Embed Size (px)

Citation preview

International Journal of Management (IJM), ISSN 0976 – 6502(Print), ISSN 0976 - 6510(Online),

Volume 5, Issue 12, December (2014), pp. 12-23 © IAEME

12

A STUDY ON CUSTOMER RELATIONSHIP

MANAGEMENT (CRM) EFFECTIVENESS IN PRIVATE

BANKS, TIRUCHIRAPPALLI

R. RAMACHANDRAN

Assistant Professor, Urumu Dhanalakshmi

College, Tiruchirappalli - 620 019.

Dr. S. SEKAR

Principal, Urumu Dhanalakshmi College,

Tiruchirappalli - 620 019.

ABSTRACT

Customer Relationship Management is a philosophy that places the customer at the center of

an organization's processes, activities and culture to improve his satisfaction levels and, in turn,

maximize profits for the organization. Customer Relationship Management stands for customer

relationship management and helps the management to deal with customer concerns and issues.

Different Banking Services and products like "Anywhere Banking" "Phone-Banking" "Electronic

banking" etc. are most commonly used by the customers now a days and the banks are trying to offer

innovative and convenient technology-based services to their customers. Simultaneously, Customer

Relationship Management helps in maintaining customer database and providing better services. The

use of Customer Relationship Management in banking has gained importance with the aggressive

approaches used for customer acquisition and retention by the bank in today’s competitive era. The

study mainly considered private Bank in the Study area. The Core dimensions of CRM are

Organizational commitment, Customer experience, Process-Driven Approach, Reliability, and

Technology Orientation. Theses dimensions were considered to identify its impacts towards the

result of CRM Dimensions like Customer Satisfaction, Customer Loyalty

And Cross-Buying

INTERNATIONAL JOURNAL OF MANAGEMENT (IJM)

ISSN 0976-6502 (Print)

ISSN 0976-6510 (Online)

Volume 5, Issue 12, December (2014), pp. 12-23

© IAEME: http://www.iaeme.com/IJM.asp

Journal Impact Factor (2014): 7.2230 (Calculated by GISI)

www.jifactor.com

IJM

© I A E M E

International Journal of Management (IJM), ISSN 0976 – 6502(Print), ISSN 0976 - 6510(Online),

Volume 5, Issue 12, December (2014), pp. 12-23 © IAEME

13

Key Words: Customer Relationship Management, Customer Experience, Process Driven Approach

and Technology Orientation.

1. INTRODUCTION

The Customer Relationship Management is an overall business strategy. Customer

Relationship Management is an integrated business approach that connects back office and front

office, uniting them into a single entity for the benefit of the customer. Different and unrelated

functions like sales force automation, inventory Management, customer services, sales and after-

sales support come together for a common Cause customer satisfaction.

The use of Customer Relationship Management in banking has gained importance with the

aggressive approaches used for customer acquisition and retention by the bank in today’s

competitive era. It has resulted in the adoption of various Customer Relationship Management

initiatives by these banks. There is a shift from bank centric activities to customer centric activities.

The private sector banks in India deployed much innovative strategies to attract new customers and

to retain existing customers.

Customer Relationship Management in banking industry entirely different from other sectors,

because banking industry purely related to financial services, which needs to create the trust among

the people. Establishing customer care support during on and off official hours, making timely

information about interest payments, maturity of time deposit, issuing credit and debit cum ATM

card, creating awareness regarding online and ebanking, adopting mobile request etc are required to

keep regular relationship with customers.

This study deals with the role of Customer Relationship Management in banking sector and

the need for it is to increase customer value by using some analytical methods in Customer

Relationship Management applications.

2. ISSUES RELATED TO CHANGING BANKING INDUSTRY

Technology was the nucleus of Customer Relationship Management strategies few years ago.

The technology was new, sophisticated and very difficult to manage. Now it is evolving to a

commodity piece within Customer Relationship Management strategies. Some issues related to

changing banking industry are:

� Integration of different systems- The integration of different systems such as customer data

and product data has improved dramatically. Due to lack of channel data and the dispersion of

channel responsibilities throughout the organization, most financial institutions develop channel

strategies and manage their channels poorly and in an uncoordinated fashion. This leads to sub-

optimal resource allocation and poor customer management. Leading banks have realized this

problem and are addressing this aggressively. The whole area of integrated channel management

which is tightly coupled with Customer Relationship Management will rapidly evolve to higher

levels of sophistication.

� Usage of multi-channel by customers- Multi-channel customers having real-time interface is

a buzzword. The First, customers use different channels to go to their bank such as the branch, self

service machines, the service center or the internet, Customer Relationship Management goes

multichannel. Second, in addition to cross selling, the processes of client retention and improvements

in client loyalty are getting more important. Firms have been slow to adopt due to the greater

complexity of the relationships and number of touch-points.

International Journal of Management (IJM), ISSN 0976 – 6502(Print), ISSN 0976 - 6510(Online),

Volume 5, Issue 12, December (2014), pp. 12-23 © IAEME

14

Branding- Customer Relationship Management will contribute more to branding. Not just

ROI on every contact will be leading, but the way customers want to be perceived as a brand will

become more important. Lot of effort is put on being there at customers' moments-of-truth.

3. THEORETICAL FRAMEWORK

(i) Effect of Customer Relationship Management Effectiveness and customer

satisfaction on customer loyalty

Customer loyalty is one of the most expected outcomes of successful Customer Relationship

Management efforts. It was argued that the Customer Relationship Management efforts lead to a

stronger relational bond and intense customer loyalty (Abratt and Russell, 1999; Farquhar, 2004).

The relationship efforts directed towards an individual customer influence his/her loyalty towards the

firm than when directed towards a group (Palmatier, 2006). Also, specific Customer Relationship

Management efforts such as expertise, promoting customer dependency, and increasing similarity to

customers increase customer commitment and loyalty than relationship investment and interaction

frequency. This indicated a differential impact of relationship activities Customer Relationship

Management in Indian retail banks on loyalty. Thus, it is argued that the impact of Customer

Relationship Management Effectiveness dimensions on customer loyalty to be context specific.

