Embed Size (px)

Citation preview

VOLUME I / EXPLORATION, PRODUCTION AND TRANSPORT

2.1.1 Definition of exploration

Exploration is the first phase of the petroleum cycleand includes all activities relating to the search forhydrocarbons. In the literature (Langenkamp, 1994;Williams and Meyers, 2003) the term exploration isdefined as “the search for oil and gas [...], includingaerial surveys, geophysical surveys, geological studies,coring and the drilling of exploration wells”. Otherclassification systems include exploration under thebroader heading of reservoir development. However,according to the universally accepted definition,exploration is a phase of the petroleum cycle aimed atfinding hydrocarbon accumulations, which to this endmakes use of various scientific disciplines. Theexplorationist is a geologist who uses the data obtainedwith various methodologies to develop a geologicalmodel of the area, and who formulates workinghypotheses on the basis of all the geological andgeophysical data collected, evaluated within a generalcontext. In the United States there are two categoriesof explorationists: ‘generalists’ who are able toevaluate the data as a whole, and ‘specialists’, such asmicropalaeontologists, seismologists, log analysts,sedimentologists and geochemists, who capture andinterpret specific types of data. Specialists appear onthe oil scene at the end of the 1920s (before this datethe geologist managed the entire process,concentrating on the fundamentals of exploration),indicating the importance of interpretative tools suchas stratigraphy, sedimentology, the petrography ofclastic and carbonate rocks, and log analysis.

In the context of an oil company’s activities, therole of exploration is to provide the informationrequired to exploit the best opportunities presented inthe choice of areas, and to manage research operationson the blocks acquired. Exploration is responsible formanaging the risk inherent in this activity, selecting

the best of a range of options in probabilistic andeconomic terms (see below). Risk is an inherentcomponent of the various phases of exploration. Forexample, it is risky to request an exploration permit onthe basis of more or less detailed data, taking onsubsequent work obligations (a number of wells to bedrilled, financial commitments), as is deciding to drilla given well rather than another. This element of riskcannot be eliminated entirely but it can be managedsuccessfully. Some exploration choices are of astrategic nature, such as that between high-risk virginareas where the probability of success is lower, andareas in mature basins where results are more easilyachieved, but discoveries modest.

In the sequence of activities characterizing thepetroleum cycle, exploration represents an extremelydelicate initial phase. This is the start of a process onwhose results (success or failure) the future economicchoices of the project depend. In the case of petroleumsuccess (discovery), a long time may be required toproduce the accumulation found (from 20 to 100 yearsdepending on the size of the reservoir discovered).

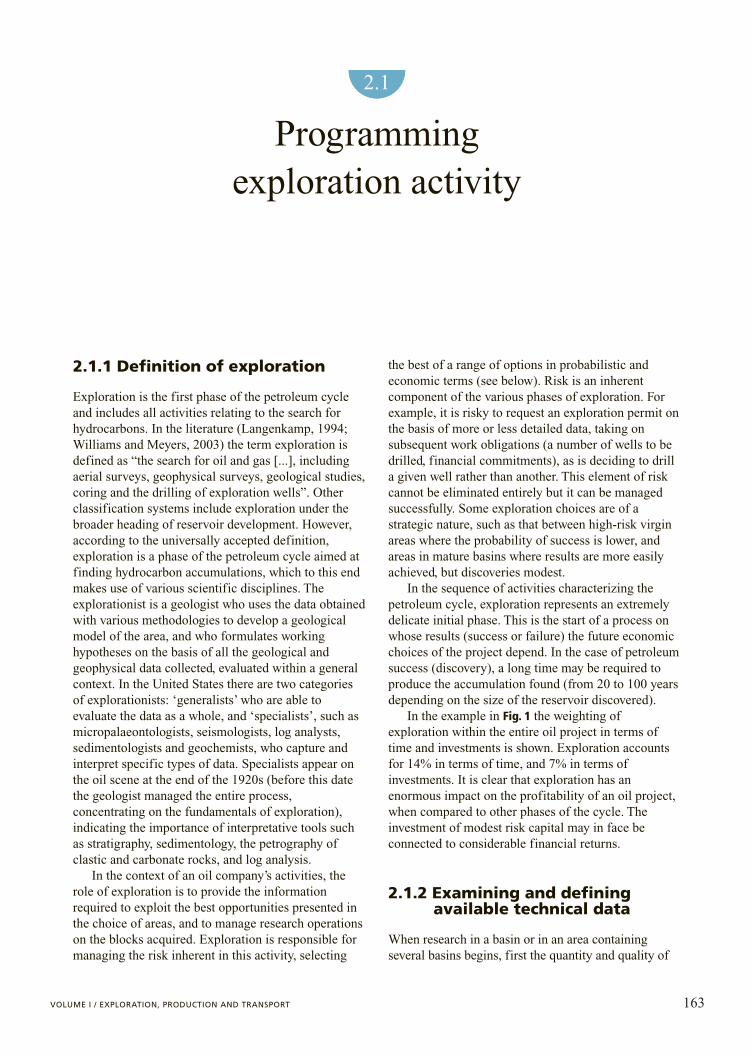

In the example in Fig. 1 the weighting ofexploration within the entire oil project in terms oftime and investments is shown. Exploration accountsfor 14% in terms of time, and 7% in terms ofinvestments. It is clear that exploration has anenormous impact on the profitability of an oil project,when compared to other phases of the cycle. Theinvestment of modest risk capital may in face beconnected to considerable financial returns.

2.1.2 Examining and definingavailable technical data

When research in a basin or in an area containingseveral basins begins, first the quantity and quality of

163

2.1

Programming exploration activity

available data must be checked. In little-known areas,data on geology, stratigraphy, tectonics, the type ofreserves, the production of existing fields, the layerscontaining hydrocarbons represent essential basicinformation. Sometimes the geological data areinsufficient for the type of research which is intendedto undertake. This was the case during the 1970s whenexploration was directed towards continental shelvesand in the 1980s when attention was turned towardsdeep offshore areas. At the time, the only available datareferred to environments which could not be easilycorrelated with the areas under investigation.Sometimes, data are difficult to interpret or are in anon-standard format, as Western oil companies foundin the early 1990s when they tackled the documentationfor reservoirs in some ex-Soviet countries.

Whether we are dealing with preliminary studies ofvirgin basins, regional exploration or in-depthexploration of known basins, the problem of availableand usable data is fundamental. It must be borne inmind that petroleum-related activities take placewithin the context of an extremely competitive system.Different companies exploit the same basicinformation on the potential of a basin, on ‘researchtopics’ (play, the combination of geological-stratigraphic and structural factors which may lead tothe accumulation of hydrocarbons) and on the

characteristics of geological formations. It is thereforeimportant to use all available data to select the mostpromising areas. The mechanisms for acquiringexploration permits are so complex, the methodologiesso expensive, the signature bonuses for new areas sohigh that it is inadvisable to run the risk of havingincomplete information.

Various types of data may be available for useduring the preliminary phase of petroleum exploration: • Preliminary (scouting) data marketed by specialist

companies. These might include, for example,information on operational activities in a givenarea, on wells being drilled, on mineral results(‘successful wells’ or ‘dry wells’, depending onwhether or not they produce hydrocarbons incommercial quantities), on operating oil fields andtheir principal characteristics, or technical reportscontaining an initial processing of geological data,including maps, facies analyses, palaeogeographicreconstructions of areas and basins. These data,which are generally very expensive, may bepurchased on the market, but it is obvious that onlymajor companies with a large turnover are in aposition to make systematic use of it. The reportsprovide preliminary information on the traits of abasin and allow us to build a geological model ofthe area.

164 ENCYCLOPAEDIA OF HYDROCARBONS

PETROLEUM EXPLORATION

(4%) (10%) (10%) (12%) (60%) (4%)

(2%) (5%) (8%) (45%) (35%) (5%)

life cycleproject

costsproject

cumulativecash flow

abandonmentproductiondevelopmentreservoir

delineation & modelling

prospectsdefinition/discovery

• wellsplugging

• plantremoval

• environmentalrestoration

• productionmanagement& optimization

• reservoirmanagement

• wellsinterventions

• development plan & environmentalaspects

• drilling &completion

• surface facilitiesconstruction &installation

• appraisaldrilling

• reservoir studies

• reservoirmodelling& reserves definition

• feasibilitystudies

• regionalstudies

• geologicalmodelling

• bid evaluation

• farm in/outopportunities

• seismic survey & interpretation

• drilling

• subsurfacegeology

• productiontests

basins/areas assessment

time

Fig. 1. Activities in the petroleum cycle.

• Non-exclusive geophysical (gravimetric, magnetic,and especially seismic) surveys commissionedfrom service companies (contractors). Thesecompanies, in agreement with the State owning theareas, programme and carry out surveys at theirown expense, on the basis of parameters suited tothe basin type and the relevant mineral objective,and place these at the disposal of oil companies.Obviously, the cost is considerably higher than forthe previous type of data. However, the informationis more complete, since it includes original seismicdata. At times, the purchaser may process theseoriginal data so as to highlight characteristicsuseful for the interpretation of the basin’s geology.These technical documents (packages) oftencontain well data, including electrical logs. Thesepermit to assign a specific geological meaning tothe seismic horizons, thus making an initialinterpretative evaluation of the area possible. Inthis type of non-exclusive purchase, the buyernever owns the original data, which remain theproperty of the State with which the servicecompany has signed the agreement.

• Photogeological and geological surveys. These,like on-site surveys or genuine geologicalcampaigns, may be undertaken directly at relativelylow cost, and may therefore also be carried outduring the preliminary stage of exploration. Othertypes of extremely expensive survey, on the otherhand, cannot be undertaken without mineral rights(e.g. an exploration permit) to protect their holder.The preliminary gathering of information about a

basin may confirm the parameters required to predictthe presence of hydrocarbons. At this point, it isnecessary to consolidate the knowledge of the basin bydeveloping a more sophisticated geological andgeophysical model. There are two possible scenarios:• The State has yet made no official decision

regarding the granting of exploration permits forthe area to be investigated. Oil companies candecide to carry out, at their own risk, seismicsurveys in the area without being protected byminerary rights, as has happened in the North Seaat the beginning of the 1970s.

• The area or group of areas to be analysed form theobject of a bid round announced by the competentauthority (the State, directly or through the nationaloil company). In this case, oil companies aresupplied with packages of seismic, geological andwell data, enabling them to study the potential ofthe area and prepare the terms of their bids. Thelatter must contain a series of evaluationsincluding, for example, the number of wells to bedrilled, the cost of completing all necessaryoperations, the kilometres of seismic (set of

surveys useful to understand the structure anddepth of subsurface geological layers) to beacquired. These data remain the property of theState, whilst the company has the right to use them.Once the areas up for bid have been examined, and

the potential for discoveries of commercialsignificance ascertained, the oil company which winsthe bid round is assigned mineral rights. Suchcompany can thus make investments, since it has aformal guarantee in the shape of a contract signed withthe relevant authority. At this point it has the right toobtain all available data on the area (both directly fromthe State, and from private companies which haveoperated there previously), and to process them in themost appropriate way.

