Embed Size (px)

Citation preview

1

ICON Plc.

Jefferies 3rd Annual Healthcare Conference

June 2009

2

Certain statements contained herein including, without limitation, statements containing the words “believes,” “anticipates,” “intends,” “expects” and words of similar import, constitute forward-looking statements concerning the Company's operations, performance, financial condition and prospects. Because such statements involve known and unknown risks and uncertainties, actual results may differ materially from those expressed or implied by such forward-looking statements. Given these uncertainties, prospective investors are cautioned not to place undue reliance on such forward-looking statements. The Company undertakes no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise.

Forward Looking Statements

3

Global Full Service Clinical Development

US 45%

EU 47%

ROW 8%

4

ICON’s Global Footprint

5

ICON plc Staff Growth 1990 - Today

5 18 40 70 100 180 250 340580

8301300

1500

199524182588

3036

4293

5292

69757100

6

Market Environment

7

Market Fundamentals still intact

• Outsourcing Penetration expected to increase

¯ More Strategic approach to outsourcing

¯ Cost containment

¯ Globalisation of clinical research

• Continued R&D Spending Growth.

¯ Pipelines remain solid

¯ Scientific innovation continues to expand

• Increasing Regulation

¯ More patients/ more studies

¯ Post marketing surveillance

8

• Clients are increasingly focused on their core competencies of¯ Discovery¯ Strategic Development¯ Marketing

• Clients are engaging CROs at a more strategic level¯ Level of management engagement (Executive to executive)¯ Level of co-operative engagement i.e. sharing drug pipeline intentions¯ Deeper reliance on CRO scientific and therapeutic expertise

• Reduced internal capacity in the companies of strategic partners e.g. staff or asset transfers/reductions

• Clients likely to move their % outsourced from ≈ 30% to >50% over the next 5+ years

Increased Outsourcing

9

Market Fundamentals still intact

• Outsourcing Penetration expected to increase

¯ More Strategic approach to outsourcing

¯ Cost containment

¯ Globalisation of clinical research

• Continued R&D Spending Growth.

¯ Pipelines remain solid

¯ Scientific innovation continues to expand

• Increasing Regulation

¯ More patients/ more studies

¯ Post marketing surveillance

10

Clinical Compounds in Development

11

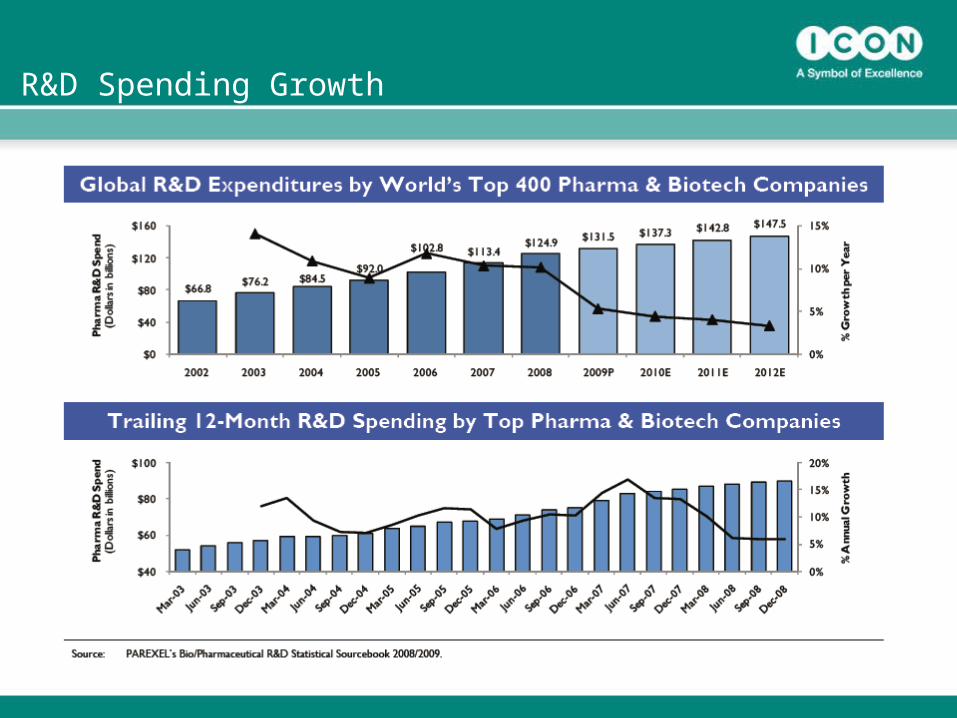

R&D Spending Growth

12

CRO Market Size (1996-2012E)

