Embed Size (px)

Citation preview

16th ANNUAL MULTIFAMILY DEVELOPERS FORUM

Presented by:

Russ Callahan: Tavernier Capital Partners, LLC

Al Moczul: Tavernier Capital Funding, LLC

FANNIE, FREDDIE & LIFE COMPANY FINANCINGPresented by: Russ Callahan

Tavernier Capital Partners, LLC is a privately owned full service commercial mortgage banking company.

Senior Managers of Capmark Finance Inc. formed Tavernier Capital in February 2007 with the acquisition of the Florida Mortgage Banking Operations of Capmark, formerly GMAC Commercial Mortgage.

Tavernier Capital is a leading commercial mortgage banking operation in Florida and one of the largest commercial mortgage bankers in the Southeast, with offices in Jacksonville, Orlando, Tampa, Boca Raton and Miami.

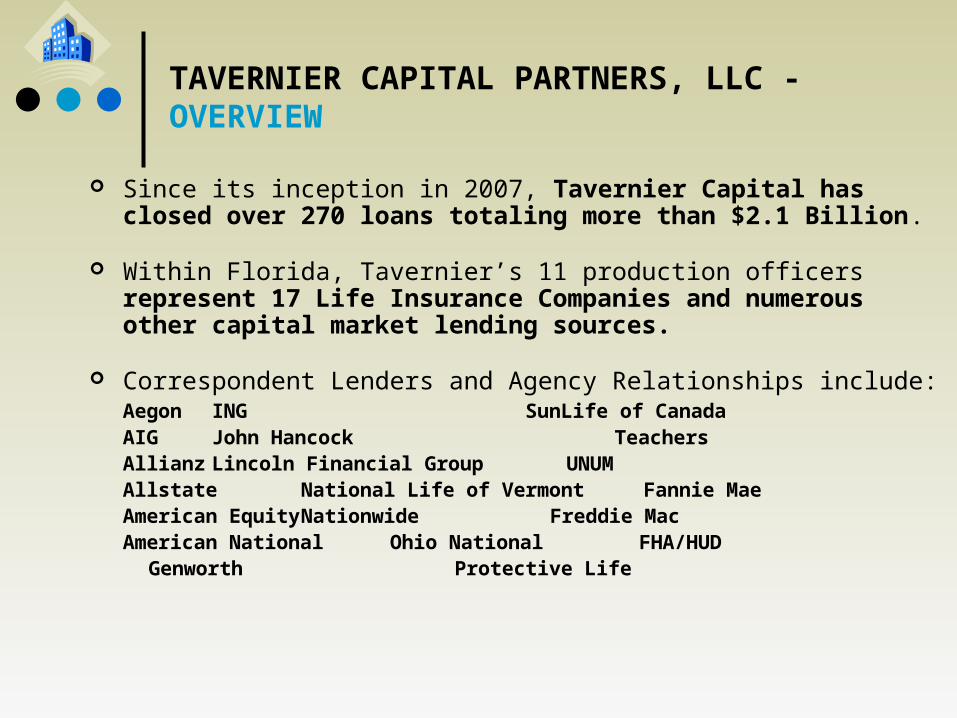

TAVERNIER CAPITAL PARTNERS, LLC - OVERVIEW

Since its inception in 2007, Tavernier Capital has closed over 270 loans totaling more than $2.1 Billion.

Within Florida, Tavernier’s 11 production officers represent 17 Life Insurance Companies and numerous other capital market lending sources.

Correspondent Lenders and Agency Relationships include: Aegon ING SunLife of CanadaAIG John Hancock TeachersAllianz Lincoln Financial Group UNUMAllstate National Life of Vermont Fannie MaeAmerican Equity Nationwide Freddie MacAmerican National Ohio National FHA/HUD

