Embed Size (px)

Citation preview

A TEXTILE INDUSTRY FO

IHE WEST COMPARED WITH THE NATION

:

% OF U^Si TOTAL

WESTERN MARKET POTENTIALS

P o p u l a t i o n I

ΓΘ))»)»»»»)»)»»)»)) Tire Product ion

s'"^--~>yK

r*$$

T e x t i l e Use ( a v g . est . )

Assumed T e x t i l e I n d u s t r y

MAJOR RAW MATERIALS FOR WESTERN TEXTILE INDUSTRY

^ tzèzzzzzzzz C o t t o n

Chemica l Cel lulose

j ^ ?

Caustic S o d a

ψχζζζζζζ ψ Xfçp[ Sul fur ic Ac id

v f ^ ï l Carbon Disulfide

70%

PRESENT WESTERN PRODUCTION

REQUIREMENT

Si£S£

30 '4tfc

A N I T A KASTENS

\JTREAT distances, vast natural resources, and a rapidly growing population characterize the 11 western states. These factors have contributed to a substantial growth of industry in the area during the past decade. Resource-oriented industries, particularly steel, aluminum, chemicals, pulp, and paper, have shown very high rates of growth. Timbering, food processing, and petroleum refining -were already well established.

The only important reso»urce-oriented industry which has neither significant volume nor a high growth rate in the West is textiles. For this reason, the industry has been the object of particular attention by those concerned witfci western industrial development. One such group, the Western Chemical Marlcet Research Group of San Francisco, joined forces with the Division of Chemical Marketing and Economics at the Los Angeles meeting last March 16 to discuss the economic feasibility and practicality of a textile industry in the West.

The Economic "Need" The basic assumption for such a dis

cussion is that an economic "need" exists for a Western textile industry. Such an addition to western industry would help to utilize available resources, supply the demands of the regional maxket, provide employment for the ever increasing labor force, and balance the economy, i.e., agriculture and extractive industries with manufacturing. Traditionally, however, the textile industry has centered along the eastern seaboard where it started in the early days of this country's development. On the basis of 1950 employment, almost half of it was in the Southeast, with another 45% in the Middle Atlantic and New England states. The Pacific Coast contributed about 0 .8% of the national value added by manufacture in the industry. Employment in the three Pacific Coast states totaled 8400, of which 6500 were production workers. There was no employment in the eight mountain statest Whether or not the West's need for a textile industry can be met, toerefore, depends on the requirements for expanded national capacity and the economic advantage of the regional location.

3132 C H E M I C A L A N D E N G I N E E R I N G N E W S

Λ Includes* B«C. & Alaska

Acetone

THE WEST

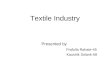

W h y not α western textile industry? In 1951 the West accounted for 1 9 % of the United States cotton production and over half of the dissolving pu lp—yet was an almost insignificant factor in the conversion of raw materials to finished products

Actually there is currently adequate nat ional capacity. The expansion of textiles, as measured by the total consumption of textile fibers, has approxiniatetd 2 . 8 % per annum over the 30 years 1920 to 1950. T h e growth of t h e industry as measured b y p lan t capacity has not , however, followed such a s teady course. T l ie cotton textile industry, for instance, grew steadily throughout its history until t h e mid-twent ies . Following this expansion total spindles in place declined substantially dur ing the 20-year per iod beginning 1925. Since 1945 the number has been fairly static. T h e difference between consumption and capacity has been made up by more efficient use of existing facilities, i.e., three shifts per day versus two. At the tradit ional growth ra te of t h e entire industry, however, new capaci ty must ult imately b e buil t . At tha t t ime regional economic advantage will determine whether t he capacity will b e added in existing product ion centers or in n e w areas, i.e., the West . T h e factors which affect plant location in the textile industry are similar to those in o ther industries. They include r a w materials , related industries, availability of water and power , markets , costs, etc.

Raw Materials Are Available T h e Wes t has the raw mater ia ls neces

sary for establishment of a textile industry. T h e chart on the facing page indicates t h e quanti t ies of raw materials t ha t would b e required for an industry based on 1 0 % of current U. S. consumption of viscose textile rayon, tire cord, acetate, a n d cotton. W h i l e this 1 0 % figure is arbitrary, it serves to p u t raw material requirements on a uniform basis. W i t h 1 3 % of the U. S. populat ion in t he 11 western states this figure represents a reasonable port ion of the indus t ry for this area.