Customer satisfaction is one of the main predictors of loyalty. In a banking context,

satisfaction with the relationship serves as a basis for loyalty (Bloemer, 1998; Licata and

Chakraborty, 2009). Leverin and Liljander (2006) found that relationship satisfaction did indeed lead

to higher loyalty among customers who were treated with the sales-orientation approach. Similarly,

in the context of Australian bank customers, a higher level of satisfaction with relationship activities

was found to increase customer loyalty towards the bank (Pont and McQuilken, 2005).

(ii) Impact of customer satisfaction and customer loyalty on cross-buying

Customer intention to purchase multiple financial products depends on the level of overall

satisfaction they experience with the bank (Li, 2005). In addition, cross-selling reinforces customers’

relationship with the service provider and thereby influences their future purchase behaviors (Lemon

and Wangenheim, 2009). However, various studies have reported a contradictory finding of a weak

or insignificant relationship between satisfaction and cross-buying. For example, Ngobo (2004)

reported an insignificant relationship between customer satisfaction and cross-buying. While

customers might be satisfied with the current offerings of their primary service provider, they may

find other products offered by other providers as equal or more attractive. Moreover, when faced

with the need to buy a new product/service, customer satisfaction could be less relevant to cross-

buying (Gustafsson et al., 2005). However, since overall satisfaction and past purchase history

provide opportunities for firms to cross-sell related and unrelated products to existing customers.

Though customer loyalty has been a prominent area of research in marketing, remarkably few

studies have examined the link between loyalty and cross-buying. Many firms believe that loyalty

can result in multiple future purchases of the same product or other products. Nevertheless, the

evidence of this relationship is correlational (Gupta and Zeithaml, 2006). Reinartz (2008)

investigated the direction and strength of the relationship between loyalty and cross-buying using a

Granger causality test. They found that loyalty drives cross-buying. However, it was observed that

the level of customer spending differed across different product categories. Similarly, Gounaris

(2007) proposed that extremely loyal customers are motivated to buy additional products

International Journal of Management (IJM), ISSN 0976 – 6502(Print), ISSN 0976 - 6510(Online),

Volume 5, Issue 12, December (2014), pp. 12-23 © IAEME

15

4. SCOPE FOR THE STUDY

This study will provide a health scale to measure Customer relationship management

effectiveness in the banking context. The study will bring out the relationship between CRM efforts

and relational outcomes of satisfaction, loyalty and cross buying.

5. STATEMENT OF THE PROBLEM

Customer loyalty is one of the most expected outcomes of successful CRM efforts. It was

argued that the CRM efforts lead to a stronger relational bond and intense customer loyalty. Specific

CRM efforts such as expertise, promoting customer dependency, and increasing similarity to

customers increase customer commitment and loyalty than relationship investment and interaction

frequency. This indicated a differential impact of relationship activities on loyalty. Thus CRM

dimensions create positive impact towards customer loyalty which will lead to satisfaction and cross

buying.

6. OBJECTIVES FOR THE STUDY

1. To study the customer relationship management effectiveness dimensions

2. To identify the customer satisfaction level towards bank

3. To predict customer loyalty and cross buying.

7. METHODS AND METHODOLOGY

The Study is descriptive in nature. The study is done to measure customer relationship

management effectiveness in private banks in Tiruchirapalli. The population of the study constitutes

to the customers of the selected private sector banks (ICICI, KVB, Axis and HDFC Banks) in

Tiruchirapalli. The purpose of the study was explained to the customers. The customers who were

wished to participate were considered as Sample Size. The sample size for the study is 210 by

adopting simple random sampling technique.

Scaling involves ranking individuals according to a classificatory system. It is ordering of a

number of related items (descriptive characteristic or attitude statements) to form a continuum in

order to provide a means of quantitative measurement of qualitative variables. It requires assigning

scores or numbers to the variables or attributes being measured. For the present study, five point

scaling technique were used for getting responses from the respondents (customers) in the study area

through appropriate scoring pattern and it was collected in the form of questionnaire type of research

tool.

Both Primary and Secondary data were considered for the study. The primary data were

collected from questionnaire, which consists of eight dimensions Organization Commitment,

Customer Experience, Process Driven Approach, Reliability, Technology Orientation, Customer

Satisfaction, Customer loyalty and Cross buying and finally questions regarding the personal details

of the customers. Secondary data were collected from books, study materials and internet.

Appropriate Statistical technologies are used to supplement the analysis and data

interpretation. Statistical techniques like Chi-square and Correlation are applied with the help of

SPSS. V 18 (Statistical Package Tools for Social Science) at the appropriate juncture.

International Journal of Management (IJM), ISSN 0976 – 6502(Print), ISSN 0976 - 6510(Online),