Genworth Protective Life

TAVERNIER CAPITAL PARTNERS, LLC - OVERVIEW

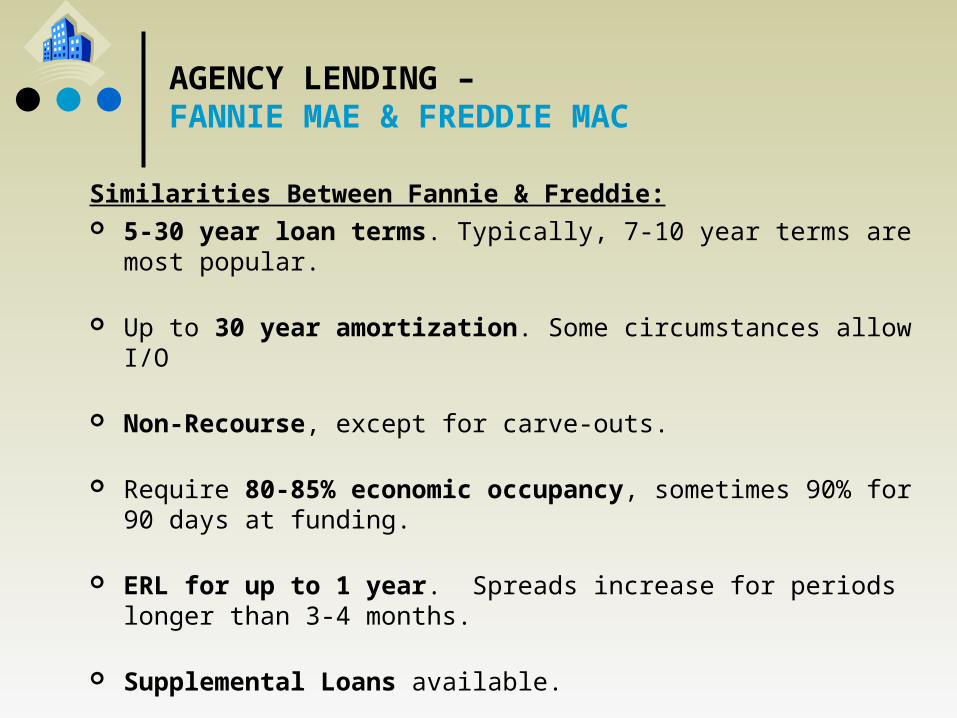

Similarities Between Fannie & Freddie: 5-30 year loan terms. Typically, 7-10 year terms are most

popular.

Up to 30 year amortization. Some circumstances allow I/O

Non-Recourse, except for carve-outs.

Require 80-85% economic occupancy, sometimes 90% for 90 days at funding.

ERL for up to 1 year. Spreads increase for periods longer than 3-4 months.

Supplemental Loans available.

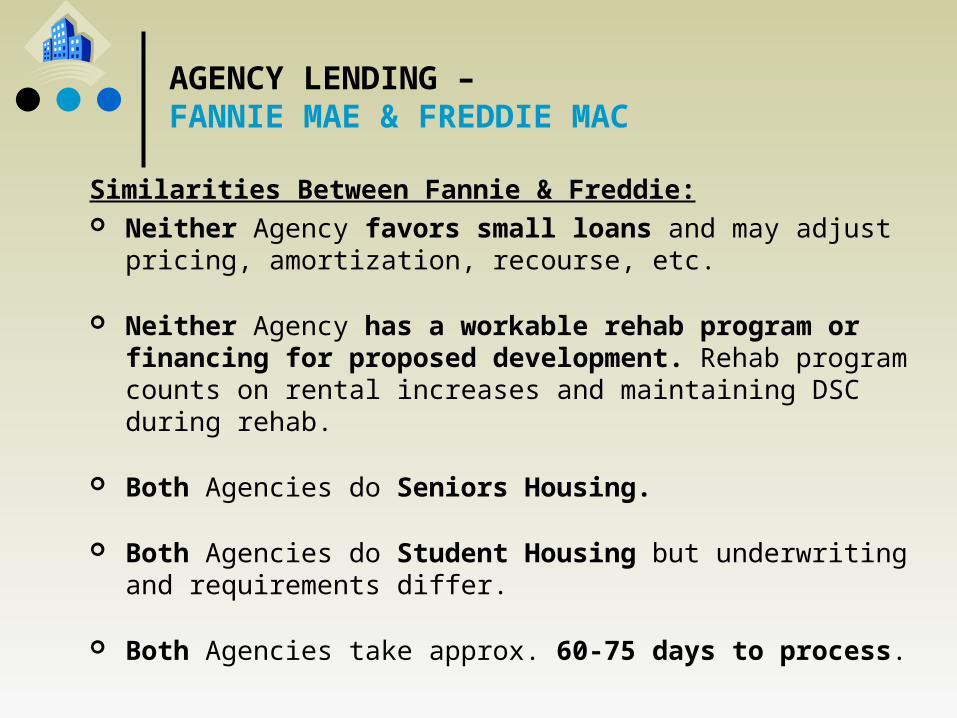

AGENCY LENDING – FANNIE MAE & FREDDIE MAC

Similarities Between Fannie & Freddie: Neither Agency favors small loans and may adjust

pricing, amortization, recourse, etc.

Neither Agency has a workable rehab program or financing for proposed development. Rehab program counts on rental increases and maintaining DSC during rehab.

Both Agencies do Seniors Housing.

Both Agencies do Student Housing but underwriting and requirements differ.

Both Agencies take approx. 60-75 days to process.

