Embed Size (px)

Citation preview

1 (of 18)

IBUS 302: International Finance

Topic 9–Fisher Effects

Lawrence Schrenk, Instructor

2 (of 18)

Learning Objectives

1. Distinguish real versus nominal values. ▪

2. Calculate the real exchange rate and discuss its implications for international competition.

3. Describe the evidence for PPP and the reasons there may be deviations from it.

4. Explain the international Fischer effect and the forward expectations parity.▪

3 (of 18)

Real versus Nominal Values

Nominal Values Values before an adjustment for inflation The price stated in a contract The actual price you will pay either now or later

Real Values Values after an adjustment for inflation ‘Constant’ dollars Incorporates only productivity changes

The Fisher Effect (FE)

Variables Nominal return (i) Real Return (r) Inflation (p)

Relationship

NOTE: Do not use the approximation: i ≈ + rp

4 (of 18)

1 1 1 i E

5 (of 18)

If PPP Holds

If PPP holds There is inflation (i.e., price levels change) FX rates change cancelling the effects of inflation

So the changes have been only nominal Real exchange rate (q) = 1. International competitiveness does not

change The amount you can buy in dollar terms has not

changed.

6 (of 18)

If PPP Does Not Hold

If PPP does not hold There is inflation (i.e., price levels change) FX rates may change, but do not completely

cancel the effects of inflation So some part of the changes are real

Real exchange rate (q) ≠ 1. International competitiveness does change

The amount you can buy in dollar terms has changed.

7 (of 18)

q is the deviation from PPP q is the real exchange rate

e is the (empirical) percentage change in F based on current data. (Do not confuse it with ePPP which is the (theoretical) percentage change in F consistent with relative PPP.)

Real Exchange Rate

$1

1 1 x

qe

8 (of 18)

Formula:

Notation (not in the textbook)

ePPP is the percentage change in F predicted by PPP.e is the (empirical) percentage change in F based on

current data. If e = ePPP, then

PPP holds, i.e., no deviation and q = 1 International competitiveness does not change.

ePPP versus e

F Se

S

9 (of 18)

q and competitiveness < 1 domestic more competitive = 1 no change > 1 domestic less competitive

Real Exchange Rate and Competitiveness

10 (of 18)

Real Exchange Rate Example

p$ = 5%

p€ = 4% S($/€) = 1.4300 F($/€) = 1.4500 What is q?

Solution

Actual Change in Forward Rate

Real Exchange Rate

11 (of 18)

1.4500 1.4300

1.43000.0140 1.40%

F Se

S

$1 1.05

1.02121 1 1.0140 1.014x

qe

Analysis

If PPP held, then the forward rate should be:

The actual forward rate, F, is 1.4500, so PPP does not hold, and q > 1, so domestic trade is less competitive

12 (of 18)

$ 0.05 0.040.0096

1 1.04

1.4300 1.0096 1.4438

xPPP

x

PPP

e

F

Practice: Absolute PPP

Data US Big Mac $3.54 UK Big Mac £2.29 S($/£) = 1.4689

Questions What is SPPP($/£)? Does absolute PPP hold?

13 (of 18)

Practice: Relative PPP

S($/£) = 1.4689, F12($/£) = 1.4722, p$ = 7.4%, p£ = 6.1%

Question: Does relative PPP hold? What is ePPP?

What is FPPP?

14 (of 18)

$

1x

PPPx

e

PPPF ($/x) S($/x) 1 e

Practice: Relative PPP

S($/£) = 1.4689, F12($/£) = 1.4722, p$ = 7.4%, p£ = 6.1%

Question: If not what is the real exchange rate? What is e ? (Remember this is different from ePPP)

What is q?

15 (of 18)

F Se

S

$1

1 1 x

qe

Practice: Relative PPP

S($/£) = 1.4689, F12($/£) = 1.4722, p$ = 7.4%, p£ = 6.1%

Question: What are the implications for international competition?

16 (of 18)

19 (of 18)

PPP Deviations

Transportation Costs Shipping costs can remove arbitrage

opportunity; imports become relatively more expensive.

