Embed Size (px)

Citation preview

COST MANAGEMENT

COPYRIGHT © 2009 South-Western Publishing, a division of Cengage Learning.Cengage Learning and South-Western are trademarks used herein under license.

1

Accounting & ControlHansen▪Mowen▪Guan

Chapter 18Activity Resource Usage

Model and Tactical Decision Making

2

Study Objectives

1. Describe the tactical decision-making model.

2. Define the concept of relevant costs and revenues.

3. Explain how the activity resource usage model is used in assessing relevancy.

4. Apply the tactical decision-making concepts in a variety of business situations.

3

Tactical Decision Making

Steps of the tactical decision making process1. Recognize and define the problem.2. Identify alternatives as possible solutions to the

problem, and eliminate alternatives that are not feasible.

3. Identify the predicted costs and benefits associated with each feasible alternative. Eliminate the costs and benefits that are not relevant to the decision.

4

Tactical Decision Making

4. Compare the relevant costs and benefits for each alternative, and then relate each alternative to the overall strategic goals of the firm and other important qualitative factors.

5. Select the alternative with the greatest benefit which also supports the organization’s strategic objectives.

Continued from previous slide

5

Each year 25 percent of the harvest by an apple processor is small and odd-shaped.

These apples cannot be sold in the normal distribution channels and have simply been dumped in the orchards for fertilizer.

What should the firm do with these apples?

Step 1: Define the Problem

Tactical Decision Making

6

Step 2: Identify Feasible Alternatives

Tactical Decision Making

• Sell the apples to pig farmers.– Eliminate: not enough local farmers

• Bag the apples in five-pound bags and sell them to local supermarkets as seconds.– Feasible

• Rent a local canning facility and convert the apples to applesauce.– Feasible

• Rent a local canning facility and convert the apples to pie filling.– Eliminate: major capital investment required

• Continue with the current dumping practice.– Eliminate: status quo

7

Step 3: Identify Predicted Costs and Benefits; Eliminate Irrelevant Costs

Tactical Decision Making

Bagging Alternative5 lbs of apples per bag

Cost: $0.05 per pound for labor and materials (bags and ties)

Revenue: $1.30 per bag

Applesauce Alternative6 lbs of apples to produce five 16-ounce cans of applesauce

Cost: $0.40 per pound for rent, labor, apples, cans, and other materials

Revenue: $0.78 per can

8

Step 4: Compare Relevant Costs and Relate to Strategic Goals

Tactical Decision Making

Bagging AlternativeRevenue per lb$0.26Cost per lb0.05Net benefit per lb$0.21

Applesauce AlternativeRevenue per lb$0.65Cost per lb0.40Net benefit per lb$0.25 Forward

integration strategy

Product differentiation

strategy

9

Step 5: Select Best Alternative

Tactical Decision Making

• The apple producer is reluctant to follow a forward integration strategy

• The bagging alternative should be chosen

10

Tactical Decision Making

continued

11

Tactical Decision Making

Continued from previous slide

continued

12

Tactical Decision Making

Continued from previous slide

13

Relevant Costs and Revenues

• Relevant costs– future costs that differ across alternatives

• Irrelevant Costs– Past costs: already incurred “sunk costs”

are the same across alternatives; ignore

14

Relevancy, Cost Behavior, and the Activity Resource Usage Model

• Flexible Resources– Easily purchased in the amount needed– Purchased at the time of use

• Committed resources– Purchased before they are used

15

Relevancy, Cost Behavior, and the Activity Resource Usage Model

• Flexible resources– The activity resources demanded equal the

resources supplied

Demand changes relevant

Demand constant not relevant

16

Relevancy, Cost Behavior, and the Activity Resource Usage Model

• Committed resources– Excess of supply over demand is unused

capacity

Demand increase < unused capacity not relevantDemand increase > unused capacity relevantDemand decrease

Activity capacity reduced relevantActivity capacity unchanged non relevant

17

Relevancy, Cost Behavior, and the Activity Resource Usage ModelA company has five manufacturing engineers who supply a capacity of 10,000 engineering hours (2,000 hours each).The cost of this activity capacity is $250,000, or $25 per hour. The firm expects to use 9,000 hours.If the firm decides to reject a special order requiring 500 hours, the cost of engineering would be irrelevant.

18

Relevancy, Cost Behavior, and the Activity Resource Usage ModelThe firm can purchase a component that will drop the demand from engineering hours from 9,000 to 7,000.Since engineering activity capacity is acquired in chunks of 2,000, the company can lay off one engineer or reassign the engineer to another plant.

19

Relevancy, Cost Behavior, and the Activity Resource Usage Model

20

Illustrative Examples ofTactical Decision Making

Assumptions of C-V-P Analysis1. The analysis assumes a linear revenue function and a

linear cost function.2. The analysis assumes that price, total fixed costs, and

unit variable costs can be accurately identified and remain constant over the relevant range.

3. The analysis assumes that what is produced is sold.4. For multiple-product analysis, the sales mix is assumed

to be known.5. The selling price and costs are assumed to be known

with certainty.

21

Illustrative Examples ofTactical Decision Making

• Common Decisions– Make or Buy– Keep or Drop– Special Order– Sell or Process Further

• Cost analysis informed by– Activity-based cost management system– Functional-based cost management system

22

Talmage Company produces a mechanical part used in one of its engines. (Talmage produces engines for snowblowers.) An outside supplier has offered to sell a part (Part 34B) for $4.75. The company normally produces 100,000 units of the part each year.