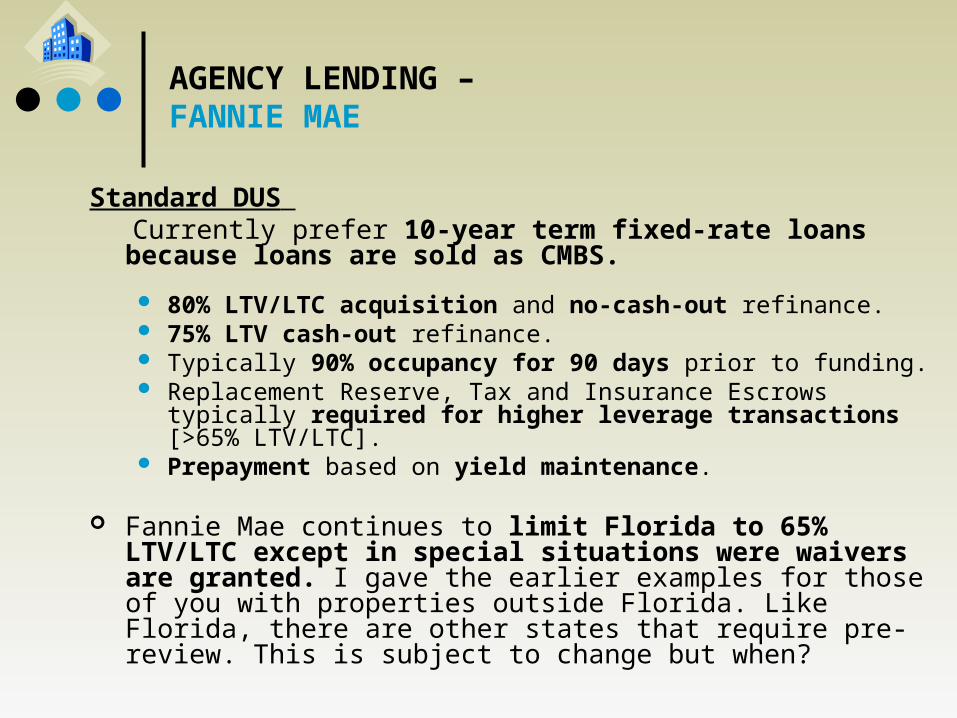

AGENCY LENDING – FANNIE MAE & FREDDIE MAC

Standard DUS Currently prefer 10-year term fixed-rate loans because

loans are sold as CMBS.

80% LTV/LTC acquisition and no-cash-out refinance. 75% LTV cash-out refinance. Typically 90% occupancy for 90 days prior to funding. Replacement Reserve, Tax and Insurance Escrows typically

required for higher leverage transactions [>65% LTV/LTC]. Prepayment based on yield maintenance.

Fannie Mae continues to limit Florida to 65% LTV/LTC except in special situations were waivers are granted. I gave the earlier examples for those of you with properties outside Florida. Like Florida, there are other states that require pre-review. This is subject to change but when?

AGENCY LENDING – FANNIE MAE

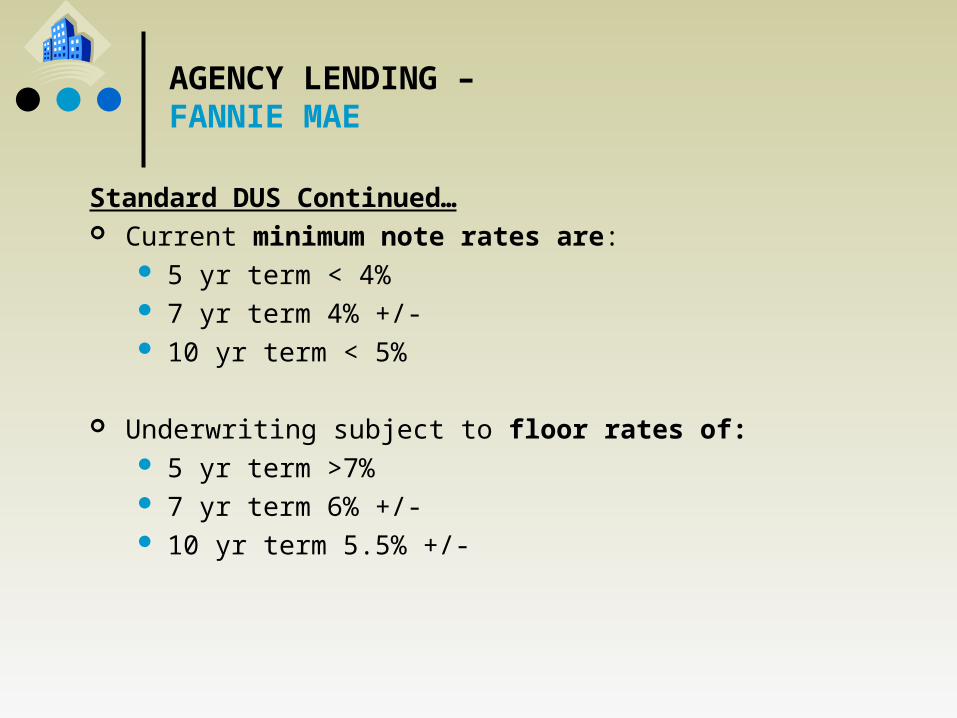

Standard DUS Continued… Current minimum note rates are:

