Embed Size (px)

Citation preview

www.ajbms.org Asian Journal of Business and Management Sciences

ISSN: 2047-2528 Vol. 1 No. 9 [28-47]

©Society for Business Research Promotion | 28

Accounting and Control Systems Practiced By Small and Micro Enterprise Owners within the Cape Coast Metropolitan Area of Ghana

John Kwaning Mbroh Head, Dept of Accountancy Studies, Cape Coast Polytechnic Ghana, West Africa E-mail: [email protected] / [email protected] & Ben Ebo Attom Lecturer, Dept of Accountancy Studies Cape Coast Polytechnic Ghana, West Africa E-mail: [email protected]

ABSTRACT

Small and micro enterprises contribute significantly to socio-economic

development and growth in both developed and developing countries.

However, there are fundamental problems militating against the realization of

their roles to the benefit of economies, especially in a developing one like

Ghana. Business management know-how in the specific areas of accounting

and control systems have mainly lacked coupled with the current realization

that 12% of their owners lack basic education. This paper examines survey

results on these practices by two-hundred and seventeen business owners

within the CCMA of Ghana. Findings reveal that basic book-keeping practices

were not in operation in many of the enterprises with majority (52%) frequently

seeking external assistance in their business accounting. Also, the absence of

control systems has contributed significantly to their exposure to lapses,

perceived misappropriations and reported losses with the micro business

segment being the worse affected. Future research and policy directions in

respect of training and capacity development targeting specifically business

segment differences and needs have been recommended.

Keywords: Small and Micro Enterprise Owners (SMEOs); Small and Micro

Enterprises (SMEs); Cape Coast Metropolitan Area (CCMA); Accounting and Control Systems.

INTRODUCTION It is often said that the world has now become a global village. Currently, the way and manner individuals, enterprises and nations react to this assertion of globalization tells it all. Specifically with business enterprises, this era requires much more inputs of some sort to be able to establish, survive and grow in order to properly assess the concept of globalization. However, to merely survive as a business enterprise requires a rigorous application of accounting to every incident in a proper manner. This is due to the fact that, resources of business enterprises are often limited and their proper control in terms of allocation and performance measurement has become the order of the day. Small business enterprises (SMEs) have an important role to play in Ghana’s socio-economic development. The extent of contribution these business units can make towards the growth and development of Ghana is dependent on the level of success attained by their

www.ajbms.org Asian Journal of Business and Management Sciences

ISSN: 2047-2528 Vol. 1 No. 9 [28-47]

©Society for Business Research Promotion | 29

operations. Fact is that, underlying the success of a business enterprise are the establishment and application of controls by the owners or management in addition to the systematic record keeping of business transactions, which, at the end of the period, keeps the owner well-informed about the performance of the business. NEED FOR THE STUDY The need to look into the existing accounting and control systems practiced by small and micro enterprise owners (SMEOs) arose from the results of a reconnaissance survey that was carried out among randomly selected SMEOs. These owners had reported to have been making losses but are unable to substantiate with accounts or fact and figures, as the case must be. It is in view of this revelation that the study was conducted to ascertain the accounting and control systems practiced by SMEOs with the aim of finding the existence, strengths and weaknesses of such systems. OBJECTIVES OF THE STUDY The main objectives were:

- To identify different types of accounting records kept and the level of usage of such records to generate specific types of accounts as per their respective business classification;

- To ascertain various accounting controls practiced by the selected small and micro enterprise owners;

- To evaluate the adequacy of the accounts and control systems relative to the level of business enterprises and their operations;

- To offer ways and means by which to improve on existing or non-existing practices by way of recommendation; and

- To suggest areas of future policy and research direction in these respects. METHODOLOGY The study was conducted on SMEOs within the Cape Coast Metropolitan Area of Ghana. However, there is no reliable data on the number of SMEs in the metropolis. In view of this, the metropolitan area was divided into thirteen zones and this was only possible after an initial reconnaissance study had revealed their concentration of the defined business units. The final questionnaire was mainly administered and on few cases, used as a schedule for discussion with the respective business owners where illiteracy had permitted. Five research assistants went into the zones with the intention to question or interview any qualified entrepreneur who was available and willing to be questioned or interviewed. The differences in the business segments were initially ascertained. This is a purposive sampling where a minimum of 130 respondents were considered acceptable for the sample and consequently, the study’s conclusions. Out of 250 questionnaires sent out, 217 responded. For the purpose of this study, a business enterprise is considered small or micro if it satisfies any one of the following conditions:

- Employs less than 29 workers; - Has a total assets of less than GHS150,000 (or USD100,000); and - Has an annual turnover of between GHS15,000 and GHS300,000 (or USD10,000

and USD200,000). ASSUMPTIONS AND HYPOTHESES The following assumptions underlie the study, that:

- The samples of small and micro business enterprises are representative enough to enable the researcher arrive at the conclusions of the study;

- Most of the small and micro enterprise owners do not keep proper accounts and also do not practice adequate accounting controls;

www.ajbms.org Asian Journal of Business and Management Sciences

ISSN: 2047-2528 Vol. 1 No. 9 [28-47]

©Society for Business Research Promotion | 30

- The government of Ghana and other relevant institutions, bodies and/ or agencies have designed business management training programmes specifically for small and micro business owners, but have not reached all of them; and

- The existing accounting and control systems do not affect the operations of the selected business enterprises.

SMALL AND MICRO BUSINESS DEFINED There are several ways of defining a small or micro business. Regardless of their differences, all the definitions agree on the common views that small or micro businesses employ few persons and are characterized by a relatively small amount of capital and turnover. According to the International Labour Organisation (ILO, 1997), no single definition can capture all the dimensions of “micro”, “small”, “medium” or “large”. Nor can it expect to reflect the differences between firms, sectors or countries at different levels of development. They noted for instance, that, an annual turnover of less than UDS100,000 would probably define a micro business in the United States of America but could well include a medium-sized firm in other economies. The United States Committee for Economic Development for Small Businesses indicates that, “a small business will have at least two of the following characteristics: Managers are also owners; Owners supplied capital; Area of operation mainly local; and Small in size within the industry”. On his part, Oshagbemi (1985) states the main criteria used throughout the world to describe small businesses as including: Sales value; Number of employees; Financial strength; Relative size; Initial capital outlay; Comparison with its past standards; Independent ownership; and Type of industry. The UNCTAD (2000), defines a micro enterprise as “a business involving one to five persons (typical a sole trader). Its character would be such that its activities are simple enough to be managed directly on a person-to-person basis and the scale of the operations means it is unlikely to need or be able to afford to devote significant staff time to accounting. Its operations are likely to concern a single product, service or type of operations. Only basic accounting is needed to record turnover, control expenses and profitability, and if necessary, compute profits for tax purposes. It is unlikely to have extensive credit transactions”. It also defines a small enterprise as “a business employing 6 to 50 persons. Such a business would probably have several lines of activity and conceivably more than one physical location. It would probably need loan finance and have to report to lenders. Its payroll would potentially be quite large and relatively complex and it would need management information on turnover and costs analysed by product line. It would potentially do a substantial proportion of its business on credit. It would therefore need a more sophisticated accounting and control system, but probably without having to consider issues such as pensions, provisions, leases and financial instruments. It would probably need a full-time book-keeper to maintain records and information flow to management”. SMALL AND MICRO BUSINESS IN GHANA The nature of SBs in Ghana is that, they are often simply registered with the Metropolitan Assembly, the Internal Revenue Service and where applicable, the VAT Service. In addition, the well-established ones are also registered with the Registrar General’s Department. The owner or manager who often doubles as the financial manager is charged with the day-to-day management of cash. This function includes the handling of cash receipts in the manner of safe-keeping, depositing at the bank and control over disbursements. Others include investing idle cash and necessary planning to maintain safe cash levels at all times (Mbroh, 2011). A small business owner (SBO) is a person who establishes and manages a business to attain personal objectives and sees the business as an extension of his or her needs, goals and personality since growth might not be such person’s major objective (Boachie-Mensah

www.ajbms.org Asian Journal of Business and Management Sciences

ISSN: 2047-2528 Vol. 1 No. 9 [28-47]

©Society for Business Research Promotion | 31

and Marfo-Yiadom, 2005). An apex body established by Act of Parliament (Act 434 of 1981) with the tasks of promoting small scale industries is the National Board for Small Scale industries (NBSSI). In its categories of business units, it considers “small enterprises as those which have 29 or less employees and enterprises whose capital investment requirements do not exceed the cedi equivalent of USD100,000 (i.e. GHS150,000)”. On the other hand, enterprises employing up to 5 persons with an annual turnover of not less than GHS15,000 (i.e. equivalent of the USD10,000) has been adopted as defining a micro enterprise for the purpose of this study. Similarly, the NBSSI definition of a small enterprise has been adopted for the same purpose. ACCOUNTING SYSTEM AND CONTROLS FOR THE SMALL BUSINESS Hussein (1983) noted that, a good accounting system is not only judged by how well records are kept but by how well it is able to meet the information needs of both internal and external decision-makers. In his view, Clute (1980) maintained that it is common for qualified accountants to do a good job of keeping records up to date but they fail to provide information needed by decision-makers. For a businessperson, an accounting system should be capable of providing the following information:

1. Interim statements, quarterly or six-monthly that can provide information about

the progress of the business. Such statements need not be detailed, but capable of addressing the special needs of the business. Such documents can also be circulated, if necessary, among external users such as lenders.

2. Efficiency cash flow planning is very important for the small business. Fuller (1978) felt that an annual cash flow forecast, reviewed periodically, could indicate overall financial requirements. Such a statement can be prepared only with the help of a well-designated accounting system.

3. An accounting system, in addition to providing financial statements, must be

capable of generating other useful information in the form of reports. These include aged accounts receivable, aged accounts payable, stock and bank balances, etc.

