Embed Size (px)

Citation preview

1

Holiday Inn Harbourside Holiday Inn Harbourside •• Indian Rocks Beach, Florida Indian Rocks Beach, Florida

Irvin N. GleimIrvin N. GleimOctober 8, 2004October 8, 2004

2

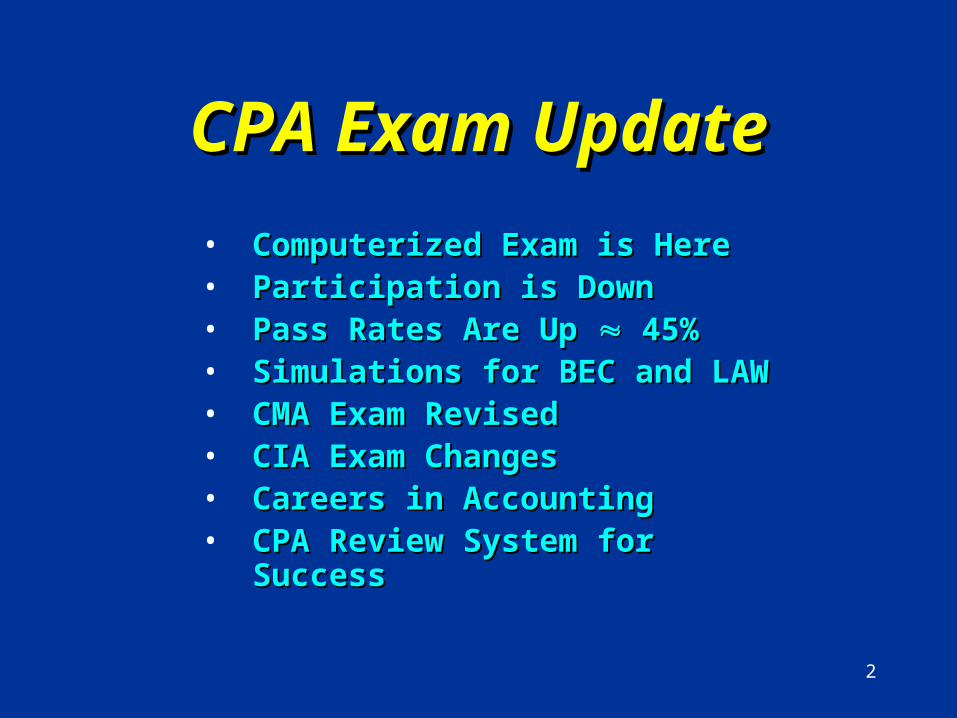

CPA Exam UpdateCPA Exam Update

• Computerized Exam is HereComputerized Exam is Here• Participation is DownParticipation is Down• Pass Rates Are Up Pass Rates Are Up 45% 45%• Simulations for BEC and LAWSimulations for BEC and LAW• CMA Exam RevisedCMA Exam Revised• CIA Exam ChangesCIA Exam Changes• Careers in AccountingCareers in Accounting• CPA Review System for SuccessCPA Review System for Success

3

http://www.cpa-exam.orghttp://www.cpa-exam.org

4

Thomson PrometricThomson Prometric

5

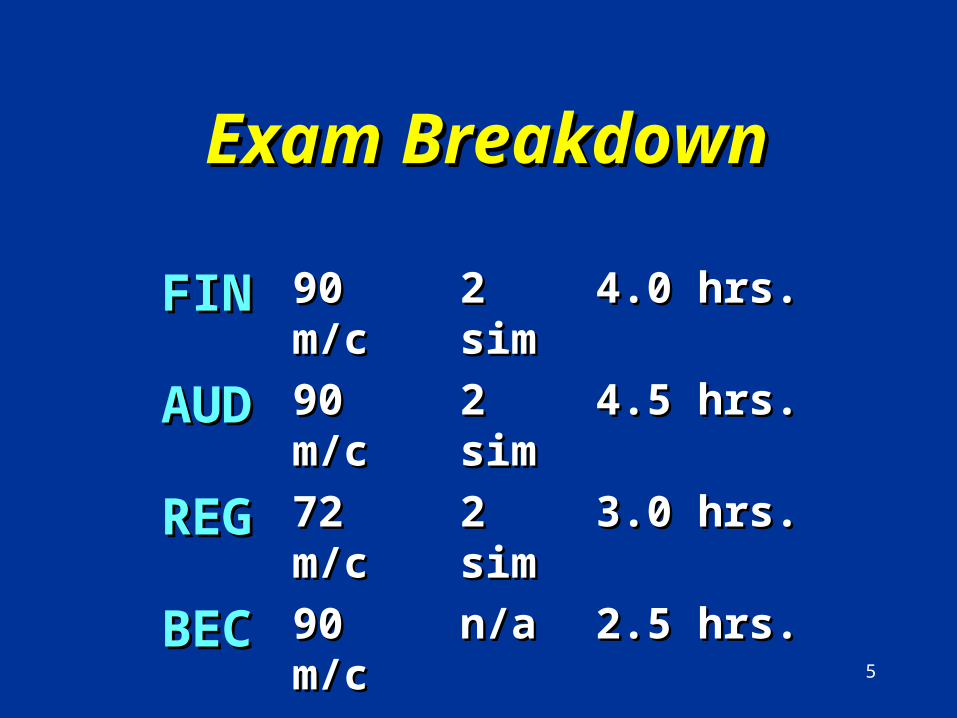

Exam BreakdownExam Breakdown

FINFIN 90 m/c90 m/c 2 sim2 sim 4.0 hrs.4.0 hrs.