5 yr term < 4% 7 yr term 4% +/- 10 yr term < 5%

Underwriting subject to floor rates of: 5 yr term >7% 7 yr term 6% +/- 10 yr term 5.5% +/-

AGENCY LENDING – FANNIE MAE

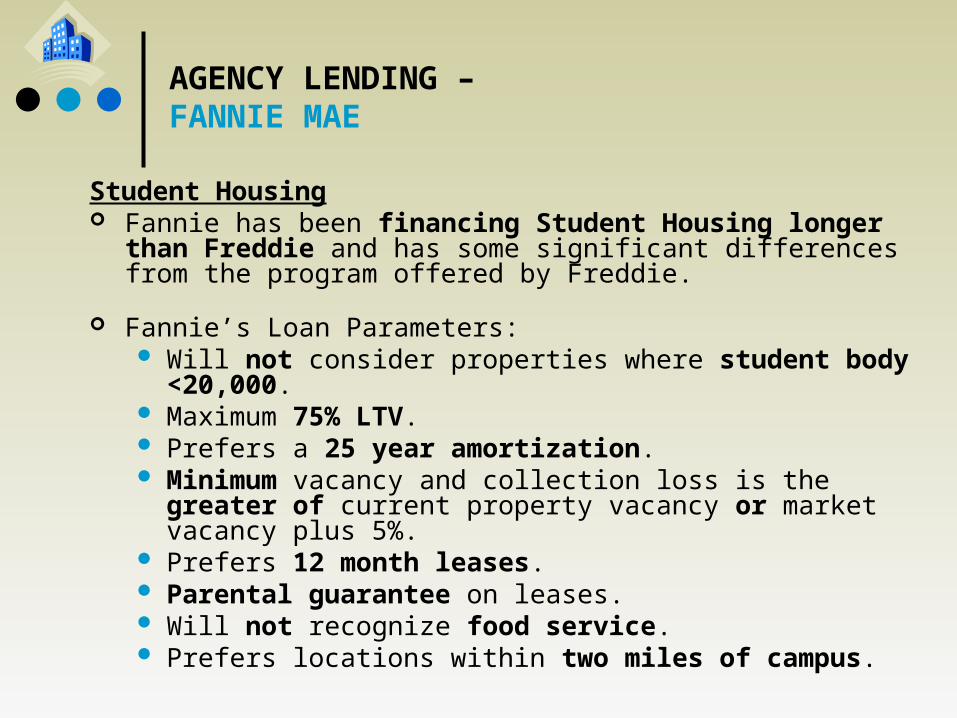

Student Housing Fannie has been financing Student Housing longer than

Freddie and has some significant differences from the program offered by Freddie.

Fannie’s Loan Parameters: Will not consider properties where student body

<20,000. Maximum 75% LTV. Prefers a 25 year amortization. Minimum vacancy and collection loss is the greater of

current property vacancy or market vacancy plus 5%. Prefers 12 month leases. Parental guarantee on leases. Will not recognize food service. Prefers locations within two miles of campus.

