Embed Size (px)

Citation preview

Session 66, Predictive Analytics Tools for Life Insurance

Moderator:

Dorothy L. Andrews, ASA, MAAA

Presenter: Dorothy L. Andrews, ASA, MAAA Missy A. Gordon, FSA, MAAA Timothy S. Paris, FSA, MAAA

2016 Valuation ActuarySymposium

Predictive Modeling Tools for Life InsuranceSession 066

August 30, 2016

Dorothy L. Andrews, ASA, MAAAConsulting ActuaryMerlinos & Associates

2

Agenda

• What is Predictive Analytics?• Predictive Analytics Software Tools• Advanced Modeling Theory• An Actuarial Predictive Model Application

3

Predictive Analytics – Science or Art?

“The practice of extracting information from existing

data sets in order to determine patterns and

predict future outcomes and trends.”

-Webopedia

“The use of data, statistical algorithms and

machine-learning techniques to identify the likelihood of future

outcomes based on historical data.”

- SAS

“It’s the process of using modeling and data

analysis techniques on large data sets to

discover predictive patterns and

relationships for business use.”

- SOA

4

Common Themes

• Identification of Historical Big Data • Application of Advanced Mathematical Theory• Determination of Predictive Data Patterns• Forecasting of Likely Future Data Patterns• Application of Model to Improve Business Results

5

Current Technologies for Modeling

Technology Programming GLM Method Machine Learning Documentation

R Yes Yes Yes Yes

Python Yes Yes Yes Yes

SAS & SPSS Yes Yes Yes Yes

DataRobot No Yes Yes Only on Screen

Skytree No No Yes Only on Screen

Talon No Yes Yes Yes – Excel Files

Emblem No Yes No Yes

6

Big Data AnalyticsData Reduction Techniques

Descriptive

Descriptive statistics used to condense big data into easily

digestible nuggets of information.

Prescriptive

A predictive model that uses feedback

data to improve information used in

decision making.

Predictive

Probability based forecasts allowing

for extrapolations to future time periods

where data does not exist.

