Embed Size (px)

Citation preview

SMEs and Public Equity Financing: A New Dataset of SME

Boards in Emerging-Market and Developing Economies

JohnSchellhaseandJimWoodsome

August2017

IntroductionInrecentyears,anumberofstockexchangesinemerging-marketanddevelopingeconomieshave

establisheddedicatedmarketsegmentsforsmallandmedium-sizedenterprises(SMEs).Themain

purposeoftheseSMEboards,astheyareoftencalled,istoexpandaccesstoequityfinancefor

relativelysmallbutgrowingfirmswiththepotential,asagroup,tosignificantlycontributetoeconomic

growthandemployment.Insomecases,SMEboardsalsoserveasfeederexchanges,incubatingfirms

forlatergraduationtoastockexchange’smainboard.Today,therearound30dedicatedSMEboardsin

emerging-marketanddevelopingeconomies,themajorityofwhichhavebeenestablishedinthelast

decadeorso.

Duetotherolethesefirmscanplayincreatingjobsanddiversifyingeconomies,improvingaccessto

financeforSMEsisalong-standingpolicygoalindevelopedanddevelopingcountriesalike.Asbanks

havecurbedtheirlendingtoSMEsinthewakeoftheglobalfinancialcrisis,policymakersandindustry

bodiesarenowincreasinglyemphasizingnon-bankfinancingalternativesforSMEs.Publicequity

financingisoneoptionthatmaybesuitableforfast-growingSMEswiththecapacitytomeetthelisting

requirements.SMEboardsmaycontributetoexpandingfinancialaccessforSMEsbothdirectly,by

facilitatingaccesstopublicequityfinancing,andindirectly,byincentivizinglistingfirmstoimprovetheir

financialreportingandcorporategovernancepractices,whichmay,inturn,makethemmoreappealing

tocredit-basedlenders.

WhatfollowsisabriefstocktakingofSMEboardsinemerging-marketanddevelopingcountries.The

analysisisbasedonauniquedatasetcreatedjointlybytheMilkenInstituteCenterforFinancialMarkets

andtheWorldFederationofExchanges.Thedatasetcovers26SMEboardsovertheperiod2002-2015.

2

Asfarasweknow,thiswillbethefirsttimethiskindoftime-series,compositedatasetonmultiple

indicatorsforSMEboardshasbeenpublished.Below,weexaminewhethertheseSMEboardshave

managedtomaintainorgrowtheirlistingsovertime,howmuchcapitallistedfirmshaveraised,and

howcommonitisforfirmstodelist.Additionally,weofferaninitialassessmentofhowwellthese

boardshaveperformedasincubatorsforgraduatingfirmstoseniormarkets.Weexpectthatthedata

presentedintheappendixattheendofthispaperwillbeofinterestandofusetopolicymakersand

researcherswhowanttofurtherinvestigateandevaluatetheroleofSMEboardsinexpandingaccessto

capital.

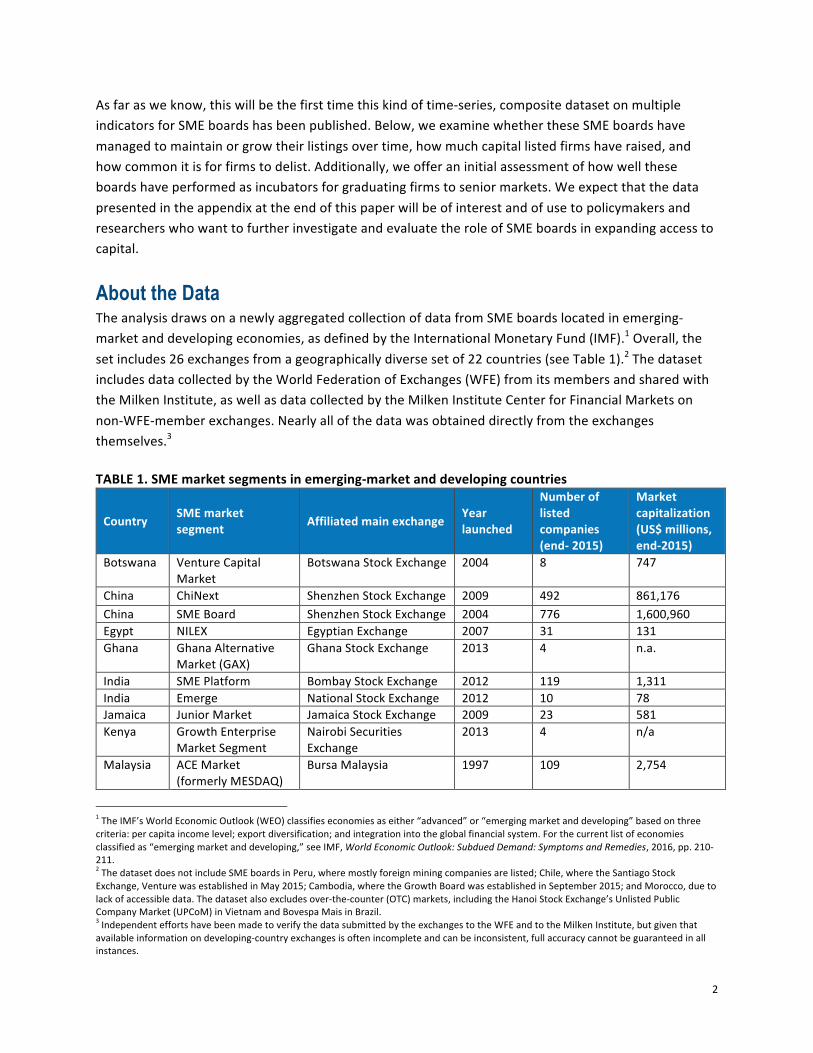

About the DataTheanalysisdrawsonanewlyaggregatedcollectionofdatafromSMEboardslocatedinemerging-

marketanddevelopingeconomies,asdefinedbytheInternationalMonetaryFund(IMF).1Overall,the

setincludes26exchangesfromageographicallydiversesetof22countries(seeTable1).2Thedataset

includesdatacollectedbytheWorldFederationofExchanges(WFE)fromitsmembersandsharedwith

theMilkenInstitute,aswellasdatacollectedbytheMilkenInstituteCenterforFinancialMarketson

non-WFE-memberexchanges.Nearlyallofthedatawasobtaineddirectlyfromtheexchanges

themselves.3

TABLE1.SMEmarketsegmentsinemerging-marketanddevelopingcountries

Country SMEmarketsegment Affiliatedmainexchange Year

launched

Numberoflistedcompanies(end-2015)

Marketcapitalization(US$millions,end-2015)

Botswana VentureCapital

Market

BotswanaStockExchange 2004 8 747

China ChiNext ShenzhenStockExchange 2009 492 861,176

China SMEBoard ShenzhenStockExchange 2004 776 1,600,960

Egypt NILEX EgyptianExchange 2007 31 131

Ghana GhanaAlternative

Market(GAX)

GhanaStockExchange 2013 4 n.a.

India SMEPlatform BombayStockExchange 2012 119 1,311

India Emerge NationalStockExchange 2012 10 78

Jamaica JuniorMarket JamaicaStockExchange 2009 23 581

Kenya GrowthEnterprise

MarketSegment

NairobiSecurities

Exchange

2013 4 n/a

Malaysia ACEMarket

(formerlyMESDAQ)

BursaMalaysia 1997 109 2,754

1TheIMF’sWorldEconomicOutlook(WEO)classifieseconomiesaseither“advanced”or“emergingmarketanddeveloping”basedonthree

criteria:percapitaincomelevel;exportdiversification;andintegrationintotheglobalfinancialsystem.Forthecurrentlistofeconomies

classifiedas“emergingmarketanddeveloping,”seeIMF,WorldEconomicOutlook:SubduedDemand:SymptomsandRemedies,2016,pp.210-211.2ThedatasetdoesnotincludeSMEboardsinPeru,wheremostlyforeignminingcompaniesarelisted;Chile,wheretheSantiagoStock

Exchange,VenturewasestablishedinMay2015;Cambodia,wheretheGrowthBoardwasestablishedinSeptember2015;andMorocco,dueto

lackofaccessibledata.Thedatasetalsoexcludesover-the-counter(OTC)markets,includingtheHanoiStockExchange’sUnlistedPublic

CompanyMarket(UPCoM)inVietnamandBovespaMaisinBrazil.3IndependenteffortshavebeenmadetoverifythedatasubmittedbytheexchangestotheWFEandtotheMilkenInstitute,butgiventhat

availableinformationondeveloping-countryexchangesisoftenincompleteandcanbeinconsistent,fullaccuracycannotbeguaranteedinall

instances.

3

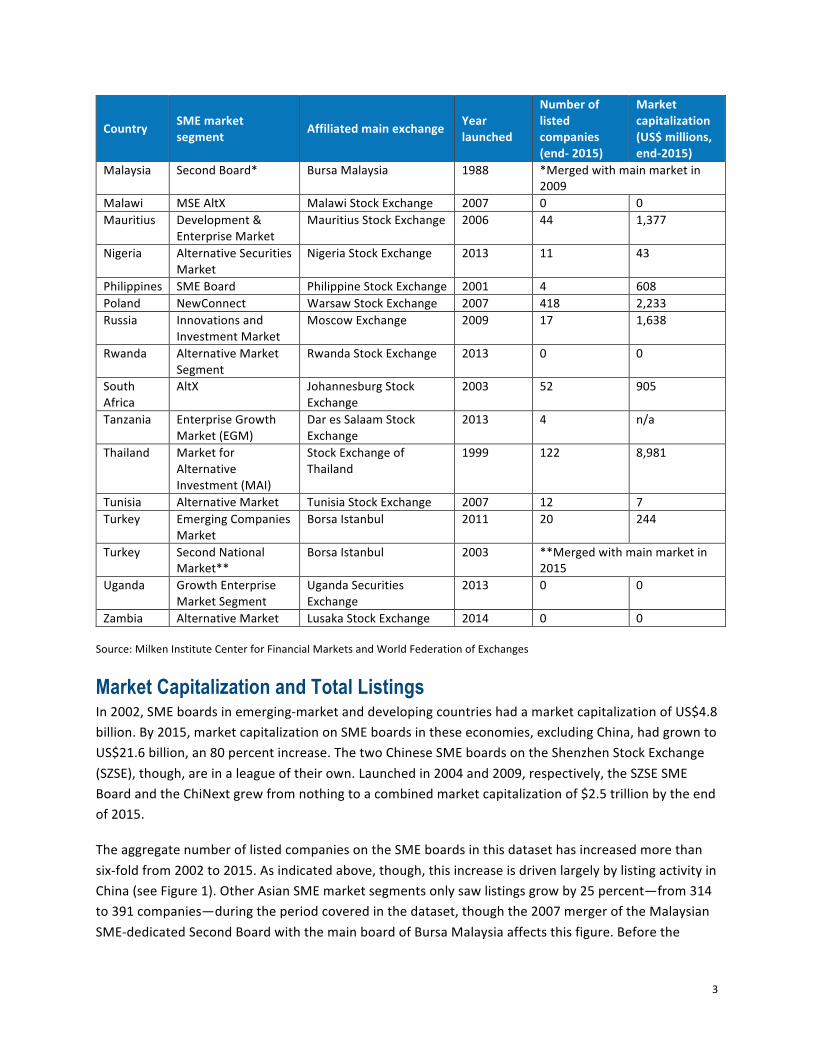

Country SMEmarketsegment Affiliatedmainexchange Year

launched

Numberoflistedcompanies(end-2015)

