Embed Size (px)

Citation preview

A Guide to Activity Based Costing

The Crown

Prosecution Service

The Activity Based Costing Team within Operations Directorate

2

CONTENTS Why use ABC ? ..................................................................................................... Page 3 The Guide .............................................................................................................. Page 4 What is Activity Based Costing ? ........................................................................... Page 5 What is an Activity Based Cost ? .......................................................................... Page 6 How does ABC use ABC – Distribution v Determination ? ................................... Page 7 What does ABC cover and where is it used ? ...................................................... Page 8 How does ABC measure work ?....... ................................................................... Page 10 Caseload finalisations are important ............................................................... Page 11 How does ABC measure work elements ? .......................................................... Page 13 How does ABC measure considerative work ? ................................................... Page 14 Why does ABC sample and analyse cases ? ....................................................... Page 15 What is Relaxation Allowance ? .......................................................................... Page 16 What is Indirect Work ? ..................................................................................... Page 17 What is the Absence Factor ? ............................................................................ Page 18 To sum up ............................................................................................................ Page 19 FURTHER INFORMATION / CONTACTS ............................................................. Page 20 Technical Annexes Annex 1 The Allowances attached to ABC Annex 2 How the ABC model is developed

3

WHY USE ABC ? The decision to use ABC timings within the CPS ‐ Internal pressures

Prior to ABC timings there were concerns as to whether the service was providing an equitable distribution of scarce resource – or whether those who shouted loudest got the most resource. Imbalances of resourcing created a culture of ‘fat cats versus the rest’, which in turn caused unrest throughout the service. Addressing this was a prime motivation for the introduction of ABC timings. Helping managers to manage. You cannot cut costs unless you know what your costs are. Equally, the good manager needs to know the cost of what is being managed. The decision to use ABC timings ‐ External pressures CPS, as a responsible public organisation, must have tight control of running costs at a time when resources provided by central government are strictly limited. This is unimpeachable economic sense and is an absolute requirement of any responsible public body. The Treasury was looking for reductions in Civil Service expenditure and for Departments to have greater awareness on how and where resources were consumed, in a drive for greater efficiency. CPS costs rising against falling/static caseload (NB not workload). In the early to mid 1990’s, for example, CPS expenditure was increasing, in real terms, by around 6% a year, whilst at the same time caseload was gently declining. Less cases perhaps, but was there more to do on each of them? Law Officers (the Attorney & Solicitor General) raised concern about costs rising (increasing staffing levels) versus falling caseload. CPS argued that greater case complexity and additional tasks (such as new rules on disclosure) accounted for rising costs, but, had little evidence to support the argument. Increased emphasis on establishing wider CJS costs and models with numerous projects aimed at costing impacts across the various CJS agencies. Consequently, it is important for the CPS to know its contribution to the larger CJS picture and furthermore to be able to assess resource impacts of cross CJS initiatives. This is particularly important in an environment where any new investment is expected to show a return or realise “benefits”. Changes in work practices, criminal legislation and developing case law, which continues to grow in complexity, had significant impacts on our use of resources. The increased focus on disclosure, for example, increased the workload of prosecutors and caseworkers and cost CPS between an estimated £6m and £7m per annum in (at the time unrecognised) additional work. CPS assuming the responsibility for Charging, changes brought about by the Advocacy Strategy and the introduction of the COMPASS case management IT system, for example, also required examination of costs. How efficient are we? ‐ openness and external accountability. We spend taxpayer money. Do we spend it wisely? We need to demonstrate this when the questions are asked.