Dr. Michael Wu, Chief Scientist, Lithium Technologies

7

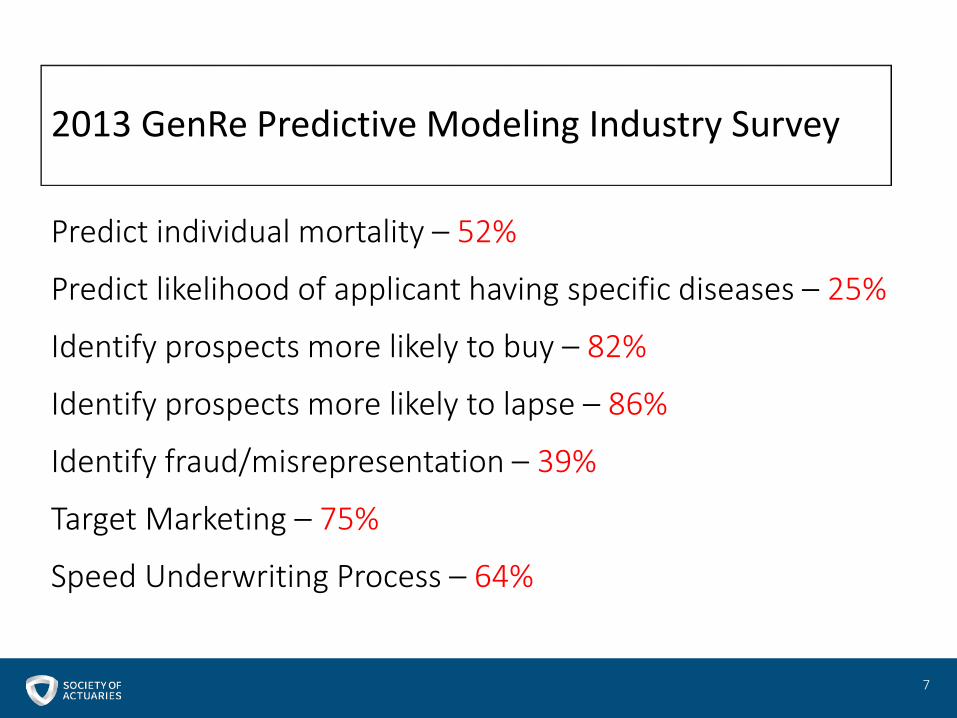

Predict individual mortality – 52%

Predict likelihood of applicant having specific diseases – 25%

Identify prospects more likely to buy – 82%

Identify prospects more likely to lapse – 86%

Identify fraud/misrepresentation – 39%

Target Marketing – 75%

Speed Underwriting Process – 64%

2013 GenRe Predictive Modeling Industry Survey

2016 Valuation ActuarySymposium

Predictive Modeling Tools for Life InsuranceSession 066

August 30, 2016

Timothy Paris, FSA, MAAAChief Executive Officer Ruark Consulting LLC

Behavioral Analytics

9

Frequency

10

Severity

11

Modeling Techniques

12

13

y|xSimple Linear Modeling

E(y|x)Classical Linear Modeling

g[E(y|x)]Generalized Linear Modeling

(GLM)Flexible framework

Non-normal

Non-constant variance

Generalized Linear Modeling

14

15

Poisson Regression Model

ln 𝜇𝜇 = 𝛽𝛽0 + �𝛽𝛽𝑖𝑖𝑥𝑥𝑖𝑖

Counts, such as number of claims

16

Exponential Regression Model

1𝜇𝜇

= 𝛽𝛽0 + �𝛽𝛽𝑖𝑖𝑥𝑥𝑖𝑖

Positive values, such as claim amounts

17

Logistic Regression Model

ln𝜇𝜇

1 − 𝜇𝜇= 𝛽𝛽0 + �𝛽𝛽𝑖𝑖𝑥𝑥𝑖𝑖

Binary values, such as surrenders or deaths

Cluster Analysis

18

Torture the datauntil the cohorts

are identified!

19

Decision Tree Analysis

20

Effectivetop-down

classification

21

Greedyalgorithms

22

Random Forests

23

24

Machine Learning

25

Can a computer programinfer distribution functions

as well as you can?