Some of these data may already have been suppliedfor the bid round. Generally, these packages do notinclude all existing data. Once mineral rights areobtained, it is possible to organize an archive (ordatabase) containing all the information needed toundertake exploration in operational terms in the areascovered by the licenses. Usually, the most useful formsof data are well data and seismic data.

Well data must be evaluated with specific referenceto the well’s location, effective depth and coordinatesof the point of maximum depth (or total depth). It isalso important to know the classification of the wellbefore and after drilling, the depths of individualstratigraphic and productive layers, and the type ofgeological formations crossed, to check if thesecorrespond to the sequences adopted for the basinmodel. If they differ, further analyses are needed. Thestratigraphic sequence at the well must also containany information on samples of rock (cores) and fluidstaken, and the information required to find these or theanalyses carried out on them.

A second set of well data is represented by welllogs (electrical, acoustic and radioactive logs). Wheredata from the original logs exist, any reprocessingneeded for specific objectives can be undertaken.Considerable difficulties were encountered, forexample, in finding and reading Russian logs, whichwere recorded in formats different from those used byWestern companies and which therefore requiredreprocessing.

Another set of data is seismic data. Often thedocumentation provided for the bid round containsonly paper copies of seismic sections, which are of useonly for a preliminary and very general interpretation.Once rights to the area, with specific workcommitments, have been obtained, the originalrecordings (field data) are needed in order to carry outany necessary reprocessing. Above all, the differentsets of data must be compatible with one another;surveys from different seismic campaigns must be

165VOLUME I / EXPLORATION, PRODUCTION AND TRANSPORT

PROGRAMMING EXPLORATION ACTIVITY

rendered uniform, it is also important to ensure thatthe acquisition parameters are sufficient to proceedwith specific studies aimed at pursuing explorationobjectives.

The need to obtain a set of historical data within ashort space of time is often a critical aspect for manycompanies. The volume of data needed to prepare aproject may be extremely large, and the time requiredto find it extremely long. These delays often result in aseries of inefficiencies in the process, especially in thetransition from the exploration to the developmentphase. Moreover, the databases belonging to individualprojects are often unable to ‘talk’ to one another, andthus tend to become obsolete. Many companies havetherefore felt the need to develop databases whichremain stable over time, and which guaranteecompatibility with individual projects on the one hand,and with regional information (supplied by theaforementioned international service companies) onthe other, using a series of codified procedures toupload and manage all the information.

2.1.3 Selecting areas

The core business of an oil company is finding,producing and selling hydrocarbons and their by-products. The company’s most important activities aretherefore operations which allow it to activateavailable reserves by managing known reservoirs, andto replace the quantity of hydrocarbons produced withnew reserves. The hydrocarbon reserves (oil and gas)produced are generally replaced by a) discovering newreservoirs or broadening earlier discoveries; b) increasing the recovery of hydrocarbons fromreservoirs already in production; c) acquisition ofreservoirs from other oil companies.

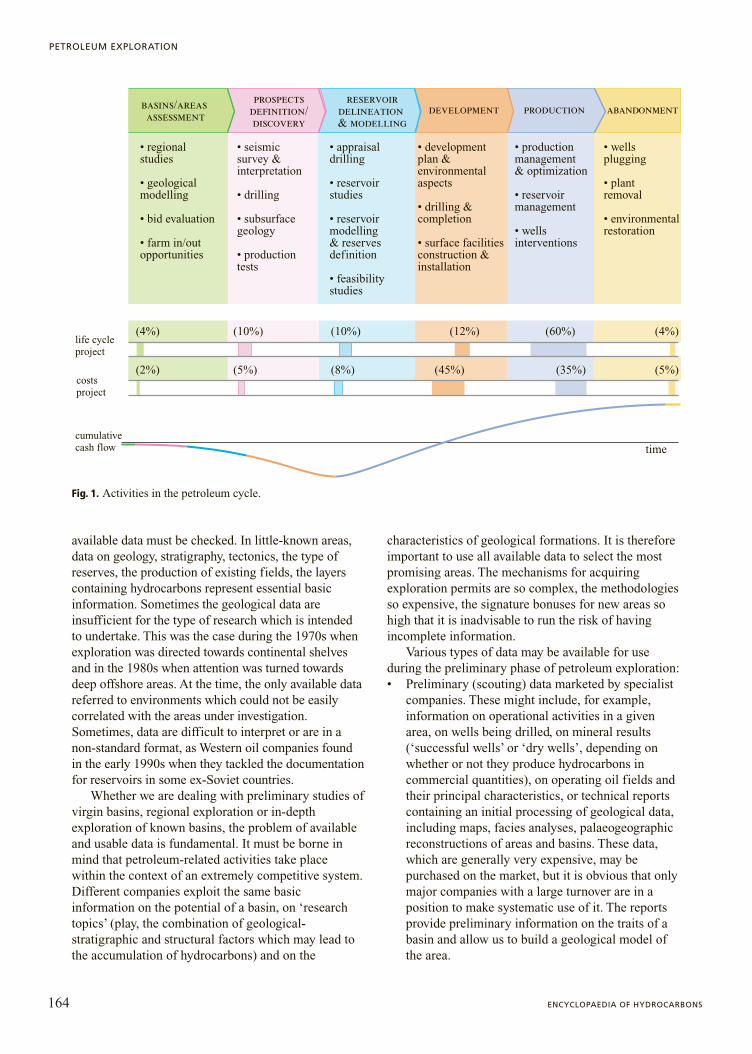

For an oil company the percentage of reservesreplaced with the three methodologies mentionedabove may vary over the years (Fig. 2); the discovery ofnew reservoirs is usually the most effective system.

The first stage in the petroleum cycle, exploration,aims to discover new reserves, and takes place in twodistinct phases: regional exploration and in-depth (ordetailed) exploration.

Regional exploration has the role of examiningsedimentary basins to indicate traits conducive to thegeneration, accumulation and preservation ofhydrocarbons. In-depth exploration focuses onselected smaller areas (covered by explorationpermits) where classic exploration methods can beused. These aim to make a direct study of the prospect(a potential structural or stratigraphic trap describedand located using geological and geophysical data, andforming part of a given play). The study of an

unexplored basin, where no data on previousdiscoveries are available, aims to assess the possibilitythat conditions conducive to the generation ofhydrocarbons exist. Where available geological data donot allow us to assume that rocks capable ofgenerating hydrocarbons are present, any futureactivity is compromised. Where the response ispositive, it is important to attempt an evaluation of thesize of accumulations in the exploration area, and thusthe potential for future economic success. Theexplorationist can suggest the acquisition of an areaonly on the basis of a careful evaluation (of the natureof the basin, the number and size of possiblereservoirs, the possible types of play found).

Preliminary evaluation of resourcesThe characteristics of a hypothetical reservoir in a

basin must be predicted on a statistically reliable basisin order for the model to have any meaning. Whenpreliminary geological data are available, the possibleresponses are probabilistic, in the sense that all theinformation inserted into the geological model ishypothetical, deriving from a series of observationsgenerally made in different parts of the basin, oftendistant from one another. Without going into excessivedetail, it is sufficient to know that parameters such asthe thickness of a mineralized layer in an area, theporosity values of a layer, the geometrical closure of aprospect, the height of the assumed hydrocarboncolumn, the reserves within a basin’s reservoirs, maysupply a probability or relative frequency distribution.This can be plotted on a graph, with the values of the

166 ENCYCLOPAEDIA OF HYDROCARBONS

PETROLEUM EXPLORATION

100

200

01998 1999 2000 2001 2002

%

discoveries revision and recovery improvement

acquisition

Fig. 2. Example of the replacement of reserves in a medium-sized oil company over a five-year period.

parameter on the x axis, and the probability or relativefrequency with which the parameter assumes thesevalues on the y axis. Probability distributions may alsobe represented as cumulative curves: in this case theclasses of values are still represented on the x axis,with the y axis showing the probability of a givenvalue being exceeded (Rose, 1992; Megill, 1992). Thistype of graph allows us to show the probability that aparameter assumes a value within a given intervalcompatible with available data.

When a basin is analysed, even before interpretingany seismic data which have been found, its overallpotential is estimated. Some methods for estimatingthe resources of a basin described in the literature(White and Gehman, 1979) are, for example,geological analogy, the Delphi method, areal andvolumetric yield, the number and size of fields, andthe extrapolation of discovery rates.

Geological analogy. This is the most basic method,and that which historically has been most widely used.It starts from the assumption that basins with similargeological characteristics have the same hydrocarboncontent. This type of evaluation makes use of anextremely complex basin classification system, basedon a number of parameters used as points ofcomparison. In fact, geological analogy is a cognitiveapproach common to all evaluation methods, since itanalyses the conditions for the formation of the basin,its evolution, and direct (analysed) and indirect(hypothetical) elements. Often the disappointingresults obtained by applying this method are due to thefailure to assess the importance of individual elementswithin a broader context.

The Delphi method. This method takes account ofthe opinion of a group of experts who examine thearea and express individual opinions on the probabledistribution of petroleum potential. These differentevaluations come together in a final report which takesaccount of the different points of view. This methodhas been used particularly in Canada and by theUnited States Geological Survey.

The areal yield method. It involves multiplying theeffective area (potential) of a basin by the unitproduction of a known productive area. Thedisadvantage of this method is that it fails to take intoaccount the third dimension (depth).

The volumetric yield method. It takes intoconsideration the thickness of the reservoir as well asof the effective area. This approach to evaluation maybe reliable on a regional scale in the early stages ofexploration when little data are available, takingaccount of specific parameters such as the type anddistribution of reservoir rock or the distribution andthickness of source rocks. However, it may bemisleading if the information used is not consolidated,

extending to the entire basin local situations which arenot confirmed by exploration.

The geochemical evaluation approach. Thisvolumetric model, widely used by Soviet geologists,takes account of the basin’s organic contents and itscomposition during the various stages of migrationand preservation in order to define the postulatedaccumulation. The greatest difficulty lies in creating ahypothetical model without an adequate understandingof migration pathways and the quantities ofhydrocarbons which actually migrated and becametrapped.

The field size distribution method. It analyses thedistribution of reservoirs discovered on the basis oftheir size. The distribution of prospects must followthe same pattern found for the reservoirs, so as toapply the same probabilistic estimation approach tothem. In order to use this method satisfactorily, a largequantity of data is required.