Trade Restrictions Example: Pharmaceutical Industry

Cost of Non-Tradable Inputs Taxes Productivity

‘Big Mac’ Index

Index Analysis

20 (of 18)

21 (of 18)

International Fischer Effect and the Forward

Expectations Parity

Overview

Interest Rate Parityinterest rates (i) → forward rate

Purchasing Power Parityinflation (p) → forward rate

Fisher Effect

interest rates (i) ↔ inflation (p)

22 (of 18)

23 (of 18)

Implications

IRP connects FX and interest rates PPP connects FX and inflation Fisher Effect connects interest rates and

inflation

PPP IRP

Fisher Effect

FX

Inflation Interest Rates

24 (of 18)

Fisher Effect (FE)

Inflation increases causes interest rate increase. Recall time value of money (TVM) motivations

Opportunity Costs Inflation Risk

Interest rates must compensate the investor for expected inflation:

1 1 1i E

Fisher Effect

Fisher Effect applies to all currencies individually:

25 (of 18)

$ $ $1 1 1i E

£ £ £1 1 1i E

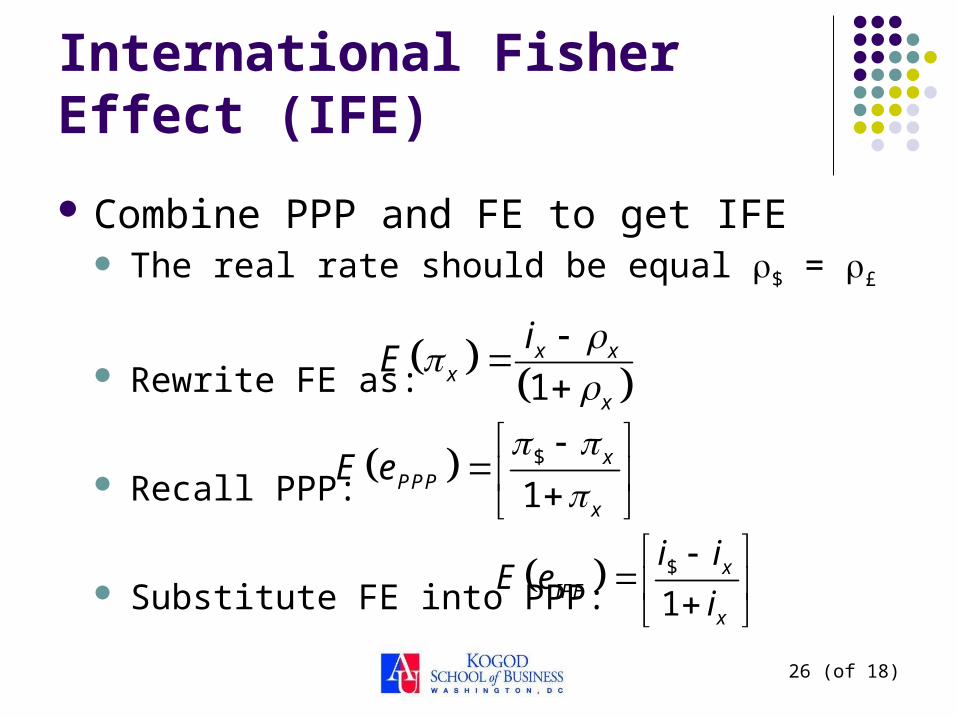

International Fisher Effect (IFE)

Combine PPP and FE to get IFE The real rate should be equal r$ = r£

Rewrite FE as:

Recall PPP:

Substitute FE into PPP:

26 (of 18)

1x x

xx

iE

$

1x

PPPx

E e

$

1x

IFEx

i iE e

i

Forward Expectations Parity (FEP)

Combine IFE and IRP to get FEP

Recall IFE:

Recall IRP (in a different form):

Combine IFE and IRP for FEP:

27 (of 18)

$

x1xIRP

IFE

i iF SE e

S i

$

1x

IFEx

i iE e

i

$

x1xIRP

i iF S

S i

Forward Expectations Parity (FEP): Implications I

Percentage Change Analysis

The percentage change in the exchange rate, i.e., the forward premium or discount, is equal to the expected change in the exchange rate.

28 (of 18)

$

x1xFEP

IFE

i iF SE e

S i

Forward Expectations Parity (FEP): Implications II

Forward Rate Analysis

The expected forward rate is equal to the spot rate increased by the expected change in the exchange rate.

29 (of 18)

$

x

1

where 1

FEP IFE

xIFE

E F S E e

i iE e

i

FEP Example

S($/A$) = 0.6495, i$ = 4.2%, iA$ = 3.3%

30 (of 18)

$ $

$

11

0.042 0.0330.6495 1 0.6552

1.033

AFEP

A

i iE F S

i

31 (of 18)

Implications

IRP connects FX and interest rates PPP connects FX and inflation Fisher Effect connects interest rates and

inflation ▪

PPP IRP

Fisher Effect

FX

Inflation Interest Rates

IFE

FEP ▪

Fisher Required Formulae

Fisher Effect (FE)

International Fisher Effect (IFE)

Forward Expectations Parity (FEP)

32 (of 18)

1 1 1i E

$

1x

IFEx

i iE e

i

$

x1xFEP

IFE

i iF SE e

S i