Volume 5, Issue 12, December (2014), pp. 12-23 © IAEME

16

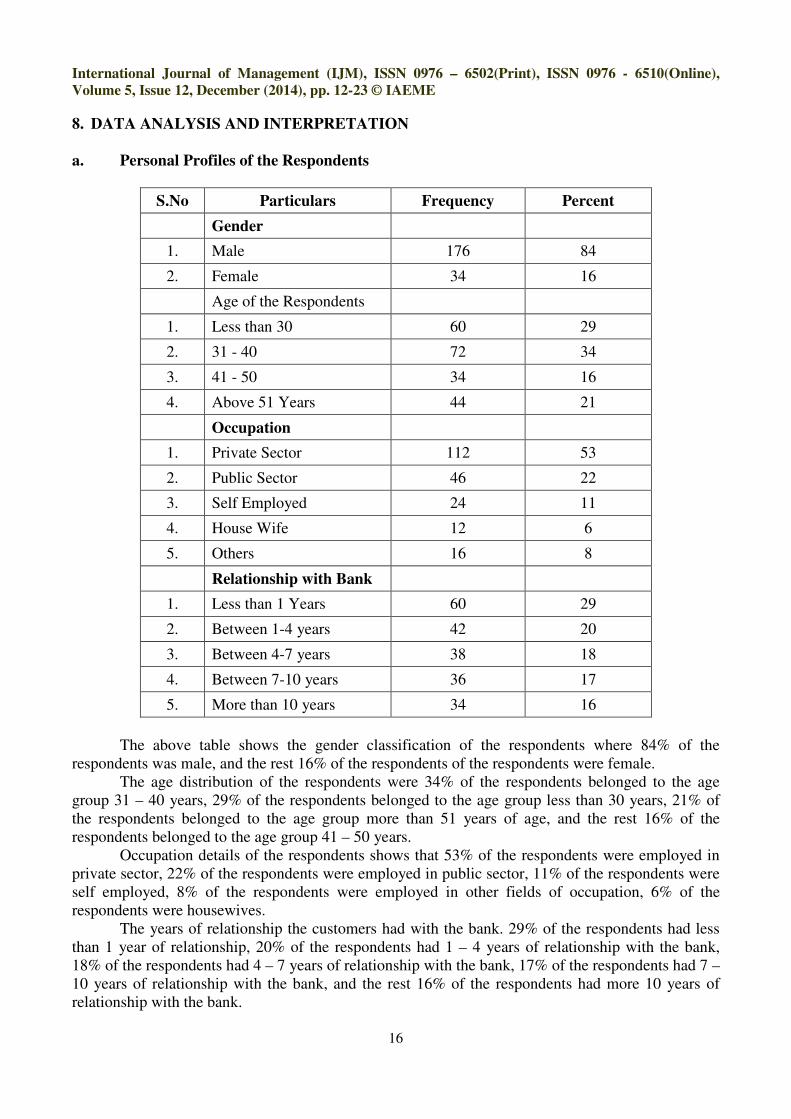

8. DATA ANALYSIS AND INTERPRETATION

a. Personal Profiles of the Respondents

S.No Particulars Frequency Percent

Gender

1. Male 176 84

2. Female 34 16

Age of the Respondents

1. Less than 30 60 29

2. 31 - 40 72 34

3. 41 - 50 34 16

4. Above 51 Years 44 21

Occupation

1. Private Sector 112 53

2. Public Sector 46 22

3. Self Employed 24 11

4. House Wife 12 6

5. Others 16 8

Relationship with Bank

1. Less than 1 Years 60 29

2. Between 1-4 years 42 20

3. Between 4-7 years 38 18

4. Between 7-10 years 36 17

5. More than 10 years 34 16

The above table shows the gender classification of the respondents where 84% of the

respondents was male, and the rest 16% of the respondents of the respondents were female.

The age distribution of the respondents were 34% of the respondents belonged to the age

group 31 – 40 years, 29% of the respondents belonged to the age group less than 30 years, 21% of

the respondents belonged to the age group more than 51 years of age, and the rest 16% of the

respondents belonged to the age group 41 – 50 years.

Occupation details of the respondents shows that 53% of the respondents were employed in

private sector, 22% of the respondents were employed in public sector, 11% of the respondents were

self employed, 8% of the respondents were employed in other fields of occupation, 6% of the

respondents were housewives.

The years of relationship the customers had with the bank. 29% of the respondents had less

than 1 year of relationship, 20% of the respondents had 1 – 4 years of relationship with the bank,

18% of the respondents had 4 – 7 years of relationship with the bank, 17% of the respondents had 7 –

10 years of relationship with the bank, and the rest 16% of the respondents had more 10 years of

relationship with the bank.

International Journal of Management (IJM), ISSN 0976 – 6502(Print), ISSN 0976 - 6510(Online),

