Embed Size (px)

Citation preview

2012 Redwood Analytics® User ConferenceAnalysis. Insight. Action.

Billing & Collections 101: Best Practices for Managing Firm Finances

Stuart AllenProduct Manager

2012 Redwood Analytics® User ConferenceAnalysis. Insight. Action.

Billing & Collections 101

• Inventory Management• Revenue Management• Tracking Time Entry

2012 Redwood Analytics® User ConferenceAnalysis. Insight. Action.

Inventory Management

4

Key Inventory Questions

• How old are my WIP and A/R?• How quickly can I bill/collect that work?• What happens if I don’t do so in a timely fashion?• How can I quantitatively tell which A/R to go after

first?

5

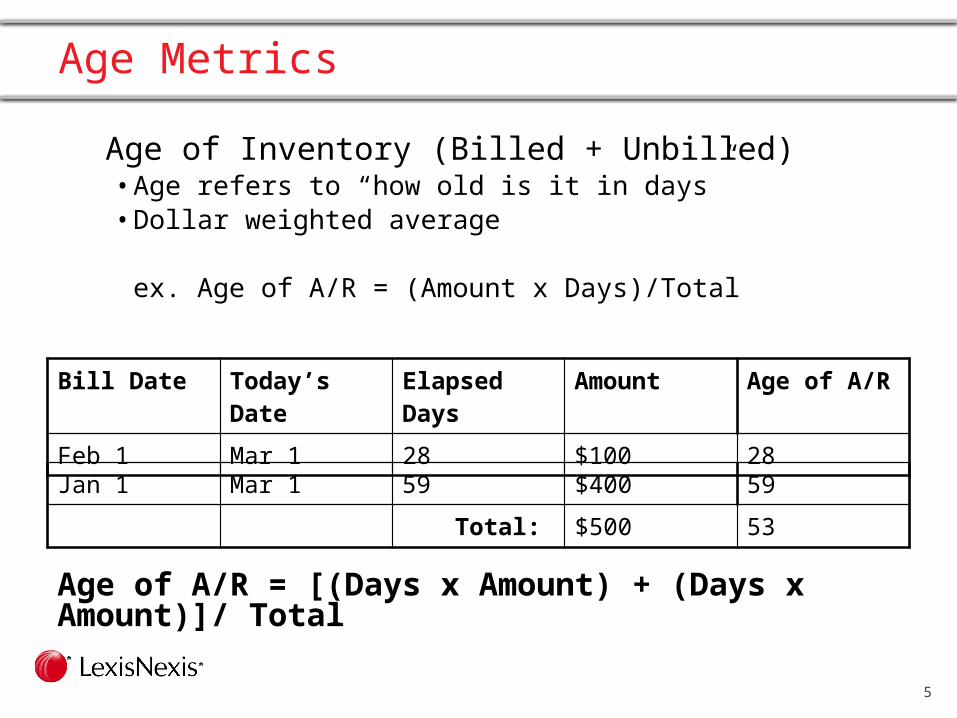

Age of Inventory (Billed + Unbilled)• Age refers to “how old is it in days”• Dollar weighted average

ex. Age of A/R = (Amount x Days)/Total

Bill Date Today’s Date

Elapsed Days

Amount Age of A/R

Feb 1 Mar 1 28 $100 28

Jan 1 Mar 1 59 $400 59

Total: $500 53

Age of A/R = [(Days x Amount) + (Days x Amount)]/ Total

Age Metrics

6

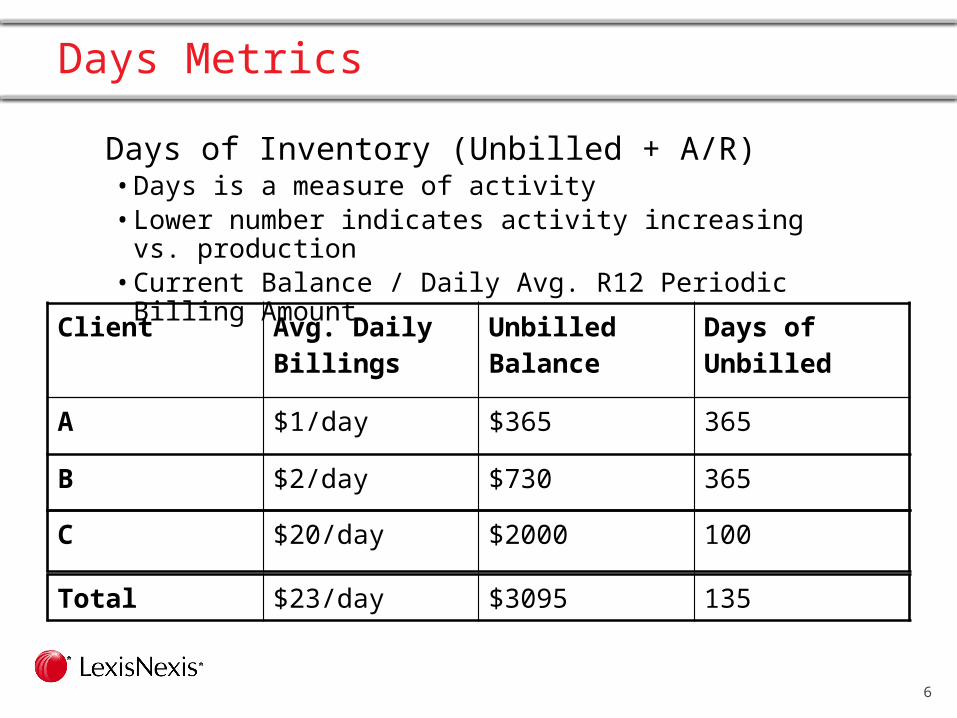

Days of Inventory (Unbilled + A/R)• Days is a measure of activity• Lower number indicates activity increasing vs. production• Current Balance / Daily Avg. R12 Periodic Billing Amount