Extrapolation of discovery rates. It has been usedfor forecasting with limitations due to the fact thatunexplored areas, on which detailed information arenot available, are difficult to insert into a probabilisticforecast.

Each of these evaluation methods has advantagesand gaps, especially in the phase of comparisonbetween different basins, where similarities are oftenevident, but points of divergence, far more important,are much less obvious.

Degree of exploration knowledge of a basinFrom the point of view of exploration, every

sedimentary basin may find itself in a different stageof ‘operational maturity’ (Royal Dutch-Shell Group ofCompanies, 1987); consequently, knowledge of thebasin and related exploration topics may be more orless exhaustive.

Preliminary Stage. Pratt’s statement (1937; 1944)that “oil is in the minds of men” is well-suited to thepreliminary stage of the exploration process, whendata are scarce or barely existent, neighbouring areasof little help, the depth of water sometimes prohibitive,direct geological knowledge non-existent, and whenthe petroleum system can only be hypothesized on thebasis of analogies. This was the case, for example, forthe Angolan deep offshore in the early 1990s, or thesea off the Nile delta, where an attempt was made tobuild a geological model with only a few seismic linesavailable.

Initial Stage. Our knowledge increases when thoseoperating in the basin attempt to formulate hypotheseson petroleum characteristics, the type of trap and thetechniques most suited to our objectives. In this phaseit is important to find keys to interpretation. For thisreason, the first control wells are drilled, allowing us

167VOLUME I / EXPLORATION, PRODUCTION AND TRANSPORT

PROGRAMMING EXPLORATION ACTIVITY

to test the models developed. For example, thediscovery of turbidite channels in the Angolan deepoffshore led to a long series of exploration successes.

Mature Stage. The model has been perfected.Discovery rates and the quantities of hydrocarbonsshown at each well remain constant over a certainnumber of years. Exploration techniques (acquisition,processing, interpretation) are consolidated. This is themature phase of basin exploration.

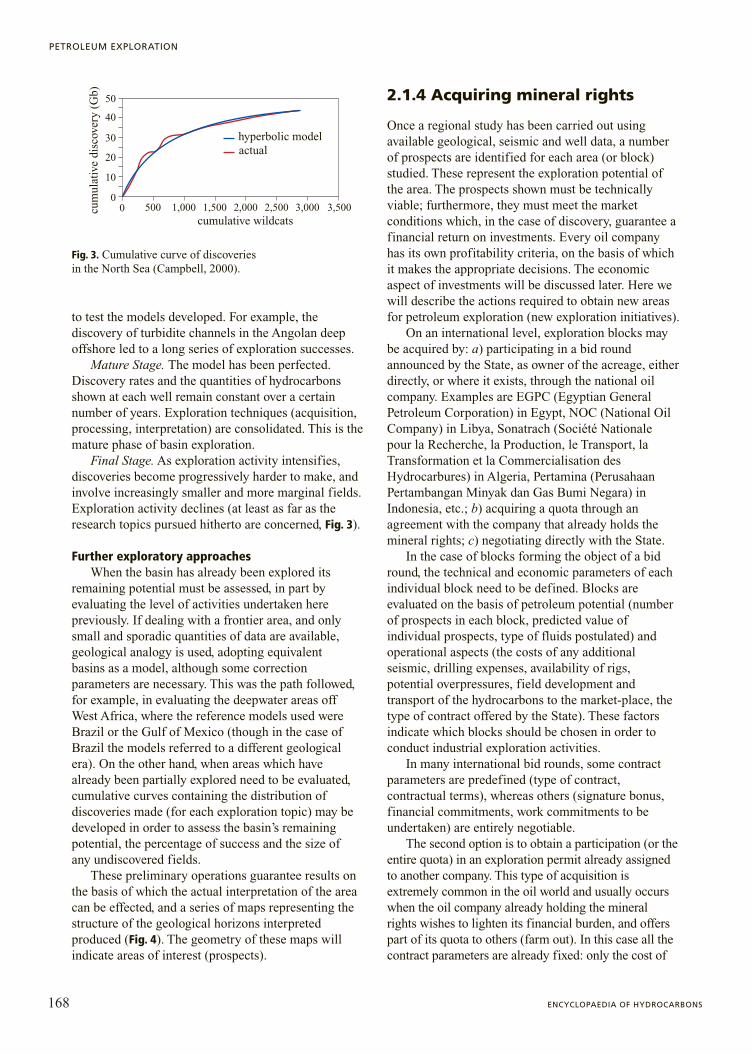

Final Stage. As exploration activity intensifies,discoveries become progressively harder to make, andinvolve increasingly smaller and more marginal fields.Exploration activity declines (at least as far as theresearch topics pursued hitherto are concerned, Fig. 3).

Further exploratory approachesWhen the basin has already been explored its

remaining potential must be assessed, in part byevaluating the level of activities undertaken herepreviously. If dealing with a frontier area, and onlysmall and sporadic quantities of data are available,geological analogy is used, adopting equivalentbasins as a model, although some correctionparameters are necessary. This was the path followed,for example, in evaluating the deepwater areas offWest Africa, where the reference models used wereBrazil or the Gulf of Mexico (though in the case ofBrazil the models referred to a different geologicalera). On the other hand, when areas which havealready been partially explored need to be evaluated,cumulative curves containing the distribution ofdiscoveries made (for each exploration topic) may bedeveloped in order to assess the basin’s remainingpotential, the percentage of success and the size ofany undiscovered fields.

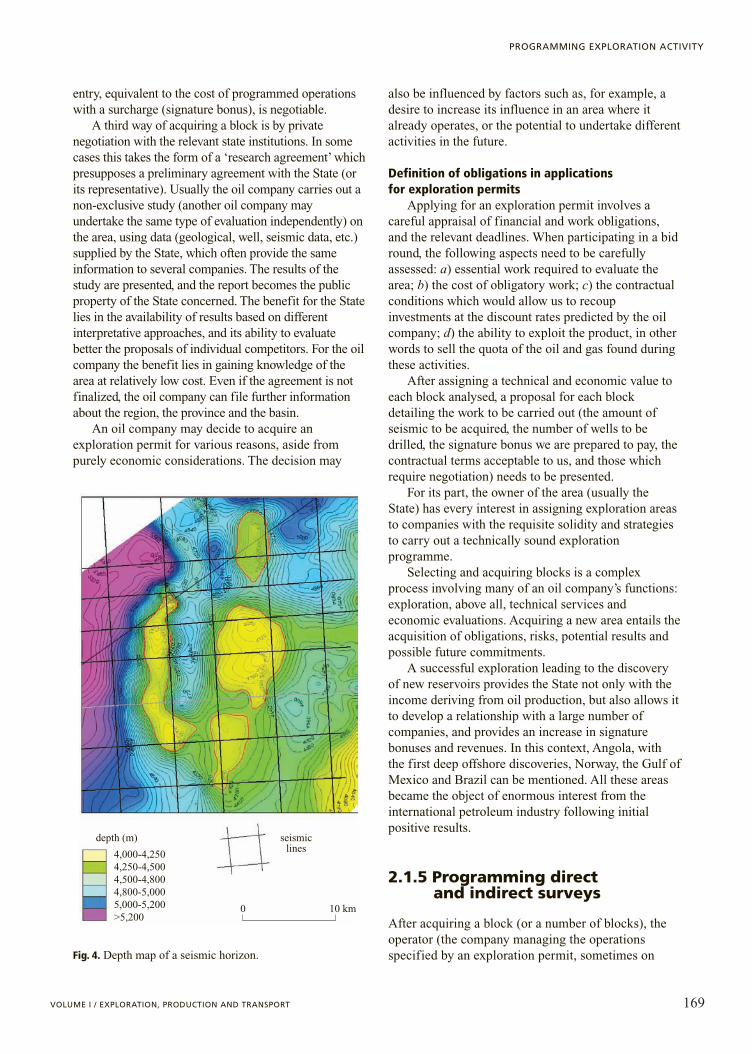

These preliminary operations guarantee results onthe basis of which the actual interpretation of the areacan be effected, and a series of maps representing thestructure of the geological horizons interpretedproduced (Fig. 4). The geometry of these maps willindicate areas of interest (prospects).

2.1.4 Acquiring mineral rights

Once a regional study has been carried out usingavailable geological, seismic and well data, a numberof prospects are identified for each area (or block)studied. These represent the exploration potential ofthe area. The prospects shown must be technicallyviable; furthermore, they must meet the marketconditions which, in the case of discovery, guarantee afinancial return on investments. Every oil companyhas its own profitability criteria, on the basis of whichit makes the appropriate decisions. The economicaspect of investments will be discussed later. Here wewill describe the actions required to obtain new areasfor petroleum exploration (new exploration initiatives).

On an international level, exploration blocks maybe acquired by: a) participating in a bid roundannounced by the State, as owner of the acreage, eitherdirectly, or where it exists, through the national oilcompany. Examples are EGPC (Egyptian GeneralPetroleum Corporation) in Egypt, NOC (National OilCompany) in Libya, Sonatrach (Société Nationalepour la Recherche, la Production, le Transport, laTransformation et la Commercialisation desHydrocarbures) in Algeria, Pertamina (PerusahaanPertambangan Minyak dan Gas Bumi Negara) inIndonesia, etc.; b) acquiring a quota through anagreement with the company that already holds themineral rights; c) negotiating directly with the State.

In the case of blocks forming the object of a bidround, the technical and economic parameters of eachindividual block need to be defined. Blocks areevaluated on the basis of petroleum potential (numberof prospects in each block, predicted value ofindividual prospects, type of fluids postulated) andoperational aspects (the costs of any additionalseismic, drilling expenses, availability of rigs,potential overpressures, field development andtransport of the hydrocarbons to the market-place, thetype of contract offered by the State). These factorsindicate which blocks should be chosen in order toconduct industrial exploration activities.

In many international bid rounds, some contractparameters are predefined (type of contract,contractual terms), whereas others (signature bonus,financial commitments, work commitments to beundertaken) are entirely negotiable.

The second option is to obtain a participation (or theentire quota) in an exploration permit already assignedto another company. This type of acquisition isextremely common in the oil world and usually occurswhen the oil company already holding the mineralrights wishes to lighten its financial burden, and offerspart of its quota to others (farm out). In this case all thecontract parameters are already fixed: only the cost of

168 ENCYCLOPAEDIA OF HYDROCARBONS

PETROLEUM EXPLORATION

0

50

30

40

20

10

hyperbolic modelactual

cum

ulat

ive

disc

over

y (G

b)

cumulative wildcats0 500 1,000 1,500 2,000 2,500 3,000 3,500

Fig. 3. Cumulative curve of discoveries in the North Sea (Campbell, 2000).

entry, equivalent to the cost of programmed operationswith a surcharge (signature bonus), is negotiable.