Viscose Rayon. One p o u n d of viscose rayon requires for its manufac ture about 1 p o u n d of chemical cellulose, 1.2 pounds of caust ic soda, 1.4 pounds of sulfuric acid, 0.35 pound of carbon disulfide, a n d smaller amounts of glucose, zinc sulfate, and other metal sulfates, depend ing upon the part icular type of spinning b a t h b e ing used. Purifying and b leach ing of textile yarn requires chiefly sodium sulfide and hypochlori te . Consider ing now t h e basic assumption that the western viscose rayon industry will p roduce 1 0 % of t he national output, and listing separately t h e textile and t i re cord product ion, the chemical raw material requirements will be ob tained as shown in Tab le I, as is present production capacity for these basic chemi

cals now existing in t h e far western states.

It is seen from Tab le I that t h e increase in caustic soda capacity requi red for t h e prospective viscose rayon industry would b e over 2 0 % . Caust ic soda is now produced in the Pacific Northwest by Hooker Electrochemical Co. at T a c o m a and by Pennsylvania Salt Co. a t Tacoma and Portland. These companies sell approximately 7 0 % of their caustic ou tpu t to the pu lp and pape r industry of the Pacific Northwest and British Columbia. The re is more demand in this region for the caustic than there is for the chlorine m a d e at the same t ime. On the other hand , in the southern portion of the western region, caustic and chlorine are p roduced by Stauf-fer Chemical Co. at Henderson, Nev., and Dow Chemical Co. in t h e San Francisco Bay area, and t h e chlorine is in greater demand than t h e caustic. In general, t he market for caust ic soda is stable and growing. In the pas t five years, in fact, the caustic product ion of t he western region has more t han doubled.

In the case of sulfuric acid, t h e required increase over t he present existing capacity in the western Uni ted States amounts to less than 1 0 % . The wes tern region is liberally suppl ied with sulfur-bearing minerals upon which a large sulfuric acid industry could b e based. Dur ing the past few years, there has been a rap id increase in the recovery of waste sulfur from smelters and other forms of flue gas and its conversion to by-product sulfuric acid. Production of t h e acid is distr ibuted generally over t he region, and, in the past five years, t he total product ion has increased about one fifth.

Carbon disulfide has been p roduced by Stauffer near San Francisco for over 70 years, b u t only in small amounts to mee t demand . T h e 20,000 tons required for the assumed viscose rayon industry would be a large increase. However, t h e process for making carbon disulfide, in which sulfur

V O L U M E 3 1, N O . 3 1 » » A U G U S T 3, 1 9 5 3 3133

Table L Chemicals Required if οΠα Viscose Rayon Industry;

A T E X T I L E I N D U S T R Y F O R T H E W E S T

A symposium presented by the Western Chemical Market Research Group of San Francisco in the sessions of the Division of Chemical Marketing and Economics at the 123rd national meeting of the American Chemical Society, Los Angeles, March 16, 1953.

Opening Remarks. A. George Stern, Heyden Chemical Corp., San Francisco

The Need for a Western Textile Industry. Charles L. Hamman, Stanford Research Institute, Palo Alto, Calif.

Chemical Raw Materials. Edwin L Lovell, Rayonier Incorporated, Shelton, Wash.

Textile Raw Materials. Ernest R. Kaswall, Fabric Research Lab., Inc., Los Angeles, Calif.

The Textile Industry Looks Ahead. Mi l ton Harris, Harris Research Lab., Washington, D. C.

The Manufacture of Textile Fabrics. Graeme G. Whytlaw, American Viscose Corp., Marcus Hook, Pa.

Dyes tuff s and Finishing Chemicals. Sidney M. Edelstein, Dexter Chemical Corp., New York, Ν. Υ.

Investment Involved and Financing. Emery Cleaves, Celanese Corp. of America, New York, Ν. Υ.

Operating Costs, Including Labor. Frank P. Bennett, III, America's Textile Reporter, Boston, Mass.

Anita S. Kastens took her Vassar degree to an editorial position on the Journal of Chemical Education in 1945, and in 1948 star ted four and a half years as a chemical writer in t h e general publicity depar tment of the Union Carb ide and Carbon Corp. Now living in Menlo Park , Calif., where her husband (ex-ACS edi tor Merritt L, Kas tens) is assistant to the director of Stanford Research Inst i tute , Mrs. Kastens is doing free-lance wr i t ing—opera t ing what she calls the "Kastens Kopy Klatsch."

vapor is heated in the presence of carbon, is easily carried out, and plants may be located almost any place where t he re is a reasonable supply of sulfur and charcoal. There is no reason to expect that the required increase in the western product ion of carbon disulfide could not b e readily accomplished. T h e required charcoal, for example, may Be produced from available waste wood.