Client Avg. Daily Billings Unbilled Balance Days of Unbilled

A $1/day $365 365

B $2/day $730 365

C $20/day $2000 100

Total $23/day $3095 135

Days Metrics

7

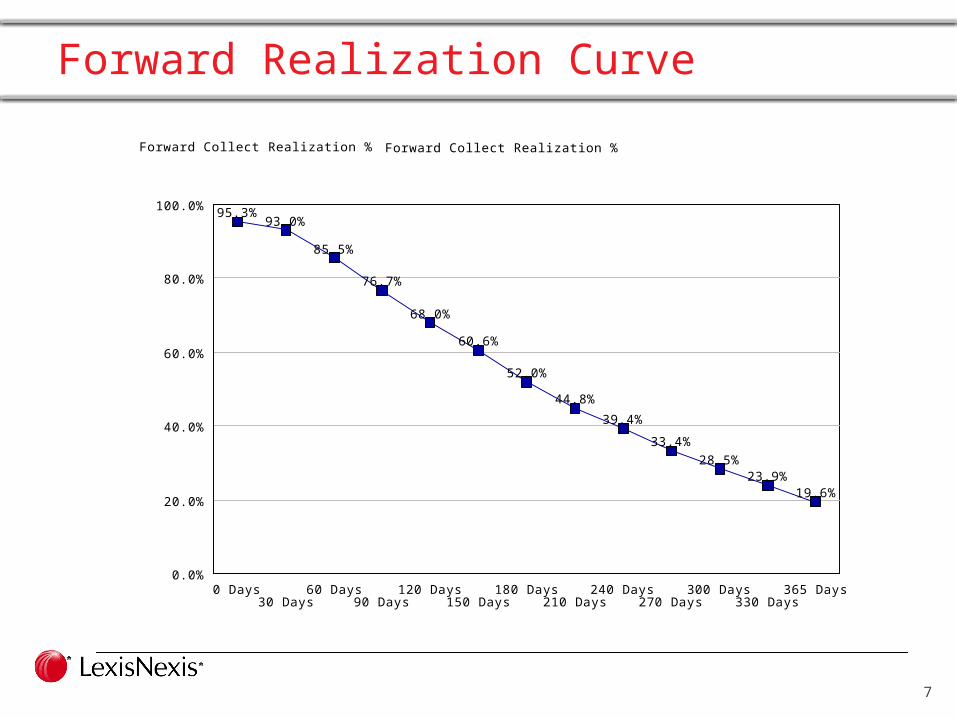

Forward Realization Curve

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

0 Days30 Days

60 Days90 Days

120 Days150 Days

180 Days210 Days

240 Days270 Days

300 Days330 Days

365 Days

95.3%93.0%

85.5%

76.7%

68.0%

60.6%

52.0%

44.8%

39.4%

33.4%

28.5%23.9%

19.6%

Forward Collect Realization %Forward Collect Realization %

Risk Adjustment

Likely to Bill / Collect

At Risk

Forward Billing / Collection Realization %

8

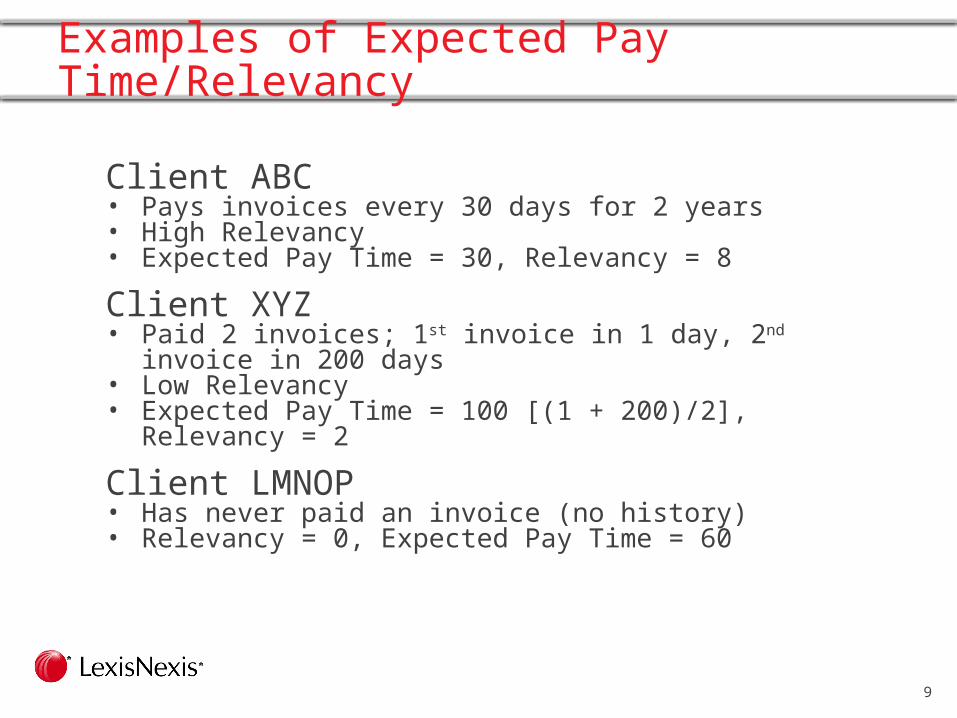

Expected Pay Time

Based on a clients history, when we expect payment on an invoice• Not dependent on age of invoice but rather past client

activityRelevancy• An Expected Pay Time is only as relevant as the quality of

the client’s history• Index of 0 – 9 reflecting “relevancy’ of Expected Pay Time

measure• 9 = very relevant, 1 = not relevant, 0 = clients with no history

Based on the Client level NOT the Related Client/Parent Client level

9

Client ABC• Pays invoices every 30 days for 2 years• High Relevancy• Expected Pay Time = 30, Relevancy = 8

Client XYZ• Paid 2 invoices; 1st invoice in 1 day, 2nd invoice in 200 days • Low Relevancy• Expected Pay Time = 100 [(1 + 200)/2], Relevancy = 2

Client LMNOP• Has never paid an invoice (no history)• Relevancy = 0, Expected Pay Time = 60

