Embed Size (px)

Citation preview

Statement of Financial Position format and its elements

Basic accounting equation

Effects of transactions on the basic accounting equation

Expanded accounting equation.

Effects of transactions on the expanded accounting equation

Nik Nurul Aswani binti Nik Kamarudin (UiTM Perak Branch)

1

After completing this chapter, students should be able to:

Identify the elements in the Statement of Financial Position and relate them with the accounting equation.

Identify the effects of business transactions on accounting equation.

2

Nik Nurul Aswani binti Nik Kamarudin (UiTM Perak Branch) 2

Madam Nik Ent.

Financial institutions / Banks

Suppliers / Creditors / Payables Employees / Bills(Expenses)

Customers / Debtors / Receivables

Madam Nik

Business Transactions

suppl ier s

Purchase of assets on cash/ credit

Capital

Nik Nurul Aswani binti Nik Kamarudin (UiTM Perak Branch) 3

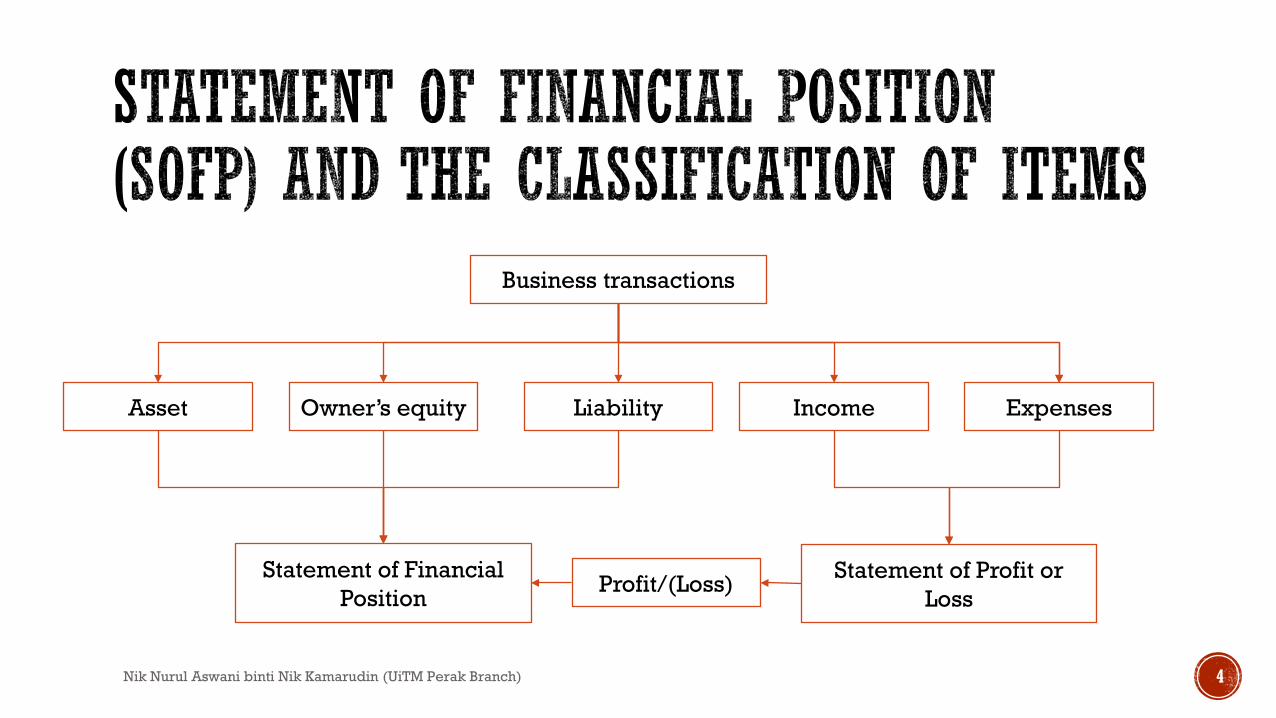

Business transactions

Asset Liability Income ExpensesOwner’s equity

Profit/(Loss)Statement of Financial

PositionStatement of Profit or

Loss

Nik Nurul Aswani binti Nik Kamarudin (UiTM Perak Branch) 4

Nik Nurul Aswani binti Nik Kamarudin (UiTM Perak Branch) 5

Nik Nurul Aswani binti Nik Kamarudin (UiTM Perak Branch) 6

• Asset:• A present economic resource controlled by

the entity as a result of past events, and has the potential to produce economic benefits.

Nik Nurul Aswani binti Nik Kamarudin (UiTM Perak Branch) 7

Asset bought not for resale but to be used in business operation and has estimated useful life of more than one year.

3 categories: Tangible NCA NCA that has physical substance

Intangible NCA NCA with no physical substance

Investments Sum of money placed in other organisation with the expectation of getting returns.

Nik Nurul Aswani binti Nik Kamarudin (UiTM Perak Branch) 8

Tangible NCA Intangible NCA InvestmentsLandBuildingMotor vehicles (Car, Van, Lorry, Motorcycle)EquipmentMachineryFurnitureFixture and fittings

PatentTrademarkRightsLicensesGoodwill

Fixed depositLong-term investment

Nik Nurul Aswani binti Nik Kamarudin (UiTM Perak Branch) 9

Assets that are either cash or can be converted into cash within one year.

