Embed Size (px)

Citation preview

1

XBRL Taxonomies

By:

IRIS Business Services Ltd.

2

Objective

To get introduced to the term ‘Taxonomy’

To understand the Indian GAAP taxonomy

To know the process of creating XBRL documents

3

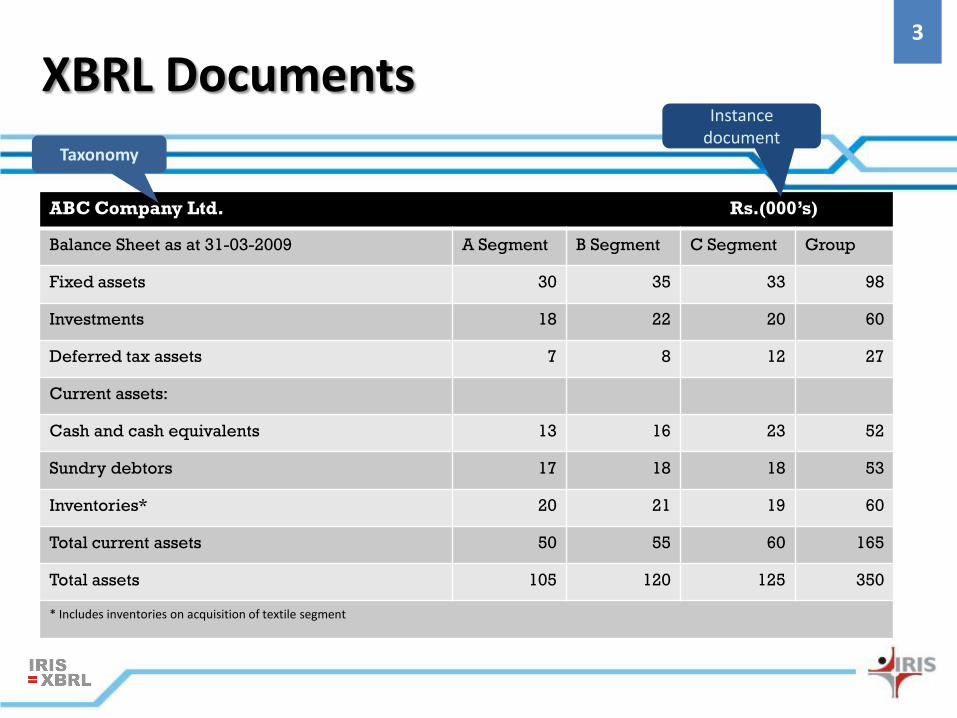

ABC Company Ltd. Rs.(000’s)

Balance Sheet as at 31-03-2009 A Segment B Segment C Segment Group

Fixed assets 30 35 33 98

Investments 18 22 20 60

Deferred tax assets 7 8 12 27

Current assets:

Cash and cash equivalents 13 16 23 52

Sundry debtors 17 18 18 53

Inventories* 20 21 19 60

Total current assets 50 55 60 165

Total assets 105 120 125 350

* Includes inventories on acquisition of textile segment

Taxonomy

Instancedocument

XBRL Documents

4

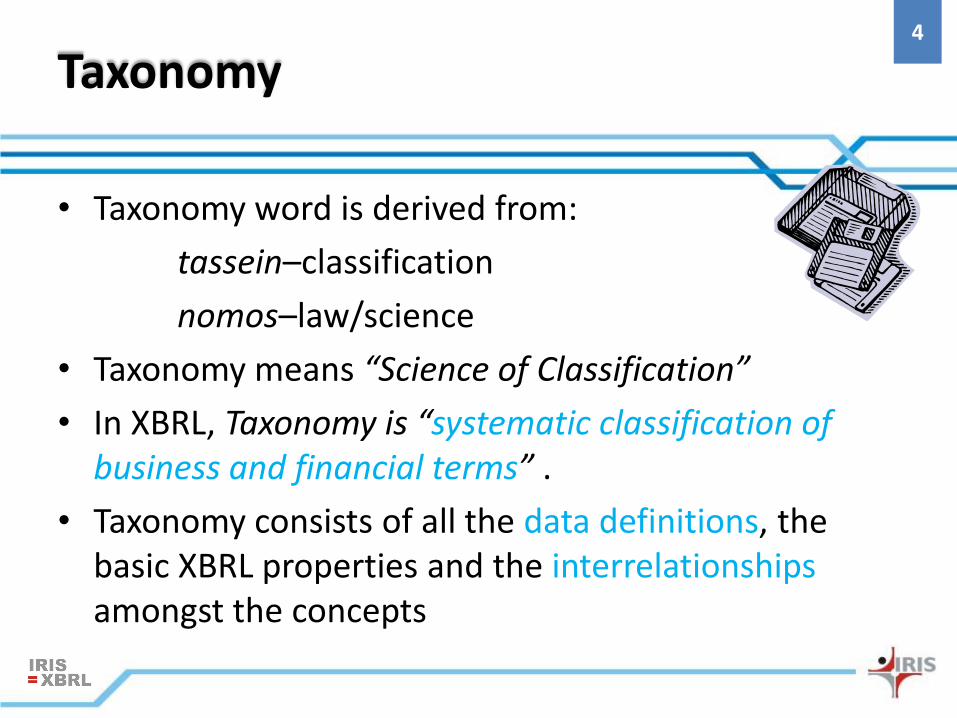

Taxonomy

• Taxonomy word is derived from:

tassein–classification

nomos–law/science

• Taxonomy means “Science of Classification”

• In XBRL, Taxonomy is “systematic classification of business and financial terms” .

• Taxonomy consists of all the data definitions, the basic XBRL properties and the interrelationships amongst the concepts

