Embed Size (px)

Citation preview

ACCOUNT OFFICER’SBASIC TRAINING

Procedures for Filling up the Debt Procedures for Filling up the Debt Capacity AnalysisCapacity Analysis

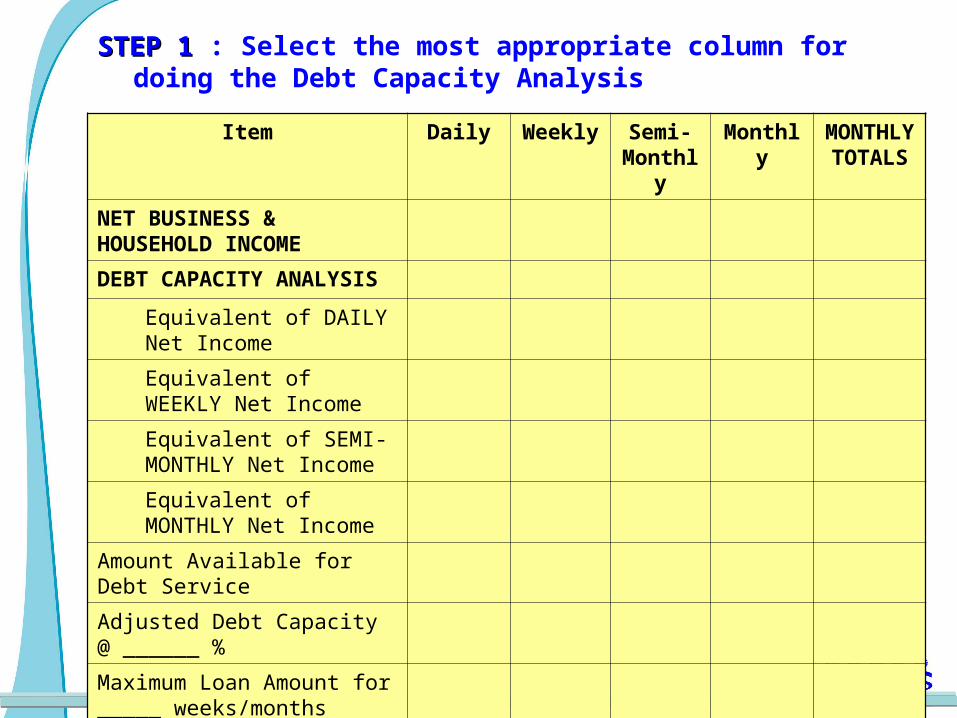

STEP 1STEP 1 : Select the most appropriate column for doing the Debt Capacity Analysis