Marketcapitalization(US$millions,end-2015)

Malaysia SecondBoard* BursaMalaysia 1988

*Mergedwithmainmarketin

2009

Malawi MSEAltX MalawiStockExchange 2007 0 0

Mauritius Development&

EnterpriseMarket

MauritiusStockExchange 2006 44 1,377

Nigeria AlternativeSecurities

Market

NigeriaStockExchange 2013 11 43

Philippines SMEBoard PhilippineStockExchange 2001 4 608

Poland NewConnect WarsawStockExchange 2007 418 2,233

Russia Innovationsand

InvestmentMarket

MoscowExchange 2009 17 1,638

Rwanda AlternativeMarket

Segment

RwandaStockExchange 2013 0 0

South

Africa

AltX JohannesburgStock

Exchange

2003 52 905

Tanzania EnterpriseGrowth

Market(EGM)

DaresSalaamStock

Exchange

2013 4 n/a

Thailand Marketfor

Alternative

Investment(MAI)

StockExchangeof

Thailand

1999 122 8,981

Tunisia AlternativeMarket TunisiaStockExchange 2007 12 7

Turkey EmergingCompanies

Market

BorsaIstanbul 2011 20 244

Turkey SecondNational

Market**

BorsaIstanbul 2003

**Mergedwithmainmarketin

2015

Uganda GrowthEnterprise

MarketSegment

UgandaSecurities

Exchange

2013 0 0

Zambia AlternativeMarket LusakaStockExchange 2014 0 0

Source:MilkenInstituteCenterforFinancialMarketsandWorldFederationofExchanges

Market Capitalization and Total ListingsIn2002,SMEboardsinemerging-marketanddevelopingcountrieshadamarketcapitalizationofUS$4.8

billion.By2015,marketcapitalizationonSMEboardsintheseeconomies,excludingChina,hadgrownto

US$21.6billion,an80percentincrease.ThetwoChineseSMEboardsontheShenzhenStockExchange

(SZSE),though,areinaleagueoftheirown.Launchedin2004and2009,respectively,theSZSESME

BoardandtheChiNextgrewfromnothingtoacombinedmarketcapitalizationof$2.5trillionbytheend

of2015.

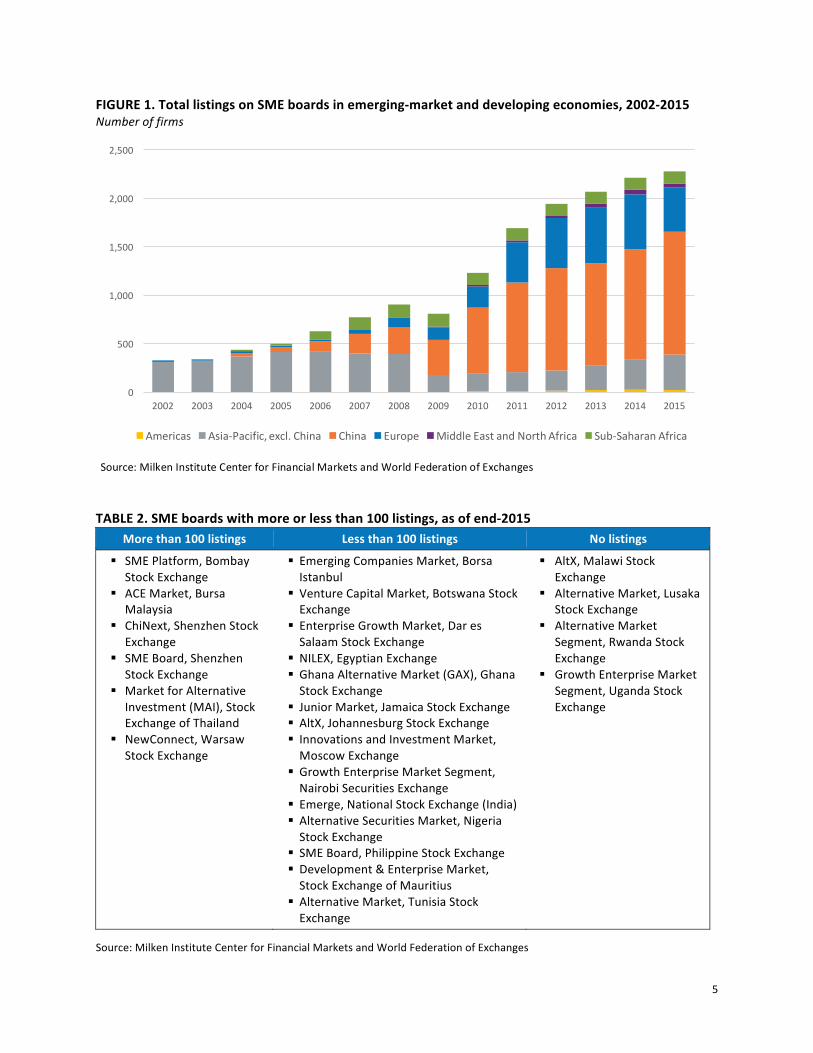

TheaggregatenumberoflistedcompaniesontheSMEboardsinthisdatasethasincreasedmorethan

six-foldfrom2002to2015.Asindicatedabove,though,thisincreaseisdrivenlargelybylistingactivityin

China(seeFigure1).OtherAsianSMEmarketsegmentsonlysawlistingsgrowby25percent—from314

to391companies—duringtheperiodcoveredinthedataset,thoughthe2007mergeroftheMalaysian

SME-dedicatedSecondBoardwiththemainboardofBursaMalaysiaaffectsthisfigure.Beforethe

4

launchoftheAltXinSouthAfricain2003,therewerenoSMEboardsinSub-SaharanAfrica.Bytheend

of2015,though,therewere127listingsacrosssevenactiveSMEboardsinthisregion.4

Fourexchangesinthedataset—mostofthemnewer—didnotreportasinglelistingasofend-2015.

TheseincludedtheMalawiStockExchange’sAltX(foundedin2007),theRwandaStockExchange’s

AlternativeMarketSegment(foundedin2013),theUgandaSecuritiesExchangesGrowthEnterprise

MarketSegment(foundedin2013),andtheLusakaStockExchange’sAlternativeMarket(foundedin

2014).AddressingthelackoflistingsinRwanda,theRwandaCapitalMarketsAuthoritynotedthatmost

SMEsinthecountrywerefamily-runand“arenotusedtohavingoutsidersexaminetheirbusinesses.”5

Similarly,theCEOoftheMalawiStockExchangeattributedthelackoflistings“toissuesofcontrolof

theirentities...[and]issuesofcorporategovernance.”6

Onereasonthenumberoflistedcompaniesisofinterestisthatitmaygivesomeindicationofthe

sustainabilityofanSMEboard’sbusinessmodel.Inastudyofcapital-marketfinancingforSMEsacross

developedanddevelopingcountries,Peterhoff,Romeo,andCalvey(2014)estimatedthat,basedonthe

costsofsettingupSMEplatforms,makingSMEmarketsegmentssustainablerequireshavingacritical

massof100-150listingsinplaceafterfiveyears.7Overall,onlysix—lessthanathird—oftheexamined

SMEboardsnowexceed100listings(seeTable2).However,manySMEboardsaresubsidizedbythe

mainexchange;insuchcases,itmaynotbenecessaryfortheseboardstobecomefinanciallyself-

sufficient.SMEboardsnecessarilyadopttheirbusinessmodelstosuitthelocalcontextandthe

particularSMEpopulationtheyserve,though,inmanysmallermarkets,eventhemainboardsmay

struggletoattractaregularstreamofnewlistings.