A third way of acquiring a block is by privatenegotiation with the relevant state institutions. In somecases this takes the form of a ‘research agreement’ whichpresupposes a preliminary agreement with the State (orits representative). Usually the oil company carries out anon-exclusive study (another oil company mayundertake the same type of evaluation independently) onthe area, using data (geological, well, seismic data, etc.)supplied by the State, which often provide the sameinformation to several companies. The results of thestudy are presented, and the report becomes the publicproperty of the State concerned. The benefit for the Statelies in the availability of results based on differentinterpretative approaches, and its ability to evaluatebetter the proposals of individual competitors. For the oilcompany the benefit lies in gaining knowledge of thearea at relatively low cost. Even if the agreement is notfinalized, the oil company can file further informationabout the region, the province and the basin.

An oil company may decide to acquire anexploration permit for various reasons, aside frompurely economic considerations. The decision may

also be influenced by factors such as, for example, adesire to increase its influence in an area where italready operates, or the potential to undertake differentactivities in the future.

Definition of obligations in applications for exploration permits

Applying for an exploration permit involves acareful appraisal of financial and work obligations,and the relevant deadlines. When participating in a bidround, the following aspects need to be carefullyassessed: a) essential work required to evaluate thearea; b) the cost of obligatory work; c) the contractualconditions which would allow us to recoupinvestments at the discount rates predicted by the oilcompany; d) the ability to exploit the product, in otherwords to sell the quota of the oil and gas found duringthese activities.

After assigning a technical and economic value toeach block analysed, a proposal for each blockdetailing the work to be carried out (the amount ofseismic to be acquired, the number of wells to bedrilled, the signature bonus we are prepared to pay, thecontractual terms acceptable to us, and those whichrequire negotiation) needs to be presented.

For its part, the owner of the area (usually theState) has every interest in assigning exploration areasto companies with the requisite solidity and strategiesto carry out a technically sound explorationprogramme.

Selecting and acquiring blocks is a complexprocess involving many of an oil company’s functions:exploration, above all, technical services andeconomic evaluations. Acquiring a new area entails theacquisition of obligations, risks, potential results andpossible future commitments.

A successful exploration leading to the discoveryof new reservoirs provides the State not only with theincome deriving from oil production, but also allows itto develop a relationship with a large number ofcompanies, and provides an increase in signaturebonuses and revenues. In this context, Angola, withthe first deep offshore discoveries, Norway, the Gulf ofMexico and Brazil can be mentioned. All these areasbecame the object of enormous interest from theinternational petroleum industry following initialpositive results.

2.1.5 Programming direct and indirect surveys

After acquiring a block (or a number of blocks), theoperator (the company managing the operationsspecified by an exploration permit, sometimes on

169VOLUME I / EXPLORATION, PRODUCTION AND TRANSPORT

PROGRAMMING EXPLORATION ACTIVITY

0 10 km

depth (m) seismiclines

4,000-4,2504,250-4,5004,500-4,8004,800-5,0005,000-5,200>5,200

Fig. 4. Depth map of a seismic horizon.

behalf of other companies associated in a consortiumor joint venture) must honour a series ofcommitments set out by the contract, within a periodof validity and respecting a series of predetermineddeadlines (Fig. 5).

Validity period of the permitThe validity of a permit is generally broken into

three periods. The first period usually lasts three or fouryears, and the second and third periods one or two yearseach. This variation in length depends on the locationand logistic conditions of the block concerned, whichmay be in an inaccessible area, or in deep water.

The first validity period (Fig. 5 shows a permitwith a first period of four years, and second and thirdperiods of two years each) is obligatory, and for itsduration the company which has obtained mineralrights takes on a number of work obligations (a givennumber of kilometres of seismic to be acquired and agiven number of wells to be drilled). If theseobligations are not met, sanctions are incurred.

At the end of each exploration period the ownermust release part of the area (normally around 25-30%of the initial acreage) so as to avoid penalizingexploration in the area by others. This aspect must alsobe taken into consideration: the area needs to beexplored as fully as possible in order to avoid releasingpotential remaining reserves.

The second and third periods are optional. Afteranalysing the results of drilling during the first period,the owner decides whether or not to ‘enter’ the second(and subsequently the third) period, thereby taking onthe obligation to carry out further exploration and theresulting financial commitments.

This decision is especially difficult whereexploration results are disappointing and the wellsdrilled turn out to be dry. In this situation it is only

appropriate to continue with the next phase ofexploration if there are other research interests beyondthose already pursued.

Another aspect covered by the exploration permitconcerns the consequences of a discovery, with thetransformation of the area into a ‘development lease’.Leases have a much longer validity period (twenty orthirty years), since producing the reservoir discoveredrequires a series of operations (evaluation of theaccumulation discovered, formulation of adevelopment plan), often with the direct contributionof the State, which may have a participation quota inthe joint venture.

During the exploration period, costs are borneentirely by the operator; if exploration is unsuccessful,they remain at the company’s expense. If there is apetroleum success, the operator and the State (the latterpotentially through the national oil company) set up amixed company to produce the field. This mixedcompany, which is generally non-profit, has the task ofmanaging the reservoir discovered, producing it andselling the product on behalf of the two shareholders. Inthis case the operator may obtain a reimbursement ofexpenditure and participate in profits from operations.

The work programme is defined in the agreement,both as concerns operational activities (in particular theamount of seismic needed to delineate the areas ofmineral interest), and the number of wells to be drilled.Furthermore, the minimum depth or the geologicallayers which must be reached by drilling are specified,in order to commit the operator to a strict workprogramme. This avoids the risk of keeping the areafrozen during the entire exploration period, without therequisite mineral evaluations being completed.

Drafting the exploration programme is a teameffort involving the participation of all the specialistsworking on different aspects of the project, including

170 ENCYCLOPAEDIA OF HYDROCARBONS

PETROLEUM EXPLORATION

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

1

1 2 3 4

2

3

4

YEARS

explorationperiods

work obligation

minimumexpenditures

relinquishment

1st period

16 million dollars

2 million dollars

20million dollars

10million dollars

30% of original area

30% oforiginal area

2 wells 1 well

2nd period(optional)

3rd period(optional)

1,000 km 2D2,000 km2 3D 1 well

24-01-2000 effective date23-01-2004 exp. date 1st period23-01-2006 exp. date 2nd period23-01-2008 exp. date 3rd period

original area: 7,000 km2

signature bonus

Fig. 5. Example of an exploration permit: exploration periods, work obligations and financial commitments.

the feasibility study, the geophysical survey, surveyingparameters and the recording of well logs.

The sequence of activities covered by anexploration permit is fairly uniform, and involves thecreation of a database, the analysis of available data,the programming of mapping, geological andphotogeological surveys, seismic surveys, theinterpretation of seismic data, the choice of welllocations, drilling, the analysis of results and thedecision as to whether or not to proceed with theapplication for a lease or to release the area after acomplete exploration.

In mountainous areas such as the Cordillera of theAndes, the Caucasus or internal basins in China,surface geology may still play an important role.Offshore, other surveying methods, especiallygeophysics, are used from the outset.

Each of the activities listed takes place within aspecific time-frame (for example the start date for theseismic survey or the drilling of the first explorationwell) which represents an integral part of theagreement with the State. Furthermore, whilst draftinga work plan, it is important to forecast the length oftime required to interpret the data, so as to act in timeto find a drilling rig on the market suited to thedrilling of the well, predict the costs of all theoperations and ensure that sufficient funds areavailable to cover these.

Seismic surveys, which are the most frequentlyused and consolidated methodology, may haveextremely variable execution times. Onshore and inimpervious areas, given the high cost of field surveys,the acquisition often takes place in several phases: aregional large-scale survey followed by in-depthsurveys of areas which turn out to be of interest.Offshore, seismic surveys are easier to carry out. Fromthe mid 1980s, pioneered by Shell, the petroleum

industry began to acquire three-dimensional surveys oflarge areas during the initial phases of exploration, soas to have at their disposal a large volume of data, alsouseful in case of discovery.

Each time topographic, geophysical or drillingwork is assigned to a service company, this is precededby an evaluation of the prices and of the potentialquality of the service. Often, especially offshore,teams available near the survey area must be ensured,so as to avoid the high cost of mobilizing the boatsneeded to carry out seismic surveys.

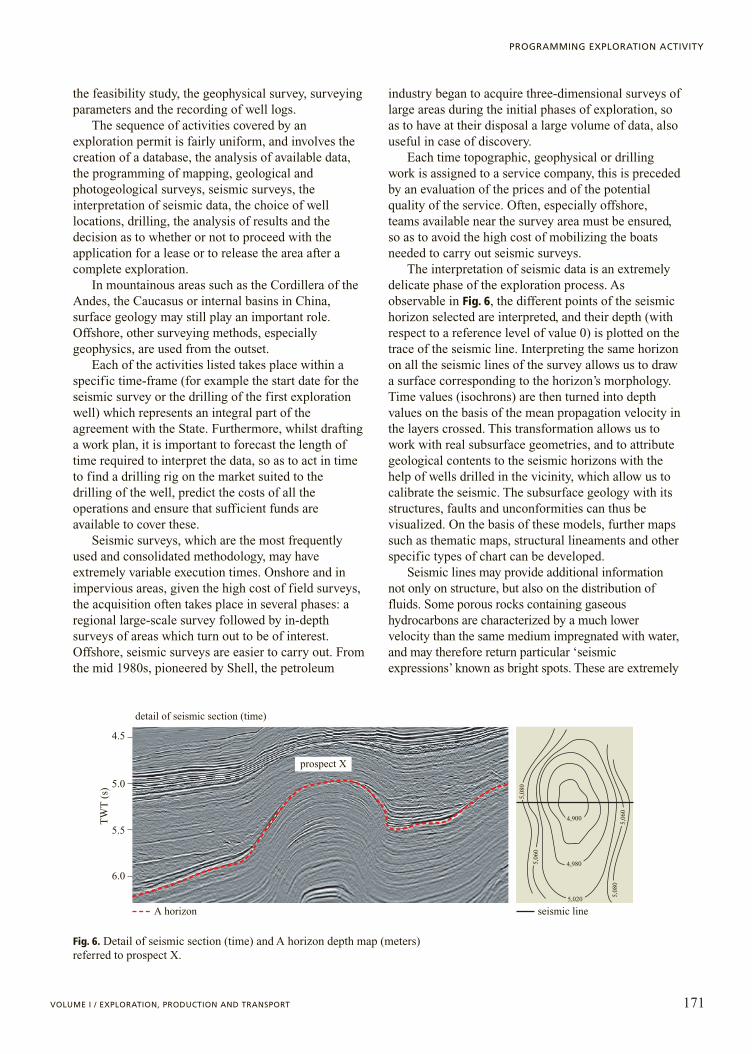

The interpretation of seismic data is an extremelydelicate phase of the exploration process. Asobservable in Fig. 6, the different points of the seismichorizon selected are interpreted, and their depth (withrespect to a reference level of value 0) is plotted on thetrace of the seismic line. Interpreting the same horizonon all the seismic lines of the survey allows us to drawa surface corresponding to the horizon’s morphology.Time values (isochrons) are then turned into depthvalues on the basis of the mean propagation velocity inthe layers crossed. This transformation allows us towork with real subsurface geometries, and to attributegeological contents to the seismic horizons with thehelp of wells drilled in the vicinity, which allow us tocalibrate the seismic. The subsurface geology with itsstructures, faults and unconformities can thus bevisualized. On the basis of these models, further mapssuch as thematic maps, structural lineaments and otherspecific types of chart can be developed.