4

The Guide This guide is intended to answer the most common questions about ABC as practised in CPS, and should enable you to develop an understanding of the power and effectiveness of the CPS Activity Based Costing system and how it can be used as one of the factors in determining the provision of accurate resources to all CPS Areas. This guide is not intended as a detailed explanation of the theory behind Activity Based Costing or Activity Based Management, as many publications from the academic and business worlds cover these subjects in great depth. The aim is to provide a simple overview of how and why the CPS has used and adapted ABC to address its own particular needs. The Guide also focuses on how ABC timings are developed and their contribution to ABC models. The timings are just one of several key inputs into an ABC model. The outputs of the ABC model are one of the sources of information taken into account by Financial Planning and Budgeting each year when they are considering the budgetary requirements of each CPS Area. Annex 2 provides a brief overview of how ABC models are developed by colleagues in Financial Planning and Budgeting. Information on the work of the Financial Planning and Budgeting team can also be found on the CPS Infonet under “Finance / Financial Planning & Budgeting”. Importantly, any system such as the ABC timings system requires continuous maintenance to reflect changes in process, procedure and legislation. As such, although the material produced within this Guide is accurate at the time of publication, on‐going maintenance may well mean that elements of the system are subject to change during the currency of this Guide. Development of the ABC system in CPS is overseen by an ABC Steering Group who along with the ABC Team and Financial Planning and Budgeting within HQ, are responsible for the on‐going refinement and maintenance of the system in partnership with CPS Areas and other CJS Agencies. Resource allocation based on, or latterly partially informed by, activity costs has now been in place for in excess of 10 years.

5

What is Activity Based Costing?

Activity Based Costing (ABC) is exactly what it says it is, namely costing based on activity, be that of a person, team or an organisation. It is an internationally recognised system in which staff timings and costs are produced by breaking down each activity into its constituent parts to determine the work effort involved. This enables staff costs to be attributed to all activities within an organisation and provides a measurement of the amount of resource used to undertake specific elements of work. This invaluable data can be used to support any planning, monitoring and control systems, enabling managers to make better and more informed business decisions. If you cannot measure a task, you cannot manage it or, more importantly, improve it. We are all involved in costing activities every day of our lives although we may not always realise it. When we pay for goods in a shop, we are part of a complex costing transaction that helps the manufacturer pay wages, heating, lighting, rent, VAT, taxation and so on. Another portion of the payment goes to the upkeep of the shop we bought the goods in to pay salaries and support their continuance in the market place. Further elements will cover profit and possibly some shareholder dividend. Faced with a wages bill of tens of billions of pounds, Government should also know the true cost of its ‘product’ at every stage, so that it can truthfully demonstrate its efficiency around election time and prove that it is making best use of that most precious commodity – taxpayers money. For CPS, ABC means in‐depth measurement of the CPS/CJS processes and timings attributed to those processes to assist with equitable and fair resource distribution for all its Areas.

6

Number of files handled * staff time * salary costs = the cost of prosecution

What is an Activity Based Cost? CPS is not alone in using ABC. Most government agencies, particularly the bigger ones, use some form of ABC measurement, as do major companies, manufacturers, insurance companies, banks, retailers, building societies, airlines, universities, and so on. The techniques of ABC are used all over the world wherever there is a work process to be measured or a cost to be determined.

Activity Based Cost Management identifies the factors that drive costs in organisations. It also measures and analyses costs in a way that helps managers understand better what influences their core business. It also helps them to exert control in achieving objectives. An activity cost is simply a measure of the amount of resource used to undertake a specific element of work. The broad concept of activity costs within CPS is that the number of files handled, multiplied by staff time and staff salary costs, is equal to the total cost of staff time spent on the CPS prosecution process. The system is built purely on staff time (as this accounts for around three quarters of the cost) and excludes accommodation and other ancillary costs, e.g. Capital expenditure or payments to third parties such as Counsel. ABC does not replace performance indicators but illuminates them to make their messages more meaningful. Indicators on their own are rather like the controls in a car which tell you how many revs and what speed you are doing, but not if you are a good driver or are respecting the speed limit. After all, the simple cost of a case can always be determined by dividing expenditure by caseload but this tells you nothing about the efficiency or quality of the product or how the organisation is running, only how much the case costs on average.

7

How does CPS use ABC?