4. In the case of manufacturing enterprises, cost records are very useful in estimating costs and determining prices. The accounting system for such enterprises must provide reliable data for cost estimation.

Regarding accounting control procedures for small and micro business enterprises, Sathyamoorthi (2001) observed that, it is important to have a system of control over all business activities, as a well-designed and properly implemented control system can ensure: Protection of resources against waste and fraud; Accuracy and reliability in accounting data; and Success in the evaluation of the performance of the business. In their view, Meigs, Johnson and Meigs (1977), accounting controls are measures that relate to protection of assets and to the reliability of accounting and financial reports. PRIOR STUDIES ON SMALL AND MICRO BUSINESSES In all forms of business units, financial management systems are of crucial importance. In fact, they are of significance to business success. Indeed, prior research has asserted that the quality of accounting information utilized within the SME sector has a positive relationship with an entity’s performance (Lybaert, 1998). Similarly, it has been emphasized that there is the need for financial information for small and micro business units due to the volatility normally associated with their situation such as unstable cash and profit positions, and reliance on short-term debt (McMahon and Holmes, 1991; and Dodge, Fullerton and Robbins, 1994). However, despite increasing research in accounting in the past decade little is known of its form and effectiveness within the small business sector (McChlery, Godfrey and Meechan, 2005). For instance, Mitchell, Reid and Smith (1999) and Marriott and Marriot (2002)

www.ajbms.org Asian Journal of Business and Management Sciences

ISSN: 2047-2528 Vol. 1 No. 9 [28-47]

©Society for Business Research Promotion | 32

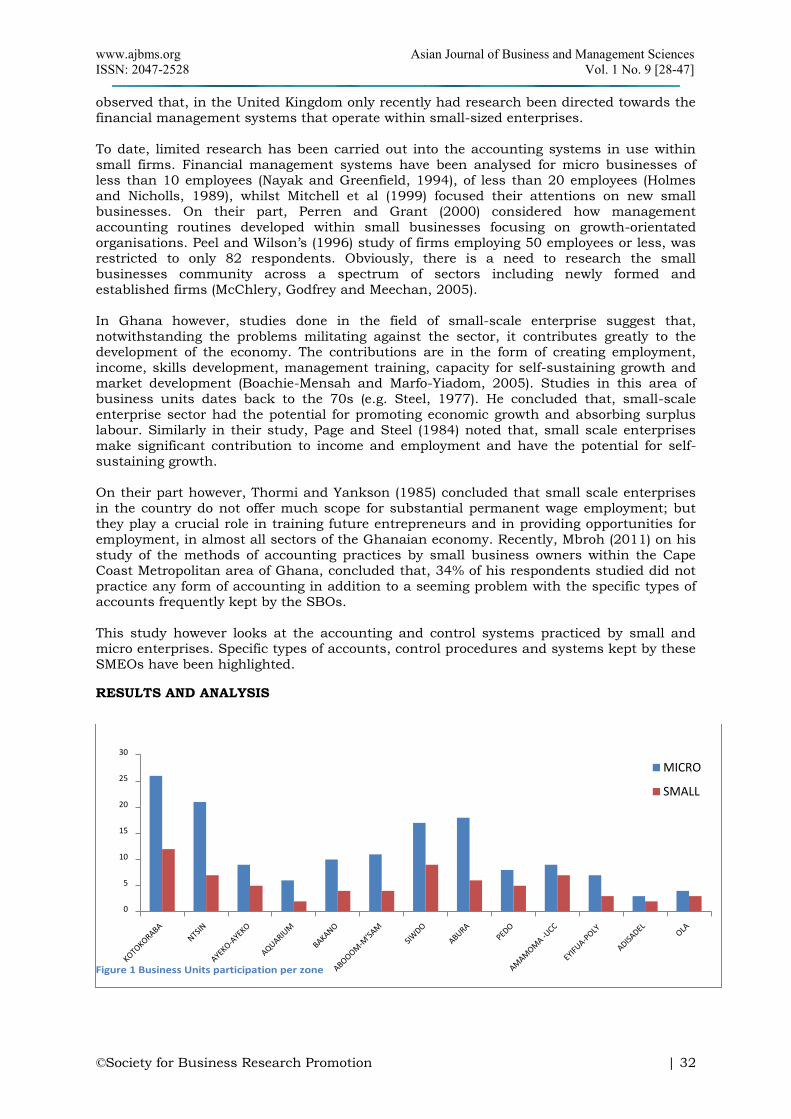

observed that, in the United Kingdom only recently had research been directed towards the financial management systems that operate within small-sized enterprises. To date, limited research has been carried out into the accounting systems in use within small firms. Financial management systems have been analysed for micro businesses of less than 10 employees (Nayak and Greenfield, 1994), of less than 20 employees (Holmes and Nicholls, 1989), whilst Mitchell et al (1999) focused their attentions on new small businesses. On their part, Perren and Grant (2000) considered how management accounting routines developed within small businesses focusing on growth-orientated organisations. Peel and Wilson’s (1996) study of firms employing 50 employees or less, was restricted to only 82 respondents. Obviously, there is a need to research the small businesses community across a spectrum of sectors including newly formed and established firms (McChlery, Godfrey and Meechan, 2005). In Ghana however, studies done in the field of small-scale enterprise suggest that, notwithstanding the problems militating against the sector, it contributes greatly to the development of the economy. The contributions are in the form of creating employment, income, skills development, management training, capacity for self-sustaining growth and market development (Boachie-Mensah and Marfo-Yiadom, 2005). Studies in this area of business units dates back to the 70s (e.g. Steel, 1977). He concluded that, small-scale enterprise sector had the potential for promoting economic growth and absorbing surplus labour. Similarly in their study, Page and Steel (1984) noted that, small scale enterprises make significant contribution to income and employment and have the potential for self-sustaining growth. On their part however, Thormi and Yankson (1985) concluded that small scale enterprises in the country do not offer much scope for substantial permanent wage employment; but they play a crucial role in training future entrepreneurs and in providing opportunities for employment, in almost all sectors of the Ghanaian economy. Recently, Mbroh (2011) on his study of the methods of accounting practices by small business owners within the Cape Coast Metropolitan area of Ghana, concluded that, 34% of his respondents studied did not practice any form of accounting in addition to a seeming problem with the specific types of accounts frequently kept by the SBOs. This study however looks at the accounting and control systems practiced by small and micro enterprises. Specific types of accounts, control procedures and systems kept by these SMEOs have been highlighted. RESULTS AND ANALYSIS

0

5

10

15

20

25

30

MICRO

SMALL

Figure 1 Business Units participation per zone

www.ajbms.org Asian Journal of Business and Management Sciences

ISSN: 2047-2528 Vol. 1 No. 9 [28-47]

©Society for Business Research Promotion | 33

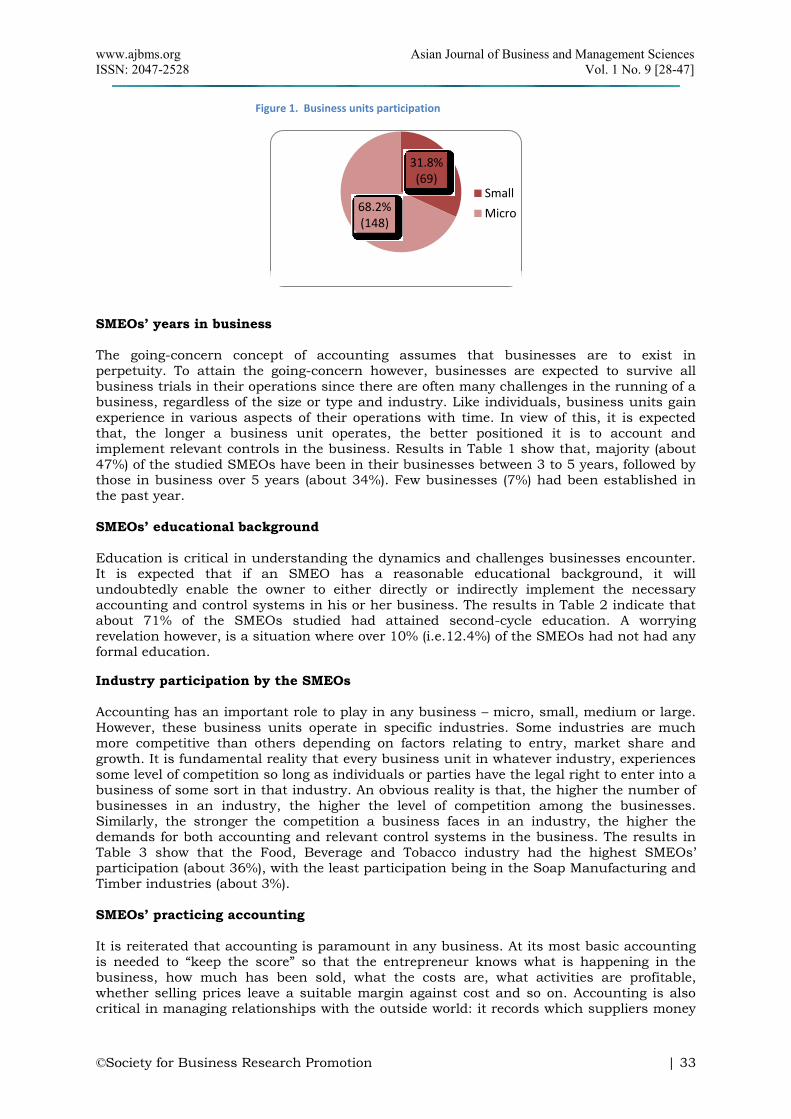

31.8% (69)

68.2% (148)