Examples of Expected Pay Time/Relevancy

10

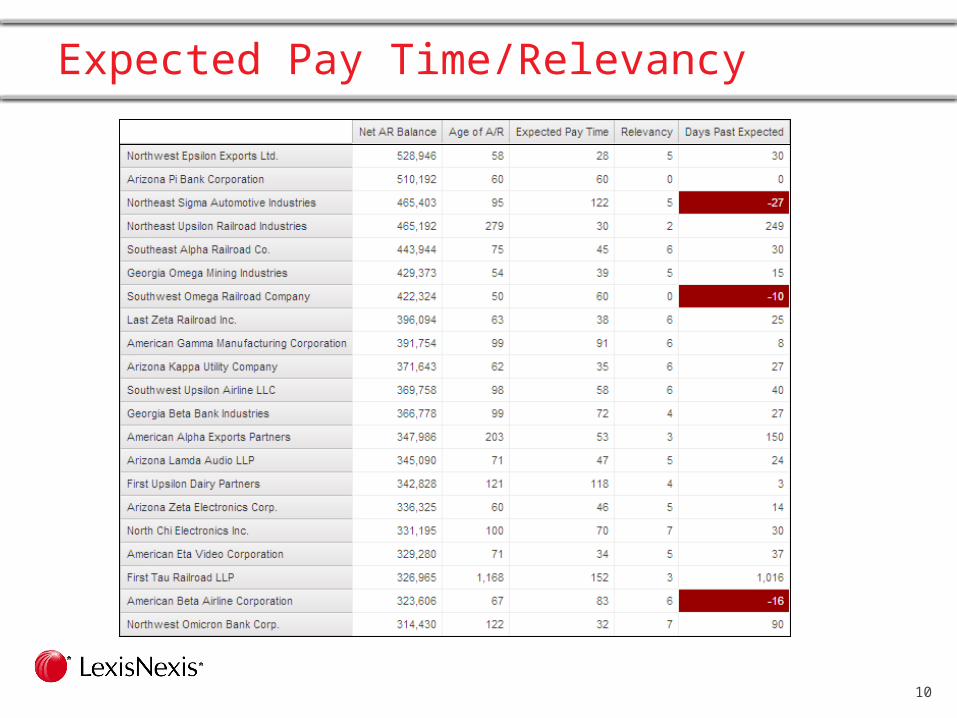

Expected Pay Time/Relevancy

11

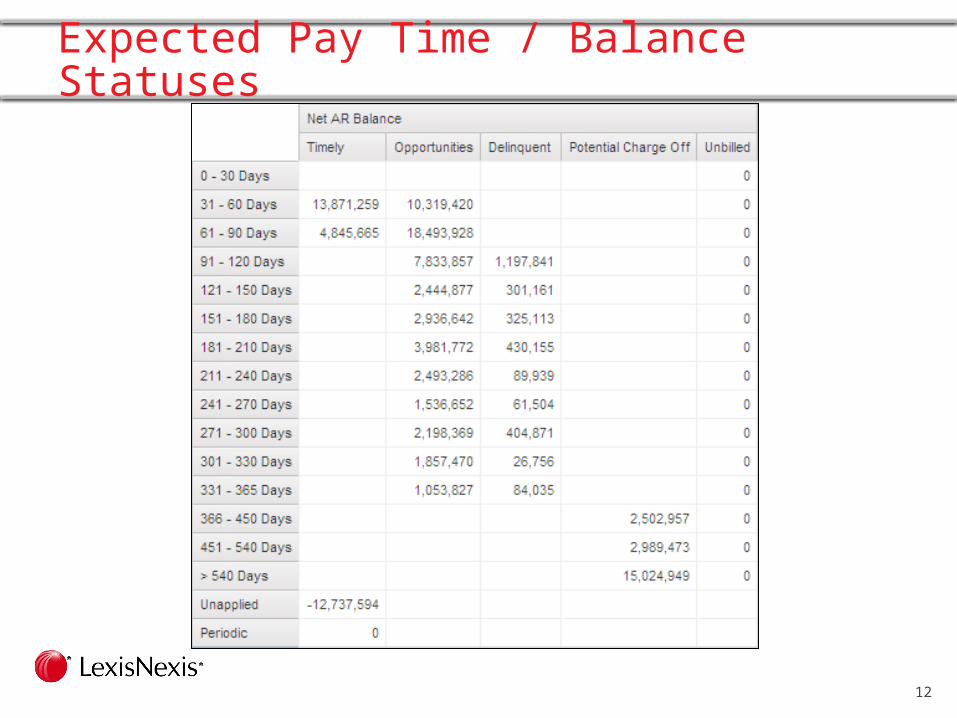

Balance Statuses

Expected Pay Time allows the use of Balance Statuses to define opportunities for collections

• Timely – Invoices <= Delinquency Date, Not Past Expected Pay Time

• Opportunities – Invoices Past Expected Pay Time• Delinquent – Invoices > Delinquency Date, Not Past

Expected Pay Time• Potential Charge-off – Invoices > 365 Days regardless of

Expected Pay Time• Unbilled – All WIP

12

Expected Pay Time / Balance Statuses

13

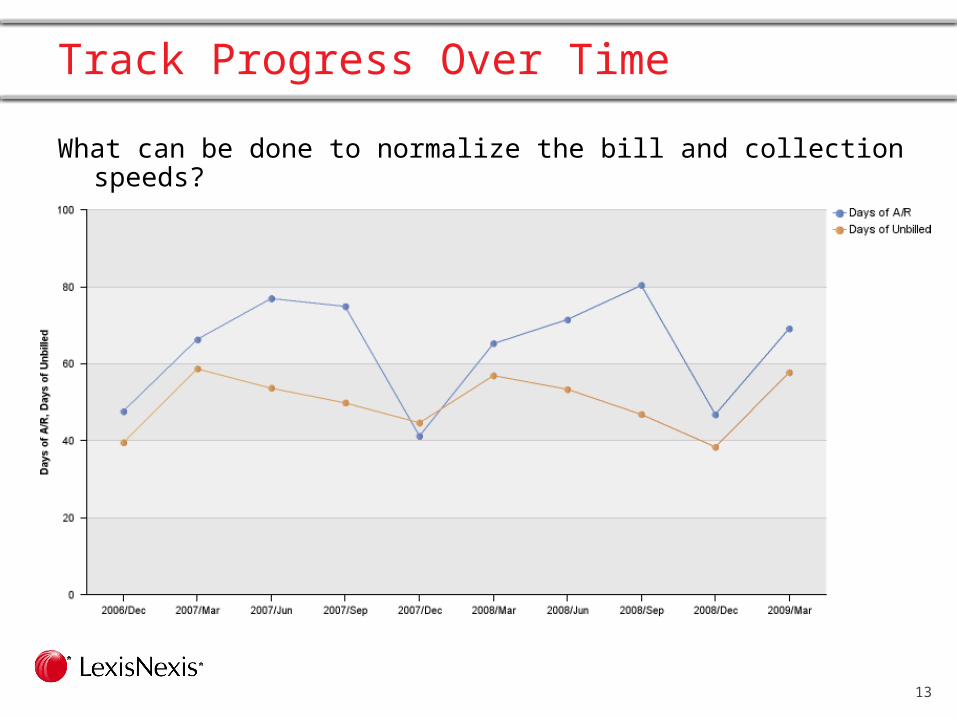

Track Progress Over Time

What can be done to normalize the bill and collection speeds?

