Embed Size (px)

Citation preview

1 © Experian Public

2 © Experian Public

Overview

Snapshot of Experian

For the year ending 31 March 2018

* At 12 November 2018

Experian is the world’s leading global

information services company. Our roots lie in

assessing credit risk; today we do much more.

Experian is the world’s leading

global information services company

We use data to help people and organisations to assess, predict, plan

and protect themselves

We are custodians of data on over 1 billion people globally

We have a diverse and growing range of clients and geographies…

… and multiple and growing uses for our data

We are the market leader in this growing market…

… and we are securing new types of data, and finding new uses for our data

We are large, stable and cash-generative:

• £17bn market cap* / currently FTSE top 35*

• 16,500 employees / 39 countries

• FY18: $4.7bn revenue / $1.3bn Benchmark EBIT

• Highly cash generative with high cash conversion rate

• 15.7% Return on Capital Employed (ROCE)

3 © Experian Public *Please refer to preliminary results or annual financial statements for definitions of organic revenue growth and Benchmark EBIT to Operating cash flow conversion

Market-leading global information

business with strong market

positions---------------------------------------------------------------

Significant growth potential

-----------------------------------------------------------

Strong financial track record

------------------------------------------------------------

• We are the market leader, holding the

number one or two positions across our

largest markets – the USA, Brazil and the UK

• We have a diversified portfolio of

businesses across different sectors and

geographies

• Our business model is scalable, which

means we can grow the business quickly

with low incremental cost

• We drive significant synergies across our

operations by combining data sources,

integrating analytics and using technology to

secure competitive advantage

• All the above creates a high barrier to entry

• We continually invest in new product

innovation to address new market

opportunities

• We are expanding our position with

existing clients and adding new ones in our

more developed markets

• We have considerable potential to

introduce and expand our services in

emerging markets

• We are expanding our services in new

industry segments, such as US

healthcare

• The revenues we generate typically have a

recurring profile and this, coupled with

successful growth investment, has meant we

have averaged organic revenue growth* of

5% each year since we became a listed

company in 2006. Our aim is to consistently

grow organic revenue at a mid-single digit

rate

• We are a highly cash generative, low

capital intensity company. Our Benchmark

EBIT to Operating cash flow* conversion rate

has averaged 99% since demerger

• We make the best use of cash we generate,

balancing the need for organic investment in

innovation, acquisitions and returns to

shareholders through dividends and share

repurchases

Overview

The Experian investment case

4 © Experian Public

Overview

Experian business activities – our services

● Large databases

● Credit history data on >1bn people and 145m businesses

● Segmentation data on markets with 2.8bn people

● Automotive information

● 18 consumer credit bureaux

● 11 business credit bureaux

● Credit reports

● Analytical sandbox

● Advanced software and analytics

● Credit scores

● Decisioning software

● Data quality

● Fraud software ● Health

● Analytical tools ● Expert consulting

● Direct to consumer credit monitoring

● Credit comparison services / lead generation

● Identity theft protection services

● Affinity (white label) credit and identity monitoring services

Decisioning

US$1.2bn*

Consumer Services

US$0.9bn

Data

US$2.6bn*

Business-to-Business (B2B)

Business-to-Consumer (B2C)

Revenue for 31 March 2018. * Reconciled for the new business segment Business-to-Business and its sub-divisions Data and Decisioning.

5 © Experian Public

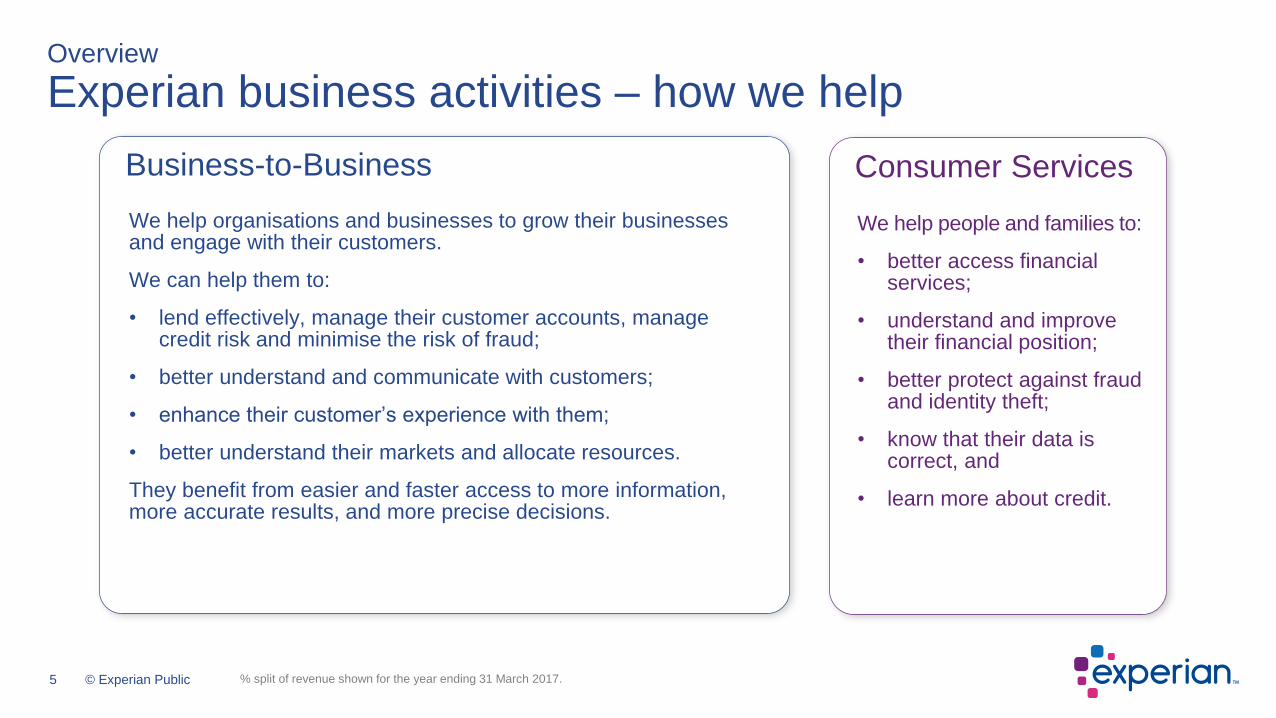

Consumer ServicesBusiness-to-Business

Overview

Experian business activities – how we help

We help organisations and businesses to grow their businesses and engage with their customers.

We can help them to:

• lend effectively, manage their customer accounts, manage credit risk and minimise the risk of fraud;

• better understand and communicate with customers;

• enhance their customer’s experience with them;

• better understand their markets and allocate resources.

They benefit from easier and faster access to more information, more accurate results, and more precise decisions.

We help people and families to:

• better access financial services;

• understand and improve their financial position;

• better protect against fraud and identity theft;

• know that their data is correct, and

• learn more about credit.