Item Daily Weekly Semi-Monthly

Monthly MONTHLY TOTALS

NET BUSINESS & HOUSEHOLD INCOME

DEBT CAPACITY ANALYSIS

Equivalent of DAILY Net Income

Equivalent of WEEKLY Net Income

Equivalent of SEMI-MONTHLY Net Income

Equivalent of MONTHLY Net Income

Amount Available for Debt Service

Adjusted Debt Capacity @ ______ %

Maximum Loan Amount for _____ weeks/months

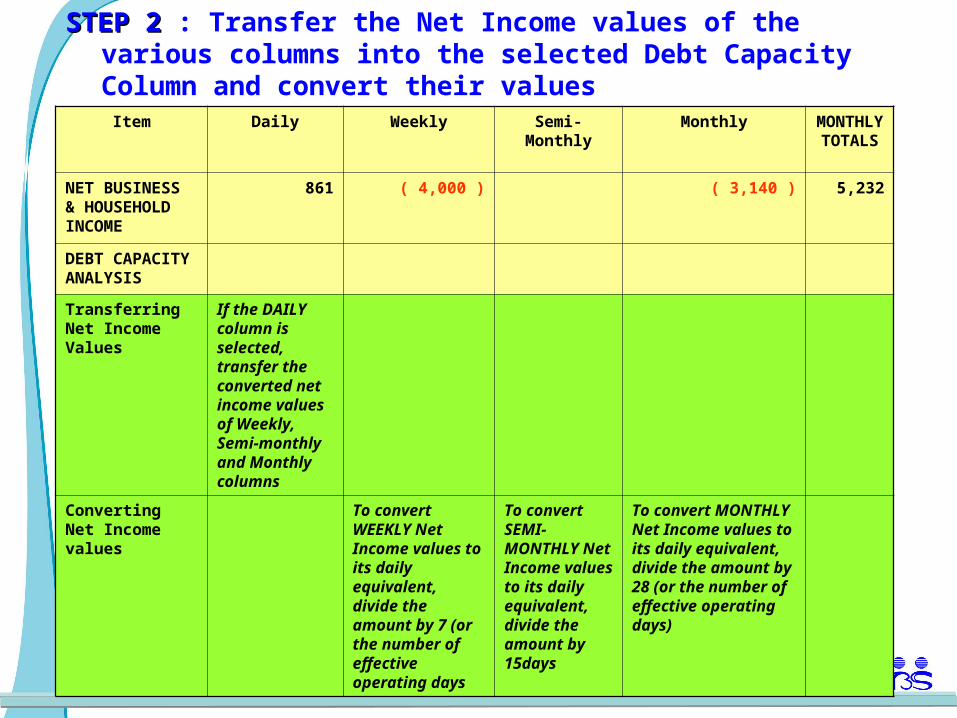

STEP 2STEP 2 : Transfer the Net Income values of the various columns into the selected Debt Capacity Column and convert their values

Item Daily Weekly Semi-Monthly Monthly MONTHLY TOTALS

NET BUSINESS & HOUSEHOLD INCOME

861 ( 4,000 ) ( 3,140 ) 5,232

DEBT CAPACITY ANALYSIS

Transferring Net Income Values

If the DAILY column is selected, transfer the converted net income values of Weekly, Semi-monthly and Monthly columns

Converting Net Income values

To convert WEEKLY Net Income values to its daily equivalent, divide the amount by 7 (or the number of effective operating days

To convert SEMI-MONTHLY Net Income values to its daily equivalent, divide the amount by 15days

To convert MONTHLY Net Income values to its daily equivalent, divide the amount by 28 (or the number of effective operating days)

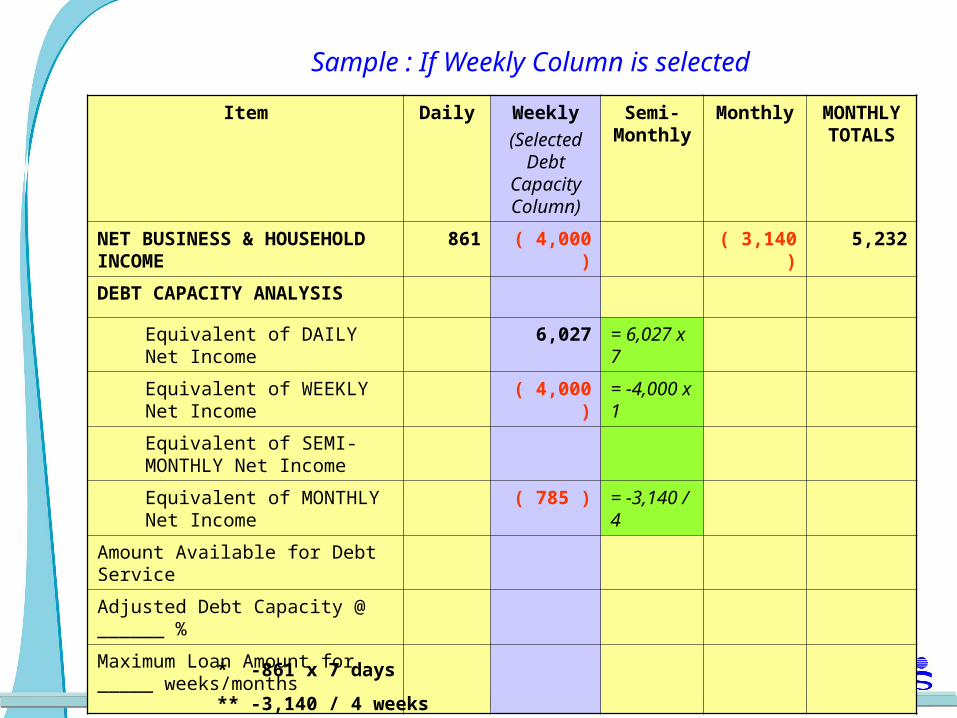

Item Daily Weekly

(Selected Debt

Capacity Column)