2012 Redwood Analytics® User ConferenceAnalysis. Insight. Action.

Revenue Management

15

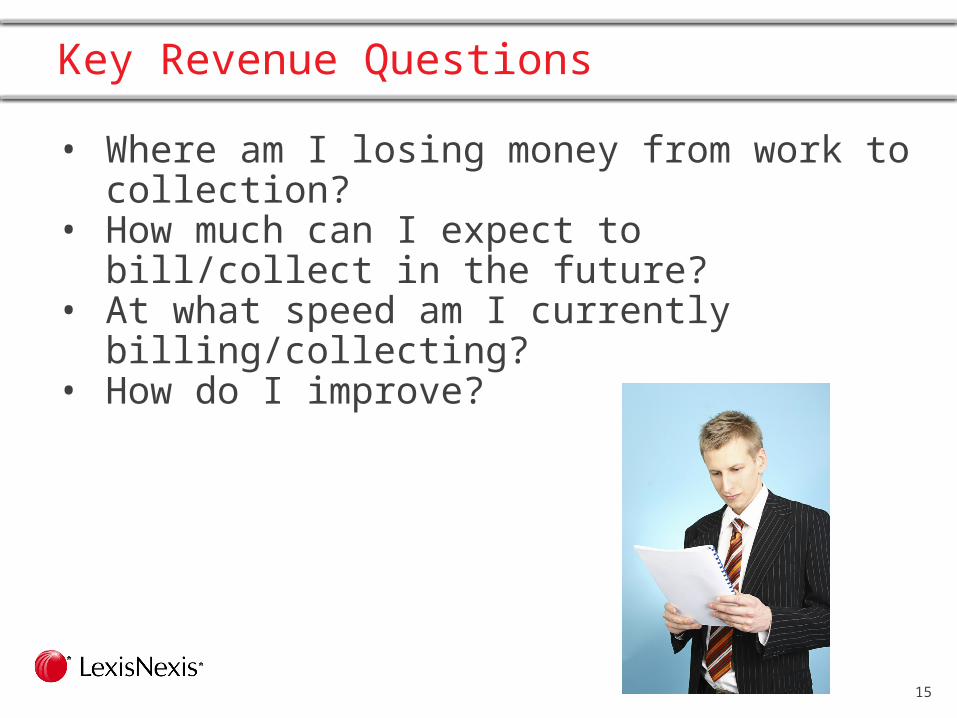

Key Revenue Questions

• Where am I losing money from work to collection?• How much can I expect to bill/collect in the future?• At what speed am I currently billing/collecting? • How do I improve?