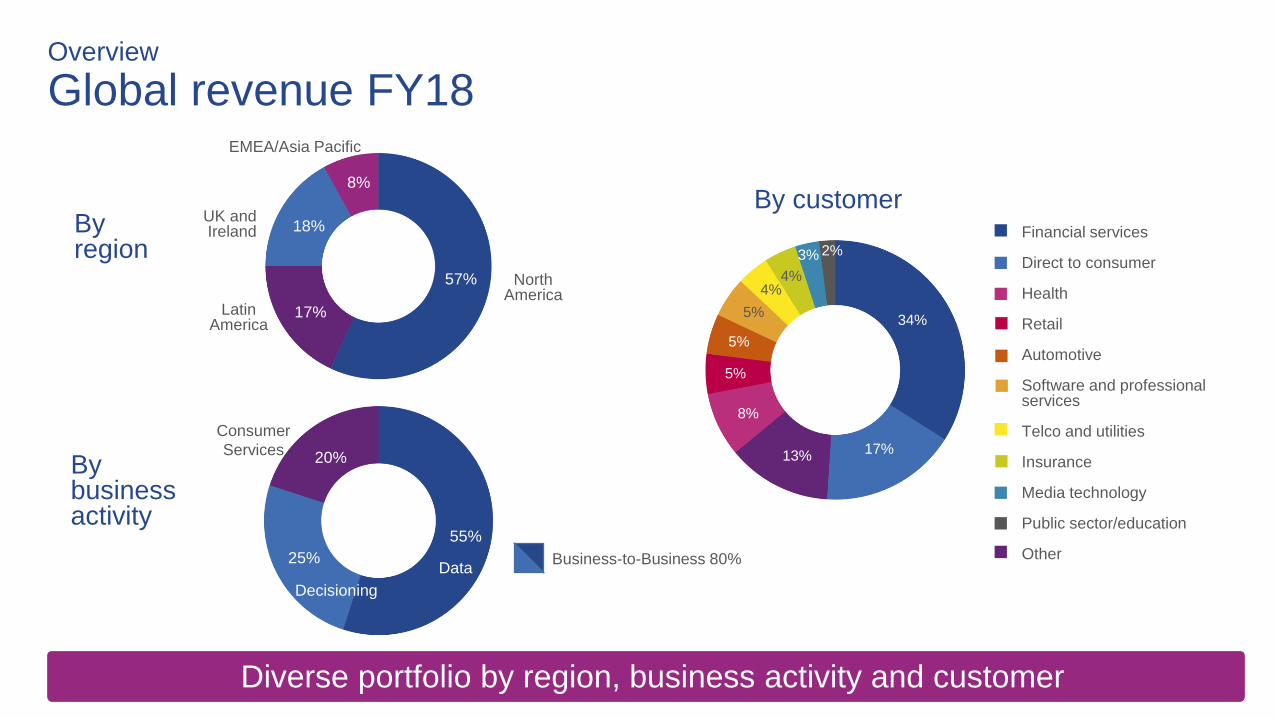

% split of revenue shown for the year ending 31 March 2017.

By customer

Overview

Global revenue FY18

Diverse portfolio by region, business activity and customer

Data

Decisioning

55%

25%

20%By business activity

EMEA/Asia Pacific

UK and Ireland

North America

Latin America

8%

18%

57%

17%

Consumer

Services

By region

Business-to-Business 80%

Financial services

Direct to consumer

Health

Retail

Automotive

Software and professionalservices

Telco and utilities

Insurance

Media technology

Public sector/education

Other

17%13%

8%

5%

5%

5%

4%

3% 2%

34%

4%

7 © Experian Public

57% 75%

82%* 83%

91%

43%

25%

18%17%

9%

4,6571

3,3622

1,9982

1,7432

9171

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

Experian Equifax TransUnion D&B FICO

North America Other regions

Overview

Market leader with unparalleled global reach and range

1 Year ended 31 March 2018

2 Year ended 31 December 2017

This analysis covers traditional competitors that are publicly listed. It does not include companies where a single division competes against Experian.

*US only.

Source: Latest full year revenue, company SEC filings

Glo

ba

l re

ve

nu

e U

S$

m

8 © Experian Public

Strategic overview

9 © Experian Public

Strategic overview

First-half financial highlights

All growth rates are at constant currency.

Organic revenue

Total revenue

Benchmark EBIT

Benchmark EPS

+8%

+9%

+10%

+12%

10 © Experian Public

Strategic overview

First-half strategic highlights

Build data depth and quality Engage more consumersAccelerate innovation

Ascend: 14* strategic clients in US, launching US mid-market, introduced in UK and EMEA

PowerCurve: major new agreements; SaaS version pending

CrossCore: additional 28 agreements signed

Text for Credit: 5 markets

Verdus (open data): engaging with clients

Alternative data:

• Clarity pipeline grows

• Adding consumer-permissioned data

Trended data

• US for mortgages

• UK introduced Nov 2018

IdentityWorks:

• 280,000 members

Free memberships: over 45m across 3 markets

• US 16m

• UK 4.7m

• Brazil over 25m

Credit marketplace agreements in Asia Pacific

* As at 31 October 2018.