Examples:

Current AssetsClosing inventoryAccount receivablesShort-term investmentCash in handCash at bankPrepaid expensesRevenue not yet received

Nik Nurul Aswani binti Nik Kamarudin (UiTM Perak Branch) 10

Owner-supplied funds to the business / The amount of financing by the owner.

The amount of equity may increase due to PROFITS earned by the business.

The amount of equity may decrease due to LOSSES made by the business as well as DRAWINGS made by the owner.

Drawings: The amount of cash or other assets took by the owner for personal use.

Nik Nurul Aswani binti Nik Kamarudin (UiTM Perak Branch) 11

Capital Profit/(Loss) Drawings Owner’s equity

Income – ExpensesIf Income > Expenses = ProfitIf Income < Expenses = (Loss)

Funds supplied by external parties to the business

Two types: Non-current liabilities: Amounts owed by

the business that are not

repaid within one year Current Liabilities: Amounts owed by the

business that are to be paid within one year.

Nik Nurul Aswani binti Nik Kamarudin (UiTM Perak Branch) 12

Examples:

Non-currentliabilities

Current Liabilities

• Long-term loan• Bank loan• Mortgage

• Account payables• Short-term loan• Accrued

expenses• Revenue received

in advance

Nik Nurul Aswani binti Nik Kamarudin (UiTM Perak Branch) 13

Asset Owner’s equity Liability

14

Nik Nurul Aswani binti Nik Kamarudin (UiTM Perak Branch)

Date Jan.

Transactions ASSETS = LIABILITIES + OWNERS’ EQUITY

Effects

1 Started business with RM35,000 cash.

+ Cash 35,000

= + Capital 35,000

Asset: Increase Equity:Increase

2 The business acquired bank loan worth RM50,000.

+ Bank50,000

= + Loan50,000

Asset:IncreaseLiability:Increase

4 The business paid the bank loan amounting to RM5,000 bycheque

- Bank5,000

= - Loan5,000

Asset:DecreaseLiability:Decrease

Nik Nurul Aswani binti Nik Kamarudin (UiTM Perak Branch) 15

Asset + Expense + Drawings = Capital + Income + Liability

Asset = Capital + Income – Expense – Drawings + Liability

Asset = Capital + [Income – Expense] – Drawings + Liability

Asset = [Capital + Profit/(Loss) – Drawings] + Liability

Asset = Owner’s equity + Liability

INCOME is increases in economic benefits during the accounting period in the form of inflows or enhancements of assets or decreases of liabilities that result in increases in equity, other than those relating to contributions from equity participants. Income encompasses both revenue and gains. Revenue arises in the course of the ordinary activities of an entity and is referred to by

a variety of different names including sales, fees, interest, dividends, royalties and rent. Gains represent other items that meet the definition of income and may, or may not,

arise in the course of the ordinary activities of an entity. E.g., gain on disposal of non-current assets.

Nik Nurul Aswani binti Nik Kamarudin (UiTM Perak Branch) 16

EXPENSES are decreases in economic benefits during the accounting period in the form of outflows or depletions of assets or incurrences of liabilities that result in decreases in equity, other than those relating to distributions to equity participants. Expenses encompasses losses as well as those expenses that arise in the course of the

ordinary activities of the entity. Expenses that arise in the course of the ordinary activities of the entity include, for example, cost of

sales, wages and depreciation. They usually take the form of an outflow or depletion of assets such as cash and cash equivalents, inventory, property, plant and equipment.

Losses represent other items that meet the definition of expenses and may, or may not, arise in the course of the ordinary activities of the entity. E.g., loss on disposal of non-current assets.

Nik Nurul Aswani binti Nik Kamarudin (UiTM Perak Branch) 17

Nik Nurul Aswani binti Nik Kamarudin (UiTM Perak Branch) 18

Date Jan.

Transactions A + EXP. + D = C + INC. + L Effects

Increase Decrease

5 The owner took RM2,000 cash from the business for personal use

- Cash 2,000

+ Drawings 2,000

AssetEquity

6 Paid water bills RM1,000 by cash

- Cash 1,000

+ Water Bills 1,000

= Expense Asset

7 Bought goods oncredit worthRM3,500

+ Purchase 3,500

= + Payables 3,500

ExpenseLiabilities

8 Sold products tocustomer on credit worth RM2,400

+ Receivables2,400

= + Sales2,400

AssetIncome

9 Received RM1,000cash fromreceivables

- Receivables 1,000+ Cash 1,000

= Asset Asset

Fatimah Abd Rauf, Amla Abu, Radziah Mahmud, FINANCIAL ACCOUNTING FOR NON-ACCOUNTING STUDENTS, 6th Edition, Mc Graw Hill, 2020, ISBN:978-967-0761-38-1.

Malaysia Accounting Standard Board (MASB), CONCEPTUAL FRAMEWORKS (2018)

UiTM Lecturer’s Notes

Nik Nurul Aswani binti Nik Kamarudin (UiTM Perak Branch) 19