26

Data Considerations

27

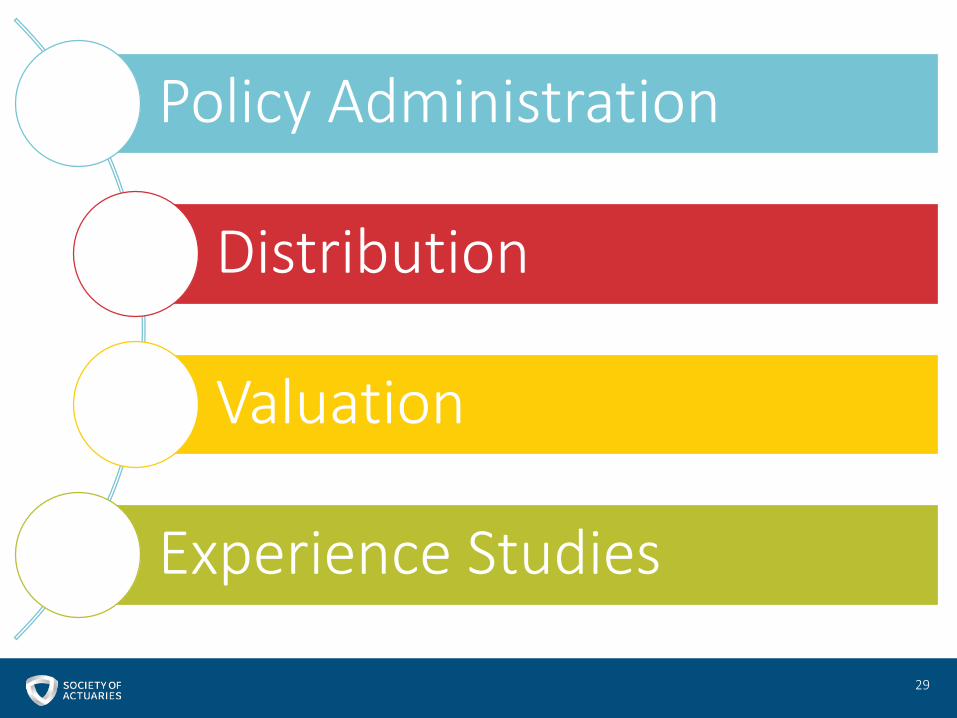

Internal Data

28

29

Policy Administration

Distribution

Valuation

Experience Studies

External Data

30

31

Direct vs Third Party

Public vs Private

Exact vs Proxy

Validity vs Propriety

Data Scrubbing

32

33

Who Cared

Which Fields

Control Totals

Reasonable Visuals

The Art ofData Preparation

34

35

Ideals Usability

An Actuarial Predictive Model Application2016 Valuation Actuary SymposiumPredictive Modeling Tools for LTC InsuranceSession 066August 30, 2016

Missy Gordon, FSA, MAAAPrincipal and Consulting ActuaryMilliman, Inc.

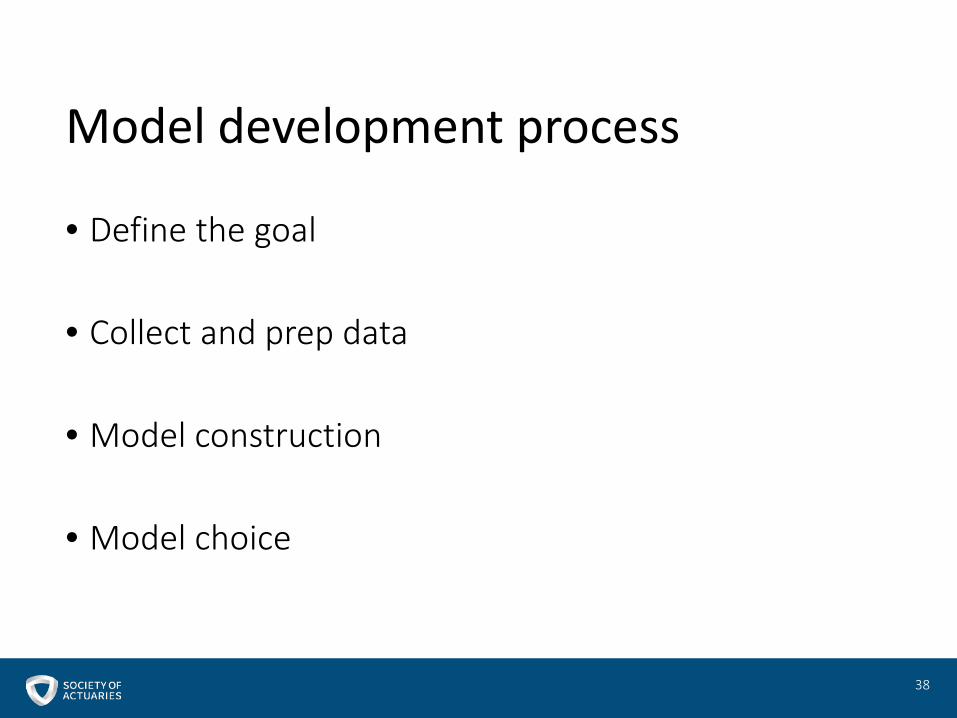

Model development process

37

• Define the goal

• Collect and prep data

• Model construction

• Model choice

38

Model development process

Define the goal

39

• What problem are we trying to solve?

• LTC claimant’s length of stay

• Predict for existing and future claimants

• What do we want to get out of model?