Seismic lines may provide additional informationnot only on structure, but also on the distribution offluids. Some porous rocks containing gaseoushydrocarbons are characterized by a much lowervelocity than the same medium impregnated with water,and may therefore return particular ‘seismicexpressions’ known as bright spots. These are extremely

171VOLUME I / EXPLORATION, PRODUCTION AND TRANSPORT

PROGRAMMING EXPLORATION ACTIVITY

prospect X

TW

T (

s)

A horizon seismic line

4.5

5.0

5.5

6.0

5,06

0

5,08

0

5,06

0

5,08

0

5,020

4,980

4,900

detail of seismic section (time)

Fig. 6. Detail of seismic section (time) and A horizon depth map (meters)referred to prospect X.

useful for a preliminary definition of areas of interest.The final result of the interpretation consists of

maps (isobaths) forming a geometrical expression ofthe different seismic horizons studied (see again Fig. 4). The presence of crests, culminations, etc. (so-called ‘structural highs’) indicates areas ofprobable interest (if made up of a porous nucleus andan impermeable seal, and charged with hydrocarbonsgenerated by source rocks).

If the structural conditions shown are notsupported by sufficient seismic evidence, they areknown as leads. To turn a lead into a prospect, theseismic information must be completed withadditional surveys.

The various prospects are listed in order ofimportance, on the basis of the parameters shown(volume, structural closure, vicinity to the basin wherethe hydrocarbons were generated).

In the example shown in Fig. 5, the first explorationperiod involves the obligatory drilling of one well; it istherefore needed to choose which of the differentprospects shown to drill. It is worth bearing in mind thatthe well alone allows us to check whether the geologicalmodel developed is correct, or whether the programmerequires modifications during later exploration work.

After identifying the prospect to be drilled and thecoordinates where the drilling rig will be placed, somepreliminary work must be carried out before drillingcan start. For onshore wells, the area where the drillingrig will be installed with all its support structures isprepared. If the well is offshore, a seismic survey ofthe sea floor (bottom survey) in the area selected needsto be carried out. This allows us to check themorphological conditions of the sea floor where therig is to be positioned, and to indicate the potentialpresence of gas in the upper layers which mayrepresent a safety issue during drilling.

The drilling of the well presupposes a programmeand the choice of a rig suited to this programme. Theprogramme, formulated by the exploration team, setsout the predicted depths of the rock formations to becrossed, the geological characterization of seismichorizons, the mineral objectives, the overpressures. Thisdocument also provides the information upon which thedrilling programme must be based (drill bits, tubing,muds, etc.). It is the task of exploration to establish thesedimentary sequences in which to take core samples,the frequency with which drill cuttings should beanalysed, the type of logs and any measurement ofseismic velocities in the well. On the basis of therecordings made in the wells, and any hydrocarbonshows recorded during drilling, it must be decidedwhich layers are to be ‘sampled’ using production testsbased on the direct recovery of fluids from themineralized layer and pressure measurements.

2.1.6 Analysing petroleumpotential

Evaluating the prospect before drilling the wellPetroleum risk and geological success. Petroleum

exploration, as stressed on several occasions, has aninherent element of risk, since it operates on the basisof probabilistic scenarios. It is never certain that a wellwill lead to the discovery of hydrocarbons, even if thegeological model contains all the parameter for this tobe the case. This element of risk cannot be avoided,but it can be successfully managed to optimize results.

For each prospect shown (Fig. 7; see again Fig. 6),a number of factors allowing us to quantify theprobability of success (discovery of hydrocarbons) orfailure (dry well) must therefore be taken into account.In some cases, an idea of the probability of success indrilling a well in a given basin can be obtained byusing historical statistics on past wells drilled in thearea; however, this method is not particularly reliable.

A number of conditions are required for anaccumulation to form: the presence of a source rockable to generate and release hydrocarbons; a pathwayallowing the hydrocarbons to migrate; the presence ofa reservoir rock, covered by an impermeable seal, tocapture and preserve the hydrocarbons after migration.

If just one of these elements is lacking, theprobability of finding hydrocarbons is virtually nil. Thepresence of each of these conditions, in the relevantgeological period, is associated with a probability: theproduct of these probabilities gives the probability ofsuccessful hydrocarbon discovery. In a prospect wherethe estimated probability that a mature source rockexists is 70%, that the prospect is charged is 60% andthat the trap exists in the correct geological era is 50%,the probability of geological success (in other wordsthat the well will find hydrocarbons) is 21%.

A correct assessment of petroleum risk thereforerequires us to take two aspects into account. The firstis the geological model, while the second aspect islinked to the quality of the available data used to buildthe geological model: the volume of geological data,the quality and type of seismic and other geophysicalevidence used, the number of wells analysed.Combining all these elements allows us to check theeffectiveness in a prospect of all the components of thepetroleum system (generation of hydrocarbons,migration, trapping and preservation) and to estimatethe probability of success.

There are numerous reasons why a well may turnout to be dry: absence of the geological structure,inadequate sealing, absence of reservoir rock, absenceof porosity or permeability, failure of hydrocarbons toaccumulate or generate, etc. The map of the prospectitself often contains subjective elements, and may vary

172 ENCYCLOPAEDIA OF HYDROCARBONS

PETROLEUM EXPLORATION

according to the different interpretative modelsadopted by individual specialists, who producediffering maps on the basis of identical data. Thegeophysical interpretation also conditions the model ofmigration, drainage pathways and watersheds; allelements which contribute to the description of apetroleum system. The mechanism of charging andaccumulation is not a simple one: there are caseswhere, though hydrocarbons are generated, migrationconditions are such that they are unable to fill the trap.In the field of basin geology there are a series ofstudies providing a numerical simulation of petroleumsystems which allow us to better define the history ofthe maturing, release and migration of hydrocarbonsand the charging phases of the various prospects. Inthe case of prospects with multiple objectives, theprobability of achieving at least one of the goalsidentified increases. In any case, the probabilitiescannot be summed because the elements considered areindependent. The explorationist must avoid introducingsecondary objectives into the programme; in otherwords those relating to minor accumulations presentwithin the structure, or at greater depth, whose modestdimensions fail to justify the cost of additional work.

The oil industry uses various systems to evaluaterisk. These range from the basic elements describedhere to far more complex systems which take accountnot only of the geological model, but also of theinformation model (in other words the type andaccuracy of data used). When appropriately weightedthese allow us to express risk numerically.

Estimating the reserves in the prospect. Hitherto theproblem of petroleum success has been consideredwithout defining what success means in terms ofaccumulation size. In a frontier area, in an unexploredbasin, a well which finds hydrocarbons even in minimal

quantities is important, since it confirms that thegeneration of hydrocarbons has occurred, and thusinvites operators to define other evaluation parametersand continue exploration in the area. However, undernormal conditions, in known basins, a show ofhydrocarbons in a well cannot necessarily be describedas a success. We can speak of success only when thewell discovers an accumulation of hydrocarbonssufficient to be produced, and if it meets the specificcommercial requirements established by SEC (Securitiesand Exchange Commission) regulations. As such, beforeinvesting in the drilling of one or more prospects theexpected size of reserves needs to be specified.

The hydrocarbon accumulation can be easilyestimated using the available elements (geologicaldata, seismic interpretation, data on wells previouslydrilled in the area), and on the basis of the volume ofthe trap multiplied by various factors (includingporosity, the thickness of porous rock, the hydrocarbonsaturation, the recovery factor, etc.). However, giventhat none of these data are measured directly, norchecked experimentally, it is obvious that everymagnitude concerned is a postulation based on amodel into which available regional data are inserted.Factors such as porosity, the height of the hydrocarboncolumn and the size of the mineralized area aredefined by a probability distribution with a minimumvalue, a maximum value, and a value considered mostlikely. Given the small amount of data generallyavailable, a simplified distribution for each element isoften used (porosity, thickness of the mineralizedlayer, hydrocarbon saturation, etc.). Combining thesedistributions using the Montecarlo method provides aprobabilistic distribution with several variables for thevalues relating to the expected reserves.

The analysis of a number of prospects included ina drilling programme allows us to estimate the numberof discoveries and the resulting additional reserves.The greater the number of prospects to drill, the morereliable the result.

Economic evaluation. To conclude this chapter onrisk analysis and on the probabilistic distribution ofpostulated reserves in the prospect, it must be borne inmind that oil exploitation is an industry, and istherefore governed by the profitability of investments.It is thus obvious that the entire process describedabove must be considered within an economic context,and that every exploration operation must be evaluatedaccording to this criterion. We will describe theeconomic aspects of exploration in detail later on. Hereit is briefly outlined what is intended by the economicvalue of a prospect. This evaluation is carried out onthe basis of a series of development scenarios (for thereserves), each associated with a risk factor. The finalresult is the EMV (Expected Monetary Value), which