Small

Micro

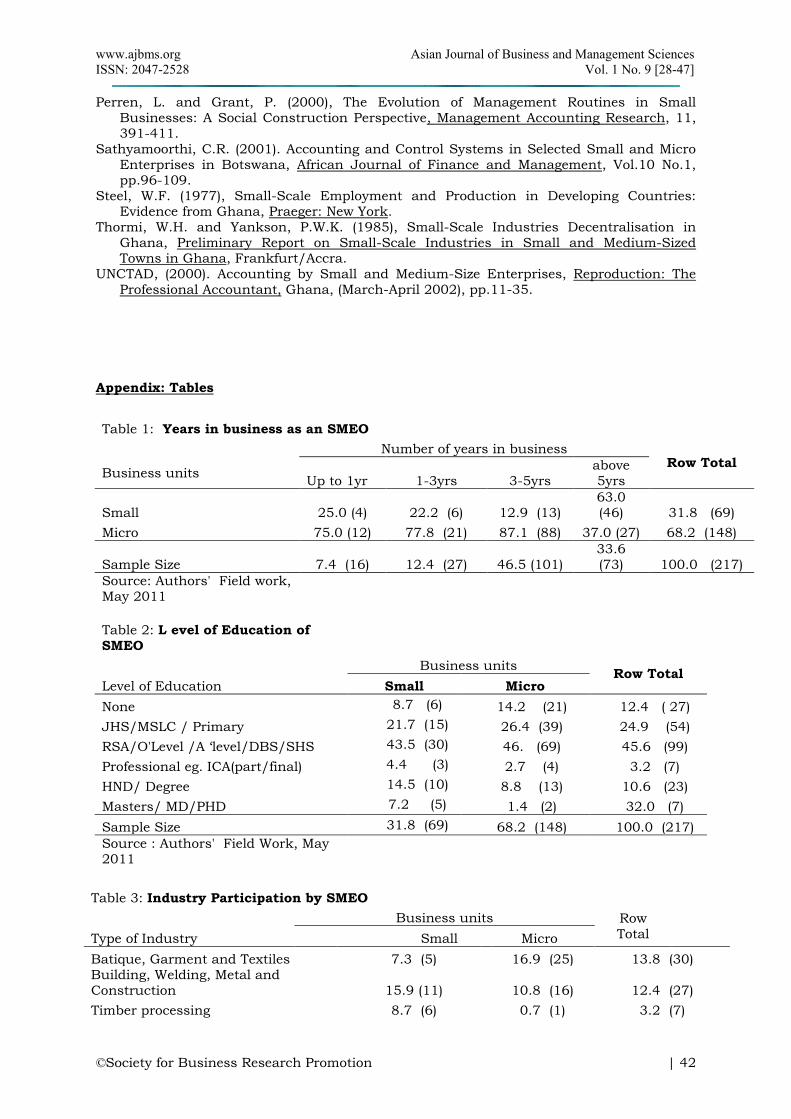

SMEOs’ years in business The going-concern concept of accounting assumes that businesses are to exist in perpetuity. To attain the going-concern however, businesses are expected to survive all business trials in their operations since there are often many challenges in the running of a business, regardless of the size or type and industry. Like individuals, business units gain experience in various aspects of their operations with time. In view of this, it is expected that, the longer a business unit operates, the better positioned it is to account and implement relevant controls in the business. Results in Table 1 show that, majority (about 47%) of the studied SMEOs have been in their businesses between 3 to 5 years, followed by those in business over 5 years (about 34%). Few businesses (7%) had been established in the past year. SMEOs’ educational background Education is critical in understanding the dynamics and challenges businesses encounter. It is expected that if an SMEO has a reasonable educational background, it will undoubtedly enable the owner to either directly or indirectly implement the necessary accounting and control systems in his or her business. The results in Table 2 indicate that about 71% of the SMEOs studied had attained second-cycle education. A worrying revelation however, is a situation where over 10% (i.e.12.4%) of the SMEOs had not had any formal education.

Industry participation by the SMEOs Accounting has an important role to play in any business – micro, small, medium or large. However, these business units operate in specific industries. Some industries are much more competitive than others depending on factors relating to entry, market share and growth. It is fundamental reality that every business unit in whatever industry, experiences some level of competition so long as individuals or parties have the legal right to enter into a business of some sort in that industry. An obvious reality is that, the higher the number of businesses in an industry, the higher the level of competition among the businesses. Similarly, the stronger the competition a business faces in an industry, the higher the demands for both accounting and relevant control systems in the business. The results in Table 3 show that the Food, Beverage and Tobacco industry had the highest SMEOs’ participation (about 36%), with the least participation being in the Soap Manufacturing and Timber industries (about 3%). SMEOs’ practicing accounting It is reiterated that accounting is paramount in any business. At its most basic accounting is needed to “keep the score” so that the entrepreneur knows what is happening in the business, how much has been sold, what the costs are, what activities are profitable, whether selling prices leave a suitable margin against cost and so on. Accounting is also critical in managing relationships with the outside world: it records which suppliers money

Figure 1. Business units participation

www.ajbms.org Asian Journal of Business and Management Sciences

ISSN: 2047-2528 Vol. 1 No. 9 [28-47]

©Society for Business Research Promotion | 34

is owed to (where credit has been received) and which customer money is due from (where credit is given). It also enables the entrepreneur to represent the business to outside interests, particularly potential lenders and also the tax authorities (UNCTAD, 2000). As a business aims at its going-concern and possibly, growth, it needs to seek further funding, investment and trading partners, particularly, where operations may take place across different types or levels of business units, it needs accounting as a justification – in the form of clear financial statements that are prepared on a basis that is understood across the world. In view of the aforesaid, UNCTAD (2000) observed the need for promoting transparency with adequate records-keeping early on in the business developmental phase of SMEs as paramount. Table 4 shows that 59% of the SMEOs practiced formal accounting, with the remainder ignoring the practice. In contrast, Sathyamoorthi (2001) observed that, only 30% of his respondents managed to prepare their own financial statements. Regarding those who did not practice any formal accounting (see Table 5), about 76% of the SMEOs maintained that they either lacked basic education or basic working knowledge in accounting. In support, UNCTAD (2000) concluded that, if entrepreneurs are to look after their own accounts, this presumes that they are already literate, and preferably numerate as well, which already excludes a large slice of the entrepreneur population. For an entrepreneur to be trained in accounting supposes that courses are available and that the entrepreneurs can afford to take time away from working to acquire the knowledge (or can be subsidized to do so). The remaining (24%), though would not disclose their knowledge or educational background, did not see the need for practicing accounting in their businesses. Coping strategies by SMEOs not practicing accounting On its part, Table 6 attempts to explain some of the strategies mainly adopted by SMEOs who do not undertake any form of formal accounting. The results show that, majority of such SMEOs (about 65% of their number) maintained that, they rather kept personal notes of transactions to ascertain their total purchases and sales for a given period. This situation, though convenient and may be a useful internal guide to an SMEO defeats the object of accounting which seeks to relate the business to the outside world for the desirable level of trade and business partners, further funding, investors and so on, which are necessary for growth from an existing business unit to another. In support, Nthejane (1997) reported that, “in Lesotho there are approximately 2000 enterprises, which employ six or people and these have mostly grown from the micro-business sector”. SMEOs’ understanding of key components of accounts A business unit may belong to a formal or an informal economy. For instance, entities, which keep no accounts and pay no taxes, are part of the informal economy and the reverse is the formal type. For a business unit to account under a formal economy in order to generate the necessary benefits, equally requires a standard or fundamental practices (though it has to be recognized that accounting needs of a simple business are simple, but as the business gets bigger, so does its needs for more sophisticated internal information and disclosures to the outside world – UNCTAD, 2000). Standard accounting practices require certain specific information disclosures, though their contents may differ from one business unit to another. It should be noted that standard accounting in business of a formal economy ends with information to the outside world in the form of financial statements. However, for uniformity in practice and reporting financial information, the International Accounting Standard one (IAS 1) sets out clearly, the content of financial statements in this order, that,….“a complete set of financial statements comprises:

a. a statement financial Position; b. an income statements; c. a statement of changes in equity showing either: (i) all changes in equity, or

www.ajbms.org Asian Journal of Business and Management Sciences

ISSN: 2047-2528 Vol. 1 No. 9 [28-47]

©Society for Business Research Promotion | 35

(ii) changes in equity other than those arising from transactions with equity holders acting in their capacity as equity holders;

d. a cash flow statement; and e. notes, comprising a summary of significant accounting policies and other

explanatory notes”. The above prescription is for both general purpose reporting and businesses in the formal economy. In addition, this requirement mainly targets public companies (in context of the Ghana Companies Code, Act 179 of 1963). However, some fundamental elements of the requirement equally apply to the SMEOs and their knowledge in these aspects was tested (see Table 7). It is worthy of note that, SMEs have been considered specifically in a proposed accounting compliance requirement under the caption “IFRS for SMEs”. This has been tailored to the peculiar accounting needs of the SMEs. These seemingly separate requirements notwithstanding, SMEOs’ maintaining their going-concern are also expected to bring into focus, their growth strategies from an existing business unit to a higher one. To be able to realise such an objective, both the performance at an existing business level and the growth business level require specific accounting – compliance with fundamental practices. In view of this, it is expected that, the SMEOs having this twin prospect should be well-abreast with what accounting entails. However, of those who stated to be practicing accounting (i.e. 128 SMEOs), a slight test of their understanding of the commonly known elements of financial statements showed that, about 41% had the understanding, with the majority (i.e.59%) having no knowledge at all about these elements of accounts. SMEOs’ budgetary control practices Budgets are simply, the financial plans that relate to an operation or an entity for a forthcoming period. If it relates to an entire business, then it is expected that, all aspects of the business’s operation are budgeted for. Once accepted by the respective manager, management or owner of the business, the budget becomes a form of control or a restrictive instrument on the firm’s operations. Budget may also only relate to a segment or an aspect of a business – cash, purchases, labour, overheads and so on. To a given business for instance, Marfo-Yiadom (2002) observed that, theoretically, a cash budget serves two purposes; first they alert the financial manager to future cash needs. Second the cash flow forecasts provide a standard, or budget, against which subsequent performance can be judged, since using the budget on expenditure for example, the business owner can readily compare actual cash expenditures to targeted values. In support, Choyal (1990) noted that, an integral aspect of financial management is planning with forecast and budget. Cash budget (also called cash forecast) is a technique to plan for and control the use of cash. Conventional cash budget identifies anticipated cash inflows, outflows and balances over a specified planning horizon. It is described as the heart of the financial management function. It protects the financial condition of the business by developing projected cash inflows and outflows for a given period. It also specifies the required action at various stages of the cash conversion cycle. Results in Table 9 indicate that only 10% of the SMEOs studied used budgeting as a form of control to their business operations, with almost 77% of them not in the use of budgeting. Book-keeping and recording of cash transactions by SMEOs Efficient financial managers dwell on the past and present in order to predict the future and for proper evaluation and comparison of financial activities. To achieve this aim, proper book-keeping remains integral. It is equally acknowledged that by their nature, the SMEOs’ relevant academic and accounting backgrounds are expected to influence the success or otherwise of this critical function. Table 8 shows that about 12% overall maintained adequate book-keeping on their own, 73% either used personal notes or jotters (21%) or sought external assistance (52%). However, in his study, Sathyamoorthi (2001) found 6% of his respondent enterprises had maintained all the required ledger accounts, with 34% seeking assistance from accounting firms.