Volume 5, Issue 12, December (2014), pp. 12-23 © IAEME

17

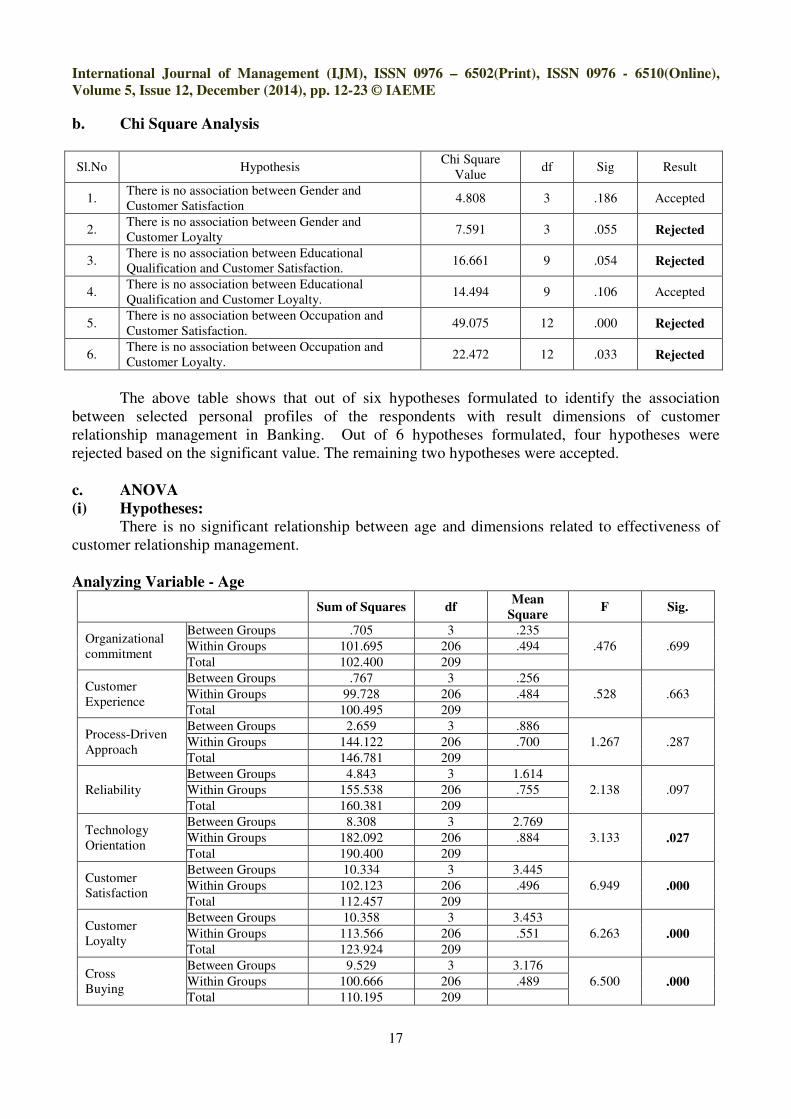

b. Chi Square Analysis

Sl.No Hypothesis Chi Square

Value df Sig Result

1. There is no association between Gender and

Customer Satisfaction 4.808 3 .186 Accepted

2. There is no association between Gender and

Customer Loyalty 7.591 3 .055 Rejected

3. There is no association between Educational

Qualification and Customer Satisfaction. 16.661 9 .054 Rejected

4. There is no association between Educational

Qualification and Customer Loyalty. 14.494 9 .106 Accepted

5. There is no association between Occupation and

Customer Satisfaction. 49.075 12 .000 Rejected

6. There is no association between Occupation and

Customer Loyalty. 22.472 12 .033 Rejected

The above table shows that out of six hypotheses formulated to identify the association

between selected personal profiles of the respondents with result dimensions of customer

relationship management in Banking. Out of 6 hypotheses formulated, four hypotheses were

rejected based on the significant value. The remaining two hypotheses were accepted.

c. ANOVA

(i) Hypotheses:

There is no significant relationship between age and dimensions related to effectiveness of

customer relationship management.

Analyzing Variable - Age

Sum of Squares df Mean

Square F Sig.

Organizational

commitment

Between Groups .705 3 .235

.476 .699 Within Groups 101.695 206 .494

Total 102.400 209

Customer

Experience

Between Groups .767 3 .256

.528 .663 Within Groups 99.728 206 .484

Total 100.495 209

Process-Driven

Approach

Between Groups 2.659 3 .886

1.267 .287 Within Groups 144.122 206 .700

Total 146.781 209

Reliability

Between Groups 4.843 3 1.614

2.138 .097 Within Groups 155.538 206 .755

Total 160.381 209

Technology

Orientation

Between Groups 8.308 3 2.769

3.133 .027 Within Groups 182.092 206 .884

Total 190.400 209

Customer

Satisfaction

Between Groups 10.334 3 3.445

6.949 .000 Within Groups 102.123 206 .496

Total 112.457 209

Customer

Loyalty

Between Groups 10.358 3 3.453

6.263 .000 Within Groups 113.566 206 .551

Total 123.924 209

Cross

Buying

Between Groups 9.529 3 3.176

6.500 .000 Within Groups 100.666 206 .489

Total 110.195 209

International Journal of Management (IJM), ISSN 0976 – 6502(Print), ISSN 0976 - 6510(Online),

Volume 5, Issue 12, December (2014), pp. 12-23 © IAEME

18

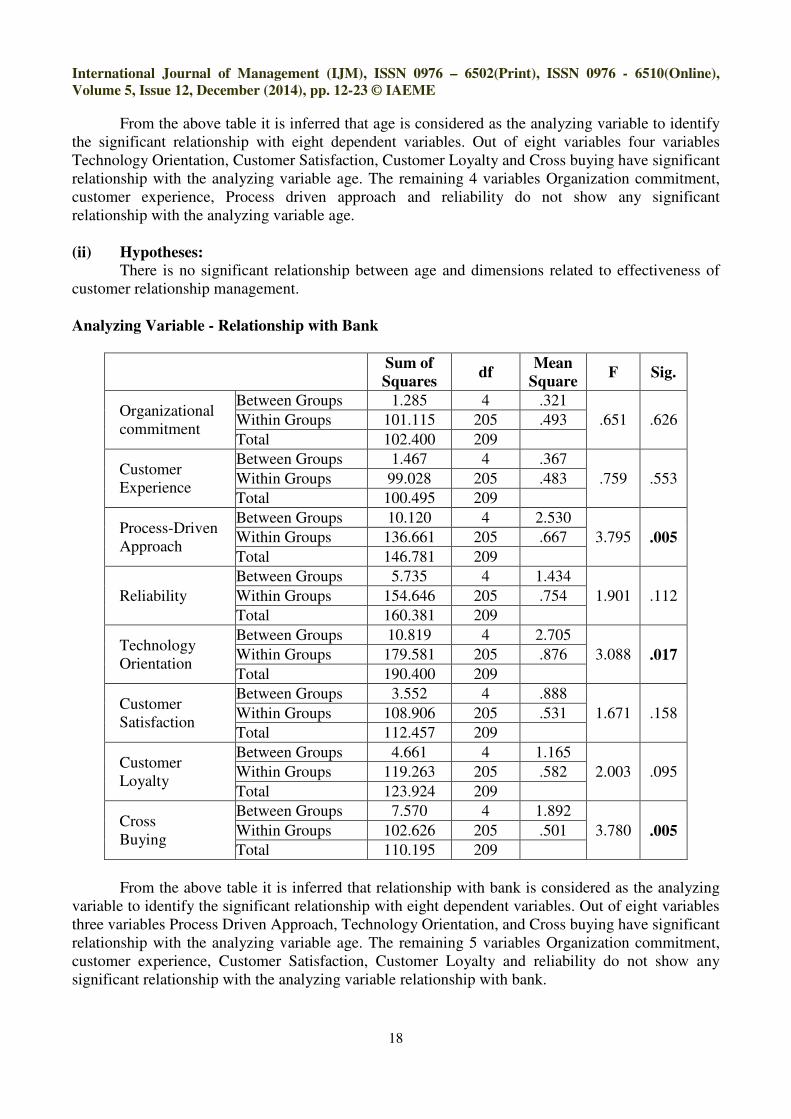

From the above table it is inferred that age is considered as the analyzing variable to identify

the significant relationship with eight dependent variables. Out of eight variables four variables

Technology Orientation, Customer Satisfaction, Customer Loyalty and Cross buying have significant

relationship with the analyzing variable age. The remaining 4 variables Organization commitment,

customer experience, Process driven approach and reliability do not show any significant

relationship with the analyzing variable age.