An appreciable quant i ty of zinc sulfate is also required as it controls the ra te of coagulation of t he filaments in t h e viscose spinning bath. Zinc is mined extensively in the western states, and the sulfate is readily produced by roasting of t he sulfide ores. Similarly, sodium sulfide and hypochlorite are available or readily made.

Cellulose A c e t a t e . One pound of cellulose acetate yarn requires for its p roduction only about 0.62 pound of chemical

cellulose, since the added acetyl groups increase the weight by more than 50%. Also required are about 0.03 pound of sulfuric acid, 1.55 pounds of acetic anhydr ide , and (assuming 9 5 % recovery) about 0.22 p o u n d of acetone. In addit ion to the yarn , about 3 /4 to 1 pound of acetic acid will be produced as a by-product.

If the estimate of 10% of the United Sta tes product ion is applied now to the aceta te industry, a production of approximate ly 5 7 million pounds of acetate filam e n t and staple yarn in the Western region is obtained. In addition, it has been es t imated that there is presently a market in t h e F a r West for some 10 million pounds of flake acetate for the production of solid plastics. Taking these two together, the figures shown in Table I I are obtained.

These data also should b e related to the presently existing Far Western produc

tion capacity. It is evident that t l ie sulfuric acid required is not a significant proportion of the present production o r even of that required for the proposed viscose industry. The procurement of this qFuantity-of sulfuric acid should therefore n o t constitute a problem.

The picture with relation to tln.e procurement of acetone is less favorable. The-table shows that approximately 12~6 million pounds or acetone w o u l d b e requirecL for the spinning of the ace ta te yarn-, again assuming 95c/c recovery. In additions, over 103 million pounds of acetic anraydride-would be required for the product ion of both fibers and plastics. Acetic anlmydride is largely rnoduced from acetone arad acetic acid. T h e acetone may t>e erae-ked to-ketene with about 9 0 % yield, amd this combined with acetic acid to for-m the** anhydride. T h e requirement for anheydride would approximately consume the? yield of acetic acid as a by-product fro»rn the acetylation process (about 60 icnillion pounds) and, in addition, would rrequire? some 66 million pounds of acetones The total annual requirement of acetone would therefore be in excess of 7 8 million pounds.

The present sole producer of acetone on the Pacific Coast is the Shell Cheinioal Co. While its production is est imated to» be in excess of 50 million pounds , by f a r the majority of this is now exported onr consumed in reactions to form other products, the present acetone market i n the ÏPacific area consuming only abou t 2 onillion pounds per year. The Oronî te Chomical Co. is now bui lding a p lan t whiclh will produce phenol and acetone from isoiipropyi benzene. T h e yield of acetone will be approximately 18 million pounds peir year. I t is therefore evident tha t t h e projected Western acetate industry, to t>e equivalent to 10% of the national production, would require the present Western manufacture of acetone to b e more than doubled unless exports from the area were considerably reduced. But since t h e acetone is readily produced—as, for examtple, by^ Shell —from isopropyl alcohol obtained from petroleum gases, it would appear th^at the necessary increase in product ion ,<would not be too difficult to obtain.. The= total U. S. production of acetone for 1952 was 480 million pounds , h a v i n g increased nearly 5 0 % since 1946,

Since the requirement of acet ic acid for the production of anhydride a n d the yield of acid from the acetylation process are approximately in balance, it is questionable whether there would be an over-all yield of acid or a small requirement to maintain the process. Commercial Solvents Corp. has made acetic acid a t Agnew, Calif., b a t this plant is not now operating.

Chemical Cellulose. T h e ahemicaLl cellulose industry is based in tu rn uposn another raw material, namely, ^wood. The Pacific Northwest—Oregon, ^Vashimgton, British Columbia, and Alaska—is fortunate in having a large supply of wood particularly suitable for the manufacture of cllieirri-cal cellulose, and , as a conseqruence, over half of the industry is located the re . At the present t ime, all of this outpa.it is

3134 C H E M I C A L A N D E N G I N E E R I N G N E W S

Table II. Chemicals Required

Chemical Cellulose

tons

Per lb. of Acetate, lb .

1 0 % of U. S. Acetate Yarn = 57,000,000 lb.

+ 10,000,000 lb .

Flake

To make Anhydride

Total Required Western States '

Product ion, tons

0.62

17,600 3,100

20,700

20,700

500,000*

per Year for a Cellulose A c e t a t e Industry

Sulfuric Acid tons

0.03

850 150

1,000

1,000

980,000

Acetone million lb .

