Embed Size (px)

Citation preview

1 (of 31)

FIN 200: Personal Finance

Topic 5-BudgetingLawrence Schrenk, Instructor

2 (of 31)

Learning Objectives

1. Explain the elements contained in a personal cash flow statement and balance sheet. ▪

2. Construct a personal cash flow statement and balance sheet. ▪

4 (of 31)

Cash Flow Categorization I

Inflow versus Outflow Pay Period versus Pro Rated Single versus Repeated Expected versus Unexpected Voluntary versus Involuntary Cyclical versus Non-Cyclical

5 (of 31)

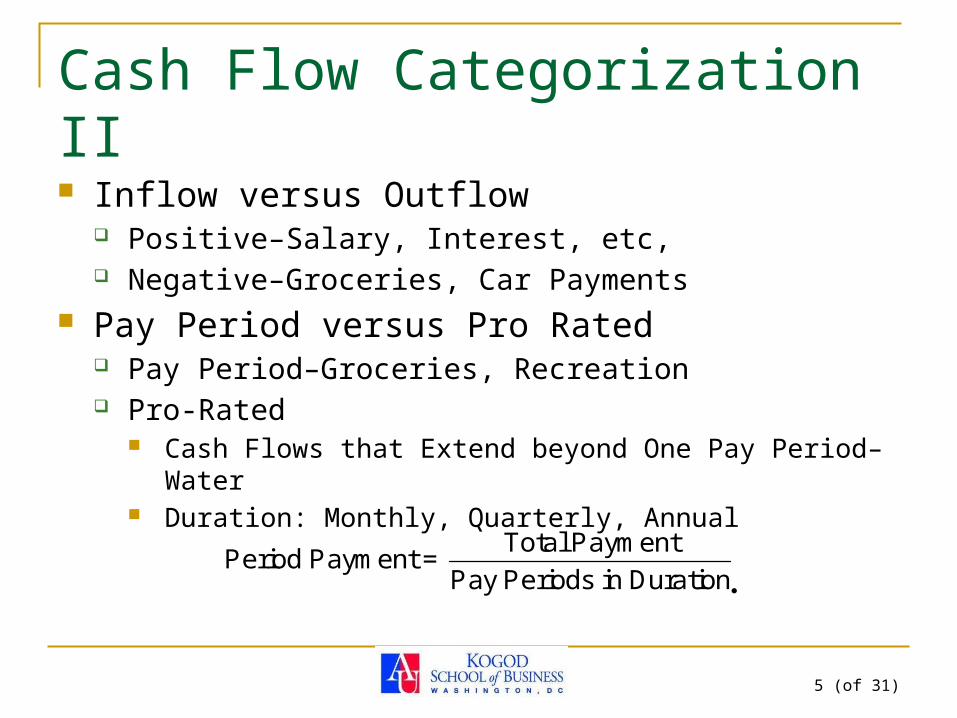

Cash Flow Categorization II

Inflow versus Outflow Positive–Salary, Interest, etc, Negative–Groceries, Car Payments

Pay Period versus Pro Rated Pay Period–Groceries, Recreation Pro-Rated

Cash Flows that Extend beyond One Pay Period–Water Duration: Monthly, Quarterly, Annual

Total PaymentPeriod Payment =

Pay Periods in Duration

6 (of 31)