ABC measurement was initially introduced primarily to address the need for a fair and equitable allocation of running cost budgets to Areas. Imbalances of staff distribution were common knowledge within CPS with many believing that those who shouted loudest got most, with other areas being disadvantaged. Use of ABC data offered the opportunity to distribute funds within CPS based on need related to workload, rather than precedent. ABC, within the CPS, is used (amongst other things) to help inform the resource distribution exercise. Only the core prosecution process on the majority of cases in CPS Areas is measured in ABC. The work in other parts of CPS outside the Areas prosecution process is not covered by ABC models. How does ABC distribution work? ABC models are one of the factors used when Financial Planning and Budgeting decide on Area shares. In simple terms, an ABC staff profile is calculated for each Area. This staff profile is calculated by multiplying the ABC times to deal with different types of case by the volume of those cases dealt with in each Area. The total time required tells us how many staff at different levels are needed (as we know how many minutes per year equals one member of staff). The number of staff is then converted into £ costs by applying the average annual salary costs for each staff level in each Area. So for each Area we can calculate a total ABC cost based on its caseload and case mix. Aggregating these results from all the CPS Areas provides a National ABC cost. We can then determine what proportion of the National ABC cost is appropriate to each Area based on its ABC share. This, along with other factors, then helps inform the budget distribution exercise completed by Financial Planning and Budgeting colleagues ‐ contact details shown at Page 20. The ABC share principle can also be applied to assist in assessing the balance of staffing between different Business Units in Areas/Districts, or if your Area/District is restructuring and you are seeking an indication of how to distribute existing staff. An easy‐to‐use Excel based package has been developed for this and along with appropriate training is available from the ABC Team contacts at the end of this Guide or on the CPS Infonet . Please note that this tool is designed to assist purely in decisions re allocation of staff and should not be seen as providing an indication of staff numbers actually required.

8

What does ABC cover and where is it used?

ABC currently focus on the core prosecution process work undertaken in CPS Areas by both legal and administrative staff in levels A to D, excluding work undertaken by those staff not directly involved in the casework process i.e. staff within Area Operations Centres (AOCs). This is where the majority of operational staff are based, and where casework is more predictable and averages can be more readily applied. Associate Prosecutor activity is included within the timings but Higher Court Advocacy is excluded as this is funded via other means at present. ABC timings do not cover work in National HQs, Business Support Centres, or CPS Direct.. It also does not cover cases within the Casework Divisions dealing with aspects such as Counter Terrorism, Special and Organised Crime etc. Whilst ABC modelling assigns funding within Area share calculations for cases finalised in Area Complex Casework Units (CCU’s) separate timings are not produced by the ABC Team for CCU cases as they deal with cases of widely variable duration, and complexity. Cases of this sort do not lend themselves to the application of averages as such averages would be unreliable and therefore specific case timings are not viable. Alternative measurement techniques are being explored by the service which may, in time, capture times and costs applicable to such work. ABC models produced by Financial Planning and Budgeting deal only with payroll costs and do not encompass prosecution costs i.e. counsel fees, other general administrative costs or capital expenditure. ABC models do not cover what is called “non baseline” funding provided for specific purposes or projects from other CJS sources. For example, the introduction of Statutory Charging was funded via ring fenced funding for several years, until deemed to be “business as usual”. ABC modelling produces a profile of the staff generated, by level, for each Area. This information can be used by the Finance Directorate to assist them in deciding appropriate budget allocations. ABC data is used by departments such as the Ministry of Justice to inform models such as the Waterfall Model. Such models can be used to inform the Home Secretary and Government in general, of the estimated impact of legislative changes on the cost of the criminal justice system, as well as to measure the impact and benefits of key CJS change initiatives. ABC provides support to many initiatives within and beyond the bounds of CPS, particularly in terms of business cases and benefits realisation for many change projects e.g. the Digital Business Programme and Cross CJS Efficiency. Members of the team also work from time to time with Policy colleagues in assessing impacts of new procedures arising from policy change.