4ElevencountriesinSub-SaharanAfricahaveestablishedSMEboards,butfouroftheseboardshavenotlistedasinglecompany.5Gasore,“SMEsShyAwayfromListingontheBourse,”TheNewTimes,April17,20146Chinamulungu,“MSEUrgesSMEstoListonAltXMarket,”TheNation,September17,2016.7Peterhoff,Romeo,andCalvey,“TowardsBetterCapitalMarketsSolutionsforSMEFinancing,”OliverWyman,2014,p.6

5

FIGURE1.TotallistingsonSMEboardsinemerging-marketanddevelopingeconomies,2002-2015Numberoffirms

TABLE2.SMEboardswithmoreorlessthan100listings,asofend-2015Morethan100listings Lessthan100listings Nolistings

§ SMEPlatform,Bombay

StockExchange

§ ACEMarket,Bursa

Malaysia

§ ChiNext,ShenzhenStockExchange

§ SMEBoard,Shenzhen

StockExchange

§ MarketforAlternative

Investment(MAI),Stock

ExchangeofThailand

§ NewConnect,Warsaw

StockExchange

§ EmergingCompaniesMarket,Borsa

Istanbul

§ VentureCapitalMarket,BotswanaStock

Exchange

§ EnterpriseGrowthMarket,Dares

SalaamStockExchange

§ NILEX,EgyptianExchange§ GhanaAlternativeMarket(GAX),Ghana

StockExchange

§ JuniorMarket,JamaicaStockExchange

§ AltX,JohannesburgStockExchange§ InnovationsandInvestmentMarket,

MoscowExchange

§ GrowthEnterpriseMarketSegment,

NairobiSecuritiesExchange

§ Emerge,NationalStockExchange(India)

§ AlternativeSecuritiesMarket,Nigeria

StockExchange

§ SMEBoard,PhilippineStockExchange

§ Development&EnterpriseMarket,

StockExchangeofMauritius

§ AlternativeMarket,TunisiaStock

Exchange

§ AltX,MalawiStock

Exchange

§ AlternativeMarket,Lusaka

StockExchange

§ AlternativeMarket

Segment,RwandaStock

Exchange

§ GrowthEnterpriseMarket

Segment,UgandaStock

Exchange

Source:MilkenInstituteCenterforFinancialMarketsandWorldFederationofExchanges

0

500

1,000

1,500

2,000

2,500

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Americas Asia-Pacific,excl.China China Europe MiddleEastandNorthAfrica Sub-SaharanAfrica

Source:MilkenInstituteCenterforFinancialMarketsandWorldFederationofExchanges

6

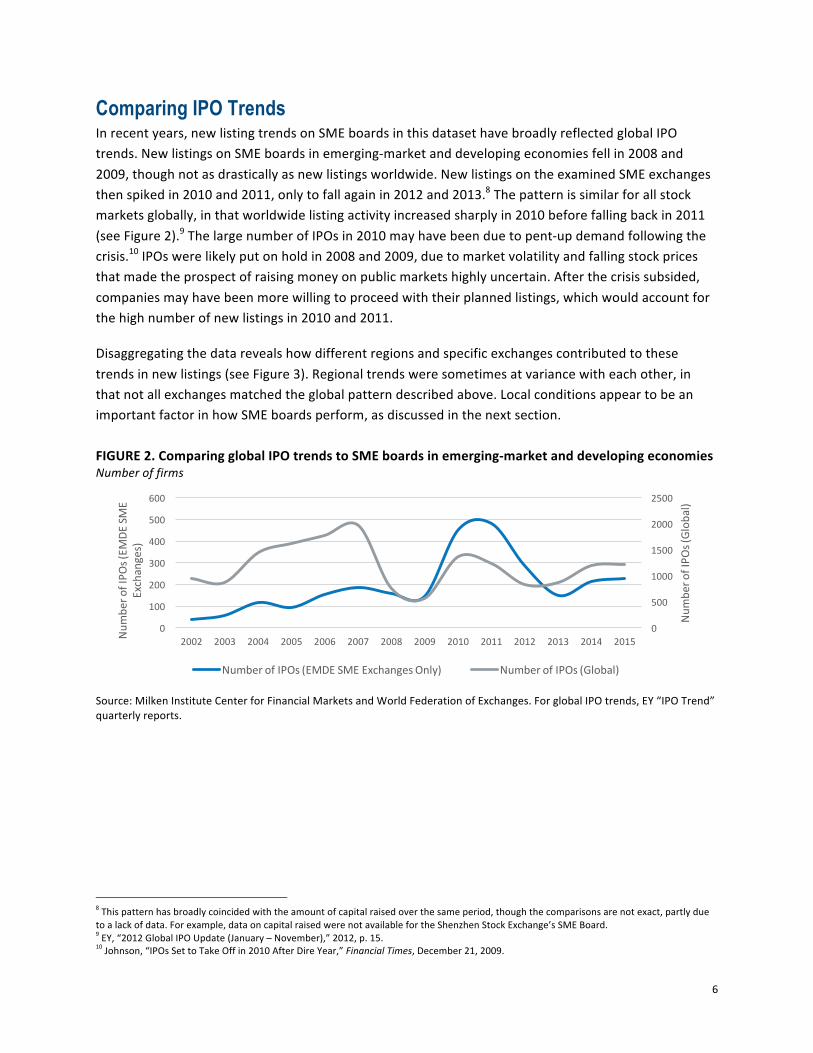

Comparing IPO TrendsInrecentyears,newlistingtrendsonSMEboardsinthisdatasethavebroadlyreflectedglobalIPO

trends.NewlistingsonSMEboardsinemerging-marketanddevelopingeconomiesfellin2008and

2009,thoughnotasdrasticallyasnewlistingsworldwide.NewlistingsontheexaminedSMEexchanges

thenspikedin2010and2011,onlytofallagainin2012and2013.8Thepatternissimilarforallstock

marketsglobally,inthatworldwidelistingactivityincreasedsharplyin2010beforefallingbackin2011

(seeFigure2).9ThelargenumberofIPOsin2010mayhavebeenduetopent-updemandfollowingthe

crisis.10IPOswerelikelyputonholdin2008and2009,duetomarketvolatilityandfallingstockprices

thatmadetheprospectofraisingmoneyonpublicmarketshighlyuncertain.Afterthecrisissubsided,

companiesmayhavebeenmorewillingtoproceedwiththeirplannedlistings,whichwouldaccountfor

thehighnumberofnewlistingsin2010and2011.

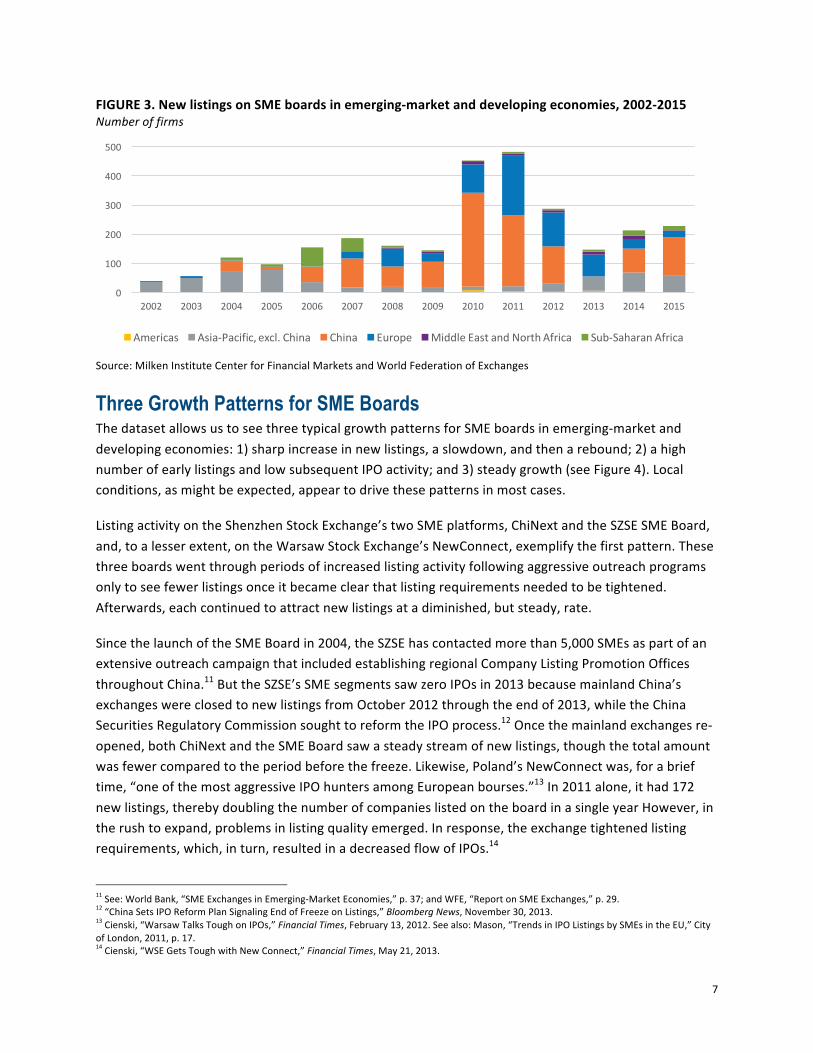

Disaggregatingthedatarevealshowdifferentregionsandspecificexchangescontributedtothese

trendsinnewlistings(seeFigure3).Regionaltrendsweresometimesatvariancewitheachother,in

thatnotallexchangesmatchedtheglobalpatterndescribedabove.Localconditionsappeartobean

importantfactorinhowSMEboardsperform,asdiscussedinthenextsection.

FIGURE2.ComparingglobalIPOtrendstoSMEboardsinemerging-marketanddevelopingeconomiesNumberoffirms

Source:MilkenInstituteCenterforFinancialMarketsandWorldFederationofExchanges.ForglobalIPOtrends,EY“IPOTrend”

quarterlyreports.

8Thispatternhasbroadlycoincidedwiththeamountofcapitalraisedoverthesameperiod,thoughthecomparisonsarenotexact,partlydue

toalackofdata.Forexample,dataoncapitalraisedwerenotavailablefortheShenzhenStockExchange’sSMEBoard.9EY,“2012GlobalIPOUpdate(January–November),”2012,p.15.10Johnson,“IPOsSettoTakeOffin2010AfterDireYear,”FinancialTimes,December21,2009.

