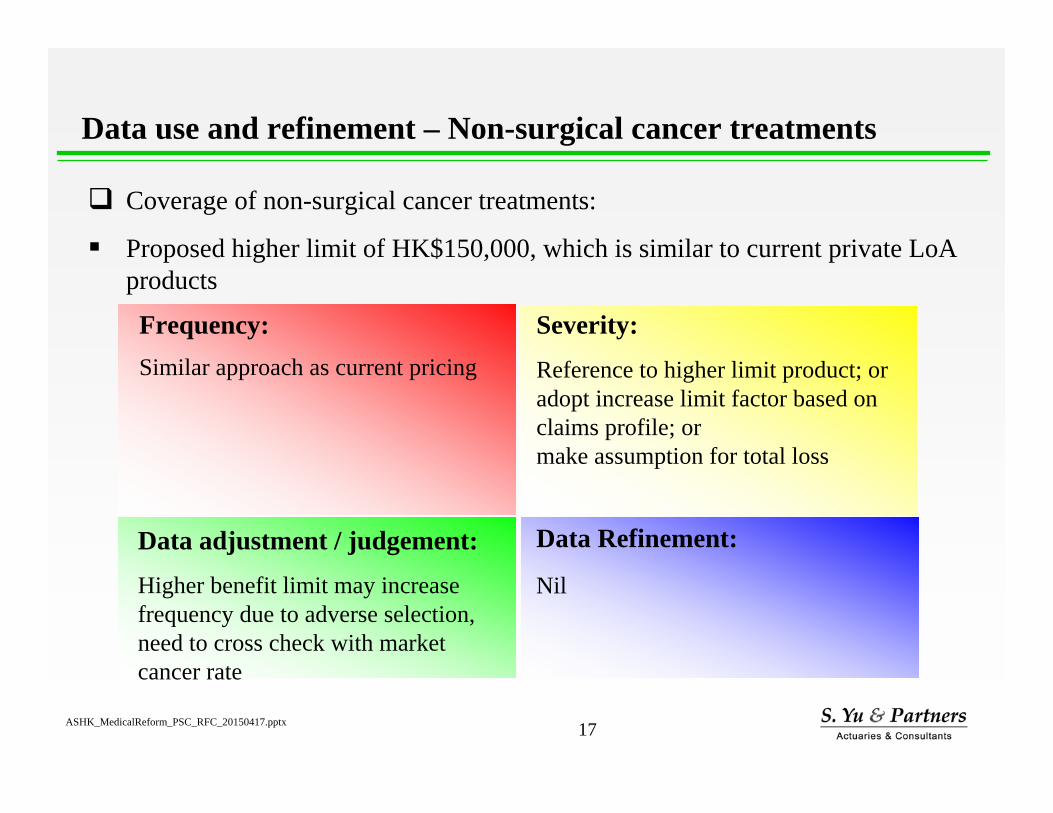

Data use and refinement – Non-surgical cancer treatments

17

Coverage of non-surgical cancer treatments:

Proposed higher limit of HK$150,000, which is similar to current private LoA products

Frequency:Similar approach as current pricing

Severity:

Reference to higher limit product; or adopt increase limit factor based on claims profile; ormake assumption for total loss

Data adjustment / judgement:

Higher benefit limit may increase frequency due to adverse selection, need to cross check with market cancer rate

Data Refinement:

Nil

ASHK_MedicalReform_PSC_RFC_20150417.pptx

Data use and refinement – Minimum Benefit Limits

18

Frequency:Similar approach as current pricing

Severity:

Similar approach as current pricing

Data adjustment / judgement:

If the Standard Plan limit is higher than existing product, may need to make reference to data with similar limit

Data Refinement:

Nil

For typical benefit items like Room & Board, Physician’s visit, Specialist’s visit and Surgical:

