Embed Size (px)

Citation preview

8/4/2019 2006 Global Ag Blumenthal

http://slidepdf.com/reader/full/2006-global-ag-blumenthal 1/12

Limitations of Policies in“Creating Competitiveness”

Gary Blumenthal

World Perspectives, Inc.

The ne us between markets andpolicies…

rarely leads to a straightforwardstory of successful“competitiveness” in agriculture.

8/4/2019 2006 Global Ag Blumenthal

http://slidepdf.com/reader/full/2006-global-ag-blumenthal 2/12

Policy and Market Fundamentals

I. Farm Policy

II. Uruguay Round/Doha

III. Midwest AgriFood SystemFundamentals

I. False Premise of the Farm Bill

8/4/2019 2006 Global Ag Blumenthal

http://slidepdf.com/reader/full/2006-global-ag-blumenthal 3/12

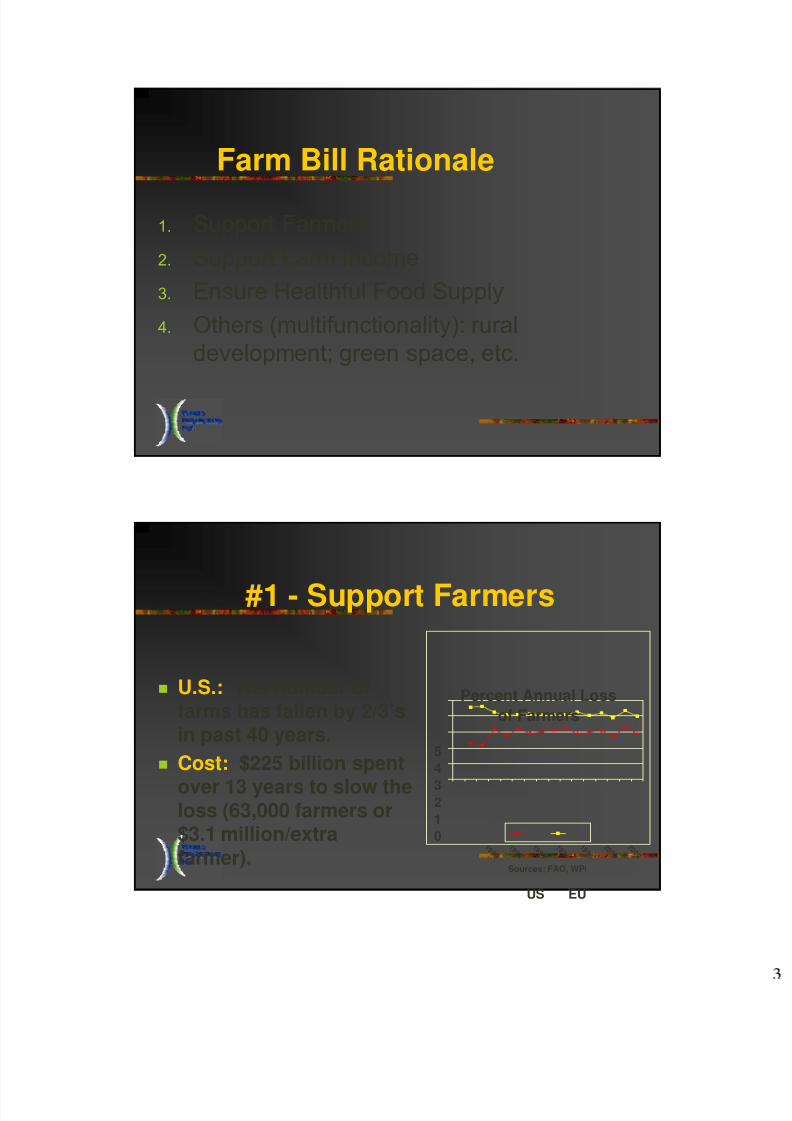

Farm Bill Rationale

1. Support Farmers

2. Support Farm Income

3. Ensure Healthful Food Supply

4. Others (multifunctionality): ruraldevelopment; green space, etc.

#1 - Support Farmers

U.S.: The number offarms has fallen by 2/3’sin past 40 years.

Cost: $225 billion spent

over 13 years to slow theloss (63,000 farmers or$3.1 million/extrafarmer).

Percent Annual Loss

of Farmers

0

1

23

4

5

1 9 9 0

1 9 9 2

1 9 9 4

1 9 9 6

1 9 9 8

2 0 0 0

2 0 0 2

Sources; FAO, WPI

US EU

8/4/2019 2006 Global Ag Blumenthal

http://slidepdf.com/reader/full/2006-global-ag-blumenthal 4/12

Efficiency Sheds Labor

102

104

106

108

110

112

114

M i l l i o

n s

1995 1997 1999 2001

Source: FAO

Latin American Farmers

012

345

M u l t i p l e o f A r e a

E x p a n s i o n

W h e a t

S o y b e a n s

G e n e r a l

Source: WPI

Survey of US Farmer

Expansion Ambition

2. Support Farm Income

Income higher under decoupling due to benefit of volatility; less harmful to competitiveness.