0

500

1000

1500

2000

2500

0

100

200

300

400

500

600

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

NumberofIPOs(Global)

NumberofIPOs(EMDESME

Exchanges)

NumberofIPOs(EMDESMEExchangesOnly) NumberofIPOs(Global)

7

FIGURE3.NewlistingsonSMEboardsinemerging-marketanddevelopingeconomies,2002-2015Numberoffirms

Source:MilkenInstituteCenterforFinancialMarketsandWorldFederationofExchanges

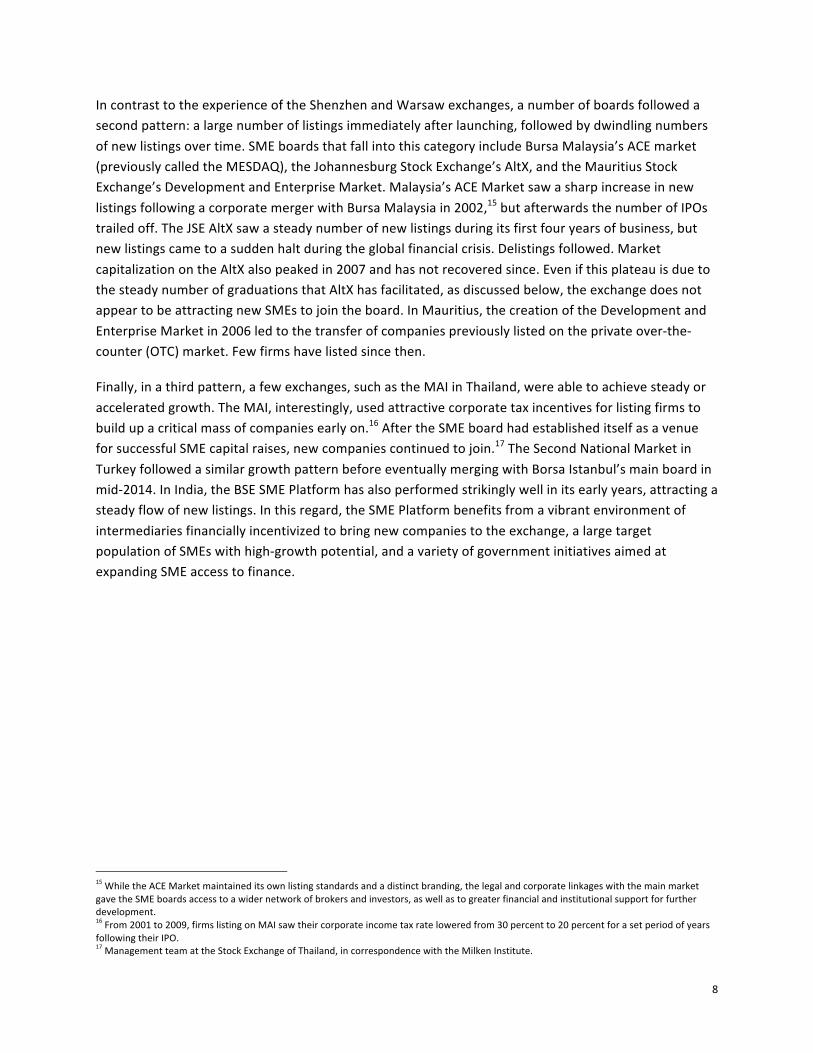

Three Growth Patterns for SME BoardsThedatasetallowsustoseethreetypicalgrowthpatternsforSMEboardsinemerging-marketand

developingeconomies:1)sharpincreaseinnewlistings,aslowdown,andthenarebound;2)ahigh

numberofearlylistingsandlowsubsequentIPOactivity;and3)steadygrowth(seeFigure4).Local

conditions,asmightbeexpected,appeartodrivethesepatternsinmostcases.

ListingactivityontheShenzhenStockExchange’stwoSMEplatforms,ChiNextandtheSZSESMEBoard,

and,toalesserextent,ontheWarsawStockExchange’sNewConnect,exemplifythefirstpattern.These

threeboardswentthroughperiodsofincreasedlistingactivityfollowingaggressiveoutreachprograms

onlytoseefewerlistingsonceitbecameclearthatlistingrequirementsneededtobetightened.

Afterwards,eachcontinuedtoattractnewlistingsatadiminished,butsteady,rate.

SincethelaunchoftheSMEBoardin2004,theSZSEhascontactedmorethan5,000SMEsaspartofan

extensiveoutreachcampaignthatincludedestablishingregionalCompanyListingPromotionOffices

throughoutChina.11ButtheSZSE’sSMEsegmentssawzeroIPOsin2013becausemainlandChina’s

exchangeswereclosedtonewlistingsfromOctober2012throughtheendof2013,whiletheChina

SecuritiesRegulatoryCommissionsoughttoreformtheIPOprocess.12Oncethemainlandexchangesre-

opened,bothChiNextandtheSMEBoardsawasteadystreamofnewlistings,thoughthetotalamount

wasfewercomparedtotheperiodbeforethefreeze.Likewise,Poland’sNewConnectwas,forabrief

time,“oneofthemostaggressiveIPOhuntersamongEuropeanbourses.”13In2011alone,ithad172

newlistings,therebydoublingthenumberofcompanieslistedontheboardinasingleyearHowever,in

therushtoexpand,problemsinlistingqualityemerged.Inresponse,theexchangetightenedlisting

requirements,which,inturn,resultedinadecreasedflowofIPOs.14

11See:WorldBank,“SMEExchangesinEmerging-MarketEconomies,”p.37;andWFE,“ReportonSMEExchanges,”p.29.

12“ChinaSetsIPOReformPlanSignalingEndofFreezeonListings,”BloombergNews,November30,2013.

13Cienski,“WarsawTalksToughonIPOs,”FinancialTimes,February13,2012.Seealso:Mason,“TrendsinIPOListingsbySMEsintheEU,”City

ofLondon,2011,p.17.14Cienski,“WSEGetsToughwithNewConnect,”FinancialTimes,May21,2013.

0

100

200

300

400

500

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Americas Asia-Pacific,excl.China China Europe MiddleEastandNorthAfrica Sub-SaharanAfrica

8

IncontrasttotheexperienceoftheShenzhenandWarsawexchanges,anumberofboardsfolloweda

secondpattern:alargenumberoflistingsimmediatelyafterlaunching,followedbydwindlingnumbers

ofnewlistingsovertime.SMEboardsthatfallintothiscategoryincludeBursaMalaysia’sACEmarket

(previouslycalledtheMESDAQ),theJohannesburgStockExchange’sAltX,andtheMauritiusStock

Exchange’sDevelopmentandEnterpriseMarket.Malaysia’sACEMarketsawasharpincreaseinnew

listingsfollowingacorporatemergerwithBursaMalaysiain2002,15butafterwardsthenumberofIPOs

trailedoff.TheJSEAltXsawasteadynumberofnewlistingsduringitsfirstfouryearsofbusiness,but

newlistingscametoasuddenhaltduringtheglobalfinancialcrisis.Delistingsfollowed.Market

capitalizationontheAltXalsopeakedin2007andhasnotrecoveredsince.Evenifthisplateauisdueto

thesteadynumberofgraduationsthatAltXhasfacilitated,asdiscussedbelow,theexchangedoesnot

appeartobeattractingnewSMEstojointheboard.InMauritius,thecreationoftheDevelopmentand

EnterpriseMarketin2006ledtothetransferofcompaniespreviouslylistedontheprivateover-the-

counter(OTC)market.Fewfirmshavelistedsincethen.

Finally,inathirdpattern,afewexchanges,suchastheMAIinThailand,wereabletoachievesteadyor

acceleratedgrowth.TheMAI,interestingly,usedattractivecorporatetaxincentivesforlistingfirmsto

buildupacriticalmassofcompaniesearlyon.16AftertheSMEboardhadestablisheditselfasavenue

forsuccessfulSMEcapitalraises,newcompaniescontinuedtojoin.17TheSecondNationalMarketin

TurkeyfollowedasimilargrowthpatternbeforeeventuallymergingwithBorsaIstanbul’smainboardin

mid-2014.InIndia,theBSESMEPlatformhasalsoperformedstrikinglywellinitsearlyyears,attractinga

steadyflowofnewlistings.Inthisregard,theSMEPlatformbenefitsfromavibrantenvironmentof

intermediariesfinanciallyincentivizedtobringnewcompaniestotheexchange,alargetarget

populationofSMEswithhigh-growthpotential,andavarietyofgovernmentinitiativesaimedat

expandingSMEaccesstofinance.

15WhiletheACEMarketmaintaineditsownlistingstandardsandadistinctbranding,thelegalandcorporatelinkageswiththemainmarket

gavetheSMEboardsaccesstoawidernetworkofbrokersandinvestors,aswellastogreaterfinancialandinstitutionalsupportforfurther

development.16From2001to2009,firmslistingonMAIsawtheircorporateincometaxrateloweredfrom30percentto20percentforasetperiodofyears

followingtheirIPO.17ManagementteamattheStockExchangeofThailand,incorrespondencewiththeMilkenInstitute.

9

FIGURE4.Newdomestic-companylistingsonselectedSMEboards,2002-2015

4a.Sharpincreaseinnewlistings,slowdown,andreboundNumberofnewdomesticlistingsperyear

Source:MilkenInstituteCenterforFinancialMarketsandWorldFederationofExchanges4b.AlargenumberofnewlistingsearlyonfollowedbyveryfewnewIPOsNumberofnewdomesticlistingsperyear

Source:MilkenInstituteCenterforFinancialMarketsandWorldFederationofExchanges4c.SteadygrowthNumberofnewdomesticlistingsperyear

Source:MilkenInstituteCenterforFinancialMarketsandWorldFederationofExchanges

0

50

100

150

200

250

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

ShenzhenSEChiNext ShenzhenSESMEBoard WarsawSENewConnect

0

10

20

30

40

50

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

BursaMalaysiaACE JohannesburgSEAltX MauritiusSE- Dev.&Ent.Market

-10

0

10

20

30

40

50

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

SETMAI Istanbul-SecondMarket BSESME

10

Liquidity Remains a ChallengeTheabilitytotransactshareseasilyandwithoutcausingpricestoshiftisanimportantfeatureofall

successfulstockexchanges.Mostfundamentally,stockmarketsprovidereal-timeinformationonthe

valueofafirm,andthisinformationvalueisunderminedifsharesdonottrade.Second,lackofliquidity

makesitmoredifficultforinvestorstoexittheirpositions,andtherefore,moreunlikelytoinvestinthe

firstplace.Unfortunately,manystockexchangesinemerging-marketanddevelopingeconomies

strugglewithlowlevelsofliquidity,particularlythoseservingsmalleconomieswithfewpublic

companies.ManySMEboardsfaceevengreaterdifficultiesinthisregard,owingtothelownumberof

listingsandthesmallfloatsize,meaningfewsharesareavailablefortrading.

AsthedatasetcompiledbytheMilkenInstituteandtheWFEshows,liquidityremainsachallengeto

marketdevelopmentformostSMEboards.TheNASDAQintheUnitedStatesseesmorevaluetradedon

adaily–andevenhourly–basisthanmanySMEboardsdoinayear.AhandfulofthelargerSME

exchanges,mostlyinAsia,havemanagedtoachieveannualturnoverratiosofgreaterthan100percent

ofmarketcapitalization(seeFigure5).Notably,alloftheexchangesthathaveachievedtheserelatively

highturnoverratioshavemorethan100listedcompanies.Incontrast,exchangeswithveryfewlisted

companieshaveexperiencedturnoverratesof50percentorlower.Thosewiththefewestcompanies,

suchasthePhilippineStockExchange’sSMEBoard,havebarelyanyliquidityatall,withturnoverratios

oflessthan10percent.