9

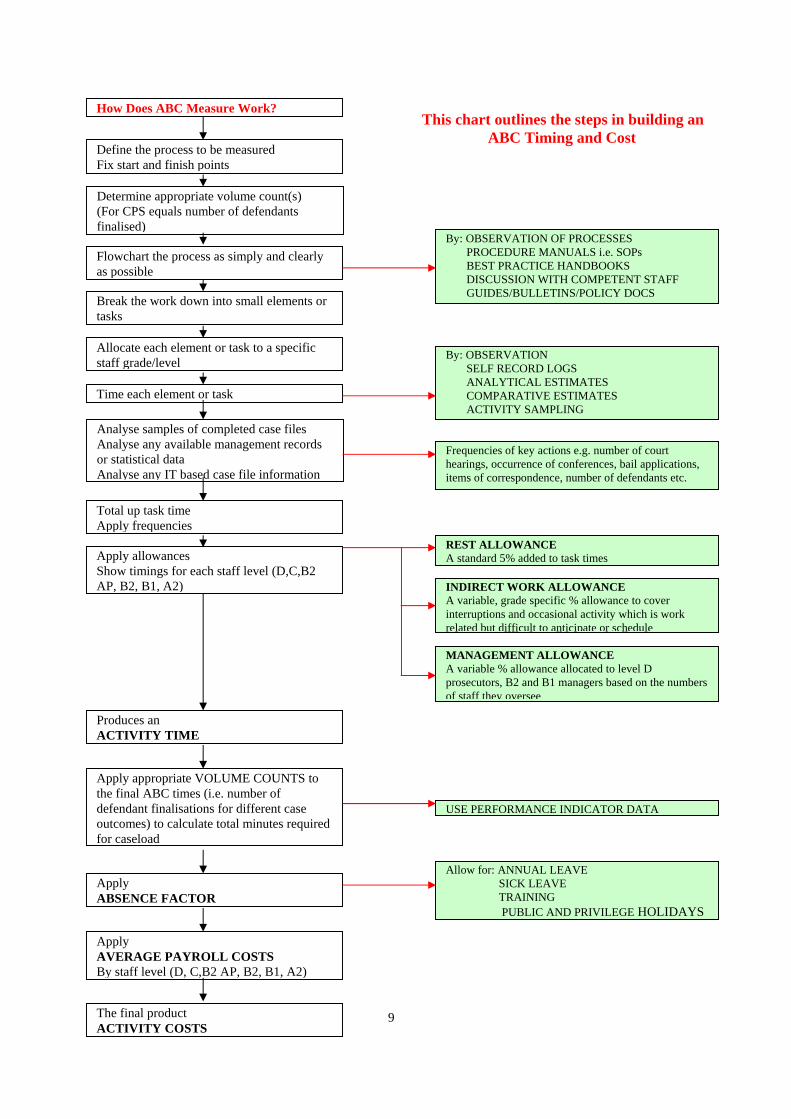

How Does ABC Measure Work?

Produces an ACTIVITY TIME

Apply appropriate VOLUME COUNTS to the final ABC times (i.e. number of defendant finalisations for different case outcomes) to calculate total minutes required for caseload

Apply ABSENCE FACTOR

Apply AVERAGE PAYROLL COSTS By staff level (D, C,B2 AP, B2, B1, A2)

REST ALLOWANCE A standard 5% added to task times

INDIRECT WORK ALLOWANCE A variable, grade specific % allowance to cover interruptions and occasional activity which is work related but difficult to anticipate or schedule

MANAGEMENT ALLOWANCE A variable % allowance allocated to level D prosecutors, B2 and B1 managers based on the numbers of staff they oversee

By: OBSERVATION OF PROCESSES PROCEDURE MANUALS i.e. SOPs BEST PRACTICE HANDBOOKS DISCUSSION WITH COMPETENT STAFF GUIDES/BULLETINS/POLICY DOCS

By: OBSERVATION SELF RECORD LOGS ANALYTICAL ESTIMATES COMPARATIVE ESTIMATES ACTIVITY SAMPLING

Frequencies of key actions e.g. number of court hearings, occurrence of conferences, bail applications, items of correspondence, number of defendants etc.

Allow for: ANNUAL LEAVE SICK LEAVE TRAINING PUBLIC AND PRIVILEGE HOLIDAYS

USE PERFORMANCE INDICATOR DATA

The final product ACTIVITY COSTS

Apply allowances Show timings for each staff level (D,C,B2 AP, B2, B1, A2)

Total up task time Apply frequencies

Analyse samples of completed case files Analyse any available management records or statistical data Analyse any IT based case file information

Time each element or task

Break the work down into small elements or tasks

Allocate each element or task to a specific staff grade/level

Flowchart the process as simply and clearly as possible

Determine appropriate volume count(s) (For CPS equals number of defendants finalised)

Define the process to be measured Fix start and finish points

This chart outlines the steps in building an ABC Timing and Cost

10

Caseload Finalisations are important Although there are various techniques to measure and quantify work, an equally important part of the ABC modelling undertaken by Financial Planning and Budgeting are Performance Indicators which act as Volume Counts, and tell us how many defendants finalisations have been completed. Knowing how long or how much money a case takes to finalise is useful but unless we know how many of them we have done in the past or will do in future, the information has limited use. In the ABC timings system, timings have been measured for types of case that Areas routinely count as part of the standard CIS Performance Indicators package. The counts relate to the different types of CASE OUTCOME in both magistrates’ and Crown Courts.