www.ajbms.org Asian Journal of Business and Management Sciences

ISSN: 2047-2528 Vol. 1 No. 9 [28-47]

©Society for Business Research Promotion | 36

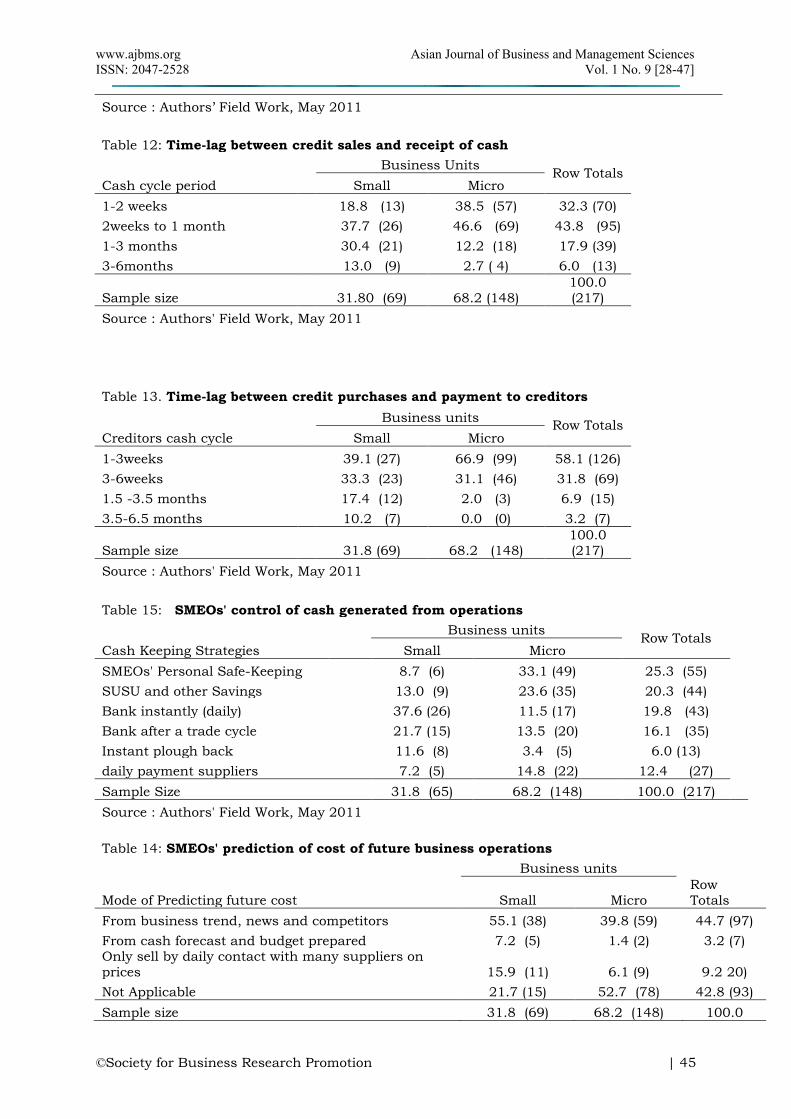

Cash is the basic unit needed to keep businesses running on a continuous basis; it is also the ultimate output expected to be realised by selling the products of a firm. That, cash shortages will disrupt the firm’s operations, while excessive cash will simply remain idle without contributing anything towards the firm’s profitability (Marfo-Yiadom, 2002). Cash transactions constitute a major part of business transactions in a small and micro business enterprise. It therefore seems sensible for the small business owner to exercise reasonable control over cash transactions so that cash is not misappropriated by employees. Moreover, by introducing a fair system for recording business cash transactions, the owner is able to exercise control on himself regarding withdrawals of funds for his person use which would otherwise have been available for business expansion (Sathyamoorthi, 2001). Commenting on the need for records on cash transactions, Kilvington (1976) maintained that it is pre-requisite of accounting for solvency that cash records are impeccable and that cash controls are proof against fraudulent manipulation (see also Gentry, 1988). The nature, frequency and sometimes volume of transactions handled by SMEOs and the importance of cash in business, point to the fact that cash transactions should be governed by a control system. Again Table 8 shows that on their own, 27% of the SMEOs had adequately accounted for cash transactions. Twenty-one percent however did not account for cash transaction with 52% seeking external assistance regarding their book-keeping. Accounting control practices by SMEOs According to Meigs, Johnson and Meigs (1977), accounting controls are measures that relate to the protection of assets and to the reliability of accounting and financial reports. For a small or micro business, accounting controls will involve the maintenance of adequate Cash Book (if possible with analysis), Bank Accounts (with policies on deposits and withdrawals), Petty Cash system, irregular or regular preparation of Bank Reconciliation statement, Credit Policies with creditors for Purchases and with customers on Sales, Stock-keeping policy, Fixed Asset register and Budgeting for the entire business. However, a simple question on the SMEOs’ understanding of the term accounting control revealed (see Table 10) that 57% of the SMEOs had no understanding of the term with 22% indicating that they understand and are already in use in their businesses. A more specific question rather revealed (see Table 11) that 26% understand the real accounting procedures SMEOs credit systems and policies It is rear for businesses to operate only on cash basis. In view of this, it is expected that the business owners think-through and adopt a suitable credit policy for both suppliers (regarding purchases) and with customers (in respect of sales). At a glance, the decision should be for a system that allows for suppliers credit period to be longer than that given to customers. In his view, Pandy (1991) recommended a twin object of cash management as the acceleration of cash inflows (collection from debtors) and a reasonable delay in cash outflows (payments to creditors). A sharp contrast of the results in Tables 12 and 13 paints a gloomy situation where majority of the SMEOs rather pay creditors earlier than they collect account receivables from customers (debtors). Cost prediction and cash receipt control system practices by SMEOs In real life businesses, cost predictions are normally done through budgets. Budgets are essential to every serious business because resources are limited and the allocation of which should be properly prioritised. However, the results in Table 14 show that only 3% of the SMEOs used budgeting to predict their future costs. This situation is in contrast with the results in Table 9. However, it appears that considering the nature of businesses and industries involved as well as the economic situation in Ghana coupled with the background of the SMEOs, the use of budgets specifically to predict future costs of operations may not be a realistic one. Majority (about 45%) rather followed business news and competitors in predicting their future costs. In addition, regardless of the profit levels of a business, persistent cash shortages may result in its liquidation. This means that cash control is very essential to the survival and

www.ajbms.org Asian Journal of Business and Management Sciences

ISSN: 2047-2528 Vol. 1 No. 9 [28-47]

©Society for Business Research Promotion | 37

growth of any business – micro, small, medium or large. In his view, Marfo-Yiadom (2002) observed that cash shortages will disrupt the firm’s operations, while excessive cash will simply remain idle without contributing anything towards the firm’s profitability. About 41% of the SMEOs were carelessly handling cash generated from their operation (see Table 15). Payment control system practices by SMEOs Ideally, all business payments are to be made according to a planned payment schedule or budget. If this is done, it is expected to properly synchronise the timing of cash flows to avoid either impromptu or excess payments on one side or cash crises. In support, Logli (1981) noted that one of the significant problems in the small business sector is how resources are managed. On their part, Bosa (1969); Levy (1993); Keasey and Watson (1994) were specific in attributing the root cause of the problems in this business sector to inadequate cash levels. However, results in Table 17 show that majority (54%) of the SMEOs studied did not bother to distinguish business payments from their personal or domestic ones. From Table 16, about 68% just made payments as and when the need arose or there was cash to pay, with about 7% who had only made payments according to a plan of payment (budget). Table 18 on its part shows that 69% used Cash as the only means of payment, 26% of them had as a policy maintained bank accounts and as a result made payments with Cheques and the remainder used either Letters of Credit or Bankers’ Drafts. A recall from Table 8 shows that SMEOs who on their own prepared the cash book were in the following proportions: Small (24); and Micro (11). However, Table 19 shows that about 54% and 18% of the small and micro business units respectively prepared bank reconciliation statements and the remainder did not. Similarly, the petty cash book under the imprest system had only been maintained by 67% and 27% of the small and micro business units respectively and the others did not. Credit purchases and credit sales by SMEOs It is a common practice in real life business that goods and services are either purchased or sold on credit basis. However this is expected to be handled very carefully in order not to either over-stretch liberties with suppliers or import the problems with bad debts. Credit purchases for instance requires a good system of record-keeping to identify at any given time the dates, quantity, quality, price, value and suppliers involved as well as suppliers payment dates. Fact is that a credit purchase does not preclude liability and payment responsibilities by the SMEO. In view of this, the necessary steps must be taken to ensure that the right thing is done from ordering to receipt or storage. Tables 20 and 22 show that 67% and 70% of the SMEOs were making credit purchases and credit sales respectively. Further, Table 21 indicates that irregular order frequency with respect to credit purchases were experienced by all SMEOs. This implies that in such circumstances the SMEOs may end up making impromptu purchases at the cost of quality and price. The design of official or specific order forms for a business is expected to serve as a control measure especially, with the appropriate authorizations and approvals. Overall, only about 24% of the credit purchases had been sanctioned by a well-documented order forms with about 36% of all orders (i.e. whether documented or not) carried out by employees. Regular ordering of fresh supplies formed about 5% of all credit purchases and inspection of fresh deliveries accounted for 48% overall. On its part, Table 23 shows that the use of tickler cards as a reminder of which customer accounts are due represented 56% of the SMEOs who offered credit sales. A good number of credit sales were offered to ‘valued’ or regular customers (80%) with about 36% of the SMEOs occasionally offering credit sales to irregular customers. The danger with the latter however is that there may be a high degree of bad debt as result. Overall, 56% of those selling on credit undertake daily tallying of cash collection from debtors with sales invoices. Accounting for stock, labour, fixed assets and liabilities by SMEOs Stock is often an integral and a major component of a firm’s working capital. To the SMEs, these are in the form of materials bought to be processed or for manufacture, finished