(ii) Hypotheses:

There is no significant relationship between age and dimensions related to effectiveness of

customer relationship management.

Analyzing Variable - Relationship with Bank

Sum of

Squares df

Mean

Square F Sig.

Organizational

commitment

Between Groups 1.285 4 .321

.651 .626 Within Groups 101.115 205 .493

Total 102.400 209

Customer

Experience

Between Groups 1.467 4 .367

.759 .553 Within Groups 99.028 205 .483

Total 100.495 209

Process-Driven

Approach

Between Groups 10.120 4 2.530

3.795 .005 Within Groups 136.661 205 .667

Total 146.781 209

Reliability

Between Groups 5.735 4 1.434

1.901 .112 Within Groups 154.646 205 .754

Total 160.381 209

Technology

Orientation

Between Groups 10.819 4 2.705

3.088 .017 Within Groups 179.581 205 .876

Total 190.400 209

Customer

Satisfaction

Between Groups 3.552 4 .888

1.671 .158 Within Groups 108.906 205 .531

Total 112.457 209

Customer

Loyalty

Between Groups 4.661 4 1.165

2.003 .095 Within Groups 119.263 205 .582

Total 123.924 209

Cross

Buying

Between Groups 7.570 4 1.892

3.780 .005 Within Groups 102.626 205 .501

Total 110.195 209

From the above table it is inferred that relationship with bank is considered as the analyzing

variable to identify the significant relationship with eight dependent variables. Out of eight variables

three variables Process Driven Approach, Technology Orientation, and Cross buying have significant

relationship with the analyzing variable age. The remaining 5 variables Organization commitment,

customer experience, Customer Satisfaction, Customer Loyalty and reliability do not show any

significant relationship with the analyzing variable relationship with bank.

International Journal of Management (IJM), ISSN 0976 – 6502(Print), ISSN 0976 - 6510(Online),

Volume 5, Issue 12, December (2014), pp. 12-23 © IAEME

19

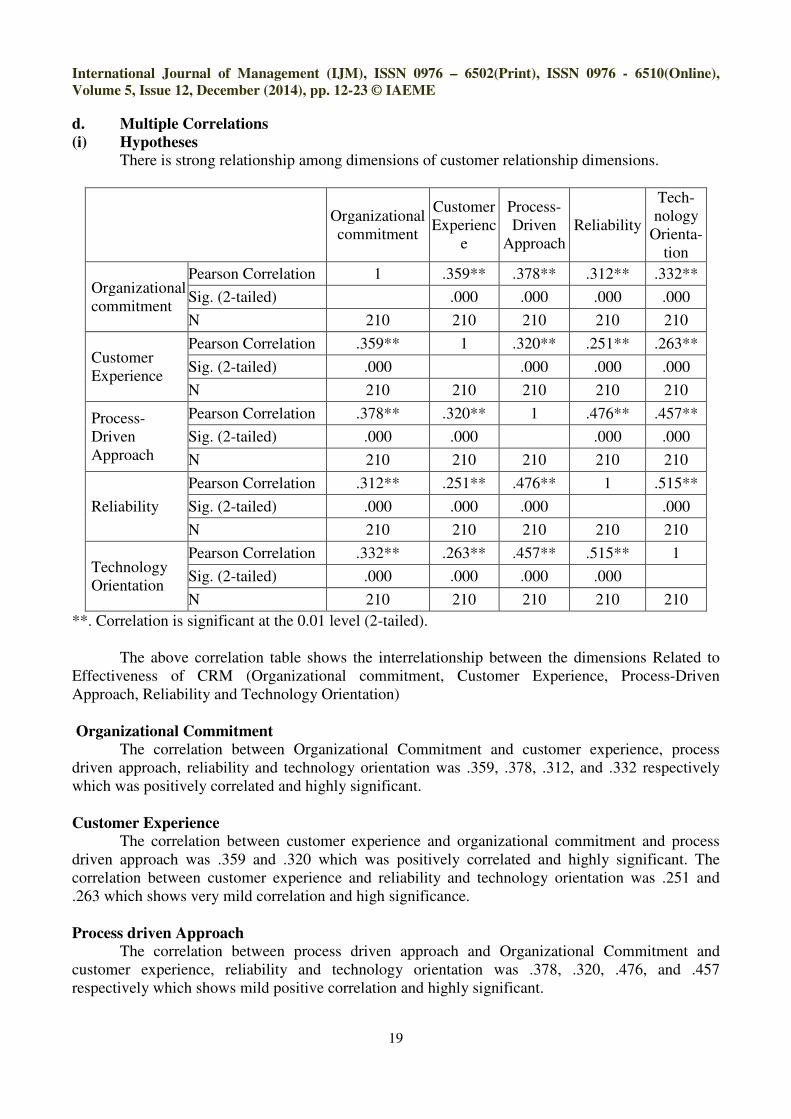

d. Multiple Correlations

(i) Hypotheses

There is strong relationship among dimensions of customer relationship dimensions.