AUDAUD 90 m/c90 m/c 2 sim2 sim 4.5 hrs.4.5 hrs.

REGREG 72 m/c72 m/c 2 sim2 sim 3.0 hrs.3.0 hrs.

BECBEC 90 m/c90 m/c n/an/a 2.5 hrs.2.5 hrs.

6

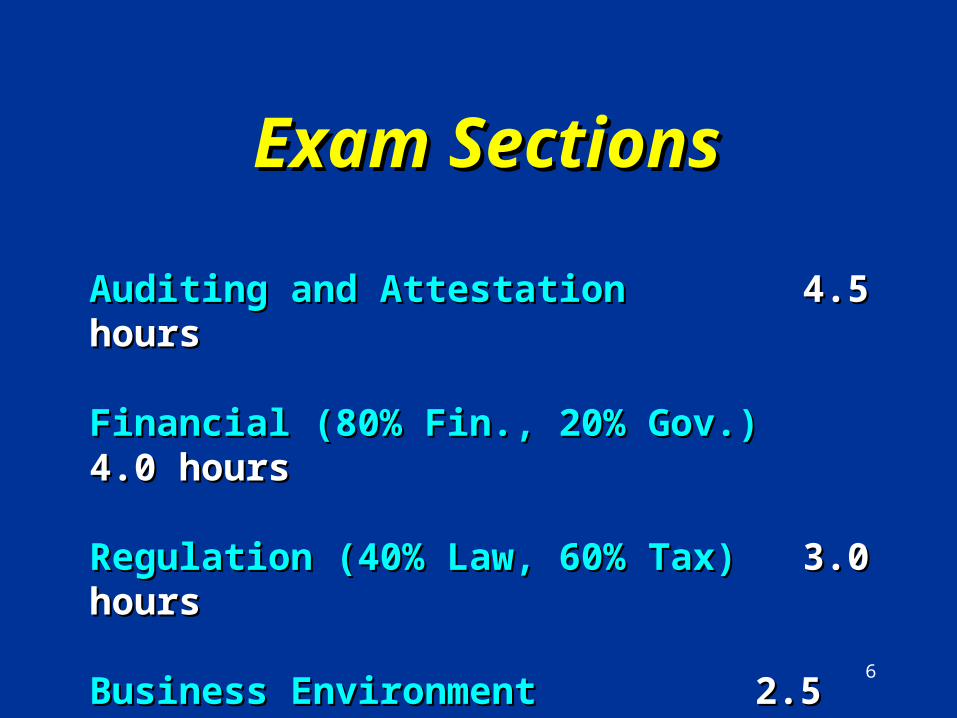

Auditing and AttestationAuditing and Attestation 4.5 hours4.5 hours

Financial (80% Fin., 20% Gov.)Financial (80% Fin., 20% Gov.) 4.0 hours4.0 hours

Regulation (40% Law, 60% Tax)Regulation (40% Law, 60% Tax) 3.0 hours3.0 hours

Business EnvironmentBusiness Environment 2.5 hours2.5 hours

Exam SectionsExam Sections

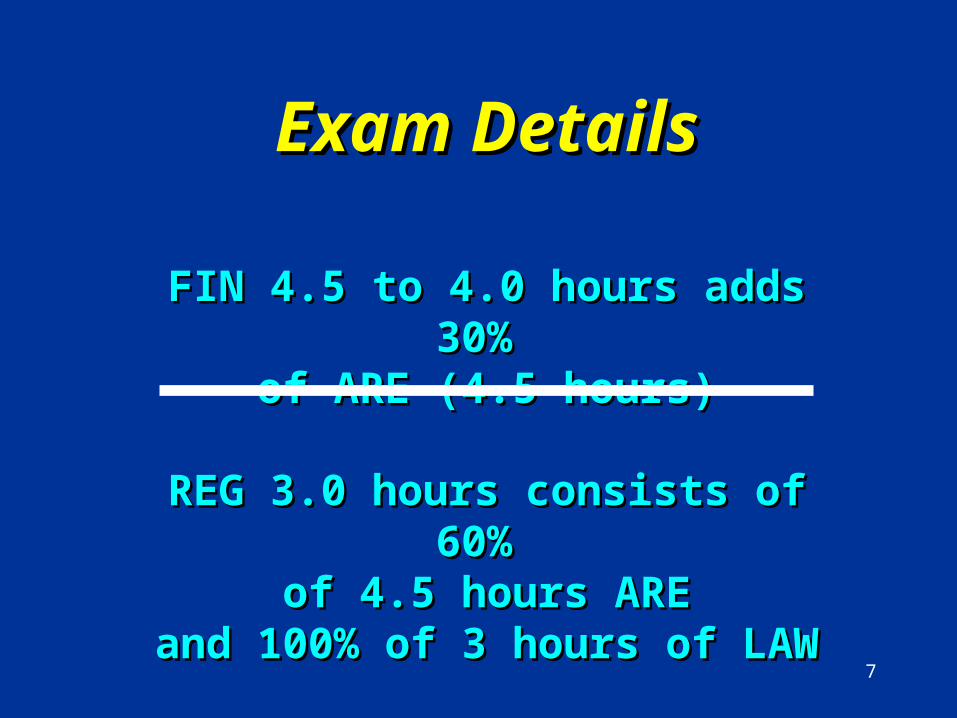

7

FIN 4.5 to 4.0 hours adds 30% FIN 4.5 to 4.0 hours adds 30% of ARE (4.5 hours)of ARE (4.5 hours)