11 © Experian Public

Strategic overview

Our growth drivers

Data proliferation unlocks new opportunities

Advances in technology drive demand for better decision making

Consumers seek instant and frictionless experiences

12 © Experian Public

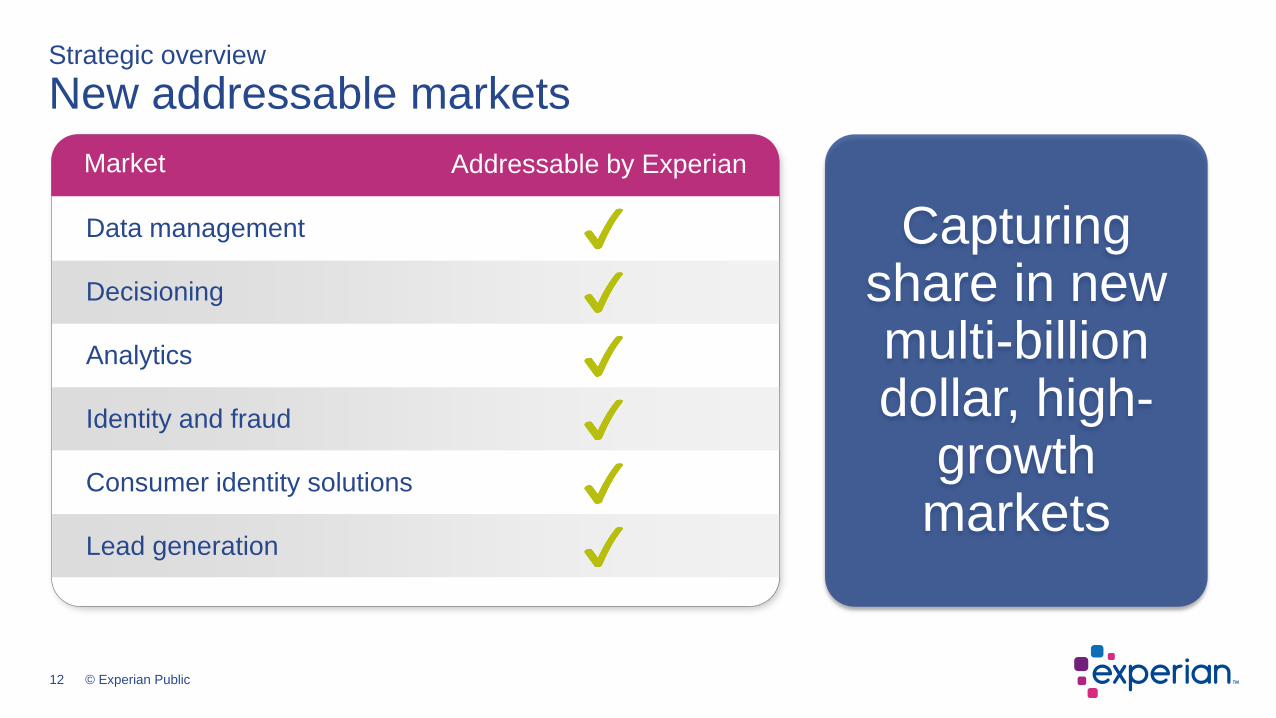

Strategic overview

New addressable markets

Lead generation

Data management

Decisioning

Analytics

Identity and fraud

Consumer identity solutions

Addressable by ExperianMarket

Capturing share in new multi-billion dollar, high-

growth markets

13 © Experian Public

Strategic overview

North America: strong momentum in B2B, +12% organic revenue growth

• New product innovation drives more of our growth

• Ascend successful initial phase

• Extended to include Clarity Services, automotive and business credit data in addition to consumer credit data

• Ascend for mid-market, launching soon

13 © Experian Public

14 © Experian Public

Strategic overview

North America: strong momentum in B2B

Winning in the marketplace with Decisioning

• Large organisations upgrading infrastructure

• PowerCurve secures major wins

• Health grows double-digit, with strong pipeline

14 © Experian Public

15 © Experian Public

Strategic overview

North America Consumer Services: +8% organic revenue growth

Identity protection

• Strategy centred on:

• Putting consumers in control

• Driving engagement

• Strong new product roadmap for H2

Good progress in identity

16 © Experian Public

Experian Financial Profile

CreditMatch

New product pipeline

Helps consumers understand their position

Enables consumers to get offers at higher approval odds

To broaden reach and increase free member base

1

2

3

Strategic overview

North America Consumer Services: lead generation grows strongly

16m free members

17 © Experian Public

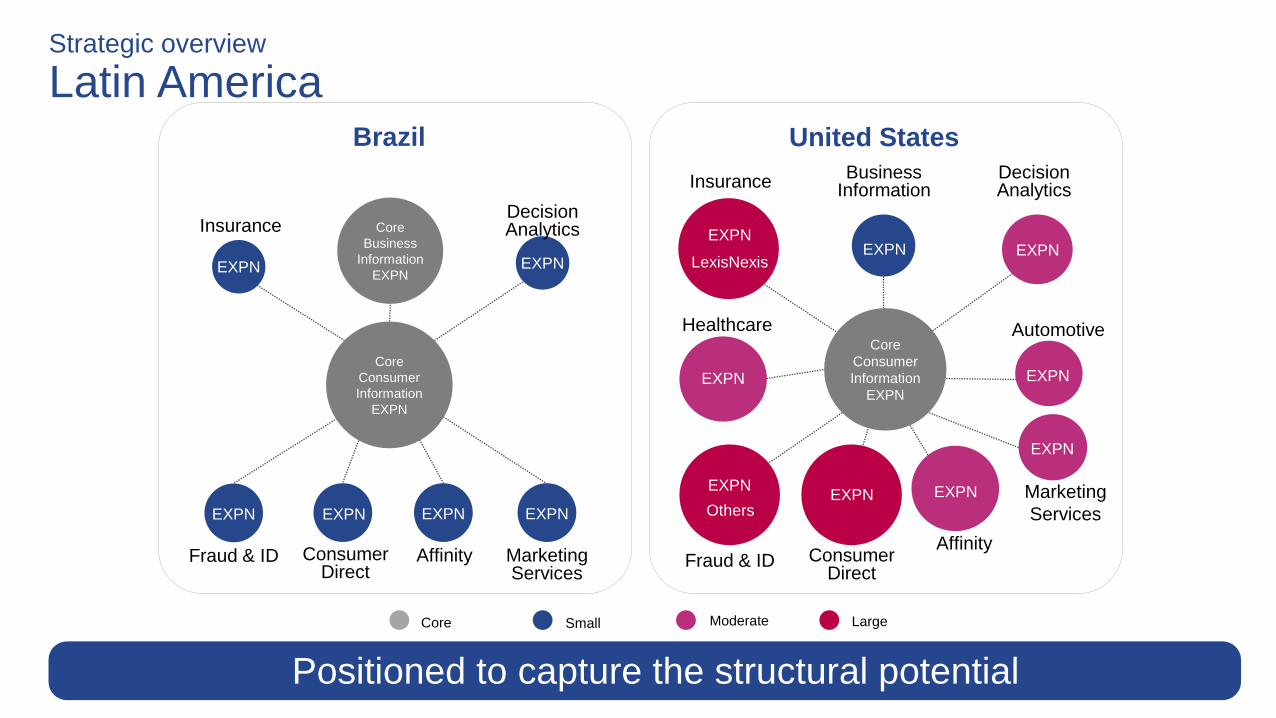

Strategic overview

Latin America: +4% organic revenue growth

• Spanish Latin America recovery

• Brazil

• Affected by political uncertainty

• Strong growth across largest clients

• Strong demand for global products

17 © Experian Public

18 © Experian Public

Strategic overview

Brazil: consumer initiative

Engage through free offers

Consulta Score Ensina Positive data

Revenue streams

Over 25m free members

AntifraudeLimpa Nome eCred

0 300 700 1,000

Serasa score range

• Free offers drive

engagement

• Consumers are

contributing valuable

data

• Products suited to

different consumer

profiles

19 © Experian Public

Others

EXPN

LexisNexis

Strategic overview

Latin America

Small Moderate LargeCore

Positioned to capture the structural potential

BusinessInformation

DecisionAnalytics

EXPN

Marketing

Services

EXPN

ConsumerDirect

Healthcare

EXPN

Automotive

Fraud & ID

EXPN

Insurance

Affinity

EXPN

Core

Consumer

Information

EXPN

EXPN

EXPN

Core

Business

Information

EXPN

DecisionAnalytics

EXPN

Insurance

EXPN

EXPN

United StatesBrazil

MarketingServices

EXPN

ConsumerDirect

EXPN

Fraud & ID

EXPN

Affinity

EXPN

Core

Consumer

Information

EXPN

20 © Experian Public

Strategic overview

UK and Ireland B2B: +5% organic revenue growth

• Big wins for traditional credit and software

• Bringing new products to market:

• Ascend

• Trended data

• Engaging clients with Verdus (open data)