Why is it important to accurately record all cases dealt with? The key factor in determining an Area’s ABC share is its caseload and case mix, and so it is very important that all staff members are properly trained and aware of the need to correctly finalise all cases. Failure to do so could impact on an Areas ABC share which in turn may affect decisions taken by Financial Planning and Budgeting in relation to budget allocations, as well as distorting the true position on caseload figures. HOW CAN WE ENSURE THAT WE CORRECTLY RECORD OUR CASELOAD?

Make all staff aware of the importance of recording case finalisations with regard to potential budgetary impacts and therefore staffing;

Ensure that staff responsible for recording case finalisations are appropriately trained;

Ensure that training needs are monitored with regard to case finalisations, especially when new procedures/policies mean that changes may occur;

Regularly review your Area’s system for ensuring that cases are finalised to reduce the risk of cases being overlooked;

Complete regular dip sample checks to ensure that bad practice and incorrect interpretation does not creep in;

Keep caseload finalisations under review – identify trends or anomalies at an early stage, investigate and question

Remember – perhaps as few as 25 missed Crown Court finalisations each year can equate to a B1 caseworker in your Areas ABC profile! SOME COMMON PROBLEM AREAS RELATING TO FINALISATIONS –

11

Pre Charge Decisions and Consultations

Specified offences

Other proceedings

Guilty pleas as opposed to Guilty verdicts

Late finalisation of Crown Court cases

Guilty pleas not marked as on day of trial where required

12

How does ABC measure work elements? Most people walking into a work situation would not know where to begin to convert what they see into facts and figures. The ABC team has been trained to do this. Work‐study and Measurement is a professional qualification and ABC Team members are accredited by the Institute of Management Services. The foundation of ABC is in‐depth analysis of cases across a sample of Areas to examine the prosecution process as it really is. The starting point is construction of workflow process charts showing the work steps for each part of the process, and who completes the task, followed by calculation of how long on average, would be required for completion of each part of the process. The timing of the work steps is done in various ways: a) Observation, which is direct timing and activity sampling undertaken by the team b) Analytical estimation, where experienced lawyers and caseworkers provide estimates based on their

own experience of time required for actions such as review and court attendance. c) Simulation – where team members perform certain tasks and time them, for example some tasks

involving the Compass Case Management system. d) Self record logging by members of staff involved in the process. e) Comparative estimation where a new work task is compared to one already timed where there is

similar work content and then allocated a time accordingly There are also certain aspects of prosecution work that cannot be anticipated, such as interruptions, or telephone calls but which are legitimate and necessary parts of the process. These are dealt with by additional allowances added to the basic times. Details of these allowances are covered later in the guide

13

How does ABC Measure Considerative work?

Considerative work and reading time represents the highest proportion of time spent by prosecutors and counsel working on CPS case files. There are a number of ways to estimate average considerative time, although no method guarantees observed measured exactness: a) Estimation by an experienced prosecutor An experienced lawyer examines completed cases and estimates the consideration time for each element of the case over the range of case types, based on their personal approaches (“I would need 30 minutes to deal with this aspect”, and so on). b) Estimation by focus groups A group of experienced lawyers examine completed cases and argue towards an agreed estimate of the consideration time required for each element of the case over the range of case types, based on their personal experience and approaches. c) Self‐record logs A self‐record log is attached to each file or held electronically and prosecutors enter timings appropriate to each considerative action undertaken. d) Combination of all above approaches Combine the above approaches to determine an effective average timing per case type. Predominantly, we use methods a) and c) as these are the approaches which result in minimal disruption to the normal day to day running of the service.