REG 3.0 hours consists of 60% REG 3.0 hours consists of 60% of 4.5 hours AREof 4.5 hours ARE

and 100% of 3 hours of LAWand 100% of 3 hours of LAW

Exam DetailsExam Details

8

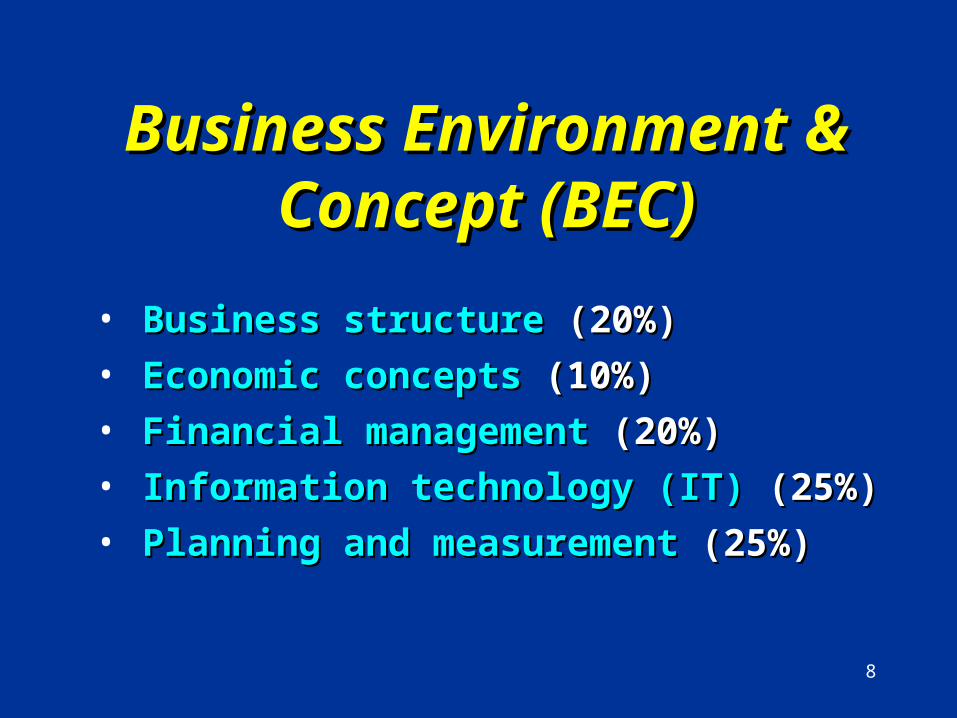

• Business structure Business structure (20%)(20%)

• Economic concepts Economic concepts (10%)(10%)

• Financial management Financial management (20%)(20%)

• Information technology (IT) Information technology (IT) (25%)(25%)

• Planning and measurement Planning and measurement (25%)(25%)

Business Environment & Business Environment & Concept (BEC)Concept (BEC)