20 © Experian Public

21 © Experian Public

Strategic overview

UK and Ireland Consumer Services Further sequential improvement

4.7m free members

Expand sectors to meet more needs

Create a true financial marketplace

Launch data-driven recommendations

Our vision

The one place to manage all your finances

Get your next credit card with just a single click

Auto Switch – never pay more than you need to

22 © Experian Public

Strategic overview

EMEA/Asia Pacific: +13% organic revenue growth

Bureau builds

New products: Experian One, Ascend

Leadership through PowerCurve and CrossCore

Establishing data marketplaces, e.g. C88

Customer experience

Commercial strategy

Bureau modernisationG

row

th p

illa

rsF

oun

da

tio

ns

22 © Experian Public

23 © Experian Public

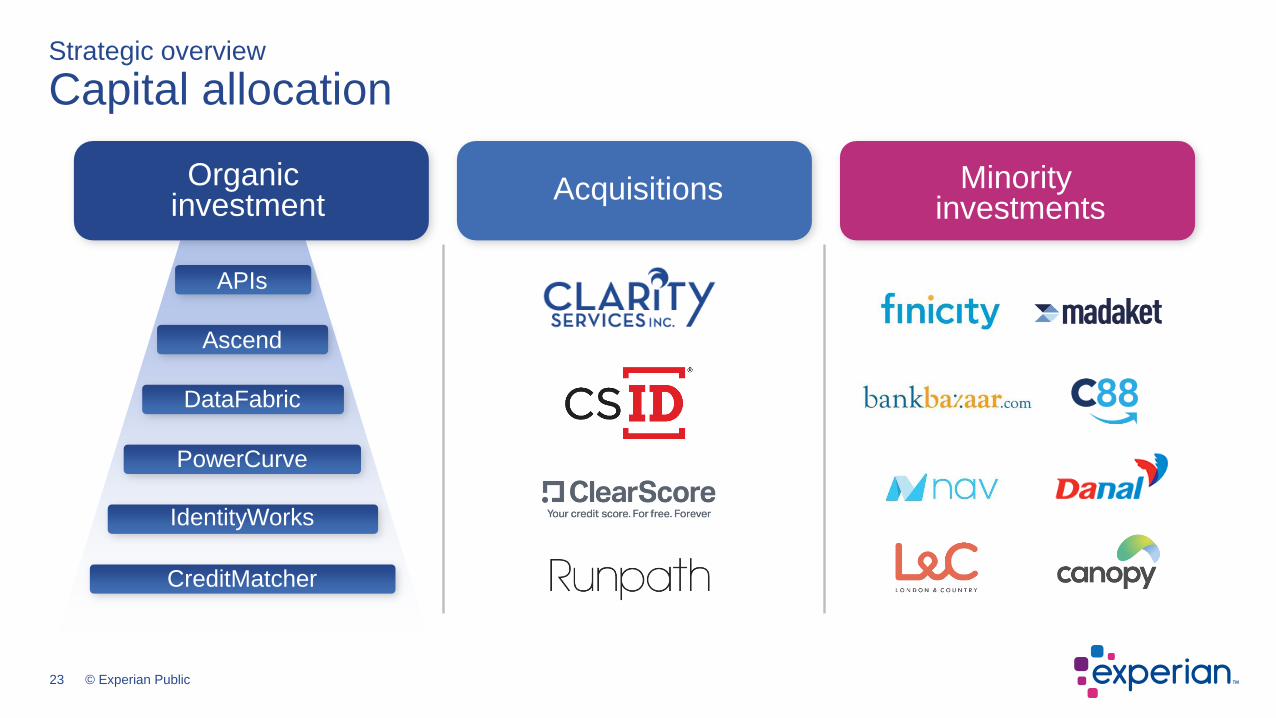

Strategic overview

Capital allocation

Ascend

PowerCurve

APIs

DataFabric

IdentityWorks

CreditMatcher

Organic investment

Acquisitions Minority investments

24 © Experian Public

Capital strategy

Our medium-term financial framework

Organic business

Mid single-digit organic growth

Operating cash flow application

Strong growth in Benchmark earnings per share

• Structural growth

• Strong cash generation

• Strong core and portfolio optionality

Organic investment Portfolio

Shareholder returns

Optimised capital allocation

25 © Experian Public

Recent performance

26 © Experian Public

Recent performance

Highlights – H1 FY19

Certain financial data have been rounded within this presentation. As a result of this rounding, the totals of data presented may vary slightly from the arithmetic totals of such data.Revenue, Benchmark EBIT growths and Benchmark EBIT margin are on an ongoing activities basis.

Margin progression

Total revenue growth

Organic revenue growth

Benchmark EBIT margin

Dividend per share growth 4%Dividend

Benchmark operating cash flow conversion 74%Operating cash flow

Benchmark earnings per share growth 8%Earnings

27.5%EBIT

7%Revenue Growth

Actualrates

Constant rates

8%

9%

12%

20 bps (10) bps

27 © Experian Public

Recent performance

Organic revenue trends

B2B defined as Credit Services, Decision Analytics and Marketing Services for FY17 and FY18.B2B defined as Data and Decisioning for FY19.

Strong B2B growth12%

10%

8%

6%

4%

2%

0%

FY17 FY18 FY19

H1 H2 H1 H2 H1

Consumer Services growing well

-10%

2%

0%

-2%

-4%

-6%

-8%

4%

6%

H1 H2 H1 H2 H1

FY18 FY19FY17

28 © Experian Public

Recent performance

Foreign exchange translation impact on EPS

FX rates FX movementsCurrencyRule of thumb full-year impact

on Benchmark EPS

3.751 ± 10%Brazilian real

(BRL)c. ± 2 US cents

1.291 ± 10%Pound sterling

(GBP)c. ± 1 US cents

1. FX rates are spot rates as at 12 November 2018.

29 © Experian Public

Recent performance

FY18 capital framework

1 Share repurchases as at 31 March 2018.

2 Funds from Operations is defined as Benchmark free cash flow plus organic capital investment (capital expenditure).

Capital summary

Organic capital investment

Share repurchaseprogramme

Dividends

Acquisitions and minority investments

Funds from Operations 2

Increase in net debt

Other

Capital allocation

• Organic innovation investment

• Acquisitions in the year included Clarity and Runpath

• FY18 shareholder returns:

• Dividend growth of 8%

• US$566m1 net share repurchases completed during FY18

• Return on Capital Employed (ROCE) of 15.7%, up 0.2% from prior year

• Expect to make up to $400m of net share repurchases

US$m

0

200

400

600

800

1,000

1,200

1,400

1,600

Cashgenerated

Uses ofcash

30 © Experian Public

Summary and outlook

• Good financial and strategic progress in the first half

• Strong B2B performance

• Good contribution from Consumer Services

• Outlook for FY19; at constant currency

• Strong revenue growth

• EBIT growth at or above rate of revenue growth

• Strong progress in Benchmark EPS

• Continued focus on investments to drive future value

creation

31 © Experian Public

This slide has been left intentionally blank

32 © Experian Public

Appendix

33 © Experian Public

Appendix

Modelling considerations for FY19

Acquisitions• FY18 acquisitions performing well and are now all included in organic

numbers from 1 October 2018

Foreign exchange• Based on recent rates, expect foreign exchange to be c.500bps headwind to