Gross Cash Receipts - 8 Commodities

46000

5100056000

61000

2 0 0 1

2 0 0 3

2 0 0 5

2 0 0 7

Sources: WPI, AgriLogic

$

M

i l l i o

n s

High Loan Rate

Current Policy

Baseline

All AMTA

Payment Type Influences Land Value

1000

1100

1200

1300

1400

1500

1600

1700

2002 2003 2004 2005 2006 2007 2008

Source: AgriLogic, WPI

$ / A c r e Inflation Only

Direct Payment

High Mkt Loan

8/4/2019 2006 Global Ag Blumenthal

http://slidepdf.com/reader/full/2006-global-ag-blumenthal 5/12

3. Ensure Healthful Food Supply

Obesity: #1 health issue

U.S.: F&V production isflat; imports up 50% infour years;

4. Other Farm Policy Goals

Rural - Development

Green Space Stewardship

Reduced commercial crop production…= reduced competitiveness

8/4/2019 2006 Global Ag Blumenthal

http://slidepdf.com/reader/full/2006-global-ag-blumenthal 6/12

Program Effectiveness versus Budget

OMB’s Program Assessment Rating Tool (PART)

Program PART Ranking

Bioenergy (ethanol) Adequate

CCC Marketing Loans Moderately Effective

CCC Export Guarantees Moderately Effective

Counter Cyclical Payments Adequate

Conservation Assistance Results Not DemonstratedCrop Insurance Results Not Demonstrated

Direct Crop Payments Adequate

Food Aid Moderately Effective

II. Trade Rounds

Helpful but Not the Sole Panacea

8/4/2019 2006 Global Ag Blumenthal

http://slidepdf.com/reader/full/2006-global-ag-blumenthal 7/12

8/4/2019 2006 Global Ag Blumenthal

http://slidepdf.com/reader/full/2006-global-ag-blumenthal 8/12

Constraints on Competitiveness

Rules-Based Trade:

Reduced government policies

≈ increased competition.

Trade is driven foremost by capacity

III. Competitive Advantages

8/4/2019 2006 Global Ag Blumenthal

http://slidepdf.com/reader/full/2006-global-ag-blumenthal 9/12

1. Capital/Resource Base

2. Technology

3. Management Capacity

Fundamental Midwest CompetitiveAdvantages

Capital/Resources

• $11 Trillion GDP;$38,000 per capita

• Water

• Land

4

1.7

1

0

1

2

3

4

Sources: UN, WPI

Fresh Water Per Capita

Nor th America Eurpope Asia

0.4 0.85

8.810.56

20.4

0

5

10

15

20

25

Sources: FAO, WPI

Arable Hectares Per Agricultural Person

Africa Asia Europe S. America NAFTA

8/4/2019 2006 Global Ag Blumenthal

http://slidepdf.com/reader/full/2006-global-ag-blumenthal 10/12

Technology Development and Utilization

Rabobank Study: Labor + Machinery -- U.S. is 25-45% less expensive thanBrazil and Argentinarespectively; technologieseclipse labor.

GIS, GPS, remotesensing, auto-steering

Biotechnology

53.8

17.5

7.7

0

10

20

30

40

50

60

MMT

GM Crop Expansion

Soybean

Corn

Wheat

Management Capacity

More highly educated farmers

Entrepreneurship

Readily transferable skills Culture

8/4/2019 2006 Global Ag Blumenthal

http://slidepdf.com/reader/full/2006-global-ag-blumenthal 11/12

8/4/2019 2006 Global Ag Blumenthal

http://slidepdf.com/reader/full/2006-global-ag-blumenthal 12/12

U.S. Farmer Attitudes

Government subsidies have actually stifled incentives for entrepreneurship among grain farmers by relieving financial pressure for them to adapt.

Those who prosper in this future agriculture must be willing to challenge their traditional comfort zone…

Create competitive advantages rather than protect old ones…[but this] will be much more difficult if

policymakers continue to emphasize income subsidies instead of strategic investments.

0

5

10

15

20

Liberalize Protect

Major U.S. Farm

OrganizationLiberalize by 2019?

Food Processing

“Agriculture” Sector

Production >20%

Growth: Labor,Packaging, Marketing

52,000 graduatesneeded (2005-2010),

49,300 projected. Food processing and

machinery the most prominentMidwest industry.

Once the most advanced inthe world.

•Attraction of capital.

•Risk/Reward

•Attention to regulatory

burden.

•U.S. fiscal management.

![D. S. Nº 043-2006-AG[1]](https://img.dokumen.tips/doc/110x75/5571f85c49795991698d4080/d-s-nao-043-2006-ag1.jpg)