9

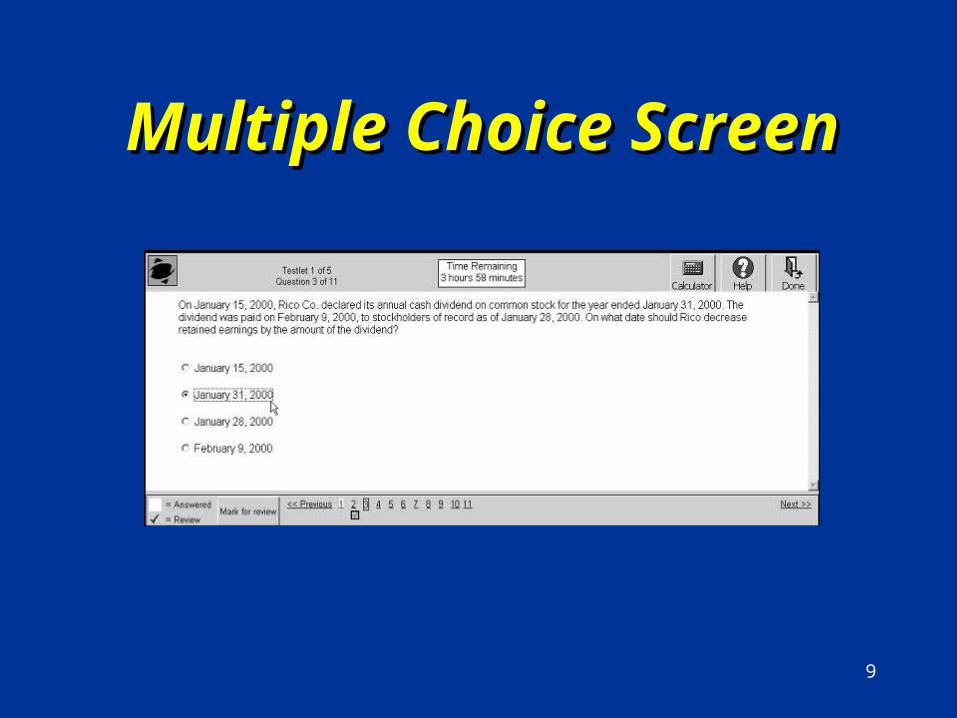

Multiple Choice ScreenMultiple Choice Screen

10

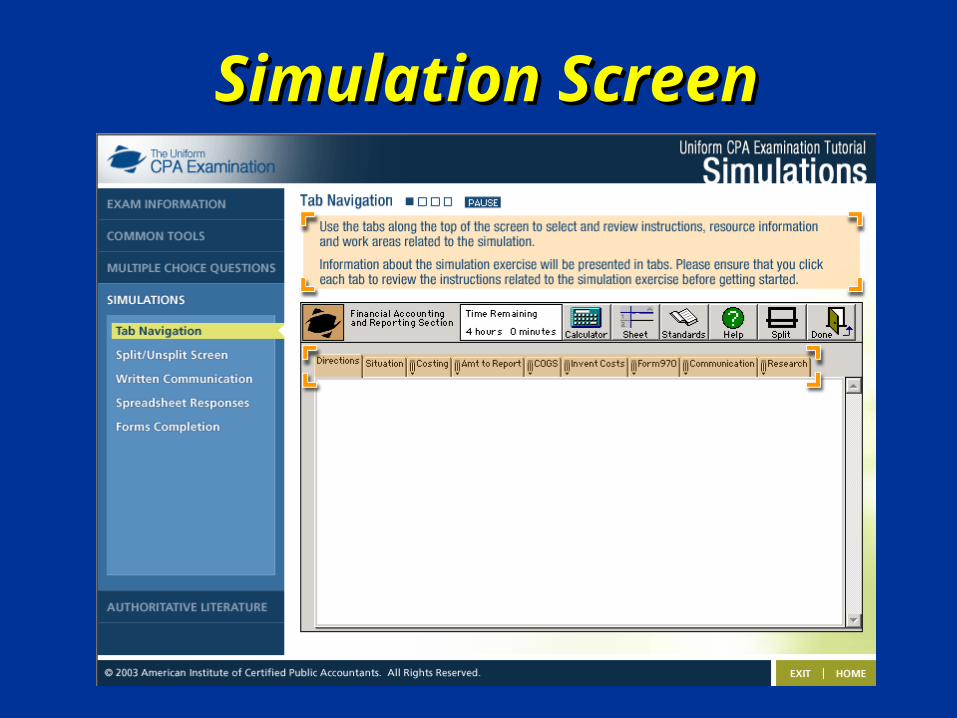

Simulation ScreenSimulation Screen

11

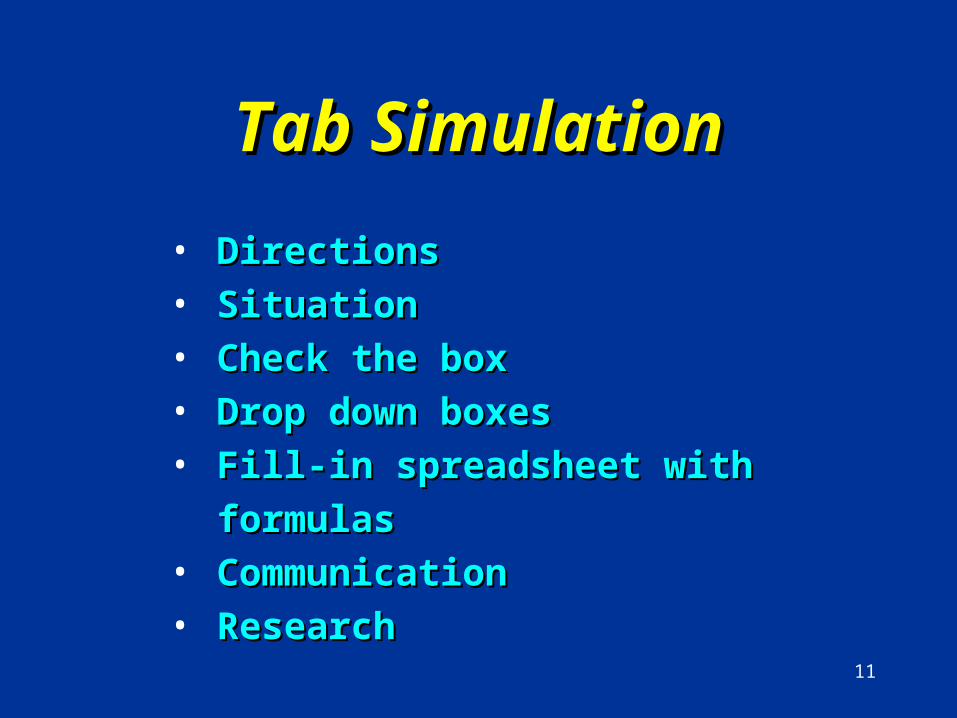

• DirectionsDirections• SituationSituation• Check the boxCheck the box• Drop down boxesDrop down boxes• Fill-in spreadsheet with formulasFill-in spreadsheet with formulas• CommunicationCommunication• ResearchResearch