EBIT versus 400bps expected at Q1

Net interest • Expected to be c.US$110m; inclusive of share repurchase programme

Tax • Benchmark tax rate to be c. 26%

Share repurchases • Full year WANOS1 expected to be in the region of 903m shares

Capital expenditure • Capital expenditure of c.9% of revenue

1. Weighted average number of shares.

34 © Experian Public

Appendix

H1 revenue walkthrough

1 At actual foreign exchange rates.

+12% +4%

+5% +13%

+5%

FY19 H1revenue before

FX and acquisitions

FY19 H1 reported revenue

from ongoing activities

North

America B2B

Foreign

exchange

UK and

Ireland B2B

EMEA/

Asia PacificLatin

America

Acquisitions

FY18 H1revenue from

ongoing activities

Consumer

Services

+7%Total

revenue growth1

+9%Total

revenue growth

+8% Organic revenue growth

+9%B2B organic revenue growth

US$2,204m

US$2,364m

35 © Experian Public

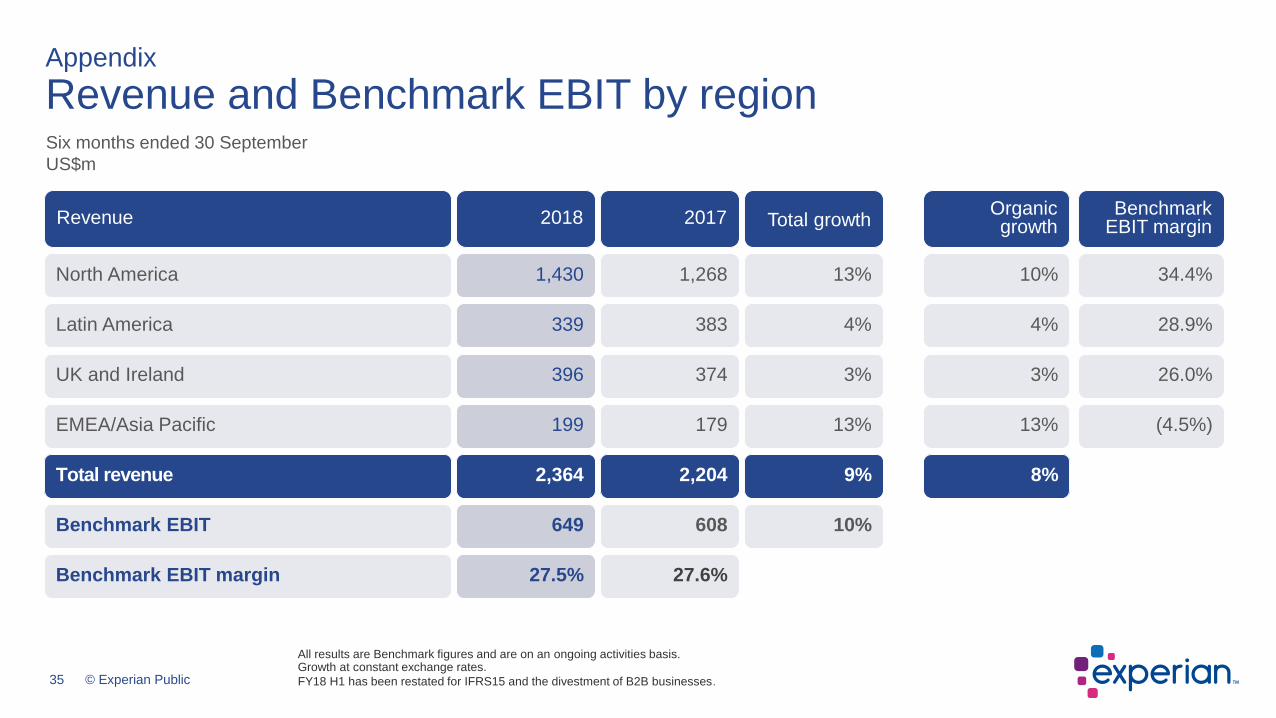

Appendix

Revenue and Benchmark EBIT by region

All results are Benchmark figures and are on an ongoing activities basis.Growth at constant exchange rates.

FY18 H1 has been restated for IFRS15 and the divestment of B2B businesses.

Six months ended 30 September

US$m

Revenue

North America

Latin America

UK and Ireland

EMEA/Asia Pacific

Total revenue

Benchmark EBIT

Benchmark EBIT margin

Organic growth

Benchmark EBIT margin

10% 34.4%

4% 28.9%

3% 26.0%

13% (4.5%)

8%

Total growth 20172018

13%1,2681,430

4%383339

3%374396

13%179199

9%2,2042,364

10%608649

27.6%27.5%

36 © Experian Public

Total growth

301Decisioning

Six months ended 30 September

US$m

Appendix

North America

All results are Benchmark figures and are on an ongoing activities basis.Growth at constant exchange rates.

FY18 H1 has been restated for IFRS15 and the divestment of B2B businesses.

2018

1,027

403

1,430

492

34.4%

Business-to-Business

Consumer Services

726Data

274

2017

893

375

1,268

411

32.4%

619

Total revenue

Benchmark EBIT

Benchmark EBIT margin

10%

15%

8%

13%

20%

17%

Organic growth

10%

12%

8%

10%

12%

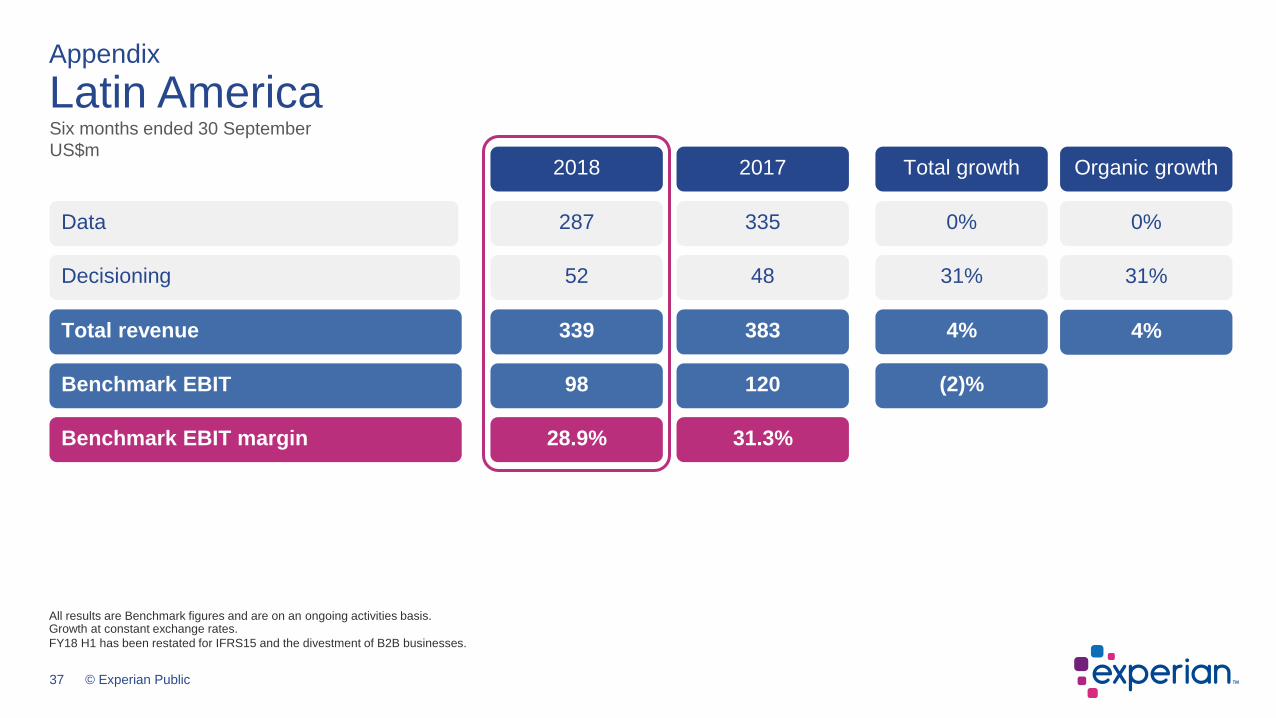

37 © Experian Public

339

98

28.9%

383

120

31.3%

Total revenue

Benchmark EBIT

Benchmark EBIT margin

4%

(2)%

4%

52Decisioning

Six months ended 30 September

US$m

Appendix

Latin America

287Data

48

335

31%

0%

31%

0%

All results are Benchmark figures and are on an ongoing activities basis.Growth at constant exchange rates.