16

Static versus Periodic Concepts

17

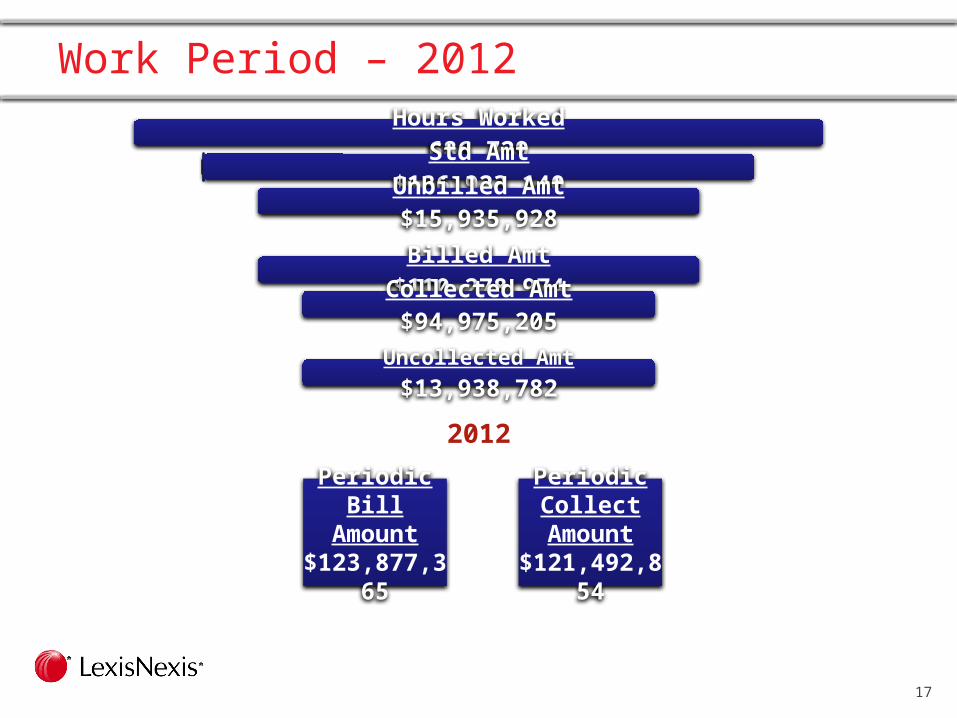

Hours Worked686,729Std Amt

$136,923,140Unbilled Amt$15,935,928

Billed Amt$110,278,974Collected Amt$94,975,205

Uncollected Amt$13,938,782

Periodic Bill Amount

$123,877,365

Periodic Collect

Amount$121,492,854

2012

Work Period – 2012

18

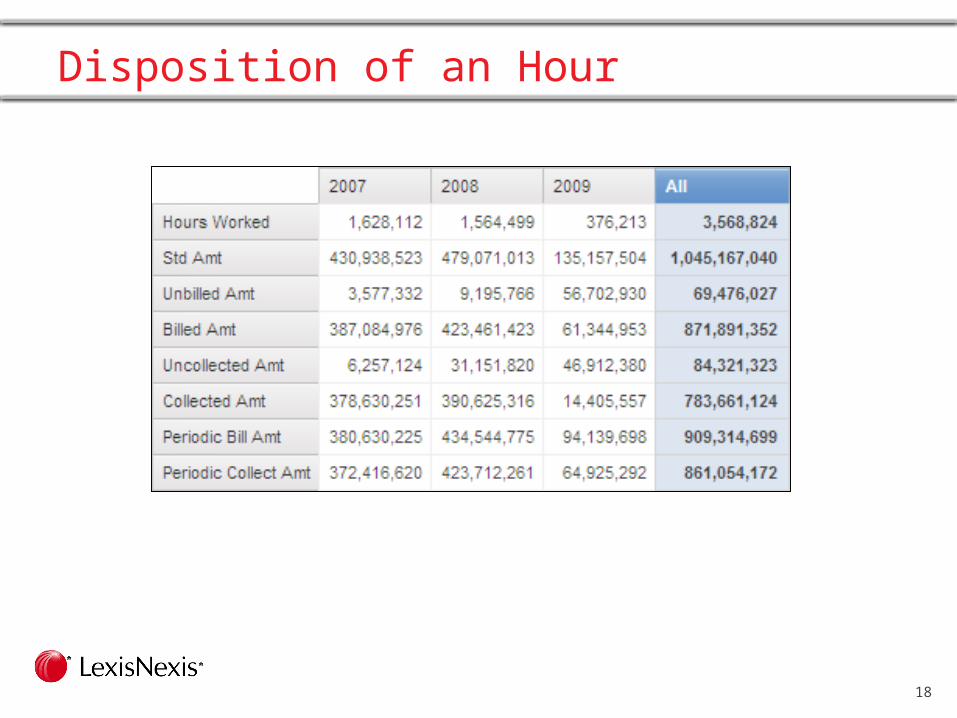

Disposition of an Hour

19

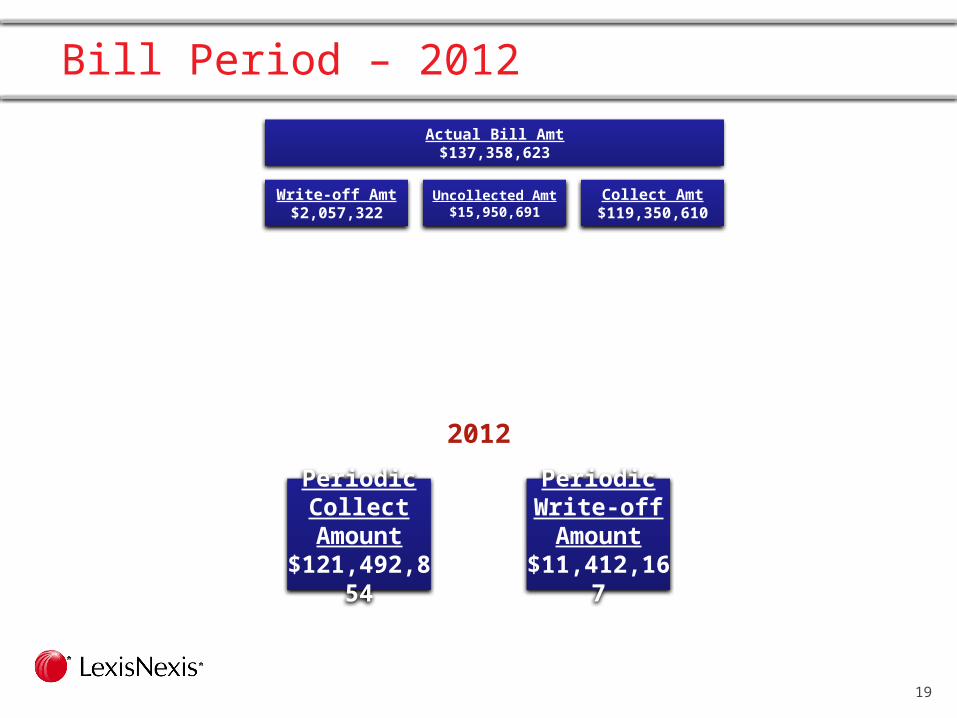

Actual Bill Amt$137,358,623

Write-off Amt$2,057,322

Uncollected Amt$15,950,691

Collect Amt$119,350,610

Bill Period – 2012

Periodic Collect

Amount$121,492,854

Periodic Write-off Amount

$11,412,167

2012

20

Reversals

Jan 2012 Feb 2012 Mar 2012Billed Amt. (Actual)

$500 $500 $500

Periodic Bill Amt.

$500 $500 $500

Jan 2012 Feb 2012 Mar 2012Billed Amt. (Actual)

$400 $500 $500

Periodic Bill Amt.

$500 $500 $400

*The effect of a $100 reversal in March based on invoice originally billed in January