5

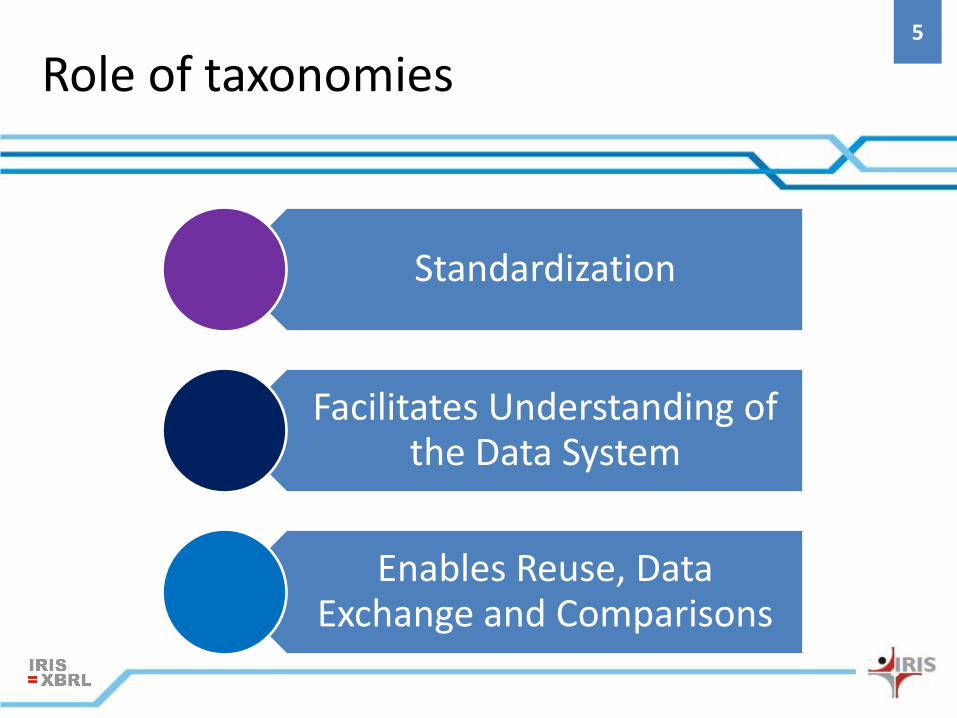

Role of taxonomies

Standardization

Facilitates Understanding of the Data System

Enables Reuse, Data Exchange and Comparisons

6

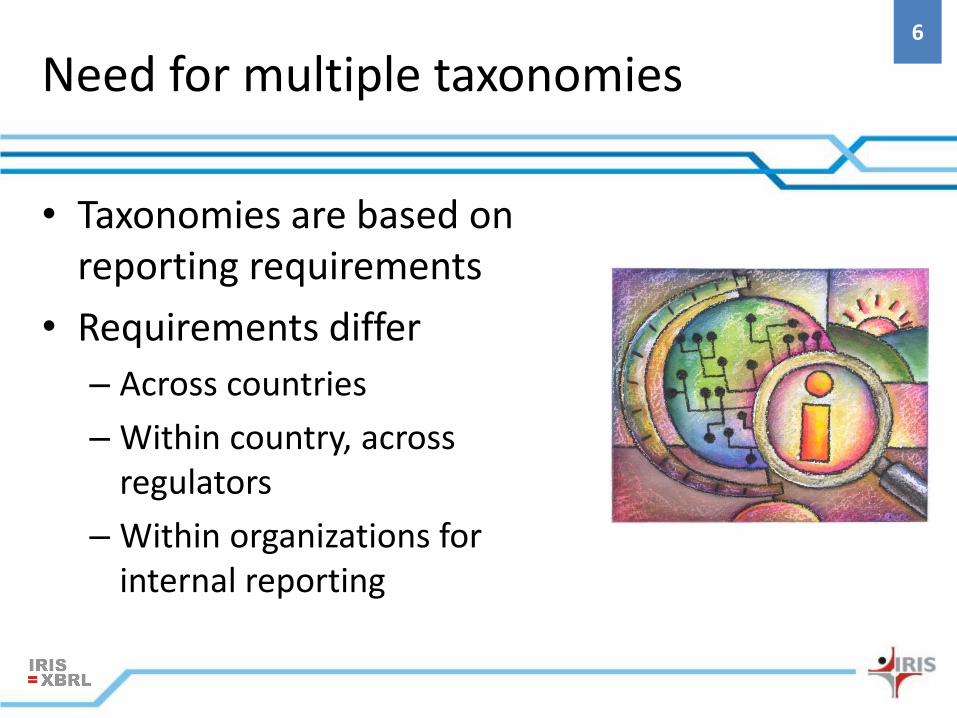

Need for multiple taxonomies

• Taxonomies are based on reporting requirements

• Requirements differ

– Across countries

– Within country, across regulators

– Within organizations for internal reporting

7

Steps in Taxonomy Building

• Analysis and Element identification

• Data modeling and taxonomy designing

• Validating and Testing taxonomy

8

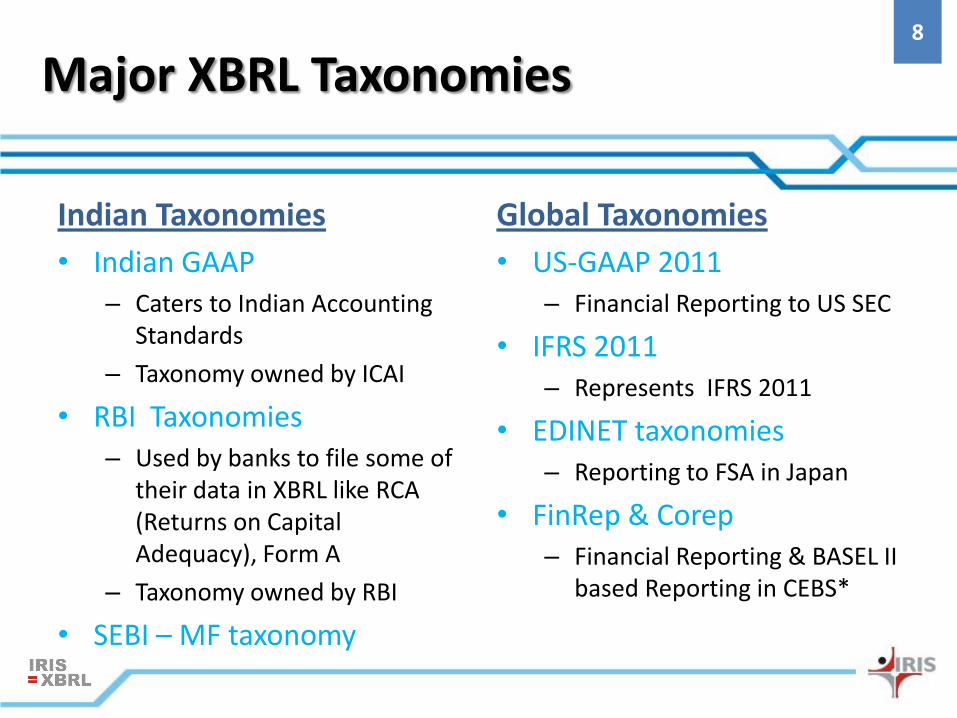

Major XBRL Taxonomies

Indian Taxonomies

• Indian GAAP– Caters to Indian Accounting

Standards

– Taxonomy owned by ICAI

• RBI Taxonomies – Used by banks to file some of

their data in XBRL like RCA (Returns on Capital Adequacy), Form A

– Taxonomy owned by RBI

• SEBI – MF taxonomy

Global Taxonomies

• US-GAAP 2011– Financial Reporting to US SEC