Proposed benefit limits similar or slightly lower than current ward products

ASHK_MedicalReform_PSC_RFC_20150417.pptx

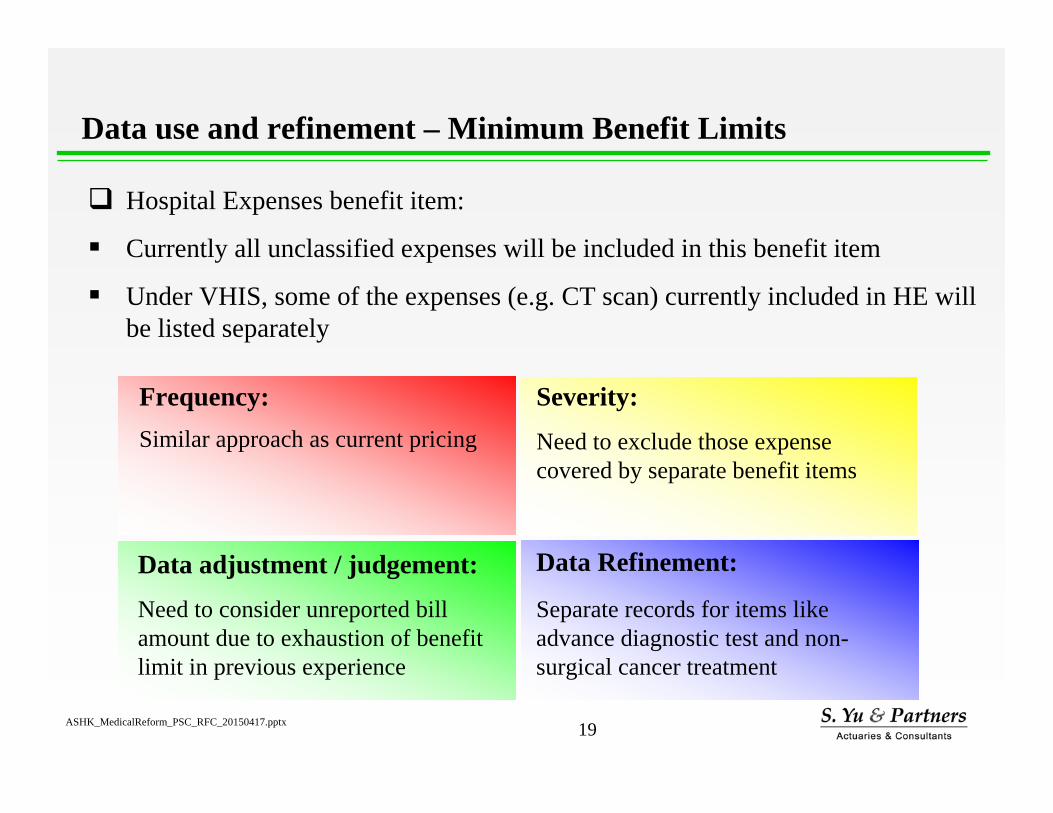

Data use and refinement – Minimum Benefit Limits

19

Frequency:Similar approach as current pricing

Severity:

Need to exclude those expense covered by separate benefit items

Data adjustment / judgement:

Need to consider unreported bill amount due to exhaustion of benefit limit in previous experience

Data Refinement:

Separate records for items like advance diagnostic test and non-surgical cancer treatment

Hospital Expenses benefit item:

Currently all unclassified expenses will be included in this benefit item

Under VHIS, some of the expenses (e.g. CT scan) currently included in HE will be listed separately

ASHK_MedicalReform_PSC_RFC_20150417.pptx

VHIS impact on pricing – Budget certainty

20

Budget certainty:

Severity become more certain and stable

Higher utilization of panel doctor and hospital

Impact on claim cost depends on network size and bargaining power

ASHK_MedicalReform_PSC_RFC_20150417.pptx

Data use and refinement – Budget certainty

21

Frequency:Similar approach as current pricing

Severity:

Non-panel: current practice;Panel: based on contractual fee for prescribed procedures and doctors

Data adjustment / judgement:

Need to make assumption for the migration of non-panel to panel doctors

Data Refinement:

Include doctor, clinic and test information in claim records

“No-gap/known-gap” arrangement applicable to specific:

Procedures / Tests

Hospitals / Clinics

Doctors

ASHK_MedicalReform_PSC_RFC_20150417.pptx

Agenda

Overview

VHIS Minimum Requirement for Standard Plan

VHIS Impact on Pricing, Data Use and Refinement

Data Field Checklist

Questions and Answers

22

ASHK_MedicalReform_PSC_RFC_20150417.pptx

Data Field Checklist

23

Data is vital for actuaries to estimate burning costs properly.