21

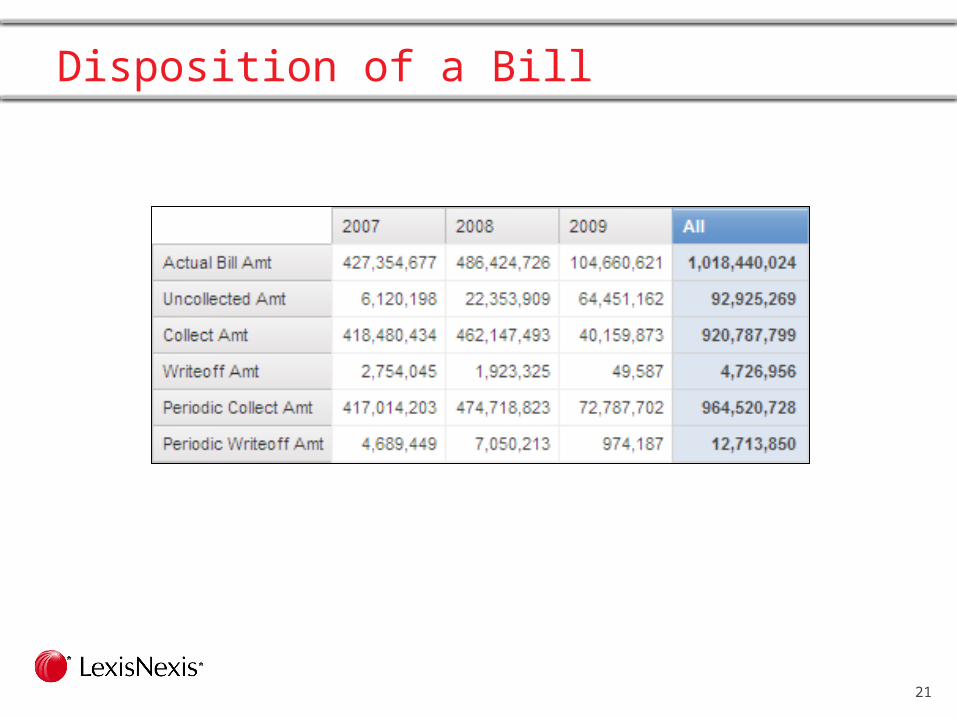

Disposition of a Bill

22

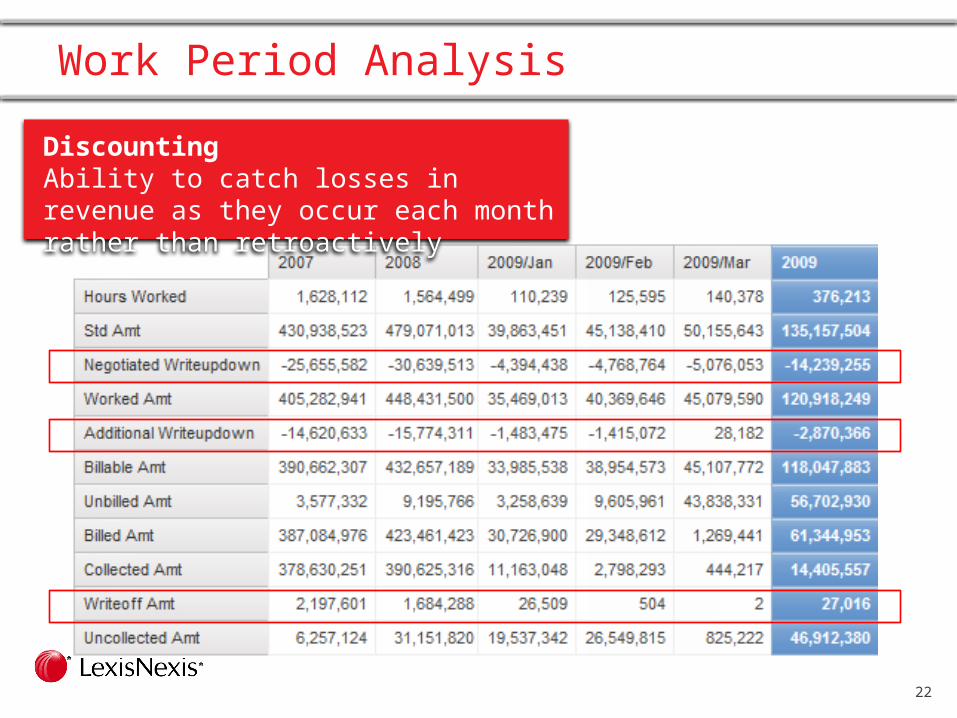

Work Period Analysis

DiscountingAbility to catch losses in revenue as they occur each month rather than retroactively