Figure5.LiquidityonSMEboardsinemerging-marketanddevelopingeconomiesTurnoverratiosversusnumberoflistedcompanies(latestyearavailable)

Source:MilkenInstituteCenterforFinancialMarketsandWorldFederationofExchanges

DelistingsTheoccasionaldepartureoflistedcompaniesisanormaloccurrenceinstockexchangesinadvancedand

developingmarkets,ascompaniesmaydelistforanumberofreasons.First,theymaybeforcibly

delistediftheygobankruptorfailtomeetthestockexchange’slistingrequirements.Theymayalso

delistasaresultofamergeroraleveragedbuyout.

ChiNext2013

ACEMarket2015ThaiMAI2015

SHZNSMEBoard2007

IstanbulEmerging2015

MalaysiaSecondBoard2008

NILEX2015

NewConnect2014

0

100

200

300

400

500

0% 50% 100% 150% 200% 250% 300% 350%

11

AccordingtoIOSCO(2015),withfewexceptions,involuntarydelistingsweretypicallyloweronSME

boardsthanonmainboardsworldwide.18Theprecisereasonforthisdifferenceisunclear,thoughitmay

resultfromlowerlistingrequirements,lackofenforcementofthoselistingrequirements,awillingness

ofexchangesand/orintermediariestoworkwithcompaniestoavoiddelisting,orsomecombinationof

thesefactors.Thereareexceptions,ofcourse.InMalaysia,anumberoffirmsontheSecondBoard

(whichlatermergedwiththemainboard)delistedduetobankruptcyintheearly2000s.Likewise,

bankruptcyandviolationsofcompliancestandardsaccountedforabout80percentofdelistingsfrom

thePolishNewConnectboardsince2008.19InSouthAfrica,ontheotherhand,themainfactorbehind

the27AltXdelistingsbetween2008and2015wasM&Aactivity.20

Surprisingly,giventhelargenumberoffirmslistedonthesemarketsegments,theShenzhenStock

Exchange’sChiNextandSMEBoarddidnotdelistasinglefirmthrough2015.Alackofenforcementis

perhapsthemostpersuasiveexplanation.Morerecently,though,theChinaSecuritiesRegulatory

Commissionhassignaleditsintenttomorestrictlyenforcesecuritiesregulationsbyforciblydelistinga

ChiNextcompanyinAugust2016forsecuritiesfraud.21Thedegreetowhichthisnewfoundconcern

aboutlistingqualitywillpersistremainstobeseen.

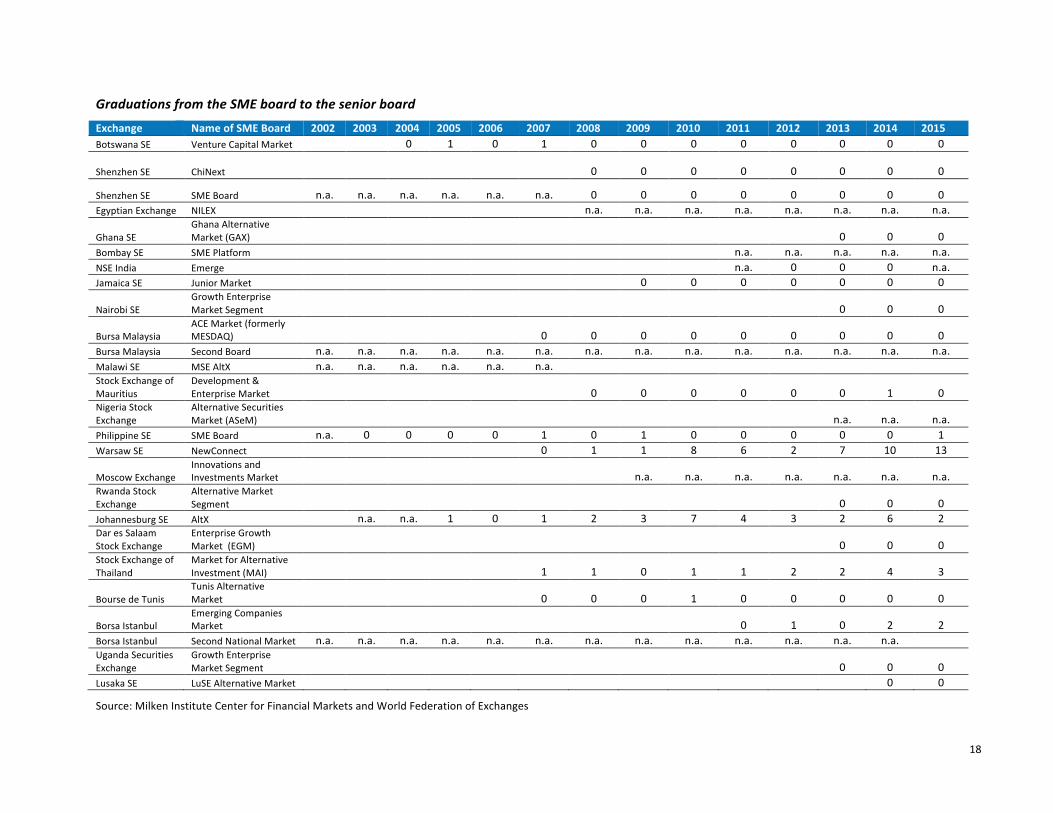

GraduationsFormanySMEboards,listedfirmsareallowed,andsometimesevenencouraged,tograduatetothe

stockexchange’smainboardoncetheyreachcertaincriteria.Graduationsareoftenconsidereda

markerofsuccessfortheseSMEboards.Thisistrueinanarrowsenseforboardsthatweredesignedto

feednewlistingstotheirseniorboardaspartofthestockexchange’sbusinessmodel.Itisalsotrueina

broadersense,asitvalidatestheroleofSMEboardsasincubatorsofcompaniesthatmightnothave

otherwisereceivedthefinancingneededtorealizetheirgrowthpotential.22

CriteriaforgraduationmayincludetimespentlistedontheSMEboard,aswellastheattainmentof

specifiedthresholdsforprofitability,size,ornumberofshareholders.23Beyondencouragementor

compulsionfromtheexchange,firmslistedonanSMEboardmaychoosetograduateforanumberof

reasons.Accordingtorecent,survey-basedworkfromtheMilkenInstitute,commonmotivationsto

graduateincludegreaterliquidity,accesstoabroaderandmorestableinvestorbase,andanenhanced

reputation,asfirmsoftenbelievealistingontheseniorboardwillleadtogreatervisibilityanda

strongerbrand.

Graduationdataarenotcollectedsystematicallyforallemerging-marketanddevelopingcountry

exchanges,soacomprehensiveviewofgraduationtrendsisnotyetavailable.Thatsaid,ahandfulof

18ISOCO,“SMEFinancingthroughCapitalMarkets,”2015,p.39.

19NewConnectReport2015,WarsawStockExchange;calculationsbyMilkenInstitutestaff.

20JSEstaff,incorrespondencewiththeMilkenInstitute.

21“China’sFirstSmall-CapStockDelistingSpursSpeculativeFrenzy,”BloombergNews,August4,2016.

22Mostboardsallowforgraduation,thoughnotall.Importantly,China’sShenzhenStockExchangedoesnothaveaprocessforcompaniesto

graduatefromChiNextortheSMEBoardtothemainboard.Thismaychange,though.23AfewverySMEboardsallowfirmstomigratedownfromthemainboardtotheSMEboard.Thepurposebehindsuchmigrationistoallow

thefirmtoremainlistedatalowercostand,perhaps,therebytoavoiddelistingorfirmclosure.Theonlydownwardmigrations(“demotions”?)

ofthissortintheWFE-MilkenInstitutedatasethaveoccurredontheStockExchangeofThailand,wheresixfirmshavemoveddownfromthe

seniorboardtotheMAI.

12

boardshaveseensignificantgraduationactivity.TheWarsawStockExchange’sNewConnect,for

example,reported38graduationsfrom2011to2015.AnotheristheJSEAltX,whichreported17

graduationsoverthesameperiod,and31sinceitsinception(seeFigure6).AltXgraduatesrepresent

about10percentofalllistingsontheJSE’smainboard,asignificantnumberandasignthatSME

segmentscanserveaseffectiveincubators.Likewise,theStockExchangeofThailand’sMAIhas

facilitated15graduationsfromitsinceptionin2007to2015,earningareputationas“apreparatory

venueforSMEstotaptheregularmarketofthestockexchange.”24

Manynewerexchangeshaveseenonlyahandful—ifany—graduations.Theformerincludesthe

MauritiusStockExchange’sDevelopmentandEnterpriseMarket(1graduationin2014)andthe

PhilippineStockExchange’sSMEBoard(3since2003).Meanwhile,severalnewboardsthatencourage

graduationbuthavenotfacilitatedanyto-datearelikelytodosointhefutureastheymature.Thisis

especiallytrueofJamaica’sJuniorMarket,aswellastheBSESMEplatformandtheNSEEmergein

India—allofwhichrequiregraduationoncecompaniesmeetcertaincriteria.TheJamaicaStock

Exchange’sJuniorMarket,forexample,requiresgraduationafterlistedSMEscompletetwotiers,each

ofwhichlastsfiveyears.TheNSEEmergesegmentrequiresgraduationtothemainboardoncea

company’sequitycapitalreaches$400million.25

FIGURE6.AnnualgraduationsfromSMEboardstoseniorboardsinPoland,SouthAfrica,andThailandNumberoffirms

Source:MilkenInstituteCenterforFinancialMarketsandWorldFederationofExchanges

ConclusionPublicequityfinancingisnotasolutionforall,orevenmost,SMEs,butitmaybeappropriatefora

certainsubsetofSMEswithspecificcharacteristics—namely,SMEsthatareyoung,havestronggrowth

prospects,andlimitedcollateral.26SuchSMEsaretheminority,buttheymakeadisproportionate

contributiontoemploymentandproductivitygrowth;indevelopingcountries,theyrepresentan

estimated16percentofSMEsbutaccountfor38percentofnetjobcreation.27Therefore,evenifpublic

24ADB,AsiaSMEFinanceMonitor2014,p.231

25WorldBank,“SMEExchangesinEmerging-MarketEconomies,”p.17.