Tab SimulationTab Simulation

12

ParticipationParticipation

Pre 2004Pre 2004

140,000140,000++ 108,000 parts 108,000 parts

320,000 320,000 340,000 parts 340,000 parts

20042004

Window 1 Window 1 –– 23,000 parts 23,000 parts

Window 2 Window 2 –– 40,000 parts 40,000 parts

13

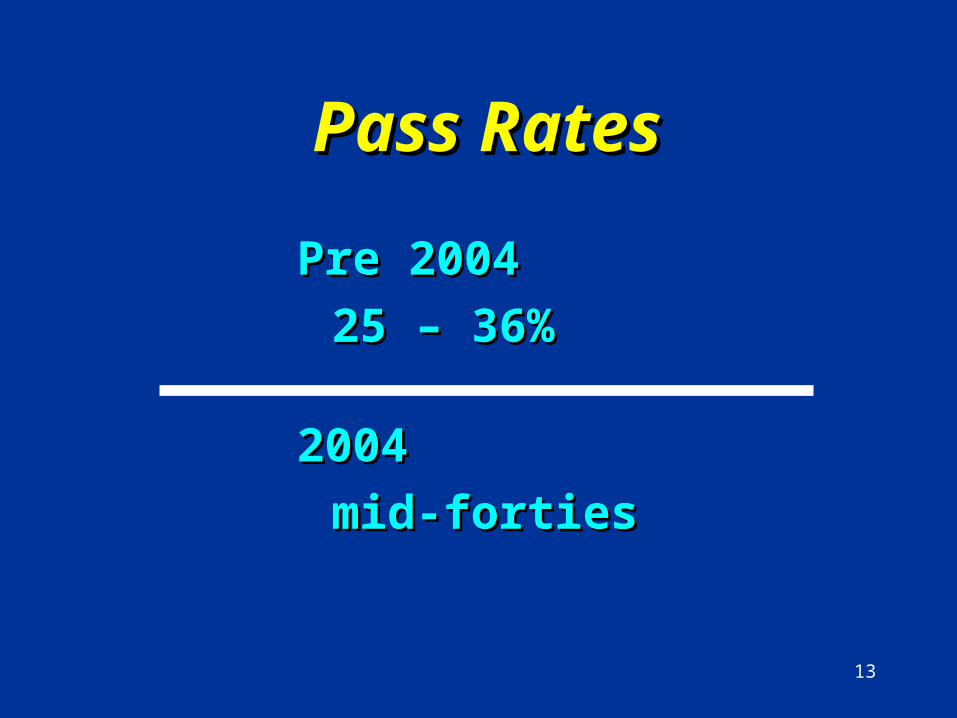

Pass RatesPass Rates

Pre 2004Pre 2004

25 – 36%25 – 36%

20042004

mid-fortiesmid-forties

14

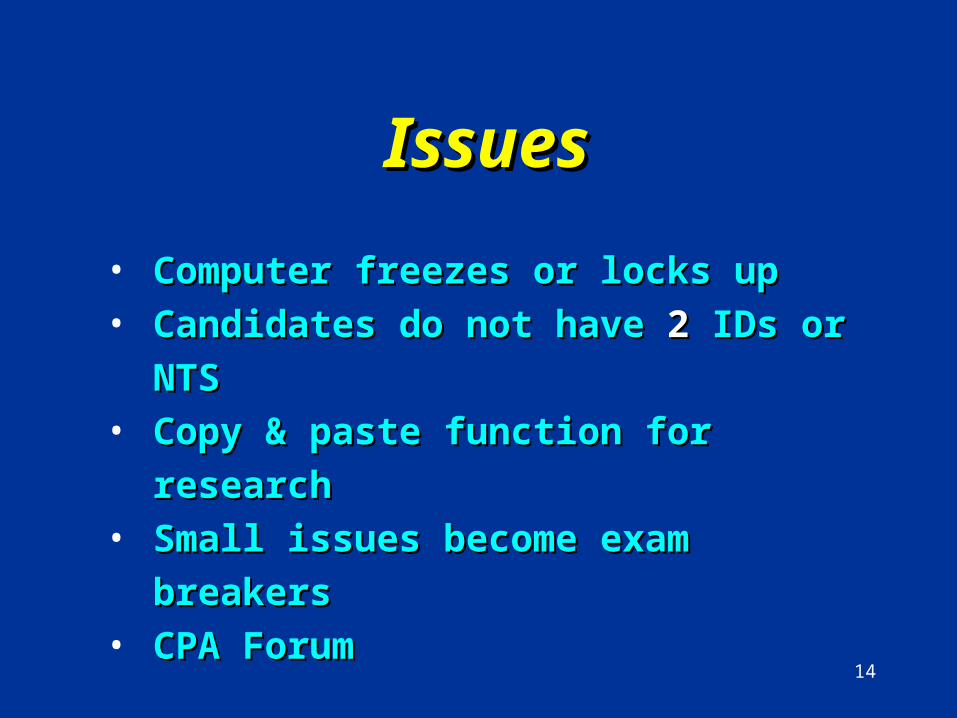

• Computer freezes or locks upComputer freezes or locks up• Candidates do not have Candidates do not have 22 IDs or NTS IDs or NTS• Copy & paste function for researchCopy & paste function for research• Small issues become exam breakersSmall issues become exam breakers• CPA ForumCPA Forum

IssuesIssues

15

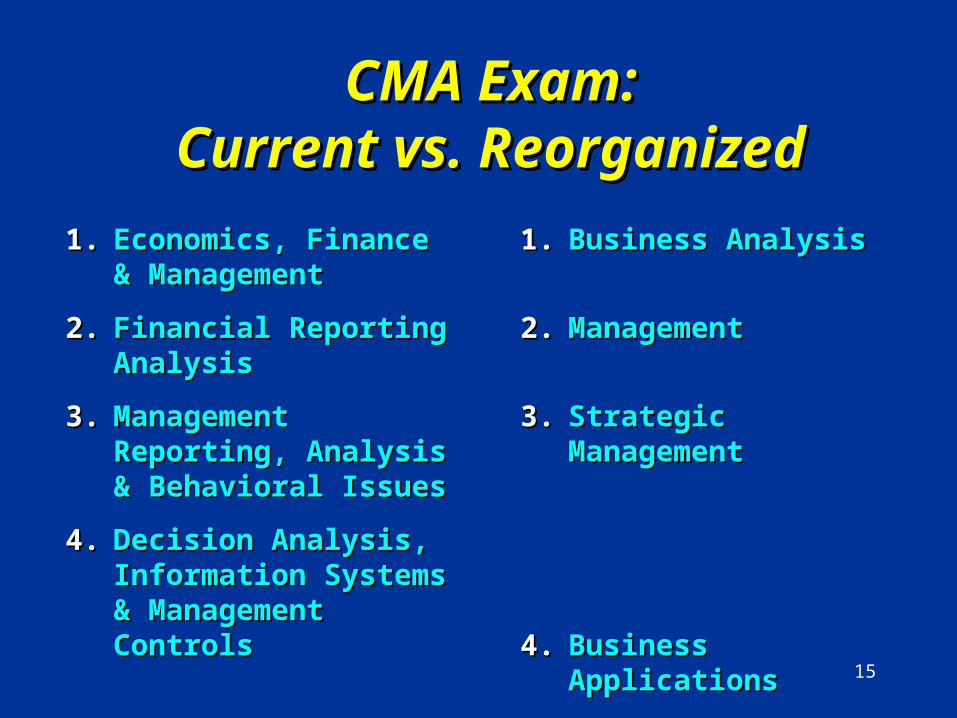

CMA Exam:CMA Exam:Current vs. ReorganizedCurrent vs. Reorganized

1.1. Economics, Finance & Economics, Finance & ManagementManagement

2.2. Financial Reporting Financial Reporting AnalysisAnalysis

3.3. Management Reporting, Management Reporting, Analysis & Behavioral Analysis & Behavioral IssuesIssues

4.4. Decision Analysis, Decision Analysis, Information Systems & Information Systems & Management ControlsManagement Controls

1.1. Business Analysis Business Analysis Management

2.2. Management Management Accounting &

3.3. Strategic Management Strategic Management Strategic Management Strategic Management

4.4. Business ApplicationsBusiness Applications Information Systems & Management Controls

16

CIA ExamCIA Exam

• 80 – 125 questions80 – 125 questions• Still paper and pencilStill paper and pencil• High growthHigh growth

17

CIA ExamCIA Exam

• Internal Audit RoleInternal Audit Role• Internal Audit EngagementInternal Audit Engagement• Business Analysis & Business Analysis &

Information TechnologyInformation Technology• Business Management SkillsBusiness Management Skills