Semi-Monthly

Monthly MONTHLY TOTALS

NET BUSINESS & HOUSEHOLD INCOME 861 ( 4,000 ) ( 3,140 ) 5,232

DEBT CAPACITY ANALYSIS

Equivalent of DAILY Net Income 6,027 = 6,027 x 7

Equivalent of WEEKLY Net Income ( 4,000 ) = -4,000 x 1

Equivalent of SEMI-MONTHLY Net Income

Equivalent of MONTHLY Net Income

( 785 ) = -3,140 / 4

Amount Available for Debt Service

Adjusted Debt Capacity @ ______ %

Maximum Loan Amount for _____ weeks/months

* -861 x 7 days

** -3,140 / 4 weeks

Sample : If Weekly Column is selected

Specific guidelines for converting Net Specific guidelines for converting Net Income: Income: Values – Values –

• Positive balances to the leftleft of the selected Debt Capacity Column areare included in the analysisincluded in the analysis since these refer to cash flows that have already been received by the client

• Positive balances to the rightright of the selected Debt Capacity Column are not to be included in the are not to be included in the analysisanalysis– Why? Columns to the right often refer to longer time frames – future

cash flows – and including these figures could overstate the figures of the Debt Capacity Column

Item Daily Weekly

(Debt Capacity Column)

Semi-Monthly

Monthly MONTHLY TOTALS

NET BUSINESS & HOUSEHOLD INCOME 861 4,000 3,140 5,232

DEBT CAPACITY ANALYSIS

Equivalent of DAILY Net Income 6,027

Equivalent of WEEKLY Net Income 4,000

Equivalent of SEMI-MONTHLY Net Income

0

Equivalent of MONTHLY Net Income 0

Amount Available for Debt Service 10,027

Adjusted Debt Capacity @ 35 % 3,509

Maximum Loan Amount for _____ weeks/months

42,434

Term : 3 months

Interest ; 2.5%/month

Item Daily Weekly

(Debt Capacity Column)

Semi-Monthly

Monthly MONTHLY TOTALS

NET BUSINESS & HOUSEHOLD INCOME 861 4,000 3,140 5,232

DEBT CAPACITY ANALYSIS

Equivalent of DAILY Net Income 6,027

Equivalent of WEEKLY Net Income 4,000

Equivalent of SEMI-MONTHLY Net Income

0

Equivalent of MONTHLY Net Income 785 3,140 / 4

Amount Available for Debt Service 10,812

Adjusted Debt Capacity @ 35 % 3,784

Maximum Loan Amount for _____ weeks/months

45,760

Term : 3 months

Interest ; 2.5%/month

Including positive net income values from longer time frame columns could unduly bloat maximum loan amounts

For conservatism (considering loans are character-based/collateral free), long time-frame positive values should not be included.

Positive net income value columns could serve as buffer fund should daily or weekly cash flows not turn out as expected.

Long time-frame columns (e.g. semi-monthly, monthly) with positive net income values indicate sufficient cash flow to support expenditures in those periods.