0.221

12.6 0

12.6

66.02

78.6

68.0

Acetic Anhydride million lb.

1.55

88.0 15.5

103.5

0

Acetic Acid

million lb .

—0.92

—51 — 9

—60*

+ 6 1

1

0

* Assuming 9 5 % recovery from spinning 2 Yield as by-product, approximate 3 Acetone to ketene conversion, 9 0 % yield 4 Including British Columbia and Alaska

shipped to the eastern plants of the fiber manufacturers, or to the Far East, South America, or Europe. T h e industry is a stable one with advanced forestry practices designed to perpetuate the supply of the basic commodity, wood.

The heavy chemicals required for the manufacture of chemical cellulose include some used in the preparation of cellulosic-base textiles, particularly, caustic soda and chlorine. T h e chemical cellulose industry of Washington and British Columbia is estimated to consume about 25,000 tons of caustic and slightly more than this amount of chlorine pe r year. Other heavy chemicals consumed in large quantities by the chemical cellulose industry are lime, or more recently magnesia or ammonia, and sulfur, or pyrites. These chemicals are, of course, consumed in even larger amounts b y the pu lp and paper industry, which is similar in some of its basic manufacturing processes.

The projected viscose and acetate industries described would require a total of about 76,000 tons of cellulose. If, in accord with the national average, 2 0 % of this is supplied by cotton linters, there remains a market for 61,000 tons of chemical cellulose from wood. This represents a daily output of 175 tons, considerably less than the average of any one of the several mills now making chemical cellulose on a full-time basis in the Northwest. If, however, the total market were actually increased b y this amount, it would b e an increase of 1 5 % for the industry in the Northwest including British Columbia. There would then b e a corresponding increase in the industry's consumption of caustic, chlorine, sulfur, and other chemicals. Since the chemical cellulose industry has made great strides of growth in recent years, there is no doubt further increases could be made .

Cotton. In spite of the enormous growth of the man-made fiber industry in recent years, cotton still supplies over 70% of our total fiber needs. California, Arizona, and New Mexico grow about one fifth of the nation's cotton crop, and it is of especially

high quality because of the highly controlled growing methods used. Because this high quality cotton is in demand throughout the country for special uses, a western textile industry would not consume entirely western cotton. Eastern grades of cotton should b e imported for many types of fabrics.

Much cotton is used for heavy goods or low-grade materials in its natural form or with only a min imum of treatment. Some is purified, b y kier-boiling and bleaching. A large but undetermined proportion is given thorough cleaning and bleaching and is mercer ized to improve its strength and luster. For this kier-boiling, bleaching, and mercerizing, the chemical requirements have been estimated as shown in Table I I I . It i s assumed that 100 million pounds of cotton, about one fifth of the prospective industry using 10% of the national cotton ou tpu t , would be mercerized. The requirements for this operation would b e about 14,000 tons of caustic soda, 6000 tons of 100-volume hydrogen peroxide, and 250O tons of sodium silicate.

Hydrogen peroxide is made by Wes t -vaco in the Wes t . I t is made nationally by Du Pont, Pennsylvania Salt Mfg. Co., and Buffalo Electrochemical Co. by electrolytic processes. Since the processes are not exceedingly complex and depend on availability of power, it should be economic to start a plant i n the West if a market for it were developed.

Sodium silicate is produced in the San Francisco and L o s Angeles areas. The total national production is over 500,000 tons. There should b e no problem in its procurement.

In addition to the primary cotton fibers for textiles, there is also the accompanying yield of cotton linters. Linters as a source of pure cellulose in competition with chemical cellulose from wood are used chiefly for the manufacture of cellulose acetate and nitrocellulose. The linters are refined for chemical use by boiling in a caustic soda solution of about 3 .5% concentration ( b a s e d on the linters). Some 135,000 tons of l inters were consumed na

tionally in 1950 for rayon and acetate manufacture; if 10% of this processing were done in the West, t he caustic required would be about 5000 tons.

Synthetic Fibers. In addition to the cellulosic-based textiles which we have discussed, the growing production of the truly synthetic fibers must also be mentioned. These include nylon, Orion, Dac-ron, Acrilan, Dynel, and probably others to come, with a present total production of 300 million pounds per year. The chief raw materials for these fibers are adipic acid, adiponitrile ( these two making about half d ie total) , aerylonitrile, ethylene glycol, terephthalic acid, and vinyl acetate and chloride. The original source of all these compounds is petroleum, with the possible exception of adiponitrile based on furfural. Thus these chemicals are being made or could be made in the oil-producing areas of the West if a plant to make one of the fibers were established.