FY18 H1 has been restated for IFRS15 and the divestment of B2B businesses.

Total growth2018 2017 Organic growth

38 © Experian Public

129Decisioning

Six months ended 30 September

US$m

Appendix

UK and Ireland

313

83

396

103

26.0%

Business-to-Business

Consumer Services

184Data

115

288

86

374

116

31.0%

173

Total revenue

Benchmark EBIT

Benchmark EBIT margin

9%

6%

(6)%

3%

(14)%

4%

9%

5%

(6)%

3%

3%

Total growth2018 2017 Organic growth

All results are Benchmark figures and are on an ongoing activities basis.Growth at constant exchange rates.

FY18 H1 has been restated for IFRS15 and the divestment of B2B businesses.

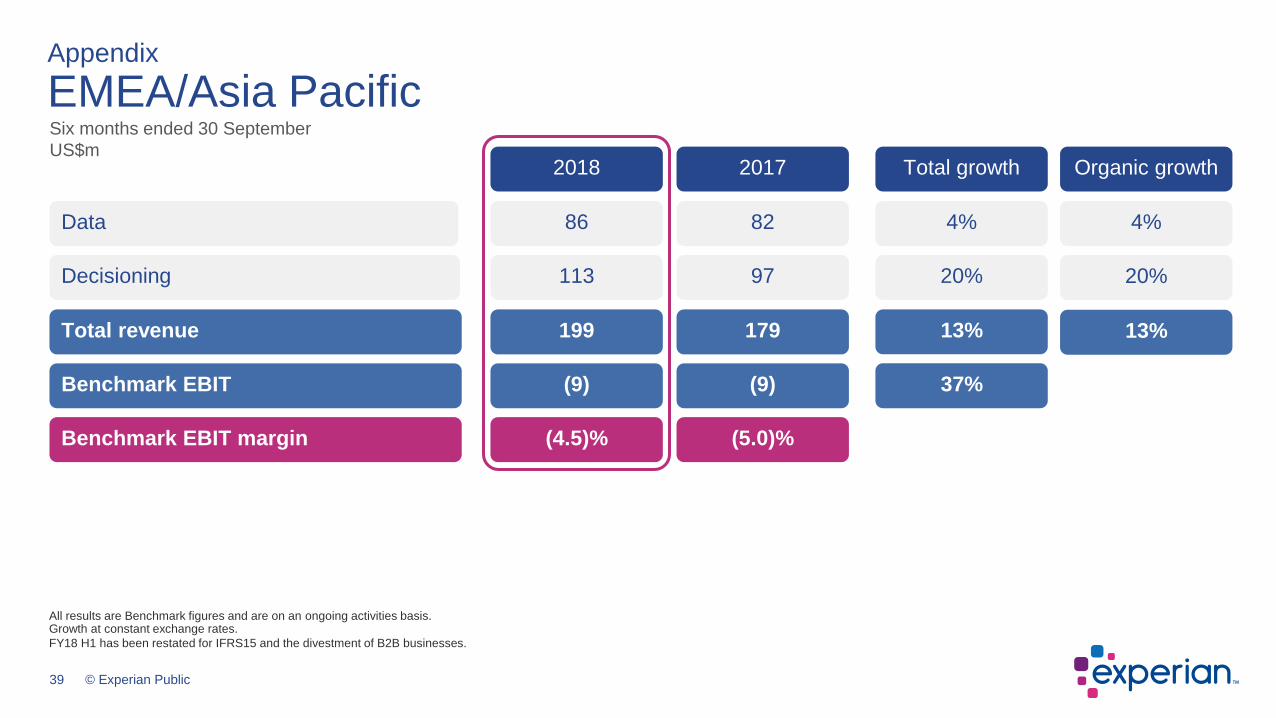

39 © Experian Public

199

(9)

(4.5)%

179

(9)

(5.0)%

Total revenue

Benchmark EBIT

Benchmark EBIT margin

13%

37%

13%

113Decisioning

Six months ended 30 September

US$m

Appendix

EMEA/Asia Pacific

86Data

97

82

20%

4%

20%

4%

Total growth2018 2017 Organic growth

All results are Benchmark figures and are on an ongoing activities basis.Growth at constant exchange rates.

FY18 H1 has been restated for IFRS15 and the divestment of B2B businesses.