www.ajbms.org Asian Journal of Business and Management Sciences

ISSN: 2047-2528 Vol. 1 No. 9 [28-47]

©Society for Business Research Promotion | 38

goods for resale and component parts to be used as parts or to be assembled for a complete system. Control over stock should be of prime interest to the SMEO. Depending on the quantities, specific types and nature of stock items, they can easily be stolen, burnt, become obsolete, evaporated, result in stock-out and/or over-stocked. Sathyamoorthi (2001) observed that the first control measure to be introduced would be to maintain a detailed stock register with the following columns: Item code; Date of purchase; Quantity received with specifications; Items issued; and Balance at the end of a certain period. Such a stock register he cautioned must be handled by a responsible employee who should not be in any way connected with the settlement of accounts with the suppliers. He should develop a system for stocktaking that will ensure that all stock is systematically counted, preferably, by responsible employee or in the presence of the SMEO. Stock-taking is a critical control event to avert all manner of losses associated with stock-keeping. The results on stock control practices by the SMEOs strangely revealed that none of the studied SMEOs kept any formal or standard stock registers or records but mainly (67%) kept some sort of personal records on stock movements. The remaining (33%) only relied on physical stock count and supplier (purchase) invoices. The results on stock-taking practices specifically show that 81% of the SMEOs either used stock-taking regularly or otherwise as a means of placing orders for fresh supplies. The remaining 19% never bothered to take stock. Labour is human effort engaged in production, service or business. It involves both the physical and mental efforts in a business. They may be classified as either direct or indirect to a cost object. The nature of their existence in a business may be permanent or temporal as well as being either full-time or casual. Primarily, reward systems are tied to output or time and it is either the norm that they are paid salaries or wages. In a more dynamic business, control mechanisms exist to evaluate both the labour efforts expended and the associated reward. A realistic accounting procedure would be to use a wage-sheet, payroll or better-still, wage-book for all categories of employees, their status, rates of pay and the exact labour cost for the entire business for any given period, a specified job or department. Really discouraging is the hard-truth that none (0%) of the SMEOs had maintained acceptable wage records in addition to the amazing reality that all the businesses (100%) had paid wages only on cash basis. Fixed assets include Land and Buildings, Plant and Machinery, Furniture, Fixtures and Fittings, Motor Van and so on. They are acquired by satisfying the future benefit test of businesses. In order for a given firm’s accounting to be complete, proper records on this class of assets should be kept so as to ascertain their entry costs or book values, estimation of their expected useful years so that their replacements would be planned in-line with the firm’s going-concern concept. In his view, Sathyamoorthi (2001) suggested a suitable accounting system would require the maintenance of assets register for each type of asset and this should contain: Date of purchase of the asset; Description of the asset; Quantity in use; Leasehold or freehold; Cost price of the asset; Depreciation; Date of disposal; and Balance of asset left and its cost and book values. The study found that with the exception of their possession of acquisition documentations and in many instances the tenancy agreements (for those rented land and buildings and some cases Machinery types) no records of such nature were available in all the businesses. However, those employing the services of external parties in the preparation of their accounts had captured information on fixed assets in their statements of financial position (Balance Sheets). Liabilities are financial obligations on a given business. They include expenses outstanding at the end of a particular year, short, medium and long-term liabilities such as overdrafts, bank loans and loans from other financial institutions. In order to ascertain the actual position on a firm’s liabilities, it is expected that a liability register be properly drawn-up to always ascertain how much liability is outstanding at every given time. The study found that liabilities other than expenses outstanding were only incurred by SMEOs who had maintained bank accounts with acceptable banking practices. However with the exception of loan agreements no records on loans were kept. In addition, SMEOs who had any type of bank loans were those by virtue of their accounts been prepared by external parties (52% overall).

www.ajbms.org Asian Journal of Business and Management Sciences

ISSN: 2047-2528 Vol. 1 No. 9 [28-47]

©Society for Business Research Promotion | 39

SUMMARY OF FINDINGS

- Majority of SMEOs (47%) had been in business between 3 to 5 years and 7% had been established in the past year. A majority of 46% had up to second-cycle education. 12% had no formal education.

- 59% practiced formal accounting and the difference did not. 65% of those who did not practice accounting rather kept personal notes and jotters. Only 10% prepared and used budgets in their businesses. Book-keeping was undertaken by 12% of the SMEOs, 52% sought external assistance in keeping books of accounts and 21% overall kept personal jotters instead.

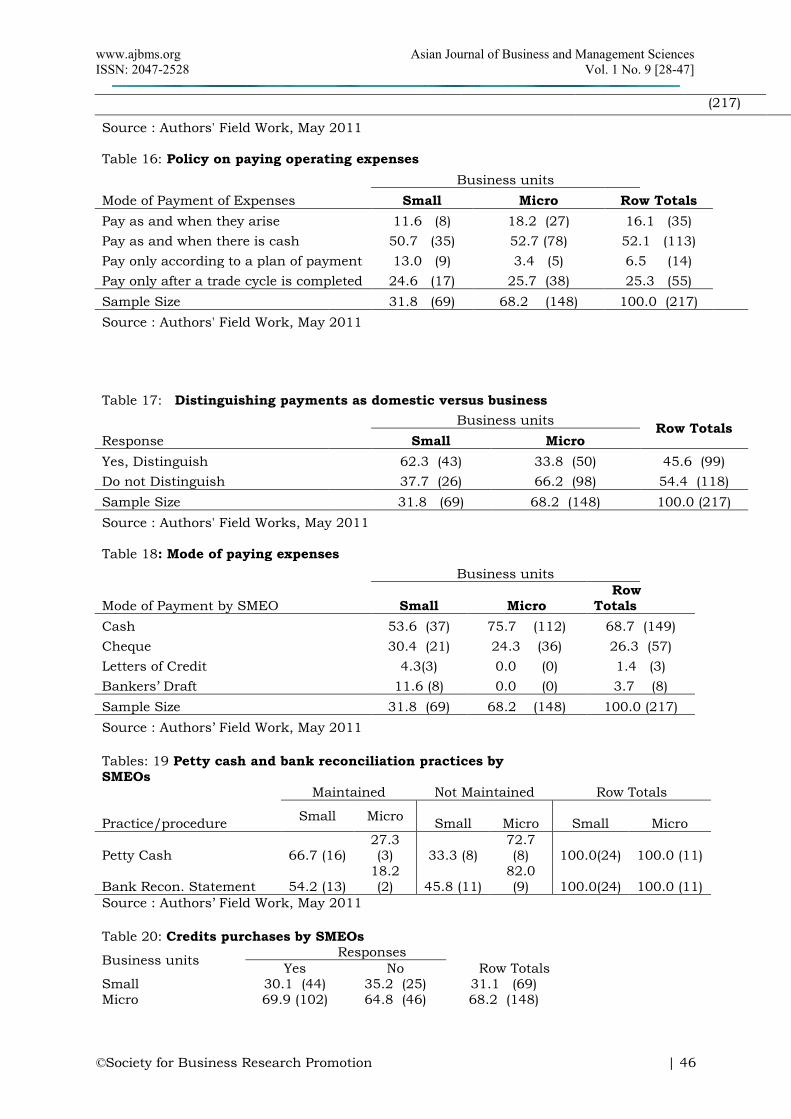

- 27% kept cash book on cash transactions themselves, 21% did not and 52% sought external help on their cash book. Control systems were neither understood nor practiced by 78%. Twenty-two percent had some control systems in use. 26% of those who practiced accounting had accounting procedures. Credit policies were an average very irregular as majority of SMEOs were paying creditors (3 weeks) earlier than they were collecting from debtors (1 month).

- Future cost predictions were mainly done determined by business news, trends and competitors’ pricing. Overall, only 3% used budget in this respect. Cash control practices were bad. 41% were careless in handling business cash, 54% did not differentiate between business and domestic payments, 68% paid as and when there was cash available, only 7% made payments according to plan, 69% used cash for all payments with only 26% overall maintaining business bank accounts. Of those who kept cashbook, only 54% small and 18% micro proportions prepared bank reconciliation statements. Similarly, petty cash books were only kept as 67% small and 27% micro proportions.