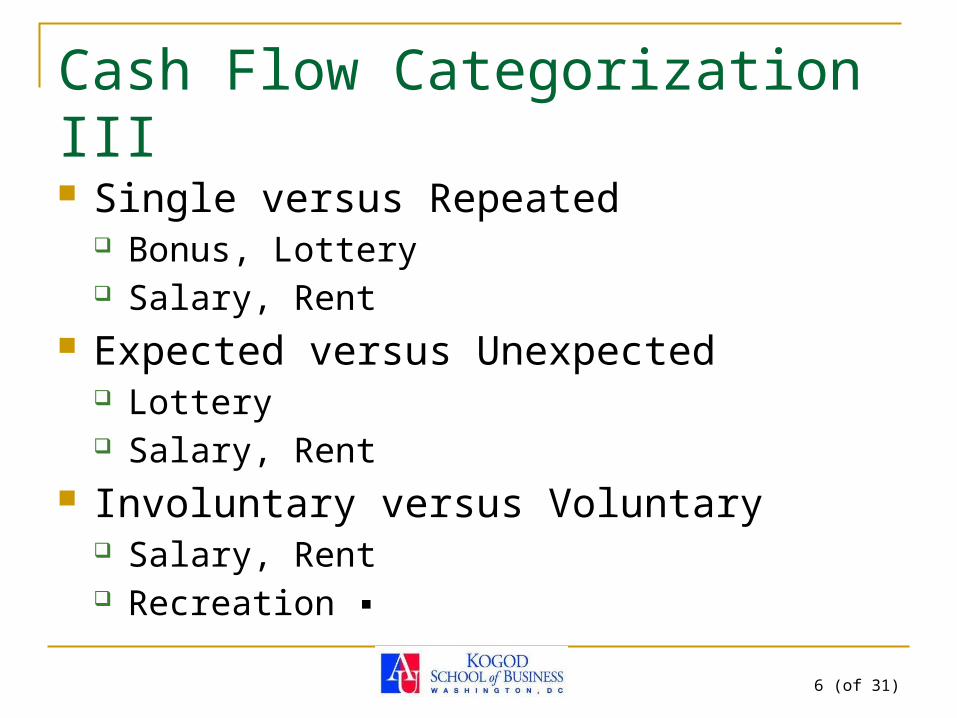

Cash Flow Categorization III

Single versus Repeated Bonus, Lottery Salary, Rent

Expected versus Unexpected Lottery Salary, Rent

Involuntary versus Voluntary Salary, Rent Recreation ▪

7 (of 31)

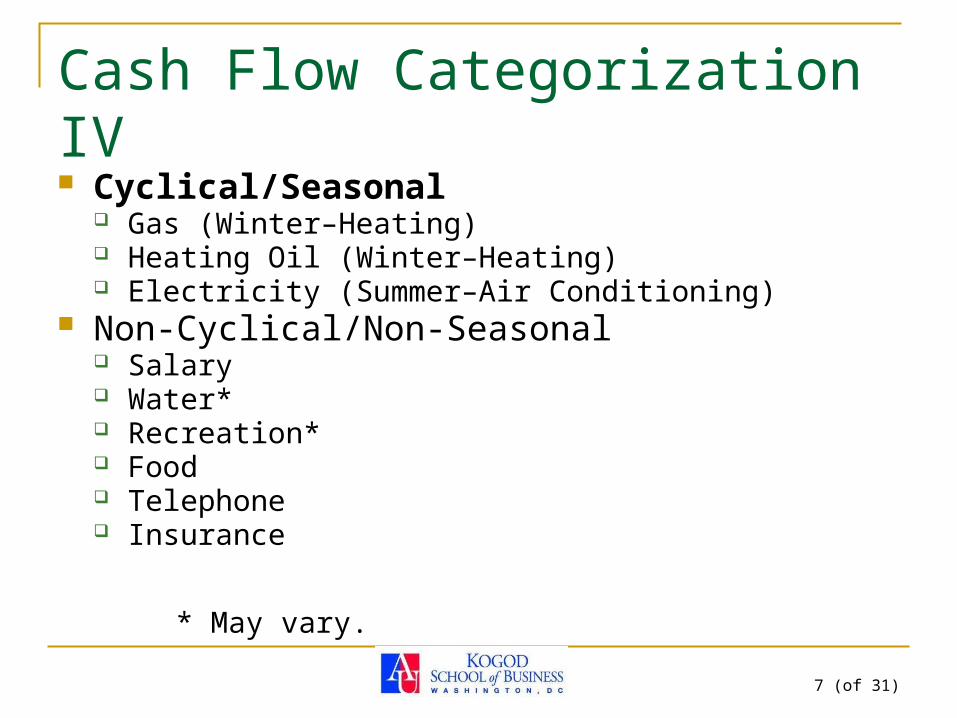

Cash Flow Categorization IV

Cyclical/Seasonal Gas (Winter–Heating) Heating Oil (Winter–Heating) Electricity (Summer–Air Conditioning)

Non-Cyclical/Non-Seasonal Salary Water* Recreation* Food Telephone Insurance

* May vary.