26OECD,“OpportunitiesandConstraintsofMarket-BasedFinancingforSMEs,”2015,p.12.

27IFC,“SmallandMediumEnterpriseFinance:NewFindings,Trends,andG-20/GlobalPartnershipforFinancialInclusionProgress,”2013,p.7.

0

2

4

6

8

10

12

14

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

WarsawSENewConnect JSEAltX SETMAI

13

equityfinancingdoesnotrepresentabroadsolutiontotheSMEfinancinggap,SMEboardscan

potentiallymakeanoutsizedcontributiontoeconomicgrowthandemployment.

ToadvancethecurrentunderstandingofwhetherSMEboardscanexpandaccesstofinancein

emerging-marketanddevelopingcountries,theMilkenInstitute,inpartnershipwiththeWorld

FederationofExchanges,collectedandorganizeddataforavarietyofindicatorsfor26SMEboards

acrossanumberofcountries.Thisdatasethasallowedustoconductaninitialstocktakingofmarket

activityontheseboardsduringtheperiodof2002to2015,atimeperiodthatincludestheglobal

financialcrisisandtheestablishmentofanumberofnewSME-dedicatedmarketsegments.

Overall,thisinitialreviewofavailabledatashowsthatovertwo-thousandcompaniesinemerging-

marketanddevelopingeconomieshaveturnedtoSMEboardsforfinancingoverthepastdecade,witha

peakofactivityoccurringaround2010-2011,intheimmediateaftermathoftheglobalfinancialcrisis.

Totallistingsontheexaminedexchangeshaveincreasedsteadilysince2002,thoughthetrackrecordsof

individualexchangeshavevarieddramatically.Someexchangeshaveseenasteadyincreaseinnew

listings,whileothersexperiencedaninitialburstofactivityfollowedbyverylowsubsequentIPOactivity.

Delistingsdataaremorefragmentary,buttheavailabledatashowthatheightenedperiodsofdelistings

aremoreoftenassociatedwithatighteningoflisteningrequirementsbytheexchangesthemselves,as

wasthecase,forinstance,forPoland’sNewConnect.Finally,whilegraduationdataarealsoincomplete,

theavailabledatasuggestthatatleastforolder,moreestablishedSMEboardsinmiddle-income

countries—suchasPoland,SouthAfrica,andThailand—suchboardshaveindeedservedasincubators

forfirmstoeventuallylistonthemainboardsoftheirexchanges.

Earlyevidence,though,alsounderlinestherealitythatestablishinganSMEexchangedoesnot

guaranteenewmarketactivity.Thoughsomeexchangeshavedonewell,othershavefloundered.

Policymakersmustconsidertheopportunitycostsofthepoliticalandfinancialcapitalrequiredto

establishanSMEboardandthesubsequentworkrequiredtoattractlistingsandincubatecompaniesfor

graduation.ThequestionofwhetheritiseconomicallyrationaltoestablishandthensubsidizeSME-

dedicatedmarketsegmentsiftheyarenotabletobecomeself-sustainingisthereforeworthexamining

infurtherresearch.FutureresearchmayalsousefullyexplorehowtheperformanceofSMEboards

relatestolocalmacroeconomicconditions,financialsectordevelopment,industrycomposition,and

SMEs’accesstootherformsoffinance.

14

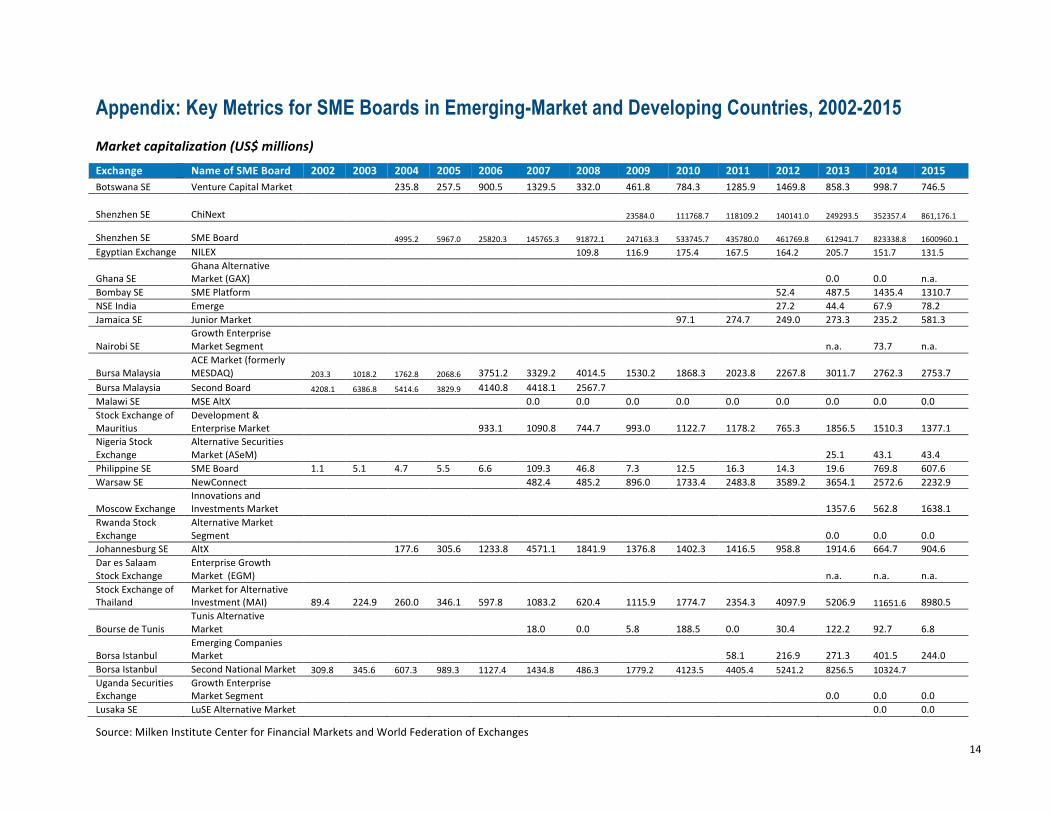

Appendix: Key Metrics for SME Boards in Emerging-Market and Developing Countries, 2002-2015 Marketcapitalization(US$millions)

Exchange NameofSMEBoard 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015BotswanaSE VentureCapitalMarket 235.8 257.5 900.5 1329.5 332.0 461.8 784.3 1285.9 1469.8 858.3 998.7 746.5

ShenzhenSE ChiNext 23584.0 111768.7 118109.2 140141.0 249293.5 352357.4 861,176.1

ShenzhenSE SMEBoard 4995.2 5967.0 25820.3 145765.3 91872.1 247163.3 533745.7 435780.0 461769.8 612941.7 823338.8 1600960.1EgyptianExchange NILEX 109.8 116.9 175.4 167.5 164.2 205.7 151.7 131.5

GhanaSEGhanaAlternativeMarket(GAX) 0.0 0.0 n.a.

BombaySE SMEPlatform 52.4 487.5 1435.4 1310.7NSEIndia Emerge 27.2 44.4 67.9 78.2JamaicaSE JuniorMarket 97.1 274.7 249.0 273.3 235.2 581.3

NairobiSEGrowthEnterpriseMarketSegment n.a. 73.7 n.a.

BursaMalaysiaACEMarket(formerlyMESDAQ) 203.3 1018.2 1762.8 2068.6 3751.2 3329.2 4014.5 1530.2 1868.3 2023.8 2267.8 3011.7 2762.3 2753.7

BursaMalaysia SecondBoard 4208.1 6386.8 5414.6 3829.9 4140.8 4418.1 2567.7 MalawiSE MSEAltX 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0StockExchangeofMauritius

Development&EnterpriseMarket 933.1 1090.8 744.7 993.0 1122.7 1178.2 765.3 1856.5 1510.3 1377.1

NigeriaStockExchange

AlternativeSecuritiesMarket(ASeM) 25.1 43.1 43.4

PhilippineSE SMEBoard 1.1 5.1 4.7 5.5 6.6 109.3 46.8 7.3 12.5 16.3 14.3 19.6 769.8 607.6WarsawSE NewConnect 482.4 485.2 896.0 1733.4 2483.8 3589.2 3654.1 2572.6 2232.9

MoscowExchangeInnovationsandInvestmentsMarket 1357.6 562.8 1638.1

RwandaStockExchange

AlternativeMarketSegment 0.0 0.0 0.0

JohannesburgSE AltX 177.6 305.6 1233.8 4571.1 1841.9 1376.8 1402.3 1416.5 958.8 1914.6 664.7 904.6DaresSalaamStockExchange

EnterpriseGrowthMarket(EGM) n.a. n.a. n.a.