13

Total Biotech Funding (In Millions USD$)

Source: Burrill and Company

$9,397

$13,549

$10,332

$11,062

$6,647$6,249

$5,476

$11,754

$9,810

Q1 07 Q2 07 Q3 7 Q4 07 Q1 08 Q2 08 Q3 08 Q4 08 Q1 09

14

Market Fundamentals still intact

• Outsourcing Penetration expected to increase

¯ More Strategic approach to outsourcing

¯ Cost containment

¯ Globalisation of clinical research

• Continued R&D Spending Growth.

¯ Pipelines remain solid

¯ Scientific innovation continues to expand

• Increasing Regulation

¯ More patients/ more studies

¯ Post marketing surveillance

15

Opportunities…. but also Risks

16

ICON in this Market Environment

17

Gross and Net Volume of RFPs

2003 to Q1 2009

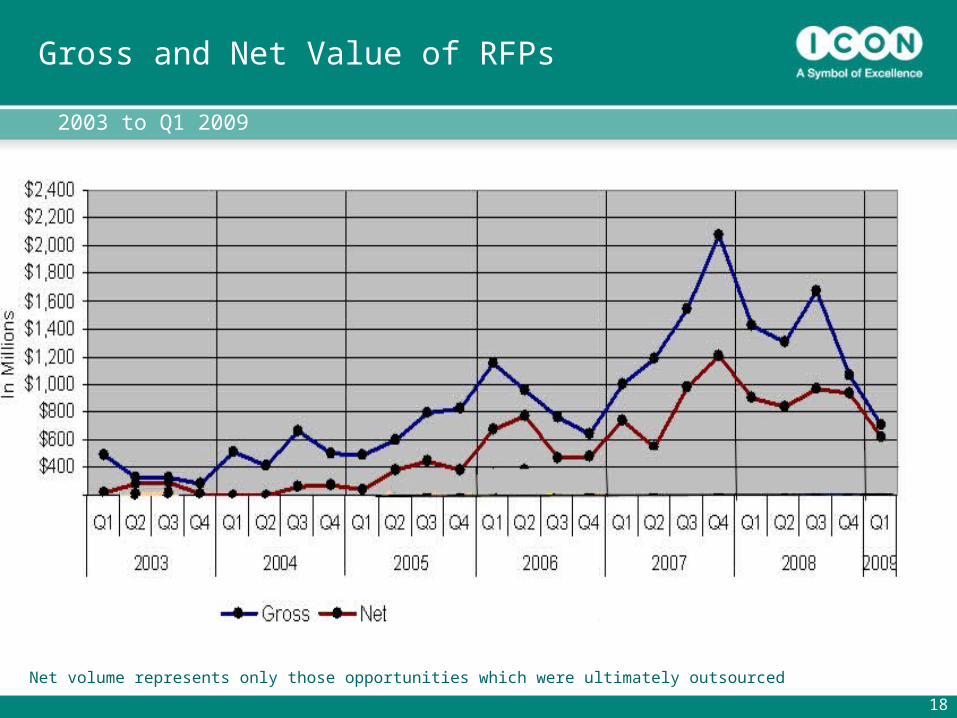

Net volume represents only those opportunities which were ultimately outsourced

1818

Gross and Net Value of RFPs

2003 to Q1 2009

Net volume represents only those opportunities which were ultimately outsourced

19

Net New Business wins and book to bill ratios

$344

$369

$337$350

$261 $265

Q4 07 Q1 08 Q2 08 Q3 08 Q4 08 Q1 09

1.9

1.6

1.21.2

1.5

1.8

Net Business Wins Book to Bill Ratio

20

Analysis of Business Wins

Q1 09 Net Wins

53% Large

Pharma

2008 Net Wins

Large Pharma

Large Bio

Mid PharmaMid BioSmall Bio and Small Pharma

50%

13%

18%

12%7%

68%7%

18%6%

21

Analysis of Backlog by Client at the end of Q1 09

53% Large

Pharma

Large Pharma

Large Bio

Mid PharmaMid BioSmall Bio and Small Pharma

53%

16%

17%

2% 12%

22

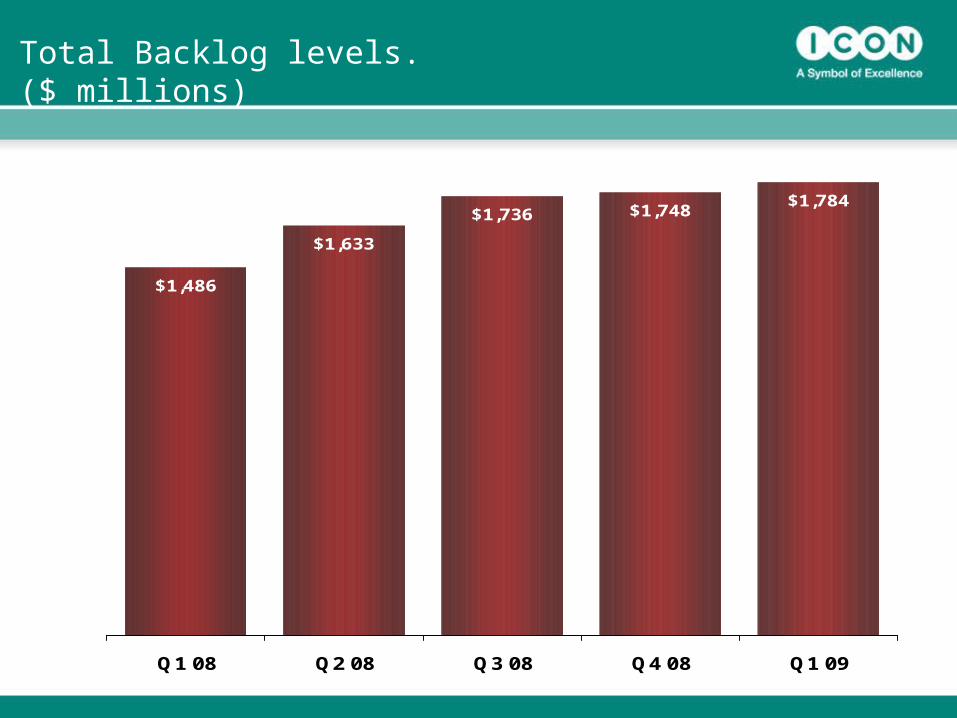