173VOLUME I / EXPLORATION, PRODUCTION AND TRANSPORT

PROGRAMMING EXPLORATION ACTIVITY

CB

A

D

C B A D

possible probable proven potential

oil-water contact

field prospect

oil-water contact

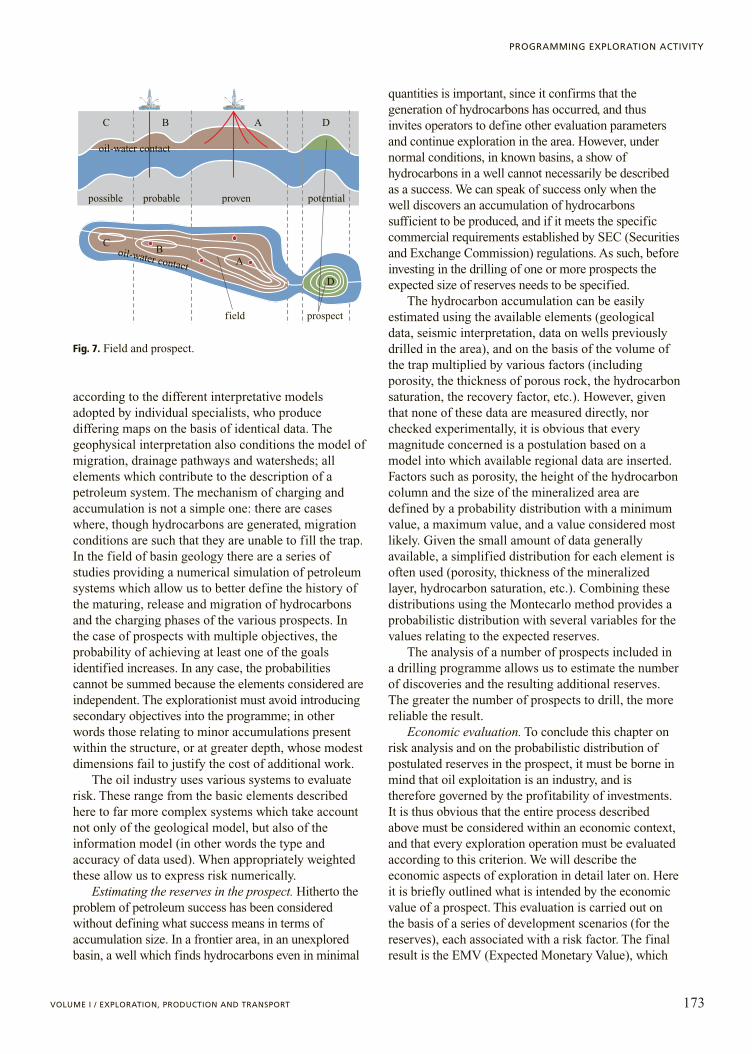

Fig. 7. Field and prospect.

takes account of all the geological, technical andeconomic variables of the project, and is expressed by anumber. This value is particularly useful when it isnecessary to assess and compare exploration projectsof different origin, or to allocate investmentsappropriately in order to decide how to distributefunding for individual drilling activities.

Post-drilling evaluation of resultsPost-drilling analyses. The evaluation process

which follows drilling (post-drilling) is an extremelyimportant phase in the exploration project since itallows us to use the results of exploration for industrialpurposes.

The first step is the analysis of the wells drilled,which permits to test the geological modelexperimentally. The results obtained by drillingindicate whether the initial hypotheses on the depths ofthe geological horizons, their consistencies andporosities, the type of lithology and the presence ofhydrocarbons in given layers were correct, or whethervariations are found. The data emerging from well

analysis are carefully evaluated and compared with theparameters used to generate the prospect. This type ofevaluation should be carried out systematically forboth mineralized and dry wells. Obviously, dry wellsrequire more in-depth treatment. An understanding ofthe causes of failure and of volumetric discrepanciesoften leads to a new interpretation of the data whichhighlights the strong and weak points of the process ofgenerating and evaluating prospects, and theassociated risk.

The analysis of drilled wells may also provideimportant information on the distribution of the majorcauses of failure. The identification of systematiccauses of failure may allow us to single out individualcritical points in work flows, or in the application oftechnologies.

Furthermore, statistical analysis of results mayindicate whether the methods used to assess risk areaccurate. Analyses are truly valid only if made withina general operational context, and if they take intoaccount all the exploration wells drilled over a givenperiod.

174 ENCYCLOPAEDIA OF HYDROCARBONS

PETROLEUM EXPLORATION

1 2 3

4

6 5

? ?? ?

? ??

??

drilling for a new field on a structure or in anenvironment never before productive

drillingfor a new poolon a structure

or ina geologicalenvironment

alreadyproductive

drilling for long extension of a partly developed pool

drilling to exploit a hydrocarbon accumulationdiscovered by previous drilling

1 new-field wildcat

2 new-pool (pay)wildcat

3 deeper pool(pay) test

4 shallower pool(pay) test

5 outpost or extension test

6 development well

extension well

development well

dry outpost or dry extension test

dry development well

new-pool discoverywildcat

deeper pooldiscovery

well

shallower pooldiscovery

well

dry shallower pooltest

dry deeper pooltest

dry new-poolwildcat

drynew-pool

tests

new-pooldiscovery

wells

dry new-field wildcat

initialclassification

(when drilling is started)

final classification (after completion or abandonment)

successful unsuccessful

new pooltests

drilling outside limits ofa proved area of pool

drilling insidelimits

of provedarea of pool

for a new poolbelow

deepestproven pool

for a new poolabove

deepestproven pool

new-field discovery wildcat

objective of drilling

structureknown productive limits of proven pool

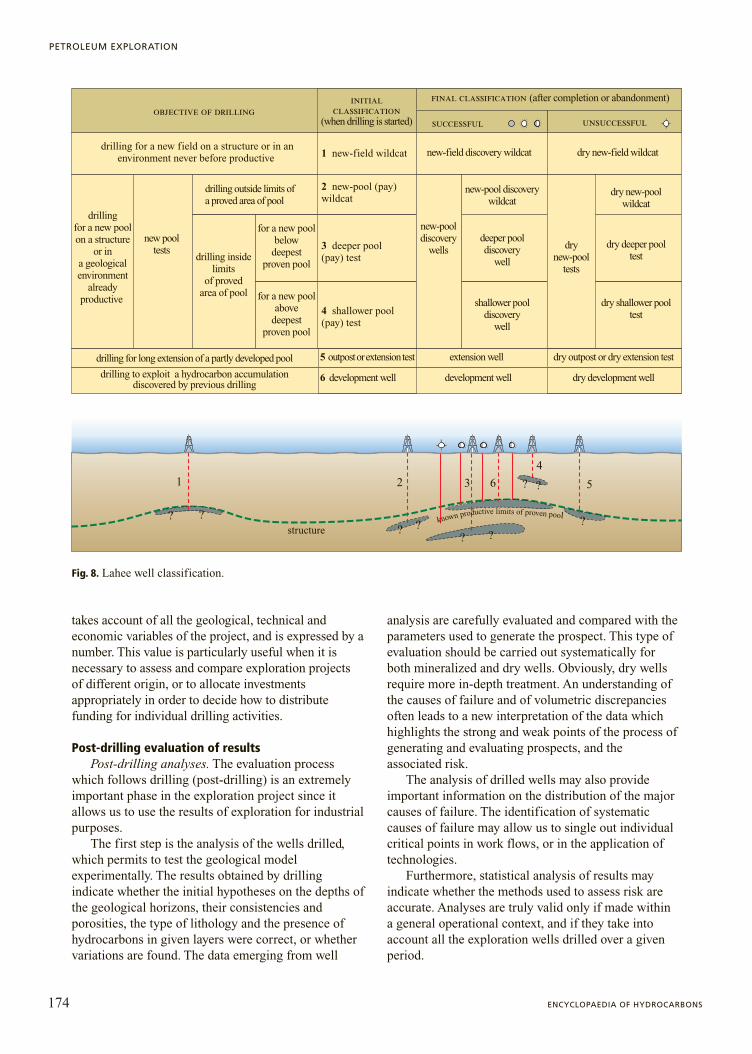

Fig. 8. Lahee well classification.

It has been shown, using a large number of wells(over 500), that: the number of successful wells inprospects with an estimated Probability Of Success(POS) below 20% is practically nil, whilst the numberof successful wells in prospects with an estimatedprobability of success over 20% is in line withforecasts.

This means that it is important to be very carefulwhen including prospects with an excessively low POSvalue in drilling programmes. If the well is successful,this represents the start of an evaluation process whichis able to turn hypothetical reserves into provedreserves, followed by the development of the reservoiror, where profitability does not meet the standards ofthe company, by the termination of furtherinvestments.

Well classification. Exploration wells are treateddifferently on the accountancy level, depending onwhether or not drilling was successful. The cost of drywells is expensed during the financial year in question,whereas that of successful wells is capitalized. It istherefore important to know the exact classificationattributed to the well before drilling, with respect tothe aim for which it is drilled (finding newaccumulations, deeper accumulations, verifying thesize of a known accumulation, or developing a field),and that assigned to it after drilling, which also takesaccount of results (success or failure).

Fig. 8 shows a schematic version of the Laheeclassification (1944) also used by the AAPG(American Association of Petroleum Geologists) andby the API (American Petroleum Institute). To thesecategories (successful wells and dry wells) a thirdcategory of wells defined as suspended should beadded. This category includes all those wells which,though having reached the depth specified by theprogramme at the end of each year, for various reasonscannot be classified (e.g. awaiting a production test).

Results of exploration and exploration reserves.The result of exploration is only partially representedby proved reserves in the year of discovery. After thefirst discovery well, doubts often remain as to thedistribution of petrophysical parameters and thegeometry of the structure drilled, with furtherassessments required to gain an accurate idea of thereserves.

During the pre-drilling evaluation, both thegeometry of the prospect and the size of reserves areestimated probabilistically.

Once the well has been drilled, an initial evaluationof the volume of hydrocarbons in place and a roughestimate of the recovery factor are formulated. Thesubsequent detailed technical analysis, in accordancewith the company’s development plan, permits to definethree different categories of reserves: proven, probable

and possible. Proven reserves are those consideredreliable and for which development is defined at certaineconomic conditions. Probable reserves are those likelyto be developed despite no precise developing projecthas been defined. Possible reserves are those uncertainfrom a technical point of view. It must also be borne inmind that, aside from the economic factors affecting thedefinition, only a small part of the structure – thatinvestigated by the well – can be considered technicallyverified (see again Fig. 7).

To conclude, we can say that the reservescalculated during the proper exploration phase requirea certain length of time to become certified andproducible.

The performance of oil companies. To measure theperformance of an oil company a list of regulations,which must be followed in the description of itseconomic results, has been created. This ensures thataccounts and results are published using uniformcriteria, and are therefore easy to read. A number ofindicators representing the performance of oilcompanies have been established. These describe howcompanies manage their core business of explorationand production, using investments in the optimal way.The results achieved by different oil companies on aninternational level can thus be compared. One importantfinancial indicator is the ROACE (Return On AverageCapital Employed), which measures the economicreturn on investments. Other important parameters –together with routine data such as oil and gasproduction and the quantity of available reserves in thevarious categories – for measuring technicalperformance are the Reserve Replacement Rate and theFinding Cost, which measures the ratio of investmentsin exploration and development to the proved additionalreserves deriving from these activities.

Some indicators refer more specifically toexploration. An example is the Rate Of Success (ROS),which calculates the number of successful wells out ofthe total number of wells drilled. In recent years,Exxon-Mobil, BP (British Petroleum), Shell, Chevron-Texaco, Total and Conoco-Phillips have achievedresults averaging over 50%, with peaks of 70%. Thisfact, extremely reassuring in statistical terms, showsthat technology and greater care in allocatingexploration investments have allowed companies totackle increasingly difficult exploration conditionssuccessfully.