• IFRS 2011– Represents IFRS 2011

• EDINET taxonomies – Reporting to FSA in Japan

• FinRep & Corep– Financial Reporting & BASEL II

based Reporting in CEBS*

9

UNDERSTANDING TAXONOMY

10

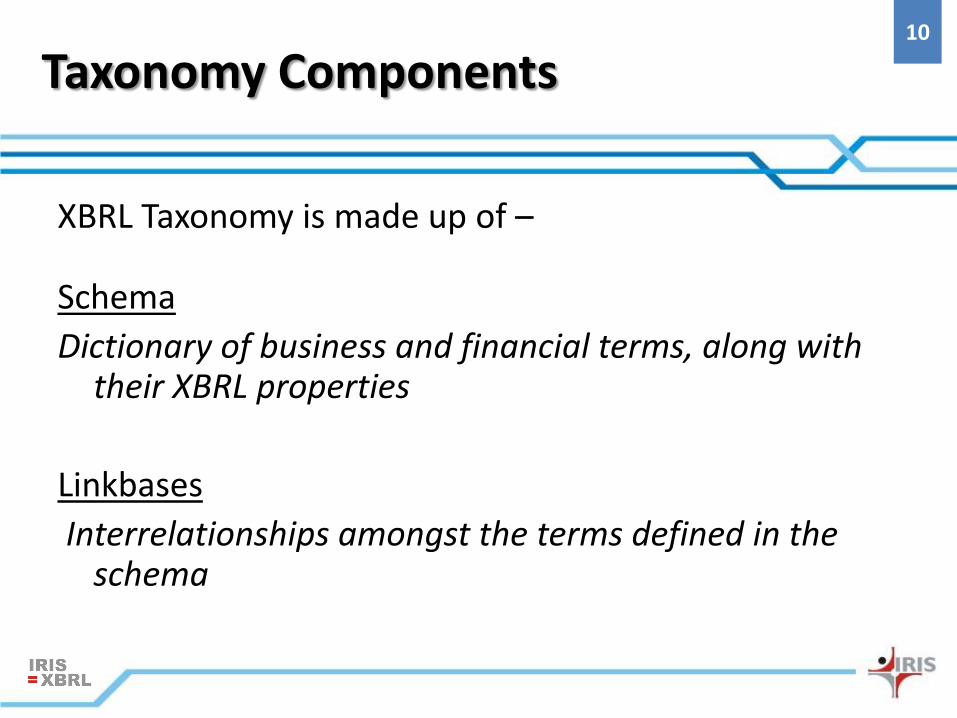

XBRL Taxonomy is made up of –

Schema

Dictionary of business and financial terms, along with their XBRL properties

Linkbases

Interrelationships amongst the terms defined in the schema

Taxonomy Components

11

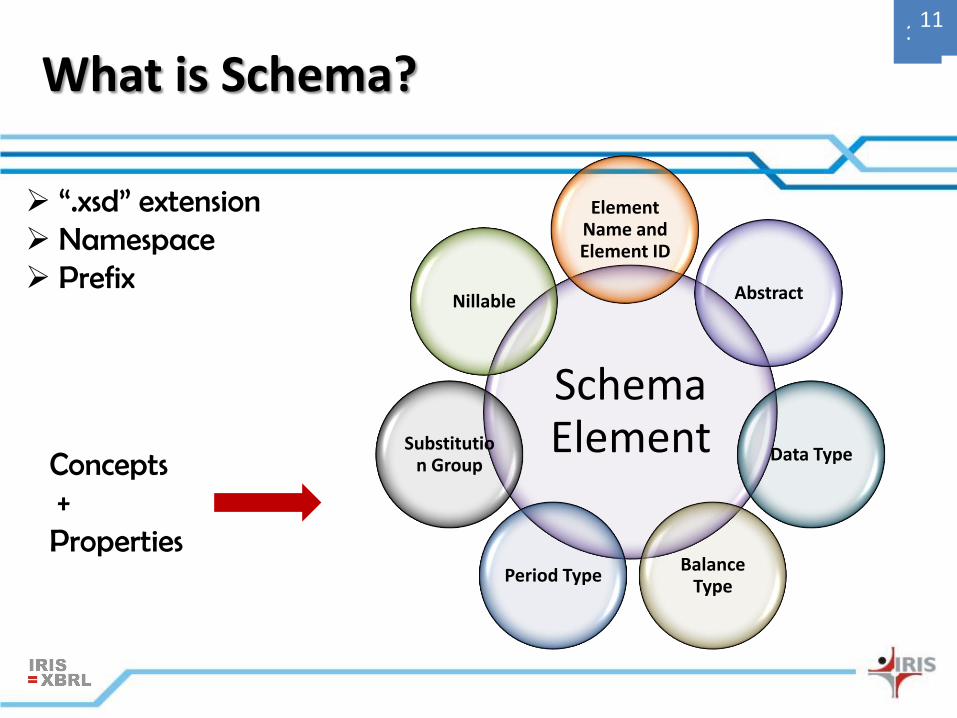

What is Schema?11

Schema Element

Element Name and Element ID

Abstract

Data Type

Balance Type

Period Type

Substitution Group

Nillable

“.xsd” extension Namespace Prefix

Concepts+Properties

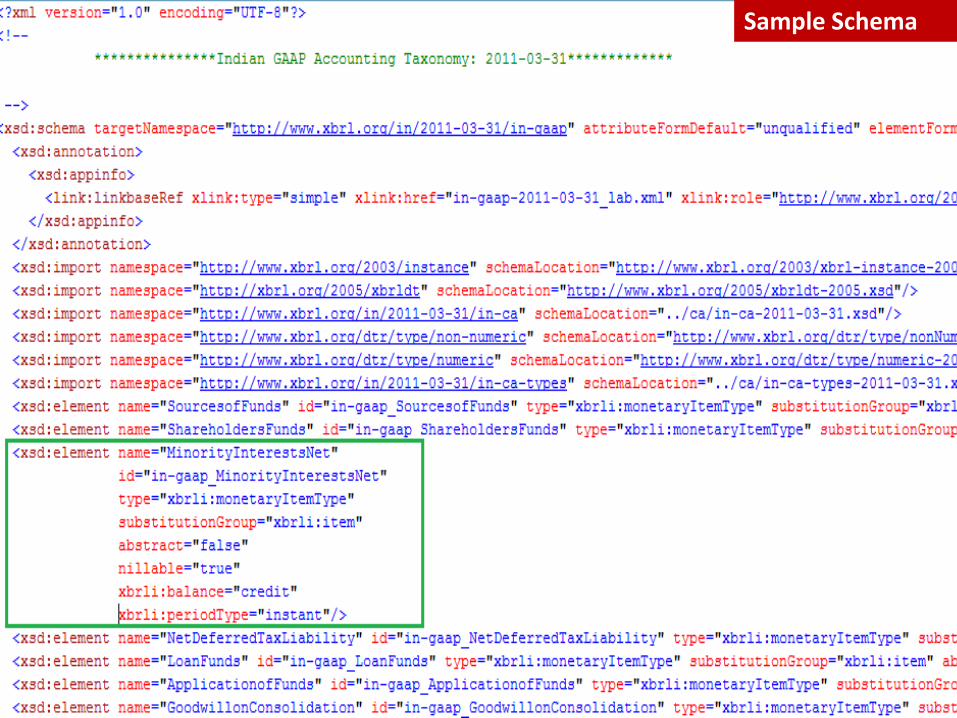

12Sample Schema

13

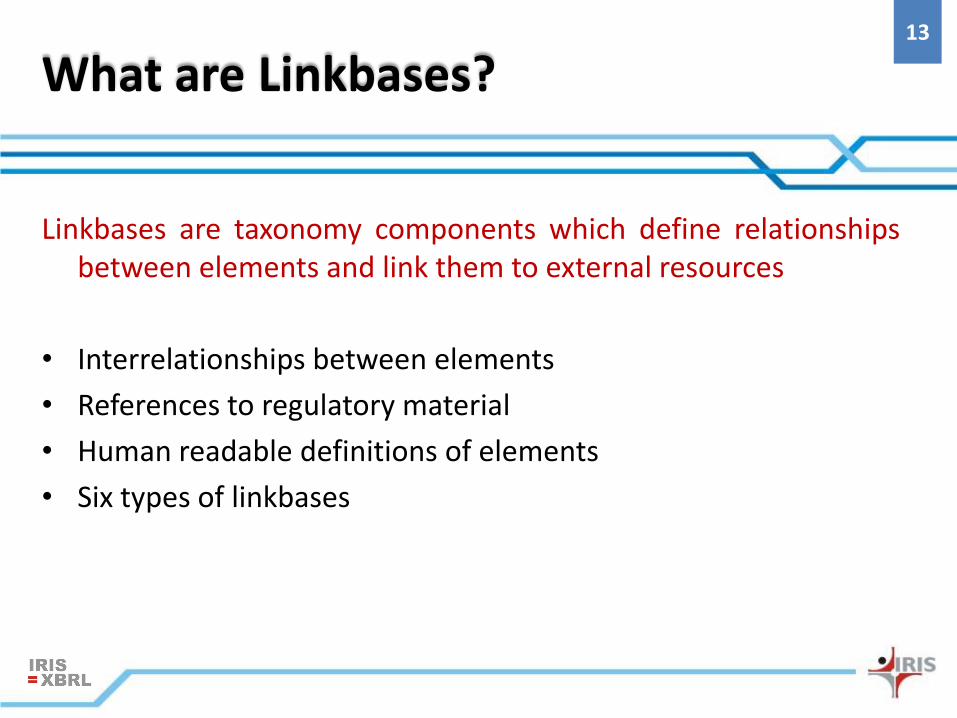

What are Linkbases?

Linkbases are taxonomy components which define relationshipsbetween elements and link them to external resources