9 (of 31)

Salary

Paycheck versus Direct Deposit Pay Stub (Proof Monthly Earnings) Salary Estimation

Bureau of Labor Statistics (BLS) Data Salary Wizard (CNNMoney.com)

10 (of 31)

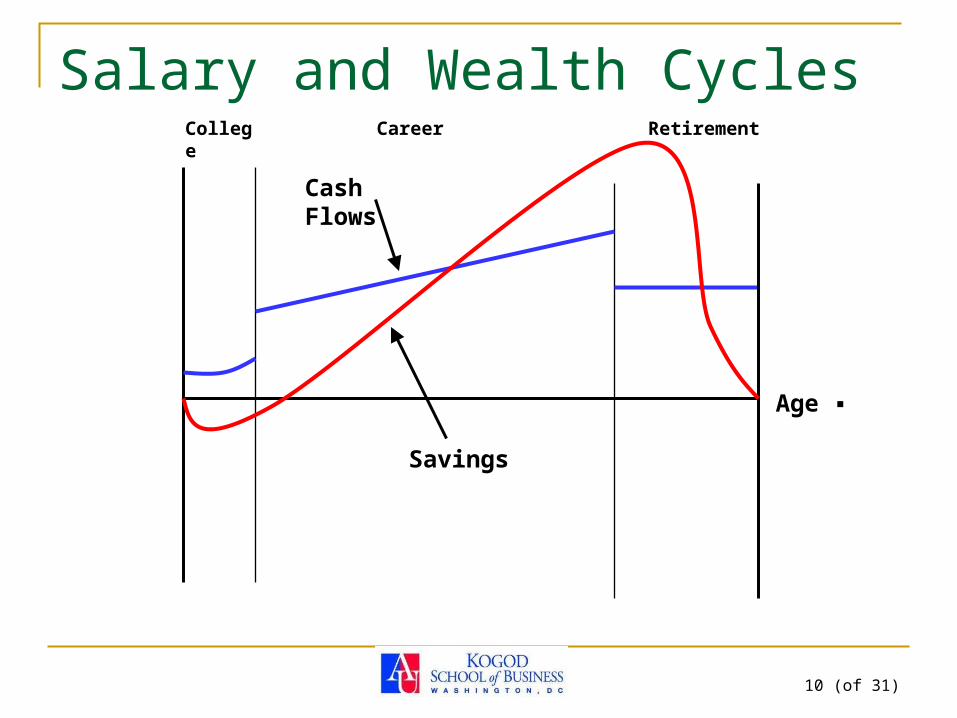

Salary and Wealth Cycles

Age ▪

Cash Flows

College Career Retirement

Savings

12 (of 31)

Withholdings

Employee’s Earnings Statement (Pay Stub) Federal Tax FICA/Med

FICA/Med (Social Security) Medicare

State Taxes Insurance (Medical and Life) Flexcomp (Flexible Spending Plan)

Medical Dependent Care

Retirement Contribution

13 (of 31)

Typical Cash Outflows

Rent/Mortgage Monthly, Constant Utilities (Some minimally voluntary) Insurance Auto Expenses Miscellaneous

Food, Recreation, Clothing

15 (of 31)

Assets

Market Value versus Price Paid Liquid Assets

Immediate Liquidity No Selling Loss Day-to-Day Expenses

Household Assets Very Little Liquidity High Selling Loss

Investments Moderate Liquidity No Selling Loss, but Commissions, etc.