Related Markets. T h e textile industry is a highly competitive one, and flexibility is vital to successful operation. While 3 2 % of the cotton textile firms and olVc of the rayon firms are integrated units, there are still a great many independent spinning, weaving, and converting firms. This provides the operating flexibility necessary to meet market demands. The established mutual interdependence of these units introduces a locational factor, since they must of necessity locate where the other elements of the industry are. The importance of related industrial establishments has been and may continue to be a factor inhibiting regional decentralization within the textile industry.

A few small dyeing and finishing firms are now operating in California. A textile mill locating in California would likely start with products involving relatively simple finishing operations which it could perform itself. Integration plus t he development of the existing converting plants woidd provide a solution to the problem of finishing.

The problem of chemical raw materials to serve as auxiliaries in these operations

Table I I I . Chemicals Required for Mercerizing and Bleaching Cotton

(Tons per year)

NaOH H 2 0 2 NaoSiOs 100-vol. 100%

Per 2000 lb . of cotton

Kier boiling 0.03 Bleaching 0.012 0.005 Mercerizing 0.25

Total 0.28 0.012 0.005

For industrv of 100,000,-000 lb.1 14,000 6,000 2,500

Western States' Production 310,000 0 Adequate 1 1 0 % of U. S. cotton consumption =

490 million pounds Assume 100 million pounds mercerized

V O L U M E 3 1 , N O . 3 1 » » A U G U S T 3, 1 9 5 3 3135

can hardly be thought of in critical terms. A study was recently made of the purchases of all kinds of chemical items bought by several different kinds of cotton nulls (each mill in this survey spins yarn and weaves cloth, and no attempt was made to distinguish between the needs of the spinning and weaving departments) in the course of one year. Extrapolating the results of the study to the entire cotton industry in the United States, the following rough picture of the chemical purchases was revealed:

Acetylene Sizing Compound Crayon Gasoline Glue Grease (cup) Oil (lubricating) Oxygen (welding) Soap (scouring) Solvents Starch

8500 cylinders $5 million 150,000 boxes 5,700,000 gallons $200,000 10,500,000 lbs. 3,800,000 gallons 65,000 cylinders 1,800,000 lbs. $600,000 $44 million

Similar studies of knitting mills, rayon weaving mills, and woolen mills show similar small quantities per mill of these and other chemicals like salt, caustic soda, citric acid, acetic acid, wetting agents, water softeners, humectants. The primary producers of the different materials needed are scattered in thousands of plants all over the country and any long distance supply problems at best present minor competitive and production difficulties.

Dyestuffs are available from present manufacturers on the Eastern seaboard. Since freight costs in relationship to total

cost of dyestuffs are small, and since the manufacture o f dyestuffs requires great investment for plant equipment and many raw materials o o t available in the Western states, it does not seem likely or necessary that there be manufacture of dyestuffs in the Western states,

Many of t h « most important standard chemicals required for dyeing and finishing are presently available in the Western states. Certain important standard chemicals are available from the North Central states at freigrit rates probably not much greater than paid b y die dyers and finishers of the Eastern seaboard.

No textile chemical specialties are presently being manufactured in the far western states b u t they also are available from eastern concerns. With a developing textile industry, textile chemical specialties would prob>ably b e made with sulfated fats, oils and soaps, the first step in specialty manufacturing, followed by the manufacture o f blends, emulsions and finally the synthetic organics. The rate at which such a textile chemical specialty industry developed would depend not only on the rate of growth of the textile indus-stry b u t on t h e competitive situation, and on the availability and costs of raw materials.

Water Requirements Adequate Through the r~ear 2000

The unprecedented mass migration of people to the Western states since the war bas put a .heavy burden on the water resources of tb.e area. Current estimates of the ultimate population are important

Large capacity chemical cellulose plants in the Northwest such a s Rayonier's Shelton, Wash., mill offer strong evidence that an integrated textile industry for the West is highly feasible

in the consideration of future water requirements for municipal, industrial, and irrigation uses. However, sufficient water is available or could be made available should the future growth of this area so demand. The needs of a textile industry could be supplied, for example, in Southern California with waters from the Colorado or Owens Rivers. Municipal water supplies in the San Francisco Bay area are adequate for any additional heavy consumers of water to the year 2000 if the present growth rate of this region continues.

The textile industry is a heavy consumer of water. Water requirements of various types of textile operations are listed in Table IV. It would b e a small null indeed which would not require several million gallons of good quality waterl each day.