Organizational

commitment

Customer

Experienc

e

Process-

Driven

Approach

Reliability

Tech-

nology

Orienta-

tion

Organizational

commitment

Pearson Correlation 1 .359** .378** .312** .332**

Sig. (2-tailed) .000 .000 .000 .000

N 210 210 210 210 210

Customer

Experience

Pearson Correlation .359** 1 .320** .251** .263**

Sig. (2-tailed) .000 .000 .000 .000

N 210 210 210 210 210

Process-

Driven

Approach

Pearson Correlation .378** .320** 1 .476** .457**

Sig. (2-tailed) .000 .000 .000 .000

N 210 210 210 210 210

Reliability

Pearson Correlation .312** .251** .476** 1 .515**

Sig. (2-tailed) .000 .000 .000 .000

N 210 210 210 210 210

Technology

Orientation

Pearson Correlation .332** .263** .457** .515** 1

Sig. (2-tailed) .000 .000 .000 .000

N 210 210 210 210 210

**. Correlation is significant at the 0.01 level (2-tailed).

The above correlation table shows the interrelationship between the dimensions Related to

Effectiveness of CRM (Organizational commitment, Customer Experience, Process-Driven

Approach, Reliability and Technology Orientation)

Organizational Commitment

The correlation between Organizational Commitment and customer experience, process

driven approach, reliability and technology orientation was .359, .378, .312, and .332 respectively

which was positively correlated and highly significant.

Customer Experience

The correlation between customer experience and organizational commitment and process

driven approach was .359 and .320 which was positively correlated and highly significant. The

correlation between customer experience and reliability and technology orientation was .251 and

.263 which shows very mild correlation and high significance.

Process driven Approach

The correlation between process driven approach and Organizational Commitment and

customer experience, reliability and technology orientation was .378, .320, .476, and .457

respectively which shows mild positive correlation and highly significant.

International Journal of Management (IJM), ISSN 0976 – 6502(Print), ISSN 0976 - 6510(Online),

Volume 5, Issue 12, December (2014), pp. 12-23 © IAEME

20

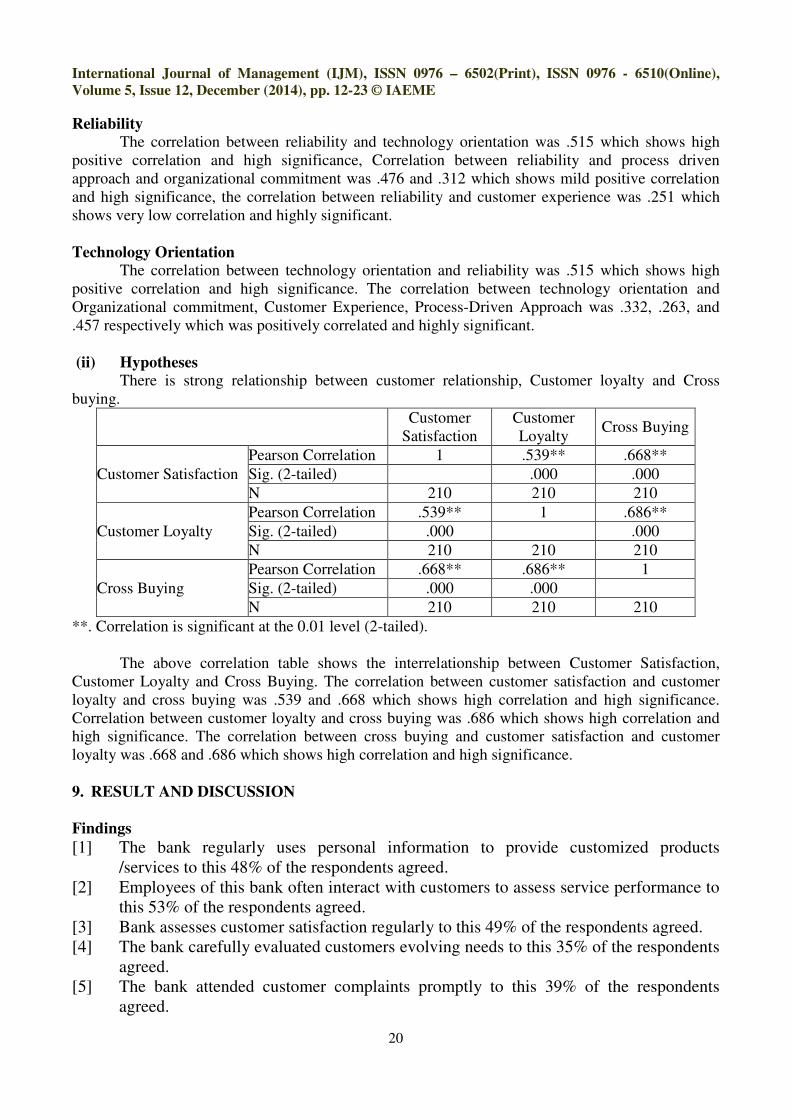

Reliability

The correlation between reliability and technology orientation was .515 which shows high

positive correlation and high significance, Correlation between reliability and process driven

approach and organizational commitment was .476 and .312 which shows mild positive correlation

and high significance, the correlation between reliability and customer experience was .251 which

shows very low correlation and highly significant.

Technology Orientation

The correlation between technology orientation and reliability was .515 which shows high

positive correlation and high significance. The correlation between technology orientation and

Organizational commitment, Customer Experience, Process-Driven Approach was .332, .263, and

.457 respectively which was positively correlated and highly significant.

(ii) Hypotheses

There is strong relationship between customer relationship, Customer loyalty and Cross

buying.

Customer

Satisfaction

Customer

Loyalty Cross Buying

Customer Satisfaction

Pearson Correlation 1 .539** .668**

Sig. (2-tailed) .000 .000

N 210 210 210

Customer Loyalty

Pearson Correlation .539** 1 .686**

Sig. (2-tailed) .000 .000

N 210 210 210

Cross Buying

Pearson Correlation .668** .686** 1

Sig. (2-tailed) .000 .000

N 210 210 210

**. Correlation is significant at the 0.01 level (2-tailed).

The above correlation table shows the interrelationship between Customer Satisfaction,

Customer Loyalty and Cross Buying. The correlation between customer satisfaction and customer

loyalty and cross buying was .539 and .668 which shows high correlation and high significance.