16 (of 31)

Software I Packages

Quicken Money

Yodlee MoneyCenter Free service, but registration required Uses data from your bank accounts, credit cards,

mortgage, etc. Categorizes by type, not payee

Shell and Citco payments both go under ‘gas’ Net-worth statement Bill reminders Should be safe: used in major banks' online products

17 (of 31)

Software II

Mint.com Free service, but registration required Less sophisticated than MoneyCenter

No investment accounts But more user friendly Online community

Budget Calculator (CNNMoney.com)

18 (of 31)

Potential Problems

Cash Leakage You cannot Easily Monitor or Analyze Cash Payments

Going beyond your Financial Limits Spending, Borrowing

Thinking of Luxuries as Necessities Jimmy Choo shoes are not necessities. Nothing made by Ferrari is a necessity.

Spending More than You Make Spending Creep Misusing ‘Windfalls’, e.g., Bonuses Relying on ‘Windfalls’

20 (of 31)

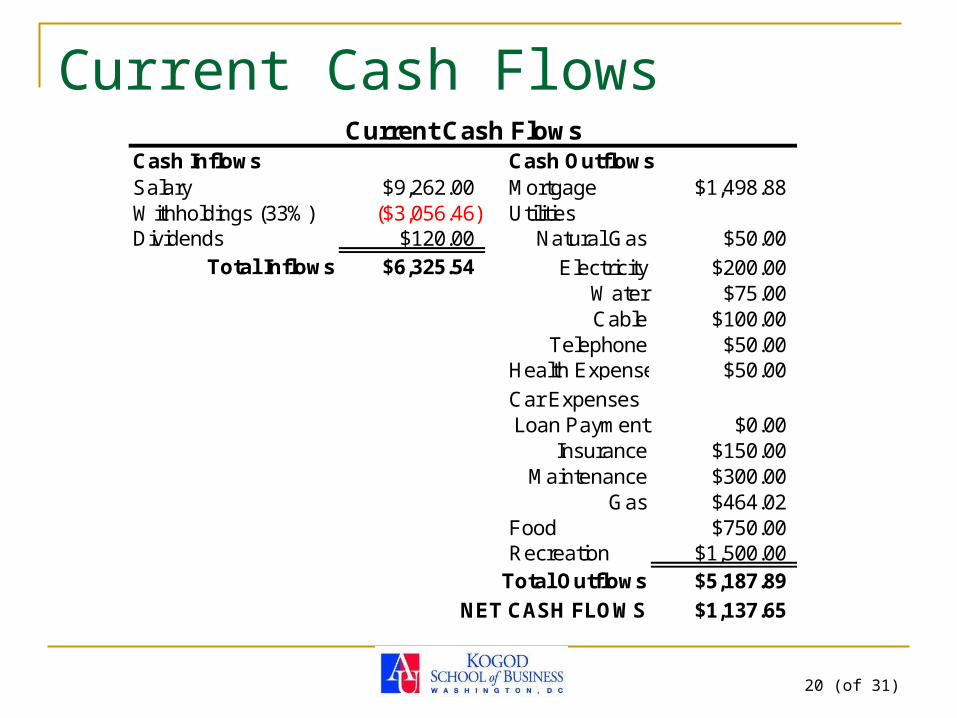

Current Cash FlowsCash Inflows Cash OutflowsSalary $9,262.00 Mortgage $1,498.88Withholdings (33%) ($3,056.46) UtilitiesDividends $120.00 Natural Gas $50.00

Total Inflows $6,325.54 Electricity $200.00Water $75.00Cable $100.00

Telephone $50.00Health Expenses $50.00

Car ExpensesLoan Payment $0.00

Insurance $150.00Maintenance $300.00

Gas $464.02Food $750.00Recreation $1,500.00

Total Outflows $5,187.89

NET CASH FLOWS $1,137.65

Current Cash Flows

21 (of 31)