AGENCY LENDING – FANNIE MAE

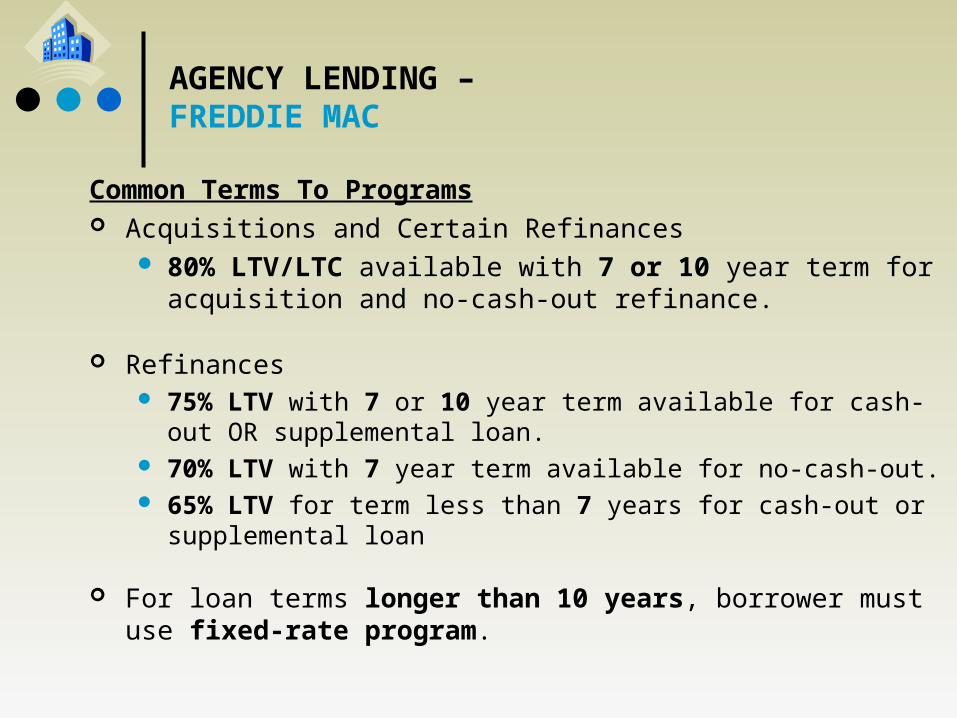

Common Terms To Programs Acquisitions and Certain Refinances

80% LTV/LTC available with 7 or 10 year term for acquisition and no-cash-out refinance.

Refinances 75% LTV with 7 or 10 year term available for cash-out OR

supplemental loan. 70% LTV with 7 year term available for no-cash-out. 65% LTV for term less than 7 years for cash-out or

supplemental loan

For loan terms longer than 10 years, borrower must use fixed-rate program.

AGENCY LENDING – FREDDIE MAC

Common Terms To Programs continued… Capital Markets Execution [CME] is the program structured

for later securitization.

CME program requires escrows for Taxes, Insurance and Replacement Reserve. Other programs may waive these escrows depending upon lower LTV and higher DSC.

Same loan amount on all programs.

Lender fee of 10 bps charged on all programs.

AGENCY LENDING – FREDDIE MAC

Fixed Rate Program May be amortizing, full term I/O, partial I/O and fixed-to-float.

Fixed-to-float provides extension of 1 year after term with floating rate for par prepayment.

Extended ERL for up to 12 months.

Standard terms 5, 7, 10, 15, 20, 25 and 30 years.

Supplemental Loan available after 1 year and with 3 years remaining.

Minimum DSC 1.25-1.30X.

AGENCY LENDING – FREDDIE MAC

Capital Market Execution Modeled for Securitization. Despite CME structure, it has

Supplemental Loan and ERL.

Key benefit is lower interest rate by 30-40 bps.

Loan terms of 5 to 30 years. Partial I/O.

Prepayment most affected by securitization. Yield Maintenance until securitization, followed by 2 year lock-out with defeasance thereafter. If not securitized within the first year, Yield Maintenance for life of loan.

Replacement Reserve, Tax and Insurance Escrows required.

Current minimum note rates are: 5 yr term: 4% +/- 7 year term: > 4% 10 yr term: <5%

AGENCY LENDING – FREDDIE MAC

Adjustable Rate Mortgage Lower short term rate with flexible prepayment.

Indices 1 month or 3 month Freddie Mac Reference Bills or LIBOR.

Loan terms of 5, 7 or 10 years, although 7 and 10 year terms most popular.

Full term I/O or partial I/O in some cases depending upon LTV/LTC and DSC.

Freddie provides embedded interest rate cap. No cap < 60% LTV.

Minimum interest rate cap 6.5%

AGENCY LENDING – FREDDIE MAC

Adjustable Rate Mortgage continued… DSC 1.05X at interest rate cap amortizing.

Early Spread Lock for 60 or 120 days.

Conversion to new fixed-rate mortgage anytime after lock out. Waive prepayment.

Most flexible prepayment option locked 1 year then open thereafter for 1%, except waived if converted to new fixed-rate loan.

Loan sizing the lesser of LTV or stressed minimum DSC or corresponding fixed-rate maximum

AGENCY LENDING – FREDDIE MAC

Student Housing The first Student Housing financings for Freddie took place in

2008. There are notable differences with the Freddie vs. Fannie loan program.

80% LTV/LTC for acquisitions and no-cash-out refinances for terms of 7 to 10 years

30 year amortization Potential I/O depending upon LTV/LTC and DSC. Permit 9 month leases Student body > 8,000 for fixed-rate loan or > 10,000 for floating rate loan

Except for the noted differences, Freddie and Fannie are very similar.

AGENCY LENDING – FREDDIE MAC

Life Insurance Companies The majority of Life Insurance Companies continue to make

commercial mortgage loans. There are some significant differences in what Fannie/Freddie will do vs. Life Insurance Companies.

Key differences with Life Insurance Companies: Maximum 70%-75% LTV/LTC. Most prefer 5, 7 and 10 year terms; some will consider

a longer term but often require self-amortizing structure. Most prefer 25 year amortization. ERL at application for 75-90 day process. Most still use yield maintenance for prepayment.

LIFE INSURANCE COMPANIES - OVERVIEW OF LENDING PARAMETERS

Life Insurance Companies The differences continued…:

Some are interested in structuring loans for securitization.

None have a workable rehab program but some provide financing for proposed development.