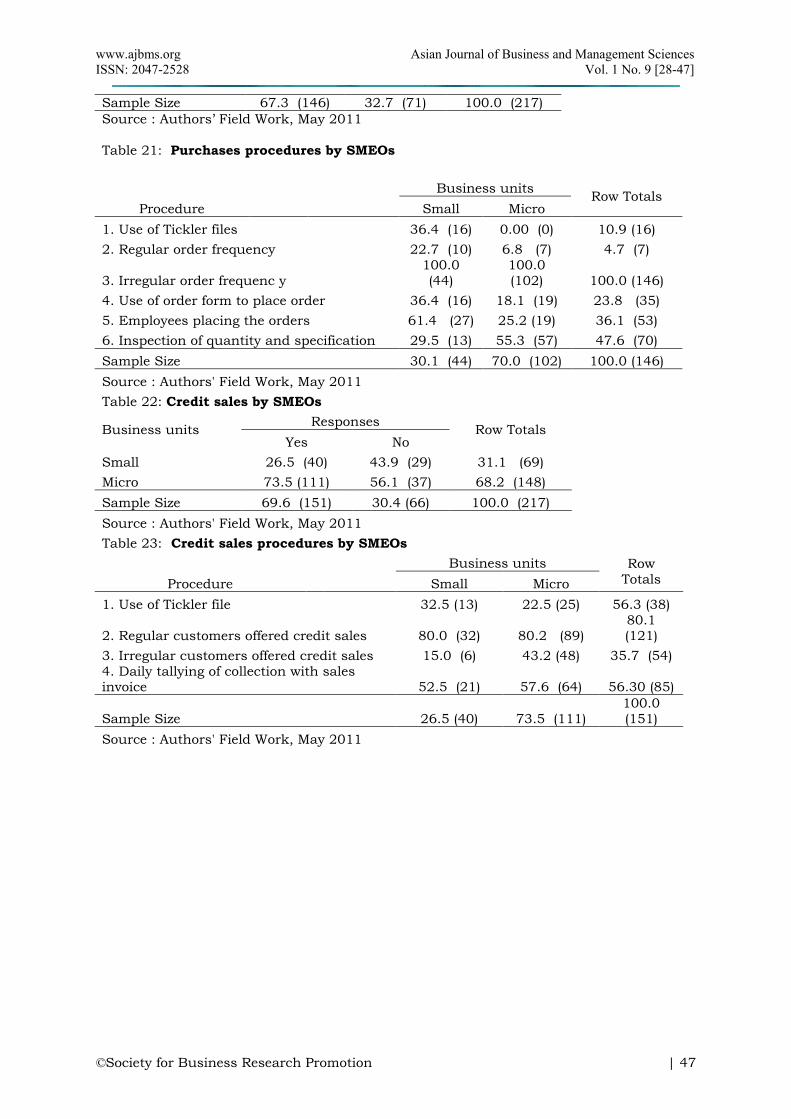

- Overall, credit purchases and credit sales were undertaken by 67% and 70% of the SMEOs respectively. However only 24% of credit purchases had proper documentation and authorization, employees orders represented 36% overall, irregular orders were 100% with the SMEOs, inspection of goods were undertaken by 48% and regular order of goods was 5%. Eighty percent of credit sales were offered to regular customers. 56% used tickler cards as a reminder of customer accounts falling due. 36% of them occasionally offered credit sales to new customers with 56% making daily tallying of cash collections with sales invoices.

- Stock control was bad since stock registers and records were not kept but instead, personal notes (67%) on stock movements, reliance on stock count (33%) were practiced. However stock-taking was undertaken by 81% overall and the others never bothered.

- 100% of the SMEOs paid wages in cash and none kept wage records. Fixed asset registers were not kept by all SMEOs however their acquisition documents were held and as result external parties had used them in the preparation of balance sheets.

- Liabilities had no records apart from (in some cases) prepared accounts and loan agreements kept. Those with commercial bank loans were SMEOs who had their accounts prepared externally.

CONCLUSIONS AND RECOMMENDATIONS The observations above depict a bleak state of affairs regarding how accounting and control systems are kept and exercised respectively by most SMEOs. It appears that these crucial ingredients of business management have been relegated to the very background. The results are somehow a reflection of the assertion by most SMEOs that they were making losses. This is perhaps as a direct result of the absence of important accounting controls in their businesses which consequently exposed their operations to lapses, misappropriations and general inefficiencies. They found that equally incalculable because a reasonable proportion of them (SMEOs) had not directly prepared or painstakingly studied the contents of those business accounts indirectly prepared. To the majority of SMEOs (especially those in the micro business sector) accounts preparation and perhaps book-keeping to a greater extent has to do with satisfying external partners - banks, taxation and so on. Some SMEOs even consider proper accounting might over-expose them to several dangers including imposition of licences, high interest rates by banks, new competitors and other market or

www.ajbms.org Asian Journal of Business and Management Sciences

ISSN: 2047-2528 Vol. 1 No. 9 [28-47]

©Society for Business Research Promotion | 40

state controls. In a nutshell, the perception that accounting is a tool of oppression is very rife amongst the SMEOs. Most of the SMEOs lack basic knowledge in business management and more specifically, basic working knowledge in accounting. Also discouraging is the fact that 12% of the respondents had not had any formal education and as a result were illiterates. The effects this however is the result where a reasonable number of the SMEOs are presently unable to keep simple books of prime entry and ledgers. In all these the specific roles expected of the tertiary institutions and bodies such as the Institute of Chartered Accountants, relevant NGOs have not been clearly spelt-out. Government of Ghana and its relevant bodies like the National Board for Small Scale Industries (NBSSI) and the Business Advisory Centres (BACs) have attempted to reach-out in training and capacity-development programmes to SMEOs but these have hardly translated into any meaningful output by the SMEOs who have already benefited. Even though these bodies have programmes for all categories of business units, their pace of outreach and business segment coverage have made majority of SMEOs lost hope in ever being attended to. Insignificant proportions have so far been captured and there is no urgency in reaching out to all in this business sector. In the absence of a laid-down time-table to this effect, few of the SMEOs have rather decided to be visiting these institutions and centres for some clarifications as and when the need arises. Reality is that the absence of relevant level of education has become a key inhibitor of these SMEOs accessing the necessary levels of training programmes as and when they require. It recommended that the Government of Ghana through it agencies like the NBSSI and the BAC segment their facilitations in a tailored manner to address certain specific and peculiar needs of the SMEOs. These may be in levels depending on the business category and the educational backgrounds of participants if carefully organized. To this end, a particular level (perhaps the maiden encounter) of training programmes might target important aspects of book-keeping which may expose SMEOs to Cash Book preparation, Purchase and Expense records, Debtors and Creditors records, Costing and Pricing and Stock Management. The next level may look at basic accounting controls, the preparation of ledger accounts, bank reconciliation statements and the business final accounts in that order. The Micro Finance and Small Loans Centre (MASLOC) may have to come in to partner with the business schools in the tertiary institutions in the metropolis to broaden access to these urgent and all-important training programmes especially in the subject area of small business accounting. On their own and with their bargaining power, the tertiary institutions may initiate specific research policies in this direction aimed at championing the capacity-building drive with these SMEOs. The present situation is that an SMEO’s initiative may be excellent, the zeal to succeed - very visible, but the attributes to success are woefully non-existent. On their own, the SMEOs are much more expected as part of their drives for success, form groups in order to discuss their challenges and short-comings so as to seek ways by which they can overcome and improve them for their desired growth. Future policy direction may consider prioritizing general growth challenges facing these business sectors on the part of the government by initiating agreements aimed at further enhancing participation in SMEs by corporate bodies especially the banks and other financial institutions, NGOs and academic institutions. For instance, research grants to tertiary institutions may consider inputs in the area of SMEs. Future research direction may consider the gender differences in these respects as well as the extent of exposure suffered by enterprises seeking external assistance in the area of accounts preparation compared to those undertaking these internally. REFERENCES Boachie-Mensah, F.O. and Marfo-Yiadom, E.(2005). Entrepreneurship and Small Business

Management, Ghana Universities Press, Accra, p.2 Bosa, G. (1969). The Financing of Small Enterprises in Uganda, Oxford University Press:

Nairobi, Kenya.

www.ajbms.org Asian Journal of Business and Management Sciences

ISSN: 2047-2528 Vol. 1 No. 9 [28-47]

©Society for Business Research Promotion | 41

Choyal, B.R. (1990). Cash Management in Public Enterprises. Clute, R.C. and Gitman, G.B. (1980). A Factor Analytic Study of the Causes of Small

Business Failure, Journal of Small Business Management, USA. Dodge, H.R., Fullerton, S. and Robbins, J.E. (1994), Stage of the Organisation Life Cycle

and competition as Mediators of Problem Perception for Smaller Businesses, Strategic Management Journal, 15, pp121-134.

Eyiah, A. (2001). An Integrated Approach to Financing Small Contractors in Developing Countries: A Conceptual Model, Construction Management Journal, Vol.19, pp.511-518.

Fuller, S. (1978). Just Say No to Wall Street, Harvard business Review Gentry, J.A. (1988). State of the Art Short-Run Financial Management, Financial

Management (Summer), p.43 Holmes, S. and Nicholls, D. (1989), Modeling the Accounting Information Requirement of

Small Businesses, Accounting and Business Research, 19 (74) 143-150. Hussein, M.E.I.M. (1983). Accounting and Control Systems for Small Business, Touché

Ross Foundation. International Labour Organisation (ILO, 1997), General Conditions to Stimulate Job

Creation in Small and Medium-Size Enterprises, Report of an International Labour Organisation conference, 85th session, Geneva.

Keasey, K. and Watson, R. (1994). The Bank Financing of Small Firms in the UK: Issues and Evidence, Small Business Economics,Vol.6, pp.349-62.

Kilvington, K.W.(1976). Accounting for Solvency, Financial Management (September), p.303 Levy, B. (1993). Obstacles to Develop Small and Medium Sized Enterprises: an Empirical

Assessment, World Bank Economic Review, Vol. 7, No 1, pp 65 – 83. Logli, P. (1981). New Support for Small and Medium-Sized Enterprise in Developing

Counties, The Courier, No. 65, pp.96-98 Lybaert, N. (1998), The Information use in an SME: Its Importance and some Elements of

Influence, Small Business Economics, 10(2), 171-191. Marfo-Yiadom, E.(2002). A Survey of Cash Management Practices of Selected Firms in

Accra-Tema Metropolitan area of Ghana, The Oguaa Journal of Social Studies, Vol.3,(June), pp.165-182.