Total Backlog levels. ($ millions)

$1,486

$1,633

$1,736 $1,748$1,784

Q1 08 Q2 08 Q3 08 Q4 08 Q1 09

23

Coverage of next 4 quarters from backlog

$690

$752 $762

$707$673

Q1 08 Q2 08 Q3 08 Q4 08 Q1 09

71%

76% 77% 77%

74%

Value of backlog forecast to be earned in next 4 quarters

% coverage of next 4 quarters forecast revenues

24

Projects of longer duration leads to slower backlog burn

15.5%14.6%

13.8%12.7% 12.6%

Q1 08 Q2 08 Q3 08 Q4 08 Q1 09

25

Strategy

26

Capitalise on market fundamentals to drive organic growth in all business units.

Cross-sell services to grow sales and margin

Build Deep Strategic Relationships

Create Stronger differentiation across our services

Retain a flexible business model to respond to differing client outsourcing strategies

Pursue acquisitions to enhance depth and scale of current operations and to add additional

complementary services e.g.

Phase I

Bioanalytical / Biomarkers

Therapeutic specialists

ICON’s Core Strategy is Organic Growth,with acquisitions made to add new services or scale.

Acquisitions to date - 13

• Revenues acquired $130m

• Staff acquired – 1,200

• => Organic growth >80%

Safety / Late Phase

Imaging

Japan

27

Market Feedback

28

ICON in Recent Survey's

“ICON is one of three CRO’s cited most frequently as sponsor’s favourite CRO vendors”

“Our confidence goes up that ICON is the right name to own in this environment, given their consistent quality”

William Blair fourth survey of Pharma and Biotech Sponsors.