Many of the textile operations require water of such quality that it could not hope to be obtained in the West without raw water treatment, such as clarification, softening, demineralization, or iron and manganese removal. Specific requirements and economic factors in each case require skillful design and selection of the various possible means of effecting the needed purification. For example, softening might be effected by the application of one of the four recognized processes or combinations thereof: cold lime soda, hot lime soda, sodium cation exchanger, or hydrogen cation exchangers. It costs money to treat water, but there are few places remaining in this country where water of sufficiently good quality can be obtained which does not require treatment. Actually, current costs of water in the Bay region compare favorably with costs in N e w England and North Carolina, and treatment costs for water of comparable quality would be little different.

In the past it has been common practice in the textile processing areas to draw water from the available sources, use the water once, and dump it into a water course with little or no treatment. Federal

Table IV. Gallons of Water Required per 1000 Pounds Processed

Cotton: Sizing Desizing Kiering Bleaching Scouring Mercerizing

Dyeing: Basic Direct Vat Sulfur Developed Naphthol Aniline Black

Printing Finishing Knit Goods bleaching Rayon Manufacture

820 1,750 1,240

300 3,400

30,000

18,000 6,400

19,000 5,400

14,400 4,800

15,600 4,500

6 8,000 9,000

3136 C H E M I C A L A N D E N G I N E E R I N G N E W S

Tab3e V. Estimated Consumption of Textile Mil! .Products Based on Raw Fiber Equivalent1,* 1950

Cotton " * , " -11 Wes te rn States Total U . S.

°fo of * % Million Western Million - of U. S. Pounds Total Pounds Total

, " - Syn the t i c F ibe r s 1 1 . Wes te rn States - *: Tota l U

- * % of Million * Wes te rn Million Pounds Total Pounds

Ç Apparel ~ Indus t ry ^ H o u s e h o l d Consumpt ion i n d u s t r i a l Use tlOther2 _."" " \ ;

83 183 113

59

^438

19 42 26 13

1O0

1492 1269 1285 634

4680

32 27 28 13

100

4 3 1 5 4 5 11

ΪΪ4

38 13 40

9

7 7 3 105 4 7 9 139

1496

of U . S . -. T o t a i ; ^

32 ^<i&

ïôô 2S »>:^Thè figuresarev.a<breakdown of total fiber consumption a m o n g major markets o n t h e basis of end products sold in those mar-<*\

' I n c l u d e s ^ s p o r t ^ - ;^'^ v·? "γ V * ' * \ v;,~ ~ - , " * ' j^JSource: Uni ted Sta tes : Cot ton—N a t ional Cotton Council of America, Cotton Counts its customers ( M a y *52). jj4- « , Λ_ *. * '% \ Synthetic Fibers—Textile Economics Bureau, Textile Organon (March , 1952) . 1

Weste rn figures h a v e b e e n der ived as a percent o f t h e national o n t he basis of t h e appropr ia te factors: \ " A p p a r e l , on t he lbas i s of employmen t b y category; ~ , - - % * ! ; .

Ή/'\ Household, o n Sales Management's index of purchasing p o w e r ; ; x ^ .^ ;

* - Industrial,- on manufac tur ing employment exceïpt t i re cord and fabric , which w e r e based on tire product ion.

a n d State regulations on pollution of water courses, a s wel l as an increasing civic consciousness of plant operators, a re rapidly eliminating this practice. More a n d more mills are being required to place into operation adequa te t r ea tmen t plants for these l iquid wastes. In spite of years of investigation such t rea tment is still expensive, a factor which is encouraging t h e development of economy in wa te r use even i n the w a t e r rich areas.

In the solution of this problem, the wes te rn plants w o u l d not b e at a great cost d isadvantage . A n integrated p lan t on t h e coast w o u l d incorporate in the basic design al l possible conservation measures. Some possibilities in this direction inc lude : u s e of wastes from one operat ion t o make u p baths or solutions from another; the re-use of relatively clean -wash waters t o make u p m o r e concentrated solutions in the same process; t h e use of counterflow equipment 'which continuously discharges a waste tha t is small in volume a n d uniform in charac ter ; t h e re tent ion of spent ba ths a n d re use after making u p to s trength; and changes in type of processes used to eliminate those t ha t p roduce la rge volumes of -wastes or wastes that are difficul t t o treat.