Some do Senior Housing and Student Housing but not as aggressively.

Smaller Life Insurance Companies entertain small loan requests while larger Life Insurance Companies prefer larger loan sizes.

LIFE INSURANCE COMPANIES - OVERVIEW OF LENDING PARAMETERS

FHA/HUD FINANCINGPresented by: Al Moczul

Tavernier Capital Funding, LLC (“TCF”) is a nationwide HUD-Approved multifamily and senior housing lender that provides developers and borrowers with direct access to all of the FHA mortgage insurance programs.

Tavernier maintains a national FHA lending presence with offices throughout New York, Michigan, Florida and Georgia.

Our staff of FHA industry veterans has over 70 years of combined experience and have closed over $4 Billion FHA transactions nationwide.

More information on Tavernier and the FHA loan programs can be found at www.TAVCAP.com

TAVERNIER CAPITAL FUNDING, LLC - OVERVIEW

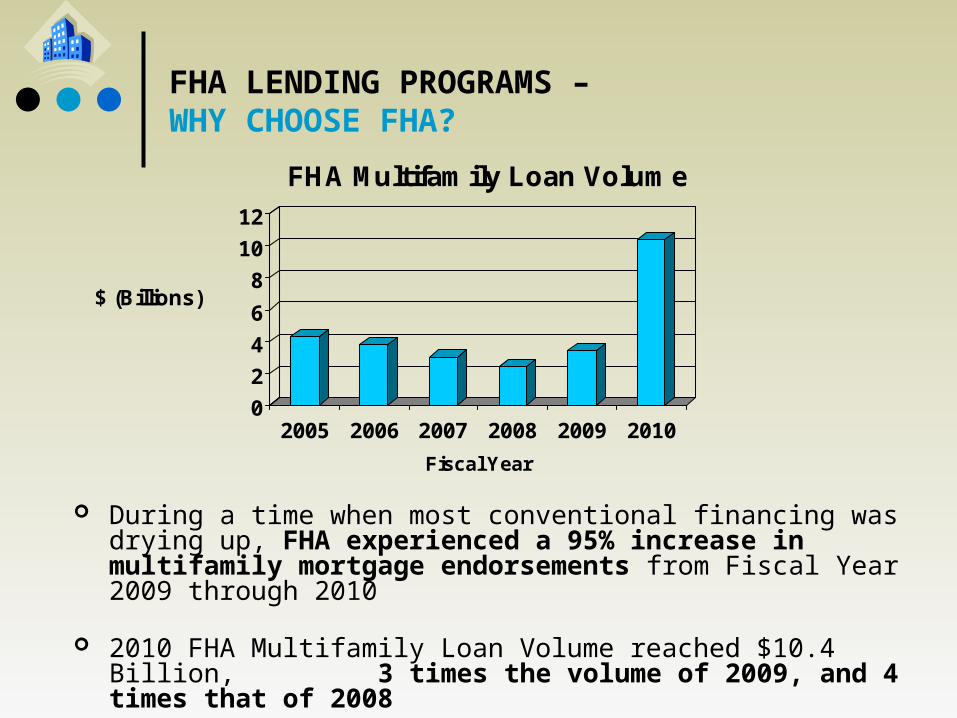

FHA LENDING PROGRAMS – WHY CHOOSE FHA?

During a time when most conventional financing was drying up, FHA experienced a 95% increase in multifamily mortgage endorsements from Fiscal Year 2009 through 2010

2010 FHA Multifamily Loan Volume reached $10.4 Billion, 3 times the volume of 2009, and 4 times that of 2008

0

2

4

6

8

10

12

$ (Billions)

2005 2006 2007 2008 2009 2010

Fiscal Year

FHA Multifamily Loan Volume

FHA closed a record $13.85 Billion in multifamily and healthcare loans during fiscal year 2010

Loan volume was so great, Congress had to grant an additional $5 Billion in commitment authority in August to keep the production pipeline open through fiscal year end

FHA processed the largest refinance ($125 M) and new construction ($187 M) transactions in its history this year, both of which were market-rate properties

FHA closed 68 tax credit transactions totaling over $446 Million, tripling the output of fiscal year 2009

Going forward, HUD predicts at least $10 Billion (or approx. 20% of the current FHA insured portfolio) will be added to the insurance fund each year

FHA LENDING PROGRAMS - SNAPSHOT OF 2010

Multifamily Programs: New Construction / Substantial Rehabilitation Acquisition / Refinance Refinance of an Existing FHA Loan

Healthcare Programs: New Construction / Substantial Rehabilitation Acquisition / Refinance Refinance of an Existing FHA Loan

FHA LENDING PROGRAMS– MOST COMMON OPTIONS

221(d)4: New Construction/Rehab Loan term up to 40 Years Amortization up to 40 Years Low, fixed interest rates (currently low 5% range) Max LTV: 83.3% market rate