• Inference, prediction, or maybe little of both

• New or update to existing assumption

40

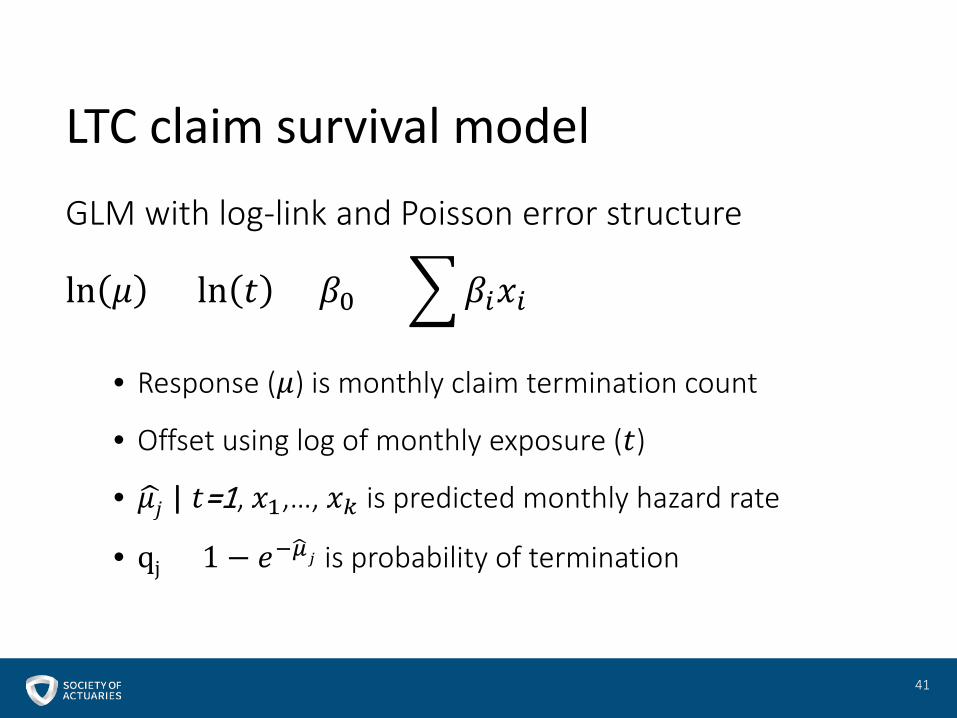

Define the

GLM with log-link and Poisson error structure

ln 𝜇𝜇 = ln 𝑡𝑡 + 𝛽𝛽0 + �𝛽𝛽𝑖𝑖𝑥𝑥𝑖𝑖

• Response (𝜇𝜇) is monthly claim termination count

• Offset using log of monthly exposure (𝑡𝑡)

• �𝜇𝜇𝑗𝑗 | 𝑡𝑡=1, 𝑥𝑥1,…, 𝑥𝑥𝑘𝑘 is predicted monthly hazard rate

• qj = 1 − 𝑒𝑒−�𝜇𝜇𝑗𝑗 is probability of termination

41

LTC claim survival model

• Use offset to update for• New experience

• Additional variables

• What is an offset?• Existing assumption as base rate

• Model adjusts only if experience deviates

ln 𝜇𝜇 = ln 𝑡𝑡 ∗ 𝑏𝑏𝑏𝑏𝑏𝑏𝑒𝑒 𝑟𝑟𝑏𝑏𝑡𝑡𝑒𝑒 + �𝛽𝛽𝑖𝑖𝑥𝑥𝑖𝑖

42

Update existing assumptions

Collect and prep data

43

• 15 years of seriatim LTC claim data

• Observation: monthly termination flag (1 or 0)

• Exposure: proportion of time on claim in a month

• Aggregate data to speed up computations

44

The data

• Training, validation, and optional final testing

• In-time sample vs. Out-of-time sample

45

Separating the data

Training ~ 60% Validation ~ 20% Test ~ 20%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

46

Training ~ 60% Validation ~ 20% Test ~ 20%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Training ~ 80% Test ~ 20%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Training ~ 100%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