• Interrelationships between elements

• References to regulatory material

• Human readable definitions of elements

• Six types of linkbases

14

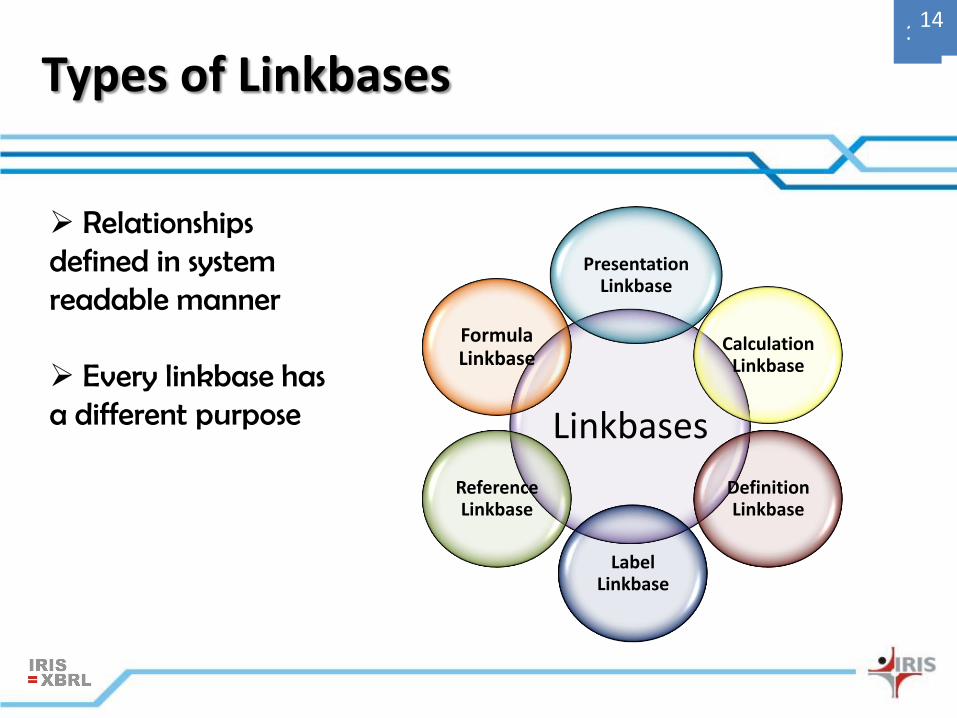

Types of Linkbases14

Linkbases

Presentation Linkbase

Calculation Linkbase

Definition Linkbase

Label Linkbase

Reference Linkbase

Formula Linkbase

Relationships defined in system readable manner

Every linkbase has a different purpose

15

Element Order

AssetsAbstract

FixedAssets 1

CurrentAssetsAbstract 2

Cash 1

AccountsReceivable 2

Inventories 3

CurrentAssets 4

Assets 3

Element Weight

Assets

FixedAssets 1

CurrentAssets 1

Cash 1

AccountsReceivable 1

Inventories 1

Presentation Link Calculation Link

Presentation v/s Calculation Linkbase

16

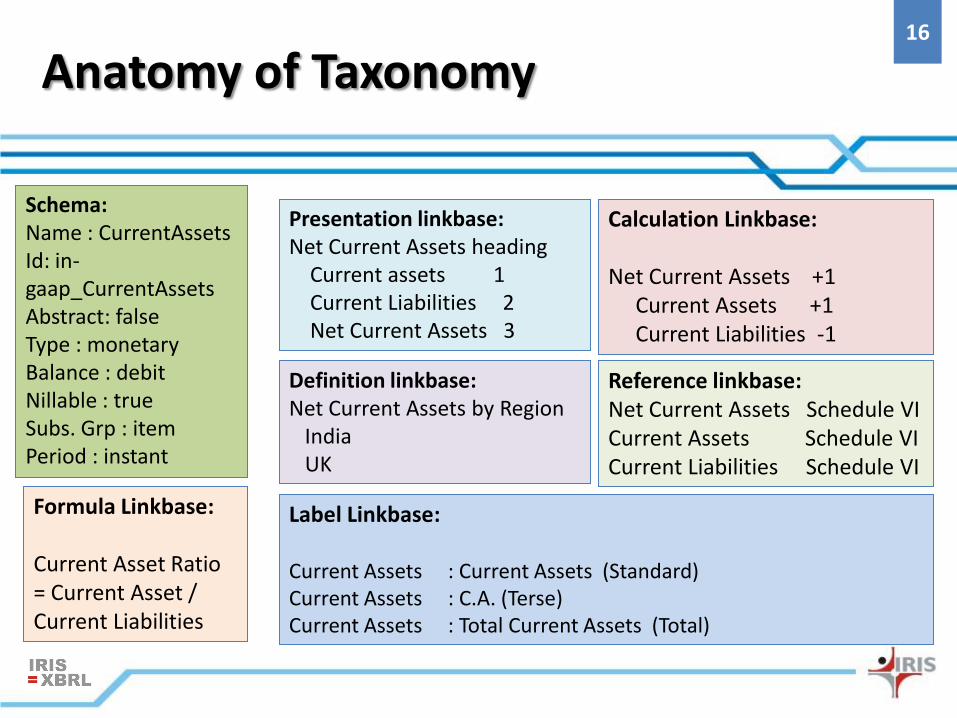

Anatomy of Taxonomy

Calculation Linkbase:

Net Current Assets +1Current Assets +1Current Liabilities -1

Presentation linkbase:Net Current Assets heading

Current assets 1 Current Liabilities 2Net Current Assets 3

Definition linkbase:Net Current Assets by Region

IndiaUK

Label Linkbase:

Current Assets : Current Assets (Standard)Current Assets : C.A. (Terse)Current Assets : Total Current Assets (Total)

Formula Linkbase:

Current Asset Ratio = Current Asset / Current Liabilities

Reference linkbase:Net Current Assets Schedule VI Current Assets Schedule VICurrent Liabilities Schedule VI

Schema:Name : CurrentAssetsId: in-gaap_CurrentAssetsAbstract: falseType : monetaryBalance : debitNillable : trueSubs. Grp : itemPeriod : instant

17

MCA Taxonomy

Taxonomy available athttp://www.mca.gov.in/XBRL/ More than 3000 concepts included in

taxonomy Based on

Schedule VI, Companies Act Accounting Standards MCA specific requirements Other regulatory requirements

Use of tuples Current version designed for Commercial

and industrial entities

18

MCA Taxonomy structure

MCA Specific(ca)

• Elements•Data types

Schedule VI and Accounting Standards

(In-gaap)

• Elements

Commercial and Industrial

(CI)

• Relationships•Entry -point

Additional folders as and when other industry taxonomies are developed

NBFC/ Power

19

Few points..

• More than 3000 concepts defined

• Use of tuples for data modelling

• Custom data types – E.g. SRN, CIN, DIN etc.

• Enumerations for certain elements included– E.g. Type of related parties, content of report etc.

Fixed taxonomy would be followed

20

CREATING INSTANCE DOCUMENT

20

21

Instance document

• Business report in electronic format