14

Q. Why does ABC sample and analyse cases? ABC timings are based on a continuous and rolling sample of finalised cases analysed in CPS Areas. With approximately 730 thousand CPS defendants per year finalised through the courts, investigating data from the whole sample is often impossible. However, where possible analysis is informed by national data within CMS/MIS. Where data is not available from management information systems to overcome the difficulty of not being able to assess data from the whole national caseload, sampling methods are used, and conclusions drawn from the sample to support the Activity Timing system, currently housed within Excel spreadsheets. The benefits of sampling particularly when using case management IT systems include quicker results, the ability to collect larger and more widespread samples and lower collection costs. Historically, some of the information from cases came from finalised paper based case files which the ABC Team manually assessed. Ongoing this will no longer be possible with the advent of the electronic case file and therefore other data sources are now used to a much greater degree. The ABC Team also use any available statistical records, local monitoring data and also any data collected by other agencies e.g. Ministry of Justice data on Crown Court hearing types and durations, and also Crown Court sitting times. Since the introduction of the CPS Compass case management system and with the increasing use of IT to store and manage case file material, sampling has now moved more and more towards the electronic case file as more and more information is held there. This enables increased numbers of cases to be sampled across a wider range of Areas at a reduced cost to the service. However, there may still need to be some requirement to examine paper files (particularly for Crown Court cases) for the foreseeable future. So why analyse cases at all? Quite simply, case analysis is the best way to establish how often different actions took place on different types of case. These are known as frequencies and are a key element in determining the work effort (time) and therefore cost, of dealing with different types of case. For example, we may establish the time required to issue a letter but it is also useful to know how many letters on average are dispatched for each type of case. Similarly the overall time required for a case will depend on the occurrence of many different activities and by sampling case files we can establish what percentage of cases have a particular action on them and how often it occurs. The ABC Team regularly update data on key or what we call sensitive frequencies, i.e. those which have the greatest impact on the overall time per case e.g. the number of court hearings for each type of case.

15

What is relaxation allowance?

Timing individual tasks, and knowing how many of those tasks occur, is not sufficient to ensure that the ABC timings can help the CPS to be able to estimate the required number of staff required to undertake a particular task. To enable such an assessment to be made a number of allowances are added to timings to reflect working in a live office environment. One key element in the welfare of staff at all levels within the workplace (CPS or wherever) is that performance must be accompanied by regular periods of rest, recovery and refreshment. This is to allow appropriate recovery from work effort and adequate rest to ensure good performance after the rest period. If these are not taken, performance often suffers. Only machines work all the time and those that work all the time often break down. Rest Allowance rates can vary from organisation to organisation, and this is often dependent on the type of work being measured and how physically and mentally debilitating it can be. The rate may also be dependent upon the predominant method of measurement where timings based on “looser” methods such as self‐record or estimating will use a lower rest allowance rate than other timings where the measurement methods such as pre‐determined timing data or observer based recording are “tighter” At present, the CPS ABC timings include a relaxation allowance set at a 5% enhancement to the basic timings. The overall impact of these allowances is a further enhancement of ABC timings to ensure that staffing numbers generated are commensurate with the prosecution process while allowing regular breaks for all staff.

16

What is Indirect Work? The situation is a familiar one. It's lunchtime, the office is deserted and a phone rings. It’s not your phone but you stop what you are doing and answer it. You answer the query. After a 5‐minute chat that sorts the whole situation out, you put the phone down, scribble a note for the absent colleague and return to your desk to carry on with what you were doing before you were interrupted. Although this is a simple sequence of events the interruption adds to the time taken to do your own job This additional time is called Indirect Work and these activities are legitimate work‐related tasks which support the core process but which occur only occasionally or which are difficult to anticipate or plan. There are numerous examples of Indirect Work every day within CPS, at all levels – telephone calls, e‐mails, case related discussion, meetings, personal development reporting activity, giving and receiving advice to each other. All are proper working activities that cannot generally be anticipated or placed precisely within a process chart. A distinction is made between personal telephone calls or non‐work related discussions, which are classed as personal time. ABC must accurately capture the impact of these interruptions to provide realistic assessments of resources required to do the job. Historically this has been achieved through a measurement process known as Activity Sampling and the results produce allowances, which enhance basic ABC timings to reflect any time spent legitimately on interruptions.

17

What is the Absence Factor? Activity Cost Timings are initially calculated on the basis of 100% attendance at work by staff. Obviously, there are occasions when staffare not in attendance and allowance has to be made for these within ABC. In simple terms, we know that ABC may indicate that 4 people are needed to do a particular job, but the combined impacts of annual leave, sickness and training courses can reduce attendance and mean that 5 people are actually needed to cover that specific workload. Activity timings are enhanced by a specific absence factor for CPS covering –

Annual leave (an average of 31.15 days per person per annum),

Sickness (an average of 8.2 days per person per annum)

Training (an average of 5 days per person per annum).