Other indicators which are particularly sensitive toexploration activities are the Discovery Cost (whichcorrelates additional proved reserves more directlywith investments in exploration and the acquisition ofnew acreage), and the Exploration Discovery Cost,which measures proved reserves against explorationinvestments alone. In recent years the oil industry has

175VOLUME I / EXPLORATION, PRODUCTION AND TRANSPORT

PROGRAMMING EXPLORATION ACTIVITY

improved the overall efficiency of explorationactivities, bringing the discovery cost to about 0.9dollars per barrel, out of a total technical cost in theorder of 7-8 dollars per barrel.

2.1.7 Economic aspects of petroleum exploration

IntroductionA company of any size and type must have criteria

with which to evaluate its own success, generallymeasured by its ability to generate profits.

In the oil industry, too, the main objective is tocreate value for shareholders through the core businessof searching for, producing and commercializinghydrocarbons. This means that these activities must notonly be managed in the best possible way to reduce andcontrol expenditure, and optimize returns, but that thecompany must also be able to choose between differentinvestment opportunities to ensure the maximum yieldfrom the capital employed. Profits also guarantee theavailability of capital for further investments.

The petroleum sector has a number of distinctivefeatures which distinguishes it from other industries.In assessing the performance of an oil it must be bornein mind that profit is often associated with specificparameters (replacement of reserves produced,exploration results), which are important, but difficultto quantify in economic terms. Additionally, oilcompanies are exposed to mineral, geographical,political and environmental risk to a far greater extentthan other businesses. For political risk, we could citesome nationalizations introduced in the past with theirconsequent negative impact on the operatingcompanies.

Alongside these critical aspects, it should beconsidered the frequent use of short-term investmentswith a risk capital that can be obtained only throughself-financing. The strategic choices of an oil companyinfluence the type of exploration initiatives which canbe undertaken. These may be aimed at maintenance orgrowth, and always have as their end goal thepreservation of a balanced relationship betweenreserves and production. The programmes of an oilcompany must therefore take into account the need tooperate with a given percentage of risky investmentswhich must nevertheless not penalize its overall results.

The economic aspect of petroleum research,important in all the different phases of the productionprocess (development, transport, commercialization),plays a particularly significant role during theexploration phase. It has a notable impact on someoperational choices (the acquisition of a givenpermit and its conditions, the drilling of a well or the

release of mineral rights to a third party). Theeconomic aspect is crucial when it is necessary toevaluate offers to purchase petroleum properties(assets) or whole companies. These acquisitionsoften include known reservoirs to be produced andpermits with a petroleum potential that still requiresexploration.

In conclusion, the economic approach to anexploration project is important because it makes itpossible to evaluate if some decision variables (theprobable size of the discovery, the existence of amarket, forecast sales prices, the estimate of theproject’s technical costs, the location of productionareas) can be combined with an adequate return on thecapital invested. Without this, any research activitywould be unjustified.

Decision analysisThe concept of decision analysis is closely linked

to economic aspects. This basically involves evaluatingdifferent investment opportunities, comparing themand choosing the most promising one in terms both ofthe guaranteed return and of the risk involved. Anapproach of this type confronts the explorationcompany with a series of questions, to which it is notsufficient to give a positive or negative response, butwhich must be considered in relation to the variouspossibilities generated by each working hypothesis.

In fact, the result of exploration activity isunknown, and its estimate depends on the evaluationof the petroleum potential of an area, a permit or abasin. As already stated, this evaluation is subject touncertainty, both in terms of the confirmation of theexploration hypothesis (actual existence of thepetroleum deposit), and in terms of the size of thediscovery (extraction potential of the reserves). Theeconomic evaluation, for sale or purchase, of anexploration permit – in contrast, for example, to aknown reservoir – thus requires the formulation ofscenarios concerning on the one hand the probabilityof success (existence of the petroleum basin), and onthe other the estimate of its predicted potential (innumbers of barrels). Furthermore, if an explorationarea with a given predicted potential is acquired,however many data are available, negative results (drywell) may still be obtained, or a reservoir which issmaller than forecast may be discovered; alternativelyinsufficient investments may have been allocated withthe consequent negative financial results.

Deciding on an exploration investment thusinvolves trying to predict the outcomes which mayresult from a given choice, whilst always bearing inmind the possibility of failure. The application ofdecision analysis to petroleum exploration hasreplaced the simple ‘intuition’ of the geologist, and

176 ENCYCLOPAEDIA OF HYDROCARBONS

PETROLEUM EXPLORATION

provided a more correct and complete frameworkwithin which to exploit available information. Thisallows us to compare projects of highly diverse nature.Often those working in petroleum exploration considerthese methods a pointless exercise, which does notprevent the drilling of dry wells. However, it should beborne in mind that turning the probability of anoutcome and its economic consequences into amethodological approach is simply one way ofexploiting available knowledge to predict and compareresults. The various steps (Newendorp, 1975)characterizing a decision analysis process are asfollows: a) definition of possible scenarios derivingfrom individual choices and their alternatives; b) definition of the advantages and disadvantages ofeach scenario; c) estimate of the probability that eachpossible outcome will occur; d) calculation ofweighted average profits for each decision taken.

Terms of the problemThe main ‘asset’ of an oil company is represented

by hydrocarbon reserves. In the official presentationsmade by oil companies to their shareholders (roadshows) two aims are often stressed: the need toactivate existing reserves to generate profits in theshort term, and the need to invest in order to guaranteea satisfactory ratio of reserves to production in thelong term. These concepts recur frequently in thestrategic programmes of major companies, such asShell, BP, Chevron-Texaco, Exxon-Mobil,TotalFinaElf and Eni. Growth requires not onlyreplacement of the reserves produced, but also theacquisition of additional reserves; this frequentlyoccurs through exploration which, as we have seen, isa risky activity.

Within a company context the geologist developsthe initial exploration idea. The hypothesis that a givenarea may contain hydrocarbons must then be turnedinto an operational proposal involving a series ofcosts, both during the initial phase of acquiring theblock (study of the area, acquisition ofdocumentation), and during the permit’s validityperiod (detailed geological studies, geophysicalsurveys, drilling of wells).

The implementation of the original idea thus has acost and, if the validity of the project is to bedetermined, it is essential to know if there will be aresult, and whether or not this result justifies theexpenditure. It is therefore important to predict all thepossible outcomes of the initial hypothesis, andanalyse the cost of each in operational terms. Once adiscovery has been made, it must be assessed what thefinal economic results expected are for each scenarioregarding the reserves. Even the correct allocation ofexploration investments in accounting terms (Megill,

1988) represents a useful element for the developmentof accurate economic evaluations in the petroleumindustry.

Evaluating the object of explorationIn the economic evaluation of an exploration

project two factors are of particular significance:• The petroleum risk, in other words the possibility

of success. The oil industry now uses tools toevaluate geological risk which allow us to quantifythe probability that a given prospect will be drilledsuccessfully or otherwise. The probability ofsuccess is thus an extremely important parameterin evaluating exploration potential, since it allowsus to calculate petroleum risk before the investmentis actually made. Statistics show that companies inpossession of up-to-date technologies or technicaldrilling capabilities which allow them to achievetheir predetermined aims within the time-framespecified obtain far better results than smallerbusinesses which rely on service companies. Inother words, initial investments in technologicalresearch (often seen as costs) have a positiveimpact on future operational activities;

• Commercial success. Alongside petroleum risk, itmust also be taken into account potentialcommercial aspects, and thus establish theminimum reserves able to guarantee profitableproduction. It is therefore necessary to predict thequality of the discovery in terms of reserves andtheir distribution, expressed as a probability rangebounded by maximum and minimum values, andcompatible with historical data from reservoirs inthe basin or the area. There is a difference betweengeological and commercial success in that thereserves found by a well may be whollyinsufficient for development. Alternatively, theproductivity of individual wells may be insufficientto support acceptable production profiles. Often,the viability of a project is determined more by theproduction capacities of individual wells than byreserves.Discovery statistics show that only a small

percentage of geological successes translate intoeconomic success.

CostsCosts in the exploration phase. The costs of the

exploration phase include the payment of a signaturebonus, geophysical surveys in general and seismicsurveys in particular, geological and geophysicalinterpretations and finally the drilling of wellsfollowed, in the case of petroleum success, byproduction tests. These investments are normallyunavoidable in order to begin exploration in the area,

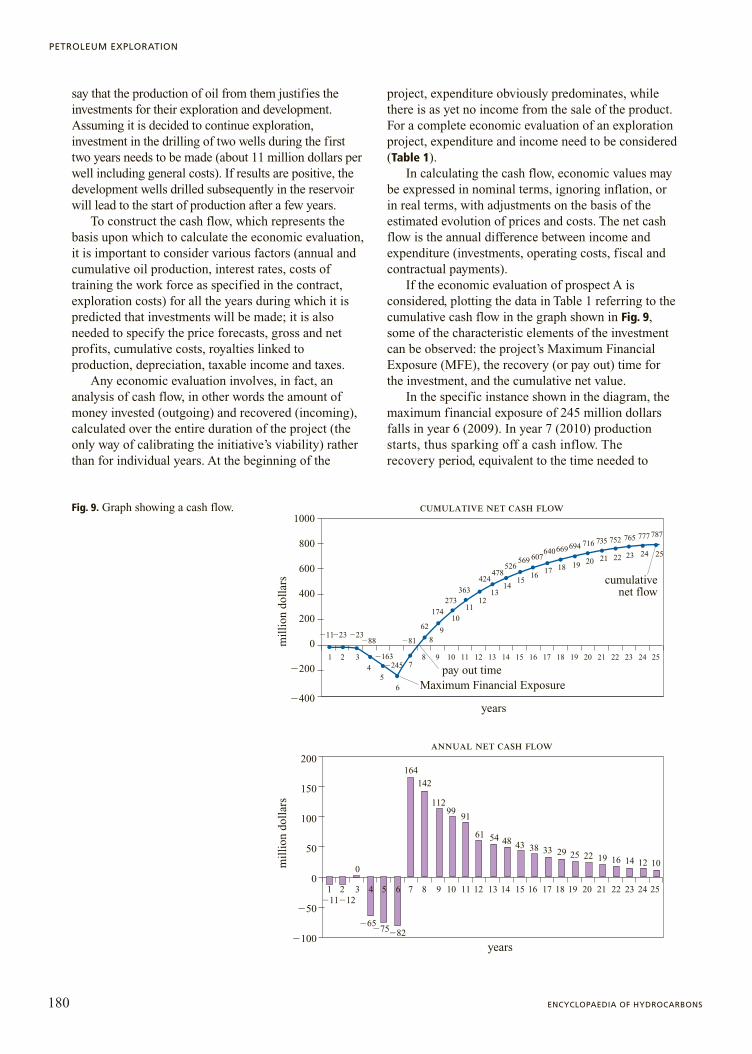

177VOLUME I / EXPLORATION, PRODUCTION AND TRANSPORT

PROGRAMMING EXPLORATION ACTIVITY

and must be included in a budget approved in thecompany’s plans and compatible with its strategies.Exploration costs are dealt with in different ways inthe accounts. It is important, for example, to establishwhich costs can be expensed and are thereforedeductible in the same financial year, and which arecapitalized; for capitalized costs it is essential to checkhow long these will take to recover. Deductibleexpenditure is represented by salaries, geological andgeophysical work, the costs of core samples, dry wells.Capitalized costs, on the other hand, include entriesconcerning tools, storage facilities, assets, successfulwells. As a general rule, it is obviously best to expenseinvestments as much as possible, in accordance withthe regulations of the country in which operations takeplace.