47

K-fold cross-validation

Model construction

48

= Domain knowledge

+Exploratory data analysis

49

Feature Engineering

• Visualize data to aid in feature engineering

• Decision trees may help gain relationship insight

• GAMs can explore non-linear relationships

• Use training data only to avoid knowledge leak

50

Exploratory data analysis

51

52

53

• Pros

• Automated and easy to use

• Useful way to analyze key drivers

• Cons

• Variables are selected based off of training data only

• Prone to overfitting

• Issues handling multicollinearity

• Takes longer than forward or backward selection

54

Bi-directional stepwise selection

• Lasso, Ridge, and Elastic Net

• Pros

• Control overfitting by minimizing prediction error

• Provide variable selection (shrinking coefficients)

• Cons

• Tuning hyper-parameters (e.g., shrinkage)

• Biased standard error estimates

55

Regularization methods

ln 𝜇𝜇 = ln 𝑡𝑡 + 𝛽𝛽0 + �𝛽𝛽𝑖𝑖𝑥𝑥𝑖𝑖

�𝜇𝜇𝑗𝑗 | 𝑡𝑡=1, 𝑥𝑥1,…, 𝑥𝑥𝑘𝑘 is predicted monthly hazard rate for observation j

�𝜇𝜇𝑗𝑗 = 𝑒𝑒�𝛽𝛽0 × 𝑒𝑒�𝛽𝛽1𝑥𝑥1 × ⋯× 𝑒𝑒�𝛽𝛽𝑘𝑘𝑥𝑥𝑘𝑘𝑒𝑒�𝛽𝛽0 = baseline monthly hazard rate

𝑒𝑒�𝛽𝛽𝑖𝑖𝑥𝑥𝑖𝑖 = multiplicative factor to adjust baseline for variable 𝑥𝑥𝑖𝑖

qj = 1 − 𝑒𝑒−�𝜇𝜇𝑗𝑗 is probability of termination in a given month

𝑆𝑆𝑗𝑗 = 𝑆𝑆𝑗𝑗−1 × (1 − 𝑞𝑞𝑗𝑗) is survival to end of month j

56

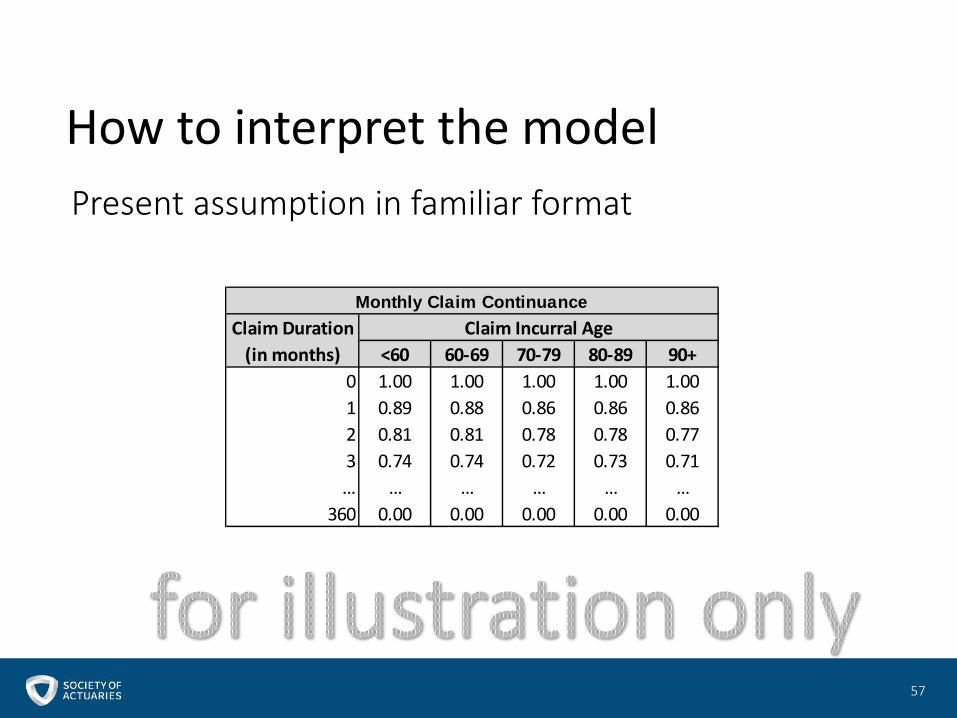

How to interpret the model

Present assumption in familiar format

How to interpret the model

57

Monthly Claim ContinuanceClaim Duration Claim Incurral Age

(in months) <60 60-69 70-79 80-89 90+0 1.00 1.00 1.00 1.00 1.001 0.89 0.88 0.86 0.86 0.862 0.81 0.81 0.78 0.78 0.773 0.74 0.74 0.72 0.73 0.71… … … … … …

360 0.00 0.00 0.00 0.00 0.00

Model choice

58

• Metrics on training data • In-sample prediction metrics - AIC, BIC, etc.• Includes adjustments to penalize model complexity

• Metrics on unseen data (i.e., validation set)• Standard error metrics - MAE, MSE, AUC, deviance, etc.• No need to adjust for model complexity

• K-fold cross-validation • Use training data to produce out-of-fold error metrics • Computationally intensive

59