Public holidays and privilege days (9 days per person per annum)

The average days quoted above are per “full time equivalent” member of staff, and are wherever possible based upon data provided by CPS HQ. The figures represent expectations for the financial year 2014/2015. In total, staff figures generated by ABC are enhanced to reflect the fact that on average, each member of CPS staff will be absent for 44.35 of the available 252 days in the working year (365 days – 104 weekend days ‐ 9 bank holidays/privilege days). Using this information we can enhance any measured time in minutes, or total staff required, to include allowance for annual leave, sickness etc.

18

To sum up.................... ABC provides CPS with a number of benefits.

The ability to use ABC data as part of the resource allocation exercise to help ensure a more equitable distribution of running cost resources/budgets to the 13 CPS Areas, based on their relative caseload and case type.

Meaningful performance management information for managers at all levels within the organisation, and beyond.

Operational costing information on all aspects of CPS casework performance, and costing support for any “what‐if” scenarios, or policy changes.

Contributes to assurances to government and other bodies on CPS cost efficiency.

Costing of new proposals for CPS and support for business cases / benefits realisation work on all major change initiative projects and programmes.

Identification and advice on the avoidance of inefficiencies within the CPS prosecution process.

Essential information to other agencies (ABC is a leading contributor to CJS planning models) about the cost of common areas of concern – important in the Criminal Justice System where performance is often dependent upon other Agencies

19

FURTHER INFORMATION If you have any other questions regarding Activity Based Costings and Timings, the ABC

team can be contacted on the following numbers: Shaun Morris Leanna Lane ABC Advisor ABC Advisor 14th Floor 14th Floor Colmore Gate Colmore Gate Birmingham Birmingham B3 2QA B3 2QA Tel: 0121 262 1122 Tel: 0121 262 1121 [email protected] [email protected] The ABC team is happy to deal at any time with queries on any aspect of timings,

workflows, allowances and absence factor. Further information on measurement methods and techniques used can also be provided.

Enquiries on Resource models, the Corporate Information System and ABC modelling

may be made to our colleagues in Financial Planning and Budgeting on the following telephone number:

Tel : 01904‐545595 If your question concerns the distribution/allocation of resources to Areas, please direct

your query to this number. ABC Team April 2014

20

Technical Annexes 1 to 2

21

Annex 1

ALLOWANCES ATTACHED TO TASK TIMINGS RELAXATION ALLOWANCE Relaxation allowance is the allowance of time made to a worker for personal needs and for recovery from fatigue caused by doing a job. A principle of work is that the worker should be able to achieve standard performance as an average over a day or shift without becoming more than reasonably tired ‐ the period of rest is calculated on that basis. Relaxation allowance is set as a percentage of the average basic time for each element, and is considered to compensate for;

a. Posture b. Motions c. Visual fatigue d. Energy output e. Personal needs f. Thermal conditions g. Atmospheric conditions h. Other environmental influences

Relaxation Allowance can vary dependent upon the nature of the work and working environment, and is a matter for each organisation to assess. INDIRECT WORK In all jobs, a workers task will include a number of elements that interrupt the core task, and a number of minor activities that may be so spasmodic or infrequent that precise work measurement cannot be undertaken economically. To provide for such situations, an Indirect Work Allowance, expressed as a percentage of the basic times, is included in the work content for the job. This enhances job timings by between 16% and 45%, dependant on staff level and function.

22

MANAGEMENT Management allowance in the CPS model is calculated as a percentage allowance and allocated to Level D lawyers, as the key management level for prosecutors within the ABC system, and Level B2 and B1 managers of administrative and casework staff. Within the ABC models management time and posts are earned via a straightforward multiplier based on the number of staff under supervision and is measured for each section under analysis. In broad terms, for every 12.42 level C lawyers earned through the ABC timings, a Level D lawyer manager is generated in the models. Similar multipliers apply for B2 staff – based on the number of B1caseworkers generated, and at B1 – based on the number of Level A staff generated. PRODUCTIVITY Productivity is the quantitative relationship between what we produce and the resources which are used in that production. Input consists of labour, materials, plant, land, buildings and energy, while output consists of product, services and information. For measurement purposes, the value of productivity is usually set at 100%. ABSENCE FACTOR Absence factor is an allowance to take account of the fact that staff do not work every day of the calendar year. It allows for absences due to major elements such as: a) Annual leave ‐ averaged at 31.15 days b) Public and privilege holidays ‐ 9 days c) Average sick absence – 8.2 days d) Training – 5 days A total absence factor is produced. For financial year 2014/15 this is 44.35 days applicable to the calculation of core workload requirements, which equates to 207.65 days worked in the normal working year of 252 days (365 days minus weekends and public/privilege holidays). Annex 2