“ ICON is a darling of the industry, the company's stunning growth in 2006 and 2007 surprised its peers. Now, the Dublin-based company is still outpacing just about everybody, but at a less accelerated clip.”

Eric Coldwell Clinpage 2009 Master Providers

29

Financial Performance

30

Net Revenue CAGR of 30% since 2005

$865

$631

$456

$327

$930

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900

$1,000

FY2005 FY2006 FY2007 FY2008 FY2009*

Mil

lio

ns

CAGR 30%

* Lower end of 2009 Guidance

(E)

31

Earnings Per Share Growth

$0.43

$0.68

$0.94

$1.30

$1.40

-$0.10

$0.10

$0.30

$0.50

$0.70

$0.90

$1.10

$1.30

$1.50

FY2005 FY2006 FY2007 FY2008 FY2009*

CAGR 34%(E)

* Lower end of 2009 Guidance

32

Cash flow from Operations/Free Cash Flow

11

26

11

47

70

82

4350

25

100

2005 2006 2007 2008 2009*

Millio

ns

CFFO

FCF

* Estimate assumes DSO of approx 60 days. Historic periods FCF exclude Head-office construction costs

1.17

0.77

0.180.19

0.45

FCF Per Share

33

Return on Equity

6%

13%

14%

17%

2005 2006 2007 2008

34

Recent Financial Performance ($ millions) Quarter 1 09

31 Mar 09 31 Mar 08 % Increase

Net Revenue 220 201 9.2%

Direct Costs 124 113 9.7%

SG & AEBITDA

6135

6028

1.2%25%

D & A 8 6 23%

EBIT 27 22 25%

Net Income 21 17 24%

EPS (Inc SFAS 123R) 35c 28c 25%

Weighted Average no. of Shares (Inc SFAS123R)

59.7m 60.1m (0.7%)

35

Recent Financial Performance ($ millions) FY 08

31 Dec FY 2008

31 Dec FY 2007

% Increase

Net Revenue 865 631 37%

Direct Costs 489 354 38%

SG & AEBITDA

248128

18988

32%45%

D & A 28 19 46%

EBIT 100 69 44%

Net Income 78 56 40%

EPS (Inc SFAS 123R) 130c 94c 38%

Weighted Average no. of Shares (Inc SFAS123R)

60.2m 59.5m 1.2%

36

Summary Balance Sheet and Cash Flow ($ millions)

Qtr endedMar 31, 09

Full Year ended

Dec 31, 08

Full Year ended

Dec 31, 07

Full Year ended

Dec 31, 06

Cash $96.9 $101.1 $118.6 $102.9

Debt $99.2 $105.4 $94.8 $5

Net Cash/Debt ($2.3) ($4.3) $23.8 $97.9

Total assets $850.5 $867.3 $693.1 $476.3

Total Liabilities $376.1 $410.9 $304.9 $173.6

Shareholder’s equity $474.4 $456.4 $388.4 $302.7

Cashflow from operations

$24.7 $81.3 $42.9 $50.4

Capital expenditures $8.1 $67.9 $75.4 $31.5

37

ICON Key Financial Metrics ($ millions)

Qtr endedMar 31, 09

Full Year ended

Dec 31, 08

Full Year ended

Dec 31, 07

Full Year ended

Dec 31, 06

Sales Growth 9.2% 37% 38% 39%

EPS Growth 25% 38% 41% 177%

EBITDA Margin 15.7% 14.7% 14% 13.8%

EBIT Margin 12.2% 11.5% 11.0% 10.5%

ROE 17.7%* 17% 14% 13%

* Annualised on the basis of Q1 net income

38

ICON plc Historic Share Price Performance

ICON

S&P 500

Nasdaq Composite

39

• Top Global Clinical CRO - #4• Deep customer relationships• Quality of staff• Experienced Management team• Excellent Reputation• Solid market fundamentals • Outstanding record of growth • Strong balance sheet

Investment Case Summary