Markets Are Available On the basis of present populat ion of

t h e western states compris ing abou t 1 3 % of t he nation a n d growing a t a ra te faster than the national average, there would seem to b e a perfectly available large scale market for textile products . Results of an analysis to de termine w h a t portion of t h e nat ional consumption of ap parel , household, and industrial textile i tems might b e a t t r ibu ted to t h e 11 western states are shown in Tab le V. T h e s e estimates h a v e been m a d e in terms of t h e pounds of r a w fiber necessary for t h e products involved. T h e total for cotton for the western states is 438 million

pounds, or 9 .4% of the nat ional total. Fo r synthetic fibers it is 114 million pounds, or 7 .6%.

The b reakdown of the western share of consumption is qui te different from tha t of the na t ion as a whole. In the case of cotton, household consumption is re latively m o r e important in t he West ; t h e industrial percen tage is about the same as for the nation; and the apparel industry consumption is lower . I t should b e no t ed t ha t the important segment of the apparel industry in the Wes t is women's sportswear. T h e Wes t accounts for nearly one fourth of total national employment in this branch. However, this is not sufficiently l a rge in the total apparel industry to affect t he western share of the market significantly. In the case of synthet ic fibers, differences also occur. Because of the importance of the tire industry on the West Coast, industrial consumption appears relatively high. Household consumption also is relatively high, b u t consumption b y the apparel industry is con-siderablv less important than it is nat ionally.

On t h e basis of preliminary analysis it would a p p e a r tha t ducks, twills, and drills would offer possibilities for t h e W e s t Coast industr ia l market . Tire cord, b o t h rayon and cotton, and tire cord fabr ic would also bear investigation. Sheetings and Osnaburgs used in the bag industry are large items of consumption, bu t t h e future outlook is not bright . For t h e household market bed sheeting, toweling, blankets, a n d pr in t cloth might offer pos sibilities. Fo r t he apparel industry denim, print cloth, broadcloth, and ginghams certainly should b e considered. Obviously, an extensive s tudy of marke t demand, not only quant i ta t ively , b u t wi th respect to construction, wid th , etc., would b e necessary t o establish feasibility in each case.

As at result of such study, some of these products would probably b e discarded. However, it seems fair to conclude tha t

in a consumption market totaling in excess of 500 million pounds, there must b e items of sufficient volume to support t h e operat ion of textile mills in t h e area. I t should be poin ted out tha t an industry involving about 25 textile mills exists in Texas; the marke t in tha t state is substantially less than tha t in California.

Finances Loom as No Problem T h e financial problems in establishing

a Western textile industry or its components are more of an economic na ture t h a n concerned with the problems of raising money. In its normal and gradual developmen t there should be no difficulty in financing, through normal channels, a n y par t of a textile industry which has a fair chance to make attractive profits. Unt i l recentiy, most units in the textile industry originated as small scale, family financed and opera ted concerns. Developmen t of a western textile industry is likely to follow the eastern pat tern and occur either as small independent units or as b ranch plants of larger concerns. A b ranch of an - established organization seems the most practical textile component to appeal to local investment circles. Supported b y the paren t organization's financial s t rength and skills, a substantial pa r t of the capital ί ucture could probably b e obtained by sale of mor tgage bonds or debentures . Direct institutional investment in the parent company's equi ty would probably produce more capital . Wi th a n e w plant in operation, it very likely might look attractive to the general public .

All sorts of estimates can b e m a d e on actual capital investments tha t wou ld be requi red : $20 million to $50 million for a single economic uni t for t he product ion of aceta te o r viscose; $180 million to $300 million for cotton facilities to supply half the populat ion requirements of the wes t ern states; $330 million for an in tegrated series of spinning, weaving, dyeing, and

V O L U M E 3 1 , N O . 3 1 » » A U G U S T 3, 1 9 5 3 3137

finishing mills for all types of fibers adequate to serve a reasonable proportion of population requirements on a competitive basis with eastern units. Such estimates are, however, meaningless until a thorough market study indicates what could be produced economically in the area.

Transportation costs also impinge on the financial problems. Transcontinental rail transportation rates for cotton and synthetic yarns are the same as for piece goods. Thus, a western textile mill properly located would probably enjoy an advantage over a southern mill in the raw material and freight costs involved in delivering a pound of finished cotton fabric to a western market. In supplying the eastern market it would be at a fairly important disadvantage, except for the style factor, and that is both unpredictable and adventitious. In the long run, freight rates are such that they do not seriously hinder or help the establishment of a textile industry in the West,. A much more critical factor is that of labor supply and wages.