Make-or-Buy Decision

Illustrative Examples ofTactical Decision Making

Flexible resources:

• Using materials

• Using direct labor

• Moving materials

• Providing power

• Inspecting products

Committed resources:

• Providing supervision

• Moving materials

• Inspecting products

• Setting up equipment

23

Illustrative Examples ofTactical Decision Making

Make-or-Buy Decision

ABC: buy the part

24

Illustrative Examples ofTactical Decision Making

Make-or-Buy Decision

Functional: make the part

25

Illustrative Examples ofTactical Decision Making

Keep-or-Drop Decision

If a segment is dropped only the traceable revenues and costs should vanish

ABC classifications provide information on traceable costs

Drop?

26

Dropping the product saves $45,000!

Illustrative Examples ofTactical Decision Making

Keep-or-Drop Decision

27

Accept or reject a special order

Illustrative Examples ofTactical Decision Making

Polarcreme, Inc., an ice-cream company, is operating at 80 percent of its 20 million half-gallon capacity.

A distributor from another geographic region offered to buy 2 million units of premium ice cream at $1.75 per unit.

Distributor will provide their own label and pay transportation costs. This sale is not subject to a sales commission.

Impact of special order on non-unit level activities:

Purchase orders increase 10,000Receiving orders increase 20,000Setups increase 13

28

Special order unit revenue$1.75

Unit-level variable costs:Dairy ingredients $0.70Sugar 0.10Flavoring 0.15Direct labor 0.25PackagingCommissionsDistribution 0.03Other 0.05Unit-level costs $1.450

Non-unit-level variable costs for special orderPurchasing ($8 × 10,000) ÷ 2M 0.040Receiving ($6 × 20,000) ÷ 2M 0.060Setting up ($8,000 × 13) ÷ 2M 0.052Non-unit-level costs 0.1521.602

Net benefit per unit on special order$0.148

Accept or reject a special order

Illustrative Examples ofTactical Decision Making

29

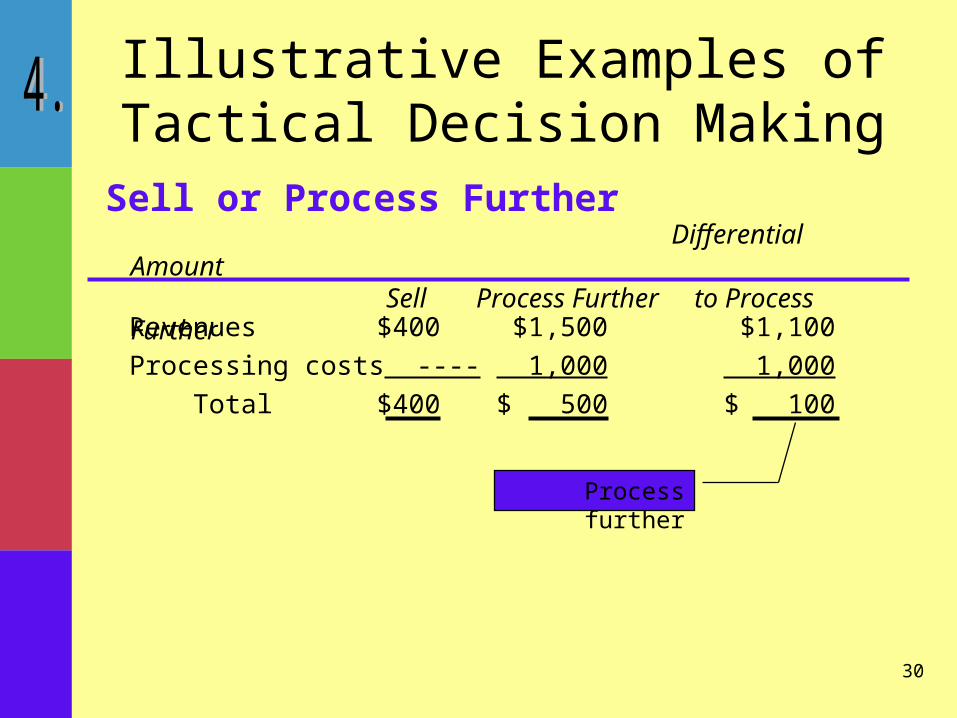

Joint products have common processes and costs of production up to a split-off point.

Sell or Process Further

Illustrative Examples ofTactical Decision Making

Joint products withcommon processesand common costs

Decision: Sell “Grade A” tomatoes as produce or process into hot sauce. 1 lb tomatoes yields 1 bottle of hot sauce.

Revenue at split-off 1,000 lb × $0.40Revenue from hot sauce 1,000 bottles × $1.50Costs to process into hot sauce $1,000

30

Differential Amount

Sell Process Further to Process FurtherRevenues $400 $1,500 $1,100Processing costs ---- 1,000 1,000 Total $400 $ 500 $ 100

Sell or Process Further

Illustrative Examples ofTactical Decision Making

Process further

COST MANAGEMENT

COPYRIGHT © 2009 South-Western Publishing, a division of Cengage Learning.Cengage Learning and South-Western are trademarks used herein under license.

31

Accounting & ControlHansen▪Mowen▪Guan

End Chapter 19