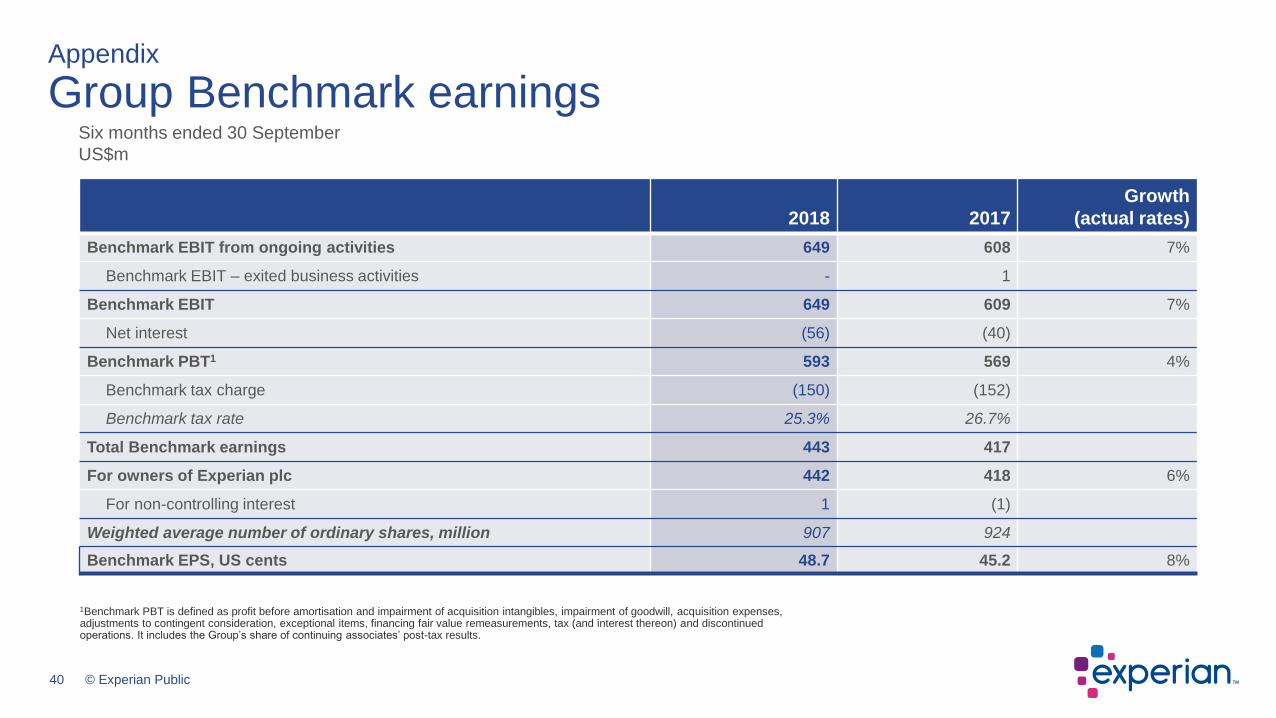

40 © Experian Public

2018 2017

Growth

(actual rates)

Benchmark EBIT from ongoing activities 649 608 7%

Benchmark EBIT – exited business activities - 1

Benchmark EBIT 649 609 7%

Net interest (56) (40)

Benchmark PBT1 593 569 4%

Benchmark tax charge (150) (152)

Benchmark tax rate 25.3% 26.7%

Total Benchmark earnings 443 417

For owners of Experian plc 442 418 6%

For non-controlling interest 1 (1)

Weighted average number of ordinary shares, million 907 924

Benchmark EPS, US cents 48.7 45.2 8%

1Benchmark PBT is defined as profit before amortisation and impairment of acquisition intangibles, impairment of goodwill, acquisition expenses, adjustments to contingent consideration, exceptional items, financing fair value remeasurements, tax (and interest thereon) and discontinued operations. It includes the Group’s share of continuing associates’ post-tax results.

Six months ended 30 September

US$m

Appendix

Group Benchmark earnings

41 © Experian Public

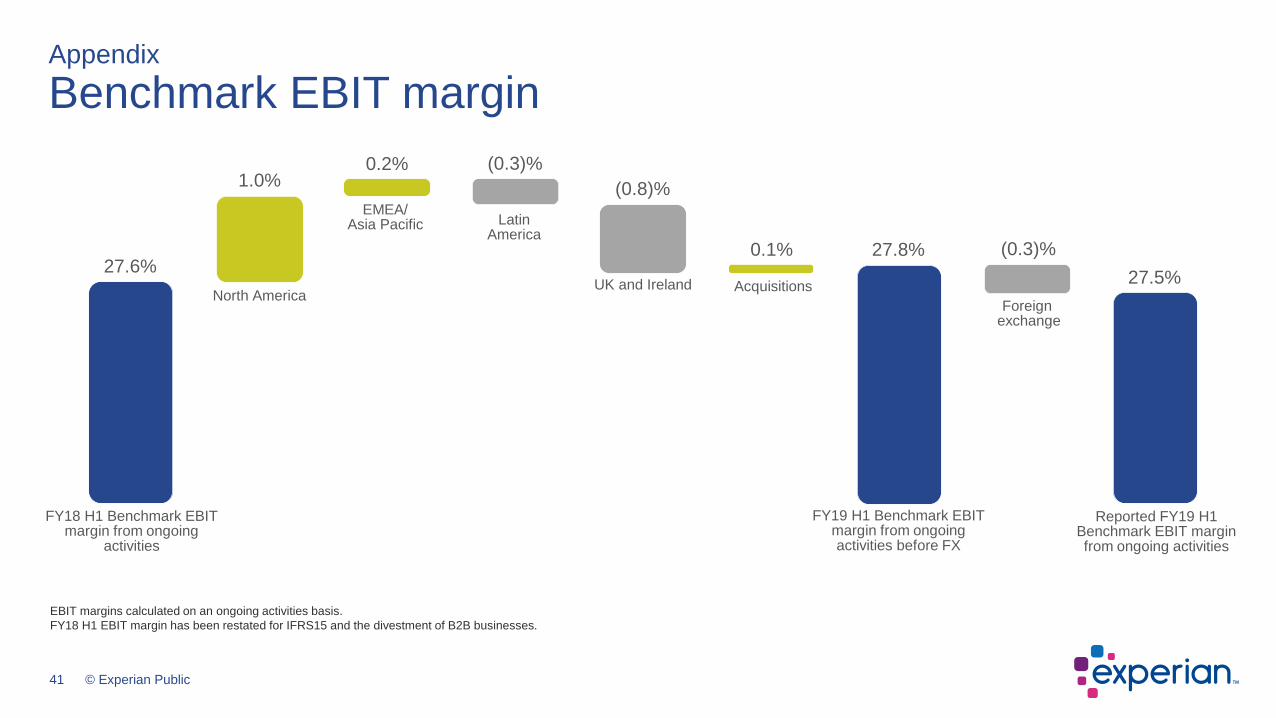

Appendix

Benchmark EBIT margin

EBIT margins calculated on an ongoing activities basis.

FY18 H1 EBIT margin has been restated for IFRS15 and the divestment of B2B businesses.

FY18 H1 Benchmark EBIT margin from ongoing

activities

FY19 H1 Benchmark EBIT margin from ongoing activities before FX

Reported FY19 H1 Benchmark EBIT margin from ongoing activities

Foreignexchange

EMEA/Asia Pacific

UK and Ireland

Latin America

North America

27.6%

1.0% 0.2% (0.3)%

(0.8)%

27.8% (0.3)%

27.5% Acquisitions

0.1%

42 © Experian Public

+8%EPS

growth

+12%EPS

growth

+10%Constant currency

growth

Appendix

Benchmark earnings per share (EPS)

FY19 H1 reported

Benchmark EPSFY19 H1

Benchmark EPS

before FX

Interest Tax & Minority

Interest

Share

repurchases Foreign

exchange

US45.2c

FY19 H1

Benchmark EBIT

growth

from continuing

operations

US48.7c

FY18 H1

Benchmark EPS

43 © Experian Public

Six months ended 30 September 2018

Appendix

Benchmark cash flow performance

US$m

Benchmark EBIT

Benchmark operating cash

flow

Working capital and

other

Net capital expenditure

Amortisation and depreciation

Benchmark free cash flow

Net interest paid

Tax paid on operating activities

649 (181)

159 (149)

478(55)

(84)

339

74%conversion of Benchmark

EBIT into Benchmark operating cash flow

77%conversion of Benchmark

earnings into free cash flow

44 © Experian Public

Appendix

Net debt reconciliationUS$m

Net debt at

1 April 2018

Net debt /

Benchmark EBITDA

2.1x

Net share

purchases

Equity

dividends paidBenchmark

operating

cash flow

Acquisitions

and minority

investments

Net debt at

30 September 2018

Net debt /

Benchmark EBITDA

2.2x

FX and other

3,408

30

(478)