87.0% affordable DSCR: 1.20x market rate

1.15x affordable Two-Stage Processing Non-Recourse Fully Assumable Negotiable prepayment options Funded by GNMA mortgage-backed securities

FHA MULTIFAMILY PROGRAMS -KEY FEATURES

223(f): Acquisition/Refinance Loan term up to 35 Years Amortization up to 35 Years Low, fixed interest rates (currently low 4% range) Max LTV: 83.3% market rate

85% affordable80% if cashing-out

DSCR: 1.20x market-rate1.176x affordable

One-Stage Processing Non-Recourse Fully Assumable Negotiable prepayment options Funded by GNMA mortgage-backed securities

FHA MULTIFAMILY PROGRAMS –KEY FEATURES

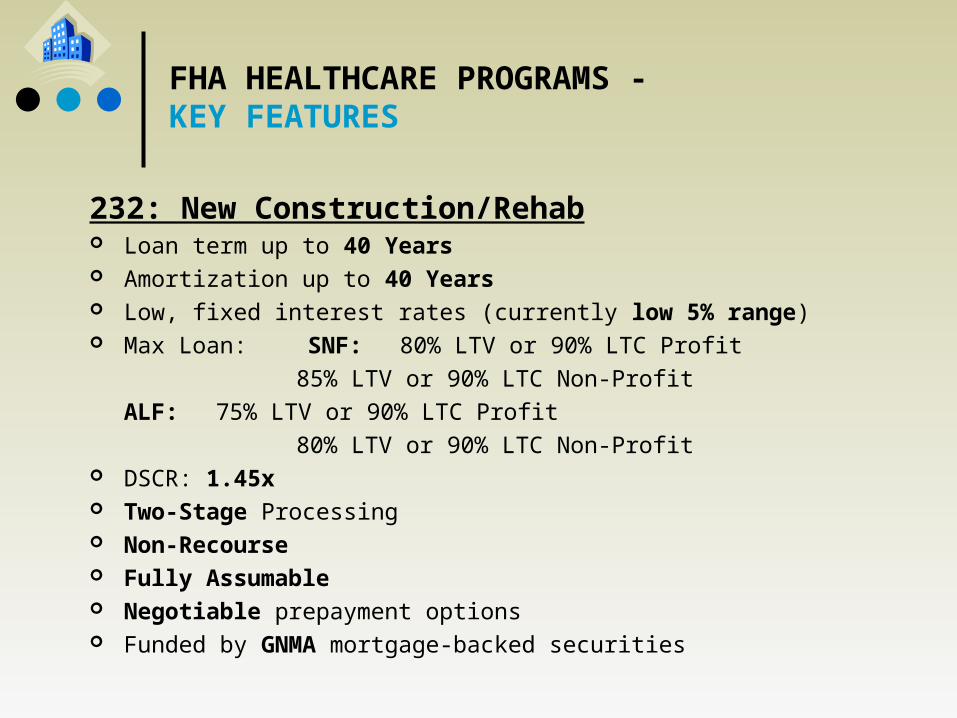

232: New Construction/Rehab Loan term up to 40 Years Amortization up to 40 Years Low, fixed interest rates (currently low 5% range) Max Loan: SNF: 80% LTV or 90% LTC Profit

85% LTV or 90% LTC Non-ProfitALF: 75% LTV or 90% LTC Profit

80% LTV or 90% LTC Non-Profit DSCR: 1.45x Two-Stage Processing Non-Recourse Fully Assumable Negotiable prepayment options Funded by GNMA mortgage-backed securities

FHA HEALTHCARE PROGRAMS -KEY FEATURES

232/223(f): Acquisition/Refinance Loan term up to 35 Years Amortization up to 35 Years Low, fixed interest rates (currently low 4% range) Max Loan: 80% LTV Profit

85% LTV Non-Profit DSCR: 1.45x One-Stage Processing Non-Recourse Fully Assumable Negotiable prepayment options Funded by GNMA mortgage-backed securities