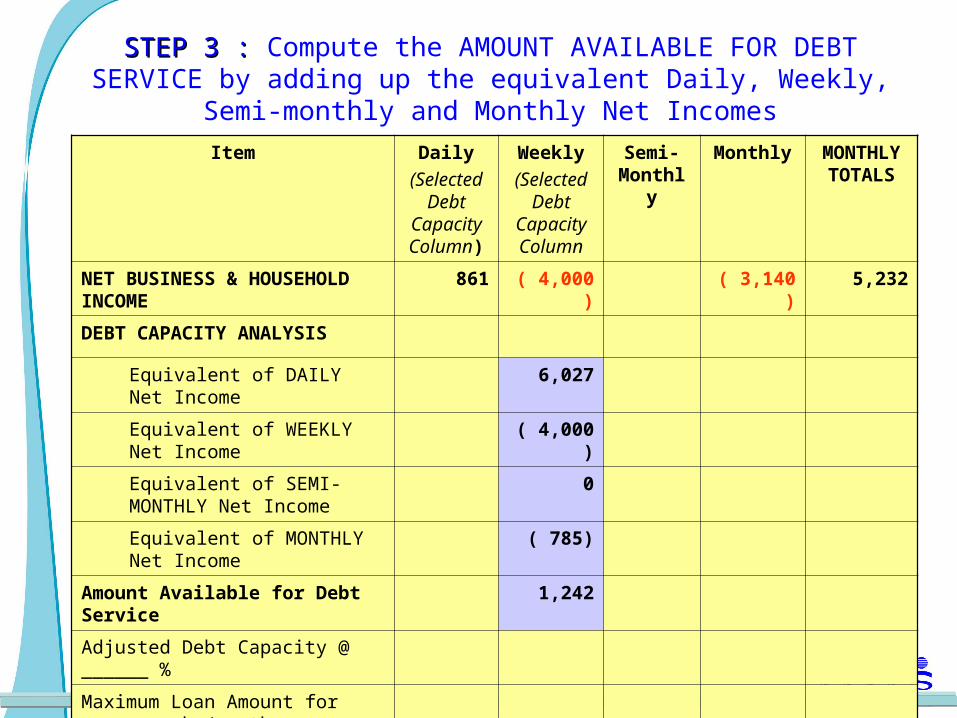

STEP 3 : STEP 3 : Compute the AMOUNT AVAILABLE FOR DEBT SERVICE by adding up the equivalent Daily, Weekly, Semi-monthly and

Monthly Net Incomes

Item Daily

(Selected Debt

Capacity Column)

Weekly

(Selected Debt

Capacity Column

Semi-Monthly

Monthly MONTHLY TOTALS

NET BUSINESS & HOUSEHOLD INCOME 861 ( 4,000 ) ( 3,140 ) 5,232

DEBT CAPACITY ANALYSIS

Equivalent of DAILY Net Income 6,027

Equivalent of WEEKLY Net Income ( 4,000)

Equivalent of SEMI-MONTHLY Net Income

0

Equivalent of MONTHLY Net Income ( 785)

Amount Available for Debt Service 1,242

Adjusted Debt Capacity @ ______ %

Maximum Loan Amount for _____ weeks/months

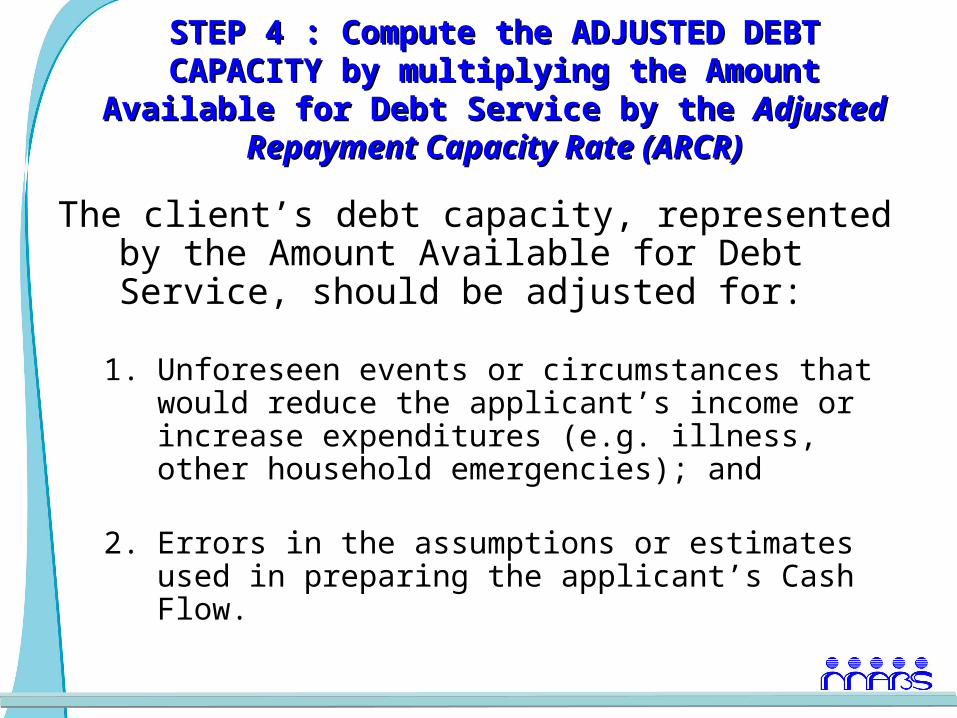

STEP 4 : Compute the ADJUSTED DEBT CAPACITY by STEP 4 : Compute the ADJUSTED DEBT CAPACITY by multiplying the Amount Available for Debt Service by multiplying the Amount Available for Debt Service by

the the Adjusted Repayment Capacity Rate (ARCR)Adjusted Repayment Capacity Rate (ARCR)