Correlation between customer loyalty and cross buying was .686 which shows high correlation and

high significance. The correlation between cross buying and customer satisfaction and customer

loyalty was .668 and .686 which shows high correlation and high significance.

9. RESULT AND DISCUSSION

Findings

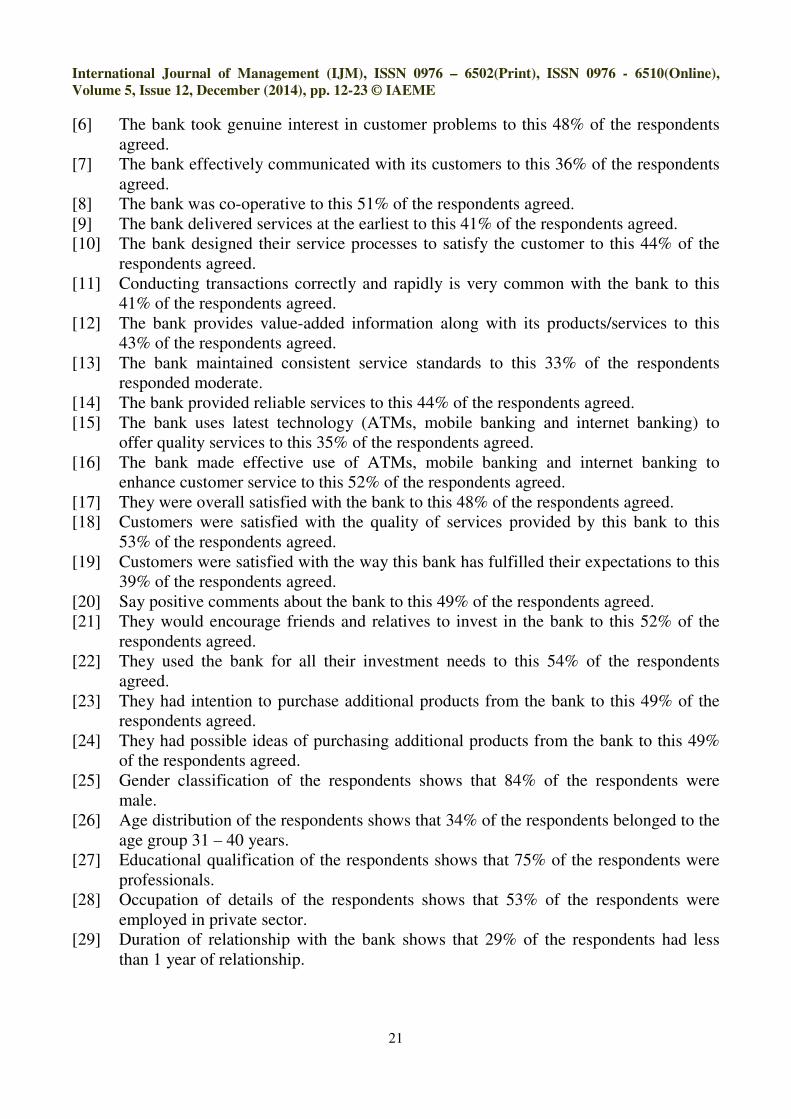

[1] The bank regularly uses personal information to provide customized products

/services to this 48% of the respondents agreed.

[2] Employees of this bank often interact with customers to assess service performance to

this 53% of the respondents agreed.

[3] Bank assesses customer satisfaction regularly to this 49% of the respondents agreed.

[4] The bank carefully evaluated customers evolving needs to this 35% of the respondents

agreed.

[5] The bank attended customer complaints promptly to this 39% of the respondents

agreed.

International Journal of Management (IJM), ISSN 0976 – 6502(Print), ISSN 0976 - 6510(Online),

Volume 5, Issue 12, December (2014), pp. 12-23 © IAEME

21

[6] The bank took genuine interest in customer problems to this 48% of the respondents

agreed.

[7] The bank effectively communicated with its customers to this 36% of the respondents

agreed.

[8] The bank was co-operative to this 51% of the respondents agreed.

[9] The bank delivered services at the earliest to this 41% of the respondents agreed.

[10] The bank designed their service processes to satisfy the customer to this 44% of the

respondents agreed.

[11] Conducting transactions correctly and rapidly is very common with the bank to this

41% of the respondents agreed.

[12] The bank provides value-added information along with its products/services to this

43% of the respondents agreed.

[13] The bank maintained consistent service standards to this 33% of the respondents

responded moderate.

[14] The bank provided reliable services to this 44% of the respondents agreed.

[15] The bank uses latest technology (ATMs, mobile banking and internet banking) to

offer quality services to this 35% of the respondents agreed.

[16] The bank made effective use of ATMs, mobile banking and internet banking to

enhance customer service to this 52% of the respondents agreed.

[17] They were overall satisfied with the bank to this 48% of the respondents agreed.

[18] Customers were satisfied with the quality of services provided by this bank to this

53% of the respondents agreed.

[19] Customers were satisfied with the way this bank has fulfilled their expectations to this

39% of the respondents agreed.

[20] Say positive comments about the bank to this 49% of the respondents agreed.

[21] They would encourage friends and relatives to invest in the bank to this 52% of the

respondents agreed.

[22] They used the bank for all their investment needs to this 54% of the respondents

agreed.

[23] They had intention to purchase additional products from the bank to this 49% of the

respondents agreed.

[24] They had possible ideas of purchasing additional products from the bank to this 49%

of the respondents agreed.

[25] Gender classification of the respondents shows that 84% of the respondents were

male.

[26] Age distribution of the respondents shows that 34% of the respondents belonged to the

age group 31 – 40 years.

[27] Educational qualification of the respondents shows that 75% of the respondents were

professionals.

[28] Occupation of details of the respondents shows that 53% of the respondents were

employed in private sector.

[29] Duration of relationship with the bank shows that 29% of the respondents had less

than 1 year of relationship.