23

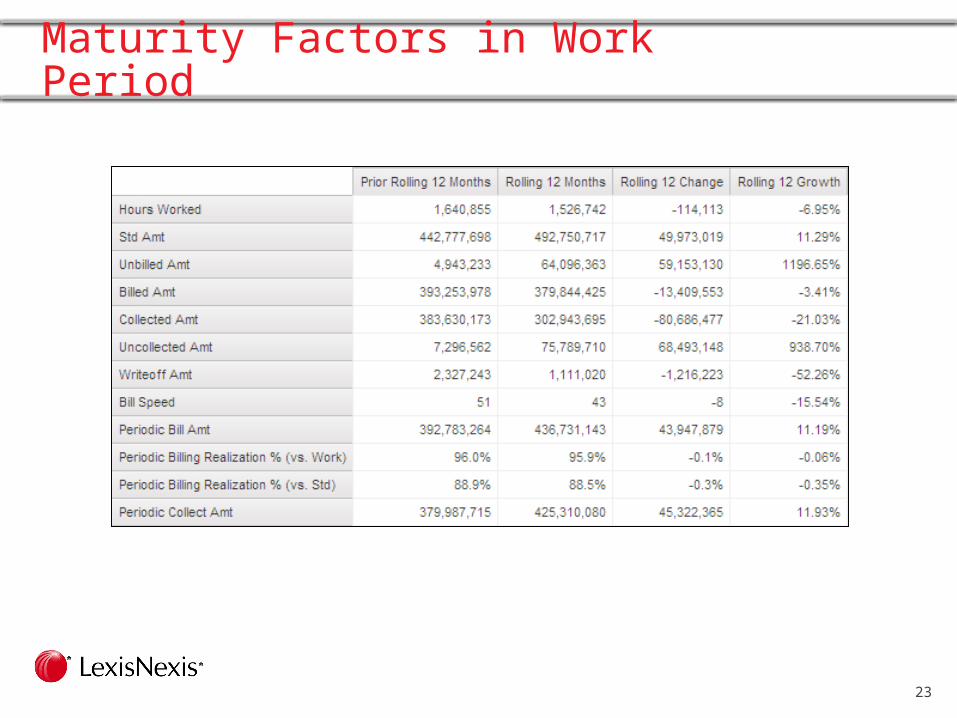

Maturity Factors in Work Period

24

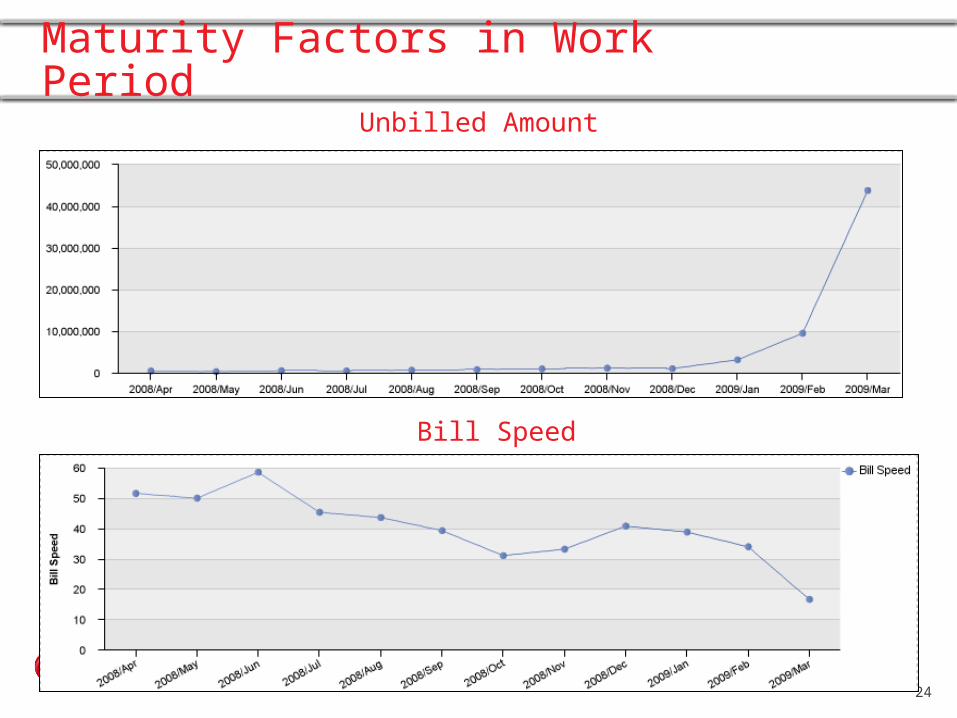

Maturity Factors in Work PeriodUnbilled Amount

Bill Speed

25

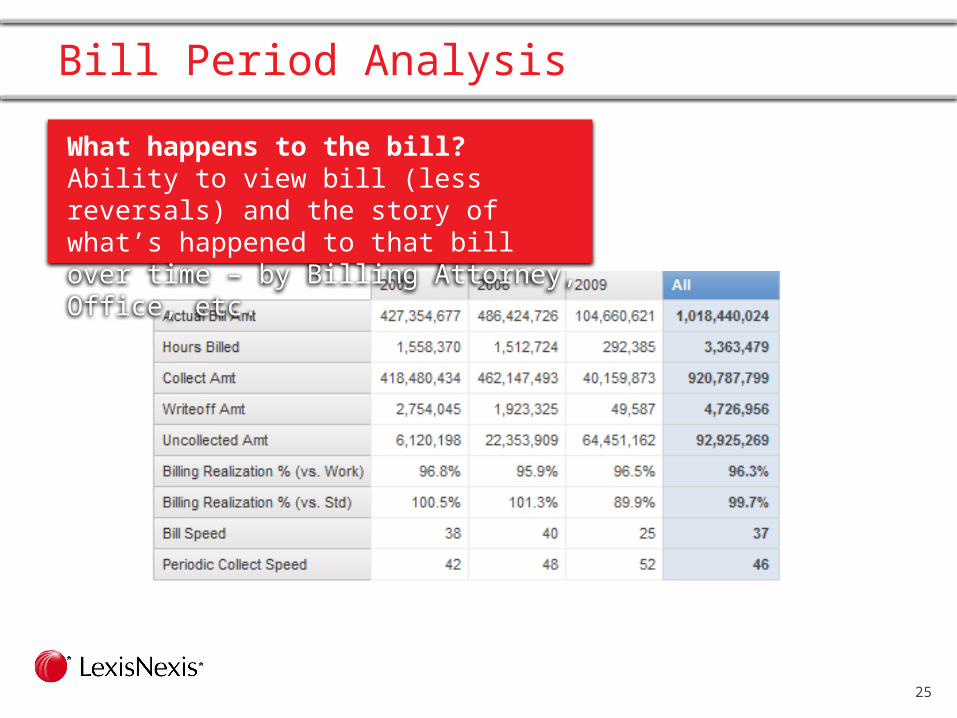

Bill Period Analysis

What happens to the bill?Ability to view bill (less reversals) and the story of what’s happened to that bill over time – by Billing Attorney, Office, etc.

26

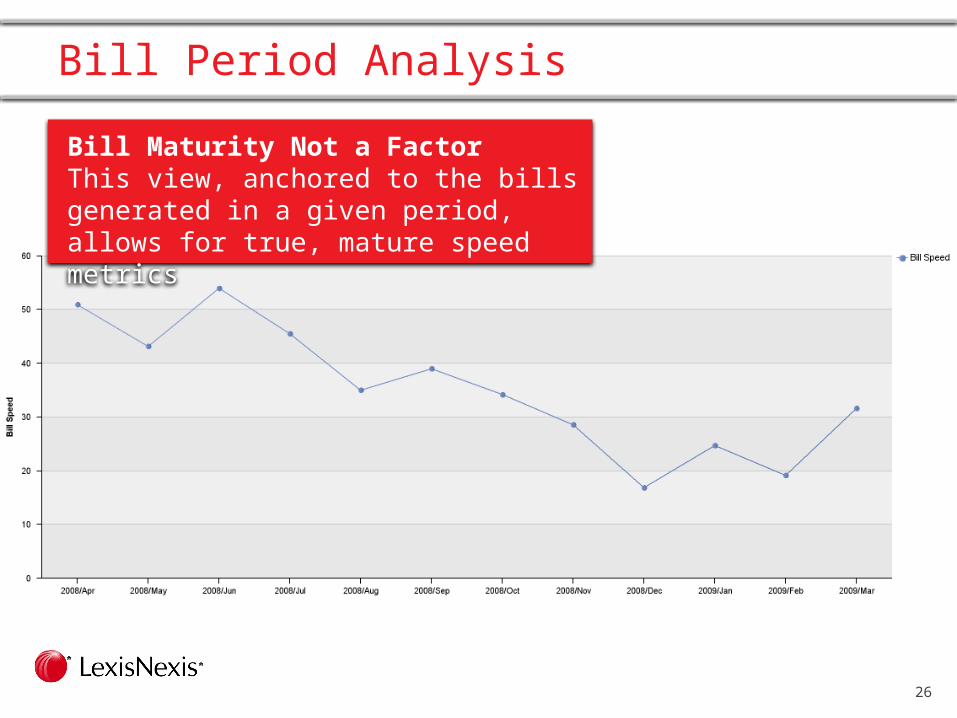

Bill Period Analysis

Bill Maturity Not a FactorThis view, anchored to the bills generated in a given period, allows for true, mature speed metrics