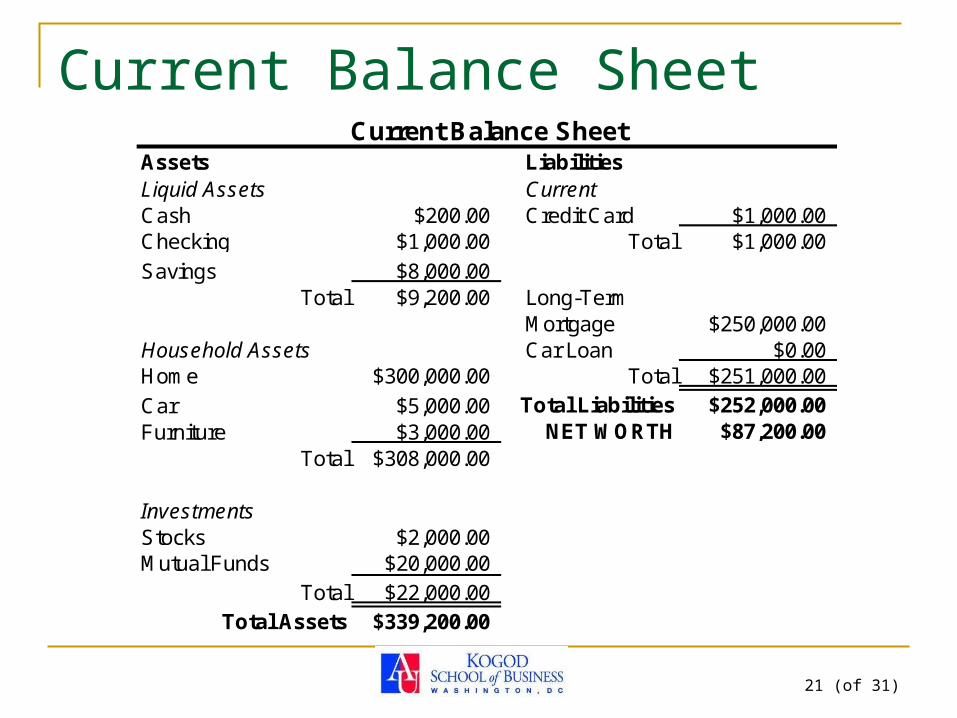

Current Balance SheetAssets LiabilitiesLiquid Assets CurrentCash $200.00 Credit Card $1,000.00Checking $1,000.00 Total $1,000.00

Savings $8,000.00Total $9,200.00 Long-Term

Mortgage $250,000.00Household Assets Car Loan $0.00Home $300,000.00 Total $251,000.00

Car $5,000.00 Total Liabilities $252,000.00Furniture $3,000.00 NET WORTH $87,200.00