• Refers to a taxonomy

• Contains – Facts (numeric and non-numeric)

– Context

– Units

• Stores values in actual

• Validating against taxonomy

22

SOUTH AMERICAArgentina – Bank of ArgentinaBrazil – Bank of BrazilChile – Bank of Chile, SECColumbia – Bank of ColumbiaPeru – Bank of Peru

MIDDLE EAST/AFRICAUAE- SCA,ADX and DFMIsrael - Securities AuthoritySouth Africa – Stock Exchange

Sample Instance

22

23

Creating XBRL instance document

a) Use XBRL software

• Buy the software

• Get people trained

b) Integrate in accounting systems

• Implement completely inside the systems

• Use bridge software which can read the accounting system output

c) Outsourced conversion process

24XBRL Document Creation

25

Process of tagging

• One time / recurring• Assigning XBRL tag to data reported

– Selecting the most appropriate element from the taxonomy

– Extending the taxonomy, if required (and if permissible)

• Defining other information– Reporting period– Unit of measurement– Level of rounding used – Footnotes

26

FEW CASE STUDIES

27

Need to know XBRL..

Ministry of Corporate Affairs has issued a mandate for companies which meet the following criteria have to file their data in XBRL All companies listed in India and their Indian subsidiaries,

having a paid up capital of Rs. 5 Crore and above

or a Turnover of Rs 100 crore or above

Is this the only reason? COMPLIANCE..

XBRL is much more than COMPLIANCE

28

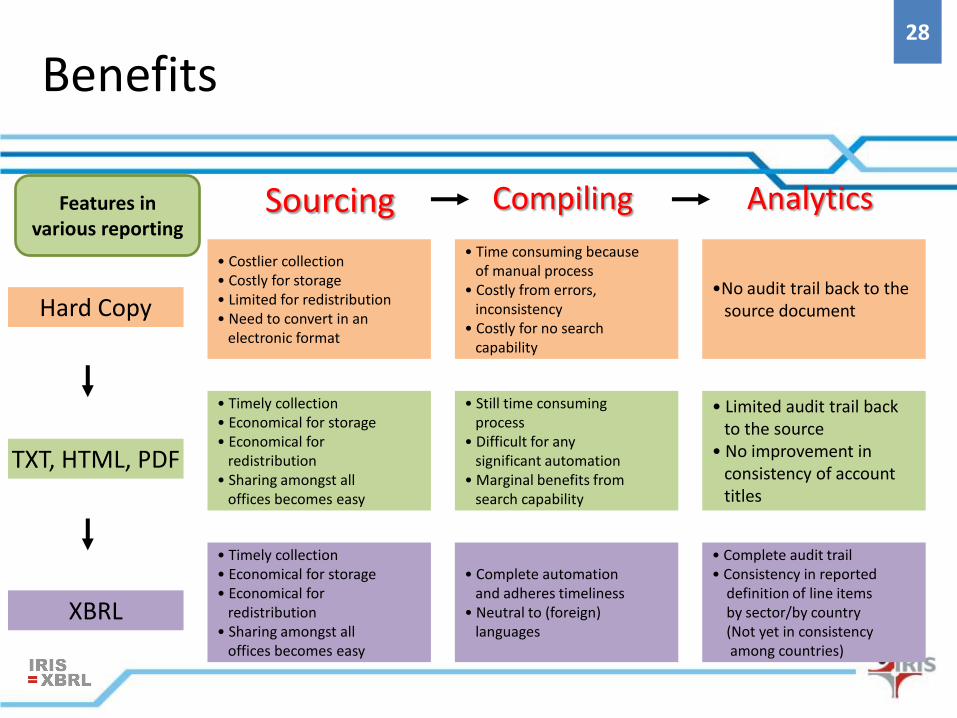

Sourcing Compiling Analytics

Hard Copy

TXT, HTML, PDF

XBRL

• Costlier collection• Costly for storage• Limited for redistribution• Need to convert in an

electronic format

• Timely collection• Economical for storage• Economical for

redistribution• Sharing amongst all

offices becomes easy

• Timely collection• Economical for storage• Economical for

redistribution• Sharing amongst all

offices becomes easy

• Time consuming becauseof manual process

• Costly from errors,inconsistency

• Costly for no searchcapability

• Still time consumingprocess

• Difficult for anysignificant automation

• Marginal benefits fromsearch capability

• Complete automationand adheres timeliness

• Neutral to (foreign)languages

•No audit trail back to thesource document

• Limited audit trail backto the source

• No improvement inconsistency of accounttitles

• Complete audit trail• Consistency in reported

definition of line itemsby sector/by country(Not yet in consistencyamong countries)