18

Careers

19

SFS

20

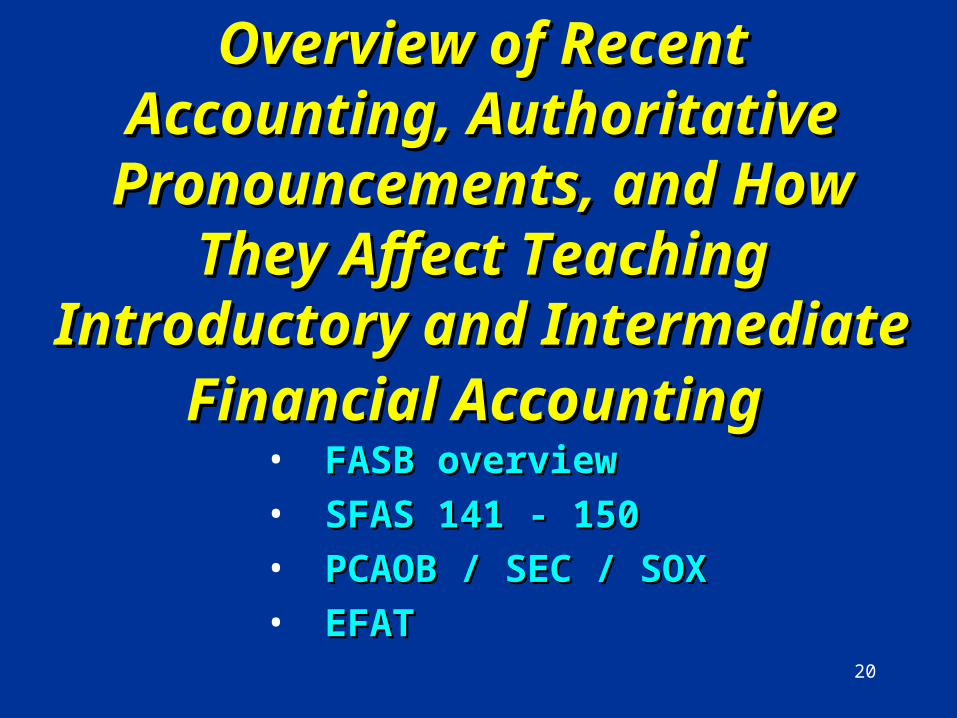

• FASB overviewFASB overview

• SFAS 141 - 150SFAS 141 - 150

• PCAOB / SEC / SOXPCAOB / SEC / SOX

• EFATEFAT

Overview of Recent Accounting, Overview of Recent Accounting, Authoritative Pronouncements, and Authoritative Pronouncements, and

How They Affect Teaching How They Affect Teaching Introductory and Intermediate Introductory and Intermediate

Financial AccountingFinancial Accounting

21

FASB

22

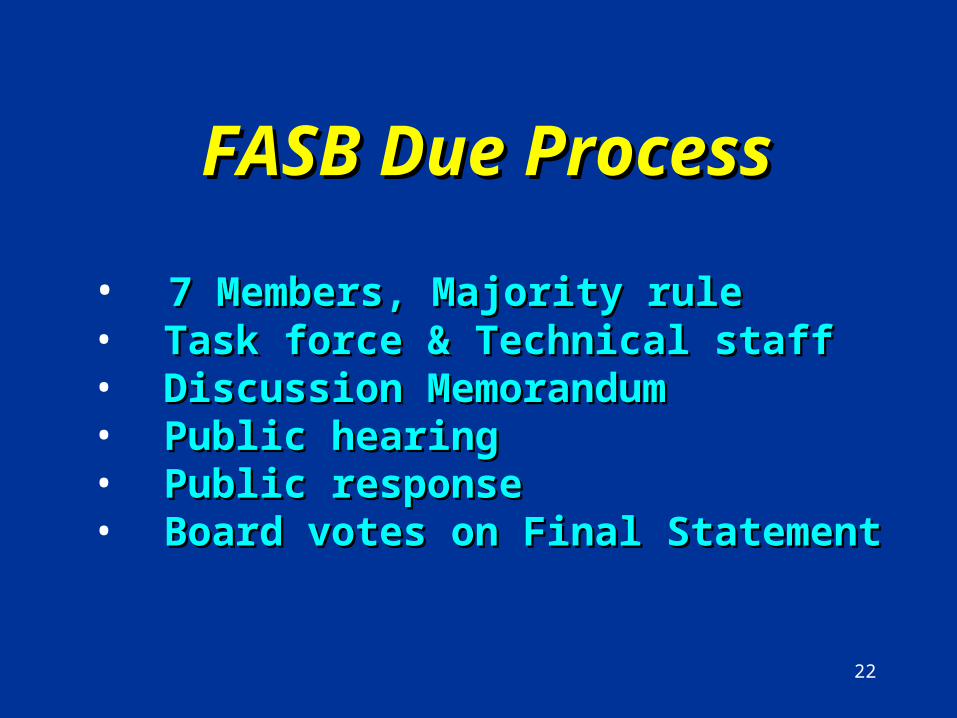

FASB Due ProcessFASB Due Process

• 7 Members, Majority rule7 Members, Majority rule• Task force & Technical staffTask force & Technical staff• Discussion MemorandumDiscussion Memorandum• Public hearingPublic hearing• Public responsePublic response• Board votes on Final StatementBoard votes on Final Statement