Total $308,000.00

InvestmentsStocks $2,000.00Mutual Funds $20,000.00

Total $22,000.00Total Assets $339,200.00

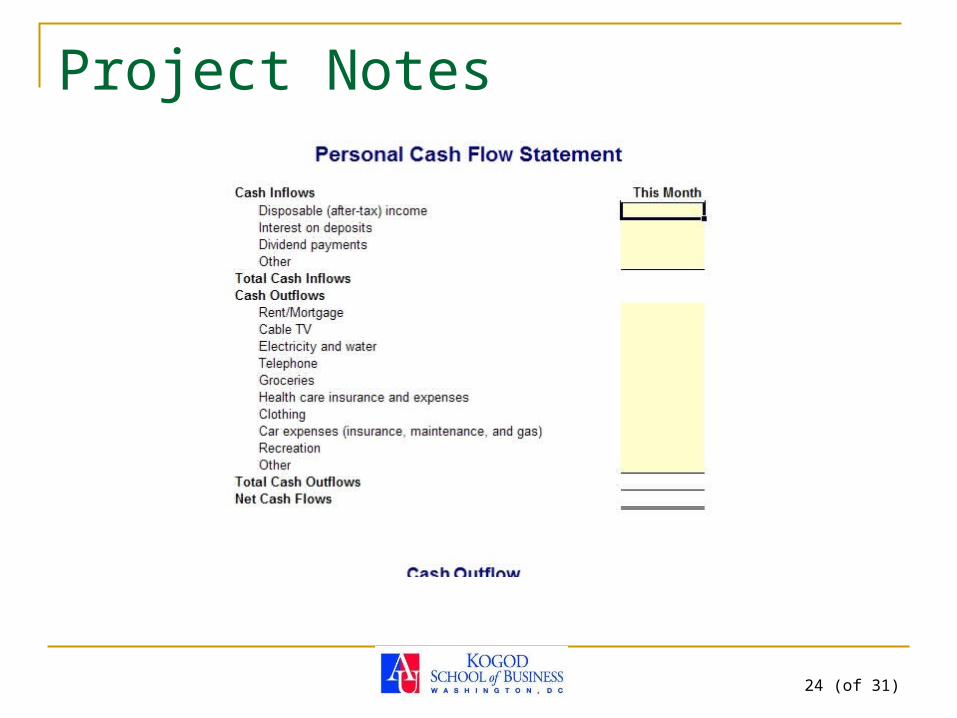

Current Balance Sheet

22 (of 31)

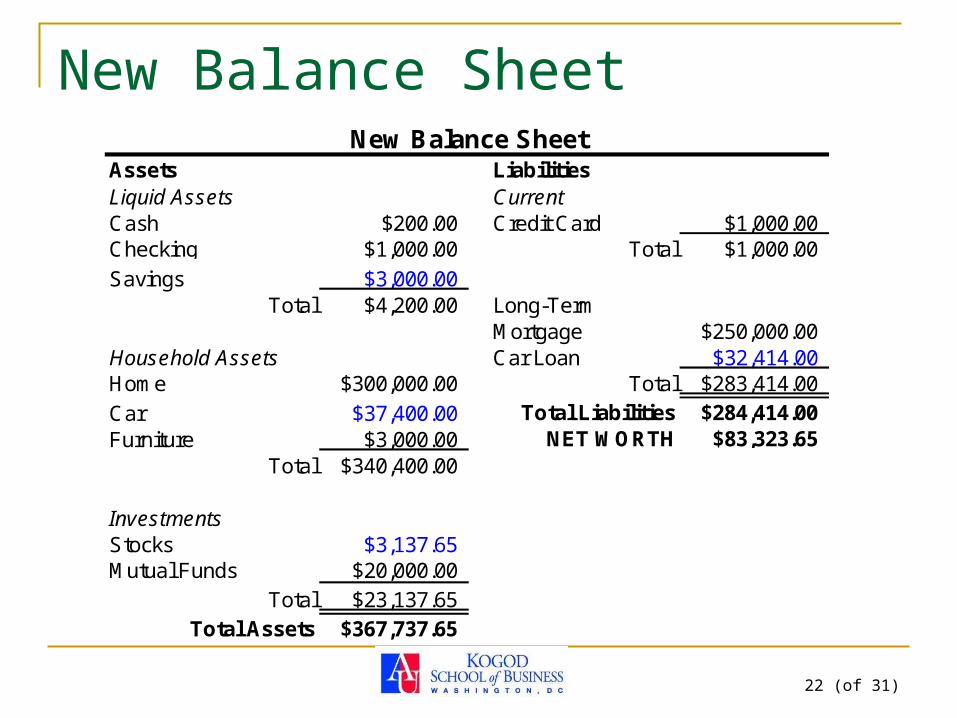

New Balance Sheet

Assets LiabilitiesLiquid Assets CurrentCash $200.00 Credit Card $1,000.00Checking $1,000.00 Total $1,000.00