2012 Redwood Analytics® User ConferenceAnalysis. Insight. Action.

Time Tracking

28

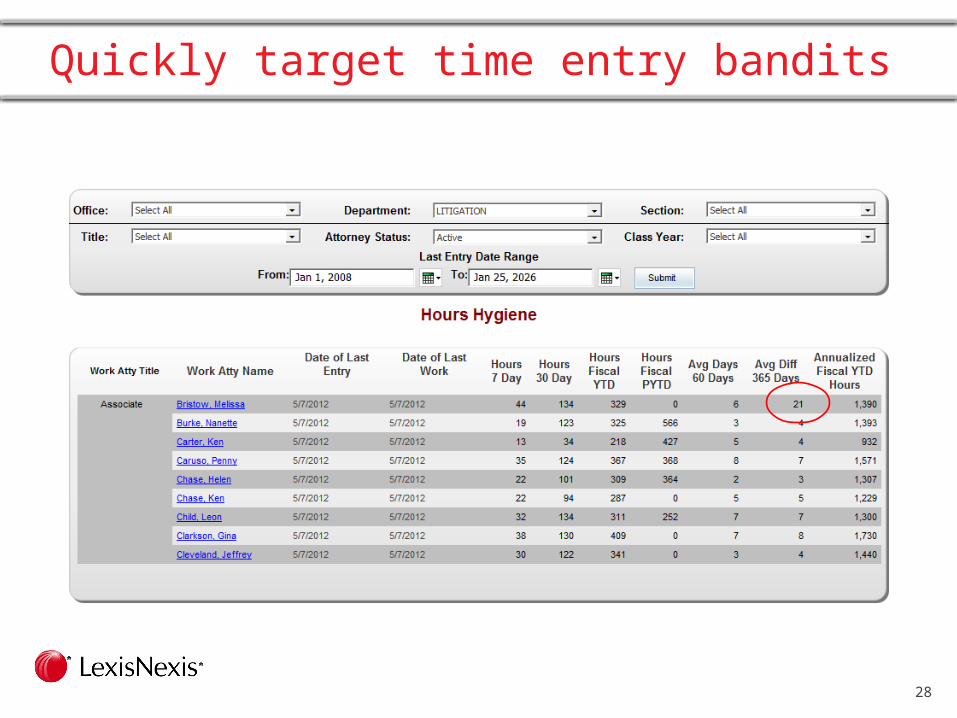

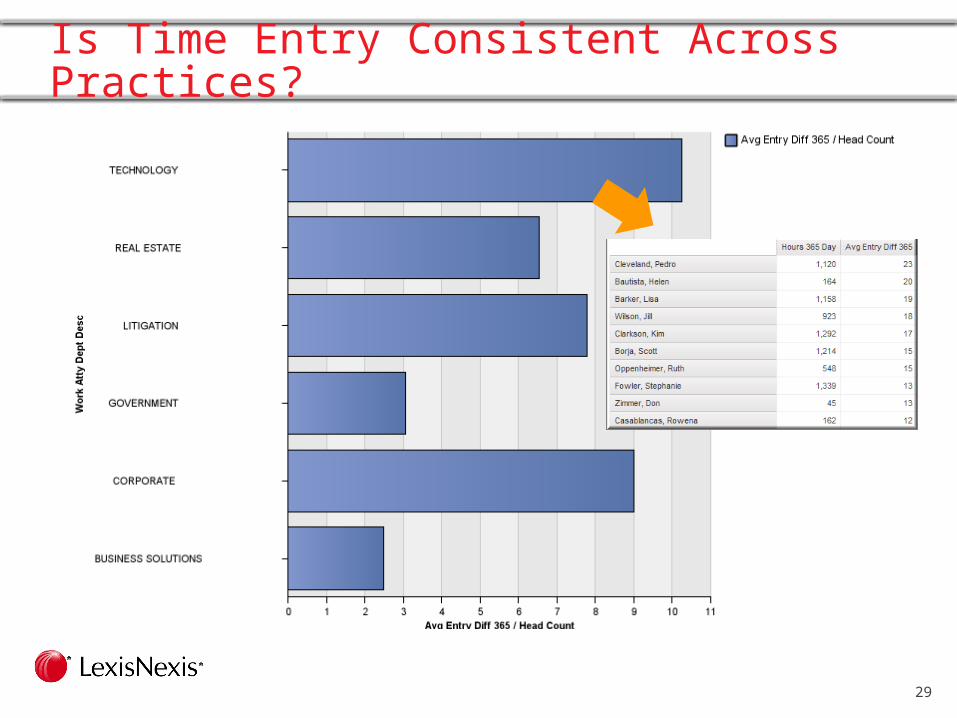

Quickly target time entry bandits

29

Is Time Entry Consistent Across Practices?

30

Review of B&C Concepts

Inventory• Indicates inventory levels/indicators at incremental points in

time• Use when interested in analyzing past performance and

looking for specific trends in inventory, A/R, and WIP

Daily Inventory• Nightly Build, Invoice Level, Fees & Costs• Most up-to-date look at current inventory, A/R, & WIP• Use when interested in influencing change now or when you

need a recent picture of your firm’s inventory status

31

Review of B&C Concepts

Work Period• Starting at the hour worked, what occurred to those hours

going forward?• Use when interested in working attorneys, departments,

etc., or when you are interested in understanding factors relating to production

Bill Period• Starting at the invoice, what occurred to the bill going

forward• Use when interested in bill attorneys and the performance

related to your billing practices

32

Review of B&C Concepts

Hours Hygiene• Allows for daily analysis of timekeeper hours and trends

related to those hours over time.• Use when interested in hours entry and analyzing the time

gaps that may exist between when work is performed versus entered into the system

2012 Redwood Analytics® User ConferenceAnalysis. Insight. Action.

Billing & Collections 101: Best Practices for Managing Firm Finances

Stuart AllenProduct Manager

![The Redwood gazette. (Redwood Falls, Minn.), 1925-06-17, [p ]. · 2019-10-27 · THE REDWOOD GAZETTE, REDWOOD FALLS, MINNESOTA The Redwood Gazette prints wedding an- nouncements or](https://img.dokumen.tips/doc/110x75/5fa04f2ead664330d06ddb4a/the-redwood-gazette-redwood-falls-minn-1925-06-17-p-2019-10-27-the.jpg)

![The Redwood gazette. (Redwood Falls, Minn.), 1915-09-29, [p ]](https://img.dokumen.tips/doc/110x75/6173cad0f9943f0e6327a621/the-redwood-gazette-redwood-falls-minn-1915-09-29-p-.jpg)

![The Redwood gazette. (Redwood Falls, Minn.), 1909-05-19, [p ]](https://img.dokumen.tips/doc/110x75/61f3066c4fb1c01f2e62eb08/the-redwood-gazette-redwood-falls-minn-1909-05-19-p-.jpg)