Features in various reporting

Benefits

29

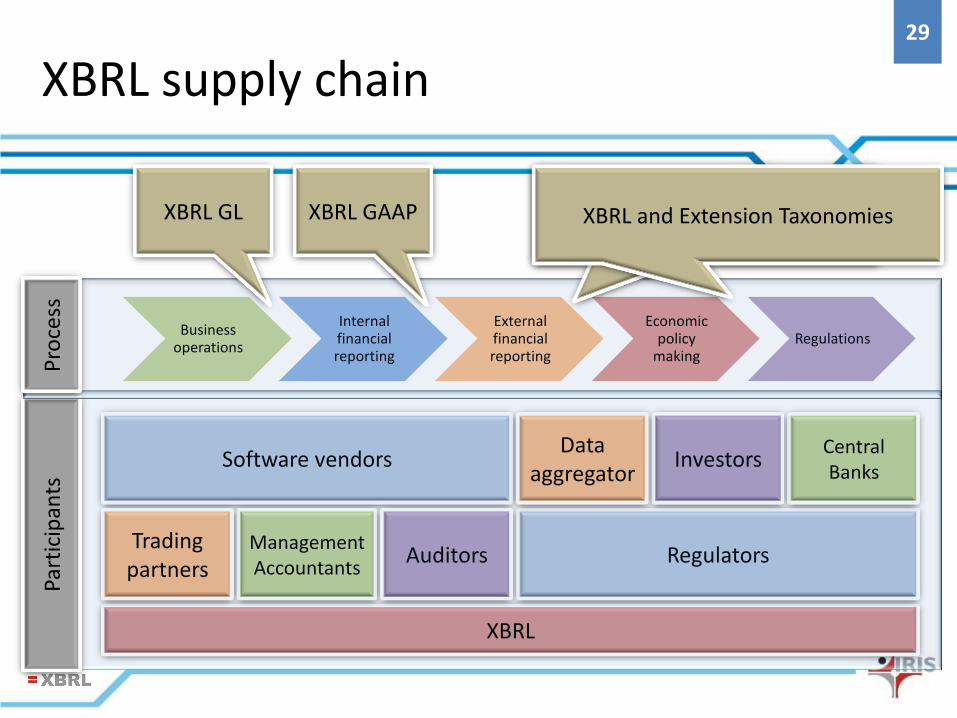

XBRL

Business operations

Internal financial reporting

External financial reporting

Economic policy

makingRegulations

Software vendors

RegulatorsManagement Accountants

Trading partners

Auditors

Central Banks

InvestorsData

aggregator

Part

icip

ants

Pro

cess

XBRL GAAPXBRL GL XBRL and Extension Taxonomies

XBRL supply chain

30

XBRL FOR REGULATORS

31

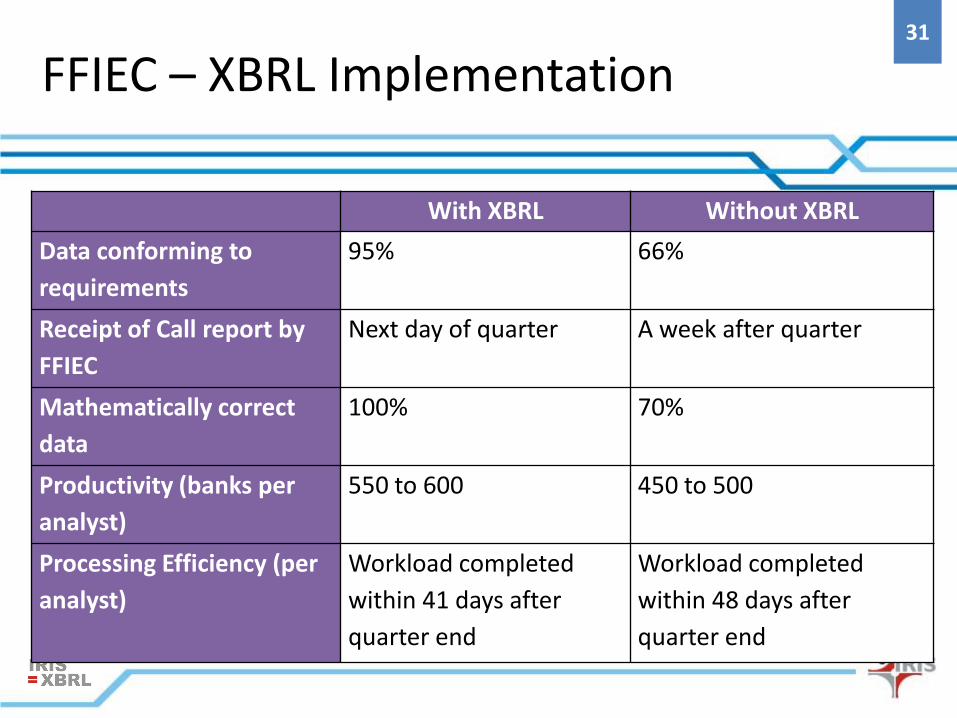

FFIEC – XBRL Implementation

With XBRL Without XBRL

Data conforming to

requirements

95% 66%

Receipt of Call report by

FFIEC

Next day of quarter A week after quarter

Mathematically correct

data

100% 70%

Productivity (banks per

analyst)

550 to 600 450 to 500

Processing Efficiency (per

analyst)

Workload completed

within 41 days after

quarter end

Workload completed

within 48 days after

quarter end

32Standard Business Reporting (SBR)