However, good data has to be accumulated over time.

Fortunately, medical claims are short-tailed and we still have time to accumulate credible data before implementation of VHIS.

Please compare your current data structure with the checklist and make necessary changes if the current structure is less comprehensive than the checklist.

ASHK_MedicalReform_PSC_RFC_20150417.pptx

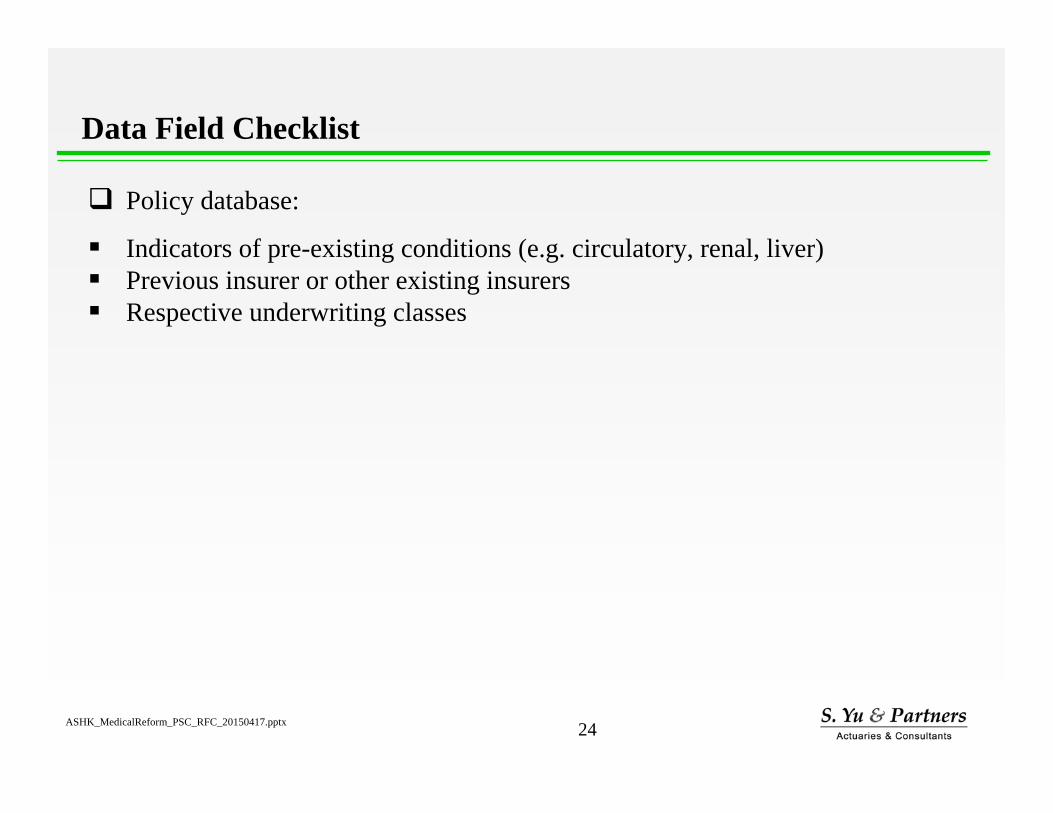

Data Field Checklist

24

Policy database:

Indicators of pre-existing conditions (e.g. circulatory, renal, liver) Previous insurer or other existing insurers Respective underwriting classes