Marriot, N. and Marriott, P. (2000), Professional Accountants and the Development of a Management Accounting Service for the Small Firm: Barriers and Possibilities, Management Accounting Research, 11, 475-492.

Mbroh, J.K. (2011), Methods of Accounting Practices by Small Business Owners in the Cape Coast Metropolitan Area of Ghana, Journal of Polytechnics in Ghana, Vol.5, No.1, pp-129-151.

McChlery, S., Godfrey, A.D. and Meechan, L.(2005), Barriers and Catalysts to sound Financial management Systems in Small-Sized Enterprises, The Journal of Applied Accounting Research, Vol.7(iii), pp1-26.

McMahon, R.G.P., and Holmes, S. (1991), Small Business Financial Management Practices in North America: A Literature Review, Journal of small Business Management, (April), pp.19-29.

Meigs, et al (1977). Accounting, The Basis for Business Decisions, McGraw Hill Limited. Mitchell, F., Reid, G. and Smith, J. (1999), Information System Development in the Small

Firm, CIMA Research Foundation. Nayak, A., and Greenfield, S. (1994), The use of Management Accounting Information for

Micro Business. In Hughes, A. and Storey, D. (eds), Finance and the Small Firm. Routledge, London.

Nthejane, P. (1997). The Process of Policy formulation in Lesotho, In Franz, J. Oesterdiekoff, P. (eds). SME Policies and Policy Formulation in SADC Countries, Botswana: Friedrich Ebert Stiftung.

Oshagbemi, T.A (1985). “Small Business Clinic”, Training Committee Report on Small Business Management in Nigeria.

Page, J.M. Jr. and Steel, W.F. (1984), Small Enterprises Development: Economic Issues from African Experience, Technical Paper No.26, World Bank, Washington, D.C., USA.

Peel, M. and Wilson, N. (1996), Working Capital and Financial Management Practices in the Small Firm Sector, International Small Business Journal, January-March.

www.ajbms.org Asian Journal of Business and Management Sciences

ISSN: 2047-2528 Vol. 1 No. 9 [28-47]

©Society for Business Research Promotion | 42

Perren, L. and Grant, P. (2000), The Evolution of Management Routines in Small Businesses: A Social Construction Perspective, Management Accounting Research, 11, 391-411.

Sathyamoorthi, C.R. (2001). Accounting and Control Systems in Selected Small and Micro Enterprises in Botswana, African Journal of Finance and Management, Vol.10 No.1, pp.96-109.

Steel, W.F. (1977), Small-Scale Employment and Production in Developing Countries: Evidence from Ghana, Praeger: New York.

Thormi, W.H. and Yankson, P.W.K. (1985), Small-Scale Industries Decentralisation in Ghana, Preliminary Report on Small-Scale Industries in Small and Medium-Sized Towns in Ghana, Frankfurt/Accra.

UNCTAD, (2000). Accounting by Small and Medium-Size Enterprises, Reproduction: The Professional Accountant, Ghana, (March-April 2002), pp.11-35.

Appendix: Tables

Table 1: Years in business as an SMEO

Number of years in business

Row Total Business units

Up to 1yr 1-3yrs 3-5yrs above 5yrs

Small 25.0 (4) 22.2 (6) 12.9 (13) 63.0 (46) 31.8 (69)

Micro 75.0 (12) 77.8 (21) 87.1 (88) 37.0 (27) 68.2 (148)

Sample Size 7.4 (16) 12.4 (27) 46.5 (101) 33.6 (73) 100.0 (217)

Source: Authors' Field work, May 2011

Table 2: L evel of Education of SMEO

Business units

Row Total Level of Education Small Micro

None 8.7 (6) 14.2 (21) 12.4 ( 27) JHS/MSLC / Primary 21.7 (15) 26.4 (39) 24.9 (54) RSA/O'Level /A ‘level/DBS/SHS 43.5 (30) 46. (69) 45.6 (99) Professional eg. ICA(part/final) 4.4 (3) 2.7 (4) 3.2 (7) HND/ Degree 14.5 (10) 8.8 (13) 10.6 (23) Masters/ MD/PHD 7.2 (5) 1.4 (2) 32.0 (7) Sample Size 31.8 (69) 68.2 (148) 100.0 (217)

Source : Authors' Field Work, May 2011

Table 3: Industry Participation by SMEO

Business units Row

Total Type of Industry Small Micro

Batique, Garment and Textiles 7.3 (5) 16.9 (25) 13.8 (30) Building, Welding, Metal and

Construction 15.9 (11) 10.8 (16) 12.4 (27) Timber processing 8.7 (6) 0.7 (1) 3.2 (7)

www.ajbms.org Asian Journal of Business and Management Sciences

ISSN: 2047-2528 Vol. 1 No. 9 [28-47]

©Society for Business Research Promotion | 43

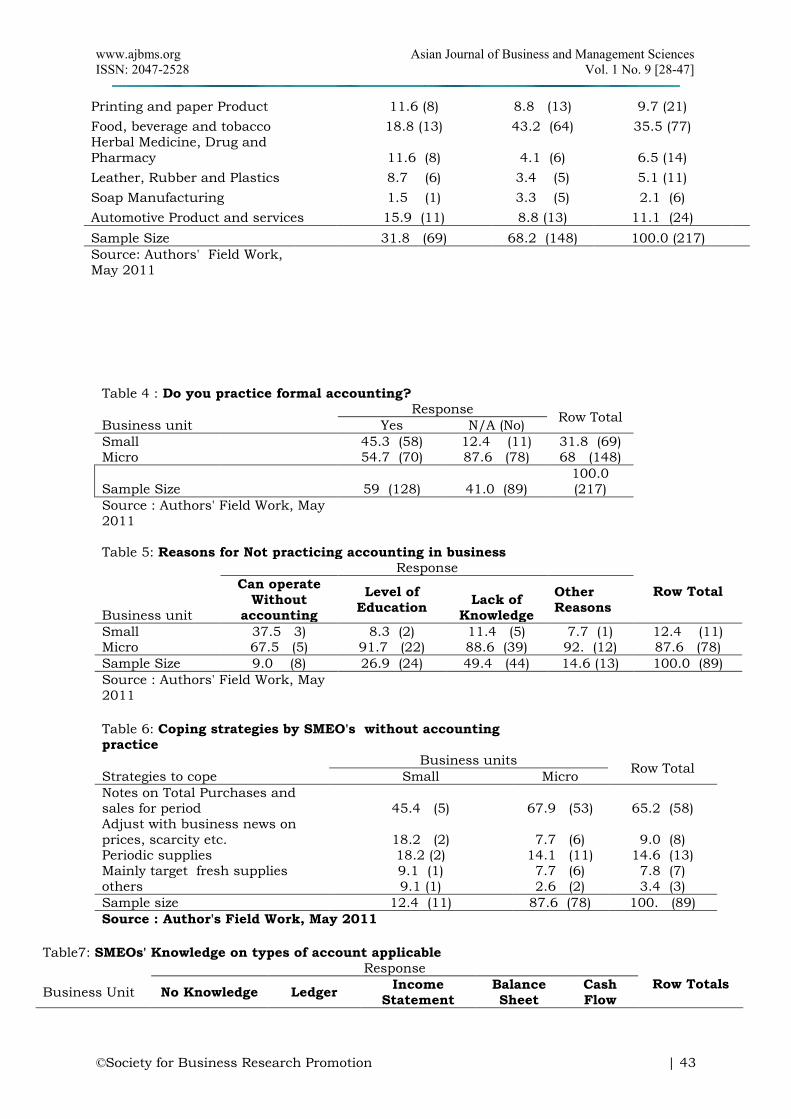

Printing and paper Product 11.6 (8) 8.8 (13) 9.7 (21) Food, beverage and tobacco 18.8 (13) 43.2 (64) 35.5 (77) Herbal Medicine, Drug and

Pharmacy 11.6 (8) 4.1 (6) 6.5 (14) Leather, Rubber and Plastics 8.7 (6) 3.4 (5) 5.1 (11) Soap Manufacturing 1.5 (1) 3.3 (5) 2.1 (6) Automotive Product and services 15.9 (11) 8.8 (13) 11.1 (24) Sample Size 31.8 (69) 68.2 (148) 100.0 (217)

Source: Authors' Field Work, May 2011

Table 4 : Do you practice formal accounting?