FHA HEALTHCARE PROGRAMS –KEY FEATURES

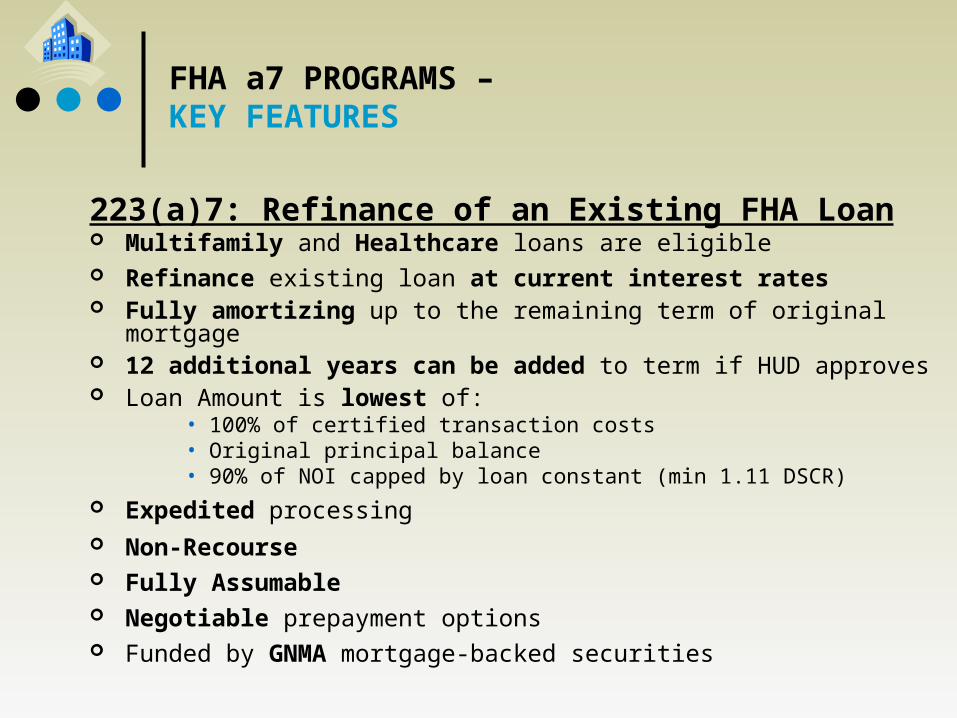

223(a)7: Refinance of an Existing FHA Loan Multifamily and Healthcare loans are eligible Refinance existing loan at current interest rates Fully amortizing up to the remaining term of original mortgage 12 additional years can be added to term if HUD approves Loan Amount is lowest of:

• 100% of certified transaction costs• Original principal balance• 90% of NOI capped by loan constant (min 1.11 DSCR)

Expedited processing Non-Recourse Fully Assumable Negotiable prepayment options Funded by GNMA mortgage-backed securities

FHA a7 PROGRAMS –KEY FEATURES

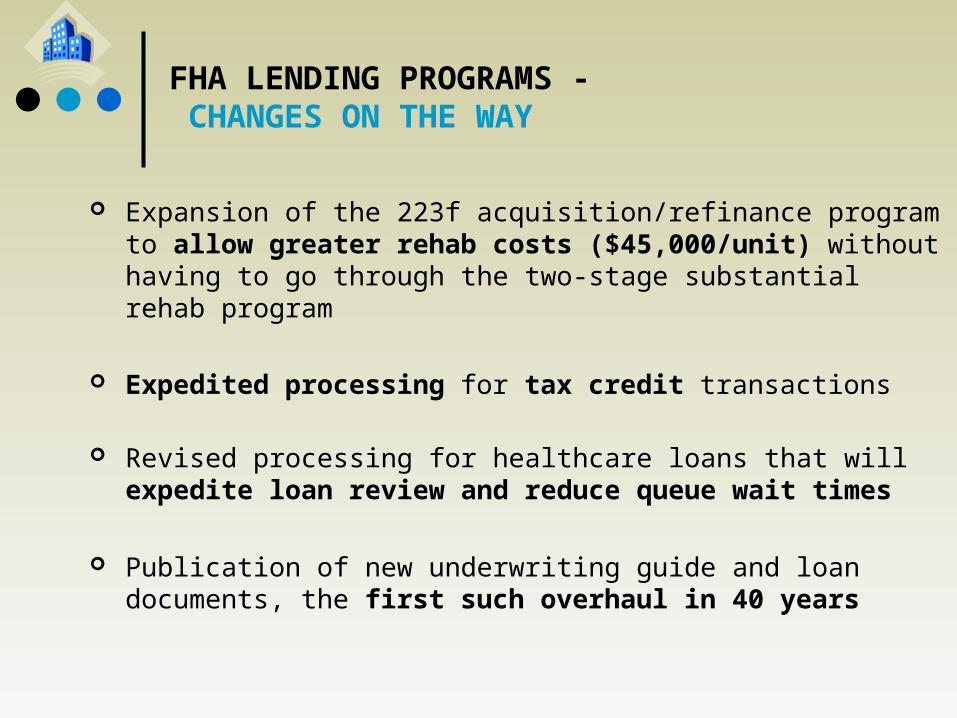

Expansion of the 223f acquisition/refinance program to allow greater rehab costs ($45,000/unit) without having to go through the two-stage substantial rehab program

Expedited processing for tax credit transactions

Revised processing for healthcare loans that will expedite loan review and reduce queue wait times

Publication of new underwriting guide and loan documents, the first such overhaul in 40 years

FHA LENDING PROGRAMS - CHANGES ON THE WAY

For more information on any of the loan programs discussed today, visit our website:

WWW.TAVERNIERCAPITAL.COM