StockExchangeofThailand

MarketforAlternativeInvestment(MAI) 89.4 224.9 260.0 346.1 597.8 1083.2 620.4 1115.9 1774.7 2354.3 4097.9 5206.9 11651.6 8980.5

BoursedeTunisTunisAlternativeMarket 18.0 0.0 5.8 188.5 0.0 30.4 122.2 92.7 6.8

BorsaIstanbulEmergingCompaniesMarket 58.1 216.9 271.3 401.5 244.0

BorsaIstanbul SecondNationalMarket 309.8 345.6 607.3 989.3 1127.4 1434.8 486.3 1779.2 4123.5 4405.4 5241.2 8256.5 10324.7 UgandaSecuritiesExchange

GrowthEnterpriseMarketSegment 0.0 0.0 0.0

LusakaSE LuSEAlternativeMarket 0.0 0.0

Source:MilkenInstituteCenterforFinancialMarketsandWorldFederationofExchanges

15

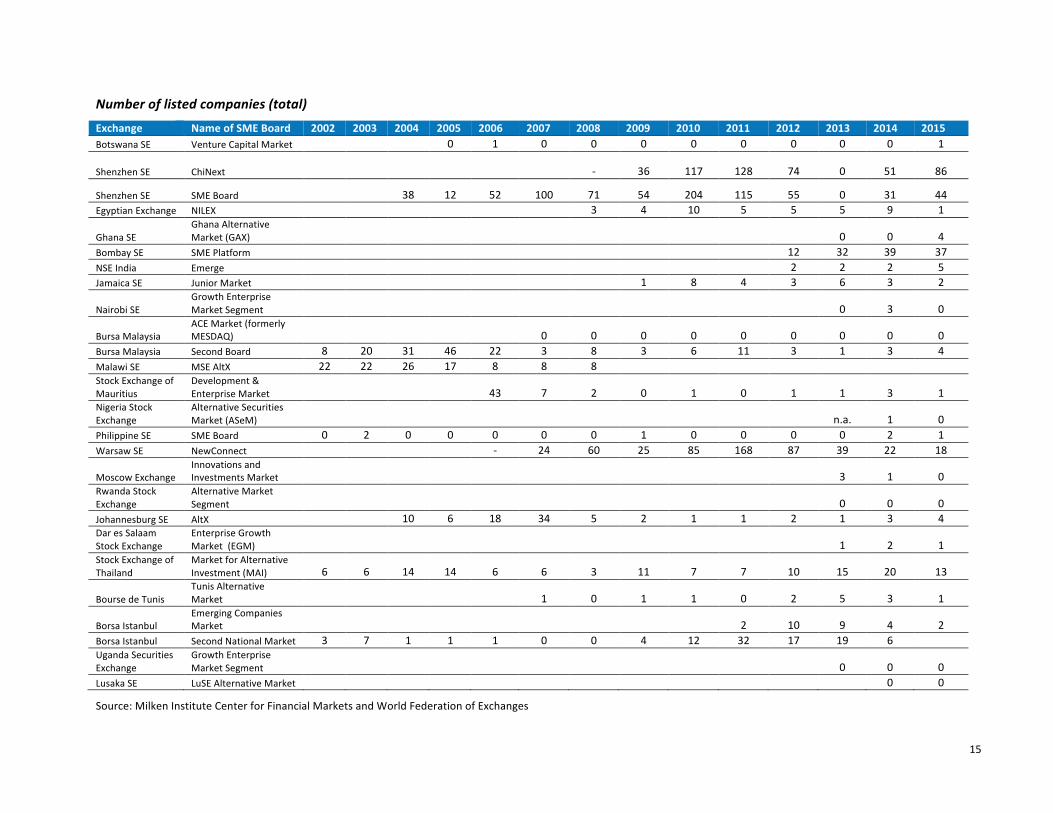

Numberoflistedcompanies(total)

Exchange NameofSMEBoard 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015BotswanaSE VentureCapitalMarket 0 1 0 0 0 0 0 0 0 0 1

ShenzhenSE ChiNext - 36 117 128 74 0 51 86

ShenzhenSE SMEBoard 38 12 52 100 71 54 204 115 55 0 31 44EgyptianExchange NILEX 3 4 10 5 5 5 9 1

GhanaSEGhanaAlternativeMarket(GAX) 0 0 4

BombaySE SMEPlatform 12 32 39 37NSEIndia Emerge 2 2 2 5JamaicaSE JuniorMarket 1 8 4 3 6 3 2

NairobiSEGrowthEnterpriseMarketSegment 0 3 0

BursaMalaysiaACEMarket(formerlyMESDAQ) 0 0 0 0 0 0 0 0 0

BursaMalaysia SecondBoard 8 20 31 46 22 3 8 3 6 11 3 1 3 4MalawiSE MSEAltX 22 22 26 17 8 8 8 StockExchangeofMauritius

Development&EnterpriseMarket 43 7 2 0 1 0 1 1 3 1

NigeriaStockExchange

AlternativeSecuritiesMarket(ASeM) n.a. 1 0

PhilippineSE SMEBoard 0 2 0 0 0 0 0 1 0 0 0 0 2 1WarsawSE NewConnect - 24 60 25 85 168 87 39 22 18

MoscowExchangeInnovationsandInvestmentsMarket 3 1 0

RwandaStockExchange

AlternativeMarketSegment 0 0 0

JohannesburgSE AltX 10 6 18 34 5 2 1 1 2 1 3 4DaresSalaamStockExchange

EnterpriseGrowthMarket(EGM) 1 2 1

StockExchangeofThailand

MarketforAlternativeInvestment(MAI) 6 6 14 14 6 6 3 11 7 7 10 15 20 13

BoursedeTunisTunisAlternativeMarket 1 0 1 1 0 2 5 3 1

BorsaIstanbulEmergingCompaniesMarket 2 10 9 4 2

BorsaIstanbul SecondNationalMarket 3 7 1 1 1 0 0 4 12 32 17 19 6 UgandaSecuritiesExchange

GrowthEnterpriseMarketSegment 0 0 0

LusakaSE LuSEAlternativeMarket 0 0

Source:MilkenInstituteCenterforFinancialMarketsandWorldFederationofExchanges

16

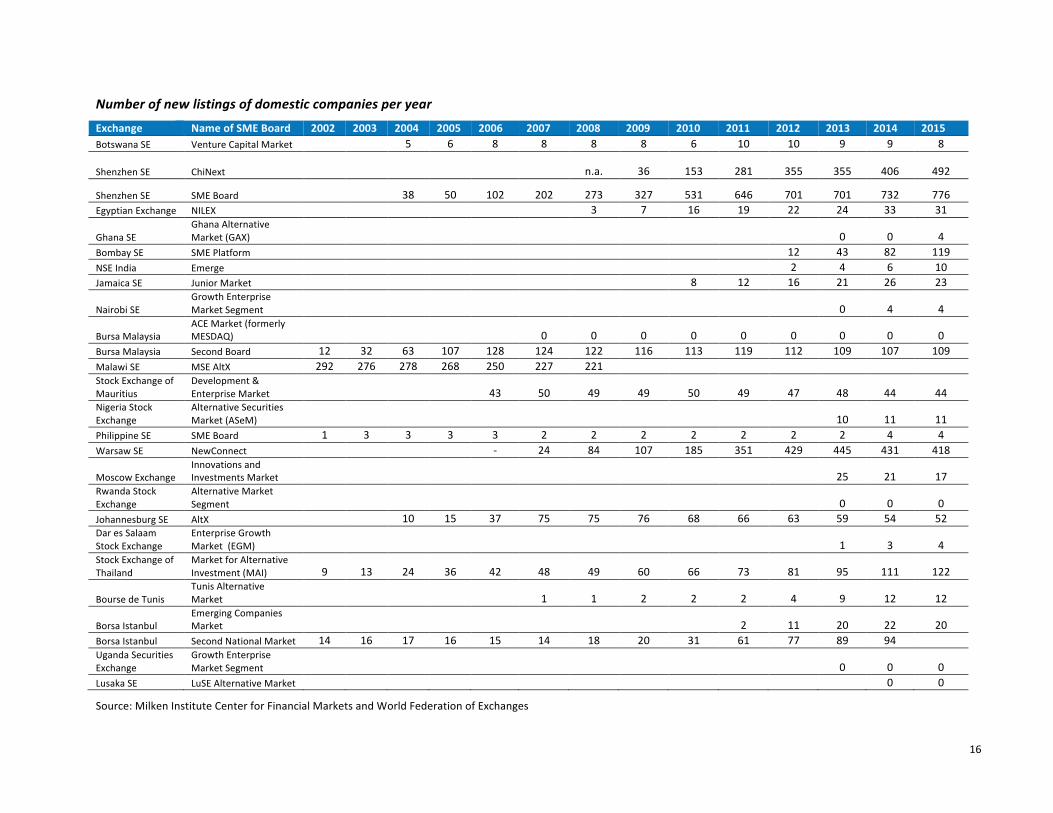

Numberofnewlistingsofdomesticcompaniesperyear

Exchange NameofSMEBoard 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015BotswanaSE VentureCapitalMarket 5 6 8 8 8 8 6 10 10 9 9 8

ShenzhenSE ChiNext n.a. 36 153 281 355 355 406 492

ShenzhenSE SMEBoard 38 50 102 202 273 327 531 646 701 701 732 776EgyptianExchange NILEX 3 7 16 19 22 24 33 31

GhanaSEGhanaAlternativeMarket(GAX) 0 0 4

BombaySE SMEPlatform 12 43 82 119NSEIndia Emerge 2 4 6 10JamaicaSE JuniorMarket 8 12 16 21 26 23

NairobiSEGrowthEnterpriseMarketSegment 0 4 4

BursaMalaysiaACEMarket(formerlyMESDAQ) 0 0 0 0 0 0 0 0 0

BursaMalaysia SecondBoard 12 32 63 107 128 124 122 116 113 119 112 109 107 109MalawiSE MSEAltX 292 276 278 268 250 227 221 StockExchangeofMauritius

Development&EnterpriseMarket 43 50 49 49 50 49 47 48 44 44

NigeriaStockExchange

AlternativeSecuritiesMarket(ASeM) 10 11 11

PhilippineSE SMEBoard 1 3 3 3 3 2 2 2 2 2 2 2 4 4WarsawSE NewConnect - 24 84 107 185 351 429 445 431 418

MoscowExchangeInnovationsandInvestmentsMarket 25 21 17

RwandaStockExchange

AlternativeMarketSegment 0 0 0

JohannesburgSE AltX 10 15 37 75 75 76 68 66 63 59 54 52DaresSalaamStockExchange

EnterpriseGrowthMarket(EGM) 1 3 4

StockExchangeofThailand

MarketforAlternativeInvestment(MAI) 9 13 24 36 42 48 49 60 66 73 81 95 111 122

BoursedeTunisTunisAlternativeMarket 1 1 2 2 2 4 9 12 12

BorsaIstanbulEmergingCompaniesMarket 2 11 20 22 20

BorsaIstanbul SecondNationalMarket 14 16 17 16 15 14 18 20 31 61 77 89 94 UgandaSecuritiesExchange