The client’s debt capacity, represented by the Amount Available for Debt Service, should be adjusted for:

1. Unforeseen events or circumstances that would reduce the applicant’s income or increase expenditures (e.g. illness, other household emergencies); and

2. Errors in the assumptions or estimates used in preparing the applicant’s Cash Flow.

In the example below, the ARCR used is 35%. This means that the lender assumes that only 35% of the client’s debt capacity will be

used for paying the new loan. By using a small portion of the client’s debt capacity, the lender is given a higher assurance that the loan is

well within the client’s capacity to pay.

Item Daily Weekly Semi-Monthly

Monthly MONTHLY TOTALS

NET BUSINESS & HOUSEHOLD INCOME 861 ( 4,000 ) ( 3,140 ) 5,232

DEBT CAPACITY ANALYSIS

Equivalent of DAILY Net Income 6,027

Equivalent of WEEKLY Net Income ( 4,000)

Equivalent of SEMI-MONTHLY Net Income 0

Equivalent of MONTHLY Net Income ( 785)

Amount Available for Debt Service 1,242

Adjusted Debt Capacity @ 35% 435

Maximum Loan Amount for _____ weeks/months

STEP 5: Compute the Maximum Loan Amount to be STEP 5: Compute the Maximum Loan Amount to be given to the client by using the Loan Size Multipliergiven to the client by using the Loan Size Multiplier

• Depending on the MFI’s policy, the formula for the Loan Size Multiplier may vary

Formula for Loan Size Multiplier

Policy Formula

Interest amortized(Standard)

(Adjusted Debt Capacity) * (No. of Installment Payments 1 + (Interest rate per month * No.

of months)

Interest discounted (deducted up-front)

(Adjusted Debt Capacity ) * (No. of Installment Payments)

Interest discounted / contractual savings 10% of loan installment

(Adjusted Debt Capacity) * (No. of Installment Payments) 1 + Contractual Deposit Rate

Interest amortized / contractual savings 10% of loan principal

(Adjusted Debt Capacity) * (No. of Installment Payments) 1 + [(Interest rate * No. of Months) +

Contractual Deposit Rate]

Interest amortized / contractual savings 10% of loan principal & interest payment

(Adjusted Debt Capacity) * (No. of Installment Payments) ((1 + (Interest rate * No. of Months)) * (1 +

Contractual Deposit Rate)]

Interest amortized (standard)Interest amortized (standard)

Max. Loan Size = Max. Loan Size = (Adjusted Debt Capacity) * (No. of Installment (Adjusted Debt Capacity) * (No. of Installment Payments)Payments)

1 + (Interest rate per month * No. of months)1 + (Interest rate per month * No. of months)

Example:

Loan Term: 3 mos. (91 days)Frequency of Payment: DailyInterest Rate: 2.5% per month

Max. Loan Size = (62.10) * (65) 1 + (.025*3)

= 4,036.50 1.075

= 3,754.88

The computed maximum loan amount is shown in the cash flow template as follows:

If a weekly amortization schedule is desired, the size of the weekly installment is computed by multiplying the adjusted daily debt capacity by 5. In the example above, the weekly installment will be:

62.10 * 5 days = P310.50

Item Daily Weekly Semi-Monthly

Monthly MONTHLY TOTALS

NET BUSINESS & HOUSEHOLD INCOME 861 ( 4,000 ) ( 3,140 ) 5,232

DEBT CAPACITY ANALYSIS

Equivalent of DAILY Net Income 861

Equivalent of WEEKLY Net Income (571.43)

Equivalent of SEMI-MONTHLY Net Income

Equivalent of MONTHLY Net Income (112.14)

Amount Available for Debt Service 177.43

Adjusted Debt Capacity @ 35% 62.10

Maximum Loan Amount for _____ weeks/months

3,754.88

Interest discounted Interest discounted ((deducted up-frontdeducted up-front))