107284

139

13

3,503Interest and

tax paid

45 © Experian Public

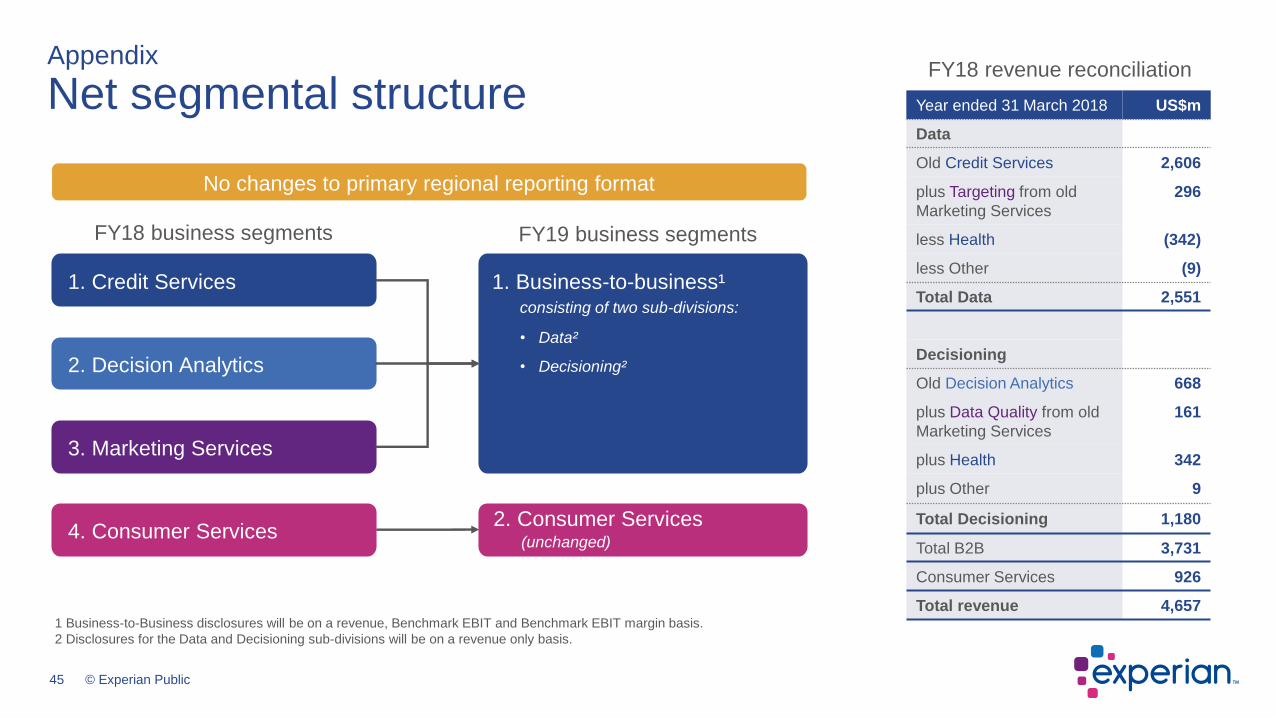

FY18 revenue reconciliation

Year ended 31 March 2018 US$m

Data

Old Credit Services 2,606

plus Targeting from old

Marketing Services

296

less Health (342)

less Other (9)

Total Data 2,551

Decisioning

Old Decision Analytics 668

plus Data Quality from old

Marketing Services

161

plus Health 342

plus Other 9

Total Decisioning 1,180

Total B2B 3,731

Consumer Services 926

Total revenue 4,6571 Business-to-Business disclosures will be on a revenue, Benchmark EBIT and Benchmark EBIT margin basis.

2 Disclosures for the Data and Decisioning sub-divisions will be on a revenue only basis.

FY18 business segments FY19 business segments

1. Credit Services

2. Decision Analytics

3. Marketing Services

4. Consumer Services

1. Business-to-business¹consisting of two sub-divisions:

• Data²

• Decisioning²

2. Consumer Services(unchanged)

No changes to primary regional reporting format

Appendix

Net segmental structure

46 © Experian Public

Appendix

Experian American Depositary Receipt (ADR) programme

For ADR shareholder enquiries,

please contact:

Shareholder Relations

BNY Mellon Shareowner Services

PO Box 505000

Louisville, KY 40233-5000

United States

T: + 1 201 680 6825

(From the US: 1-888-BNY-ADRS, toll free)

W: www.mybnymdr.com

Experian ADR shares trade on the

OTCQX under the following

information:

Symbol EXPGY

CUSIP 30215C101

Ratio 1 ADR : 1 ORD

Country United Kingdom

Effective Date October 11, 2006

Underlying SEDOL B19NLV4

Underlying ISIN GB00B19NLV48

U.S. ISIN US30215C1018

Depositary BNY Mellon

47 © Experian Public

Appendix

Contacts

Experian

Tel: +44 (0)203 042 4200

Website: www.experianplc.com

Email: [email protected]

Nadia Ridout-Jamieson Peg Smith

Chief Communications Officer Executive Vice-President

Email: [email protected] Email: [email protected]

Sarah Schibli Adam Rachlin

Investor Relations and Communications Manager Financial Reporting Manager

Email: [email protected] Email: [email protected]

Appendix

Contacts

48 © Experian Public

17 January 2019 Trading update, third quarter FY19

15 May 2019 Preliminary announcement FY19

16 July 2019 Trading update, first quarter FY20

24 July 2019 Annual General Meeting

Appendix

Event calendar

49 © Experian Public

• This presentation is being made only to, and is only directed at, persons to whom this presentation may lawfully be communicated(“relevant persons”). Any person who is not a relevant person should not act or rely on this presentation or any of its contents.

• Information in this presentation relating to the price at which relevant investments have been bought or sold in the past or the yield on such investments cannot be relied upon as a guide to the future performance of such investments.

• This presentation does not constitute or form part of, and should not be construed as, an offering of securities or otherwise constitute an invitation, inducement or recommendation to any person to underwrite, subscribe for or otherwise acquire securities in anycompany within the Experian group (the “Group”).

• Certain statements made in this presentation are forward looking statements. Such statements are based on current expectations and are subject to a number of risks and uncertainties that could cause actual events or results to differ materially from any expected future events or results expressed or implied in these forward-looking statements. Forward-looking statements speak only as of the date of this presentation.

• This presentation contains certain non-GAAP financial information. The Group’s management believes that these measures provide valuable additional information in understanding the performance of the Group or the Group’s businesses because they provide measures used by the Group to assess performance. Although these measures are important in the management of the business, they should not be viewed as replacements for, but rather as complementary to, the GAAP measures.

Appendix

Disclaimer

![manual tecnico factoringcampanha.cadastropositivo.com.br/relato/download/manual_tecnico... · 7 [Digite texto] [Digite texto] [Digite texto] LAYOUT SIMPLIFICADO SERASA EXPERIAN O](https://img.dokumen.tips/doc/110x75/5bf5d2cc09d3f279228c13b3/manual-tecnico-7-digite-texto-digite-texto-digite-texto-layout-simplificado.jpg)

![[BPM DAY RJ 2012] SERASA EXPERIAN – Desdobramento da estratégia em indicadores de gestão](https://img.dokumen.tips/doc/110x75/58f35b061a28abf1068b4577/bpm-day-rj-2012-serasa-experian-desdobramento-da-estrategia-em-indicadores.jpg)