Response

Row Total Business unit Yes N/A (No)

Small 45.3 (58) 12.4 (11) 31.8 (69) Micro 54.7 (70) 87.6 (78) 68 (148)

Sample Size 59 (128) 41.0 (89) 100.0 (217)

Source : Authors' Field Work, May 2011

Table 5: Reasons for Not practicing accounting in business

Response

Row Total

Business unit

Can operate Without

accounting

Level of Education

Lack of Knowledge

Other Reasons

Small 37.5 3) 8.3 (2) 11.4 (5) 7.7 (1) 12.4 (11) Micro 67.5 (5) 91.7 (22) 88.6 (39) 92. (12) 87.6 (78)

Sample Size 9.0 (8) 26.9 (24) 49.4 (44) 14.6 (13) 100.0 (89)

Source : Authors' Field Work, May 2011

Table 6: Coping strategies by SMEO's without accounting practice

Business units Row Total

Strategies to cope Small Micro

Notes on Total Purchases and sales for period 45.4 (5) 67.9 (53) 65.2 (58) Adjust with business news on prices, scarcity etc. 18.2 (2) 7.7 (6) 9.0 (8) Periodic supplies 18.2 (2) 14.1 (11) 14.6 (13) Mainly target fresh supplies 9.1 (1) 7.7 (6) 7.8 (7) others 9.1 (1) 2.6 (2) 3.4 (3)

Sample size 12.4 (11) 87.6 (78) 100. (89)

Source : Author's Field Work, May 2011

Table7: SMEOs' Knowledge on types of account applicable

Response

Row Totals Business Unit No Knowledge Ledger

Income Statement

Balance Sheet

Cash Flow

www.ajbms.org Asian Journal of Business and Management Sciences

ISSN: 2047-2528 Vol. 1 No. 9 [28-47]

©Society for Business Research Promotion | 44

Small 44.7 (34) 59.3 (16) 27.8 (5) 66.7 (2) 25.0(1) 45.3 (58) Micro 55.3 (42) 40.7 (11) 72.2 (13) 33.3 (1) 75.0 (3) 54.7 (70)

Sample Size 59.4 (76) 21.10 (27) 14.10 (18) 2.3 (3) 3.1 (4) 100.0 (128)

Source : Authors’ Field Work, May 2011

Table 9: The use of Budgeting in Business Operations

Response

Business units Not at all

All the time

Occasionally Row Totals

Small 26.5 (44) 59.1 (13) 41.4 (12) 31.8 (69)

Micro 73.5 (122) 40.9 (9) 58.6 (17) 68.2 (148)

Sample Size 76.5 (166) 10.1 (22) 13.4 (29) 100.0 (217)

Source : Authors' Field Work, May 2011

Table 8: System of Book-Keeping Practiced

Business units

Row Totals System in Practice (in place) Small Micro

Get External Assistance 53.4 (31) 50.0 (35) 51.5 (66) Only Cash Book maintained 12.1 (7) 8.6 (6) 10.2 (13) Cash book, Day books, journals, asset

register 22.4 (13) 2.8 (2) 11.7 (15) Only ledger account maintained 6.9 (4) 4.3 (3) 5.5 (7) Only Personal jotter/ notes 5.2 (3) 34.3 (24) 21.1 (27) Sample Size 45.3 (58) 54.7 (70) 100.0 (128)

Source : Authors' Field Work, May 2011

Table 10: Knowledge of Accounting Controls

Response

Row Totals Business Units

Understand but not

practiced

Do not understand

In practice

Small 47.8 (22) 14.5 (18) 61.7 (29) 31.8 (69)

Micro 52.2 (24) 85.5 (106) 38.3 (18) 68.2 (148)

Sample Size 21.2 (46) 57.1 (124) 21.7 (47) 100.0 (217)

Source : Authors' Field Work, May 2011 Table 11: Indicate forms of control procedures you understand

Response

Row Totals Business units

Supervision Command Structure

Keeping cash book,

BRS, Budgeting, petty cash,

credit policies

Small 17.8 (24) 68.0 (17) 49.1 (28) 31.8 (69)

Micro 82.2 (111) 32.0 (8) 50.9 (29) 68.2 (148)

Sample size 62.2 (135) 11.5 (25) 26.3 (57) 100.0 (217)

www.ajbms.org Asian Journal of Business and Management Sciences

ISSN: 2047-2528 Vol. 1 No. 9 [28-47]

©Society for Business Research Promotion | 45

Source : Authors’ Field Work, May 2011

Table 12: Time-lag between credit sales and receipt of cash

Business Units

Row Totals Cash cycle period Small Micro

1-2 weeks

18.8 (13) 38.5 (57) 32.3 (70)

2weeks to 1 month

37.7 (26) 46.6 (69) 43.8 (95)

1-3 months

30.4 (21) 12.2 (18) 17.9 (39)

3-6months

13.0 (9) 2.7 ( 4) 6.0 (13)

Sample size 31.80 (69) 68.2 (148) 100.0 (217)

Source : Authors' Field Work, May 2011 Table 13. Time-lag between credit purchases and payment to creditors

Business units

Row Totals Creditors cash cycle Small Micro

1-3weeks

39.1 (27) 66.9 (99) 58.1 (126)

3-6weeks

33.3 (23) 31.1 (46) 31.8 (69)

1.5 -3.5 months

17.4 (12) 2.0 (3) 6.9 (15)

3.5-6.5 months

10.2 (7) 0.0 (0) 3.2 (7)

Sample size 31.8 (69) 68.2 (148) 100.0 (217)

Source : Authors' Field Work, May 2011

Table 15: SMEOs' control of cash generated from operations

Business units

Row Totals Cash Keeping Strategies Small Micro SMEOs' Personal Safe-Keeping 8.7 (6) 33.1 (49) 25.3 (55)

SUSU and other Savings 13.0 (9) 23.6 (35) 20.3 (44) Bank instantly (daily) 37.6 (26) 11.5 (17) 19.8 (43) Bank after a trade cycle 21.7 (15) 13.5 (20) 16.1 (35) Instant plough back 11.6 (8) 3.4 (5) 6.0 (13) daily payment suppliers 7.2 (5) 14.8 (22) 12.4 (27) Sample Size 31.8 (65) 68.2 (148) 100.0 (217) Source : Authors' Field Work, May 2011

Table 14: SMEOs' prediction of cost of future business operations

Business units

Mode of Predicting future cost Small Micro Row Totals

From business trend, news and competitors 55.1 (38) 39.8 (59) 44.7 (97)

From cash forecast and budget prepared 7.2 (5) 1.4 (2) 3.2 (7) Only sell by daily contact with many suppliers on prices 15.9 (11) 6.1 (9) 9.2 20)

Not Applicable 21.7 (15) 52.7 (78) 42.8 (93)

Sample size 31.8 (69) 68.2 (148) 100.0

www.ajbms.org Asian Journal of Business and Management Sciences

ISSN: 2047-2528 Vol. 1 No. 9 [28-47]

©Society for Business Research Promotion | 46

(217)

Source : Authors' Field Work, May 2011 Table 16: Policy on paying operating expenses

Business units

Mode of Payment of Expenses Small Micro Row Totals Pay as and when they arise 11.6 (8) 18.2 (27) 16.1 (35) Pay as and when there is cash 50.7 (35) 52.7 (78) 52.1 (113) Pay only according to a plan of payment 13.0 (9) 3.4 (5) 6.5 (14) Pay only after a trade cycle is completed 24.6 (17) 25.7 (38) 25.3 (55) Sample Size 31.8 (69) 68.2 (148) 100.0 (217) Source : Authors' Field Work, May 2011

Table 17: Distinguishing payments as domestic versus business

Business units

Row Totals Response Small Micro

Yes, Distinguish

62.3 (43) 33.8 (50) 45.6 (99) Do not Distinguish

37.7 (26) 66.2 (98) 54.4 (118)

Sample Size 31.8 (69) 68.2 (148) 100.0 (217) Source : Authors' Field Works, May 2011

Table 18: Mode of paying expenses Business units

Mode of Payment by SMEO Small Micro Row Totals

Cash 53.6 (37) 75.7 (112) 68.7 (149) Cheque 30.4 (21) 24.3 (36) 26.3 (57) Letters of Credit 4.3(3) 0.0 (0) 1.4 (3) Bankers’ Draft 11.6 (8) 0.0 (0) 3.7 (8) Sample Size 31.8 (69) 68.2 (148) 100.0 (217) Source : Authors’ Field Work, May 2011

Tables: 19 Petty cash and bank reconciliation practices by SMEOs

Practice/procedure

Maintained Not Maintained Row Totals

Small Micro Small Micro Small Micro

Petty Cash 66.7 (16) 27.3 (3) 33.3 (8)

72.7 (8)

100.0(24) 100.0 (11)

Bank Recon. Statement 54.2 (13) 18.2 (2) 45.8 (11)

82.0 (9) 100.0(24) 100.0 (11)

Source : Authors’ Field Work, May 2011

Table 20: Credits purchases by SMEOs

Business units Responses

Yes No Row Totals

Small 30.1 (44) 35.2 (25) 31.1 (69) Micro 69.9 (102) 64.8 (46) 68.2 (148)

www.ajbms.org Asian Journal of Business and Management Sciences

ISSN: 2047-2528 Vol. 1 No. 9 [28-47]

©Society for Business Research Promotion | 47

Sample Size 67.3 (146) 32.7 (71) 100.0 (217)

Source : Authors’ Field Work, May 2011 Table 21: Purchases procedures by SMEOs

Procedure Business units

Row Totals Small Micro

1. Use of Tickler files 36.4 (16) 0.00 (0) 10.9 (16)

2. Regular order frequency 22.7 (10) 6.8 (7) 4.7 (7)

3. Irregular order frequenc y 100.0 (44)

100.0 (102) 100.0 (146)

4. Use of order form to place order 36.4 (16) 18.1 (19) 23.8 (35)

5. Employees placing the orders 61.4 (27) 25.2 (19) 36.1 (53)

6. Inspection of quantity and specification 29.5 (13) 55.3 (57) 47.6 (70)

Sample Size 30.1 (44) 70.0 (102) 100.0 (146)

Source : Authors' Field Work, May 2011 Table 22: Credit sales by SMEOs

Business units Responses

Row Totals Yes No

Small 26.5 (40) 43.9 (29) 31.1 (69)

Micro 73.5 (111) 56.1 (37) 68.2 (148)

Sample Size 69.6 (151) 30.4 (66) 100.0 (217)

Source : Authors' Field Work, May 2011

Table 23: Credit sales procedures by SMEOs

Procedure Business units Row

Totals Small Micro

1. Use of Tickler file 32.5 (13) 22.5 (25) 56.3 (38)

2. Regular customers offered credit sales 80.0 (32) 80.2 (89) 80.1 (121)

3. Irregular customers offered credit sales 15.0 (6) 43.2 (48) 35.7 (54) 4. Daily tallying of collection with sales invoice 52.5 (21) 57.6 (64) 56.30 (85)

Sample Size 26.5 (40) 73.5 (111) 100.0 (151)

Source : Authors' Field Work, May 2011