ASHK_MedicalReform_PSC_RFC_20150417.pptx

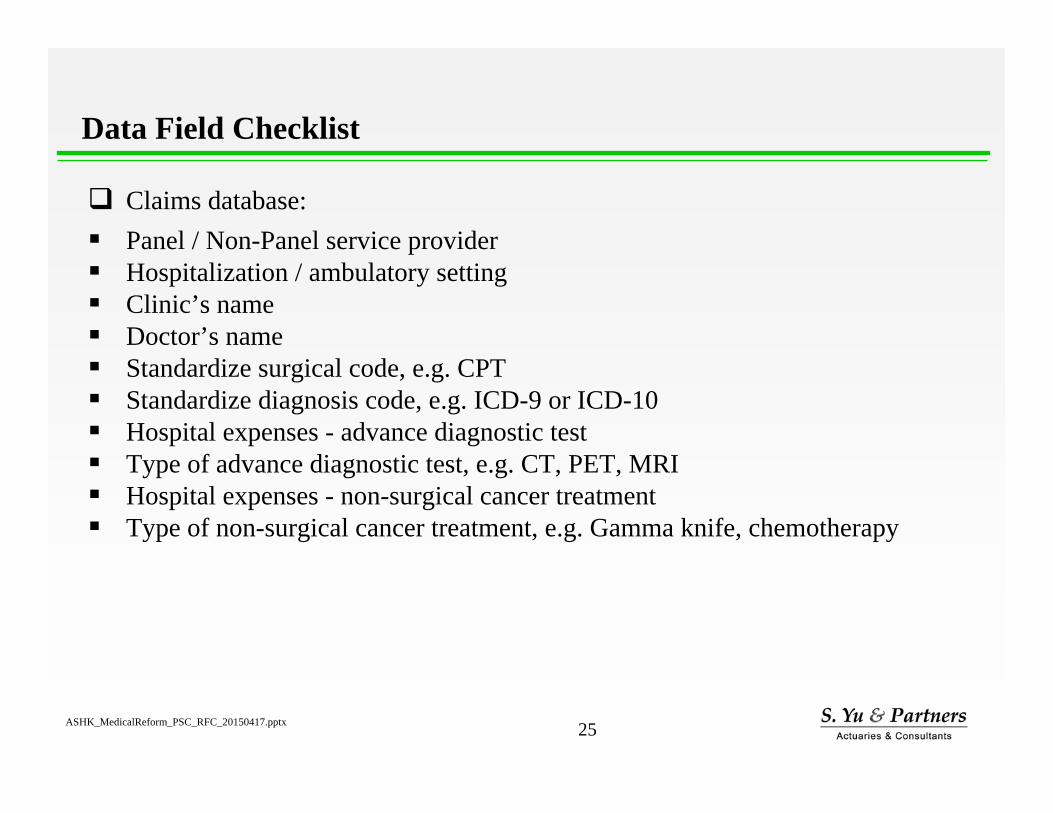

Data Field Checklist

25

Claims database: Panel / Non-Panel service provider Hospitalization / ambulatory setting Clinic’s name Doctor’s name Standardize surgical code, e.g. CPT Standardize diagnosis code, e.g. ICD-9 or ICD-10 Hospital expenses - advance diagnostic test Type of advance diagnostic test, e.g. CT, PET, MRI Hospital expenses - non-surgical cancer treatment Type of non-surgical cancer treatment, e.g. Gamma knife, chemotherapy

ASHK_MedicalReform_PSC_RFC_20150417.pptx

Agenda

Overview

VHIS minimum requirement for standard plan

VHIS impact on pricing, Data use and refinement

Data Field Checklist

Questions and Answers

26

ASHK_MedicalReform_PSC_RFC_20150417.pptx

Thank you for asking questions

Questions and Answers

27

ASHK_MedicalReform_PSC_RFC_20150417.pptx

Please feel free to contact me if you have any questions:

Mr. Fred Choi, S. Yu & Partners Ltd. at 2590 9896 or via [email protected]

Contact