Savings $3,000.00Total $4,200.00 Long-Term

Mortgage $250,000.00Household Assets Car Loan $32,414.00Home $300,000.00 Total $283,414.00

Car $37,400.00 Total Liabilities $284,414.00Furniture $3,000.00 NET WORTH $83,323.65

Total $340,400.00

InvestmentsStocks $3,137.65Mutual Funds $20,000.00

Total $23,137.65Total Assets $367,737.65

New Balance Sheet

23 (of 31)

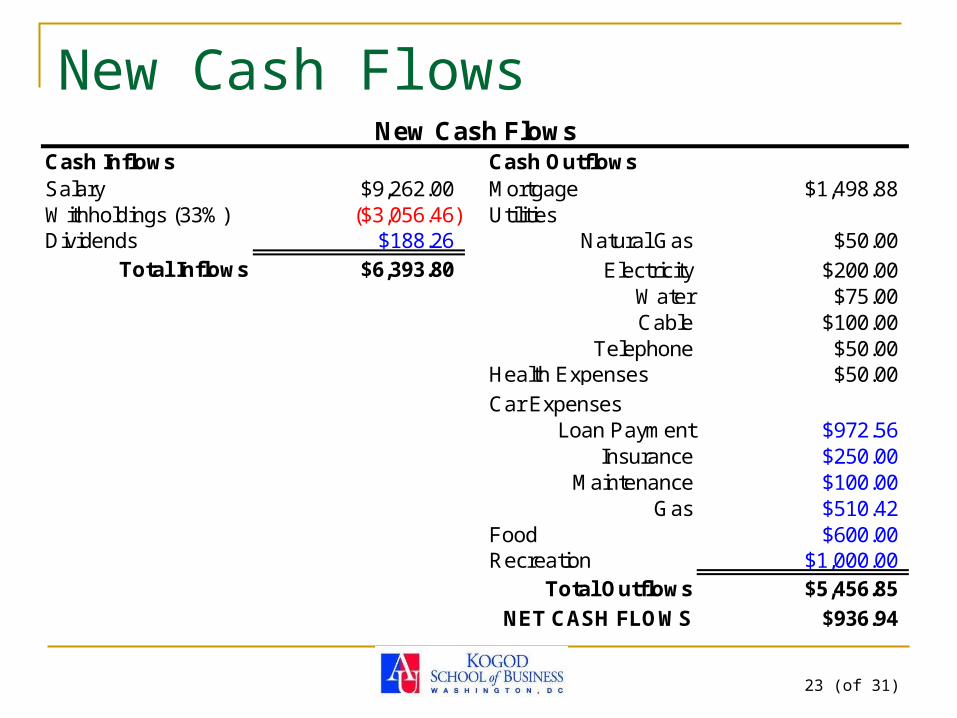

New Cash FlowsCash Inflows Cash OutflowsSalary $9,262.00 Mortgage $1,498.88Withholdings (33%) ($3,056.46) UtilitiesDividends $188.26 Natural Gas $50.00

Total Inflows $6,393.80 Electricity $200.00Water $75.00Cable $100.00

Telephone $50.00Health Expenses $50.00

Car ExpensesLoan Payment $972.56

Insurance $250.00Maintenance $100.00

Gas $510.42Food $600.00Recreation $1,000.00

Total Outflows $5,456.85

NET CASH FLOWS $936.94

New Cash Flows

25 (of 31)

Ethical Dilemma

Dennis and Nancy do not have sufficient money for a down payment on a house. Nancy's Uncle Charley has agreed to loan them the money, but requests a personal balance sheet and cash flow statement as well as tax returns for the last two years. While Dennis has been working substantial overtime, the overtime will not continue, so Uncle Charley may not loan them the money. They choose to provide the last two years' personal cash flow statements and tax returns, but not to provide any additional information unless he asks.

a. Comment on Nancy and Dennis' decision not to provide the information underlying their cash flow statement. What potential problems could result from their decision?

b. Discuss in general the disadvantages of borrowing money from relatives.