23

How the ABC model is developed (additional note to Chart on Page 9 of the Guide) The foundation of activity cost modelling in CPS is in‐depth analysis of the business processes and timings attributed to those processes. The analysis for CPS is undertaken by a team of 2.72 staff from the Operations Directorate who develop and maintain a series of timings covering the core business of processing Area casework. Data for the model is regularly gathered from a sample of Business Units and timings are updated each year in September to align with the resource allocation programme undertaken by Financial Planning and Budgeting. Timings submitted in September are one of the factors taken into account by Financial Planning and Budgeting when they decide on appropriate resource allocations for the following financial year. The integrity of the data is the key element in retaining the accuracy of ABC timings and their value as a management tool which is why all timings are continuously reviewed and updated as appropriate to reflect changes in procedures and working practices. CPS Activity Costings as produced by Financial Planning and Budgeting are derived from 3 sources

of information ‐

Timing activities involved in the prosecution process;

Applying workload volumes from caseload outcome data (PIs) and;

Applying payroll costs for each staff level involved in the prosecution process. In simple terms, to determine the cost of review on a certain type of case, we might calculate that:

A lawyer takes an average 15 minutes to review each case of that type:

There are 1000 cases to review each year and;

The lawyer has an average payroll cost of 70p per minute. The activity cost of reviewing the total caseload is therefore; 15 mins x 1000 cases x 70p per minute = £10,500 The same principle is applied in calculating activity costs for all case types across different staff levels within CPS Areas. Activity Cost models ABC models are prepared by Financial Planning and Budgeting quarterly, using total payroll figures for the current financial year. These activity costs models are designed to show for each geographical Area:

Amount of time expressed in minutes and consequential staffing profile required to carry out the work;

Payroll costs of the staff required to carry out the work

24

Average annual payroll costs by grade Using annual payroll costs enables the time required to complete each activity to be translated into monetary terms, thus facilitating budgetary planning, costing and management. Costs of activities by grade can also be established. Although activity timings are built as national averages, payroll costs for each staff grade are determined on an Area specific basis. CPS activity cost models produce figures relating to the estimated number of posts required in each grade to deal with the caseload handled in each Area. These figures are otherwise described as the ABC staff profile and have two uses, which are:

They enable rough comparisons with the numbers of staff, and staff substitutes, actually in post in Areas (although caution should be applied when doing this as ABC timings do not include all work and Area specific practices will need to be taken into account to achieve a “like for like” comparison); and

They can when converted into a monetary cost allow comparison with the actual payroll expenditure of an Area (again taking into account there will be variations due to activities not captured by ABC timings and also as a result of Area specific practices).

For the latter purpose the average annual payroll costs by grade for individual Areas are used. This information is derived directly from payroll records and takes the following payroll costs into account: Basic pay ERNIC London Allowances Overtime Allowances Other Allowances ASLC (Superannuation) Miscellaneous payments * As stated above whilst comparisons can be made it is important to bear in mind that ABC timings do not capture all work carried out within Areas and therefore we should not expect figures to correlate. The average annual payroll costs calculation includes payments of Saturday Allowances to lawyers, sickness costs incurred, excess fares and payments to part‐time staff. It does not include payments for overtime, payments to staff leaving the Service made during their last month of service, or payments made to staff allocated to the CMP (central pool). It does not therefore include staff on half or no pay. All these items are excluded because they would distort the averages.

Summary It is important that the three elements of time, volume and payroll in the activity cost equation are as accurate as possible. The old adage applies that any system is only as good as the quality of information fed into it. The benefit of accurate timings can be devalued if data in the PI system about case outcomes is inaccurate or incomplete. In summary Activity Costs produced by Financial Planning and Budgeting comprise ‐

ACTIVITY TIMINGS multiplied by case outcome volumes to provide the TOTAL TIME required;

25

TOTAL TIME required converted to staff‐years to provide TOTAL STAFF required;

TOTAL STAFF required multiplied by payroll costs to provide TOTAL COSTS