International Journal of Management (IJM), ISSN 0976 – 6502(Print), ISSN 0976 - 6510(Online),

Volume 5, Issue 12, December (2014), pp. 12-23 © IAEME

22

Suggestions

[1] The Bank should always use personal information to provide customized products and

service rather than other means of communication.

[2] The employees of the bank should periodically meet the customers and ensure their

service quality and identify the changing needs of the customers.

[3] The Bank should give priority to solve the customer’s complaints. The Complaint

handling systems should be transparent.

[4] The bank should always shows genuine interest towards customer request and the

flow of communication between Bank and Customers should be effective.

[5] The services provided by the Bank should be fast, correct, reliable and Trustworthy.

[6] The bank should always provide value added service along with it normal products.

[7] The Bank should always be consistent with its all service providing and portfolios.

[8] The Bank should always update to latest and modern technology.

[9] The Bank should adopt right strategy to satisfy all the customers’ expectations.

[10] The bank should formulate strategies to customers loyalty towards Banks which will

in turn make the customers to say positive word of mouth about the Bank.

[11] The Bank should always give priority to customer satisfaction and loyalty, which in

turn will increase the cross selling.

[12] There should be always positive relationship between dimensions of CRM, Customer

satisfaction, Customer loyalty and Cross selling

CONCLUSION

The study findings have significant implications for bank managers. The identified key

dimensions of CRM should be implemented to enhance the business performance. The five

dimensions namely, organizational commitment, customer experience, process-driven approach,

reliability and technology orientation which measured the effectiveness of CRM efforts in banks.

The identification of these dimensions enables bank managers to design an effective CRM that

fosters enduring relationships with customers. Further, these dimensions emphasize that CRM efforts

should focus on key areas such as process, technology, management and people. Thus, bank

managers should focus on all the five dimensions to maximize CRM effectiveness.

REFERENCE

[1] Abratt, R. and Russell, J. (1999), “Relationship marketing in private banking in South

Africa”, International Journal of Bank Marketing, Vol. 17 No. 1, pp. 5-19.

[2] Bloemer, J., De Ruyter, K. and Peeters, K. (1998), “Investigating drivers of bank loyalty: the

complex relationship between image, service quality and satisfaction”, International Journal

of Bank Marketing, Vol. 16 Nos 6/7, pp. 276-86.

[3] Gounaris, S.P., Tzempelikos, N.A. and Chatzipanagiotou, K. (2007), “The relationships of

customer-perceived value, satisfaction, loyalty and behavioral intentions”, Journal of

Relationship Marketing, Vol. 6 No. 1, pp. 63-87.

[4] Gupta, S. and Zeithaml, V. (2006), “Customer metrics and their impact on financial

performance”, Marketing Science, Vol. 25 No. 6, pp. 718-39

[5] Gustafsson, A., Johnson, M.D. and Roos, I. (2005), “The effects of customer satisfaction,

relationship commitment dimensions, and triggers on customer retention”, The Journal of

Marketing, Vol. 69 No. 4, pp. 210-8.

International Journal of Management (IJM), ISSN 0976 – 6502(Print), ISSN 0976 - 6510(Online),

Volume 5, Issue 12, December (2014), pp. 12-23 © IAEME

23

[6] Lemon, K.N. and Wangenheim, F. (2009), “The reinforcing effects of loyalty program

partnerships and core service usage”, Journal of Service Research, Vol. 11 No. 4, pp. 357-70.

[7] Leverin, A. and Liljander, V. (2006), “Does relationship marketing improve customer

relationship satisfaction and loyalty?”, International Journal of Bank Marketing, Vol. 24 No.

4, pp. 232-51.

[8] Li, S., Sun, B. and Wilcox, R.T. (2005), “Cross-selling sequentially ordered products: an

application to consumer banking services”, Journal of Marketing Research, Vol. 42 No. 2, pp.

233-9.

[9] Ngobo, P.V. (2004), “Drivers of customers’ cross-buying intentions”, European Journal of

Marketing, Vol. 38 Nos 9/10, pp. 1129-57.

[10] Palmatier, R.W., Dant, R.P., Grewal, D. and Evans, K.R. (2006), “Factors influencing the

effectiveness of relationship marketing: a meta-analysis”, Journal of Marketing, Vol. 70 No.

4, pp. 136-53.

[11] Reinartz, W., Thomas, J.S. and Bascoul, G. (2008), “Investigating cross-buying and customer

loyalty”, Journal of Interactive Marketing, Vol. 22 No. 1, pp. 5-20.

[12] Sandip Dhakecha, “A Study on Effectiveness of Cause Related Marketing [CRM] as a

Strategic Philanthropy in Terms of Brand Popularity & Sales”, International Journal of

Marketing & Human Resource Management (IJMHRM), Volume 4, Issue 1, 2013, pp. 28 -

39, ISSN Print: 0976 – 6421, ISSN Online: 0976- 643X.

[13] Allahyar Beigi Firoozi, Mehran Aslaniyan, Faranak Yusefvand and Mojtaba Pahlavani,

“Formulating and Prioritizing CRM Implementation Strategies in Mehr Eghtesad Bank of

Iran using Combinational Model of PIP and ANP”, International Journal of Marketing &

Human Resource Management (IJMHRM), Volume 4, Issue 2, 2013, pp. 40 - 53, ISSN Print:

0976 – 6421, ISSN Online: 0976- 643X.

[14] Dr. V.Antony Joe Raja, “New Strategy in Today Banking Sector: Bank Customer

Relationship Management (CRM) & Marketing Mix in World”, International Journal of

Marketing & Human Resource Management (IJMHRM), Volume 4, Issue 3, 2013, pp. 19 -

29, ISSN Print: 0976 – 6421, ISSN Online: 0976- 643X.

[15] T.Vijayakumar and Dr. R. Velu, “Customer Relationship Management in Indian Retail

Banking Industry”, International Journal of Management (IJM), Volume 2, Issue 1, 2011, pp.

41 - 51, ISSN Print: 0976-6502, ISSN Online: 0976-6510.