Metrics for choosing a model

• Validation data to choose between models

• Standard error metrics

• Actual-to-expected analysis

• Lift chart

• Quantiles of differences

• Choose benchmark to compare and test model

60

Choosing the final model

61

Choosing the final modelPoisson Deviance Summary on Validation Set

Summary Level Base Model New Model ImprovementOverall Overall 15,015 14,593 3%Gender F 8,577 8,326 3%Gender M 6,438 6,267 3%Care Setting ALF 3,696 3,799 -3%Care Setting HHC 5,020 4,863 3%Care Setting SNF 6,299 5,931 6%Duration 1 263 240 9%Duration 2 415 356 17%Duration 3 444 394 13%Duration 4 558 432 29%Duration 5 410 357 15%Duration 6 356 355 0%Duration 7 278 284 -2%Duration 8 353 352 0%Duration 9 297 305 -2%Duration 10 296 307 -4%Duration 11 224 236 -5%Duration 12 288 295 -3%

AtoE Analysis on Validation SetSummary Level Base Model New Model ImprovementOverall Overall 1.03 1.01 2%Gender F 1.01 1.00 1%Gender M 1.05 1.02 3%Care Setting SNF 1.07 1.05 2%Care Setting ALF 0.77 0.82 4%Care Setting SNF 1.07 1.05 2%Gender F SNF 1.05 1.04 2%Situs F ALF 0.77 0.82 5%

F HHC 1.08 1.04 4%M SNF 1.12 1.08 4%M ALF 0.78 0.81 3%M HHC 1.07 1.03 4%

Tax Status TQ 1.01 0.98 -2%NTQ 1.03 1.02 1%

Incurred Age LE_59 1.28 1.22 6%60_69 1.19 1.12 7%70_79 1.03 1.00 3%80_89 0.99 0.99 0%GE_90 1.06 1.04 2%

62

Choosing the final model

• Refit on combined calibration and validation data

• Re-run prior tests on the final testing data

• If predictive, then refit on all data and use it

• Otherwise, abandon and look for other methods

63

Testing the final model

64

Questions

Presenter Contact Info:

Timothy S Paris, FSA, MAAAChief Executive Officer Ruark Consulting LLC 530 Hopmeadow StreetSimsbury, CT 06070Tel: (860) 866-7786 Email: [email protected]

Missy Gordon FSA, MAAAPrincipal and Consulting ActuaryMilliman8500 Normandale Lake Boulevard, Suite 1850

Minneapolis, MN 55437-3830Tel: (952) – 820 – 2478 Email:[email protected]

Dorothy L. Andrews, ASA, MAAAConsulting ActuaryMerlinos & Associates3274 Medlock Bridge RoadPeachtree Corners, GA 30092Tel: (687) 684-4869 Email: [email protected]