Costs in the development phase. In thedevelopment phase other technical costs are faced. Theeconomic evaluation of an exploration initiative doesnot just concern the exploration phase in the strictsense, but also that of reservoir exploitation. If theresult of exploration is positive, the entire petroleum

cycle is activated: development, production,commercialization and abandonment of the site usedfor extraction operations. It is therefore advisable,during the preliminary evaluation, to attempt to predictpossible development scenarios and the operationalphases required to carry them out: the accuratedefinition of reserves, the number of wells required toevaluate the reservoir, the number of producing wellsneeded to produce it according to optimal operationalrules. In terms of expenditure, the project resultingfrom a successfully drilled prospect requires detailedplanning which also includes infrastructure (forexample in the case of an offshore project theconstruction of a production platform), and the drillingof injection wells which allow us to improve therecovery of oil and gas. The temporal distribution ofinvestments needs to be analysed in order to maximizeproduction without penalizing the reservoir’sproduction capacities in the long term. Alongsidethese costs, known as capex (capital expenditure), it isalso important to consider operating expenditure(opex) referring to the management of production

178 ENCYCLOPAEDIA OF HYDROCARBONS

PETROLEUM EXPLORATION

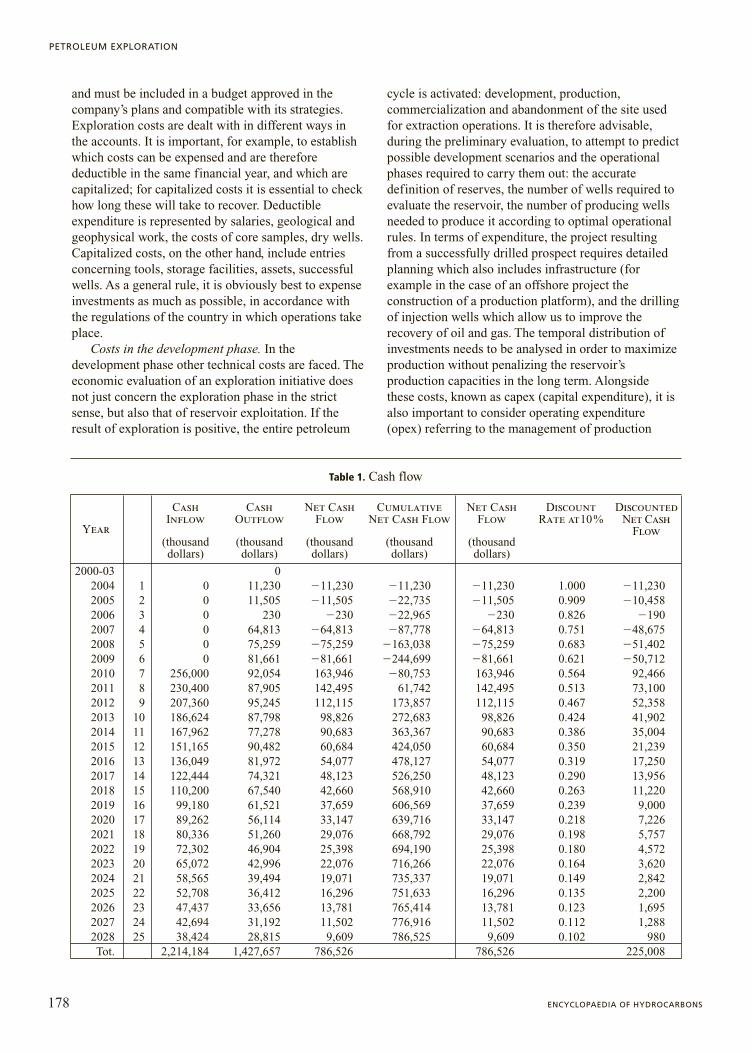

Cash Cash Net Cash Cumulative Net Cash Discount Discounted Inflow Outflow Flow Net Cash Flow Flow Rate at 10% Net Cash

Year Flow(thousand (thousand (thousand (thousand (thousand dollars) dollars) dollars) dollars) dollars)

2000-03 02004 1 0 11,230 �11,230 �11,230 �11,230 1.000 �11,2302005 2 0 11,505 �11,505 �22,735 �11,505 0.909 �10,4582006 3 0 230 �230 �22,965 �230 0.826 �1902007 4 0 64,813 �64,813 �87,778 �64,813 0.751 �48,6752008 5 0 75,259 �75,259 �163,038 �75,259 0.683 �51,4022009 6 0 81,661 �81,661 �244,699 �81,661 0.621 �50,7122010 7 256,000 92,054 163,946 �80,753 163,946 0.564 92,4662011 8 230,400 87,905 142,495 61,742 142,495 0.513 73,1002012 9 207,360 95,245 112,115 173,857 112,115 0.467 52,3582013 10 186,624 87,798 98,826 272,683 98,826 0.424 41,9022014 11 167,962 77,278 90,683 363,367 90,683 0.386 35,0042015 12 151,165 90,482 60,684 424,050 60,684 0.350 21,2392016 13 136,049 81,972 54,077 478,127 54,077 0.319 17,2502017 14 122,444 74,321 48,123 526,250 48,123 0.290 13,9562018 15 110,200 67,540 42,660 568,910 42,660 0.263 11,2202019 16 99,180 61,521 37,659 606,569 37,659 0.239 9,0002020 17 89,262 56,114 33,147 639,716 33,147 0.218 7,2262021 18 80,336 51,260 29,076 668,792 29,076 0.198 5,7572022 19 72,302 46,904 25,398 694,190 25,398 0.180 4,5722023 20 65,072 42,996 22,076 716,266 22,076 0.164 3,6202024 21 58,565 39,494 19,071 735,337 19,071 0.149 2,8422025 22 52,708 36,412 16,296 751,633 16,296 0.135 2,2002026 23 47,437 33,656 13,781 765,414 13,781 0.123 1,6952027 24 42,694 31,192 11,502 776,916 11,502 0.112 1,2882028 25 38,424 28,815 9,609 786,525 9,609 0.102 980Tot. 2,214,184 1,427,657 786,526 786,526 225,008

Table 1. Cash flow

operations and the costs of abandonment, includingthe environmental rehabilitation of the area whenproduction ends.

The production profilePredicting the production profile is a delicate

aspect because it allows us to hypothesize the actualincome from the sale of the product. The reservoir’sproduction behaviour must therefore be stimulated inorder to determine the quantity of hydrocarbonsproducible in any given year. The production profile islinked to the production capacities of individual wells,and to a recovery hypothesis for the oil in place. Assuch, an estimate of some important parameters suchas full production, its duration, the rate of decline andthe field’s maximum yield is fundamentally importantfor the economic analysis.

Contractual and fiscal aspectsAlongside the technical costs are others, especially

those of a contractual and fiscal nature, which must bepaid to the State that owns the leased acreage.

The development lease in which the operator isallowed to produce oil and gas in a given country iscovered by an agreement, signed when the explorationpermit is assigned. There are various types of contract.One frequent type is the participation contract, orProduction Sharing Agreement, where the oilproduced is divided into two parts: one part (cost oil)is assigned to the operator, allowing him to recover thecosts of putting the reservoir into production. Alsoreimbursed are prior exploration investments which inthe case of failure remain the responsibility of theoperator, with no possibility of reimbursement. Theremainder represents profit (profit oil), and is sharedbetween the operator (or the joint venture on behalf ofwhich the operator manages activities) and the State,according to different percentages linked to dailyhydrocarbon production levels. There are usually alsotaxes on taxable income (net of costs incurred).

A second type of contract is the ConcessionAgreement, in which the operator has the right toexploit the hydrocarbons on the condition thatroyalties are paid to the State; in other words, a directtax on production. In this case, too, taxable income iscalculated net of costs incurred. There may also befurther taxation affecting the profitability of anexploration project.

These commitments, together with technical costs,represent the basis for an economic evaluation of theproject to be activated.

PricesA fundamental element of the economic evaluation

is the worth of the product. Oil prices may vary

significantly. Especially in the economic evaluation ofprojects covering a span of 25-30 years it is importantto adopt a fairly realistic price forecast. There aredifferent models for this purpose (which at times areunfortunately affected by unpredictable externalfactors), which generally refer to a reference or markeroil such as Brent or Arabian Light, with specificphysical and chemical properties. The reference oil inturn influences the price of all related products, suchas natural gas, condensed gas, Liquid Natural Gas(LNG) and Liquid Petroleum Gas (LPG).

The economic evaluationOn the basis of the elements described above

regarding investments, the evaluation of costs duringthe exploration and development phases, theproduction profile, prices and the fiscal regime, aneconomic analysis of the exploration project can beundertaken. This type of economic evaluation,however, does not include the risk factor, and does notallow us to compare alternative. Below are outlinedthe principles of a ‘deterministic’ economic evaluationof a petroleum exploration project. Petroleum risk willthen be analysed considering the mineral risk variable.

To fully understand the methodologies used ineconomic evaluation, an example of a lease contractfor an offshore exploration permit, containing thefollowing obligations, can be examined:• A first period of four years with the obligation of

acquiring a three-dimensional seismic survey at acost of 6 million dollars; in this case no welldrilling is included.

• A second optional period of two years involvingthe drilling of two wells at a cost of 10 milliondollars each.

• A third optional period of two years with theobligation of drilling another well at a predictedcost of 10 million dollars.During the first period the seismic survey is

carried out, interpretation of which will show threeprospects of greatest interest:• Prospect A: estimated reserves of 138 million

barrels, 20% probability of success.• Prospect B: estimated reserves of 109 million

barrels, 16% probability of success.• Prospect C: estimated reserves of 70 million

barrels, 13% probability of success.At this point it must be decided whether to embark

in the second explorative period and drill two wells asaccording to the contract or whether to abandonproduction (the same decision will have to be taken inthe future, when evaluating whether to proceed to thethird period).