23

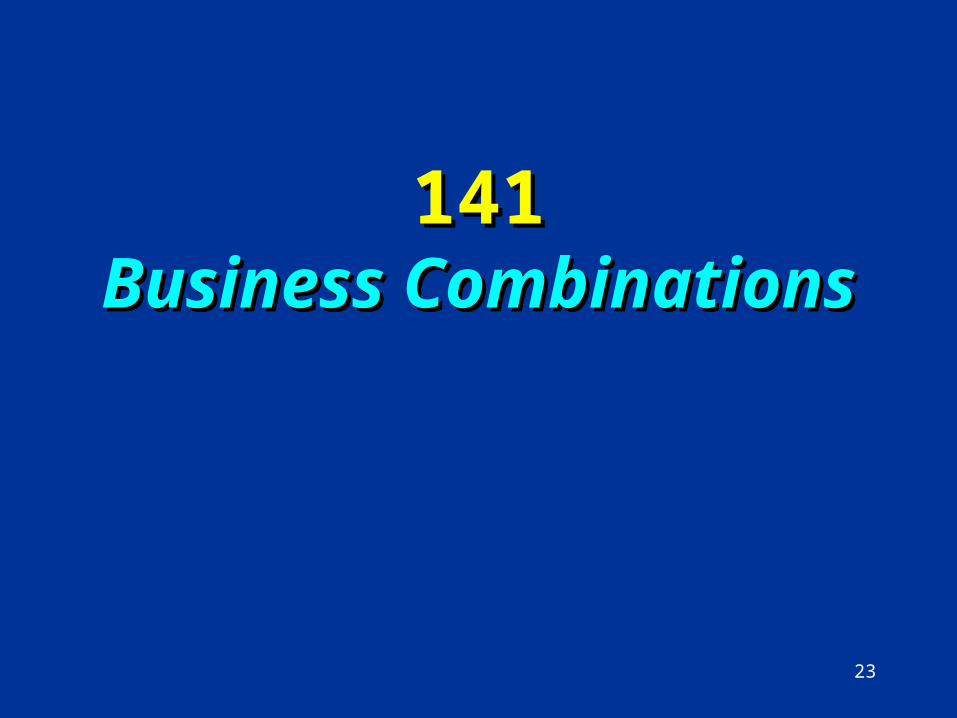

141141Business CombinationsBusiness Combinations

24

142142Goodwill and Other Goodwill and Other

Intangible AssetsIntangible Assets

25

143143AccountingAccounting

for Asset Retirementfor Asset RetirementObligationsObligations

26

144144Accounting for the Accounting for the

Impairment or Disposal of Impairment or Disposal of Long-Lived AssetsLong-Lived Assets

27

145145Rescission ofRescission of

FASB Statements No. 4, 44,FASB Statements No. 4, 44,and 64, Amendment ofand 64, Amendment of

FASB Statement No. 13, and FASB Statement No. 13, and Technical CorrectionsTechnical Corrections

28

146146Accounting forAccounting for

Costs Associated with ExitCosts Associated with Exitor Disposal Activitiesor Disposal Activities

29

147147Acquisitions ofAcquisitions of

Certain Financial Institution-Certain Financial Institution-an amendment ofan amendment of

FASB Statements No. 72 andFASB Statements No. 72 and144 and FASB144 and FASB

Interpretation No. 9Interpretation No. 9

30

148148Accounting forAccounting for

Stock-Based Compensation-Stock-Based Compensation-Transition andTransition and

Disclosure- an amendmentDisclosure- an amendmentof FASB Statementof FASB Statement

No. 123No. 123

31

149149AmendmentAmendment

of Statement 133 onof Statement 133 onDerivative Instruments and Derivative Instruments and

Hedging ActivitiesHedging Activities

32

150150Accounting forAccounting for

Certain Financial InstrumentsCertain Financial Instrumentswith Characteristicswith Characteristics

of bothof bothLiabilities and EquityLiabilities and Equity

33

132 Revised132 RevisedEmployers’ DisclosureEmployers’ Disclosure

about Pensionsabout Pensionsand Other Post-retirementand Other Post-retirement

Benefits- anBenefits- anamendment of FASBamendment of FASB

Statements No. 87,Statements No. 87,88, and 10688, and 106

34

Interpretation 46 RevisedInterpretation 46 RevisedConsolidation ofConsolidation of

Variable Interest Entities-Variable Interest Entities-an interpretation ofan interpretation of

ARB No. 51ARB No. 51

35

• 10 – 15 Minute Audio Visual10 – 15 Minute Audio Visual

• 10 True / False Study Questions10 True / False Study Questions

• Easy Study SheetEasy Study Sheet

• 10 Multiple Choice Question Quiz10 Multiple Choice Question Quiz

• 1 – 3 Review Exercises1 – 3 Review Exercises

E.F.A.T.E.F.A.T.Elementary Financial Accounting TutorialElementary Financial Accounting Tutorial