Max. Loan Size = (Adjusted Debt Capacity) * (No. Max. Loan Size = (Adjusted Debt Capacity) * (No. of of Installment Payments)Installment Payments)

Example:Max. Loan Size = 62.10 * 65 = 4,036.50

Interest discounted / contractual savings Interest discounted / contractual savings 10% of 10% of loan installmentloan installment

Max. Loan Size Max. Loan Size = = (Adjusted Debt Capacity) * (No. of Installment (Adjusted Debt Capacity) * (No. of Installment Payments)Payments)

1 + Contractual Deposit Rate1 + Contractual Deposit Rate

Example:Max. Loan Size = 62.10 * 65

1.10

= 3,669.55

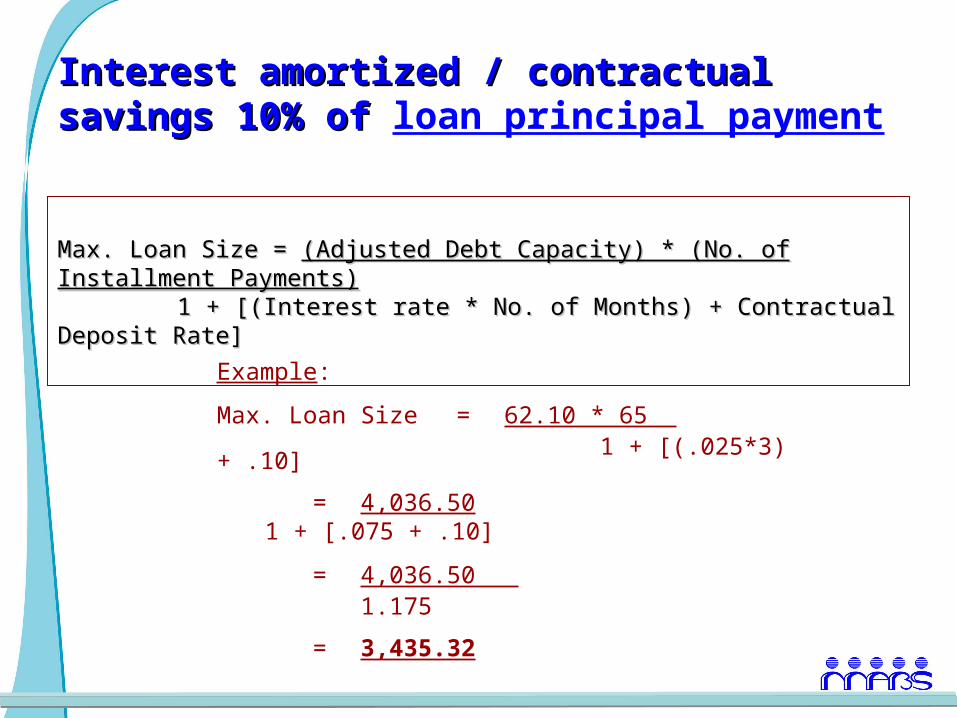

Interest amortized / contractual savings 10% of Interest amortized / contractual savings 10% of loan principal payment

Max. Loan Size = Max. Loan Size = (Adjusted Debt Capacity) * (No. of Installment (Adjusted Debt Capacity) * (No. of Installment Payments)Payments)

1 + [(Interest rate * No. of Months) + Contractual Deposit 1 + [(Interest rate * No. of Months) + Contractual Deposit Rate]Rate] Example:

Max. Loan Size = 62.10 * 65 1 + [(.025*3) + .10]

= 4,036.50 1 + [.075 + .10]

= 4,036.50 1.175

= 3,435.32

Policy Maximum Loan Amount

Interest amortized(Standard)

3,754.88

Interest discounted (deducted up-front) 4,036.50

Interest discounted / contractual savings 10% of loan installment

3,669.55

Interest amortized / contractual savings 10% of loan principal

3,435.32

Interest amortized / contractual savings 10% of loan principal & interest payment

3,413.53

21

Lending to Microenterprises without analyzing the cash flow …

… is like playing darts blind-folded. Determining how much loan the bank should give to a client is left to CHANCECHANCE.

Thank you!