• Government wide initiative

• Move towards single unified data structures across agencies

• Implemented in

– Australia

– Netherlands

– New Zealand

33

Potential benefits for MCA

• Cleaner and accurate data– Pre-validated before submitting

– Cross verified with data submitted at other points of time

– Cross verified with data submitted by other concerned parties

• Availability of more data

• Scope for building compliance dash boards using the XBRL data

34

XBRL WITHIN INTERNAL SYSTEMS

35

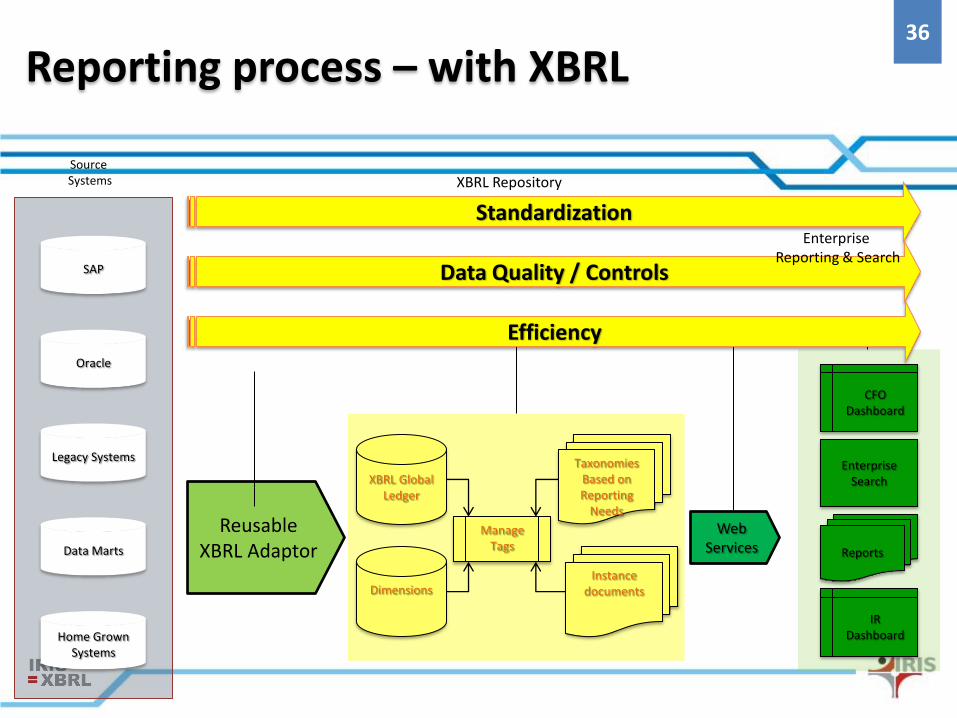

SAP

Oracle

Legacy Systems

Data Marts

Home Grown Systems

Source Systems

Interface

Interface

Spreadsheets

Paper Reports

Reporting

Performance

Analysis

Audit

Budget

Data Warehouse BI

Tools

Re-key data“Cut & Paste”“Drag & Drop”