Labor Supply, aird Wages Experience has shown that the textile

industry cannot prosper located in or adjacent to large urban areas, nor does it do well if it is competing in the labor market with the newer industries, such as steel, aircraft, chemicals. In our tremendously expanding American economy, the textile manufacturer cannot absorb the costs, nor pay the wages, commensurate with the newer industries.

It has been proved that individual textile companies do best in rural areas where there is a true, hungry need for cash wages. The general financial success of the newer textile industry in the states of North and South Carolina and Georgia comes out of the real farm and country areas. It has been the practice of the abler textile mill managements to build in very small country towns where there is an oversupply of men and women who are anxious to acquire day wages rather than to dig their living out of the ground. The policy has been to search for areas where there were from four to eight times as many employable people as would be required in an individual operation.

Over 30% of the cost of textile items is direct labor expenses. It is not a wage differential which makes the average southeastern textile company much more successful than its New England or Middle Atlantic counterpart. Simple arithmetic shows how much more successful a cotton mill in South Carolina which schedules 50 looms to the weaver will be compared to its older competitor in the Northeast with a schedule of only 24 looms to a weaver.

But there is more to this than just workloads and comparative workloads. In the more anciently industrialized Northeast, employees are not only sons and daughters and grandsons and granddaughters and great-grandsons and great-granddaughters of industrial employees with inherited conceptions of what a fit day's work should be; they are the products of

industrial employment competition. Unfortunately, textile mill employment is considered to be least desirable and the children of textile mill employees feel any other sort of employment a betterment. So northeastern textile mills receive on the average poorer grades of help. On the other hand, in South Carolina, for instance, in many many areas, the best jobs, the greatest earning opportunities are in textile plants; there are no competitive labor markets.

This discussion explains the comparatively recent, rapid growth of the textile industry in the South. Any operations in the West would be established against the momentum of this over-all trend. However, the West is tremendous, encompassing an area far beyond the size in the imaginations of most Easterners. Although it has become relatively industrialized over the past few years, the area nonetheless remains primarily rural. It appears most likely that an adequate supply of labor could be made available in several regions otherwise suitable for the location of a textile mill.

Wage rates might, however, present a problem. Figures show that average hourly wages paid in California are above those of the national average and are considerably more than those paid in either the southeastern or northeastern parts of the country. It is a fact that average sectional wages are above those of the textile industry. It is safe to say that perhaps -the average textile differential would be about 18 to 20% in favor of the Southeast. This sort of a differential, however, has a tendency to disappear as an industry matures, and should become less important with time. A Western textile industry can offset its temporary disadvantage by higher productivity through use of the newest types of equipment, versatile in their adaptability to produce yarns and fabrics currently in demand and efficient to the point of doing the job of several older machines in the East.

QUOTOONS ( R E < 5 . U . S . P A T E N T O F F I C E J

Nothing makes a man want to get back to work like a day at home with a had cold and the children,

• · m

A man reaches middle age as soon as he has to throw his shoulders back to maintain his center of gravity.

• · · A friend is a person who stops,

looks and listens to you.

—O. A. BATTISTA

( A L L R I G H T S R E S E R V E D )

Laboratory controls and the personnel to man same will be an important need of the textile industry in the West

The Crystal Ball Says, Yes The present textile industry is a com

plex affair which has become specialized and mechanized over the years to give the best possible product at the lowest possible price. This specialization means high volume production of a very small number of items in each textile plant. Under these conditions a thoroughly integrated textile industry in the West is probably very much further in the future than establishment of specialized units.

The West Coast has made a deep impression on the style market in the leisure or casual clothes category. This offshoot from the textile industry did not grow with spinning yarns or weaving fabrics or finishing and dyeing grey goods. Some specialized needs of the garment manufacturers were met by converters, dyers, and finishers who came into the picture. Still to come are the weavers and spinners. Behind them, the raw material suppliers stand ready.

That a western textile industry will grow piecemeal is indicated by the pattern established in the apparel field. Obviously, spinners and weavers are not a necessary or logical part of the early growth of a Western textile industry. The purchase of yarns and fabrics during the period of market development, thus avoiding an immediate large capital investment in various mills, has much to be commended, although dependence on remote sources of supply might be attended by a lack of interest in local problems.

The need for substantial additions to textile capacity has not been present since aie mid-twenties. Ultimately growing demand and obsolescence of existing equipment is certain to bring another expansion cycle. In the meantime, the climate for a textile industry in the West is becoming increasingly favorable. The markets are growing and deterring factors are becoming less and less significant. If these trends continue, the textile industry-should be numbered among the western industrial opportunities of the future.

3138 C H E M I C A L A N D E N G I N E E R I N G N E W S