GrowthEnterpriseMarketSegment 0 0 0

LusakaSE LuSEAlternativeMarket 0 0

Source:MilkenInstituteCenterforFinancialMarketsandWorldFederationofExchanges

17

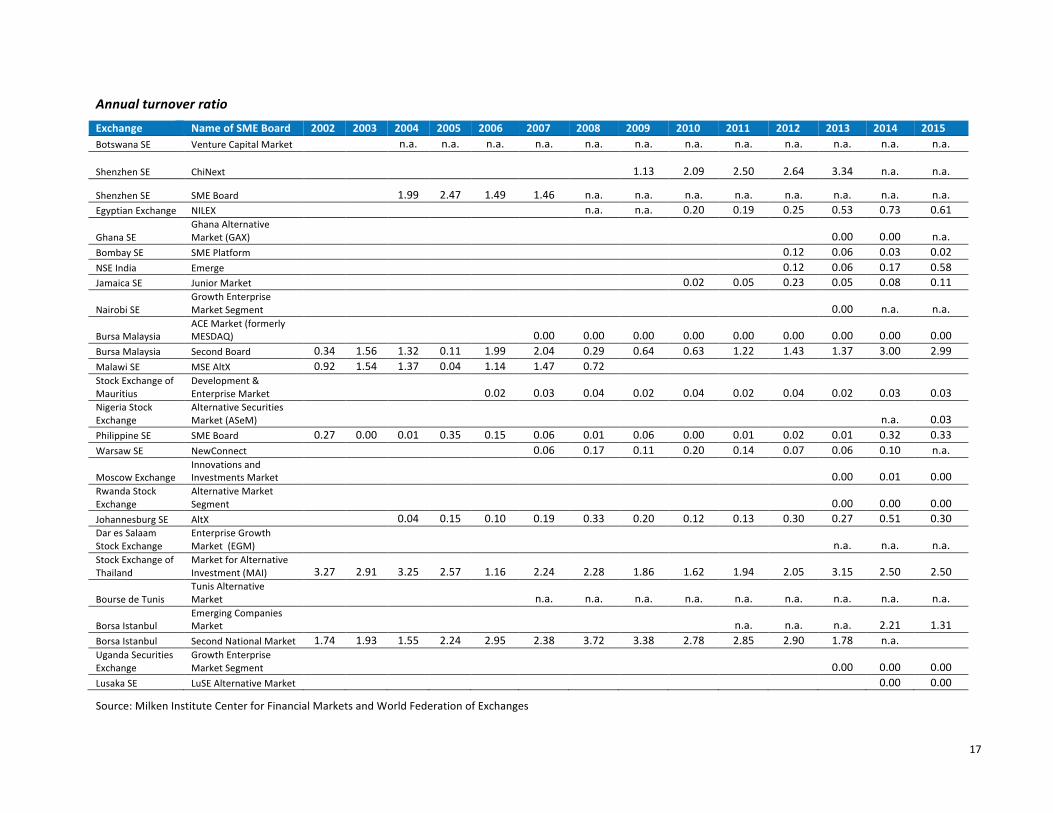

Annualturnoverratio

Exchange NameofSMEBoard 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015BotswanaSE VentureCapitalMarket n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a.

ShenzhenSE ChiNext 1.13 2.09 2.50 2.64 3.34 n.a. n.a.

ShenzhenSE SMEBoard 1.99 2.47 1.49 1.46 n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a.EgyptianExchange NILEX n.a. n.a. 0.20 0.19 0.25 0.53 0.73 0.61

GhanaSEGhanaAlternativeMarket(GAX) 0.00 0.00 n.a.

BombaySE SMEPlatform 0.12 0.06 0.03 0.02NSEIndia Emerge 0.12 0.06 0.17 0.58JamaicaSE JuniorMarket 0.02 0.05 0.23 0.05 0.08 0.11

NairobiSEGrowthEnterpriseMarketSegment 0.00 n.a. n.a.

BursaMalaysiaACEMarket(formerlyMESDAQ) 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

BursaMalaysia SecondBoard 0.34 1.56 1.32 0.11 1.99 2.04 0.29 0.64 0.63 1.22 1.43 1.37 3.00 2.99MalawiSE MSEAltX 0.92 1.54 1.37 0.04 1.14 1.47 0.72 StockExchangeofMauritius

Development&EnterpriseMarket 0.02 0.03 0.04 0.02 0.04 0.02 0.04 0.02 0.03 0.03

NigeriaStockExchange

AlternativeSecuritiesMarket(ASeM) n.a. 0.03

PhilippineSE SMEBoard 0.27 0.00 0.01 0.35 0.15 0.06 0.01 0.06 0.00 0.01 0.02 0.01 0.32 0.33WarsawSE NewConnect 0.06 0.17 0.11 0.20 0.14 0.07 0.06 0.10 n.a.

MoscowExchangeInnovationsandInvestmentsMarket 0.00 0.01 0.00

RwandaStockExchange

AlternativeMarketSegment 0.00 0.00 0.00

JohannesburgSE AltX 0.04 0.15 0.10 0.19 0.33 0.20 0.12 0.13 0.30 0.27 0.51 0.30DaresSalaamStockExchange

EnterpriseGrowthMarket(EGM) n.a. n.a. n.a.

StockExchangeofThailand

MarketforAlternativeInvestment(MAI) 3.27 2.91 3.25 2.57 1.16 2.24 2.28 1.86 1.62 1.94 2.05 3.15 2.50 2.50

BoursedeTunisTunisAlternativeMarket n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a.

BorsaIstanbulEmergingCompaniesMarket n.a. n.a. n.a. 2.21 1.31

BorsaIstanbul SecondNationalMarket 1.74 1.93 1.55 2.24 2.95 2.38 3.72 3.38 2.78 2.85 2.90 1.78 n.a. UgandaSecuritiesExchange

GrowthEnterpriseMarketSegment 0.00 0.00 0.00

LusakaSE LuSEAlternativeMarket 0.00 0.00

Source:MilkenInstituteCenterforFinancialMarketsandWorldFederationofExchanges

18

GraduationsfromtheSMEboardtotheseniorboard

Exchange NameofSMEBoard 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015BotswanaSE VentureCapitalMarket 0 1 0 1 0 0 0 0 0 0 0 0

ShenzhenSE ChiNext 0 0 0 0 0 0 0 0

ShenzhenSE SMEBoard n.a. n.a. n.a. n.a. n.a. n.a. 0 0 0 0 0 0 0 0EgyptianExchange NILEX n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a.

GhanaSEGhanaAlternativeMarket(GAX) 0 0 0

BombaySE SMEPlatform n.a. n.a. n.a. n.a. n.a.NSEIndia Emerge n.a. 0 0 0 n.a.JamaicaSE JuniorMarket 0 0 0 0 0 0 0

NairobiSEGrowthEnterpriseMarketSegment 0 0 0

BursaMalaysiaACEMarket(formerlyMESDAQ) 0 0 0 0 0 0 0 0 0

BursaMalaysia SecondBoard n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a.MalawiSE MSEAltX n.a. n.a. n.a. n.a. n.a. n.a. StockExchangeofMauritius

Development&EnterpriseMarket 0 0 0 0 0 0 1 0

NigeriaStockExchange

AlternativeSecuritiesMarket(ASeM) n.a. n.a. n.a.

PhilippineSE SMEBoard n.a. 0 0 0 0 1 0 1 0 0 0 0 0 1WarsawSE NewConnect 0 1 1 8 6 2 7 10 13

MoscowExchangeInnovationsandInvestmentsMarket n.a. n.a. n.a. n.a. n.a. n.a. n.a.

RwandaStockExchange

AlternativeMarketSegment 0 0 0

JohannesburgSE AltX n.a. n.a. 1 0 1 2 3 7 4 3 2 6 2DaresSalaamStockExchange

EnterpriseGrowthMarket(EGM) 0 0 0

StockExchangeofThailand

MarketforAlternativeInvestment(MAI) 1 1 0 1 1 2 2 4 3

BoursedeTunisTunisAlternativeMarket 0 0 0 1 0 0 0 0 0

BorsaIstanbulEmergingCompaniesMarket 0 1 0 2 2

BorsaIstanbul SecondNationalMarket n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. UgandaSecuritiesExchange

GrowthEnterpriseMarketSegment 0 0 0

LusakaSE LuSEAlternativeMarket 0 0

Source:MilkenInstituteCenterforFinancialMarketsandWorldFederationofExchanges

19

AcknowledgmentsThispaperwaspreparedfortheMilkenInstituteCenterforFinancialMarketsbyJohnSchellhase,associate

director,andJimWoodsome,seniorassociate.DuringinternshipsattheMilkenInstitute,Christopher

BensonandAtulMenonassistedincollectingandorganizingsomedatapresentedhere.Theauthorswishto

thankJacquelineIrving,director,andStaciWarden,executivedirectorattheMilkenInstituteCenterfor

FinancialMarkets,fortheirsupportofthisprojectandtheircommentsondraftsofthispaper.

TheauthorsalsowishtothankSiobhanCleary,headofresearchandpublicpolicy,andStefanoAlderighi,

senioreconomist,attheWorldFederationofExchangesfortheirpartnershipincreatingthedataset

describedinthispaperandfortheirfurthercollaborationonresearchinitiativestoexploretheroleofSME

boardsinemerging-marketanddevelopingcountries.TatianaChekanova,previouslyaneconomistatthe

WFE,alsocontributedtothecreationofthisnewdataset.

About the Authors JohnSchellhaseisanassociatedirectorattheCenterforFinancialMarketsattheMilkenInstitute.His

workprimarilyfocusesonfinancial-marketdevelopmentindevelopingcountries.

JimWoodsomewasaseniorprogramresearchanalystwiththeMilkenInstituteCenterforFinancial

Markets,wherehesupportedtheresearcheffortsandinitiativesrelatedtothecenter’sCapitalMarketsfor

Developmentprogram.Hecurrentlyworksasanindependentconsultantonfinancial-sectorissuesaffecting

developingcountries.

About the Center for Financial Markets BasedinWashington,D.C.,theMilkenInstituteCenterforFinancialMarketspromotesfinancialmarket

understandingandworkstoexpandaccesstocapital,strengthen—anddeepen—financialmarkets,and

developinnovativefinancialsolutionstothemostpressingglobalchallenges.

About the Milken Institute TheMilkenInstituteisanonprofit,nonpartisanthinktankdeterminedtoincreaseglobalprosperityby

advancingcollaborativesolutionsthatwidenaccesstocapital,createjobsandimprovehealth.Wedothis

throughindependent,data-drivenresearch,action-orientedmeetingsandmeaningfulpolicyinitiatives.

©2017MilkenInstitute

ThisworkismadeavailableunderthetermsoftheCreativeCommonsAttribution-NonCommercial-

NoDerivs3.0UnportedLicense,availableatcreativecommons.org/licenses/by-nc-nd/3.0/