Reporting process – without XBRL

36

SAP

Oracle

Legacy Systems

Data Marts

Home Grown Systems

Source Systems

Reusable XBRL Adaptor

XBRL Global Ledger

Dimensions

Manage Tags

Taxonomies Based on Reporting

Needs

Instance documents

Web Services

CFO Dashboard

IR Dashboard

Enterprise Search

Reports

Standardization

Data Quality / Controls

Efficiency

XBRL Repository

Enterprise Reporting & Search

Reporting process – with XBRL

37

Case Studies – Wacoal : Before XBRL

32 different

legacy systems

44 disparate accounting

systems

WACOAL Group

Purchasing

Sales

Materials

Inventory

Workflow

ACCOUNTING SUB-SYSTEMSBUSINESS APPLICATION SYSTEMS

38

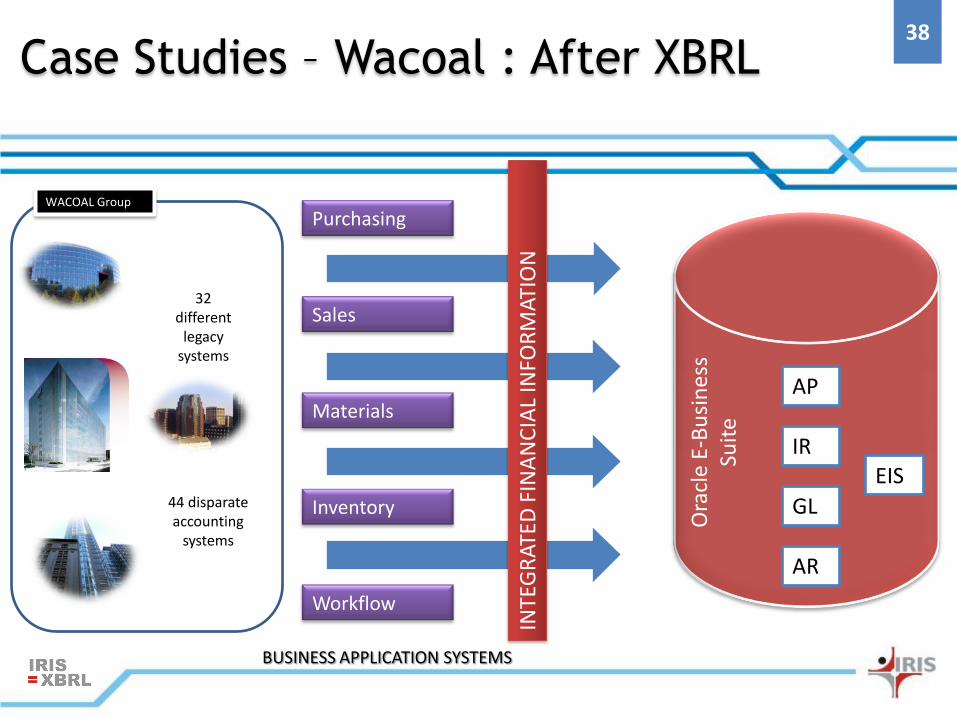

Case Studies – Wacoal : After XBRL

32 different

legacy systems

44 disparate accounting

systems

WACOAL Group

Purchasing

Sales

Materials

Inventory

Workflow

BUSINESS APPLICATION SYSTEMS

INTE

GR

ATED

FIN

AN

CIA

L IN

FOR

MAT

ION

Ora

cle

E-B

usi

nes

s Su

ite

AP

GL

AR

EISIR

39

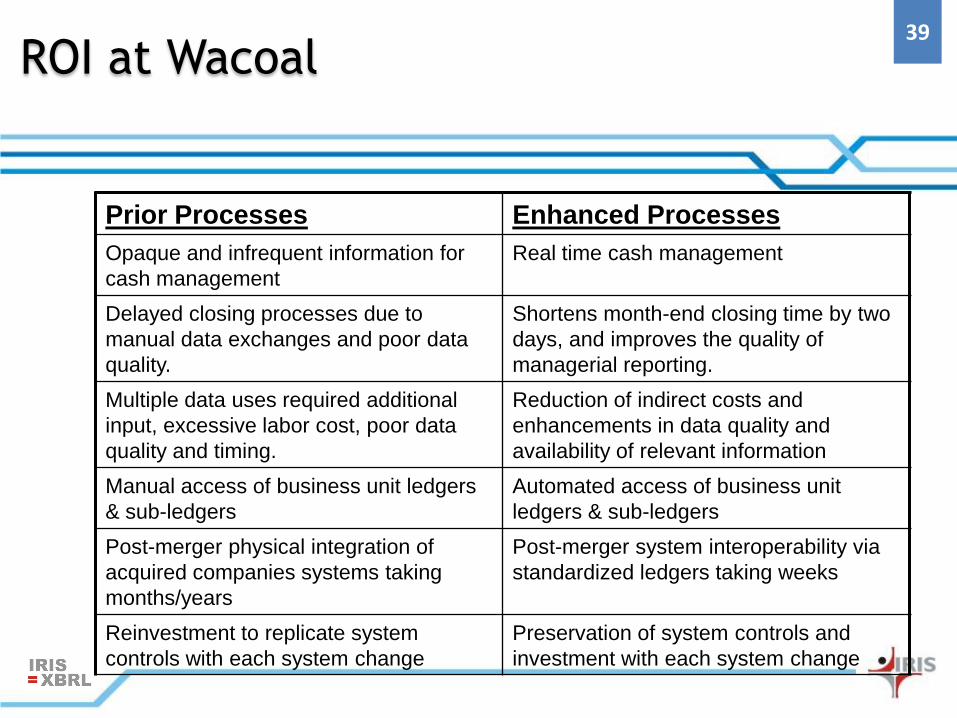

ROI at Wacoal

Prior Processes Enhanced Processes

Opaque and infrequent information for

cash management

Real time cash management

Delayed closing processes due to

manual data exchanges and poor data

quality.

Shortens month-end closing time by two

days, and improves the quality of

managerial reporting.

Multiple data uses required additional

input, excessive labor cost, poor data

quality and timing.

Reduction of indirect costs and

enhancements in data quality and

availability of relevant information

Manual access of business unit ledgers

& sub-ledgers

Automated access of business unit

ledgers & sub-ledgers

Post-merger physical integration of

acquired companies systems taking

months/years

Post-merger system interoperability via

standardized ledgers taking weeks

Reinvestment to replicate system

controls with each system change

Preservation of system controls and

investment with each system change

40

XBRL For Internal Use…

Where?

• Systems integration

• Data access, assembly and overview

• Redefinition of spreadsheets as user interfaces not data storage/transformation facilities

• Better controls – ultimately enabling continuous auditing and monitoring

Why?

• Data quality

– Validation at the “source”

– Consistency in data validation rules and analysis/visualization of data

• Abstraction of business rules and controls that can be applied across a wide range of software applications

• Lower cost operating environment

40

41

XBRL in consolidation process

• Cost savings in preparation, report creation, analysis.

• High flexibility through the use of dashboard based business rules.

• Significant savings in man hours and lead time in compliance and consolidation

• Easy data handling due to standardization and automation, centralisation of delivery

• Faster availability of data into standard reports

• A pioneering status among enterprises in the use of XBRL

42

XBRL for GAAP transformation

• Countries are adopting or converging towards IFRS

• Need to transform the accounts from existing GAAP to new IFRS or IFRS based standards

• Also, MNC companies, for consolidation have to bring all companies to one GAAP

XBRL can help in automating this process to the extent the rules can be explicitly defined

43

ROLE OF PROFESSIONALS

44

Opportunities for Professionals

• Building taxonomies

– Regulatory taxonomies

– Company taxonomies

• Creating the XBRL documents

• Assurance of XBRL documents

• Implementing XBRL within organizations

• Training

45

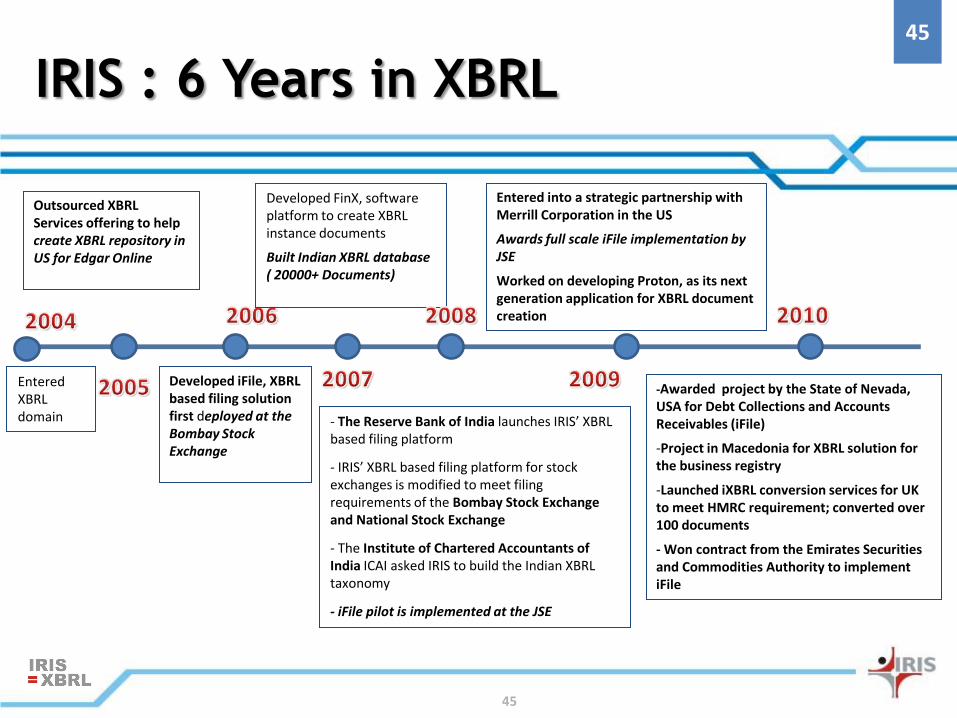

45

Entered XBRL domain - The Reserve Bank of India launches IRIS’ XBRL

based filing platform

- IRIS’ XBRL based filing platform for stock exchanges is modified to meet filing requirements of the Bombay Stock Exchange and National Stock Exchange

- The Institute of Chartered Accountants of India ICAI asked IRIS to build the Indian XBRL taxonomy

- iFile pilot is implemented at the JSE

Developed FinX, software platform to create XBRL instance documents

Built Indian XBRL database ( 20000+ Documents)

Outsourced XBRL Services offering to help create XBRL repository in US for Edgar Online

Developed iFile, XBRL based filing solution first deployed at the Bombay Stock Exchange

Entered into a strategic partnership with Merrill Corporation in the US

Awards full scale iFile implementation by JSE

Worked on developing Proton, as its next generation application for XBRL document creation

IRIS : 6 Years in XBRL

-Awarded project by the State of Nevada, USA for Debt Collections and Accounts Receivables (iFile)

-Project in Macedonia for XBRL solution for the business registry

-Launched iXBRL conversion services for UK to meet HMRC requirement; converted over 100 documents

- Won contract from the Emirates Securities and Commodities Authority to implement iFile

46

THANK YOU

Contact us:

IRIS Business Services LimitedT-131, Tower 1, 3rd Floor,International Infotech Park,Vashi, Navi Mumbai 400703,Maharashtra,India.

Website: www.irisbusiness.comPhone : 022 6723 1000Fax: 022 2781 44341800-209-9275 SHILPA DHOBALE